Exchange rate and interest parity - WZ UW · Exchange rate and interest parity ... International...

21

1 Exchange rate and interest parity Jan J. Michalek Exchange rate Exchange rate: the price of one currency expressed in another currency Definition: how many units of domestic currency are needed to buy one unit of foreign currency: e.g. 3,9 PLN/$ Changes in exchange rates: Fixed exchange rate: devaluation and revaluation Flexible exchange rates: depreciation and appreciation. JJ Michalek

Transcript of Exchange rate and interest parity - WZ UW · Exchange rate and interest parity ... International...

1

Exchange rate

and interest parity

Jan J. Michalek

Exchange rate

Exchange rate: the price of one currency expressed in another currency

Definition: how many units of domestic currency are needed to buy one unit of foreign currency: e.g. 3,9PLN/$

Changes in exchange rates:

Fixed exchange rate: devaluation and revaluation

Flexible exchange rates: depreciation and appreciation.

JJ Michalek

2

Echange rate changes:

Exchange rate

regime

Flexible Stable

Increase of

exchange rate

Depreciation Devaluation

Decrease of

exchange rate

Appreciation Revaluation

JJ Michalek

Two types of changes in exchange rates:

Depreciation of home country’s currency

A rise in the home currency prices of a foreign currency

It makes home goods cheaper for foreigners and foreign

goods more expensive for domestic residents.

Appreciation of home country’s currency

A fall in the home price of a foreign currency

It makes home goods more expensive for foreigners and

foreign goods cheaper for domestic residents.

Exchange Rates and

International Transactions

3

Major exchange regimes and their

characteristics

JJ Michalek

Exchange regimes in Poland

4

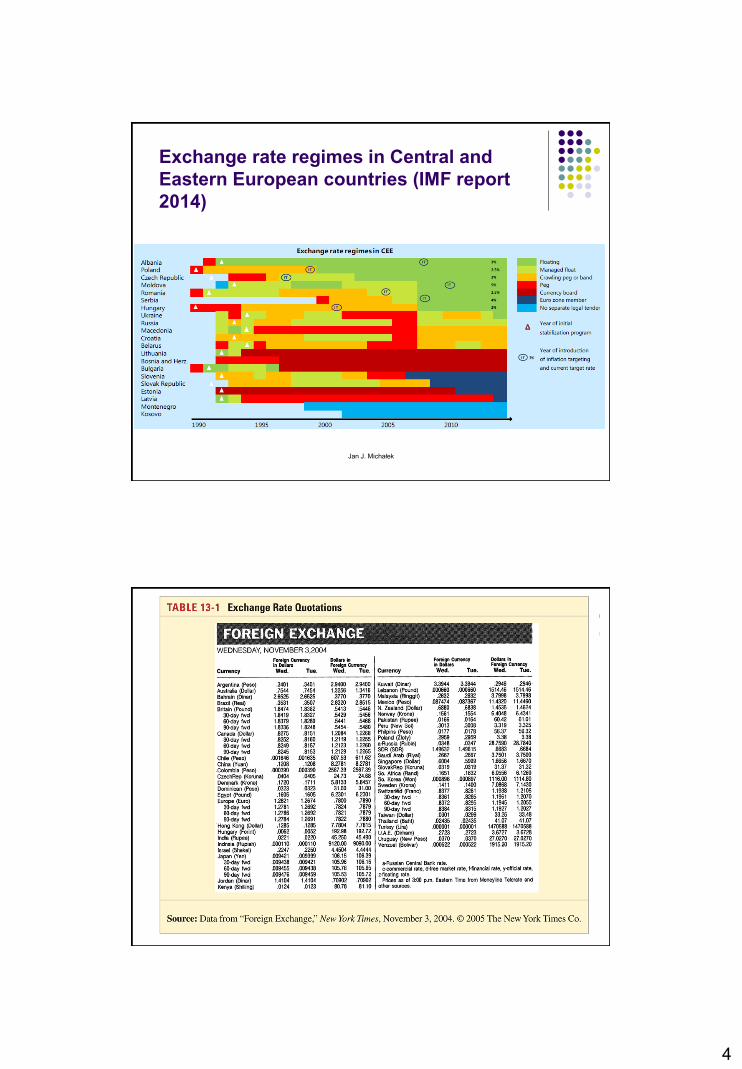

Exchange rate regimes in Central and

Eastern European countries (IMF report

2014)

Jan J. Michałek

5

Domestic and Foreign Prices

If we know the exchange rate between two

countries’ currencies, we can compute the price of

one country’s exports in terms of the other

country’s money.

Example: The dollar price of a £50 sweater with a

dollar exchange rate of $1.50 per pound is (1.50 $/£) x

(£50) = $75.

Exchange Rates and

International Transactions

Exchange rate: major world

actors

Size of the market:

For example: 1999:$1,7 trillion per day: $637 billion in London, $350 in New York, $150 billion in Tokyo.

Major actors and foreign exchange markets:

Commercial banks (interbank trading: retail operations less than $1 million, wholesale: above $1 million: more favorable rates: 90 percent of all foreign exchange rate transactions)

Multinational corporations;

Non bank financial institutions;

Central banks

Foreign exchange brokers.

JJ Michalek

6

Foreign exchange arbitrage

When banks or economic agents seek to earn benefit from discrepancies among exchange

rates prevailing simultaneously in different markets.

Example: the Exchange rate of dollar to pound sterling ES/Ł equals:

00,2NYE 20,2LE

With 100$

We can buy 50Ł in NY in exchange for $100

And sell 50Ł In London for: 50*2,20= $110

Immediate profit of 10 $ or 10% (very profitable)

Many transactions of this sort are done

Price of Ł raises (increased demand) in NY e.g. to 2,09

Price of Ł decreases (increased supply) In London e.g. to 2,11

A very small difference In Exchange rates between different foreign exchange markets

JJ Michalek

Spot Rates and Forward Rates

Spot rates are exchange rates for currency exchanges “on the spot”, or when trading is executed in the present.

Forward rates are exchange rates for currency exchanges that will occur at a future (“forward”) date.

forward dates are typically 30, 90, 180 or 360 days in the future.

rates are negotiated between individual institutions in the present, but the exchange occurs in the future.

7

Spot and Forward Rates

Hedging: covering against the risk of

exchange rate fluctuations:

If we have to pay 1000 € in three months and we have 4000 PLN & E=4,00PLN/€

We can exchange today: 4000 PLN-> 1000€ (so called balanced or closed position)

If zloty appreciates (e.g.. E=3,9) ---> we gain 100 PLN (in one month it would be possible to buy 1000 € in exchange for 3900 PLN)

If zloty depreciates (e.g. E=4,1) --> we loose 100 PLN

Another option: to keep 4000 PLN as a bank deposit and exchange PLN against Euro after 3 months. Risk of depreciation short position (short of Euro).

JJ Michalek

8

Speculation: the opposite of hedging

Making transactions on spot foreign exchange market;

Deliberately willing to profit from exchange rate changes;

- Long position: buying deposit denominated in foreign currency in the hope that currency price will raise (depreciation of domestic currency)

- Short position: promising to sell foreign currency deposit in the future (in the hope that its price will fall: expectation of appreciation of the domestic currency).

JJ Michalek

Figure 13-2: Interest Rates on Dollar and Deutschemark Deposits,

1975-1998

The Demand for

Foreign Currency Assets

9

Exchange rate equilibrium under flexible exchange

rate system

S€: supply of foreign deposits (denominated in €) expressed in PLN

D€: demand for foreign deposits (depending on real rate of return)

EPLN/€=3.8

EPLN/€=4.2

EPLN/€=4.0

EPLN/€

S€

D€

Foreign exchange in €

),,,(

))()()((

* fe EERRDD

JJ Michalek

Equilibrium under stable exchange rate regime:

Exchange rate is too high

If Exchange rate is fixed (e.g. EPLN/€=4.20) --> agents are not buying sufficient amount of €-->

excess supply of €--> BOP surplus---> Central Bank purchases € in exchange for PLN (foreign

exchange reserves increase) --> domestic money supply raises.

Intervention of CB 0

EPLN/€=4.2

EPLN/€ S€

D€

Foreign deposits In €

BOP=0

BOP>0

JJ Michalek

10

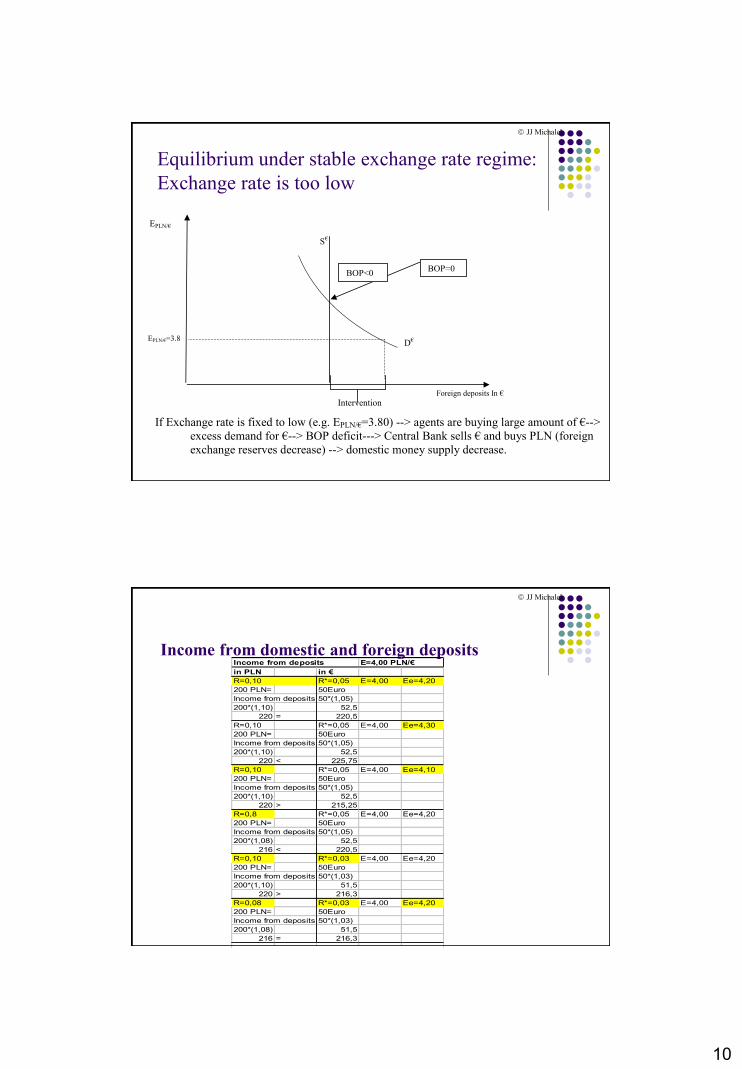

Equilibrium under stable exchange rate regime:

Exchange rate is too low

If Exchange rate is fixed to low (e.g. EPLN/€=3.80) --> agents are buying large amount of €-->

excess demand for €--> BOP deficit---> Central Bank sells € and buys PLN (foreign

exchange reserves decrease) --> domestic money supply decrease.

Intervention

EPLN/€=3.8

EPLN/€

S€

D€

Foreign deposits In €

BOP=0 BOP<0

JJ Michalek

Income from domestic and foreign deposits Income from deposits E=4,00 PLN/€

in PLN in €

R=0,10 R*=0,05 E=4,00 Ee=4,20

200 PLN= 50Euro

Income from deposits 50*(1,05)

200*(1,10) 52,5

220 = 220,5

R=0,10 R*=0,05 E=4,00 Ee=4,30

200 PLN= 50Euro

Income from deposits 50*(1,05)

200*(1,10) 52,5

220 < 225,75

R=0,10 R*=0,05 E=4,00 Ee=4,10

200 PLN= 50Euro

Income from deposits 50*(1,05)

200*(1,10) 52,5

220 > 215,25

R=0,8 R*=0,05 E=4,00 Ee=4,20

200 PLN= 50Euro

Income from deposits 50*(1,05)

200*(1,08) 52,5

216 < 220,5

R=0,10 R*=0,03 E=4,00 Ee=4,20

200 PLN= 50Euro

Income from deposits 50*(1,03)

200*(1,10) 51,5

220 > 216,3

R=0,08 R*=0,03 E=4,00 Ee=4,20

200 PLN= 50Euro

Income from deposits 50*(1,03)

200*(1,08) 51,5

216 = 216,3

JJ Michalek

11

Expected income from foreign

deposits

Uncovered interest parity:

The foreign exchange market is in equilibrium when deposits of all currencies

offer the same expected rate of return

The expected rate of return from foreign deposits equals:

111 *

*

E

ER

E

ERE ee

where:

E: spot exchange rate, and Ee expected exchange rate after period t (1 year)

While domestic rate of return equals R .

JJ Michalek

Uncovered interest parity

Precisely calculated income in foreign exchange (after adding and subtracting R*) can be written as:

E

EERR

E

EER

E

ER

E

EERR

E

ER

E

E eEeeee******* 11

And the product: EEER e * is close to 0 for small R*

and (Ee-E)/E is the expected rate of depreciation

So a proxy for foreign deposits expected rate of return can be written as:

E

EERe *

So a proxy for equality between domestic and foreign deposits can be written as:

which is uncovered interest parity:

E

EERR

e *

JJ Michalek

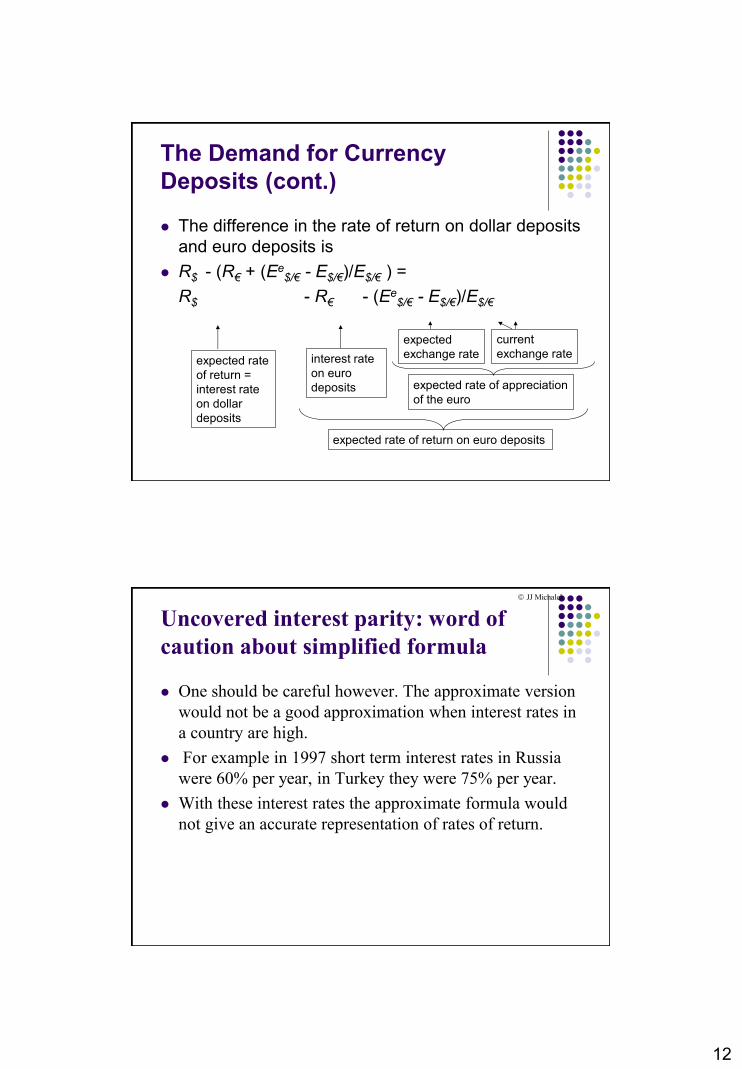

12

The Demand for Currency

Deposits (cont.)

The difference in the rate of return on dollar deposits

and euro deposits is

R$ - (R€ + (Ee$/€ - E$/€)/E$/€ ) =

R$ - R€ - (Ee$/€ - E$/€)/E$/€

expected rate

of return =

interest rate

on dollar

deposits

interest rate

on euro

deposits

expected rate of return on euro deposits

expected

exchange rate

current

exchange rate

expected rate of appreciation

of the euro

Uncovered interest parity: word of

caution about simplified formula

One should be careful however. The approximate version

would not be a good approximation when interest rates in

a country are high.

For example in 1997 short term interest rates in Russia

were 60% per year, in Turkey they were 75% per year.

With these interest rates the approximate formula would

not give an accurate representation of rates of return.

JJ Michalek

13

Rule for efficient investment The rule for efficient investment is:

==> the interest party holds

Example:

R= 15%; R*=5%; EPLN/E =2.00 a EePLN/E =2.21 -->

0.15 - 0.05 -(2.21-2.0)/2.0=0.1-0.105<0 ==> invest abroad.

And if Ee =2.20 ==>

0.15 - 0.05 -(2.20-2.0)/2.0=0.1-0.1=0 ==> interest party holds (the same

rate of return)

eatinvestE

EERR

E

hom0*

abroadinvestE

EERR

E

0*

0*

E

EERR

E

JJ Michalek

Uncovered interest parity: simple examples

Income from deposits E=4,00 PLN/€ R-R*-(Ee-E)/E=

in PLN in €

R=0,10 R*=0,05 E=4,00 Ee=4,20 0

200 PLN= 50Euro

Income from deposits 50*(1,05)

200*(1,10) 52,5

220 = 220,5

R=0,10 R*=0,05 E=4,00 Ee=4,30 -0,025

200 PLN= 50Euro

Income from deposits 50*(1,05)

200*(1,10) 52,5

220 < 225,75

R=0,10 R*=0,05 E=4,00 Ee=4,10 0,025

200 PLN= 50Euro

Income from deposits 50*(1,05)

200*(1,10) 52,5

220 > 215,25

R=0,8 R*=0,05 E=4,00 Ee=4,20 -0,02

200 PLN= 50Euro

Income from deposits 50*(1,05)

200*(1,08) 52,5

216 < 220,5

R=0,10 R*=0,03 E=4,00 Ee=4,20 0,02

200 PLN= 50Euro

Income from deposits 50*(1,03)

200*(1,10) 51,5

220 > 216,3

R=0,08 R*=0,03 E=4,00 Ee=4,20 0

200 PLN= 50Euro

Income from deposits 50*(1,03)

200*(1,08) 51,5

216 = 216,3

JJ Michalek

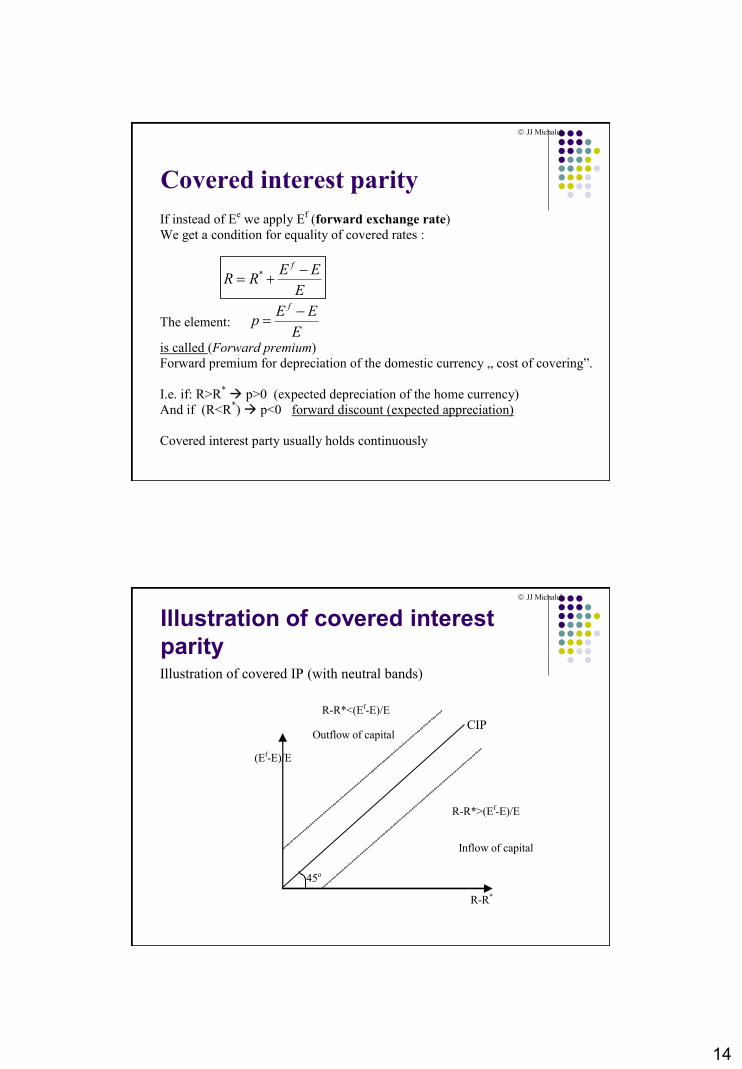

14

Covered interest parity

If instead of Ee we apply E

f (forward exchange rate)

We get a condition for equality of covered rates :

The element: E

EEp

f

is called (Forward premium)

Forward premium for depreciation of the domestic currency „ cost of covering”.

I.e. if: R>R* p>0 (expected depreciation of the home currency)

And if (R<R*) p<0 forward discount (expected appreciation)

Covered interest party usually holds continuously

E

EERR

f *

JJ Michalek

Illustration of covered interest

parity Illustration of covered IP (with neutral bands)

R-R*<(Ef-E)/E

45o

Inflow of capital

Outflow of capital CIP

R-R*

(Ef-E)/E

R-R*>(Ef-E)/E

JJ Michalek

15

The Market for Foreign Exchange

Depreciation of the domestic currency today lowers the expected

return on deposits in foreign currency.

A current depreciation of domestic currency will raise the initial

cost of investing in foreign currency, thereby lowering the

expected return in foreign currency.

Appreciation of the domestic currency today raises the expected

return of deposits in foreign currency.

A current appreciation of the domestic currency will lower the

initial cost of investing in foreign currency, thereby raising the

expected return in foreign currency.

Determination of the Equilibrium

Exchange Rate

No one is willing to

hold euro deposits

No one is willing to

hold dollar deposits

16

Flexible exchange rate: impact of

domestic interest rate increase

Increase of domestic interest rate appreciation of the exchange rate

E2PLN/€

Income from

domestic deposits R

R2PL 0

E1PLN/€

EPLN/€

R1PL

Income from foreign

deposits (R*)

JJ Michalek

Flexible exrate: impact of foreign interest rate

increase (or expected exchange rate)

1. Increase of foreign interest rate --> increase In income from foreign deposits (income curve shifts

up) --> demand for € raises --> depreciation of the exchange rate;

2. Increase of expected exchange rate (EePLN/€) --> expected depreciation --> increase of expected

income from deposits denominated in € --> demand for € raises --> increase of exchange rate -->

i.e. depreciation.

Income from domestic

deposits in PLN RPL

E2PLN/€

E1PLN/€

EPLN/€

Income from deposits

denominated In €

JJ Michalek

17

Money market equilibrium

MS/P=L(R,Y)

3

2

1

Q3 Q2 Ms/P=Q

1

R3

R2

R1

Real money

holdings

Real aggregated money

demand: L(R,Y)

R Real money

supply

JJ Michalek

Money and exchange rate: short run

equilibrium

1'

1 MS

1

E1

R1

L(RPL,YPL)

MSPL/PPL

Expected Euro return

Return from Polish deposits

(PLN)

EPLN/€

Real Polish

Money supply

R

Domestic

Money

market

Foreign exchange

rate market

JJ Michalek

18

Money and exchange rate: increase of

domestic money supply

R2

2'

2

E2

MS2

Present Euro return

1'

1 MS

1

E1

R1

L(RPL,YPL)

MSPL/PPL

Returun from Polish deposits

(PLN)

EPLN/€

Polish real

Money supply

R

Domestic

Money

market

Foreign exchange

market

JJ Michalek

Money and exchange rate

expectations: overshooting

R2

E2

3'

2'

MS2 2

Present euro return

1'

1 MS

1

E1

R1

L(RPL,YPL)

MSPL/PPL

New expected Euro

reurn

Income from domestic deposits

(PLN)

EPLN/€

Real Polish

Money supply

R

Domestic

money

market

Foreign Exchange

market

JJ Michalek

19

Exchange Rate Overshooting

The exchange rate is said to overshoot when its immediate response to a change is greater than its long run response.

We assume that changes in the money supply have immediate effects on interest rates and exchange rates.

We assume that people change their expectations about inflation immediately after a change in the money supply.

Overshooting helps explain why exchange rates are so volatile.

Overshooting occurs in the model because prices do not adjust quickly, but expectations about prices do.

Long Run and Short Run

(cont.)

In the long run, there is a direct relationship between

the inflation rate and changes in the money supply.

Ms = P x L(R,Y)

P = Ms/L(R,Y)

P/P = Ms/Ms - L/L

The inflation rate equals growth rate in money supply

minus the growth rate for money demand.

20

Money and exchange rate

expectations: long run adaptation

MS2

4' 3'

2'

R2

E3

E2

2

Previous income from

Euro deposits

1'

1 MS

1

E1

R1

L(RPL,YPL)

MSPL/PPL

New expected income

from Euro deposits

Income from domestic deposits

(PLN)

EPLN/euro

Real Polish

money supply

R

Domestic

Money

market

Foreign

exchange

market

JJ Michalek

21

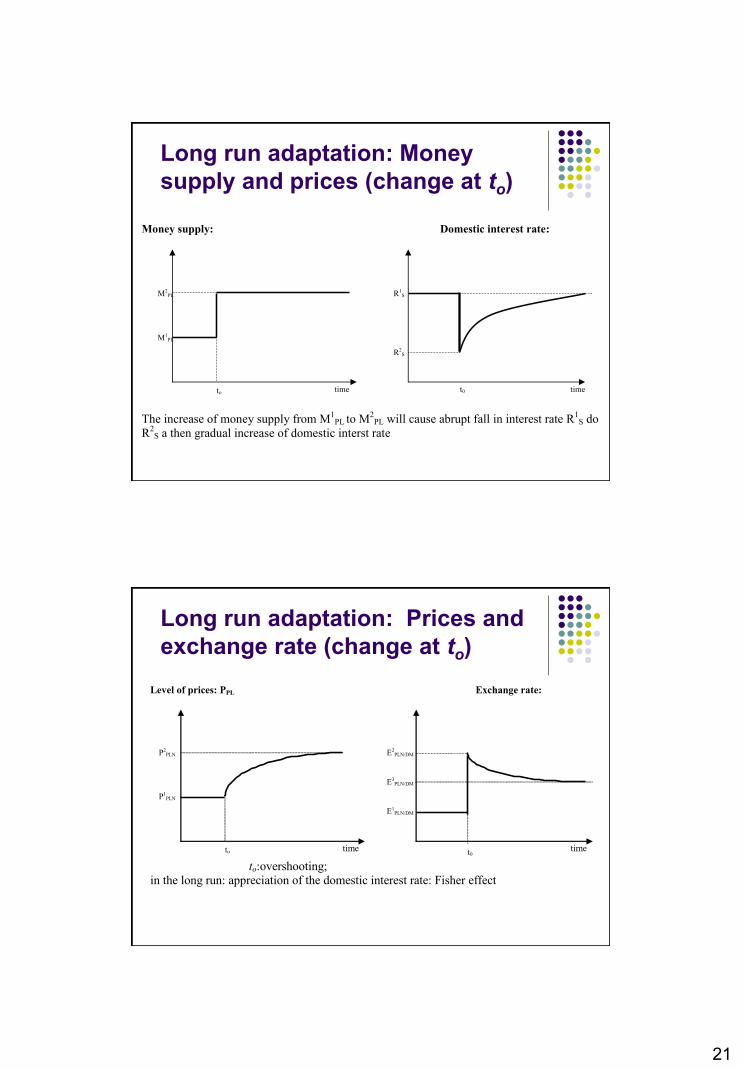

Long run adaptation: Money

supply and prices (change at to)

Money supply: Domestic interest rate:

The increase of money supply from M1

PL to M2

PL will cause abrupt fall in interest rate R1

S do

R2

S a then gradual increase of domestic interst rate

R2S

R1S

time time

M2PL

M1PL

t0 to

Long run adaptation: Prices and

exchange rate (change at to)

Level of prices: PPL Exchange rate:

to:overshooting; in the long run: appreciation of the domestic interest rate: Fisher effect

time time

E3PLN/DM

E2PLN/DM

E1PLN/DM

P2PLN

P1PLN

t0 to

![[IMF Staff Papers, Sarno] Purchasing Power Parity and the Real Exchange Rate](https://static.fdocuments.us/doc/165x107/577d35801a28ab3a6b909c8d/imf-staff-papers-sarno-purchasing-power-parity-and-the-real-exchange-rate.jpg)