Evolving Cooperative Business Structures 5 th Annual Farmer Cooperative Conference November 13-15,...

21

Evolving Cooperative Evolving Cooperative Business Structures Business Structures 5 5 th th Annual Farmer Cooperative Conference Annual Farmer Cooperative Conference November 13-15, 2002 November 13-15, 2002 Dave Swanson and Robert Dave Swanson and Robert Hensley Hensley

-

Upload

margery-hall -

Category

Documents

-

view

214 -

download

0

Transcript of Evolving Cooperative Business Structures 5 th Annual Farmer Cooperative Conference November 13-15,...

Evolving Cooperative Business Evolving Cooperative Business StructuresStructures

55thth Annual Farmer Cooperative Conference Annual Farmer Cooperative Conference

November 13-15, 2002November 13-15, 2002

Dave Swanson and Robert HensleyDave Swanson and Robert Hensley

2

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

Definitions of CooperativeDefinitions of Cooperative

• Tax Law DefinitionTax Law Definition

• Capper-Volstead Definition for Farm CoopsCapper-Volstead Definition for Farm Coops

• Borrowing Eligibility – CoBank, CFA, NCB Borrowing Eligibility – CoBank, CFA, NCB

• Coop Trade Association Eligibility StandardsCoop Trade Association Eligibility Standards

• Rochdale PrinciplesRochdale Principles

• State & Federal Securities LawsState & Federal Securities Laws

Common Theme:Common Theme:Allocate Margins by PatronageAllocate Margins by Patronage

3

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

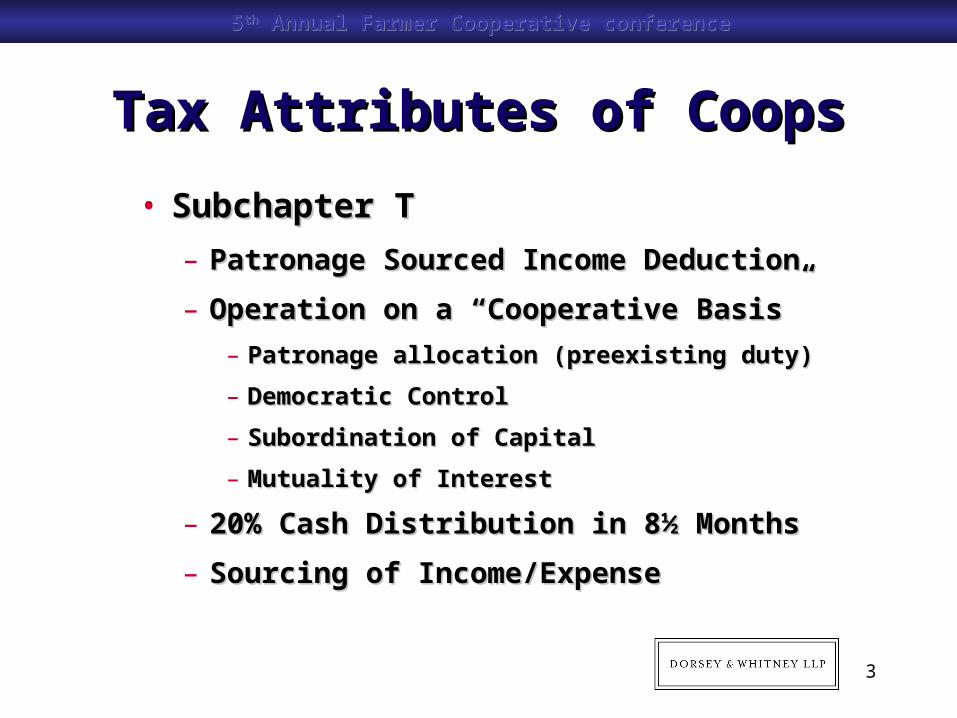

Tax Attributes of CoopsTax Attributes of Coops

• Subchapter TSubchapter T

– Patronage Sourced Income DeductionPatronage Sourced Income Deduction

– Operation on a “Cooperative Basis”Operation on a “Cooperative Basis”

– Patronage allocation (preexisting duty)Patronage allocation (preexisting duty)

– Democratic ControlDemocratic Control

– Subordination of CapitalSubordination of Capital

– Mutuality of InterestMutuality of Interest

– 20% Cash Distribution in 8½ Months20% Cash Distribution in 8½ Months

– Sourcing of Income/ExpenseSourcing of Income/Expense

4

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

Tax Attributes of LLCsTax Attributes of LLCs

• Pure Pass-Through of Tax Attributes to Pure Pass-Through of Tax Attributes to MembersMembers

• No Patronage Requirement (but it’s No Patronage Requirement (but it’s allowed) allowed) –– facilitates non-member –– facilitates non-member equityequity

• Publicly Traded Partnership RulesPublicly Traded Partnership Rules

• Self-employment TaxSelf-employment Tax

• Passive Activity Loss LimitationsPassive Activity Loss Limitations

5

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

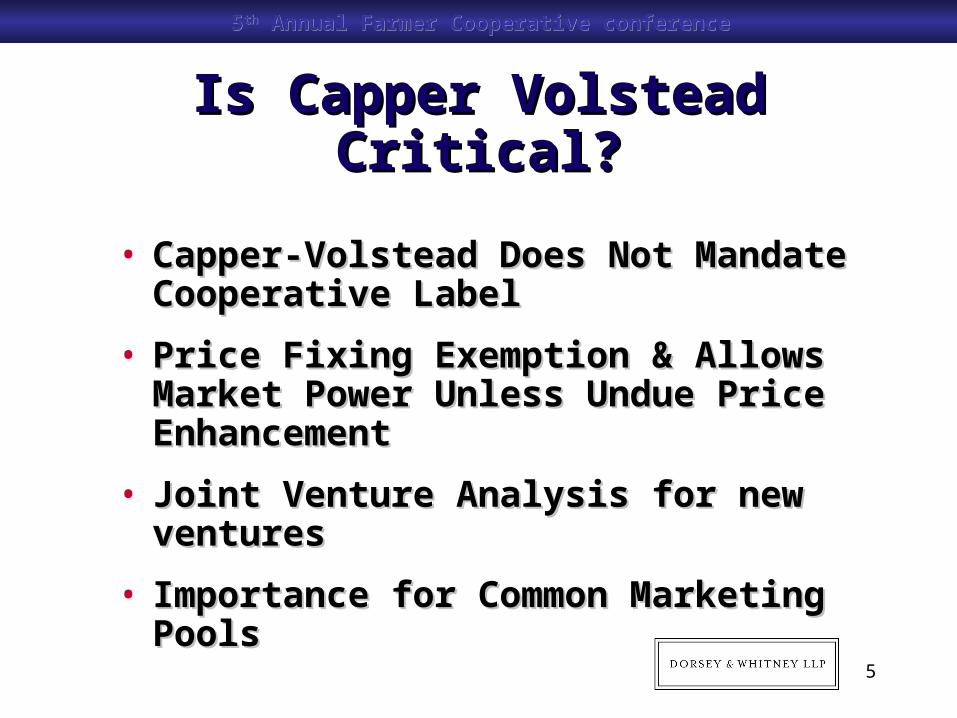

Is Capper Volstead Critical?Is Capper Volstead Critical?

• Capper-Volstead Does Not Mandate Capper-Volstead Does Not Mandate Cooperative LabelCooperative Label

• Price Fixing Exemption & Allows Market Price Fixing Exemption & Allows Market Power Unless Undue Price EnhancementPower Unless Undue Price Enhancement

• Joint Venture Analysis for new venturesJoint Venture Analysis for new ventures

• Importance for Common Marketing PoolsImportance for Common Marketing Pools

6

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

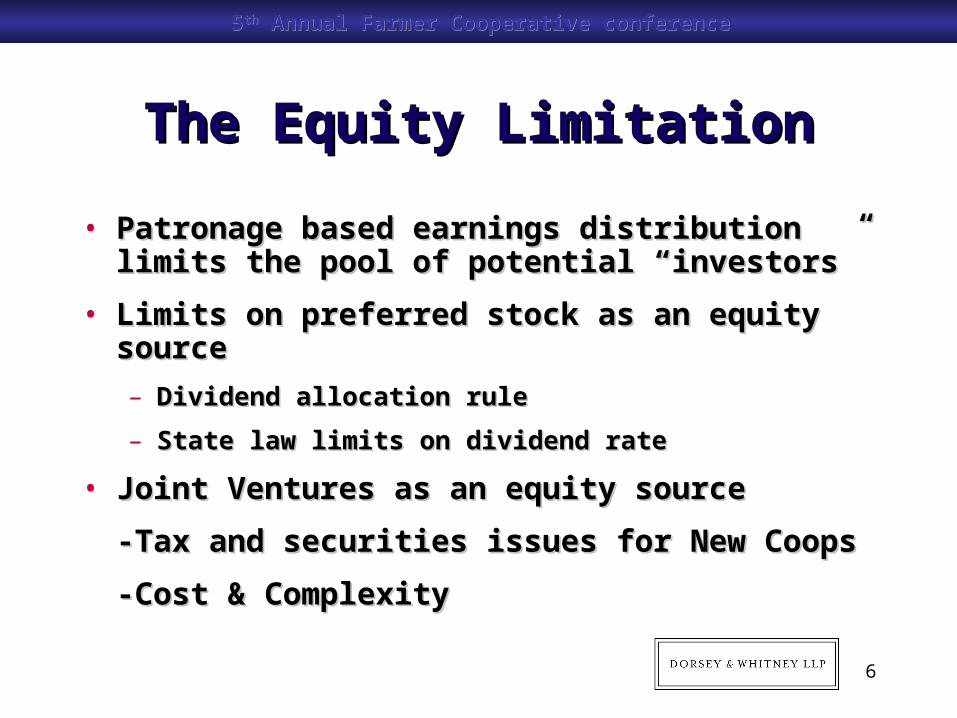

The Equity LimitationThe Equity Limitation

• Patronage based earnings distribution limits the Patronage based earnings distribution limits the pool of potential “investors”pool of potential “investors”

• Limits on preferred stock as an equity source Limits on preferred stock as an equity source

– Dividend allocation ruleDividend allocation rule

– State law limits on dividend rateState law limits on dividend rate

• Joint Ventures as an equity sourceJoint Ventures as an equity source

-Tax and securities issues for New Coops-Tax and securities issues for New Coops

-Cost & Complexity-Cost & Complexity

7

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

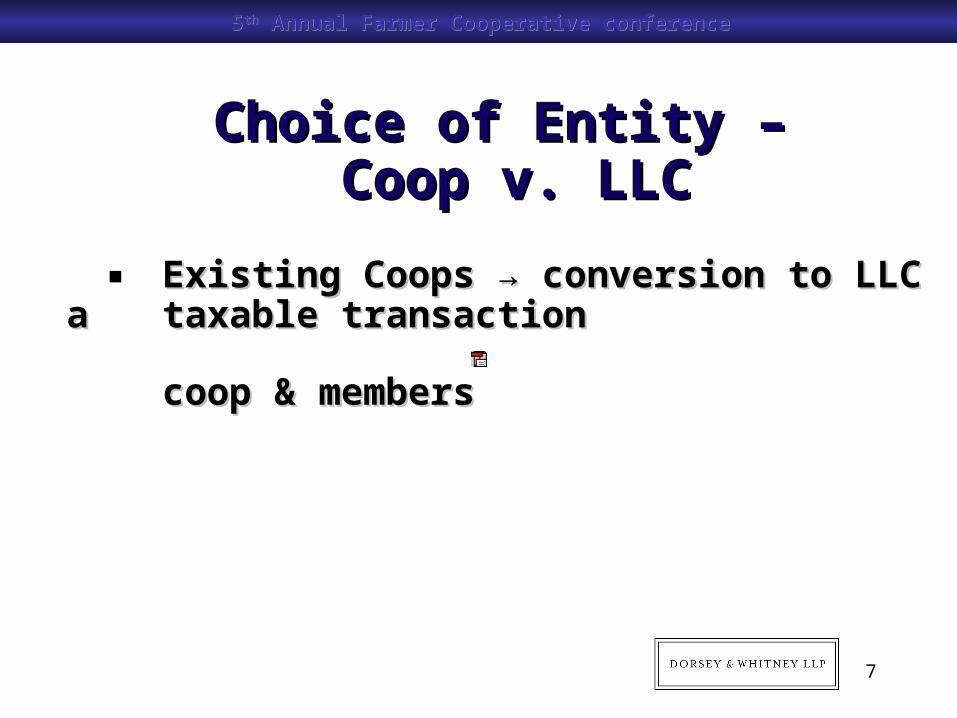

Choice of Entity – Choice of Entity – Coop v. LLCCoop v. LLC

Existing Coops → conversion to LLC a Existing Coops → conversion to LLC a taxable transactiontaxable transaction

coop & memberscoop & members

8

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

Choice of Entity —Choice of Entity —Coop v. LLCCoop v. LLC

Four Tax Models:Four Tax Models:

• Straight Coop (corporation operated on a Straight Coop (corporation operated on a cooperative basis)cooperative basis)

• Straight LLC (LLC operated as a Straight LLC (LLC operated as a partnership)partnership)

• LLC taxed as a corporation operated on a LLC taxed as a corporation operated on a cooperative basis. PLR 200119016cooperative basis. PLR 200119016

• Cooperative LLC (LLC taxed as a Cooperative LLC (LLC taxed as a partnership but operated on a cooperative partnership but operated on a cooperative basis)basis)

9

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

Choice of Entity – Choice of Entity – Coop v. LLCCoop v. LLC

• New Coops — It’s an “Art” Not a “Science”New Coops — It’s an “Art” Not a “Science”

10

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

Choice of Entity – Choice of Entity – Coop v. LLCCoop v. LLC

CoopCoop

May be tax neutral May be tax neutral

(but with limits)(but with limits)

Outside Equity Outside Equity LimitsLimits

LLCLLC

Tax neutralTax neutral

Outside Outside Equity Equity FlexibilityFlexibility

The Tax / Equity Flexibility FactorThe Tax / Equity Flexibility Factor

11

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

Choice of Entity – Choice of Entity – Coop v. LLCCoop v. LLC

Some Driving FactorsSome Driving Factors

• Securities RegistrationSecurities Registration

– CostCost

– 521 Exemption521 Exemption

– Intra-StateIntra-State

– Private PlacementPrivate Placement

• Tax Credits — EthanolTax Credits — Ethanol

• Blue Sky ExemptionsBlue Sky Exemptions

• Borrowing EligibilityBorrowing Eligibility

• Importance of Non-Importance of Non-Producer InvestmentProducer Investment

• Special Program Special Program EligibilityEligibility

• Nature of the Farm Nature of the Farm Product InvolvedProduct Involved

• Nature of the Market Nature of the Market and End Productsand End Products

12

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

Redefining CooperativeRedefining Cooperative

• To Date:To Date: Heavy emphasis on tax Heavy emphasis on tax definitiondefinition

• Evolution in Thinking About Evolution in Thinking About Organizational Models in GeneralOrganizational Models in General

• In the Future: Earnings Distributed In the Future: Earnings Distributed “Primarily” on Patronage?“Primarily” on Patronage?

13

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

14

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

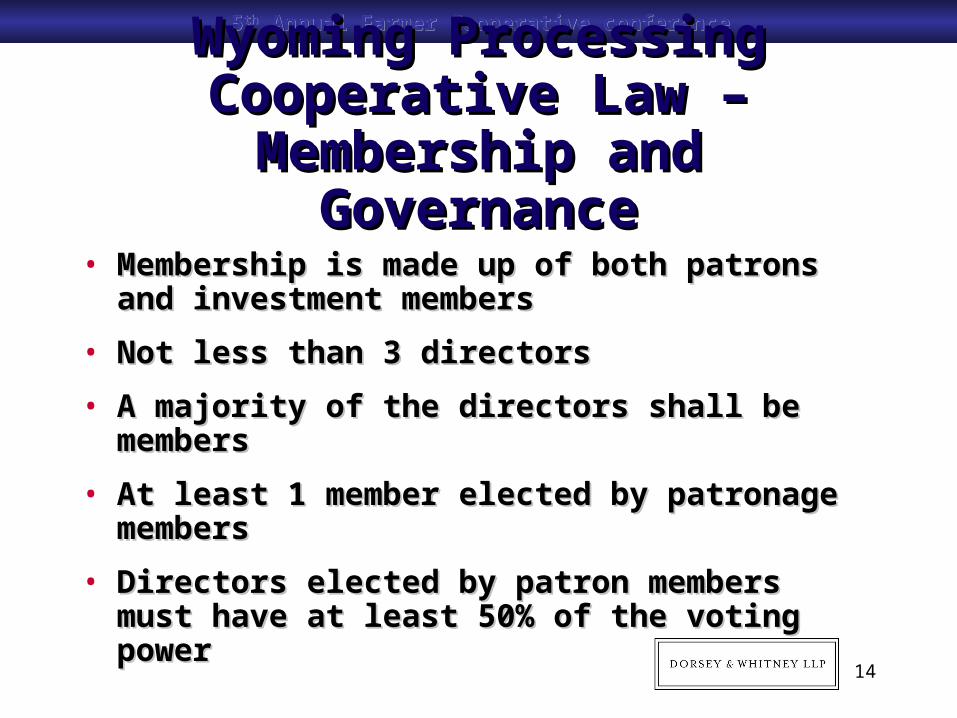

Wyoming Processing Wyoming Processing Cooperative Law – Cooperative Law –

Membership and GovernanceMembership and Governance

• Membership is made up of both patrons and Membership is made up of both patrons and investment membersinvestment members

• Not less than 3 directorsNot less than 3 directors

• A majority of the directors shall be membersA majority of the directors shall be members

• At least 1 member elected by patronage membersAt least 1 member elected by patronage members

• Directors elected by patron members must have Directors elected by patron members must have at least 50% of the voting powerat least 50% of the voting power

15

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

Wyoming Processing Wyoming Processing Cooperative Law – Financial Cooperative Law – Financial

RightsRights

• Patron members receive allocations and Patron members receive allocations and distributions based upon patronagedistributions based upon patronage

• Investment members receive allocations Investment members receive allocations and distributions based upon their and distributions based upon their investmentinvestment

• At least 15% of the profit allocations and At least 15% of the profit allocations and distribution must go to patron membersdistribution must go to patron members

16

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

Wyoming Processing Wyoming Processing Cooperative Law – Tax Cooperative Law – Tax

TreatmentTreatment

• Eligible for Subchapter K tax treatment. Eligible for Subchapter K tax treatment. All earning “pass through” to membersAll earning “pass through” to members

• Eligible for Subchapter T tax treatmentEligible for Subchapter T tax treatment

17

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

Wyoming Processing Wyoming Processing Cooperative Law – IssuesCooperative Law – Issues

• Investment member causes the Investment member causes the processing coop to sacrifice its Capper-processing coop to sacrifice its Capper-Volstead protection.Volstead protection.

• Questions concerning forming under the Questions concerning forming under the statute to “market” if there is an outside statute to “market” if there is an outside investor – regulatory issues?investor – regulatory issues?

• 50% governance can be an issue. Is it a 50% governance can be an issue. Is it a cooperative?cooperative?

18

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

What would Andrew Volstead What would Andrew Volstead say?say?

19

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

Wyoming Processing Wyoming Processing Cooperative Law – IssuesCooperative Law – Issues

• Investment member Investment member causes the processing coop causes the processing coop to sacrifice its Capper-to sacrifice its Capper-Volstead protection.Volstead protection.

• Questions concerning Questions concerning forming under the statute to forming under the statute to “market” if there is an “market” if there is an outside investor – outside investor – regulatory issues?regulatory issues?

• 50% governance can be an 50% governance can be an issue. issue.

20

55thth Annual Farmer Cooperative conference Annual Farmer Cooperative conference

Proposed Minnesota and Proposed Minnesota and Wisconsin Cooperative Law Wisconsin Cooperative Law

ReformReform

• Research and discussions well under wayResearch and discussions well under way

• DividendsDividends

• VotingVoting

• GovernanceGovernance

• Clearer definition of who qualifiesClearer definition of who qualifies

QUESTIONS?QUESTIONS?