Tidal Audio Middle East Impressions Book Middle East and Africa

Upload

trinhthuanCategory

view

223download

6

Exciting new trends in Middle East

project financings

Simon Harvey

Partner, Pinsent Masons LLP

Overview

• PROJECT FINANCE MARKET

• PPP MARKET SPECIFICALLY

• COMMON PROJECT RELATED ISSUES

• ISSUES FOR CONTRACTOR‟S TAKING EQUITY

• COMMON DEBT ISSUES

• NEW CONTRACTOR FINANCING MODEL

• PIPELINE

SECTORS

Oil/Gas – 25% Industry/Metals

– 34%

Power & Water –

46%

Oil/Gas – 75%

Power & Water

– 15%

Industry/Metals

– 6%

Others

– 4%

Source: ACWA Power

Sectors

Oil/Gas – 83%

Power & Water – 12%

Oil/Gas –

53%

Power & Water

– 37%

Other – 0%

Source: ACWA Power

Sectors (cont.)

Real Estate

- 3%

Oil & Gas - 11%

Infrastructure - 1%

Source: MEED

Petrochemicals

- 30%

2013

Sectors (cont.)

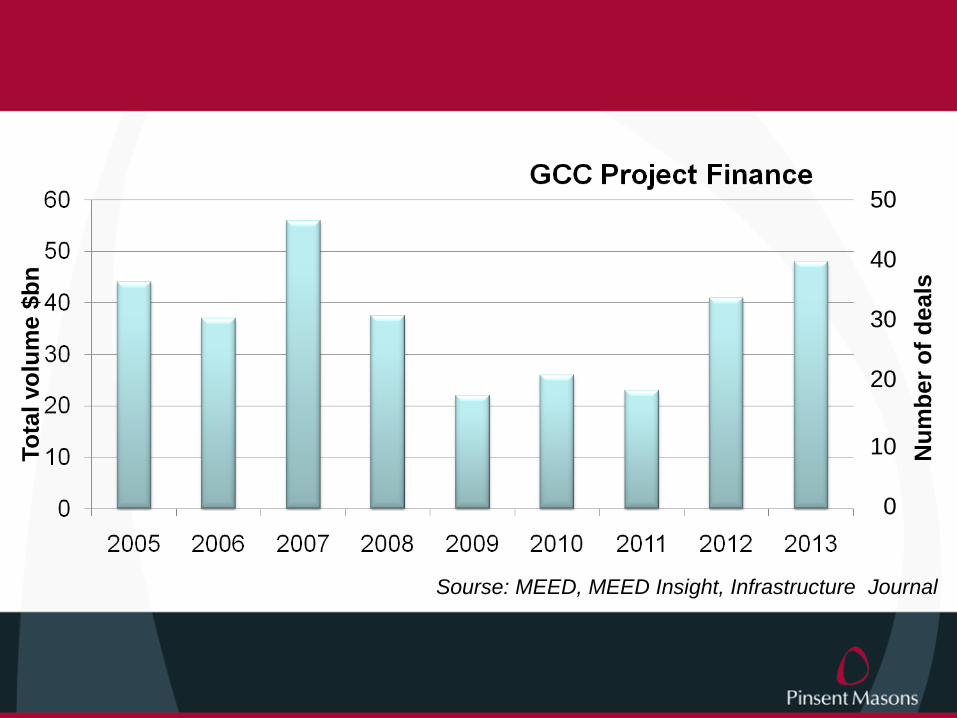

DEAL VOLUMES

50

10

20

30

40

0

To

tal vo

lum

e $

bn

Nu

mb

er

of

deals

Sourse: MEED, MEED Insight, Infrastructure Journal

FUNDERS: STRENGTH OF

REGIONAL BANKS

Financial Mix – Top 10 MENA Project

Finance ArrangersMENA Project Finance Mandate Arrangers

Rank Mandate arranger Total value ($m) Deals

1 HSBC 2,455 14

2 Standard Chartered 1,334 13

3 Public Investment Fund (KSA) 1,303 7

4 Bank of Tokyo-Mitsubishi UFJ 1,289 11

5 Qatar National Bank 1,162 3

6 National Bank of Abu Dhabi 1,132 9

7 National Bank of Kuwait 1,063 7

8Sumitomo Mitsui Banking

Corporation1,021 10

9 Samba Financial Group 955 7

10 Banque Saudi Fransi 947 5

Source: MEED

Lender Profile

PF Lenders Profile in ME (2004) PF Lenders profile in ME (2011)

European 44% European 18%

Regional 47% Regional 57%

Japanese 5% Japanese; Korean; Chinese 25%

Others 4%

Source: MEED

2013

• $48.7 billion worth of project finance deals closed in the

MENA region last year (Dealogic)

• Record breaking $12.7 billion Sadara Petrochemical

plant project financing

• Four of the top 15 global project finance deals

Top 10 MENA Project Finance deals in

2013Top 10 MENA project finance deals in 2013

Country Project financing ($m) Financial close

Sadara Chemical Saudi Arabia 12,731 Jun-14

Emirates Aluminium (Emal) phase 2 UAE 4,482 Mar-14

Zain Saudi Arabia Islamic Refinancing 2 Saudi Arabia 4,184 Jul-14

Kemya Saudi Elastomers expansion

murabaha financingSaudi Arabia 3,200 Jul-14

Shuweihat 2 IWPP (project bond

refinancing)UAE 2,294 Aug-14

Rabigh 2 IPP Saudi Arabia 1,997 Dec-14

Golar LNG Jordan 1,729 25-Jul

Al-Zour North IWPP Kuwait 1,560 12-Dec

Yanbu refinery expansion Saudi Arabia 1,399 05-May

Noor 1 concentrated solar power IPP Morocco 1,342 30-Jun

Source: Dealogic

Rank Borrower Name Project Name Country Value ($m) Notes

1Sadara Chemical

Company

Sadara

Petrochemical

Plant

Saudi

Arabia 12,731

The financing was raised

to fund the second phase

of the expansion of the

company‟s processing

plant

9Emirates Aluminim

Company – Emal

Emirates

Aluminium

(Emal) Phase 2

UAE 4,482

10

Mobile

Telecommunication

s Co Saudi Arabia

– Zain

Zain Saudi

Arabia Islamic

Refinancing 2

Saudi

Arabia 4,184

Shariah complaint re-

financing

13

Al Jubail

Petrochemical

Company (Kemya)

Kemya Saudi

Elastomer

Expansion

Murabaha

Saudi

Arabia 3,200

4 of the top 15 Project Finance deals

globally were in the MENA region in 2013

Source: Dealogic

PPP

PPP

GCC IPP/IWPP Project Financings

Source: HSBC Research

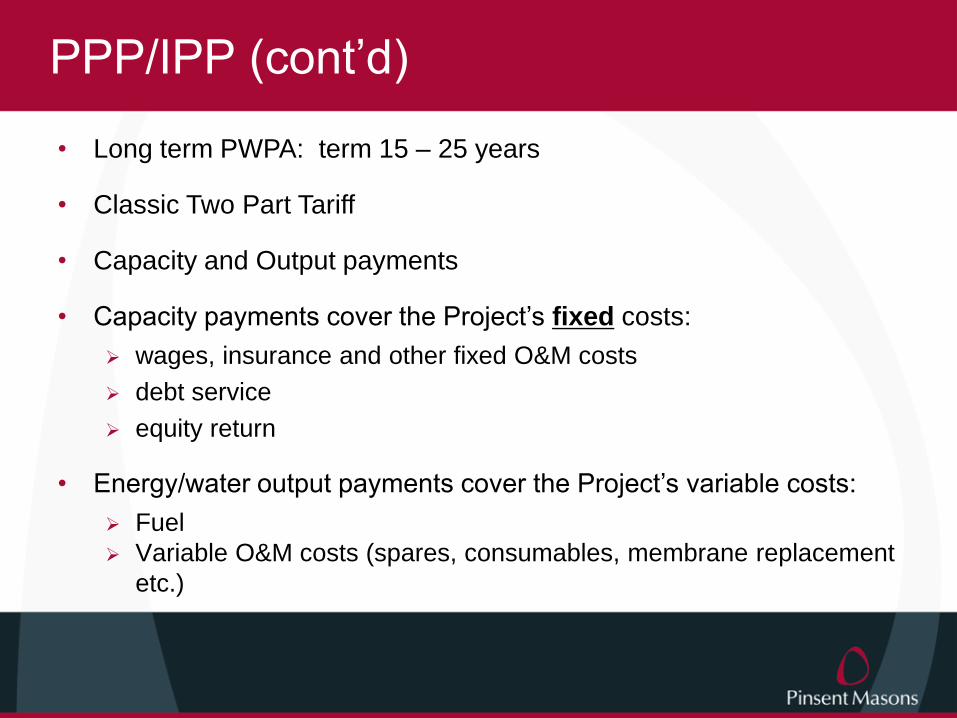

PPP/IPP (cont‟d)

• Gulf IWPP model: many projects over more than a decade based on

consistent demand growth and the development of domestic regimes to

attract foreign investment

• Enabling legislation and regulations enabling the participation of the

private sector in electricity and water production

• Most projects designed to produce both power and desalinated water

• Contract with a sovereign offtaker or stand-alone government entity

under take-or-pay arrangements for 100% power and water capacity

output

• Procuring entity releases a RfP attaching Project Agreements setting

forth its preferred risk allocation. Limited opportunity for bidding

consortia to raise departures

PPP/IPP (cont‟d)

• Long term PWPA: term 15 – 25 years

• Classic Two Part Tariff

• Capacity and Output payments

• Capacity payments cover the Project‟s fixed costs:

wages, insurance and other fixed O&M costs

debt service

equity return

• Energy/water output payments cover the Project‟s variable costs:

Fuel

Variable O&M costs (spares, consumables, membrane replacement

etc.)

PPP/IPP (cont‟d)

• Movement away from government guarantees

• Financed on a highly leveraged, limited recourse project finance

basis

• RFP will specify the level of committed funding at bid stage

• But even if less than fully underwritten commitments, Buyer not

likely to accept any reopening of the bid tariff or any other terms of

the project agreements where bidder is unable to achieve its

financing objectives

• Either BOOT projects or BOO projects with merchant tail

DEWA

Project Company

PPAMusatahaAgreement

Loan

Agreements

Turbine Manufacturer

Bidders DEWA

DEWA

O&M

O&MContractor

Supply Agreement

49% 51%

Shareholders'Agreement

IPP - structure

ECA Lenders

Com Lenders

Islamic Banks

EPC Contractor

EPC

Contract

Structure – other project financings

• Project financing for large industrial projects: refinery

and petrochemical projects and expansions, smelting,

manufacturing etc: taking advantage of available

feedstock, low electricity prices and cheap labor costs

• Often local / international JV; between NOC and

international chemicals company for example

• Supported by take-or-pay arrangements under offtake

agreements

• Significant need for ECA and multilateral commitments

COMMON PROJECT RELATED

ISSUES

Common project related issues

• Political risk and government support arrangements

• BOOT infrastructure termination payments

• Construction defects

• Dispute resolution

• Sovereign immunity

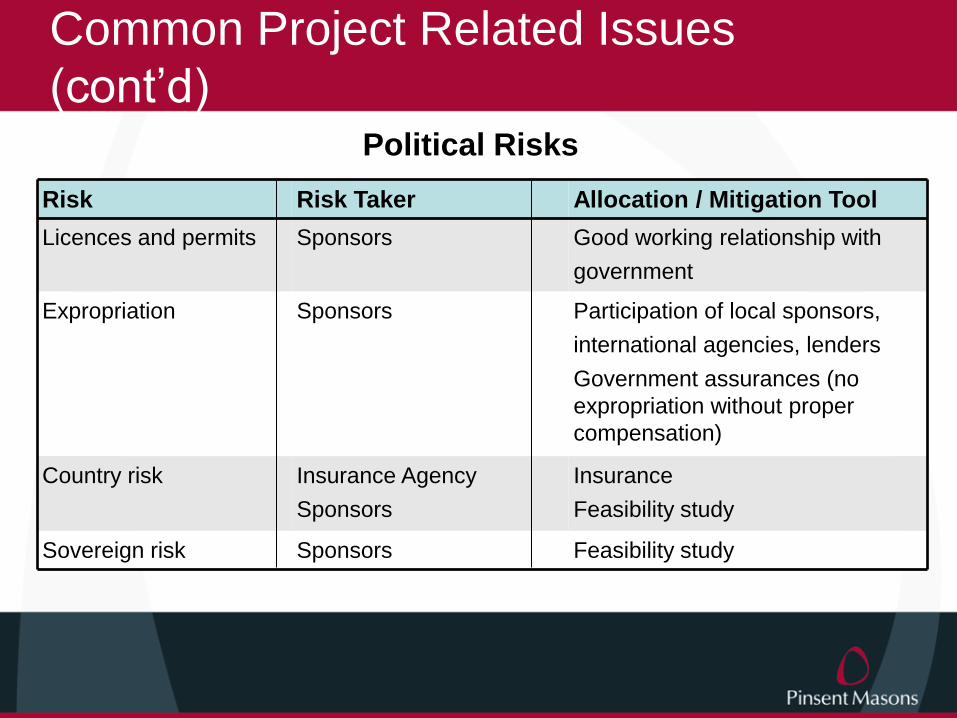

Common Project Related Issues

(cont‟d)

Risk Risk Taker Allocation / Mitigation Tool

Licences and permits Sponsors Good working relationship with

government

Expropriation Sponsors Participation of local sponsors,

international agencies, lenders

Government assurances (no

expropriation without proper

compensation)

Country risk Insurance Agency

Sponsors

Insurance

Feasibility study

Sovereign risk Sponsors Feasibility study

Political Risks

Common Project Related Issues

(cont‟d)

Government Support Arrangements

Government Guarantee

Poorly rated stand-alone entity

Implicit Government guarantee Sovereign State

with ACR

Least

Bankable

Most

Bankable

Payment into budget

allocation account

Explicit guarantee / credit support:

• of monthly obligation to pay the

purchase price?

• of compensation payable on

termination for Proj Co default?

• may fall away

Common Project Related Issues

(cont‟d)PPP Contract Termination

• Highly contentious area

• Key questions

which party can pull the trigger?

when do the lenders get paid out and how?

when does equity contribution/sponsor sub-debt get protected?

when does the Project Co recover lost revenues (i.e. profit)?

are contractors protected (problems under equivalent project

relief provisions)

• Different treatment for different projects, jurisdictions and

depending on cause of termination

Termination

by

Grounds Offtaker

obligation to

purchase (if

terminated by

Offtaker)

Offtaker

right to

purchase

Project

Company

right to

require

purchase

Purchase Price

guarantee by

Procurer Credit

Support

Termination

Costs paid

by Offtaker

Project

Company

Offtaker Event of

Default N/A No Yes Yes Yes

Project

Company

Prolonged EGAI

affecting Offtaker

and Offtaker does

not opt to continue

to pay

N/A N/A Yes Yes Yes

Offtaker Prolonged EFM

affecting Offtaker Yes No No Yes Yes

Offtaker Prolonged EGAI

affecting Offtaker Yes No No Yes Yes

Offtaker Prolonged EGAI

affecting Project

Company

Yes No No Yes Yes

Common Project Related Issues

(cont‟d)

Common project related issues (cont‟d)

Construction Defects

• Architect and construction contractor jointly liable for at least 10 years to

compensate the employer for any total or partial collapse of the structure

Dispute Resolution

• Choice of foreign governing law

• Recognition and enforcement of foreign judgments

• New York Convention

• Local arbitral bodies

Sovereign Immunity

• Immunity from suit

• Immunity from execution and attachment

Issues for contractors taking equity

Jurisdiction Ownership requirement Comments

UAELocal shareholder (an affiliate of the Buyer)

owns 60%

Under SHA international developers exercise day-

to-day control

75% majority required for certain key decisions

Saudi Arabia 50% government shareholdingEoD and put and call linked to termination of the

PWPA for shareholder default

Oman IPO at least 35% of shares on the local bourse

If not disposed of within the requisite period, EHC

may mop up the unsold balance at a pre-agreed

option price.

KuwaitIPO 50% to general public via IPO and 10% to

government

Jordan 100% foreign ownership

• Foreign ownership restrictions in many jurisdictions

• Equity injection arrangements:

pro rata with debt

Back-ended – injected at earlier of completion and occurrence of event of default.

Credit enhancement, e.g. backed by LC

• Guarantees / Equity Support

DEBT ISSUES

Debt Issues

• Multi-source financings are usual: mixture of international, regional,

Islamic and domestic banks and ECA / multilateral finance. Some bond

refinancings (Dolphin, Shuweihat 2)

• ECAs are a key feature. Covered or direct loans. Lending amounts

tied to host country procurement; vendor relationships are more

important than sponsor relationships

• 70:30 – 80:20 debt to equity ratio

• Regional variance in Islamic structures but intercreditor arrangements

between conventional and Islamic funders largely settled

• Common project financing techniques are used in the Gulf:

control of cash through project accounts and reserve accounts

payment waterfall

project ratios

Collateral

• Onshore security: take best security possible, no universal corporate charge

and not over future acquired assets, so take specific forms of security over

various project assets, plus share pledges

• Offshore security: fairly standard for PF including security over offshore

accounts, charge over English law project agreements (and any related

bonding and parent company guarantees), assignment of insurance

proceeds and share pledges/mortgages over any foreign companies in the

group structure

• Commonly enter into direct agreements (cure rights/rights to step in and

substitution rights)

• No “companies house”, limited registration systems

• Enforcement by way of a court sanctioned auction. Commonly

acknowledged questions around enforceability and bankruptcy laws

• Bankable but defensive

NEW CONTRACTOR FINANCING

MODEL

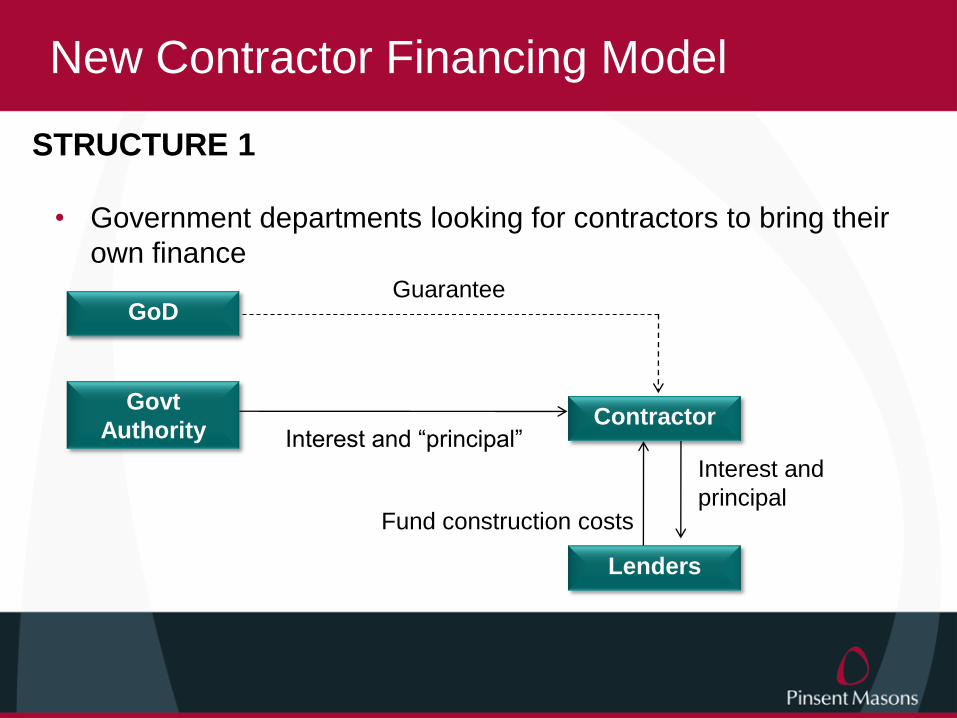

New Contractor Financing Model

• Government departments looking for contractors to bring their

own finance

GoD

Govt

AuthorityContractor

Interest and “principal”

Fund construction costs

Interest and

principal

Guarantee

Lenders

STRUCTURE 1

New Contractor Financing Model

(cont‟d)

Developer

Consultant

Team

Contractor

X Y Z

Works Contracts

Lender Covered loan

ECA

Support Agreement Certification as to local

content

Disbursement

STRUCTURE 2

Structure 1: Dubai Water Canal

Example

Structure 1 – key terms

• Finance Model 1

[84] Month Finance period with a Guarantee from Department of Finance

• Finance Model 3

[84] Month Finance Period without a Guarantee from Department of Finance

• Finance Model 5

Normal Contract: payment of contract price within 60 days of certification

Structure 1 – key terms cont‟d

• 10% Advance Payment (of Contract Price Less Finance Costs)

• Second 10% payment instalment after the Contractor completes 20% of the

Work. Advance Payment is deemed to be satisfied at that point, bond falls

away

• After that no payment on account of the balance of the Contract Price (the

“principal” amount) until the stipulated completion date

• However interest shall accrue on the certified but unpaid balance of the Contract

Price during the construction period and shall be paid monthly in arrears up to

the completion date

• Thereafter, payment monthly instalments of principal+ interest from the

completion date for a period of [84] months

• Principal to be paid/repaid in equal monthly installments over that period

• Contractor to bid the margin it is willing to accept during the interest period

(over EIBOR or LIBOR at its election)

Structure 1 – key terms cont‟d

• RTA may prepay all or part of the outstanding principal without

penalty

• Additional Works arising from a Change subject to the same terms

unless either party objects

• No retention (10% is standard in the Middle East)

Structure 2: Issues

• Amount to be funded by developer?

• Costs overruns

• Is the contractor the head contractor or a conduit?

• Avoid being the meat in the sandwich

Developer

Consultant

Team

Contractor

X Y Z

Works Contracts

Lender Covered loan

ECA

Support Agreement Certification as to local

content

Disbursement

PROJECT PIPELINE

Pipeline – 2014 project finance outlook

• Steady rather than record year

• Deals expected to come to the banking market from

nearly all of the 6 GCC states

• Increasing appetite for PPP

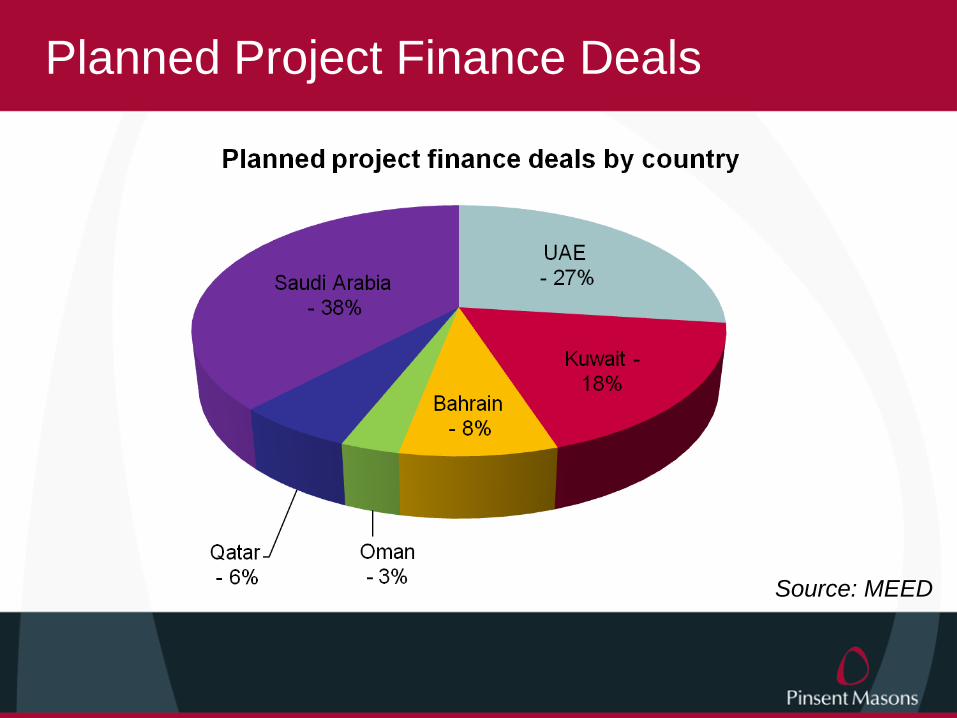

Planned Project Finance Deals

Source: MEED

Questions?

THANK YOU

Combining the experience, resources and international reach

of McGrigors and Pinsent Masons

Pinsent Masons LLP is a limited liability partnership registered in England & Wales (registered number: OC333653) authorised and regulated by

the Solicitors Regulation Authority, and by the appropriate regulatory body in the other jurisdictions in which it operates. The word „partner‟, used in

relation to the LLP, refers to a member of the LLP or an employee or consultant of the LLP or any affiliated firm who is a lawyer with equivalent

standing and qualifications. A list of the members of the LLP, and of those non-members who are designated as partners, is displayed at the LLP‟s

registered office: 30 Crown Place, London EC2A 4ES, United Kingdom. We use „Pinsent Masons‟ to refer to Pinsent Masons LLP and affiliated

entities that practise under the name „Pinsent Masons‟ or a name that incorporates those words. Reference to „Pinsent Masons‟ is to Pinsent

Masons LLP and/or one or more of those affiliated entities as the context requires. © Pinsent Masons LLP 2012

For a full list of our locations around the globe please visit our websites:

www.pinsentmasons.com www.Out-Law.com