Evaluation of the Development and Performance of Selected GCC and Non-GCC Stock MarketsProject...

37

PhD and MIF Programmes Project Paper Evaluation of the Development and Performance of Selected GCC and Non-GCC Stock Markets Islamic Capital Markets FN 6603/5603 Professor Dr. Obiyathulla Ismath Bacha September 2013- Semester Group 3 Name Student ID Idwan Hakim 1000428 Mace Abdullah 1000491 Gamal Salih Omer 1200073 Ahmed Elobied 1200074 Zulfiqar Ali Khan 1200085

-

Upload

mace-abdullah -

Category

Business

-

view

248 -

download

1

Transcript of Evaluation of the Development and Performance of Selected GCC and Non-GCC Stock MarketsProject...

Page 1

PhD and MIF Programmes

Project Paper

Evaluation of the Development and Performance of Selected GCC and Non-GCC Stock Markets

Islamic Capital Markets

FN 6603/5603

Professor Dr. Obiyathulla Ismath Bacha

September 2013- Semester

Group 3

Name Student ID

Idwan Hakim 1000428

Mace Abdullah 1000491

Gamal Salih Omer 1200073

Ahmed Elobied 1200074

Zulfiqar Ali Khan 1200085

2

1.0 INTRODUCTION

Stock markets are considered essential to economic growth. This study takes a

comparative view of 10 emerging stock markets. Five (5) are located in Gulf Cooperation

Council (GCC) countries, while the remaining five (5) are in Non-GCC countries. The GCC

stock markets are: Qatar (Qatar Stock Exchange); United Arab Emirates (Dubai Financial

Market or DFM is one of three stock exchanges in the UAE, along with Abu Dhabi Securities

Exchange (ADX) and NASDAQ Dubai-set up to trade international stocks); Kuwait (Kuwait

Stock Exchange); Saudi Arabia (Saudi Arabia Stock Exchange) and Bahrain (Bahrain Stock

Exchange). The five (5) Non-GCC stock markets are: Luxembourg (Luxembourg Stock

Exchange), Norway (Oslo Stock Exchange), Belgium (Euronext Brussels), South Korea

(Korea Exchange) and Singapore (Singapore Exchange).

1.1 Motivation for Research

The GCC countries are predominantly Islamic countries with prevalent Islamic

financial systems. The NGCC countries are predominantly non-Islamic with prevalent

convention financial systems. There are theoretical differences between Islamic and

conventional financial systems. The GCC stock markets are expected to have conventional

aspects. Conversely, the NGCC stock markets are expected to contain equities that can be

deemed Shari’ah-compliant. Much is written about the qualitative and quantitative “screens”

placed on Shari’ah-compliant equities; primarily in the context of indices and mutual funds.

This study seeks to determine whether such “screens” have impacted the selected stock

markets sufficiently enough to cause distinctions that are significant.

1.2 Research Objectives

This study applies empirical methods to look at selected markets through the prism of

a number of stock market development indicators promulgated by the World Bank

(http://data.worldbank.org/indicator) and generally accepted by researchers in the area of

stock market development. The GCC and Non-GCC stock market data and results of

empirical tests are compared, contrasted, analyzed and interpreted to provide answers to the

research questions presented.

1.3 Research Questions

The following empirical questions are asked:

(1) Are there any significant difference between stock market development and performance

among and between GCC and Non-GCC countries? (2) What are the differences, if any?

3

(3) What are the implications of these differences on cost of capital, quality of returns,

competitiveness, attractiveness to foreign investors and the economy as whole? The test

hypotheses are:

H0: There are no significant difference between stock market development and performance

in GCC and Non-GCC countries.

H1: There are significant difference between stock market development and performance in

GCC and Non-GCC countries.

The rest of the paper is organized as follows: Section 2 is a literature review of equity

markets development and it linkages to financial development and macroeconomic

determinants. It is followed by Section 3, an explanation of the research methodology.

Section 4 is a discussion of empirical results including summary statistics of selected

indicators, the test of difference in means results, and the correlations between the stock

markets development indicators. The final part, Section 5, provides conclusions and policy

implications.

2.0 LITERATURE REVIEW

Modern stock markets play an important role in economic development.

Underdeveloped and inefficient stock markets deter investment, particularly foreign and

institutional investments, because they are illiquid, more costly and riskier, i.e. volatile.

Overly restrictive capital controls can further exacerbate foreign investors and inhibit

domestic investor class deepening. Domestic firm access to capital is often stymied causing

stunted growth; forcing them to seek capital in foreign markets. They are, therefore, generally

unattractive for cross-border listings (Bekaert and Harvey, 1997).

2.1 Financial Development Theory

Schumpeter (1934) is credited with hypothesizing that financial intermediation plays a

central role in financial development; thus economic growth. Financial development is

associated with economic growth in two ways (Patrick, 1966): (1) “demand-following” in

which the “real” sector leads financial development as the “real” economy grows; and (2)

“supply-leading” where the “financial” sector is developed (e.g. intermediation) first;

stimulating demand for its supply of funds and services to the “real” sector. Patrick (1966)

proposed the “stage of development hypothesis,” wherein the two growth “paths” to financial

development may intersect with one “path” initially being dominant and later subsiding as the

other becomes more influential.

4

2.2 Financial Development Structure

Financial development can also be viewed from the perspective of financial structure.

Working through the World Bank, Demirguc-Kunt (1999), revived the polemics surrounding

bank and market based financial structures. A financial system is divided between banks (and

“shadow” banks, e.g. insurance companies) and markets (debt and equity).

For our purposes, it is the market-based equities market that is our focus, as it posits

that economic development is advanced through well-functioning markets. Larger, liquid and

well functioning market-based structures foster real economic growth, provide greater profit

incentives to a broader spectrum of the economy’s entrepreneurs and firms, enhance

corporate governance and facilitate risk management (Beck, 2002). The “financial services”

view (Levine, 1997), embraces both divisions and postulates that it is “financial services”

themselves that are more important than the channel of delivery. Thus, the “analytic

spotlight” is on how to provide better intermediation channels in whatever mix or structure.

2.3 Equity Market Development

Market-based structures provide a broader, possibly more fluid, channel for long-term

financial development. Stock markets encourage specialization, as well as acquisition and

dissemination of information (Diamond 1984; Greenwood and Jovanovic 1990). They may

also reduce the cost of mobilizing savings, thus facilitating investment (Greenwood and

Smith 1997). Well-developed stock markets mitigate the principal-agent problem, aligning

the interests of managers and owners, through maximization of firm value (Diamond and

Verrecchia 1982; Jensen and Murphy 1990). Levine (1991) and Bencivenga et al (1996) aver

stock markets ameliorate risk by allowing savers to buy, sell and quickly and cheaply alter

their portfolios. Moreover, firms enjoy easy access to capital through equity issues.

King and Levine (1993) further discuss the importance of stock markets in allowing

firms to be innovative in their capital structures. Hence, as firms mature, stock markets allow

them to transfer ownership interests to an entirely different class of investors through initial

public offerings, mergers and innovative capital structure transactions. This would be

difficult, at best, without stock markets. Risk mitigation and easy access to a broader

spectrum of capital providers improve the allocation of capital, an important function of

economic growth. More savings and investment enhance long-term economic growth. From a

monetary policy prospective, a well-developed stock market provides a channel for the issue

and repurchase of government securities, thus facilitating liquidity in the bank-based financial

structure. This is important to financial liberalization and alters the pattern of demand for

money.

5

2.4 Stock Market Development Indicators

As noted earlier, the World Bank has developed a database of indicators; some of

which are specific to stock markets. Research conducted by the International Monetary Fund

(IMF) mirrors that of the World Bank, identifying direct quantitative stock market

development key indicators: (1) number of listed companies; (2) market capitalization as a

percentage of GDP; (3) value traded as percentage of GDP; and (4) turnover (Yartley, 2008).

That study also identified qualitative indicators: (1) political risk; (2) law and order (quality

of legal system); (3) bureaucratic quality; (4) democratic accountability; and (5) corruption.

Research emphasizing the growing importance of regional and global financial integration

and the need for expanding investor bases and classes, identifies additional indicators: (1)

capital controls, e.g. taxes, information asymmetry and regulatory restrictions; and (2) pricing

models (Levine and Zervos, 1996).

2.5 Financial Integration and Cost of Capital

Co-movements in global stock markets have been shown to be correlated within lead

and lag time frames (e.g., Kasa, 1992; Siklos and Ng, 2001; Masih and Masih, 1999;

Glezakos et al., 2007). The correlation is strongest where capital control barriers are lowered

(Taylor and Tonks, 1989). Financial integration affects the cost of equity capital of firms,

improves competitiveness and often leads to more precise price discovery. Where barriers to

international investment exist, stock markets are segregated from each other and investors in

each country must bear all the risk of the economic activities of that country. A risk premium

is required to bear the risk that is specific to that country. If a specific country’s stock market

is perceived as illiquid and risky, the risk premium raises the cost of capital for its investors.

That premium is termed the beta coefficient under the capital asset pricing model (CAPM).

Changes in a firm’s cost of capital impact its valuation and its earnings forecast, both

of which influence the listing decision. This is the conclusion of Hail and Leuz (2006), who

find that cross listing in the U.S. stock market, reduces the cost of capital by 70 to 110 basis

points. If a country liberalizes its stock market, allowing foreign investors to invest therein

and domestic investors to invest abroad, research suggests that cost of capital is reduced in

some instances where domestic and foreign risks offset the other through diversification. Risk

is reduced because the portfolios pay a lower related risk premium. This generally reduces

cost of capital in a portfolio of risky securities (Shultz, 1999).

6

2.6 Financial Integration and Investor Base

Shultz further posited that financial integration brings benefits to emerging markets,

including: (1) new shareholders in a firm who possess skills and information that enables

them to monitor management differently from existing local investors; (2) transforming the

relationship between a firm and its shareholders by increasing the competition among

“suppliers” of capital, thereby reducing the cost of capital due to improved competition and

lower transaction costs; (3) transforms the market for corporate control because a firm that is

large in its local market and safe from takeovers in a closed local market is not safe in an

open market, thereby improving the monitoring of managers by existing and potential

shareholders; (4) gives firms access to financial technology that can enable them to raise

capital using new securities and to manage risks more effectively and (5) often attracting

large capital providers, e.g. institutional investors. Among Asian nations, for example, the

growth of institutional investors has resulted in a relatively new, large and lucrative investor

base. In well developed markets, this investor base approaches half of the total investors

(Purfield et al, 2006).

Finally, certain firms and industries are more externally finance dependent than

others. This dependence is ameliorated when capital needs are pursued in more developed

markets. Thus, equity markets have been found to serve as incentive for cross-border listings

among those firms (Rajan and Zingales, 1998).

2.7 Financial Integration and Improved Competitiveness

Zingales (2006) identifies several indicators and determinants of an equity market’s

competitiveness: (1) the number of initial public offerings (IPO) and (2) the ability to attract

foreign listings. The latter he explains is linked to the persistent status of an economy’s

current account and the regulatory environment in the economy. Moreover, he identifies

determinants of the above indicators as: (1) liquidity within the market; (2) visibility by the

financial services sector; (3) bonding with firms from similar industries, country, etc.; (4)

better valuation linked to a more developed financial sector; (5) product/labor market

spillovers (which may be related to strategies to manufacture within the economy of the

listing; (6) listing costs; (7) disclosure costs; and (8) exposure to liability (primarily class

action corporate and security law violations).

Research conducted at the Wharton School in the University of Pennsylvania posits

that illiquid markets affect information symmetry. This phenomenon does not exist in a

perfectly competitive market (because it is assumed that all investors are price takers and all

information is symmetric). Perfect competition exists in a market where there is: (1) low

7

entry and exit barriers; (2) homogeneity of securities, i.e. buyers can purchase a given

security from any seller and receive the same security; (3) perfect knowledge about securities

as to quality, price, and cost; and (4) no single buyer or seller large enough to influence the

market price. Hence, it is posited that competition, informational risk and cost of capital are

cointegrated (Lambert et al, 2010).

3.0 RESEARCH METHODOLOGY

3.1 Research Method

In order to investigate the possible existence of a differences between the

development and performance of the GCC and Non-GCC stock markets, pair sampled t-tests

are conducted on pairs of data consisting of market development indicators. The test is the

mean difference t-test using the standard error of the two samples i.e. pairs of countries

matched according to GDP per capita, within each group (GCC and Non-GCC) and between

the two groups. In order to test the first objective, parametric paired sample t-tests are

conducted using market size and market depth indicators. The second objective of comparing

between the GCC and Non-GCC groups, we use Sharpe and Treynor ratios for comparative

purposes. The average 3-month U.S. Treasury Bill rate and average S&P 500 annual returns

are used as benchmarks, in order to measure the performance of each stock market and to

compare it with others. Moreover, we use correlation testing as a proxy for the level of

financial integration within each group, between the groupings and with the international

market (using S&P 500 returns as a proxy for worldwide market returns).

3.2 Data

This paper focuses on the analyses of development and performance in selected stock

markets. Our main interest is to identify differences between the stock markets selected from

the GCC vis-à-vis the Non-GCC stock markets grouping (East Asia and Europe); in order to

draw conclusions as to the level of differences. We conduct panel analyses on pooled data

from the 10 selected stock markets from 2003 to 2012. The stock markets were selected

because of data availability and paired in an inter-group matching according to GDP per

capita. We gathered the data from two sources: the World Bank Database and DataStream.

All data are on annual bases except the data for market index which is on a weekly base.

3.3 Definition of Variables

Market Size. Three measures are used to determine the market size: (1) Total Market

Capitalization, (2) Total Market Capitalization to GDP, and (3) Number of Listed

Companies. Total Market Capitalization is the value of listed shares. Total Market

Capitalization to GDP Ratio is the value of listed shares divided by GDP. This measure

8

assumes that overall market size is positively correlated with the ability to mobilize capital

and diversify risk on an economy-wide basis. Number of Listed Companies proxies the

ability to mobilize capital through attracting cross-border listings.

Market Depth. Market depth is an indicator of liquidity or the ability to buy and sell

shares quickly. Three indicators of market size are used: (1) Total Volume Traded, (2) Total

Volume Traded to GDP and (3) Trading Velocity. Total Volume Traded is the value of shares

traded on the stock market exchange(s). Total Volume Traded to GDP is the total value of

shares traded on the stock market exchange divided by GDP. This ratio measures the

organized trading of firm equity as a share of national output and therefore should proxy

liquidity on an economy-wide basis. It complements the market capitalization ratio, although

as we will show, some markets may be large, but trading may be anemic.

Trading Velocity is the value of total shares traded divided by market capitalization.

Though it is not a direct measure of theoretical definitions of liquidity, high velocity is often

used as an indicator of low transaction costs. See Lambert et al (2010). This ratio

complements the market capitalization ratio and can be used to identify larger, albeit inactive

markets with inordinately low velocity. It also complements the total volume traded ratio.

While the total volume traded ratio captures trading relative to the size of the economy,

velocity measures trading relative to the size of the stock market. A small liquid market may

have a high velocity ratio but a small total volume traded ratio.

Market's Returns and Volatility. We have used the percentage change in indices to

measure the equity market returns and the standard deviation of market returns to measure the

volatility of returns.

4.0 EMPIRICAL RESULTS

In order to facilitate the analysis, this section is divided into four (4) parts: market

size, market depth, market index returns and volatility and portfolio management. In order to

meet constraints placed on this paper, only three (3) Tables are presented in the body of the

paper, namely: Table 1, the test of stock market and grouping means; Table 2, performance

evaluation; and Table 3, the correlation within and between groupings. All other tables and

figures referenced in the body of this paper are included in the Appendices A-D.

4.1 Market Size

Figure 1 shows the development changes in the 3 market size indicators during the

period from 2003 to 2012. Table A1 show the total market capitalization during the period

decreased for GCC and Non-GCC stock markets by 33.39% and 6.33 % respectively. The

9

largest decreases are 61.40% for Kuwait and 94.88% for Singapore. The capitalization ratio

increased for GCC and Non-GCC stock markets by 147.82% and 156.34% respectively. The

large growth of the capitalization ratio for GCC stock markets coincided with an increase of

the number of listed companies. Non-GCC listings, by contrast, both increased and decreased

during the test period. The number of listed companies grew during the test period by 99.25%

and 1.64% for GCC and Non-GCC stock markets respectively.

Notably, GCC equity markets are more thinly capitalized than the Non-GCC markets.

The 2012 total market capitalization for GCC countries was smaller than the Non-GCC a

decade ago. This is not atypical of emerging markets. The number of listed firms is also

significantly larger for the Non-GCC countries; about five times more than the listed firms in

the GCC countries. This can be interpreted to possibly mean that the Non-GCC stock markets

continue to attract foreign investors and cross-border listings. There may be lingering

qualitative issues that better account for the discrepancies, e.g. lack of openness, the strength

of the legal system, etc. Additionally, depending on the underlying real economies, some

stock markets may be reacting to real economy demand; lagging in the development of their

financial sector. Each economy’s stage of development may reveal some indication of the

direction of the needed corrective action. All GCC stock markets are nascent. The same

cannot be said of all of the Non-GCC markets. Among the GCC markets, Saudi Arabia is the

largest; accounting for nearly half of market capitalization. Among the Non-GCC markets, S.

Korea has the largest capitalization; although Singapore has the largest number of listed

companies. These facts may indicate that Saudi Arabia’s huge petrochemical industry sector

is now demand-leading its financial sector; notwithstanding the findings of Masih et al

(2009). S. Korea’s capitalization may also be similarly the result of demand for capital as its

technology and manufacturing sectors have mushroomed on the backs of multi-nationals, e.g.

Samsung and Hyundai.

Tables A2, A3 and A4 provide descriptive statistics for the three indicators of the

market size during the period 2003-2012 for the selected sample. These tables indicated that

there are differences in means, medians and the standard deviations among GCC and Non-

GCC stock markets. The market size as represented by the three indicators shows that the

group of GCC stock markets has lower size compared with the group of Non-GCC markets.

In order to determine the significance of these differences we conducted a difference in mean

tests.

Table A5 shows the results of the test of the difference in mean for market size

indicators between pairs of stock markets, i.e. a GCC and a Non-GCC stock market matched

10

according to GDP per capita. We find that for total market capitalization there is a significant

difference in means for all pairs of countries at 5% level of significance except the pair of

Qatar and Luxembourg for which we fail to reject the null hypothesis at any level of

significance exists. This makes sense, as these two economies have vied for the No. 1 ranking

in the world for the economy with the highest per capita GDP over a portion of the test

period.

Regarding the total market capitalization to GDP ratio, we find that there is a

significant difference in means for all pairs of countries at 5% level of significance, except

the pair of Saudi Arabia and South Korea for which we fail to reject the null hypothesis at

any level of significance. Again, this makes sense, since both economies are, as noted above,

likely on a demand-leading economic development path. Both economies have substantial

“anchor” industries with multi-national clout. Both also have financial sectors “in the

making.” The test for the number of listed companies shows there is a significant difference

in means for the pairs (UAE/ Norway, Saudi Arabia/ South Korea and Bahrain/Singapore) at

5% level of significance while for the pairs (Qatar/Luxembourg and Kuwait, Belgium) we

fail to reject the null hypothesis at any level of significance.

Tables A6 and A7 show the results of the test of the difference in mean for market

size indicators within each group of countries i.e. the GCC group and the Non-GCC group.

We find that for total market capitalization there is a significant difference in means for all

GCC countries at 5% and 10% level of significance except as between Qatar and UAE for

which we fail to reject the null hypothesis at any level of significance. This may be due to the

fact that these economies are not so far removed from being “joined at the hip,” so to speak;

as they had the same currency and monetary authority not so long ago. Within Non-GCC

group there is a significant difference in means for all stock markets at 5% level of

significance except as between Belgium and Singapore for which we fail to reject the null

hypothesis at any level of significance.

With regard to the total market capitalization to GDP ratio, we find that there is only a

significant difference in means between UAE and all other GCC countries at 5% level of

significance. On the other hand within the Non-GCC group we find that there is a significant

difference in means among all stock markets at 5% level of significance except as between

Luxembourg/Singapore and Norway/ Belgium for which we fail to reject the null hypothesis at

any level of significance.

The test for the number of listed companies shows there is a significant difference in

means for all pairs within GCC and Non-GCC groups at 5% and 10% level of significance

11

except for the pair Norway/Belgium we fail to reject the null hypothesis at any level of

significance. The test for the differences in means for market size indicators between the two

groups of countries as shown in Table 1 indicates that there is a significant difference at 5%

market capitalization (USD Billions) and number of listed companies and at 10% for market

capitalization (% of GDP).

Table 1: Test of the difference in mean between GCC and Non-GCC countries

Market Development Indicator Mean

(GCC)

Mean

(Non-GCC)

Difference

in Mean

P value

Market Size

Market Capitalization (USD Billions) 130.00 335.00 -210.00 *0.000

Market Capitalization (% of GDP) 92.35 113.96 -21.61 **0.072

Number of Listed Companies 90 526 -436 *0.000

Market Depth

Trading Velocity 67.74 87.50 -19.76 0.115

Total

Volume Traded (USD Billions) 145.00 397.00 -250.00

*0.000

Total Volume Traded (% of GDP) 58.12 75.43 -17.31 0.187

Market Returns and Volatility Percentage market index returns 4.03 7.78 -3.75 0.704 Volatility of market returns 22.85 45.12 -22.27 **0.063

*Significant at 5% . **Significant at 10% .

4.2 Market Depth

Figure 2 shows, the development in market depth indicators for the selected GCC and

Non-GCC countries during the period 2003-2012. These indicators include total volume

traded in billions of USD, the volume traded to GDP and the trading velocity. We examine

the trading velocity in order to better understand liquidity. This ratio is defined as the ratio of

the value of total shares traded to the market capitalization. It measures the activity of the

stock market relative to its size. Many analysts use this ratio as gauge of expected transaction

costs. High velocity ratio implies low transaction and consequently more efficient pricing.

Table B1 indicates that although the absolute total volume traded increased by

136.68% and 115.8% for GCC and Non-GCC stock markets respectively, the relative volume

traded to GDP decreased by 29.69% and 1.35%. This may be due to a larger growth in GDP

relative to growth in trading volume in both groups. The table also shows that the trading

velocity ratio also decreased among the groups by 18.85% for GCC markets and 25.28% for

the Non-GCC, respectively. This is due to the larger relative increases in market

capitalization as compared with that for volume traded.

Among Non-GCC markets, Korea has the deepest. Total volume traded is USD1.5

trillion; almost 10 times that of Singapore. The volume traded is almost 150% of its GDP.

12

This may relates, in part, to its market size, since Korea has the most listed firms. On the

other hand, among GCC markets, Saudi Arabia has the deepest. Saudi Arabia leads all other

GCC markets in all measures of market depth.

As was the case in market size indicators, GCC markets are much thinner when

compared with the Non-GCC markets. Total absolute volume traded in 2012 for the GCC

markets is smaller than the total volume traded in Non-GCC countries a decade ago. Growth-

wise, the volume traded did experience a significant increase during the period. This

contributed to the 54% average growth in volume traded for GCC stock markets, compared

with an 11% growth in non-GCC economies.

Tables B2, B3 and B4 provide descriptive statistics for the indicators of the market

depth during the period 2003-2012 for the selected sample. These tables indicate there are

differences in means, medians and the standard deviations among GCC and Non-GCC stock

markets in the their market depth indicators. Market depth, as represented by the 3 indicators,

shows that the group of GCC stock markets had lower growth compared with the Non-GCC

markets. Among the former group, Saudi Arabia shows the largest market liquidity and

Bahrain, the lowest one during the period 2003–2012. Among the latter group S. Korea

shows the largest market liquidity and Luxembourg, the lowest one during the same period.

In order to determine the significance of these differences we conducted tests for the

difference in means.

Table B5 shows the results of the test of the difference in mean for market depth

indicators between pairs of countries i.e. one GCC and one Non-GCC market (matched by

comparable GDPs per capita). We find that for total volume traded there is a significant

difference in means for all pairs of markets at 5% level of statistical significance. Regarding

the total volume traded (% of GDP) we find that there is a significant difference in means for

all pairs of countries at 5% level of significance, except the pair of Saudi Arabia and S.

Korea, for which we fail to reject the null hypothesis at any level of significance. The test for

the trading velocity shows there is a significant difference in means for the pairs

(Qatar/Luxembourg and Bahrain/Singapore) at 5% level of significance while for the

remaining pairs we fail to reject the null hypothesis at any level of significance.

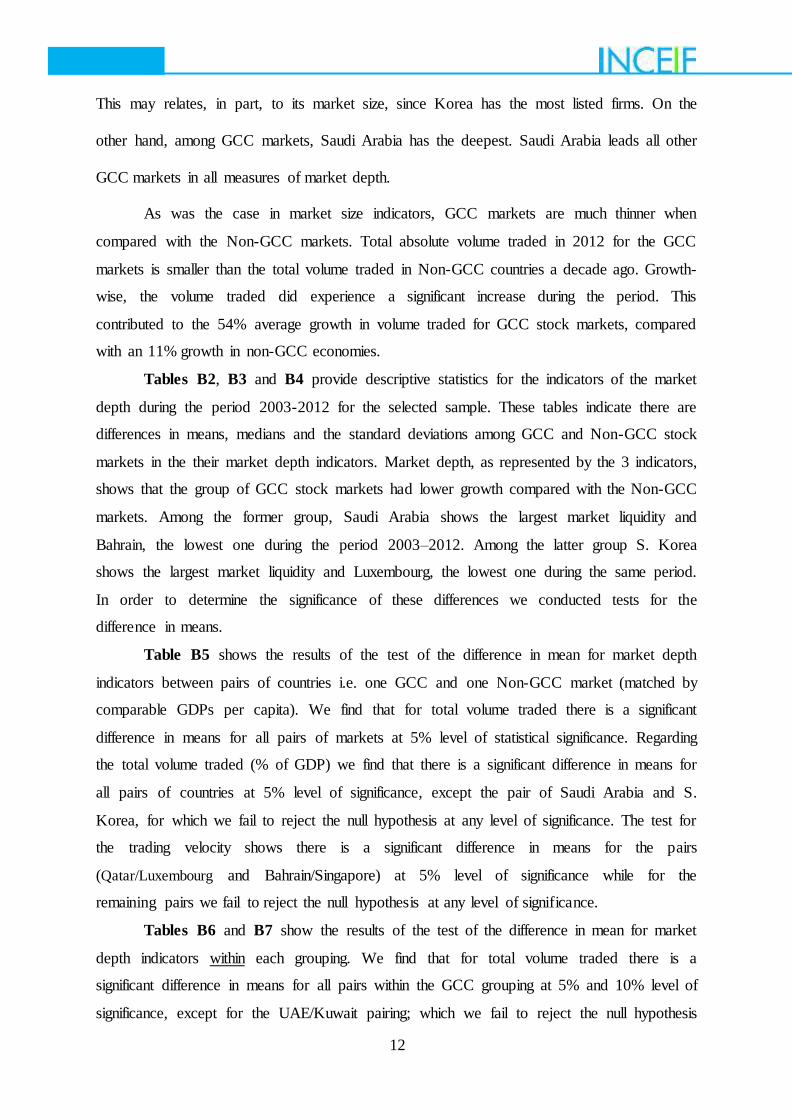

Tables B6 and B7 show the results of the test of the difference in mean for market

depth indicators within each grouping. We find that for total volume traded there is a

significant difference in means for all pairs within the GCC grouping at 5% and 10% level of

significance, except for the UAE/Kuwait pairing; which we fail to reject the null hypothesis

13

at any level of statistical significance. Within Non-GCC grouping there is a significant

difference in means for all pairs at 5% level of significance, except the pair of

Norway/Singapore; which we fail to reject the null hypothesis at any level of significance.

With regard to the total volume traded (% of GDP) we find that there is a significant

difference in means for all pairs within GCC group at 5% and 10% levels of significance,

except the pair Qatar/UAE for which we fail to reject the null hypothesis at any level of

significance.

On the other hand within the Non-GCC group we find that there is a significant

difference in means among all pairs at 5% and 10% level of significance. The test for the

trading velocity shows there is a significant difference in means for all pairs within both GCC

and Non-GCC groupings at 5% level of significance, except for the pairs UAE/Kuwait and

Belgium/S. Korea; which we fail to reject the null hypothesis at any level of significance.

The test for the differences in means for market depth indicators between the two groups, as

shown in Table 1, indicates that there is a significant difference at 5% for the total volume

traded indicator; while for other indicators the differences are insignificant.

4.3 Market Returns and Volatility

During the past decade, many of the emerging countries tried to achieve higher

growth performance through improvements and reforms in their financial sectors. Figure 3

shows the changes in the weekly market indices during the 2007-2012 period. Table C1

shows the market returns and its volatility for the GCC and Non-GCC groups of markets in

panels A and B, respectively.

Table C2 shows the corresponding descriptive statistics. The returns for GCC stock

markets increased by 31.98% during the period, while it decreased by 4.05 % for the Non-

GCC group. Among the GCC group of markets, Bahrain witnessed the smallest returns

(0.65%) and smallest market risk (19.75%); while UAE recorded the largest returns (5.51)

and largest risk (34.73%). Among Non-GCC markets, Belgium experienced the lowest

returns with 0.75%; while the highest returns were observed in the Singapore stock market

with 12.66%. Norway’s stock market shows the highest return volatility at 51.97%; while

Belgium experienced the lowest return volatility at 41.49%.

Table C3 shows the results of the test of the difference in mean for market indexed

returns and their volatility between paired markets, i.e. one GCC and one Non-GCC; matched

according to GDP per capita. We find that the difference in means for all paired markets for

percentage returns there are insignificant. Regarding the volatility of returns (Std. Dev.) we

find that there is a significant difference in means for the pair of Qatar/Luxembourg at 10%

14

level of significance and the pair of Bahrain/Singapore at 5% level of significance while for

the remaining pairs we fail to reject the null. Again, the parity between Qatar/Luxembourg is

understandable, given the similarities in their underlying economic strength; notwithstanding

Qatar’s formidable natural resources. The parity between Bahrain and Singapore may also be

linked to their underlying economies, albeit both economies have developed financial sectors

among their respective groupings.

Tables C4 and C5 show the results of the test of the difference in mean for market

indexed returns and the volatility within each group of countries. We find that for market

index returns there are insignificant differences in means for all pairs within both groups; and

accordingly, we fail to reject the null hypothesis at any level of statistical significance. With

regard to the volatility of returns, we find that there is a significant difference in means for

three pairs within GCC group, i.e.: UAE/Bahrain and Saudi Arabia/Bahrain at 5% and 10%

levels of significance, and except the pair Qatar/U.A.E for which we fail to reject the null

hypothesis at any level of significance. Within the Non-GCC group we find that there are

insignificant differences in means among all pairs, and accordingly, we fail to reject the null

at any level of statistical significance.

The test for the differences in means for market index returns and its volatility between the

two groups of countries as shown in Table 1 indicates that there is a significant difference at

10% for the volatility of returns while for market index returns the differences is

insignificant.

4.4 Portfolio Management

Research postulates that in developed open markets, portfolio investment across

national borders brings benefits of increasing returns and/or reducing risk. See, for example,

Taylor and Tonks, op. cit. The sampled stock markets has been divided into two main groups

GCC and Non-GCC in order to determine the potential role of each group in providing

diversification benefits to international investors. Table 2 provides the performance

evaluation of the selected equity markets by comparing their average returns with the average

returns of S&P500 as an international benchmark during the 2007-2012 test periods.

It indicates that the GCC group has lower incremental returns equaling 1.58%, with a

lower associated risk (22.85%). The Non-GCC group has higher incremental returns equaling

5.33%, with an associated higher risk (45.12%). Moreover, adjusting their returns for risk

using Shape and Treynor ratios indicates that the Non-GCC group has outperformed the GCC

group. The Sharpe ratios (which measure the excess returns factored by the related standard

deviations as volatility metric) were 0.17 and 0.15 for the Non-GCC and GCC stock market

15

groupings, respectively. The Treynor ratios (which measure the excess returns factored by the

beta as a metric of risk premium) also supports these findings. The Treynor ratios were 3.26

and 3.74 for the GCC and Non-GCC stock markets, respectively.

Comparing the performance within the GCC group, we find that UAE achieved the

best average annual returns, while Bahrain, the worst, during the test periods. Within Non-

GCC group, Singapore achieved the best average annual returns, while Belgium, the worst.

We further compared the performance between the paired markets, matched according to

comparable GDP per capita, and find that Qatar, Norway, Kuwait, South Korea and Singapore

had the best performance when compared with Luxembourg, UAE, Belgium, Saudi Arabia and

Bahrain respectively.

Table 2: Performance Evaluation of the Selected Equity Market

2007-2012

Equity Market Incremental

Returns

Sharpe

Ratio*

Treynor

Ratio* Average

Return

Volatility

Std. Dev. Beta

GCC countries:

4.03

22.85 1.05

1.58 0.15 3.26

Bahrain 0.65 19.76 0.91 -1.8 0.03 0.71

Qatar 4.9 26.64 1.23 2.45 0.18 3.98

Saudi Arabia 4.11 29.92 1.38 1.66 0.14 2.98

UAE 5.51 34.73 1.6 3.06 0.16 3.44

Kuwait 4.95 24.04 1.11 2.5 0.21 4.46

Non-GCC countries: 7.78 45.12 2.08 5.33 0.17 3.74

Belgium 0.75 41.5 1.91 -1.7 0.02 0.39

South Korea 12.09 41.51 1.91 9.64 0.29 6.33

Luxembourg 2.85 50.83 2.34 0.4 0.06 1.22

Norway 10.54 51.97 2.4 8.09 0.20 4.39

Singapore 12.66 44.79 2.07 10.21 0.28 6.12

* Sharpe and Treynor ratios use the averages of 3-month U.S. T-Bill rate at 0.6 and S&P 500 average returns of 2.45.

In an effort to measure financial integration between the selected stock markets and the

international stock markets, represented by S&P500, we test to determine which group of our

sample can be considered as a potential avenue for international portfolio diversification.

This, we believe, is a proxy for investor attractiveness. We test this metric by conducting a

correlation test for market returns between our sample markets and the S&P 500. Table 3

shows that there is a positive correlation among countries within each group, possibly due to

the underlying economic relationships. The table also shows that there is negative correlation

between GCC group and US stock markets which on average amounted to 0.53. Accordingly,

the GCC group can be considered as a potential avenue for international portfolio

16

diversification for investors. On the other hand, the table also shows that there is high

positive correlation between the Non-GCC group and the US markets, which equal to 0.90.

This indicates that on the whole, Non-GCC markets should be less attractive for

diversification purposes and portfolio management than their GCC counterpart.

Table 3: Correlation of Market Returns

2007-2012

U.A.E SING. S.A QAT. NOR. LUX. KUW. KOR. BELG. BAHR. GCC NON

GCC

US

UAE 1.00

SING. -0.20 1.00

S.A 0.91 -0.14 1.00

Q AT. 0.72 -0.42 0.87 1.00

NO R. -0.23 0.98 -0.12 -0.42 1.00

LUX. -0.32 0.95 -0.27 -0.57 0.96 1.00

KUW. 0.47 -0.46 0.43 0.66 -0.52 -0.49 1.00

S.KO R -0.33 0.98 -0.21 -0.44 0.98 0.94 -0.50 1.00

BELG. -0.13 0.94 -0.07 -0.36 0.92 0.83 -0.59 0.92 1.00

BAHR.

0.43 -0.70 0.30 0.54 -0.76 -0.68 0.92 -0.74 -0.80 1.00

GCC 0.88 -0.41 0.88 0.91 -0.44 -0.52 0.78 -0.49 -0.40 0.70 1.00

NO N- GCC

-0.25 0.99 -0.17 -0.46 0.99 0.96 -0.52 0.98 0.94 -0.75 -0.47 1.00

US -0.38 0.89 -0.23 -0.39 0.89 0.78 -0.58 0.93 0.94 -0.82 -0.53 0.90 1.00

5.0 Conclusions and Policy Implications

Using the results of our empirical testing, applicable financial development theory and

our intuitive interpretations as researchers, we make the following conclusions and

implications from the study conducted:

1. The GCC group’s market size indicators show that its stock markets could be as much

as a decade behind their Non-GCC counterparts in absolute terms. Even with notable growth

over the past decade, the absolute values of the GCC markets, on average, as of 2012, are less

than the corresponding values of the Non-GCC markets at the beginning of the test periods,

i.e. 2003. The implication, with possibly the notable exception of Saudi Arabia, is that GCC

financial sectors lag behind their real sector development. If this group hopes to develop

respectable equity markets and improve their competitiveness, their economies will need to

put the requisite resources into the development of those markets and possibly implement a

variety of capital flows and regulatory/legal reforms in an effort to attract listings/foreign

investors, mobilize capital and reduce perceived risk.

17

2. The market depth testing indicates that the GCC stock markets are relatively thinly

capitalized when compared to their Non-GCC counterparts. This has several significant

effects on financial development. Market depth facilitates liquidity. Liquidity, from a

developed stock market, not only provides a channel for liquidity to stock market investors,

but it also provides liquidity to the banking system and government. Though conventional

banks may not typically be heavily engaged in stock markets, Islamic banks may be more

inclined to do so if they take their profit/loss sharing obligations more seriously in the decade

to come. Equity-based markets, when deemed less volatile/risky, may serve as another

channel for monetary policy as noted by King and Levine (op cit). Moreover, high velocity is

often used as an indicator of the ability to lower transaction costs, including informational

costs and risk. The tests for the differences in means in market depth indicators between the

GCC and Non-GCC markets, indicates that among the 3 indicators, total volume traded

shows statistical significance. Again, this is an indication of the nascent state of development

of the GCC stock markets; and as noted herein above, efforts should be made to bring the

stock market development there “in line” with the development of their real sectors.

3. We conclude that in the area of returns and risks that the GCC metrics may support

investor anecdotal fears that these markets are riskier than their conventional counterparts.

There is a significant statistical difference at 10% between the 2 market groupings as to

volatility measures. This may well be ameliorated by their regulators implementing the

requisite capital flows and market regulation and legal system reforms. While returns

between the 2 groupings do not show statistically significant differences, holding returns

equal, while confronting investors with higher levels of risk, does not bid well for any capital

market. This directly impacts the quality of returns to existing and potential investors.

4. It is clear from the Sharpe and Treynor ratios that there is an investment advantage in

terms of riskiness and risk premiums that the conventional Non-GCC group holds at present.

However, given that returns themselves are fairly comparable, portfolio managers or

individual investors seeking to hedge their conventional equity positions might give ample

thought to the fact that the GCC grouping has a significant diversification advantage over

their Non-GCC counterparts. That is not to say that currency entanglements might dampen

that attractiveness, but the data does support the conclusion that GCC equity holdings have a

portfolio management, diversification advantage over their Non-GCC counterparts, since

correlation testing for market returns between the GCC group and the S&P 500 shows that

there is negative correlation of 0.53; while their Non-GCC counterparts have a positive

correlation of 0.90 with the international markets, as proxied by the S&P 500.

18

REFERENCES

Bekaert, Greet and Harvey, R. (1997). “Capital Markets: an Engine for Economic Growth,”

Cambridge, MA: National Bureau of Economic Research.

Beck, T. a. (2002). “Stock Markets, Banks and Growth: Panel Evidence,” Cambridge, MA:

National Bureau of Economic Research.

Bencivenga, Valerie R., Bruce D. Smith, and Ross M. Starr, “Equity Markets, Transactions

Costs, and Capital Accumulation: An Illustration,” World Bank Economic Review 10

(May 1996), 241-65.

Demirguc-Kunt, A. a. (1999). “Bank-based and Market-Based Financial Systems,”

Washington, DC: World Bank Policy Research Working Paper 2143.

Diamond, Douglas W. "Financial Intermediation and Delegated Monitoring," Review of

Economic Studies 51 (July 1984), 393-414.

Diamond, Douglas W., and R. E. Verrecchia, "Optimal Managerial Contracts and

Equilibrium Security Prices", Journal of Finance 37 (May 1982), 275-87

Glezakos, M., Merika, A., and Kaligosfiris, H. (2007), “Interdependence of Major World Stock Exchanges: How Is the Athens Stock Exchange Affected?” International

Research Journal of Finance and Economics, 7, 24-39.

Greenwood, Jeremy, and Boyan Jovanovic, "Financial Development, Growth, and the

Distribution of Income", Journal of Political Economy 98 (October 1990), 1076-1107

Greenwood, Jeremy, and Bruce Smith, "Financial Markets in Development and the

Development of Financial Markets", Journal of Economic Dynamics and Control 21

(January 1997), 145-82

Hail, Luzi and Christian Leuz, 2006, “Cost of Capital Effects of U.S. Cross-Listings,”

University of Chicago Working Paper.

Jensen, Michael C., and Kevin J. Murphy, "Performance Pay and Top Management

Incentives," Journal of Political Economy 98 (April 1990), 225-64

Kasa, K. (1992), “Common Stochastic Trends in International Stock Markets,” Journal of

Monetary Economics, 29, 95-124

King, R.G. and Levine R, (1993), “Financial Entrepreneurship and Growth,” Journal of

Monetary Economics, 32, 513-542

Lambert, R., C. Leuz, and R. Verrecchia, 2010, “Information Asymmetry, Information

Precision, and the Cost of Capital,” Working Paper, University of Pennsylvania.

19

Levine, Ross. "Stock Markets, Growth, and Tax Policy," Journal of Finance 46 (September

1991), 1445-65.

Levine, Ross. (1997). “Financial Development and Economic Growth: Views and Agenda,”

Journal of Economic Literature, 688-726.

Levine, Ross and Zervos, Sar (1996), “Stock Market Development and Long-Term Growth.”

The World Bank, Policy Research Paper 1582.

Masih, Mansur, Al-Elg, Ali and Madani, Haider (2009), “Causality between Financial

Development and Economic Growth: an Application of Vector Error Correction and

Variance Decomposition Methods to Saudi Arabia,” Applied Economics, 2009, 41,

1691–1699.

Masih, A.M.M. and Masih, R. (1999), “Are Asian Stock Market Fluctuations Due Mainly to Intra-Regional Contagion Effect? Evidence Based on Asian Emerging Stock

Markets,” Pacific Basin Finance Journal, 7, 251-82. OECD, (1992).”Technology and the Economy: the Key Relationships,” Organization for

Economic Cooperation and Development, Paris, 1992.

Patrick, H. (1966). “Financial Development and Economic Growth in Underdeveloped

Countries,” Economic Development and Cultural Change, Vol. 14, No. 2, 174-189.

Purfield, Catriona; Oura, Hiroko; Kramer, Charles and Jobst, Andreas (2006). “Asian Equity

Markets: Growth, Opportunities, and Challenges,” IMF Working Paper 6266.

Rajan, R.G., and L. Zingales (1998), “Financial Dependence and Growth,” American

Economic Review, 88(3), 559-586.

Schumpeter, J. (1934). “The Theory of Economic Development” (Trans. Redvers Opie).

Cambridge, MA: Harvard University Press.

Shultz, Rene M. (1999). “Globalization of Equity Markets and Cost of Capital.” National

Bureau of Economic Research, Working Paper 7021.

Siklos, P. and Ng, P. (2001), “Integration among Asia-Pacific and International Stock Markets: Common Stochastic Trends and Regime Shifts,” Pacific Economic Review,

6, 89-110.

Taylor, M.P. and Tonks, I. (1989), “The Internationalization of Stock Markets and the Abolition of UK Exchange Control,” The Review of Economics and Statistics, 71, 332-36

Yartley, C.A. (2008). “Determinants of Stock Market Development in Emerging Economies:

Is South Africa Different?” IMF Working Paper, WP/08/32

20

Zingales, Luigi. (2006). “Is the U.S. Equity Market Losing Its Competitive Edge?”

University of Chicago, National Bureau of Economic Research (NBER), & CEPR

21

APPENDICES

Appendix A: Market Size

Table A1: Market Size Indicators

2003–2012

Countries Number of Listed

Companies

Market Capitalization (% of

GDP)

Market Capitalization

(USD Billions)

2003

2012

Change

%

2003

2012

Change

%

2003

2012

Change

%

GCC Countries

53.6

106.8 99.25 86.96 53.57 -33.39 54.894 136.04 147.82

Bahrain 42 43 2.38 99.53

59.05 -40.47 0.97 16.1 1559.79

Qatar 29 42 44.83 113.46

73.14 -40.32 26.7

126 371.91

Saudi Arabia 70 158 125.71 73.31

52.51 -20.80 157

373 137.58

U.A.E. 30

102 240 24.42

20.46 -3.96 30.4 68 123.68

Kuwait 97

189 94.85 124.09

62.69 -61.40 59.4 97.1 63.47

Non-GCC

Countries 512.8 521.2 1.64

104.54 98.21 -6.33 173 443.46 156.34

Belgium 250 154 -38.40 55.68

62.03 6.35 174

300 72.41

S.Korea 1563 1767 13.05 51.20

104.50 53.30 330

1180 257.58

Luxembourg 42 29 -30.95 128.10

123.15 -4.95 37.3

70.3 88.47

Norway 158 184 16.46 42.10

50.62 8.52 94.7

253 167.16

Singapore 551 472 -14.34 245.3

150.75 -94.88 229

414 80.79

Table A2: Market Capitalization in USD Billion during the Period

2003-2012

Countries Mean Median Maximum Minimum

Std. Dev.

GCC Countries: 130 127 199 56.7 41.6

Bahrain 18.2 17.3 28.1 9.70 4.98

Qatar 86.4 87.6 126 26.7 33.3

Saudi Arabia 358 333 646 157 136

U.A.E. 76.9 74.2 121 30.4 26.5

Kuwait 110 104 188 59.4 35.9

Non-GCC Countries: 335 356 477 173 102

Belgium 275 271 396 167 76.0

S.Korea 803 836 1180 330 304

Luxembourg 79.5 69.0 166 37.3 37.2

Norway 214 223 357 94.7 78.8

Singapore 304 310 414 180 68.0

22

Table A3: Market Capitalization as a Percentage of GDP during the Period

2003-2012

Countries

Mean

Median

Maximum Minimum

Std. Dev.

GCC Countries: 92.35 86.96 150.75 53.19 31.33

Bahrain 106.35 99.52 152.29 59.05 29.55

Qatar 114.85 101.76 202.87 66.34 44.24

Saudi Arabia 93.14 74.28 196.70 47.39 47.00

U.A.E. 34.24 29.66 64.19 20.46 14.09

Kuwait 113.15 116.69 163.91 62.68 35.46

Non-GCC Countries: 113.95 117.47 163.03 67.17 27.42

Belgium 64.58 57.48 99.06 33.00 20.72

S.Korea 82.26 87.75 107.32 51.20 22.34

Luxembourg 173.45 147.14 323.65 114.22 66.02

Norway 58.30 59.56 90.83 27.74 19.60

Singapore 191.17 198.76 256.38 100.61 56.29

Table A4: Number of Companies Listed during the Period

2003-2012

Countries

Mean

Median

Maximum Minimum

Std. Dev.

GCC Countries: 90 98 110 48 22

Bahrain 45 44 49 42 3

Qatar 35 41 48 0 14

Saudi Arabia 113 119 158 70 34

U.A.E. 83 93 104 30 25

Kuwait 172 185 215 97 42

Non-GCC Countries: 512.8 527 551 508 12

Belgium 183 165 250 153 37

S.Korea 1712 1767 1792 1563 93

Luxembourg 35 34 42 29 4

Norway 189 192 209 158 16

Singapore 510 467 685 455 82

23

Table A5: Test of the Difference in Mean for Market Size between Pairs of Countries

2002-2012

Pair of Countries

Mean

(GCC)

Mean

(Non-GCC)

Difference

in Mean

P value

Market Capitalization (USD Billions)

Qatar, Luxembourg 86.40 79.50 6.90 0.5313

U.A.E, Norway 76.90 214.00 -140.00 *0.0000

Kuwait, Belgium 110.00 275.00 -170.00 *0.0000

Saudi A, South Korea 358.00 803.00 -450.00 *0.0000

Bahrain, Singapore 18.20 304.00 -290.00 *0.0000

Market Capitalization (% of GDP)

Qatar, Luxembourg 93.15 173.46 -80.31 *0.0041

U.A.E, Norway 34.25 58.30 -24.06 *0.0009

Kuwait, Belgium 113.15 64.59 48.57 *0.0034

Saudi A, South Korea 114.85 82.26 32.59 0.5068

Bahrain, Singapore 106.35 191.18 -84.82 *0.0000

Number of Listed Companies Qatar, Luxembourg 35 35 0 0.9462

U.A.E, Norway 83 189 -106 *0.0000

Kuwait, Belgium 172 183 -11 0.4080

Saudi A, South Korea 113 1712 -1599 *0.0000

Bahrain, Singapore 45 510 -465 *0.0000

*Significant at 5% .

24

Table A6: Test of the Difference in Mean for Market Size within GCC Countries

2003-2012

Pair of Countries Mean (First country)

Mean (Second country)

Difference in Mean

P value

Market Capitalization (USD Billions)

Qatar, U.A.E 86.40 76.90 9.50 0.393

Qatar, Kuwait 86.40 110.00 -24.00 **0.052

Qatar, Saudi A 86.40 358.00 -270.00 *0.000

Qatar, Bahrain 86.40 18.20 68.20 *0.000

U.A.E, Kuwait 76.90 110.00 -33.00 *0.003

U.A.E, Saudi A 76.90 358.00 -280.00 *0.000

U.A.E, Bahrain 76.90 18.20 58.70 *0.000

Saudi A, Kuwait 358.00 110.00 248.00 *0.000

Saudi A, Bahrain 358.00 18.20 340.00 *0.000

Kuwait, Bahrain 110.00 18.20 91.80 *0.000

Market Capitalization (% of GDP)

Qatar, U.A.E 93.15 34.25 58.90 *0.001

Qatar, Kuwait 93.15 113.15 -20.00 0.911

Qatar, Saudi A 93.15 114.85 -21.70 0.999

Qatar, Bahrain 93.15 106.35 -13.20 0.580

U.A.E, Kuwait 34.25 113.15 -78.90 *0.000

U.A.E, Saudi A 34.25 114.85 -80.61 *0.000

U.A.E, Bahrain 34.25 106.35 -72.10 *0.000

Saudi A, Kuwait 114.85 113.15 1.70 0.238

Saudi A, Bahrain 114.85 106.35 8.50 0.424

Kuwait, Bahrain 113.15 106.35 6.80 0.581

Number of Listed Companies

Qatar, U.A.E 35 83 -48 *0.000

Qatar, Kuwait 35 172 -137 *0.000

Qatar, Saudi A 35 113 -78 *0.000

Qatar, Bahrain 35 45 -10 **0.052

U.A.E, Kuwait 83 172 -89 *0.000

U.A.E, Saudi A 83 113 -30 *0.004

U.A.E, Bahrain 83 45 38 *0.001

Saudi A, Kuwait 113 172 -59 *0.000

Saudi A, Bahrain 113 45 68 *0.000

Kuwait, Bahrain 172 45 127 *0.000

*Significant at 5% .

**Significant at 10% .

25

Table A7: Test of the Difference in Mean for Market Size within Non-GCC Countries

2003-2012

Pair of Countries Mean

(First country)

Mean

(Second country)

Difference

in Mean

P value

Market Capitalization (USD Billions)

Luxembourg, Norway 79.50 214.00 -130.00 *0.000

Luxembourg, Belgium 79.50 275.00 -200.00 *0.000

Luxembourg, South Korea 79.50 803.00 -720.00 *0.000

Luxembourg, Singapore 79.50 304.00 -220.00 *0.000

Norway, Belgium 214.00 275.00 -61.00 *0.037

Norway, South Korea 214.00 803.00 -590.00 *0.000

Norway, Singapore 214.00 304.00 -90.00 *0.000

Belgium, Singapore 275.00 304.00 -29.00 0.252

Belgium, South Korea 275.00 803.00 -530.00 *0.000

South Korea, Singapore 803.00 304.00 499.00 *0.001

Market Capitalization (% of GDP)

Luxembourg, Norway 173.46 58.30 115.16 *0.001

Luxembourg, Belgium 173.46 64.59 108.87 *0.001

Luxembourg, South Korea 173.46 82.26 91.20 *0.003

Luxembourg, Singapore 173.46 191.18 -17.72 0.444

Norway, Belgium 58.30 64.59 -6.28 0.364

Norway, South Korea 58.30 82.26 -23.96 *0.006

Norway, Singapore 58.30 191.18 -132.87 *0.000

Belgium, Singapore 64.59 191.18 -126.59 *0.000

Belgium, South Korea 64.59 82.26 -17.68 *0.034

South Korea, Singapore 82.26 191.18 -108.92 *0.000

Number of Listed Companies Luxembourg, Norway 35 189 -154 *0.000

Luxembourg, Belgium 35 183 -148 *0.000

Luxembourg, South Korea 35 1712 -1677 *0.000

Luxembourg, Singapore 35 510 -475 *0.000

Norway, Belgium 189 183 6 0.287

Norway, South Korea 189 1712 -1523 *0.000

Norway, Singapore 189 510 -321 *0.000

Belgium, Singapore 183 510 -327 *0.000

Belgium, South Korea 183 1712 -1529 *0.000

South Korea, Singapore 1712 510 1202 *0.000

*Significant at 5% .

26

Appendix B: Market Depth

Table B1: Market Depth Indicators

2003–2012

Countries Total Volume Traded

(USD Billions)

Total Volume Traded

(% of GDP)

Trading Velocity

2003

2012

Change% 2003

2012

Change% 2003

2012

Change%

GCC

Countries: 48.22 114.14 136.68 50.61 20.93 -29.69 60.26 41.41 -18.85

Bahrain 0.27 0.31 12.80 2.81

0.96 -1.85 3.30 1.86 -1.45

Qatar 28.06 15.32 -45.40 65.19 13.49 -51.70 40.00 12.17 -27.83

Saudi Arabia 159.06 514.42 223.42 74.13 72.35 -1.78 137.03 144.45 7.42

U.A.E. 1.00 17.64 1657.59 0.81 4.54 3.73 3.96 25.34 21.38

Kuwait 52.73 23.00 -56.38 110.14 13.30 -96.84 117.03 23.23 -93.79

Non-GCC

Countries: 176.69 381.31 115.80 49.17 47.82 -1.35 80.87 55.59 -25.28

Belgium 42.67 103.26 142.03 13.69 21.35 7.66 28.34 38.97 10.63

Korea 682.71 1513.84 121.74 106.05 134.02 27.97 235.72 139.22 -96.50

Luxembourg 0.26 0.12 -55.25 0.89 0.20 -0.68 0.83 0.17 -0.66

Norway 69.97 132.88 89.90 31.12 26.59 -4.52 86.40 56.28 -30.12

Singapore 87.86 156.45 78.05 94.11 56.95 -37.16 53.05 43.31 -9.74

Table B2: Total Volume Traded (USD Billions) during the Period

2003-2012

Countries

Mean Median Maximum Minimum Std. Dev.

GCC countries: 145.00 110.00 319.00 42.60 93.20

Bahrain 0.92 0.56 2.96 0.27 0.87

Qatar 20.90 21.80 48.20 - 14.20

Saudi Arabia 569.00 494.00 1,400.00 159.00 400.00

U.A.E. 68.30 46.60 150.00 1.00 63.10

Kuwait 65.10 54.30 123.00 21.40 36.50

Non-GCC countries: 397.00 425.00 617.00 177.00 138.00

Belgium 133.00 119.00 256.00 42.70 62.70

South Korea 1,410.00 1,490.00 2,030.00 639.00 468.00

Luxembourg 0.37 0.24 1.66 0.12 0.46

Norway 240.00 213.00 472.00 70.00 124.00

Singapore 207.00 218.00 384.00 81.30 97.80

27

Table B3: Total Volume Traded (% of GDP) during the Period

2003-2012

Countries Mean Median Maximum Minimum Std. Dev.

GCC countries: 58.12 54.26 120.41 15.21 35.99

Bahrain 5.51 4.44 13.51 0.96 4.17

Qatar 25.89 26.14 65.19 0.00 21.29

Saudi Arabia 154.49 100.95 372.25 38.57 123.51

U.A.E. 30.73 24.31 79.24 0.81 28.70

Kuwait 74.00 81.79 116.35 13.30 35.11

Non-GCC countries: 75.43 73.17 118.38 47.63 21.38

Belgium 31.07 27.00 55.63 13.69 13.16

S.Korea 150.62 157.40 189.61 88.49 35.51

Luxembourg 0.85 0.54 3.03 0.21 0.86

Norway 67.88 64.06 119.93 31.12 28.87

Singapore 126.74 129.90 227.75 74.37 44.85

Table B4: Trading Velocity during the Period

2003-2012

Countries

Mean Median Maximum Minimum Std. Dev.

GCC countries: 67.74 74.32 107.52 29.09 31.08

Bahrain 5.00 4.55 12.00 1.48 3.63

Qatar 30.12 29.35 56.13 12.17 14.46

Saudi Arabia 153.53 141.14 288.40 60.46 74.91

U.A.E. 94.15 101.55 166.97 21.32 60.64

Kuwait 55.88 56.01 94.27 19.41 28.40

Non-GCC countries: 87.50 84.48 108.13 55.59 17.95

Belgium 52.32 46.61 76.48 38.97 13.37

S.Korea 188.25 188.16 237.62 139.22 29.76

Luxembourg 0.40 0.25 1.42 0.15 0.43

Norway 117.77 128.76 152.38 56.28 35.70

Singapore 78.74 78.85 122.01 40.37 29.29

28

Table B5: Test of the Difference in Mean for Market Depth Between Pairs of Countries

2003-2012

Pair of Countries

Mean

(First country)

Mean

(Second country)

Difference

in Mean

P value

Trading Velocity

Qatar, Luxembourg 30.12 0.40 29.72 *0.0007

U.A.E, Norway 94.15 117.77 -23.63 0.3069

Kuwait, Belgium 55.88 52.32 3.56 0.7336

Saudi A, South Korea 153.53 188.25 -34.71 0.2313

Bahrain, Singapore 5.00 78.74 -73.74 *0.0000

Total Volume Traded (USD Billions) Qatar, Luxembourg 20.90 0.37 20.50 *0.0013

U.A.E, Norway 68.30 240.00 -170.00 *0.0000

Kuwait, Belgium 65.10 133.00 -68.00 *0.0002

Saudi A, South Korea 569.00 1,410.00 -840.00 *0.0001

Bahrain, Singapore 0.92 207.00 -210.00 *0.0000

Total Volume Traded (% of GDP) Qatar, Luxembourg 25.89 0.85 25.03 *0.0078

U.A.E, Norway 30.73 67.88 -37.15 *0.0047

Kuwait, Belgium 74.00 31.07 42.92 *0.0063

Saudi A, South Korea 154.49 150.62 3.87 0.9273

Bahrain, Singapore 5.51 126.74 -121.23 *0.0000

*Signi ficant at 5% .

29

Table B6: Test of the Difference in Mean for Market Depth within GCC Countries

2003-2012

Pair of Countries Mean

(First country)

Mean

(Second country)

Difference

in Mean

P value

Trading Velocity

Qatar, U.A.E 30.12 94.15 -64.02 *0.000

Qatar, Kuwait 30.12 55.88 -25.75 *0.002

Qatar, Saudi A 30.12 153.53 -123.41 *0.000

Qatar, Bahrain 30.12 5.00 25.12 *0.002

U.A.E, Kuwait 94.15 55.88 38.27 0.117

U.A.E, Saudi A 94.15 153.53 -59.39 *0.028

U.A.E, Bahrain 94.15 5.00 89.14 *0.004

Saudi A, Kuwait 153.53 55.88 97.65 *0.008

Saudi A, Bahrain 153.53 5.00 148.53 *0.001

Kuwait, Bahrain 55.88 5.00 50.88 *0.002

Total Volume Traded (USD Billions) Qatar, U.A.E 20.90 68.30 -47.00 *0.000

Qatar, Kuwait 20.90 65.10 -44.00 *0.000

Qatar, Saudi A 20.90 569.00 -550.00 *0.000

Qatar, Bahrain 20.90 0.92 20.00 *0.002

U.A.E, Kuwait 68.30 65.10 3.20 0.874

U.A.E, Saudi A 68.30 569.00 -500.00 *0.000

U.A.E, Bahrain 68.30 0.92 67.40 *0.008

Saudi A, Kuwait 569.00 65.10 504.00 *0.003

Saudi A, Bahrain 569.00 0.92 568.00 *0.002

Kuwait, Bahrain 65.10 0.92 64.20 *0.000

Total Volume Traded (% of GDP) Qatar, U.A.E 25.89 30.73 -4.85 0.514

Qatar, Kuwait 25.89 74.00 -48.11 *0.000

Qatar, Saudi A 25.89 154.49 -128.61 *0.000

Qatar, Bahrain 25.89 5.51 20.37 *0.021

U.A.E, Kuwait 30.73 74.00 -43.26 *0.002

U.A.E, Saudi A 30.73 154.49 -123.76 *0.000

U.A.E, Bahrain 30.73 5.51 25.22 *0.030

Saudi A, Kuwait 154.49 74.00 80.49 **0.086

Saudi A, Bahrain 154.49 5.51 148.98 *0.007

Kuwait, Bahrain 74.00 5.51 68.48 *0.000

*Significant at 5% . **Significant at 10% .

30

Table B7: Test of the Difference in Mean for Market Depth within Non-GCC Countries

2003-2012

Pair of Countries Mean

(First country)

Mean

(Second country)

Difference

in Mean

P value

Trading Velocity

Luxembourg, Norway 0.40 117.77 -117.37 *0.000

Luxembourg, Belgium 0.40 52.32 -51.92 *0.000

Luxembourg, South Korea 0.40 188.25 -187.84 *0.000

Luxembourg, Singapore 0.40 78.74 -78.34 *0.000

Norway, Belgium 117.77 52.32 65.45 *0.001

Norway, South Korea 117.77 188.25 -70.48 *0.001

Norway, Singapore 117.77 78.74 39.03 *0.018

Belgium, Singapore 52.32 78.74 -26.42 *0.001

Belgium, South Korea 52.32 52.32 -135.93 0.999

South Korea, Singapore 188.25 78.74 109.51 *0.000

Total Volume Traded (USD Billions) Luxembourg, Norway 0.37 240.00 -240.00 *0.000

Luxembourg, Belgium 0.37 133.00 -130.00 *0.000

Luxembourg, South Korea 0.37 1,410.00 -1,400.00 *0.000

Luxembourg, Singapore 0.37 207.00 -210.00 *0.000

Norway, Belgium 240.00 133.00 107.00 *0.023

Norway, South Korea 240.00 1,410.00 -1,200.00 *0.000

Norway, Singapore 240.00 207.00 33.00 0.424

Belgium, Singapore 133.00 207.00 -74.00 *0.005

Belgium, South Korea 133.00 1,410.00 -1,300.00 *0.000

South Korea, Singapore 1,410.00 207.00 1,200.00 *0.000

Total Volume Traded (% of GDP) Luxembourg, Norway 0.85 67.88 -67.03 *0.000

Luxembourg, Belgium 0.85 31.07 -30.22 *0.000

Luxembourg, South Korea 0.85 150.62 -149.76 *0.000

Luxembourg, Singapore 0.85 126.74 -125.89 *0.000

Norway, Belgium 67.88 31.07 36.81 *0.005

Norway, South Korea 67.88 150.62 -82.74 *0.000

Norway, Singapore 67.88 126.74 -58.86 *0.000

Belgium, Singapore 31.07 126.74 -95.67 *0.000

Belgium, South Korea 31.07 150.62 -119.55 *0.000

South Korea, Singapore 150.62 126.74 23.87 **0.078

*Significant at 5% . **Significant at 10% .

31

Appendix C: Market Returns and Volatility

Table C1: Percentage Index Return and its Volatility during the Period

2003-2012

Countries Panel A: Percentage Index Returns Panel B:

Volatility of returns

(Std. Dev.)

2007

2008

2009 2010

2011

2012 Change

%

GCC Countries: -28.12 39.62 5.54 13.81 -10.55 3.86 31.98 22.85

Bahrain -2.24 34.99 -19.97 9.97 -14.37 -4.47 -2.23 19.75

Qatar -40.33 35.44 5.06 27.74 3.34 -1.86

38.47 26.64

Saudi Arabia -48.86 35.57 28.45 9.02 -3.90 4.39 53.24 29.92

U.A.E. -44.59

52.13 24.57 -6.79 -16.48 24.22 68.80 34.73

Kuwait -4.59

39.94 -10.41

29.12 -21.36

-2.99 1.60 24.04

Non-GCC

Countries: 23.66 -60.89 73.32 10.91 -19.92 19.60

-4.05 45.12

Belgium -3.13 -65.57 54.47 0.50 -15.06 33.32

36.45 41.49

Korea 27.66 -55.62 67.25 25.26 -10.90 18.88

-8.79 41.51

Luxembourg 41.87 -64.26 76.73 -3.34 -34.45 0.55

-41.32 50.83

Norway 25.90 -66.07 91.41 13.69 -18.06 16.37

-9.53 51.97

Singapore 25.97 -52.95 76.75 18.44 -21.15 28.89 2.91 44.78

Table C2: Percentage Index Return Descriptive Statistics during the Period

2003-2012

Countries Mean Median Maximum Minimum

Std. Dev.

GCC countries: 4.03 4.70 39.62 -28.12 22.85

Bahrain 0.65 -3.36 34.99 -19.97 19.76

Qatar 4.90 4.20 35.44 -40.33 26.64

Saudi Arabia 4.11 6.71 35.57 -48.86 29.92

U.A.E. 5.51 8.71 52.13 -44.59 34.73

Kuwait 4.95 -3.79 39.94 -21.36 24.04

Non-GCC countries: 7.78 15.26 73.32 -60.89 45.12

Belgium 0.75 -1.31 54.47 -65.57 41.50

Korea 12.09 22.07 67.25 -55.62 41.51

Luxembourg 2.85 -1.40 76.73 -64.26 50.83

Norway 10.54 15.03 91.41 -66.07 51.97

Singapore 12.66 22.20 76.75 -52.95 44.79

32

Table C3: Test of the Difference in Mean for Market Returns and Volatility between Pairs of Countries

2003-2012

Pair of Countries

Mean

(GCC)

Mean

(Non- GCC)

Difference

in Mean

P value

Percentage index returns

Qatar, Luxembourg 4.90 2.85 2.05 0.86

U.A.E, Norway 5.51 10.54 -5.03 0.74

Kuwait, Belgium 4.96 0.76 4.20 0.69

Saudi A, South Korea 4.11 12.09 -7.98 0.54

Bahrain, Singapore 0.65 12.66 -12.01 0.20

Volatility of returns (Std. Dev.)

Qatar, Luxembourg 26.64 50.83 -24.19 **0.073

U.A.E, Norway 34.73 51.97 -17.24 0.184

Kuwait, Belgium 24.04 41.49 -17.45 0.109

Saudi A, South Korea 29.92 41.51 -11.59 0.238

Bahrain, Singapore 19.75 44.78 -25.03 *0.035

*Significant at 5%.

**Significant at 10%.

Table C4: Test of the Difference in Mean for Market Returns and Volatility within GCC Countries

2003-2012

Pair of Countries Mean

(First country)

Mean

(Second country)

Difference

in Mean

P value

Percentage index returns

Qatar, U.A.E 4.90 5.51 -0.61 0.957

Qatar, Kuwait 4.90 4.95 -0.06 0.996

Qatar, Saudi A 4.90 4.11 0.79 0.945

Qatar, Bahrain 4.90 0.65 4.25 0.712

U.A.E, Kuwait 5.51 4.95 0.56 0.969

U.A.E, Saudi A 5.51 4.11 1.40 0.925

U.A.E, Bahrain 5.51 0.65 4.86 0.746

Saudi A, Kuwait 4.11 4.95 -0.84 0.948

Saudi A, Bahrain 4.11 0.65 3.46 0.788

Kuwait, Bahrain 4.95 0.65 4.30 0.679

Volatility of returns (Std. Dev.)

Qatar, U.A.E 26.64 34.73 -8.09 0.291

Qatar, Kuwait 26.64 24.04 2.6 0.293

Qatar, Saudi A 26.64 29.92 -3.28 0.446

Qatar, Bahrain 26.64 19.75 6.89 0.105

U.A.E, Kuwait 34.73 24.04 10.69 **0.064

U.A.E, Saudi A 34.73 29.92 4.81 0.241

U.A.E, Bahrain 34.73 19.75 14.98 *0.009

Saudi A, Kuwait 29.92 24.04 5.88 0.171

Saudi A, Bahrain 29.92 19.75 10.17 *0.043

Kuwait, Bahrain 24.04 19.75 4.29 0.192

*Significant at 5% . **Significant at 10% .

33

Table C5: Test of the Difference in Mean for Market Returns and Volatility within Non-GCC Countries

2003-2012

Pair of Countries Mean (First country)

Mean (Second country)

Difference in Mean

P value

Percentage index returns

Luxembourg, Norway 2.85 10.54 -7.69 0.726

Luxembourg, Belgium 2.85 0.75 2.10 0.923

Luxembourg, South Korea 2.85 12.09 -9.24 0.675

Luxembourg, Singapore 2.85 12.66 -9.81 0.656

Norway, Belgium 10.54 0.75 9.79 0.664

Norway, South Korea 10.54 12.09 -1.55 0.945

Norway, Singapore 10.54 12.66 -2.12 0.924

Belgium, Singapore 0.75 12.66 -11.90 0.514

Belgium, South Korea 0.75 12.09 -11.33 0.533

South Korea, Singapore 12.09 12.66 -0.57 0.974

Volatility of returns (Std. Dev.) Luxembourg, Norway 50.83 51.97 -1.14 0.443

Luxembourg, Belgium 50.83 41.49 9.34 0.186

Luxembourg, South Korea 50.83 41.51 9.32 0.186

Luxembourg, Singapore 50.83 44.78 6.05 0.266

Norway, Belgium 51.97 41.49 10.48 0.165

Norway, South Korea 51.97 41.51 10.46 0.165

Norway, Singapore 51.97 44.78 7.19 0.241

Belgium, Singapore 41.49 44.78 -3.29 0.492

Belgium, South Korea 41.49 41.51 -0.02 0.416

South Korea, Singapore 41.51 44.78 -3.27 0.493

34

Appendix D-Figures

Figure 1: Market Size Indicators

2003-2012

0 100 200 300 400 500 600 700 800 900

BAHRAIN

BELGIUM

EMIRATES

GCC

KOREA

KUWAIT

LUXEMBOURG

NONGCC

NORWAY

QATAR

SAUDI

SINGAPORE

Total Market Capitalization in Billions of US$, 2003

0 200 400 600 800 1,000 1,200 1,400 1,600 1,800 2,000 2,200 2,400

BAHRAIN

BELGIUM

EMIRATES

GCC

KOREA

KUWAIT

LUXEMBOURG

NONGCC

NORWAY

QATAR

SAUDI

SINGAPORE

Total Market Capitalization in Billions US$, 2012

0

100

200

300

400

500

600

BAHRAIN

BELG

IUM

EMIR

ATES

GCC

KOREA

KUW

AIT

LUXEM

BOURG

NONGCC

NORW

AY

QATA

R

SAUDI

SING

APORE

Total Market Capitalization as Percentage of GDP,2003

0

100

200

300

400

500

BAHRAIN

BELG

IUM

EM

IRATE

SGCC

KOREA

KUW

AIT

LUXEM

BOURG

NONGCC

NORW

AY

QATA

R

SAUDI

SIN

GAPORE

Total Market Capitalization as Percentage of GDO,2012

0

500

1,000

1,500

2,000

2,500

3,000

BAHRAIN

BELGIU

M

EMIR

ATESG

CC

KOREA

KUW

AIT

LUXEM

BOURG

NONGCC

NORW

AY

QATAR

SAUDI

SING

APORE

Number of Companies Listed,2003

0

400

800

1,200

1,600

2,000

GCC

BAHRAIN

BELG

IUM

EM

IRATE

S

KOREA

KUW

AIT

LUXEM

BOURG

NONGCC

NORW

AY

QATA

R

SAUDI

SIN

GAPORE

Number of Companies Listed, 2012

35

Figure 2: Market Depth Indicators

2003-2012

0

100

200

300

400

500

600

700

800

900

BAHRAIN

BELG

IUM

EMIR

ATES

GCC

KOREA

KUW

AIT

LUXEM

BOURG

NONGCC

NORW

AY

QATA

R

SAUDI

SINGAPORE

Total Volume Traded in Billions US$, 2003

0

400

800

1,200

1,600

2,000

BAHRAIN

BELG

IUM

EMIR

ATES

GCC

KOREA

KUW

AIT

LUXEM

BOURG

NONGCC

NORW

AY

QATA

R

SAUDI

SINGAP

ORE

Total Volume Traded in Billions US$, 2012

0

50

100

150

200

250

BAHRAIN

BELG

IUM

EM

IRATES

GCC

KOREA

KUW

AIT

LUXEM

BOURG

NONGCC

NORW

AY

QATA

R

SAUDI

SIN

GAPORE

Total Volume Traded as Percentage of GDP,2003

0

40

80

120

160

200

240

280

320

360

BAHRAIN

BELG

IUM

EM

IRATE

SGCC

KOREA

KUW

AIT

LUXEM

BOURG

NONGCC

NORW

AY

QATA

R

SAUDI

SIN

GAPORE

Total Volume Traded as Percentage of GDP, 2012

0

100

200

300

400

500

600

BAHRAIN

BELG

IUM

EM

IRATE

SGCC

KOREA

KUW

AIT

LUXEM

BOURG

NORW

AY

NONGCC

QATA

R

SAUDI

SIN

GAPORE

Trading Velocity, 2003

0

50

100

150

200

250

300

BAHRAIN

BELG

IUM

EM

IRATE

SGCC

KOREA

KUW

AIT

LUXEM

BOURG

NORW

AY

NONGCC

QATA

R

SAUDI

SIN

GAPORE

Trading Velocity, 2012

36

Figure 3: Weakly S&P Index for The Period 2007- 2012

-200

0

200

400

600

800

1,000

1,200

1,400

2007 2008 2009 2010 2011 2012

BAHRAIN BELGIUMUAE SOUTH KOREA

KUWAIT LUXEMBOURG

NORWAY QATAR

SAUDI ARABIA SINGAPORE

37

Figure 4: Nominal GDP in Billions of US$ for The Selected Countries

0

200

400

600

800

1,000

1,200

1,400

BELG

IUM

KUW

AIT

KOREA

NORW

AY

QATAR

SAUDI

SIN

GAPORE

EMIR

ATES

LUXEMBOURG

GCC

NONGCC

Nominal GDP in Billiions of US$, 2003

0

500

1,000

1,500

2,000

2,500

BELG

IUM

KUW

AIT

KOREA

NORW

AY

QATAR

SAUDI

SIN

GAPORE

EMIR

ATES

LUXEMBOURG

GCC

NONGCC

Nominal GDP in Billions of US$, 2012