Example, Study I Results

26

Results Of Analysis Of Various Scenarios For Well Off Couple Study 2015-01 James K. Orr Provider of detail personal financial simulations

Transcript of Example, Study I Results

Results Of Analysis Of Various Scenarios For Well Off Couple

Study 2015-01

James K. OrrProvider of detail personal financial simulations

Optimum Scenario Selection

• Determining what are the optimum retirement options to select is difficult and is very, very dependent on a couple’s specific individual circumstances and assumptions made.

• This study quantitatively evaluates several scenarios involving choices on Social Security and withdrawal of Tax-Deferred IRA funds for one specific set of circumstances.

• Conclusion are reached as to the optimum choices of those considered.

Case Details

• Married Couple– Both retire at the same time at age 62– No pension or other similar income– Both qualify for Social Security of $ 30,000 at 66– Post Tax savings of $ 500,000– Pre-Tax IRA savings of $ 2,000,000– Annual expenses of $ 80,000 plus federal taxes

and medical premiums (coverage equivalent to Medicare)

Case Assumptions

• Medical premiums– $ 10,000 prior to age 65 (start of Medicare)– At age 65, Medicare premiums based on Modified

Adjusted Gross Income (MAGI) levels • Inflation at 2.5 % annual rate of increase– Social Security Payments, Federal Income Tax

Tables, and Standard Deduction increase 100 % with inflation (over optimistic, but assumption)

Rate of Investment Return

• Post Tax Accounts– Rate of Return of 3.0 % as Qualified Dividends

• This is on 0.5 % above inflation rate• Later study looks at two levels of Rate of Return for Post Tax

Accounts, 3.0 % and 4.5 % (same as for Roth Accounts)

• Pre-Tax Accounts– Rate of Return of 4.5 %

• This is 2.0 % above inflation rate

• Roth Accounts– Rate of Return of 4.5 %

• This is 2.0 % above inflation rate

Retirement Decision Strategies

• Effect Of Social Security Retirement Age– Very simple scenarios• Begin Social Security at various ages from 62 to 70• Withdraw from Pre-Tax IRA based on Required

Minimum Distributions starting at 70 ½

Annual Social Security For Each Spouse62 62 64 65 66

(FRA)67 68 69 70

$ 22,500 $ 24,000 $ 26,000 $ 28,000 $ 30,000 $ 32,400 $ 34,800 $ 37,200 $ 39,600

Retirement Decision Strategies

• SS_70_Roth_Spouse_SS scenario– Start Social Security At Age 70– Spousal Benefit for one spouse at Age 66 (FRA)

• If you have not applied for your own benefits and you’re at least Full Retirement Age (FRA), deemed filing doesn’t apply and you can file solely for your Spousal Benefit, equal to 50% of your spouse’s PIA. This allows you to earn delayed retirement credits on your own record up to age 70.

– Also, withdraw from Pre-Tax IRA and deposit in Roth IRA• Subject to not exceeding Federal Income tax Marginal Rate

boundary for 25 % to 28 % • Subject to not reducing the Post Tax account below zero

Retirement Decision Strategies

• SS_70_Roth scenario– Start Social Security At Age 70– Also, withdraw from Pre-Tax IRA and deposit in

Roth IRA• At same levels as for SS_70_Roth_Spouse_SS scenario

to keep the Roth account the same in the two options

Retirement Decision Strategies

• SS_70_Roth_Spouse_SS_Spike scenario– Start Social Security At Age 70– Spousal Benefit for one spouse at Age 66 (FRA)

• If you have not applied for your own benefits and you’re at least Full Retirement Age (FRA), deemed filing doesn’t apply and you can file solely for your Spousal Benefit, equal to 50% of your spouse’s PIA. This allows you to earn delayed retirement credits on your own record up to age 70.

– Also, withdraw from Pre-Tax IRA and deposit in Roth IRA• Subject to not exceeding Federal Income tax Marginal Rate boundary for

25 % to 28 % • Subject to not reducing the Post Tax account below zero

– After 70 ½, continue to move approximately $ 50,000 per year to Roth IRA for 7 years

Retirement Decision Strategies

• SS_62_Super_Spike scenario– Start Social Security At Age 62– Also, withdraw from Pre-Tax IRA and deposit in

Roth IRA (average $ 130,000 for 8 years)• Subject to not exceeding Federal Income tax Marginal

Rate boundary for 28 % to 33 % • Subject to not exceeding $ 170,000 Modified Adjusted

Gross Income (MAGI)• Subject to not reducing the Post Tax account below

zero

• Effect Of Social Security Retirement Age– Very simple scenarios

• Begin Social Security at various ages from 62 to 70• Withdraw from Pre-Tax IRA based on Required Minimum

Distributions only starting at 70 ½

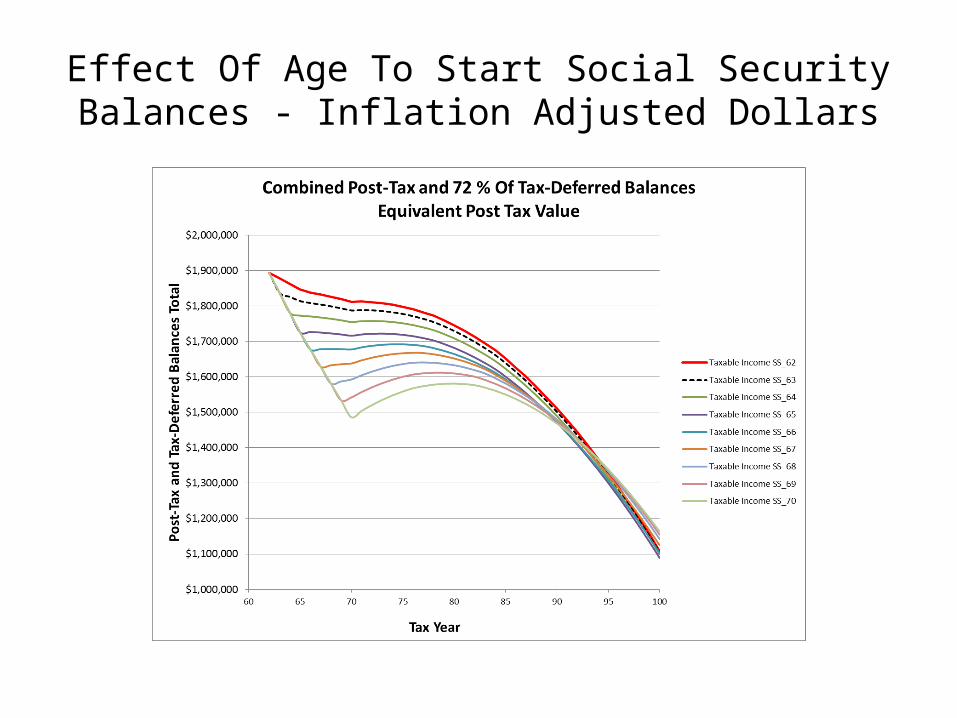

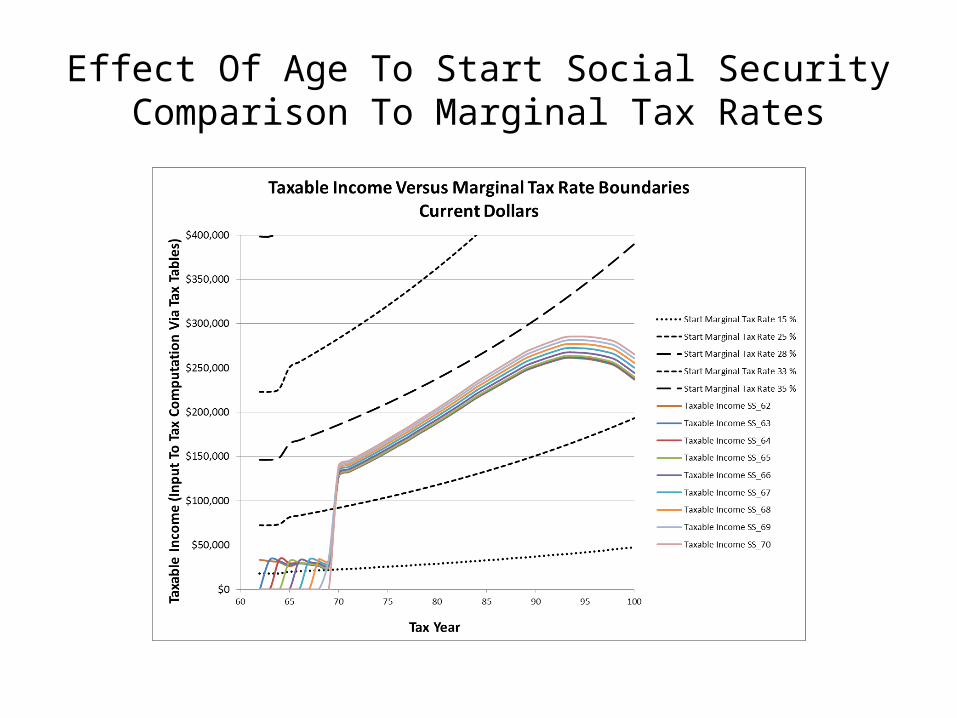

• Conclusions– Prior to age 94, starting S.S. at age 62 is optimum– Past age 94, starting S.S. at age 70 is optimum

• Rationale– Lower S.S. rate at 62 it compensated by low tax rate

in early years, especially for Qualified Dividends as Pre-Tax funds are maintained. In later years, the higher S.S. benefit finally overwhelms as

Effect Of Age To Start Social SecurityBalances - Current Year Dollars

Effect Of Age To Start Social SecurityBalances - Inflation Adjusted Dollars

Effect Of Age To Start Social SecurityComparison To Marginal Tax Rates

Effect Of Age To Start Social SecurityComparison To Medicare Rates Thresholds

• Effect Of Tax-Deferrer IRA Withdrawal Scenarios– Sample Scenarios

• Several approaches with tax-deferred IRA withdrawals in early years

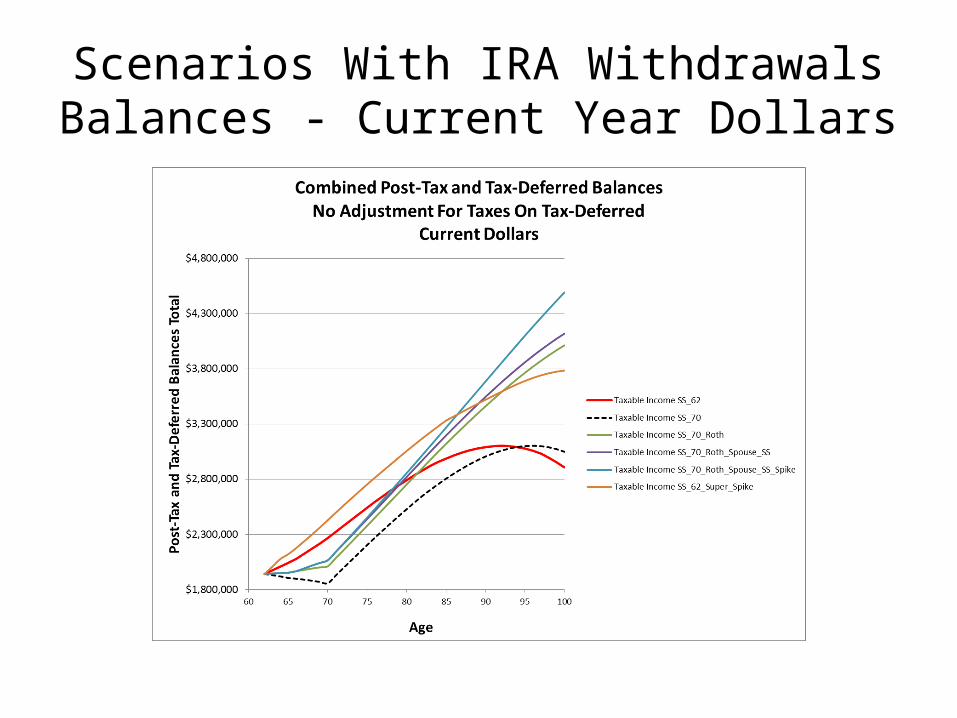

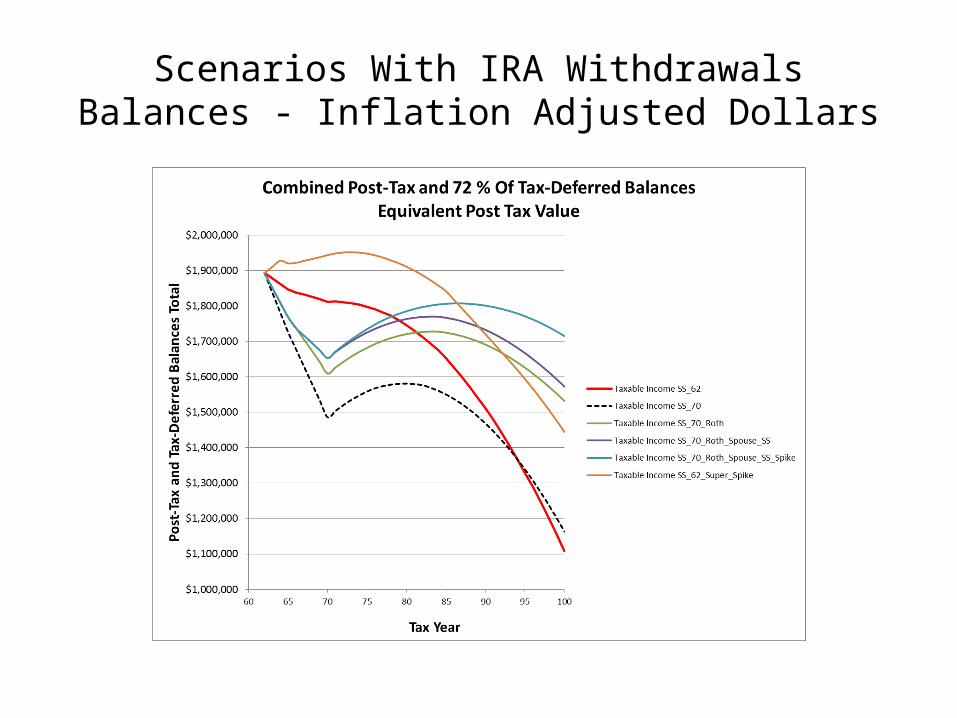

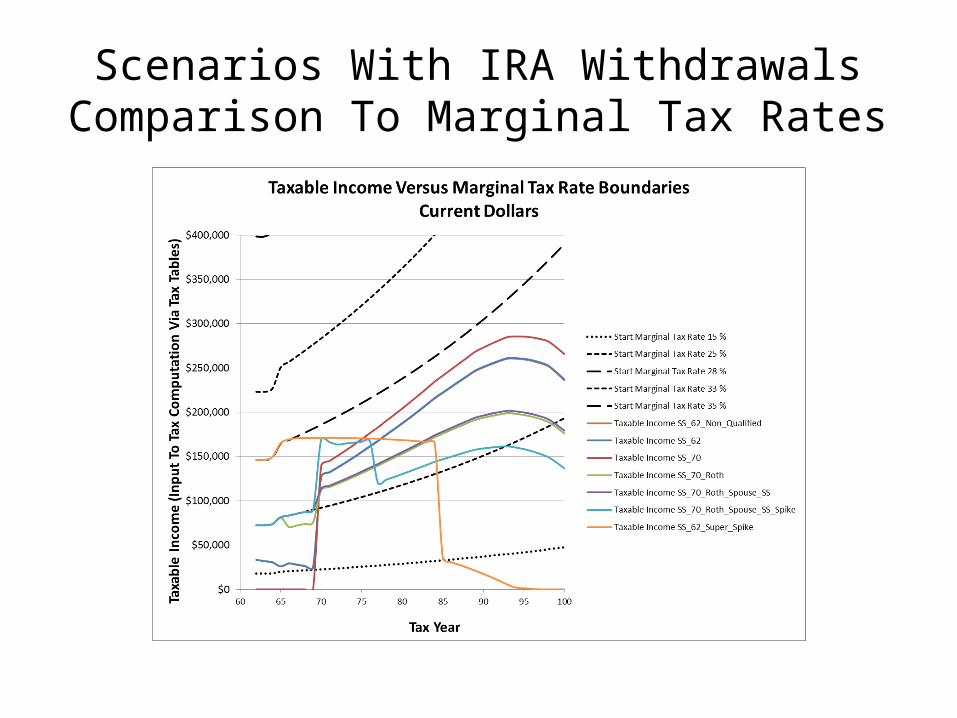

• Conclusions– Starting Social Security at Age 62, with maximum

conversion to Roth IRA is optimum prior to age 86– Starting Social Security at Age 70 with moderate

conversion to Roth IRA is optimum after age 86– Other scenarios producing better results possible.

• Rationale– Both optimum scenarios minimize Medicare cost and

maximize time below the Federal Tax marginal tax rate boundary between 25 % and 28 %.

Scenarios With IRA WithdrawalsBalances - Current Year Dollars

Scenarios With IRA WithdrawalsBalances - Inflation Adjusted Dollars

Scenarios With IRA WithdrawalsComparison To Marginal Tax Rates

Scenarios With IRA WithdrawalsComparison To Medicare Rates Thresholds

• Effect Of Different Post Tax Return Scenarios– Sample Scenarios

• Two scenarios with Social Security starting at age 62 are redone with Post Tax Return (still Qualified Dividends) at 4.5 % and compared to original scenarios at 3.0 % return.

• No change to withdrawals from Pre-Tax IRA or additions to Roth IRA (results in higher than optimum federal income tax and Medicare payments for some years).

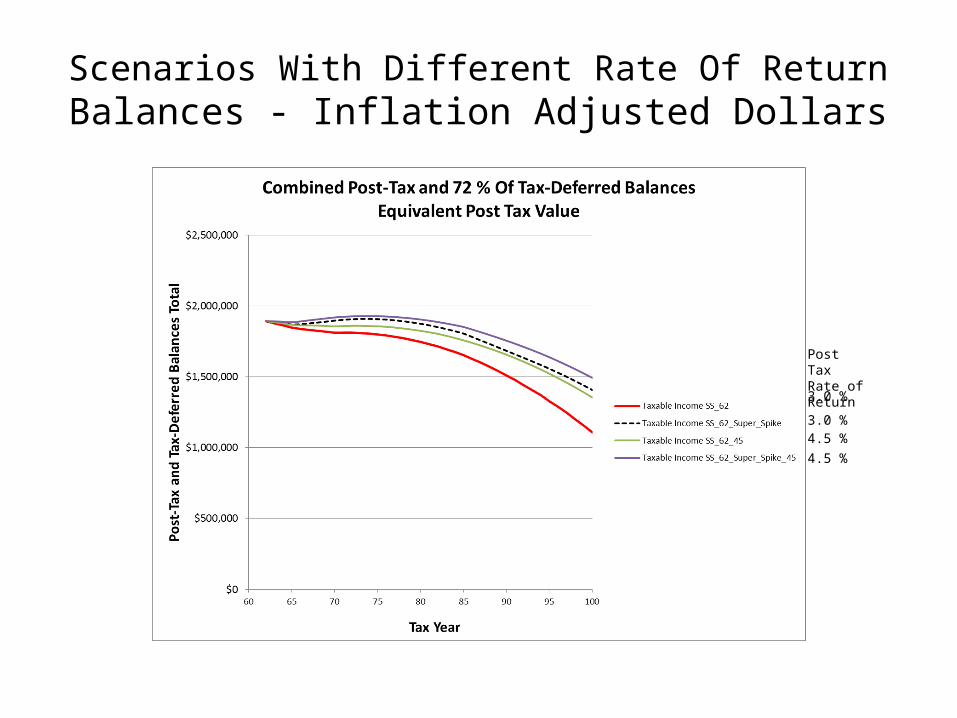

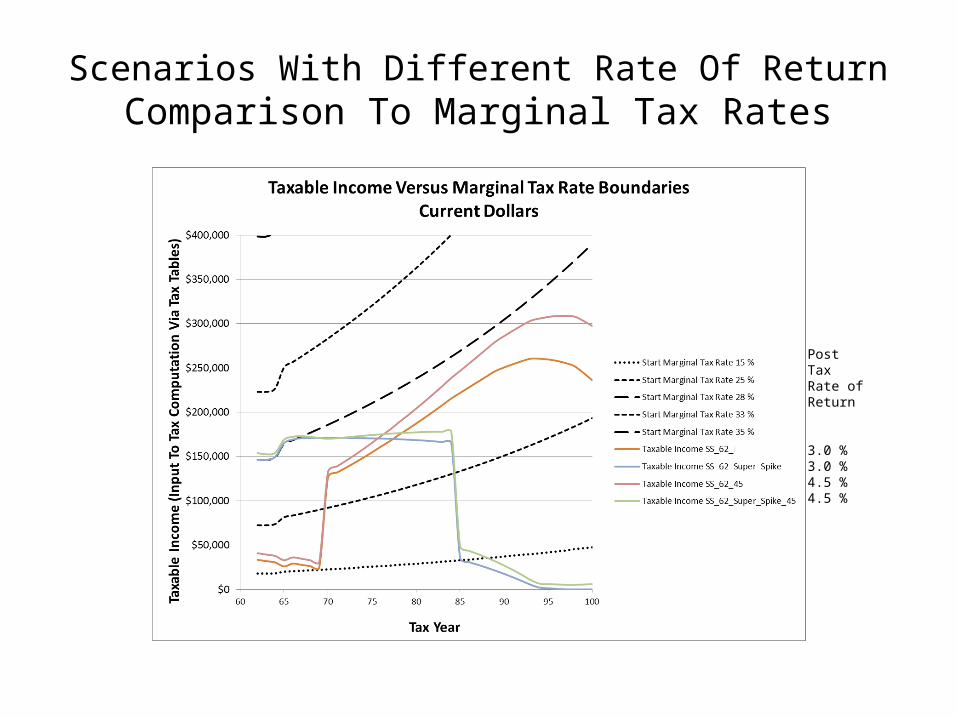

• Conclusions– Some of the improved performance due to

conversion to Roth IRA is due to the higher rate of return in Roth IRA versus Post Tax account in the original scenarios.

– Results are very sensitive to assumptions.

Scenarios With Different Rate Of ReturnBalances - Current Year Dollars

Post TaxRate of Return

4.5 %4.5 %3.0 %3.0 %

Scenarios With Different Rate Of ReturnBalances - Inflation Adjusted Dollars

3.0 %

3.0 %4.5 %4.5 %

Post TaxRate of Return

Scenarios With Different Rate Of ReturnComparison To Marginal Tax Rates

Post TaxRate of Return

4.5 %4.5 %3.0 %3.0 %

Scenarios With Different Rate Of ReturnComparison To Medicare Rates Thresholds

Post TaxRate of Return

4.5 %4.5 %3.0 %3.0 %

Conclusions

• Detail quantitative simulation of Federal Income Tax and Medicare cost for several scenarios are presented.

• For this couple’s starting conditions ($ 500,000 Post Tax, $ 2,000,000 Pre-Tax IRA) and rate of return assumptions, starting Social Security at age 62 was optimum to later ages than expected.

• Results are very, very scenario dependent as demonstrated by changing only the Post Tax account rate of return.