Excellence in Oil and Gas 2009 Narrabri Coal Seam Gas Project

18

Excellence in Oil and Gas 2009 Narrabri Coal Seam Gas Project 6 April 2009 David Casey, Managing Director

Transcript of Excellence in Oil and Gas 2009 Narrabri Coal Seam Gas Project

Excellence in Oil and Gas 2009Narrabri Coal Seam Gas Project

6 April 2009

David Casey, Managing Director

Company Overview

Excellence in Oil and Gas 2009Narrabri Coal Seam Gas Project Update

3

Company Overview - Delivering on Predictions

May 2008 Expectations 2008 to 2009 April 2009

Share Price $0.685 - $0.810

Market Cap. $520m - $692m

Acreage CSG focus Identify farmin opportunities Largest operated CSG acreage

2P Gas Reserves 185 PJ 1,300 PJ by December 2009 Upgrade to 336 PJ (Sept ‘08)

Work Programme NSW’s largest ever programme underway

Undertake seismic, corehole and pilot production work

Seismic, 7 x coreholes and first multi-lateral complete

Market

Commitment to expand Wilga Park P.S. Staged expansion to 40 MW Part 3A Approval received and

expansion underway

MoU’s for 1,300 PJ Continue phased approach HoA with APA Group for Pipeline access (Jul ‘08)

ESG’s vision is to be NSW’s leading supplier of natural gas

4

Company Overview - Highlights of last 12 months

Operating Highlights Operated Acreage Comparison

• ASX (‘ESG’) and OTCQX (‘ESGLY’) listed

• Included in ASX200

• Largest operated CSG acreage position

• Reserves Upgrade Programme early successes:

Dewhurst coreholes confirm easterly extension of thick Bohena coal seam

Edgeroi-1 wildcat corehole confirms potential of northern portion of PEL 238

First multi-lateral pilot freeflows 3,400 bwpd

Contingent resources independently certified

• Market development progressing

HoA with APA Group to access NSW markets

ESG

Origin

QGC-BG

Santos

Arrow

AGL

Pure Energy

Other

Location

Operator

5

Company Overview - ESG Acreage

Key Assets - Substantive CSG Position with Focus on Narrabri CSG Project

PEL 2389,095 km2

(Narrabri CSG Project)ESG 65%

PEL’s 433 & 43415,399 km2

ESG 65%

Arckaringa Basin27,922 km2

25% to 50% CSG farm-in

Orion Petroleum(ESG holding 23%)

Pursuing conventional opportunities

PELs 6, 427, 42818,200 km2

40% - 50% - 75% farm-in

Location

NSW

SA

Victoria

Wilga Park Power StationExpandable to 40MW

ESG 65%

70,616 km2 operated, including 42,694 km2 in NSW. Net ESG interest 31,400 to 39,671km2.

6

Company Overview - Recent CSG Industry Transactions

Source: ESG, company announcementsKey: QGC: Queensland Gas Company, Sunshine: Sunshine Gas, Gloucester: Gloucester Basin Project, SGL: Sydney Gas LimitedNotes:1 BG Group acquired a 10% equity stake in QGC (plus 20% stake in QGC’s assets) in February 2008 and acquired the remaining 90% stake in October 20082 Based on total value ascribed by AGL to SGL, taking into account options and cash. AGL allocated $115mm of the consideration to the Hunter Valley gas project,which has no certified reserves, and $49mm for the Camden assets (taking into account options and cash) which had 2P and 3P reserves of 41PJ and 54PJ respectively, which on this basis implies $1.19/GJ and $0.90/GJ for SGL’s certified 2P and 3P reserves respectively

3 Based on BG Group’s offer of 27 February 2009, and Pure Energy’s publicly stated reserves as at the same date

Transaction metrics (A$/GJ)

A$/GJ

0.67

1.65

0.77 0.74

1.88

0.77 1.00

3.03

0.40

1.94

3.99

2.111.991.74

2.72

1.57

0.00

1.00

2.00

3.00

4.00

5.00

6.00

BG Group/QGC

PETRONAS/Santos

Shell/ ArrowEnergy

QGC/Sunshine

Conoco/ OriginEnergy

BG Group/QGC

AGL Energy/Gloucester

AGL Energy/SGL

BG Group/Pure Energy

A$/GJ 3P A$/GJ 2P

A$1.21/GJ 3P (mean) A$2.78/GJ 2P (mean)

1 1

February 2008 February 2009

32

4.91

4.02

Narrabri CSG Project

Excellence in Oil and Gas 2009Narrabri Coal Seam Gas Project Update

8

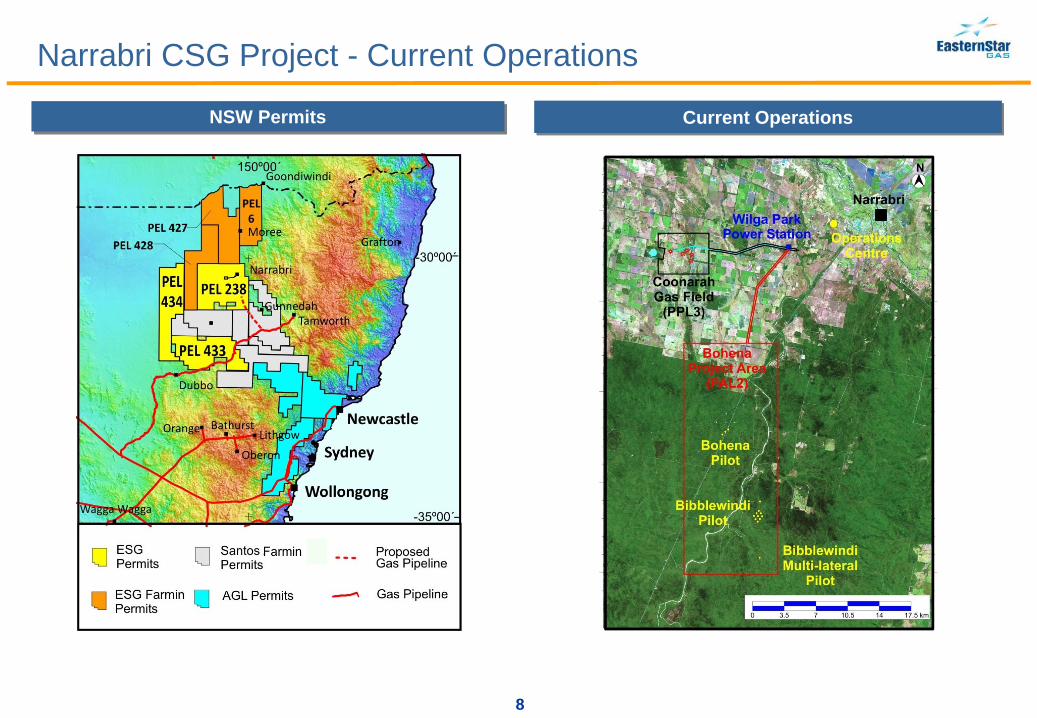

Narrabri CSG Project - Current Operations

NSW Permits Current Operations

9

Outstanding results so far from 2008/09 Reserves Upgrade Program

Narrabri CSG Project- Gas Reserves Upgrade Program

Dewhurst Coreholes:already contributing to certified reserves

Total Coal Thickness: 33.5m to 42.5m

Bohena Seam Thickness: 16.2m to 21.7m

Bohena Coal Permeabilities: up to ~100 mD

Edgeroi Corehole Results

Confirmed permit-wide development of thick, gas saturated coal

Unique Architecture of Bohena Coal

Typical Coal

BohenaCoal

Programme Potential in excess of 5,000 PJ Recoverable

10

Narrabri CSG Project - Multi-lateral Wells

Schramm TXD Drilling Rig on site at Narrabri

11

Narrabri CSG Project - Multi-lateral Wells

Animation of Multi-lateral drilling process

12

Narrabri CSG Project - Multi-lateral Wells

Multiple lateral wells, drilled perpendicular to the natural fracturing system

Connectivity with the coal and, in turn, gas production are maximised

BBD-18H BBD-12 BBD-14 BBD-13

~1,000 m

~1,000 m

Realising Project Potential

Excellence in Oil and Gas 2009Narrabri Coal Seam Gas Project Update

14

Realising Project Potential - Reserves and Resources

Independently Certified Reserves and Contingent Resources are Already Material

PEL 238 Certified Gas Reserves

1P 2P 3P

21 PJ 336 PJ 1,300 PJ

PEL 238 Certified Contingent Resources

1C 2C 3C

1,195 PJ 3,053 PJ 6,128 PJ

0

2000

4000

6000

8000

Narrabri CSG Project 20% NSW Gas Market 20 years

1,500 MW (60% capacity, 20 years)

3.5 Mtpa LNG (20 years)

PJ

Gas Requirement NSW Annual Gas Use Contingent Resource 3P Reserves

15

Realising Project Potential - Development Stages

Stage 1: Wilga Park Expansion (underway) and Stage 2: Early Access to NSW Gas Market

Longford

SydneyNewcastle

Tamworth

Brisbane

Gladstone

Townsville

Mt Isa Moranbah

WallumbillaBallera

Narrabri

Melbourne

FlowlineExtension

ExistingPipelines

GasProcessing

Lateral toAPA System

16

Realising Project Potential - Development Stages

Stage 3: Major Domestic Greenfield Opportunities and Stage 4: ‘Global’ Opportunities

Longford

Sydney

Brisbane

Gladstone

Townsville

Mt Isa Moranbah

WallumbillaBallera

Narrabri

Melbourne

Moomba

Adelaide

Newcastle

17

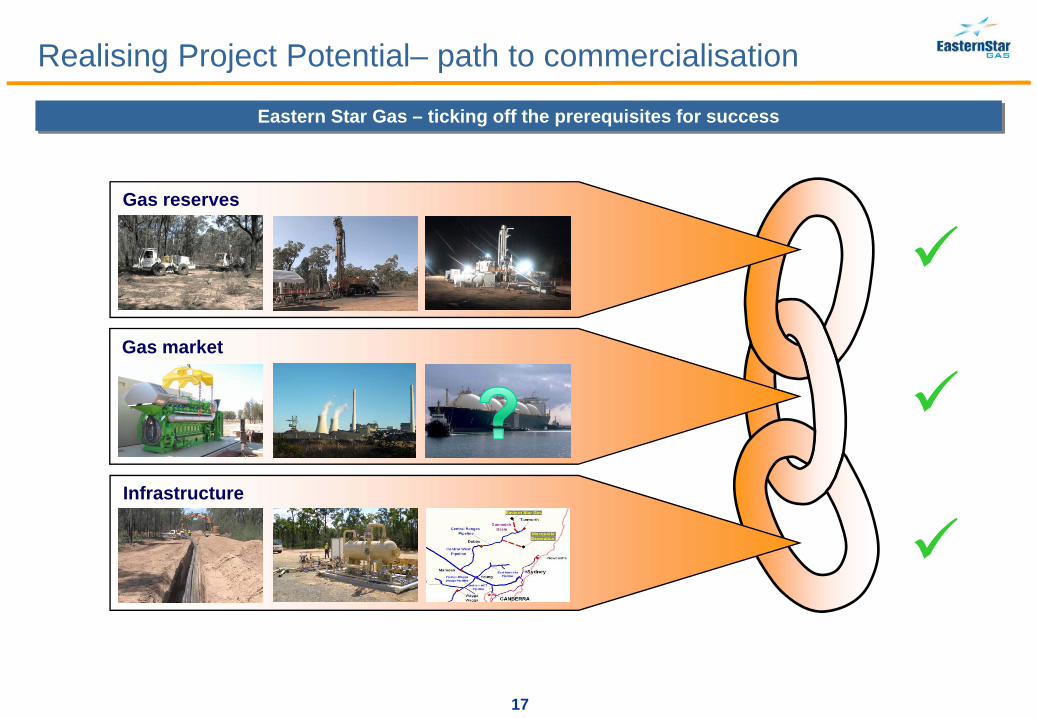

Realising Project Potential– path to commercialisation

Eastern Star Gas – ticking off the prerequisites for success

Gas reserves

Infrastructure

Gas market

18

This presentation may contain forward looking statements that are subject to risk factors associated with oil and gas businesses. It is believed that the expectations reflected in these statements are reasonable but they may be affected by a variety of variables and changes in underlying assumptions which could cause actual results or trends to differ materially, including but not limited to: price fluctuations, actual demand, currency fluctuations, drilling and production results, reserve estimates, loss of market, industry competition, environmental risks, physical risks, legislative, fiscal and regulatory developments, economic and financial market conditions in various countries and regions, political risks, project delay or advancement, approvals and cost estimates.

Investors should undertake their own analysis and obtain independent advice before investing in ESG shares.

All references to dollars, cents or $ in this presentation are to Australian currency, unless otherwise stated.

Disclaimer