Executive Board 204 EX/22 - unesdoc.unesco.orgunesdoc.unesco.org/images/0026/002615/261574e.pdf ·...

24

204 EX/22 Executive Board Job: 201800195 Two hundred and fourth session PARIS, 6 March 2018 Original: English Item 22 of the provisional agenda INTERNAL OVERSIGHT SERVICE (IOS): ANNUAL REPORT 2017 SUMMARY The annual report of the Internal Oversight Service (IOS) is submitted pursuant to a standing request by the Executive Board (160 EX/Decision 6.5 and 164 EX/Decision 6.10). The report presents the key achievements of IOS for the concerned year. The following items are attached as annexes to this report: internal audits completed in 2017 (Annex I), the Internal Audit and Evaluation workplans for 2018/2019 (Annex II) and the List of Acronyms (Annex III). The annual report of the Oversight Advisory Committee (OAC) to the Director-General is presented in 204 EX/22.INF. All financial and administrative implications of the reported activities fall within the parameters of the current C/5 document. Action expected of the Executive Board: Proposed decision in paragraph 63.

-

Upload

duongkhanh -

Category

Documents

-

view

214 -

download

0

Transcript of Executive Board 204 EX/22 - unesdoc.unesco.orgunesdoc.unesco.org/images/0026/002615/261574e.pdf ·...

204 EX/22

Executive Board

Job: 201800195

Two hundred and fourth session

PARIS, 6 March 2018 Original: English

Item 22 of the provisional agenda

INTERNAL OVERSIGHT SERVICE (IOS): ANNUAL REPORT 2017

SUMMARY

The annual report of the Internal Oversight Service (IOS) is submitted pursuant to a standing request by the Executive Board (160 EX/Decision 6.5 and 164 EX/Decision 6.10). The report presents the key achievements of IOS for the concerned year.

The following items are attached as annexes to this report: internal audits completed in 2017 (Annex I), the Internal Audit and Evaluation workplans for 2018/2019 (Annex II) and the List of Acronyms (Annex III). The annual report of the Oversight Advisory Committee (OAC) to the Director-General is presented in 204 EX/22.INF.

All financial and administrative implications of the reported activities fall within the parameters of the current C/5 document.

Action expected of the Executive Board: Proposed decision in paragraph 63.

204 EX/22

INTRODUCTION

1. The annual report presents the key activities of the Internal Oversight Service (IOS) for 2017 and its provisional work programme for 2018/19. The report of the Oversight Advisory Committee (OAC) to the Director-General, whose terms of reference call for it to be shared with the Executive Board, is presented in document 204 EX/22.INF.

OVERVIEW

2. IOS provides a consolidated oversight mechanism covering the functions described below:

Table 1: Main functions of IOS

Internal Audit Audits assess selected operations of Headquarters, field offices and information technology systems and make recommendations to improve the Organization’s administration, management control and programme delivery.

Evaluation Evaluations assess the relevance, efficiency, effectiveness, impact and sustainability of programmes, projects and operations as well as their coherence, connectedness and coverage.

Investigation Investigations assess allegations of misconduct and irregularities (e.g. fraud, abuse of assets, or harassment). It is the sole entity responsible for investigating misconduct.

Advisory role Advisory services are provided to senior management upon request, ranging from organizational advice to operational guidance.

3. IOS adheres to international professional standards1 for the conduct of its audits, evaluations and investigations. This includes continued reinforcement of its quality assurance processes through the advice of the OAC, external quality assurance reviews of the Internal Audit and Evaluation functions, and the requirement for all staff to be professionally certified and/or trained in their field, in addition to their academic credentials.

4. IOS staff are actively engaged in a number of United Nations system-wide professional networks, including the Representatives of Internal Audit Services of the United Nations Organizations and Multilateral Financial Institutions (RIAS); the United Nations Evaluation Group (UNEG); and the United Nations Representatives of Investigations Services (UNRIS). This allows for informal benchmarking and joint standard setting within the context of the United Nations system.

5. IOS is part of a broader oversight mechanism for UNESCO that includes the External Auditor, whose reports are presented directly to the Executive Board, the OAC, and the Joint Inspection Unit (JIU), whose reports are available at www.unjiu.org.

6. In addition to its main functions, IOS provides the secretariat function for the OAC as well as the focal point function for the JIU.

1 Audit follows the International Standards for the Professional Practice of Internal Auditing; Investigation: the Uniform

Guidelines for Investigations; and Evaluation: the Norms and Standards for Evaluation in the United Nations System.

204 EX/22 – page 2

7. The International Standards for the Professional Practice of Internal Auditing require that UNESCO’s chief audit executive report to a level in the Organization that allows the Internal Audit activity to fulfil its responsibilities, and must confirm to the Executive Board, at least annually, the organizational independence of the Internal Audit function. The Director of IOS hereby confirms to the Executive Board that IOS enjoyed full organizational independence in 2017 for its three core functions and was free to fully determine the scope of its work, to undertake assignments and to communicate on its results.

BUDGET AND STAFFING

8. The activity budget for IOS remains lower than it was before the budget reductions in 2011. While a range of cost-savings measures have been introduced, this has still led to gaps in Internal Audit coverage, particularly regarding field offices. Cost recovery received from sectors enabled IOS to undertake a number of strategically significant evaluation assignments that would not have been completed otherwise. IOS operates with 18 staff (16 Professional and two support staff) in comparison of 23 staff (20 Professional and three support staff) prior to the financial crisis. An additional P-4 position in internal audit to address field coverage was approved under document 39 C/5.

Table 2: IOS Budget Evolution

Source: (*) FABS – Regular Programme Budget and (**) C/5 Expenditure Plans

INTERNAL AUDIT

9. IOS conducts independent and objective internal audits designed to improve the effectiveness and efficiency of UNESCO operations, all while helping the Organization attain its objectives and results. An Internal Audit Charter and Policy defines the Internal Audit function’s purpose, authority and responsibility.

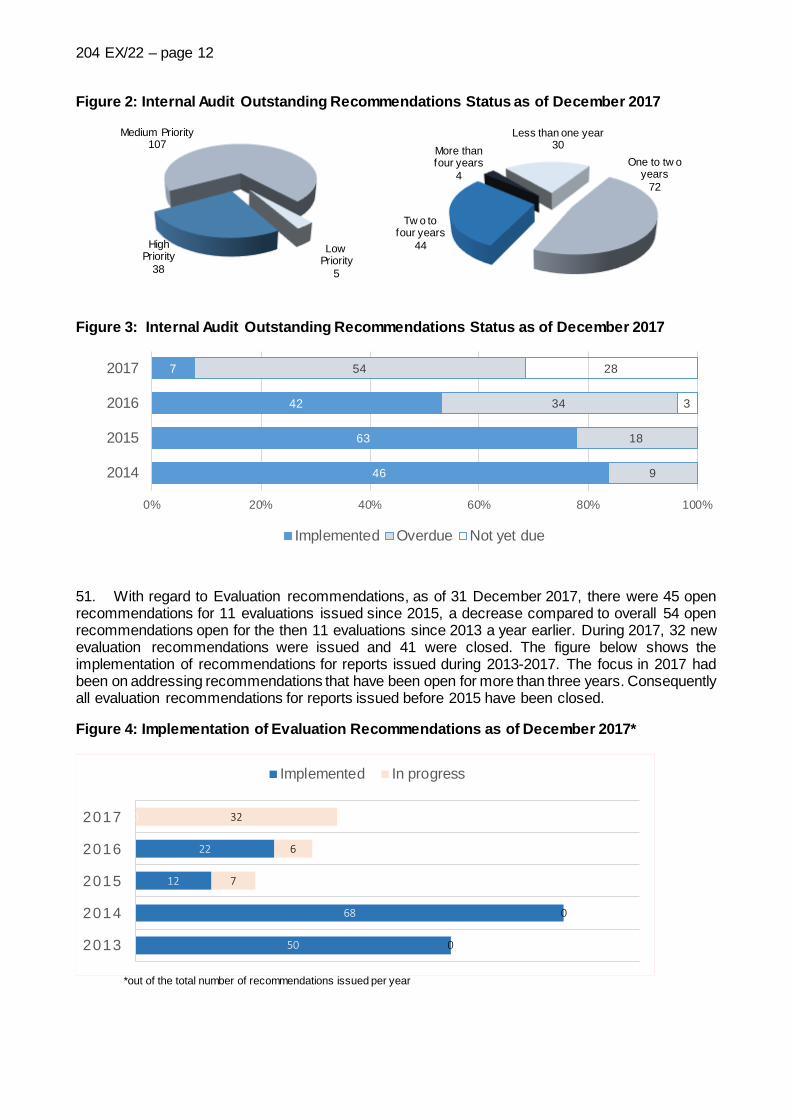

10. During 2017, internal and external processes were in place to ensure that internal audits benefit from an effective Quality Assurance and Improvement Programme. The internal assessment of audits entails the set-up of checklists to ensure compliance with the Standards, peer review as a

2010 / 2011(35C)

2012 / 2013(36C)

2014 / 2015(37C)

2016 / 2017(38C)

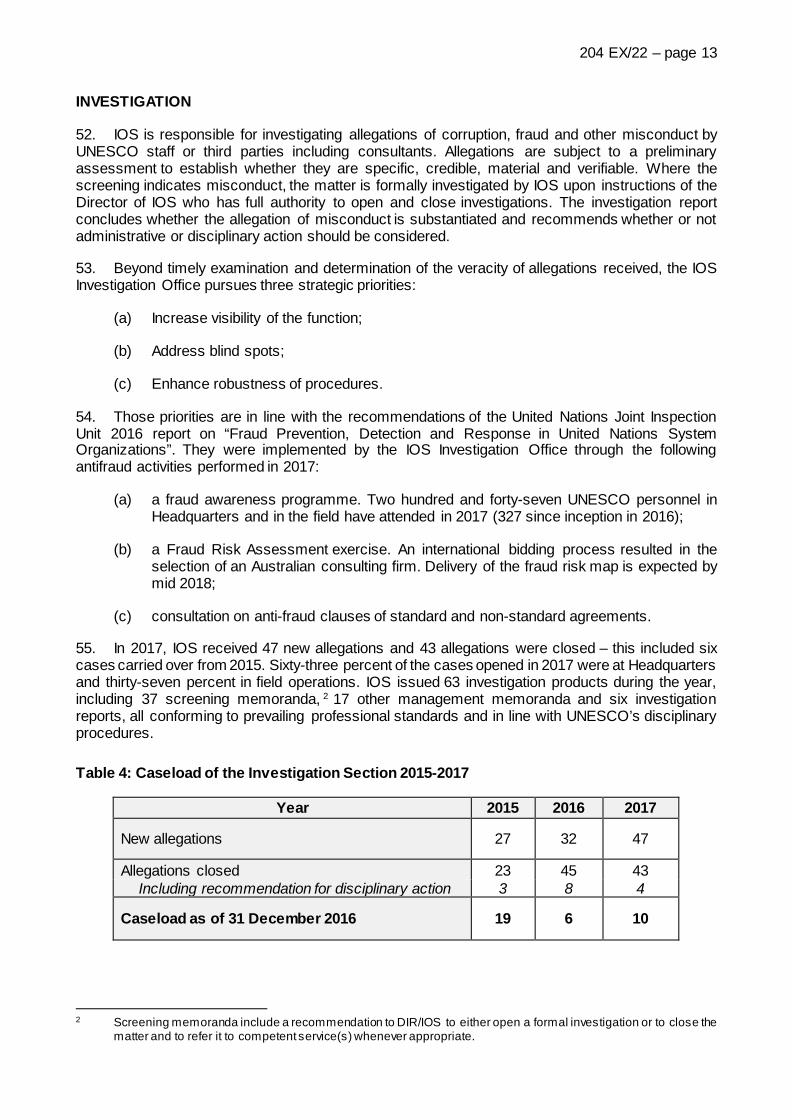

2018 / 2019(39C)

Additional Appropriations (*) - 25,000 574,000 -Cost Recovery (*) - 57,000 23,000 205,000ExB (*) 645,000 221,000 53,000 200,000 168,800FITOCA (**) 726,000 736,000 814,000 899,000 952,200RP Activity Budget (**) 1,034,000 413,000 479,000 514,000 459,400RP Staff Budget (**) 5,039,000 5,185,000 5,243,000 5,163,000 5,602,600

3

4

5

6

7

8

USD

Mill

ions

204 EX/22 – page 3

part of performance objectives, and feedback from the auditees with post-audit client surveys, which shows positive client satisfaction.

11. IOS established its provisional Internal Audit Plan 2018/19 (see Annex II) following a risk assessment of the Organization’s processes and information systems at Headquarters and in field offices. The process included consultations with Senior Management on all auditable areas as well as information sharing and joint planning with the External Auditor in order to avoid potential duplication. The entities or processes assessed at “high risk” were then included in the Internal Audit Year Plan. Decentralized entities, including field offices, are ranked by risk level. IOS believes it is critical to cover these entities in their entirety at least once within a five-year period; however, the limited resources are a constraint to achieve this minimum coverage.

12. Types of internal audits planned by IOS included:

• Governance audits assessing the internal governance processes to ascertain that these promote ethical rules and values of the Organization and properly monitor its performance achievements. These audits verify the adequate communication of risk appetite and accountability as well as the provision of reliable information to Governing Bodies.

• Risk management audits and assessments assessing the implementation and results of the risk management process at various organizational levels (overall and of individual entities).

• Performance audits that take stock and provide analysis of processes or projects and identify process improvements towards better effectiveness and efficiency.

• Management audits assessing all of the above dimensions for a specific internal entity with emphasis on strategic planning, internal control, performance of implementation and results. They cover also the relationship between the entity and central services.

13. During the year, IOS conducted nine audits at Headquarters, four audits of field offices and category 1 institutes. In addition, two audits were close to completion at year-end. Management accepted all recommendations issued and action plans have been developed for all of them. The IOS audits identified cost-savings for approximately US $4.5 million and these need to be pursued as a matter of priority. The principal audits completed in 2017 are summarized in Annex I and more information on the results of these audits is available on the IOS website at www.unesco.org/ios.

14. The audits performed in 2017 provide only limited assurance on UNESCO’s overall governance, risk management and internal control, due to limited resources. These limitations are affecting mostly the coverage of field offices.

15. Audits completed during 2017, as well as an analysis of the follow-up on recommendations from prior assignments, show that there have been a number of improvements in internal controls while at the same time some new risks have emerged or remain to be addressed. None of these, in our opinion, constitutes a material weakness in the overall system of controls. Key results from recent IOS audits are summarized below.

General management

16. Although important progress has been made towards establishing a Risk Management Framework with the approval of the risk management policy and training of staff on risk management, the finalization of the corporate risk register and the business continuity policy and plan remain pending at the end of the year. Also, while the risk management policy includes a definition and guidance on the risk appetite statement, it does not include a formal UNESCO risk appetite statement. Finally, to effectively implement risk management throughout the Organization it is necessary to establish operational risk registers across sectors/services/field units, develop a risk

204 EX/22 – page 4

management procedures manual, and rollout training across the Organization to ensure risk management is fully embedded in the organizational culture.

17. IOS audit on fixed assets concluded that controls need to be significantly improved to ensure correct recording of inventory, its proper management including periodical physical verification, and effective disposal. IOS noted discrepancies between barcode number and the asset number as recorded in the asset register, which makes the asset identification difficult. Further, the custodian system as required under the policy is not functional and needs to be established for ensuring accountability and safe custody of assets. In addition, weak inventory recording practices coupled with dysfunctional physical inventory verification process leads to inaccurate asset register and poses risk of inventory loss. In a sample testing, IOS found a number of new asset acquisitions that were either not recorded or incorrectly recorded. To strengthen the physical verification process at Headquarters, clear roles and accountabilities need to be defined.

Programme Management

18. IOS audited the management framework for category 2 institutes and centres. While recognizing the value of these partnerships the strategic policy and management of these relationships lacks direction. The growing list of category 2 institutes and centres, totalling 115 at the time of the audit, has put a strain on UNESCO’s resources without commensurate benefits. Two thirds of the institutes and centres are not operational and half of them not yet established. There is scope to improve the strategic alignment of category 2 institutes with UNESCO programmatic priorities as well as to enhance management of the reputational risk that flows from the uncertain status of many institutes. Streamlining and clarifying the number and purpose of these institutes brings an opportunity to gain better value for money from UNESCO’s budget.

19. Services from Advisory Bodies (International Union for Conservation of Nature (IUCN), International Council on Monuments and Sites (ICCOMOS) and International Centre for the Study of the Preservation and Restoration of Cultural Property (ICCROM)) constitute 75% of the total budget from the World Heritage Fund, leaving very little for other key tasks such as providing international assistance to the State Parties. The current practices for assessing nominations to the World Heritage List by the Advisory Bodies are heavy and costly when compared with those of similar international instruments and programmes. There is an opportunity to revisit the working methods and adopt practices from other international instruments and programmes. Further, some advisory services such as assessing requests for international assistance and reactive monitoring missions can be sourced differently, e.g. from a panel of experts established by the World Heritage Committee.

20. Finally, the World Academy of Sciences (TWAS) audit recommended rationalization and consolidation of the governing structure and streamlining of the administrative capacity to improve efficiency. TWAS has prepared a detailed action plan including clarity on the role of governing bodies and presented them to their Council and the Steering Committee.

Human Resources

21. Following recommendations from the 2015 audit on recruitment, IOS notes good progress on their implementation in 2017: HRM updated the recruitment policy in order to improve planning, objectivity and consistency, and have a greater involvement and accountability of HRM staff in the process. The main changes include: advance advertisement of posts due to become vacant; shifting of the preselection responsibility to HRM, together with the hiring manager; streamlining of Panels; replacement of the Personnel Advisory Boards (PABs) meetings by the Advisory Review Boards (ARB) online reviews; enhanced presence of Programme sectors in the interview panels; and the provision of feedback by hiring managers to unsuccessful candidates. Robust reference checks, clear educational requirements, harmonized language requirements and due consideration of field assignments and mobility for promotions is restated. Finally, guidance is provided on key aspects of the recruitment process such as the use of Tests and Conflicts of Interest. These changes aim at a

204 EX/22 – page 5

faster and more efficient process, which will allow the Organization to address talent organizational needs in support of the 2030 agenda.

22. In response to IOS recommendations from the 2016 audit of Doha Office, HRM and BFM established a backstopping protocol for providing increased support to field offices undertaking recruitments during periods when the Administrative Officer post is vacant and clarified the HR Manual on competent authority, required qualifications and remuneration to advertise for a post.

23. As recommended by IOS, job descriptions of category 1 institutes HR Officers have been updated to introduce a functional reporting line to DIR/HRM on matters of decentralized or delegated HR functions and accountabilities. In addition, all International Centre for Theoretical Physics (ICTP) staff have been integrated into Integrated and Results-Oriented Information System (IRIS), UNESCO’s Enterprise resource planning (ERP), allowing for a better supervision at headquarters by the Programme Sector and central services.

Financial Controls

24. The audit of the Statement on Internal Controls (SIC) process recommended greater linkages between the SIC process and the risk identification and management process emphasizing the need for better monitoring of issues as reported in the control self-assessments. UNESCO’s Administrative Manual is being revised to update the internal control framework with a view to improve its linkages with the risk identification and management process.

25. The performance audit of official travel identified some good practices due to efficiency measures introduced following the financial crisis. These had resulted in a 37% reduction of travel expenses from $16.7 million in 2011 to $10.5 million in 2016. Bearing in mind that the current volume of travel exceeds 2011 levels, the audit concluded that further biennial savings of up to USD 4 Million (18.5%) could be achieved through timely purchase of tickets, alignment of the basis of lump sum payments for statutory travel with the United Nations secretariat, implementation of a self-booking tool, and optimization of administrative processes. In addition, clear ownership under a single authority of the travel process is required to reinstate a strong second line of defense to better monitor and report on adherence with the travel rules and policy. This includes employing a travel manager to ensure cost effective procurement of travel and increase value-for-money on travel arrangements. Finally, temporary cost reduction measures in effect since 2012 need to be revisited in light of their intended impact. BFM should address current gaps in travel related administrative guidance before handover of the travel policy to MSS. Following the audit, a review of the Administrative Manual item 15 is under way to address the gaps in travel related administrative guidance.

Resource Mobilization and Communications

26. The External Auditor has undertaken an audit on Resource Mobilization and concurred with IOS 2015 audit on several aspects. Notably, the need to (i) promote the strategic importance of resource mobilization by regularly reporting to the Senior Management Team (SMT) on progress through periodic monitoring and reporting on resource mobilization, and (ii) improve the alignment of UNESCO’s communication activities with regard to fundraising efforts. Addressing both audits should be a key priority for the organization in 2018.

27. The audit of correspondence management identified the use of the SharePoint-based Correspondence Management (CM) system as an important tool that can contribute to the Organization’s responsiveness, overall credibility, and relevance. The audit noted however that over the years the system has not been updated to meet user requirements and its performance has significantly degraded due to technical deficiencies. This contributed to substantial loss of staff time, delayed correspondence handling and exposure to information security risks. As a response to the audit, the upgraded Correspondence Management System was launched in October 2017.

204 EX/22 – page 6

28. The audit of UNESCO’s transparency project noted lack of a coherent vision and overall objectives and recommended restructuring of the Transparency Project steering committee to improve programme sector involvement and organizational-wide consensus. Main recommendations of the audit are being implemented in a phased manner, and reported to the steering committee. A vision document has already been prepared and greater representation has been given to the programme sectors on the steering committee.

Field Offices, Institutes and other Decentralized Operations

29. UNESCO has demonstrated leadership in piloting the Business Operations Service (BOS) initiative in Brazil, resulting in the launch of the Joint Operations Facility (JOF), which consolidate support functions to the United Nations operations. As the JOF transitions to full operation, the Brasilia Office needs to ensure that the JOF achieves its objectives namely cost reduction and enhanced operational support. The audit also recommends that monitoring of project implementation as well as programmatic and administrative reviews of contracting and procurement are strengthened to ensure value for money in the context of national execution of self-benefitting project.

30. The audit of the International Bureau for Education (IBE) identified significant cost-saving opportunities ($520,000 per year) through rationalization of office space and recommended for improved risk management practices and resource mobilization approach. The Institute has secured smaller premises that would enable substantial savings and has implemented better risk recording and monitoring practices.

31. IOS conducted a remote audit of UNESCO’s field office in Khartoum. While the Office is making efforts to increase its engagements in the country, managing to attract funds for extrabudgetary sources and drawing on global and decentralized funds, it faces continued challenges with regard to efficiency and sustainability of interventions. Given its limited human and financial resources the audit noted the need for stronger programmatic focus, a more systematic approach to donors guided by a sound country strategy, and the need to increase efficiency by strengthening procurement and travel planning.

32. An IOS audit of field security confirmed that UNESCO cooperates effectively within the unified security system of the United Nations, the United Nations Department of Security and Safety (UNDSS) and that United Nations policies, procedures, standards and other arrangements have been applied to all personnel engaged by UNESCO. It also confirmed an improvement in field security since 2012 (the date of the previous such audit) due to the introduction of the Minimum Operational Standards for Safety and Security (MOSS) self-assessment and the implementation rate of MOSS recommendations. The audit showed that significant improvements are needed on security awareness and training of personnel both in Headquarters and the field.

33. Finally, a verification audit of the PADTICE project concluded that in general the expenses charged are eligible in nature, supported by appropriate documentation and reasonable.

Gender

34. IOS reports on Gender Responsive Auditing to UN-WOMEN for the UN System-wide Action Plan for the Implementation of the CEB (Chief Executives Board for Coordination) Policy on Gender Equality and the Empowerment of Women (UN-SWAP). In 2017, Internal Audit reported “meets requirements” for this performance indicator. Consultations were held with the Division for Gender Equality on risks related to gender equality and the empowerment of women, as part of the risk-based audit annual planning cycle. Where relevant internal audit reports now systematically reflect gender-specific findings.

35. During 2017, The UN-SWAP audit performance indicator on gender was raised in UN-SWAP 2.0. UNESCO led a UNRIAS Gender Interest Group (GIG) comprising of eight United Nations audit

204 EX/22 – page 7

services, setting out more ambitious performance indicators for audit functions and developing relevant audit toolkits and approaches in line with UN-SWAP 2.0. During the past year, the GIG established a “tool box” workplace for auditing gender equality, and undertook a comparative analysis of UN-SWAP maturity across United Nations entities. The consolidated results of this exercise were presented by the Director of IOS in her capacity of Chair of the GIG at the UNRIAS annual meeting (August 2017).

EVALUATION

36. By putting the 2014-2021 Evaluation Policy for UNESCO and the Evaluation Strategy for its implementation into practice during 2017, IOS has been further strengthening the position of evaluation as a strategic management tool to ensure the wider use of evaluation findings to improve decision-making and to promote organizational learning and accountability. In line with the updated UNESCO Administrative Manual Chapter 1.6 that reflects the adoption of recent evaluation and audit policies, IOS continued to explain and strengthen the roles and impact of corporate evaluations (conducted by the IOS Evaluation Office) and put a particular emphasis on strengthening the management and quality of decentralized evaluations (managed by UNESCO entities with a programmatic function).

Evaluation Funding and Coverage

37. Following the Ivory Note (DG/Note/16/12) issued by the Director-General in 2016 that established 3% of operational or activity budget as the minimum level of investment in evaluation, financial resources have been allocated more consistently although not yet reaching the set target. The more systematic budgeting for evaluation in the Regular Programme by the programme sectors in the 39 C/5 (Figure 1) has provided a solid base for more consistent coverage as of the 2018/19 biennium. Regarding extrabudgetary resources efforts are underway to ensure appropriate allocation for evaluations in new extrabudgetary projects. It is therefore too early to see the effect of the evaluation policy. IOS plans to track and report on evaluation expenditure for both regular and extrabudgetary resources and will reflect on lessons learned in future annual reports.

Table 3: Actual Investment in Evaluation

Year

Regular Programme resources Extrabudgetary resources

Operational budget (C/5 approved)

Actual investment*

% investment (3% target)

Estimated operational expenditure

Actual investment

% investment (3% target)

2014/15 171,000,000 2,850,000** 1.7% 280,000,000 1,750,000 0.6%

2016/17 184,000,000 2,297,000 1.25% 280,000,000 1,820,000 0.65%

2018/19 186,892,000 3,412,455 1.82% 280,000,000 n/a n/a

*Includes full IOS evaluation budget ** 574,000 additional appropriation in 2014/15

NB: assumption under extrabudgetary that the operational budget is approximately 70% of the total.

204 EX/22 – page 8

Figure 1: Actual Investment in Evaluation per Programme sectors (RP only)

38. In terms of coverage and types of evaluations, IOS undertook six programmatic evaluations, and one case study, belonging to the education (1), natural sciences (2), social sciences (2), culture (1) and communication sector (1), as was foreseen in the 2017 evaluation plan. The IOS Evaluation Office also provided guidance and technical backstopping to varying degrees to a number of decentralised evaluations, managed by sectors, offices and bureaus of which some complementary to its corporate evaluation work (such as the mid-term external evaluation of the Azerbaijan Trust Fund with a focus on projects in girls’ education, or the evaluation of the UNESCO/Flanders Trust Fund (FUST) in the field of Natural Sciences) and some of strategic relevance such as the evaluation of the Mahatma Ghandi Institute for Peace Education (MGIEP) or the ongoing evaluation of the Global Education Monitoring Report. Summaries of corporate evaluations completed in 2017 are provided in document 202 EX/5 Part II, while the full reports are publicly available on the IOS website in English with summaries in French. The provisional evaluation work programme for 2018/19 is presented in Annex II.

39. As per established practice, IOS continuously reached out to all field offices, institutes and programme sectors in order to collect decentralized evaluation plans and evaluation reports. Throughout the year and as of January 2018, 28 decentralized evaluations were completed and submitted to IOS, all of which have received some level of support from IOS. Due to the 3% target, it is expected that the investment in and volume of decentralized evaluations will increase throughout the next biennium.

Strengthening the decentralized evaluation function

40. With the aim to further strengthen the decentralized evaluation function, in particular through the new Evaluation Focal Point Network, IOS utilized the funds received from the “Invest for Efficient

0

1,42 % ED

2,55 % SC

2,65 % SHS

0

2,75 % CLT

2,61 % CI

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

2014/15 2016/17 2018/19

Programme sectors’ Investment in Evaluation

Education Natural Sciences ScienceSocial and Human Sciences CultureCommunication and Information

204 EX/22 – page 9

Delivery Fund” for the development and rollout of an evaluation management training programme in 2017. This programme included the development of online training modules as well three-day practical face-to-face capacity development sessions at Headquarters and in various field offices covering all the regions. The training sessions were principally targeting Evaluation Focal Point Network representatives from field offices, institutes and programme sectors as well as office staff in the selected locations.

41. Through this customized workshop-based training on evaluation management, approximately 200 staff have been trained during seven training events that were held in 2017 (UNESCO Headquarters, Beirut, Nairobi, Dakar, Santiago, Bangkok and International Institute for Education Planning (IIEP) in Paris). In each location, two formats have been utilized: (except in UNESCO HQ) a half-day office-wide workshop for all staff in the host office, and a subsequent three-day core workshop for the Evaluation Focal Points. Nevertheless, as is good practice, relevant improvements and minor modification had already been incorporated for each iteration of the workshop, based on immediate participants’ feedback and the facilitator’s and IOS Evaluation Office’s impressions. As an immediate outcome of the training sessions, it has been observed that a number of Evaluation Focal Points have given an adapted version of the training to their colleagues upon return to the office, so an even larger number of staff have been reached.

42. The content for the four e-learning modules on evaluation has been fully developed in 2017 and the online version of the training is currently being finalized by an e-learning developer who has been selected in response to market consultation. The e-learning material will be finalized and further refined in a pilot phase for Evaluation focal points during the first half of 2018 and will consequently be made available to all UNESCO staff, in both English and French.

43. To further support and animate the Evaluation Focal Point Network, a Community of Practice has been developed as an interactive space on the UNESTEAMS where the Evaluation Focal Points shall interact among each other and with the IOS Evaluation Office. It is intended as a virtual space to share good practice and resources such as guidance material and all the training material; and where all Decentralized Evaluation Plans and Final Evaluation Reports will be kept.

Dissemination, Communication and Learning

44. Throughout 2017, the IOS Evaluation Office continued its efforts to enhance the dissemination of its evaluation findings and thereby contribute to greater organizational learning. IOS published seven issues of the Evaluation Insights newsletter (available at www.unesco.org/ios), in two working languages. The newsletter was widely shared with UNESCO staff, Member States representatives and external partners and was downloaded extensively from the IOS website. Other efforts to raise the visibility of the IOS evaluation training initiatives and the readership of evaluation reports and initiatives included the publishing of articles on UNESCOMMUNITY and on the dedicated website for UNESCO Member States. Evaluation staff presented findings and recommendations to internal and external audiences on a number of occasions, such as at the sixth Conference of Parties to the International Convention against Doping in Sports and the UNEG Annual Meeting 2017. The six evaluation reports and the case study released by IOS in 2017 were downloaded extensively during the course of the year. Furthermore, IOS initiated a revision and modernisation of its website and communication strategy. The pilot version of the new website is envisaged to be available in early 2018.

Networking

45. IOS has continued to be actively involved in the United Nations Evaluations Group (UNEG). In particular it further increased its engagement since the election of the Director of IOS as the UNEG Chair (2017-2019) and assuming the convening role of the Culture and Evaluation Interest Group. Within the context of the work of the Humanitarian Evaluation Interest Group, the IOS Evaluation Office presented the Evaluation of UNESCO’s role in education in emergencies and protracted crises at the annual UNEG Evaluation Practice Exchange seminar in May 2017 and also continues working

204 EX/22 – page 10

with other agencies on joint initiatives. IOS prepared a Note on the development of Culturally Responsive Criteria for Evaluation and commissioned the development of guidance note on culturally responsive evaluation criteria and indicators. Furthermore, the IOS Evaluation Office was actively involved in several UNEG working groups such as the Decentralised Evaluation Interest group, working groups on Norms and Standards, Ethics and Code of Conduct, and on Knowledge Management on Use of Evaluation.

Contribution to reform and programmatic improvements

46. Several key evaluation activities have contributed to the improvement of, inter alia, the following reform efforts, strategies and policies in UNESCO over the past year:

• Evaluation reports provided a valuable contribution to strategic reflections and discussions among Member States. Findings and recommendations from IOS evaluation reports were discussed in-depth and jointly with the respective programme sectors during the 10th Intersessional Meeting of the Executive Board Members and cited significantly in relevant Executive Board and General Conference Documents issued in 2017.

• The 2015 evaluation of the EFA regional and global coordination influenced decisions for a revised coordination architecture and roadmap of the SDG 4 - Education 2030 Coordination.

• The 2015 evaluation of Culture and Sustainable Development fed into the development of operational directives to guide the implementation of the 2003 Convention (adopted by the General Assembly of the States Parties in June 2016), and helped the CLT Sector to identify synergies and better cooperation amongst several Culture Conventions. It also triggered cooperation with other programme sectors in light of the implementation of SDG Agenda.

• Inspired by the findings and recommendations of the 2016 evaluation, the ASPnet Strategy was revised in consultation with over 50 National Commissions and its future thematic focus agreed to by the end of 2017. In light of the revitalisation process of the ASPnet triggered in part by the evaluation, several collaborations with programme sectors and new flagship initiatives with external partners were launched during 2017.

• A new accountability and results matrix, developed in consultation with the UNESCO TVET Community, and approved by the Executive Board in September 2016 (200 EX/8, 200 EX/36 Action plan for the implementation of the Strategy for Technical and Vocational Education and Training (TVET) (2016-2021), is providing a more adequate monitoring framework for the New Strategy for TVET that was developed in light of the evaluation recommendations of the 2016 TVET Evaluation.

• The recent evaluation of the UNESCO Science Report has resulted in the establishment of an inter-sectoral working group within UNESCO with the aim to strategically reform the design and to streamline the production process of the upcoming UNESCO Science Report 2020.

• The 2017 evaluation of UNESCO’s work in the Basic Sciences and Engineering has raised strategic concerns about the Sector’s capacity-building work in this area and the way forward towards strengthening BSE and defining comparative advantages is currently explored together with partners such as ICTP, TWAS, category 2 institutes, and UNESCO Chairs.

204 EX/22 – page 11

Gender

47. As a member of the Working Group on Gender Equality and Human Rights, the IOS Evaluation Office participated in the 2017 UN-SWAP process. Based on a self-assessment, UNESCO scored 9.05 out of 12 (compared to a score of 8,55 in 2016) on its UN-SWAP annual rating, thus meeting the requirements of both UN Women and the United Nations Evaluation Group (UNEG) in terms of gender mainstreaming. It has to be noted that the quality gap between the corporate and decentralized evaluations has lessened compared to the 2016 rating. This improvement may be indicative of the increasing awareness and capacities resulting from the establishment of the Evaluation Focal Point Network and the training sessions on evaluation management conducted in various locations around the world, which among other included a gender equality module underlining the importance of applying a gender-sensitive approach to evaluation in UNESCO. IOS expects to register further improvement in the coming years as the lessons learned so far will be implemented more widely, and as a result of further guidance material and online training modules on evaluation which will be launched during 2018.

48. The assessment also showed that gender mainstreaming is particularly encouraged in education-related projects as women are viewed as a particularly relevant targets group and often times marginalized while their access to education and literacy is conditioning development. Hence, the highest scores in the UN-SWAP were registered in evaluations such as the evaluation of UNESCO’s Programme Interventions on Girls’ and Women’s education (12 points) or the Ramallah Office’s evaluation on the project entitled “Support Program for Palestinian University Students under Conditions of Severe Poverty Projection” (10 points). Some exceptions aside, including a gender focus in UNESCO’s other programmatic sectors has proven to be more difficult. Nonetheless, the assessment showed that most projects had a gender component and had taken measures to further engage women and girls in all activities, even though this was not always explicit in the project’s intervention logic or in its reporting and monitoring mechanisms. There are cases where gender mainstreaming has taken place informally rather than through a structured approach; hence rendering the assessment of the level of gender mainstreaming more challenging. For instance, the IIEP’s evaluation on the technical cooperation programme revealed that although 90% of the IIEP’s projects launched between early 2016 and May 2017 had not used the Gender Equality Measure foreseen in its project management information system, stakeholders interviewed had witnessed the project implementation engaging particularly with women and dealing with gender-related issues. This points to the fact that gender is taken into account in the design and implementation of projects, but project managers often do not see the importance to refer to this explicitly.

RECOMMENDATION FOLLOW-UP

49. IOS continues to issue recommendations in order to assist UNESCO in meeting its strategic objectives, to improve the organization’s programme delivery, efficiencies and controls and to inform strategic decisions and to improve programme delivery. IOS systematically follows up on the implementation of both Internal Audit and Evaluation recommendations. IOS regularly brings overdue recommendations to the attention of the Senior Management Team for action.

50. As of 31 December 2017, there were 150 open Internal Audit recommendations, an increase from the 125 open recommendations at the beginning of the year. During 2017, 87 new audit recommendations were issued and 62 recommendations were closed (of which 79 percent were fully implemented). IOS has engaged in an ongoing constructive dialogue with management in order to facilitate the implementation of older recommendations.

204 EX/22 – page 12

Figure 2: Internal Audit Outstanding Recommendations Status as of December 2017

Figure 3: Internal Audit Outstanding Recommendations Status as of December 2017

51. With regard to Evaluation recommendations, as of 31 December 2017, there were 45 open recommendations for 11 evaluations issued since 2015, a decrease compared to overall 54 open recommendations open for the then 11 evaluations since 2013 a year earlier. During 2017, 32 new evaluation recommendations were issued and 41 were closed. The figure below shows the implementation of recommendations for reports issued during 2013-2017. The focus in 2017 had been on addressing recommendations that have been open for more than three years. Consequently all evaluation recommendations for reports issued before 2015 have been closed.

Figure 4: Implementation of Evaluation Recommendations as of December 2017*

*out of the total number of recommendations issued per year

High Priority

38

Medium Priority107

Low Priority

5

Less than one year30

One to tw o years

72

Tw o to four years

44

More than four years

4

46

63

42

7

9

18

34

54

3

28

0% 20% 40% 60% 80% 100%

2014

2015

2016

2017

Implemented Overdue Not yet due

50

68

12

22

0

0

0

7

6

32

2013

2014

2015

2016

2017

Implemented In progress

204 EX/22 – page 13

INVESTIGATION

52. IOS is responsible for investigating allegations of corruption, fraud and other misconduct by UNESCO staff or third parties including consultants. Allegations are subject to a preliminary assessment to establish whether they are specific, credible, material and verifiable. Where the screening indicates misconduct, the matter is formally investigated by IOS upon instructions of the Director of IOS who has full authority to open and close investigations. The investigation report concludes whether the allegation of misconduct is substantiated and recommends whether or not administrative or disciplinary action should be considered.

53. Beyond timely examination and determination of the veracity of allegations received, the IOS Investigation Office pursues three strategic priorities:

(a) Increase visibility of the function;

(b) Address blind spots;

(c) Enhance robustness of procedures.

54. Those priorities are in line with the recommendations of the United Nations Joint Inspection Unit 2016 report on “Fraud Prevention, Detection and Response in United Nations System Organizations”. They were implemented by the IOS Investigation Office through the following antifraud activities performed in 2017:

(a) a fraud awareness programme. Two hundred and forty-seven UNESCO personnel in Headquarters and in the field have attended in 2017 (327 since inception in 2016);

(b) a Fraud Risk Assessment exercise. An international bidding process resulted in the selection of an Australian consulting firm. Delivery of the fraud risk map is expected by mid 2018;

(c) consultation on anti-fraud clauses of standard and non-standard agreements.

55. In 2017, IOS received 47 new allegations and 43 allegations were closed – this included six cases carried over from 2015. Sixty-three percent of the cases opened in 2017 were at Headquarters and thirty-seven percent in field operations. IOS issued 63 investigation products during the year, including 37 screening memoranda, 2 17 other management memoranda and six investigation reports, all conforming to prevailing professional standards and in line with UNESCO’s disciplinary procedures.

Table 4: Caseload of the Investigation Section 2015-2017

Year 2015 2016 2017

New allegations 27 32 47

Allegations closed 23 45 43 Including recommendation for disciplinary action 3 8 4

Caseload as of 31 December 2016 19 6 10

2 Screening memoranda include a recommendation to DIR/IOS to either open a formal investigation or to close the

matter and to refer it to competent service(s) whenever appropriate.

204 EX/22 – page 14

56. Of the 43 allegations closed in 2017, the allegations required a fully-fledged investigation in 23% of the cases while another 34% was referred for action to appropriate services (e.g. Ethics, HRM, Mediators, Supervisors, etc.). In 43% of the cases, the allegation did not result in an investigation, as it could not be substantiated.

Figure 5: Closures of Allegations in 2017

57. The duration of investigations conducted by IOS depends on the nature of the allegations, the required investigative steps and available resources. In 2017, the average duration of investigations was 3.6 months. In comparison, the average duration of investigations in 2016 was 5.5 months.

Figure 6: Nature of Allegations Received (2017)

ADVISORY ROLE

58. IOS advisory work is performed at the request of the Director-General and Senior Management, such as the Comparative Mapping of Forms and Models for Use of Advisory Services by International Instruments and Programmes has been performed (see more in the Audit section). IOS also follows its advisory engagement in the long-term such as accompanying the establishment of UNESCO’s risk management process.

59. IOS staff also attended a number of internal task forces and initiatives on an observer basis, inter alia on the Core Redesign project, the Constituency Relationship Management tool and the risk management committee.

OVERSIGHT ADVISORY COMMITTEE

60. IOS functions as the secretariat for the Oversight Advisory Committee (OAC), a standing committee established at the 35th session of the General Conference (35 C/Resolution 101). Its main purpose is to advise the Director-General on the proper functioning of oversight, risk management and controls and to inform the Executive Board through the submission of its annual report, which is presented as 204 EX/22.INF. The OAC is comprised of five external independent

Investigations23%

Screening -> closure43%

Screening -> referral34%

75 5

3 46

17

Entitlements, traveland expenses

Procurement Recruitment (allpersonnel)

Harassment /Retaliation

External fraud Thefts andembezzlement

Otherinappropriate

conduct

204 EX/22 – page 15

members, as per the revised Terms of Reference by the 200th session of the Executive Board. The OAC met three times in 2017.

JOINT INSPECTION UNIT (JIU)

61. IOS serves as UNESCO’s focal point and follows up on recommendations of the JIU that are relevant to UNESCO. Information on JIU recommendations is available on the IOS website at (www.unesco.org/ios) on the JIU website (www.unjiu.org) and the JIU follow-up system. Of note is a JIU management letter received by UNESCO in 2016 (JIU/ML/2016/13) which commends the Organization for its uptake and implementation of JIU recommendations. The same review requests that JIU reports, of concern to UNESCO, as stipulated in the JIU charter and as provided for in decisions 198 EX/Decision 6 (I) and 193 EX/7 (Part I, IIIb), are tabled on the agenda of the Special Committee.

LOOKING FORWARD

62. In regard to the tentative IOS work programme for 2018/19 (see Annex II), the Evaluation Office will focus on the completion of key strategically significant evaluations as per 2018/19 evaluation plan, and timely input to SRR and the Internal Audit Office will focus on key areas of risk, such as, the project management cycle, budget management, and the field offices network. The Evaluation Work Programme was developed taking into account the need to provide evaluation coverage of key organizational programme priorities, e.g. youth, freedom of expression, science, technology and innovation policy. The Internal Audit work programme for 2018/19 was developed based on a risk assessment taking into consideration internal and external factors. Both programmes include activities that are subject to the availability of additional resources. Finally, in response to the JIU report on “Fraud Awareness in the UN System”, the Investigation Office has designed a fraud risk assessment exercise, launched in 2018 and financed by the Invest for Efficient Delivery fund.

Proposed decision

63. The Executive Board may wish to adopt a decision along the following lines:

The Executive Board,

1. Recalling 160 EX/Decision 6.5 and 164 EX/Decision 6.10,

2. Having examined document 204 EX/22,

3. Welcomes the role of the Internal Oversight Service in the functioning of the Organization;

4. Appreciates the advice and recommendations provided to the Director-General by the Oversight Advisory Committee, and requests the Director-General to ensure the full and timely implementation of all recommendations accepted by the organization;

5. Requests the Director-General to ensure that all Internal Oversight Service recommendations are fully implemented within a reasonable time-frame;

6. Requests the Director-General to maintain an effective oversight function as set forth in the respective revised IOS Internal Audit and Evaluation Policies and to report annually on Internal Oversight Service strategies and activities, significant oversight recommendations and their impact, as well as actions taken by the Director-General to address and implement these recommendations;

7. Recalling 199 EX/Decision16 (III) requests the Director-General to ensure that the IOS risk-based audit work plan is fully funded within the 39 C/5.

204 EX/22 Annex I

ANNEX I

AUDITS COMPLETED IN 2017

PRINCIPAL AUDITS COMPLETED

Audit of the Field Office Security

IOS conducted an audit of field security to provide assurance that an effective accountability mechanism exists in UNESCO to ensure security of personnel and compliance with UNDSS guidelines in order to effectively mitigate security risks to field operations.

UNESCO field security arrangements are largely aligned with the UNDSS Framework of Accountability for the United Nations Security Management System. Recently established guidance on security of meetings and conferences outside Headquarters closed a crucial gap in the accountability mechanism. However, similar guidance is also required for meetings and conferences organized by the field offices. The Host Country responsibilities for security needs to be explicitly included in new seat agreements. Further, the HR Manual needs to be updated to reflect current responsibilities regarding field security.

Minimum Operating Security Standards (MOSS) self-assessment, introduced in 2015 is a welcome step. However, there is a need to establish an IT enabled monitoring tool to track the security preparedness and challenges in field offices. Further, the budgetary control on field security budget needs strengthening. The audit also noted significant under recovery of security costs from the extrabudgetary projects.

The audit showed that significant improvements are needed on security awareness and training of personnel both in Headquarters and the field.

Audit of the Correspondence Management System and related process

Correspondence management is an important component of an Organization’s communication process. At UNESCO, correspondence covers memorandums, emails, letters and faxes, and helps the Organization communicate to its various stakeholders as well as contribute to its credibility, relevance and efficient delivery . The Office of the Director General oversees correspondence including those addressed to the Director-General and the Deputy Director-General. This critical process is supported by a SharePoint based Correspondence Management (CM) system accessible at Headquarters and in UNESCO field units. Over the years, the system has not been upgraded to meet user requirements and its performance has significantly degraded due to technical deficiencies.

The decision to upgrade the CM system has been delayed mainly due to lack of funding and low prioritization vis-a-vis competing projects. As a result, despite willingness to use the system, technical deficiencies have led to substantial loss of staff time, delayed correspondence handling and exposure to information security risks. Discrepancies in administrative guidance and lack of training in correspondence management prevail. Users are not fully aware of their responsibilities and lack skills to use the CM system. Consequently, the CM system data is incomplete and the quality of its reports is impaired.

Audit of the UNESCO's Management Framework for Cat 2 Institutes/Centres

Institutes and centres under the auspices of UNESCO (category 2 institutes/centres) have experienced a rapid growth in the past ten years and now total 115. Of those, however, two thirds are not operational in conformity with the current framework. Most of these non-operational institutes/centres are not yet established as category 2 institutes/centres. The establishment process proves to be lengthy and cumbersome, requiring considerable investment in staff time from the Secretariat before benefits materialize.

Given UNESCO’s reduced capacity, efforts should be directed towards a limited number of institutes/centres, preferably with proven records of excellence and that can effectively collaborate with UNESCO to achieve its 2018-2021 programme objectives. As a priority, the Secretariat should (i) examine the non-operational institutes/centres and recommend revision or termination of the agreement, (ii) develop overarching criteria to limit the number of institutes/centres, and (iii) improve the screening process for proposals and renewals.

204 EX/22 Annex I – page 2

A Comparative Mapping of Forms and Models for Use of Advisory Services by International Instruments and Programmes

This IOS study reviewed the forms and models for the use of advisory services by similar international instruments and programmes. IOS concluded that currently the services obtained by the World Heritage Committee from Advisory Bodies (IUCN, ICCOMOS and ICCROM) constitute 75% of the total budget from the World Heritage Fund, leaving very little for other key tasks such as providing international assistance to the State Parties.

The current practices for assessing nominations to the World Heritage List by the Advisory Bodies are heavy and costly when compared with those of similar international instruments and programmes. There is an opportunity to revisit the working methods and adopt practices from other international instruments and programmes. Further, some advisory services such as assessing requests for international assistance and reactive monitoring missions can be sourced differently, e.g. from a panel of experts established by the Committee.

Audit of the UNESCO Transparency Project

IOS conducted an audit of the UNESCO Transparency Project to provide assurance that the Project is well planned and implemented in an economical, efficient and effective manner. The scope of the audit includes Phase I and Phase II of the Project. UNESCO started reporting to IATI on an annual basis since 2015 and launched the Transparency Portal in the same year, which was later upgraded in January 2017. The Portal presents UNESCO financial and activity information in an interactive and intuitive manner. An assessment of several portals developed by other United Nations agencies shows that UNESCO’s portal is generally in line with the other portals.

However, the Transparency Project faces several challenges. The Project lacks a coherent vision and overall objectives. Furthermore, the structure and purpose of the Steering Committee needs revisiting in order to increase senior management buy-in for organizational-wide consensus on the way forward and to increase involvement of programme sectors. UNESCO’s datasets on the IATI dashboard score low on the coverage-adjusted score. Greater monitoring is also needed on the usage of the portal to increase its visibility with the intended stakeholders

Performance Audit of Official Travel

IOS conducted a performance audit of UNESCO’s official global travel covering mission and statutory travel undertaken in 2015/2016. Travel expenditures amounted to $21.6 million during the period. Efficiency measures introduced following the financial crisis resulted in 37% reduction of travel expenses in 2016 when compared to 2011.

If a number of good industry practices are followed, further biennial savings of up to $4 million (18.5%) can be achieved through timely purchase of tickets, aligning the basis of lumpsum payments for statutory travel with the United Nations Secretariat, implementing a self-booking tool and optimizing administrative processes. The above savings could be further augmented by assigning travel management responsibilities to a staff with extensive experience in the travel industry for cost effectively procuring travel services through global sourcing arrangements and joint procurement with other United Nations or international organizations at UNESCO Headquarters and field offices.

As a first line of defense function, these responsibilities should also include monitoring and assessing compliance with UNESCO’s travel policy. UNESCO needs to reinstate a strong second level of defense to ensure better monitoring and reporting on adherence with the travel rules and policy. This implies clear ownership under a single authority of the travel process, both in terms of management and policy. Accordingly, in line with United Nations practices, MSS should assume travel related responsibilities including those under BFM. Finally, temporary cost reduction measures in effect since 2012 need to be revisited in light of their intended impact. BFM should address current gaps in travel related administrative guidance before handover of the travel policy to MSS.

204 EX/22 Annex I – page 3

Audit of the World Academy of Sciences (TWAS)

As part of IOS’s annual audit plan, IOS audited the UNESCO TWAS programme unit, hosted by ICTP in Trieste. Funded entirely by extrabudgetary funding, this programme aims to advance science and engineering for sustainable prosperity in the developing world. TWAS is currently hosting three entities namely, the Organization for Women in Science for the Developing World (OWSD), GenderInSITE (GIS) and InterAcademy Partnership (IAP), each with their own separate governance structure.

There is a need to clarify the relationship between TWAS and its hosted entities and consolidate into a single governing structure. Additionally, streamlining the administrative capacity present in TWAS and each of the hosted entities will result in efficiencies. TWAS generally manages its funds in accordance with the donor agreements and maintains accurate financial records of commitments. However, the administrative unit needs to exercise more control when certifying contracts to ensure competitive selection and better-developed terms of reference. TWAS also needs to establish a formal risk management mechanism and participate in UNESCO’s annual control self-assessment exercise. Greater interaction with the science sector and corporate services will help the TWAS better communicate its programmatic achievements and improve compliance and visibility.

Verification Audit of PADTICE Project Implemented by UNESCO Dakar

In line with article 10 of the PADTICE Implementation Partnership Agreement, IOS with the assistance of Grant Thornton Senegal carried out a verification audit of the project expenses with the purpose of determining whether these were incurred in compliance with UNESCO administrative and financial rules and procedures as well as the donor agreement. Since February 2013, the project was managed by UNESCO Office in Dakar (BREDA). Its technical implementation was completed in December 2015.

As of February 2017, the donor had disbursed a total of $9.66 million and the project expenses amounted to $9.15 million out of its initial total budget of $12.7 million. The audit concluded that the expenses charged to the PADTICE project are eligible in nature, supported by appropriate documentation and reasonable, with a few exceptions. In some cases, the project management did not comply with article 5 para. 9 of the donor agreement that requires UNESCO to seek donor’s no-objection for shortlisted service providers before any contract signature. The total of such contracts are valued at $659,060. In a separate instance, documents supporting an expense of $685 could not be located.

Audit of UNESCO’s Statement on Internal Control

IOS conducted an audit of the Statement on Internal Control (SIC) to provide assurance that it is well managed and effective, focusing on the Control Self-Assessment (CSA) process.

The SIC has been issued annually since 2011, putting UNESCO among the first United Nations agencies to have established an annual SIC as part of its Annual Consolidated Financial Statements. However, the SIC is typically issued before the analysis of the CSAs presented to the Senior Management Team (SMT), limiting the use of the CSAs’ analysis for SMT discussions on the SIC. Broadening consultations on the SIC with more stakeholders as stipulated in the SIC methodology would make it more meaningful.

The CSA is completed by all entities as required. However, IOS assessments of the CSA diverge significantly compared to the self-assessments in some functional areas. Additional guidance on the CSA methodology would improve its reliability and comparability. There needs to be a greater link between the SIC and CSA process and the risk identification and management process. Despite the issuance of various memos and the 2016 IOS Advisory on Enterprise Risk Management, risk registers at the entity-level are still largely missing and the corporate risk register is still under development. The Risk Management Committee (RMC) should continue to implement Action Three from the 2016 IOS Advisory on ERM (IOS/AUD/2016/05) and also continue to develop the BCP Strategy and the BCP for the field. Insufficient monitoring by entities of mitigation actions required to manage potential weaknesses means that the CSA exercise has a limited operational use. Despite the methodology requiring the elaboration of action plans, in most cases these were not reported in CSAs, and hence it is not possible to determine whether the underlying operational risk was managed/mitigated at the entity level.

204 EX/22 Annex I – page 4

Audit of IBE-UNESCO

IOS conducted an audit of the International Bureau of Education, a UNESCO category 1 institute, to assess the functioning and the effectiveness of risk management, internal controls and governance. The audit concluded that the Institute is generally governed and managed as per the criteria established by the Executive Board for category 1 institutes, however there is a need to establish a formal risk management system at the Institute.

The Institute funding mostly comes from extrabudgetary sources (66%). In light of declining contributions from the host government, the financial sustainability of the Institute is challenged and a longer term funding strategy is needed. In the short term, the Institute can save up to $520,000 per year by rationalizing the use of office space.

Expenditure, including on procurement and contracting, is in compliance with the Organization’s policies and generally follows the best value for money approach. Travel management is also well controlled. Some issues have been identified as needing improvement in the human resources management. The audit also noted that the institute has revised its royalty arrangement for its flagship publication to obtain more favorable terms. Similar arrangements should be pursued for other publications with a view to ensure full cost recovery.

Audit of the Brasilia UNESCO Office

The sustainability of the UNESCO Office in Brasilia has been a persistent challenge for the past decade. Given the Office’s reliance on self-benefitting funds and recent host country events, sustainability has become a pressing issue that the Office is proactively addressing.

The establishment of the Joint Operations Facility (JOF) that results from the Business Operation Strategy Initiative is an achievement towards harmonizing UN operations in Brazil and consolidating support functions. UNESCO needs to ensure that the JOF achieves its objectives namely cost reduction and enhanced operational support.

The audit concluded that the Office’s projects generally align with UNESCO’s programme objectives but monitoring needs strengthening given the national execution modality. Additionally, both programmatic and administrative reviews of contracting and procurement need to be more rigorous to ensure value for money.

UNESCO’s Office in Khartoum

IOS conducted a remote audit of UNESCO’s Office in Khartoum to provide assurance on the effectiveness of governance, risk management and internal control processes. While the office is making efforts to increase its country footprint, it faces continued challenges with regards to efficiency and sustainability of interventions. Given the high staff costs compared to regular programme funds, the long term financial sustainability of the office may be at risk if the Office is not able to deliver upon its UNDAF commitments and to mobilize sufficient funding.

Given the scarce human and financial resources there is need for programmatic focus and proactive resource mobilization efforts. A more systematic approach to donors guided by specific targets and supported by a sound strategy and risk management practices is required. Close monitoring of joint implementation with United Nations partners requires more efforts by the Office to ensure that UNESCO delivers upon its commitments. Finally although the control environment is generally functioning some weaknesses related to Procurement and Travel were noted. These were mainly originated by poor planning and excessive use of single source contracts which led to financial losses and the office not being able to ensure value for money.

204 EX/22 Annex I – page 5

Audit of Non-Expendable Property Management at Headquarters

IOS conducted an audit of the management of non-expendable property and the works of arts to provide reasonable assurance that these are managed in an efficient and effective manner. IOS concluded that controls need to be improved to ensure correct recording of inventory, its proper management, including periodical physical verification, and effective disposal.

IOS noted discrepancies between barcode number and the corresponding asset number as recorded in the asset register, which makes the asset identification difficult. While, this has been corrected for some IT equipment purchased since November 2016, the discrepancy persists for other items. Further, the custodian system as required under the policy is not functional and needs to be established for ensuring accountability and safe custody of assets. In addition, weak inventory recording practices coupled with dysfunctional physical inventory verification process leads to inaccurate asset register and poses risk of inventory loss. In a sample testing, IOS found a number of new asset acquisitions that were either not recorded or incorrectly recorded. There is a need to strengthen the inventory recording practices and physical verification process at Headquarters. UNESCO maintains a collection of approximately 800 works of art. Only a part of the collection has been valued with estimate of the collected value ranging from 90.5M to 124.3M euros. There is a need to put in place a risk mitigation strategy as the collection is not insured for theft or irreparable damage, while at UNESCO premises. In addition, discrepancies noted in the last physical verification need to be reconciled. Finally, there has been a significant delay in the finalization of the gift policy. Lack of guidance regarding acceptance and management of gifts potentially weakens the ethical environment of the organization. UNESCO is in the process of finalizing a wider conflict of interest policy, which would also provide guidance on how gifts should be handled, reported, registered, and disposed of.

204 EX/22 Annex II

ANNEX II

INDICATIVE WORK PROGRAMMES

RISK-BASED INTERNAL AUDIT PLAN 2018/2019

Audit Universe Audits to be Performed 2018 20193

Headquarters Audits Programme & Project Management:

Project Management Cycle

Cost Recovery

X

X

Headquarter Central and Support services

Budget Management incl. status RBB Project X

HQ Security (mix sourcing cycle) X

Revenue generating activities X

Entitlements/Payroll X

Publications and printed materials X

Follow up of Risk Management

Treasury/Cash Flow Management

Follow up on Recruitment

Procurement

Follow up on Risk Management

Audit on the effectiveness of Gender equality4

X

X

X

X

X

X

IT Audits IT Governance, Acquisition & Development X

Data Stewardship X

Follow up of Cybersecurity

Redesign Core Systems 5

IT audit (to be determined)

X

X

X

Field Audits Four Field Offices i.e. Yaoundé, Dar-Es-Salaam, Santiago (field visits) and Kingston (Remote)

X

One Category I Institute i.e. UIS

Four field offices i.e. Accra, Brazzaville, Beijing and Cairo6

One Category I Institute (to be determined)

X

X

X

Other Activities Internal audit also serves as focal point for the work of the Joint Inspection Unit and participates in a range of UNESCO initiatives, committees and working groups to improve contracting, knowledge management and ICT, investment oversight, SAP redesign and engages in inter-agency UN bodies on oversight.

3 Tentative 4 Joint exercise with Evaluation 5 Subject to funding 6 Subject to funding

204 EX/22 Annex II – page 2

EVALUATION PLAN 2018/2019

Evaluation Universe Evaluations to be Performed 2018 2019

Programmes Education:

ICT in Education x

Future of Education: Positioning UNESCO’s intellectual/normative function vs implementation in Education

x

Natural Sciences:

International Hydrological Programme (IHP) VIII x

Small Islands Developing States (SIDS) Action Plan x

International Geoscience and Geoparks programme (IGGP x

LINKS programme x

Social and Human Sciences: Operational Strategy on Youth x

History, memory and intercultural dialogue x

Culture:

UNESCO’s actions to protect culture in emergency situations (cultural and natural) x

1954 Hague Convention (and its two Protocols) on the Protection of Cultural Property in the Event of Armed Conflict x

2001 Underwater Cultural Heritage Convention x

Communication and Information:

Preventing Violent Extremism (e.g. through media and online coalitions) x

International Days (World Radio Day, World Press Freedom Day, Universal Day for Access to Information, Impunity Day, International Day for Persons with Disabilities)

x

External Relations and Cooperation:

Evaluation of UNESCO’s association with the celebration of Anniversaries x

Decentralized Bodies

UNESCO field presence in Asia x

UNESCO field presence Latin America & Caribbean x

Quality Assurance and Support to Decentralized Evaluation System

Advisory support to decentralized evaluations x x

Synthetic review and meta-evaluation of completed evaluations x x

204 EX/22 Annex III

ANNEX III

LIST OF ACRONYMS

ARB Advisory Review Boards ASPnet Associated Schools Programme Network BOS Business Operations Service BSE Basic Sciences and Engineering CEB Chief Executives Board for Coordination CM Correspondence Management EFA Education for All ERP Enterprise resource planning FUST UNESCO /Flanders Trust Fund in the field of Natural Sciences GIG UNRIAS Gender Interest Group IBE International Bureau for Education ICCOMOS International Council on Monuments and Sites ICCROM International Centre for the Study of the Preservation and Restoration of

Cultural Property ICTP International Centre for Theoretical Physics IIEP International Institute for Education Planning IOS Internal Oversight Service IRIS Integrated and Results-Oriented Information System IUCN International Union for Conservation of Nature JIU Joint Inspection Unit JOF Joint Operations Facility MGIEP Mahatma Ghandi Institute for Peace Education MOSS Minimum Operational Standards for Safety and Security OAC Oversight Advisory Committee PAB Personnel Advisory Boards PADTICE Projet d’Appui au Développement des TIC RP Regular Programme SDG Sustainable Development Goals SIC Statement on Internal Controls SMT Senior Management Team SRR Strategic Results Report TVET Technical and Vocational Education and Training TWAS The World Academy of Sciences UNDSS UN Department of Security and Safety UNEG United Nations Evaluation Group UNESCOMMUNITY online intranet website UNESTEAMS online intranet platform UNRIAS Internal Audit Services of the United Nations Organizations and

Multilateral Financial Institutions UNRIS United Nations Representatives of Investigations Services UN-SWAP UN System-wide Action Plan

Printed on recycled paper

![Holmes Anor v Commissioner of Police 2011 NTSC 108 2 Ano… · ... Ex parte Franks [1961] ... Re Refugee Review Tribunal; Ex parte Aala (2004) 204 CLR 82 ... The evidence in this](https://static.fdocuments.us/doc/165x107/5ab20f747f8b9aea528d1ab4/holmes-anor-v-commissioner-of-police-2011-ntsc-108-2-ano-ex-parte-franks-1961.jpg)