VitalSync EMR Connectivity and Remote Continuous Patient Monitoring Software

Upload

frost-sullivanCategory

view

3.237download

3

Remote Patient Monitoring Market in Europe Witnessing a High Growth Trajectory

Somsainathan C K, Research Associate Patient MonitoringHealthcare EMEAJuly 1, 2010

2

Agenda

Market Overview1

Trends in Remote Patient Monitoring2

Geographic Analysis3

Market Analysis4

Technology Trends5

Market Drivers and Restraints6

Industry Challenges7

Opportunities to capitalize8

Recommendations9

3

Market Overview

�Remote patient monitoring in Europe in 2009 was dominated by UK with 25% market share and Germany with 21%. Other prominent markets include France, Italy and Benelux.

�The scenario is likely to remain the same throughout the forecast period, with no major change in each country’s market share in the region.

Geographic ScopeMarket segmentation

Telehealth provides remote

monitoring of a patient's vital

signs through the use of devices

customized by healthcare service

providers. Vital signs data, such

as blood pressure levels, are

transmitted to a response center

or the clinician's computer where

it will be monitored and

interpreted according to the

individual's health requirements.

Telehealth provides remote

monitoring of a patient's vital

signs through the use of devices

customized by healthcare service

providers. Vital signs data, such

as blood pressure levels, are

transmitted to a response center

or the clinician's computer where

it will be monitored and

interpreted according to the

individual's health requirements.

Telecare provides real time

monitoring of emergencies

and social care directly to the

user, in their homes, with

support from information and

communication technology.

Telecare is provided through

an integration of wide range

of equipment and services

tailored to the needs of

customers.

Telecare provides real time

monitoring of emergencies

and social care directly to the

user, in their homes, with

support from information and

communication technology.

Telecare is provided through

an integration of wide range

of equipment and services

tailored to the needs of

customers.

United

Kingdom

RPM

Germany

France

Spain

Italy

Scandinavia

Benelux

4

Trends in Remote Patient Monitoring

Intensity of Rivalry

Medium

Bargaining Power

of Customers

Medium

Bargaining Power

of Suppliers

Low

Threat of New Entrants

Medium

Threat of Substitutes

Low

SocietyLegislation

Political

Economic

Technology

Environment

0

2.5

5

7.5

10

Tier I includes companies such as Philips, Biotronik, and Tunstall etc. These are companies who are the biggest

market share holders in the European RPM market. They serve all the countries in the region, and have a vast

product portfolio with huge clientele from service providers to healthcare institutes involved in RPM.

Tier II comprises of companies such as Bosch, Aerotel, Vivatec, Fold Telecare, Initial Attendo etc. These have a

significant market share in the region, but their prominence is limited to few countries in the region. This group of

companies, which are highly competitive.

Tier III includes Card Guard, TBS GB, RSL Steeper, BodyTel Scientific Inc etc. This group of companies are mostly

small in terms of revenue earned from RPM. Their core focus areas may not be RPM and are present in limited

countries. Their market share is also not significant.

5

Geographic Analysis

Long Term

Long TermShort Term

UK

Germany

France

Italy

Spain

Scandinavia

Benelux

Market prospects in long term and short term

0

50

100

150

200

250

300

350

UK Germany France Italy Spain Scandinavia Benelux Total

25%

21%

15%

15%6%

7%

11%� Remote patient monitoring in Europe in

2009 was dominated by UK with 25% market

share and Germany with 21%.

� Other prominent markets include France,

Italy and Benelux.

� UK dominated the remote patient

monitoring market in Europe with relatively

high adoption rates for telecare and telehealth

solutions.

� The scenario is likely to remain the same

throughout the forecast period, with no major

change in each country’s market share in the

region.

Factors that make a country or its market attractive

are the government spending and the public

willingness and receptivity towards technological

advancement.

UK and Germany are investing into such technology

and are leading markets. France and Italy are big

markets in terms of ageing population that demand

such services.

Source: Frost & Sullivan

6

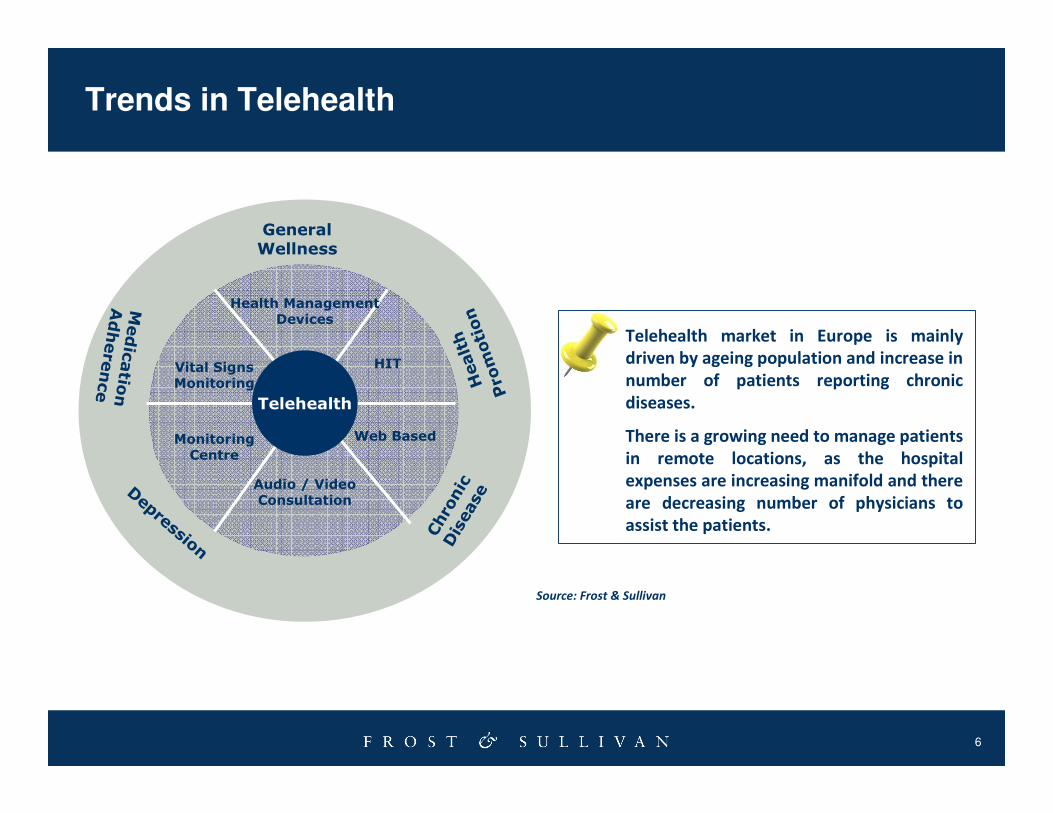

Trends in Telehealth

Telehealth market in Europe is mainly

driven by ageing population and increase in

number of patients reporting chronic

diseases.

There is a growing need to manage patients

in remote locations, as the hospital

expenses are increasing manifold and there

are decreasing number of physicians to

assist the patients.

Health Management Devices

Audio / Video Consultation

Web Based

HIT

Monitoring Centre

Vital Signs Monitoring

Telehealth

Depression

Chronic

Disease

Health

Promotion

Medication

Adherence

General Wellness

Source: Frost & Sullivan

7

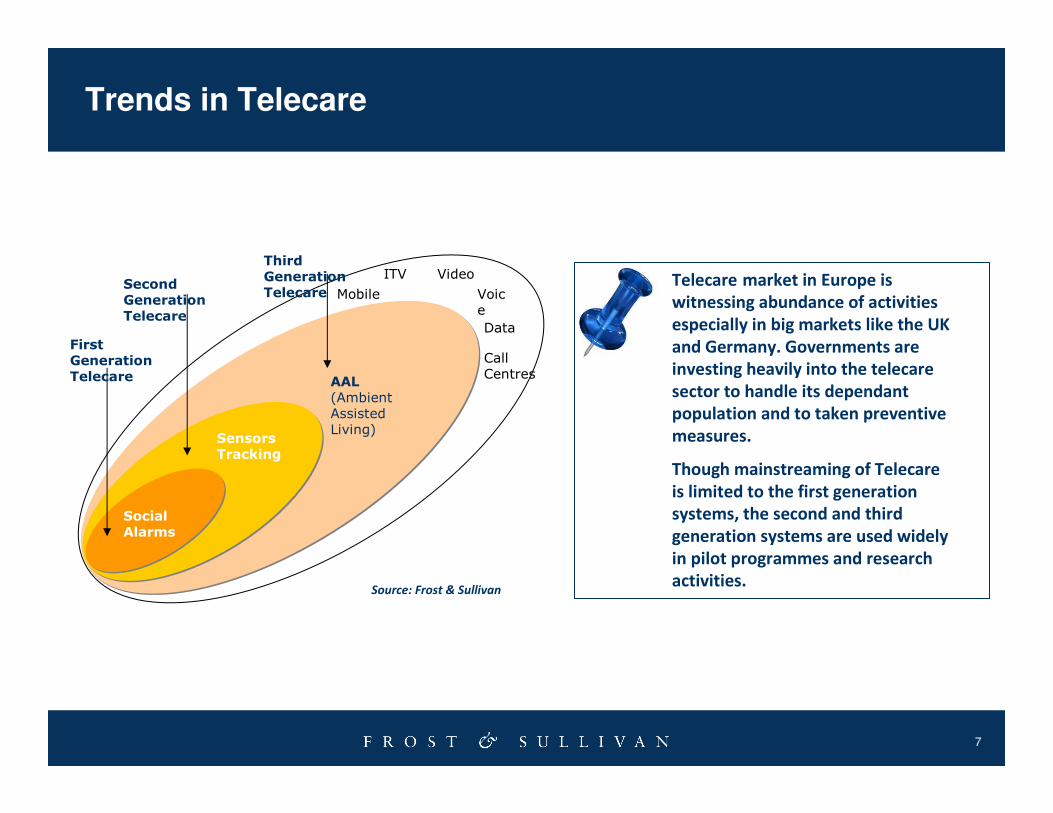

Trends in Telecare

Source: Frost & Sullivan

First Generation Telecare

Social Alarms

Second Generation Telecare

Sensors Tracking

Third Generation Telecare

AAL (Ambient Assisted Living)

Mobile

ITV Video

Voice

Data

Call Centres

Telecare market in Europe is

witnessing abundance of activities

especially in big markets like the UK

and Germany. Governments are

investing heavily into the telecare

sector to handle its dependant

population and to taken preventive

measures.

Though mainstreaming of Telecare

is limited to the first generation

systems, the second and third

generation systems are used widely

in pilot programmes and research

activities.

8

Revenue Forecast

Remote patient monitoring market in Europe registered revenues of $ 325.0 million in 2009 and is expected to

double its annual revenues by 2015. The market is expected to witness a CAGR of 12.2% during the forecast period

between 2010 to 2015. However the market was growing at the 10.0% in the period between 2006 and 2009. The

major factors that expected to drive the market are growing awareness, customization of products and services to

suit the end-user’s needs and the government initiatives and funding.

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

2007 2008 2009 2010 2011 2012 2013 2014 2015

Revenue Growth

Rate (%)

Growing awareness

Customization of

products and services

Government initiatives

and funding

Factors contributing to

growth

Source: Frost & Sullivan

9

Market Drivers and Restraints

� Ageing Population - Demographic Ageing a priority under Europe 2020

� Need for continuous care becoming a priority among the aged and the healthcare service providers

� Deployment of various European Programmes for assisted living, improving the investments and

funding into Telecare market

� Governments in Europe adopting various support structures such as Telecare Learning & Improvement

Network increases the visibility of Telecare.

� Increasing demand due increase in chronic illnesses.

� Shortage of specialists in hospitals who can dedicate their time to individual patients.

� Increasing hospital expenses, forcing patient’s to switch to affordable remote monitoring options.

� Geographical disparities in availability of services in some countries

� Unclear and varying perceptions about the value of Telecare within social care.

� Interoperability issues due to limited infrastructural readiness in certain countries. This influences the

slow adoption of advanced solutions.

� Lack of common European standards making the regulatory environment unfavorable for growth.

� High costs involved in deployment of telehealth systems are curbing wider adoption rate and the

growth rate.

� Lack of information on funding/ reimbursement practices deter many potential users from adopting this

system.

10

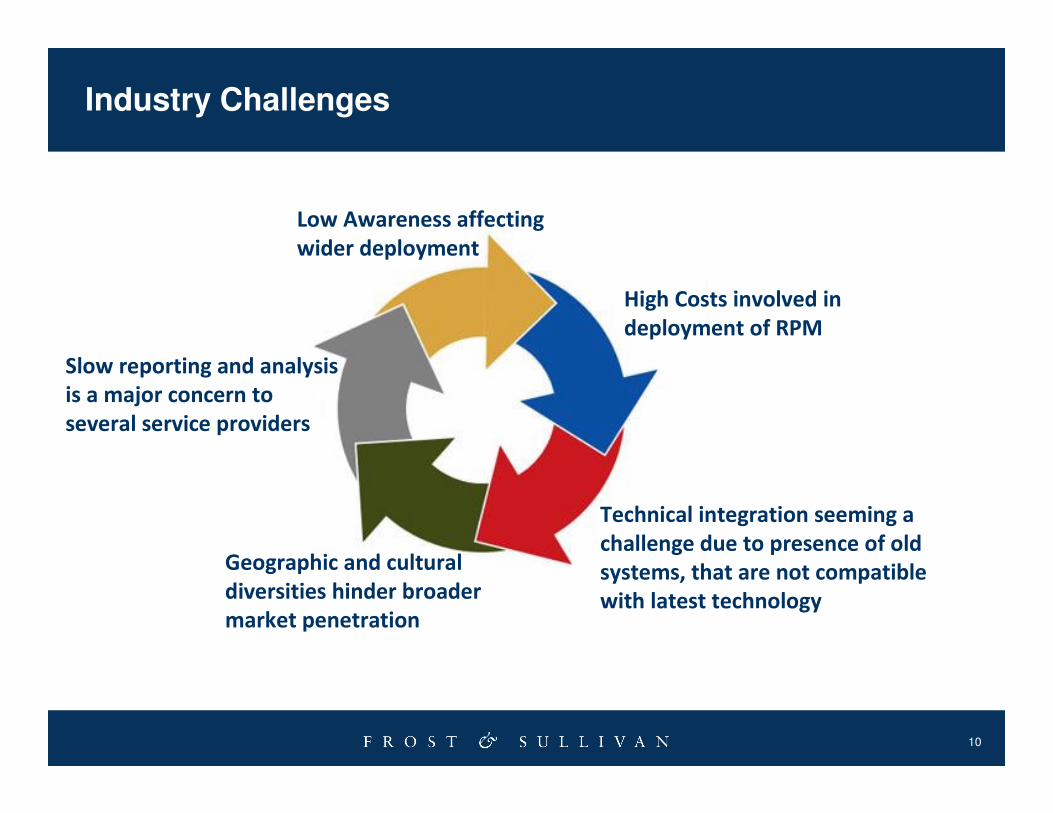

Industry Challenges

Low Awareness affecting

wider deployment

High Costs involved in

deployment of RPM

Technical integration seeming a

challenge due to presence of old

systems, that are not compatible

with latest technology

Geographic and cultural

diversities hinder broader

market penetration

Slow reporting and analysis

is a major concern to

several service providers

11

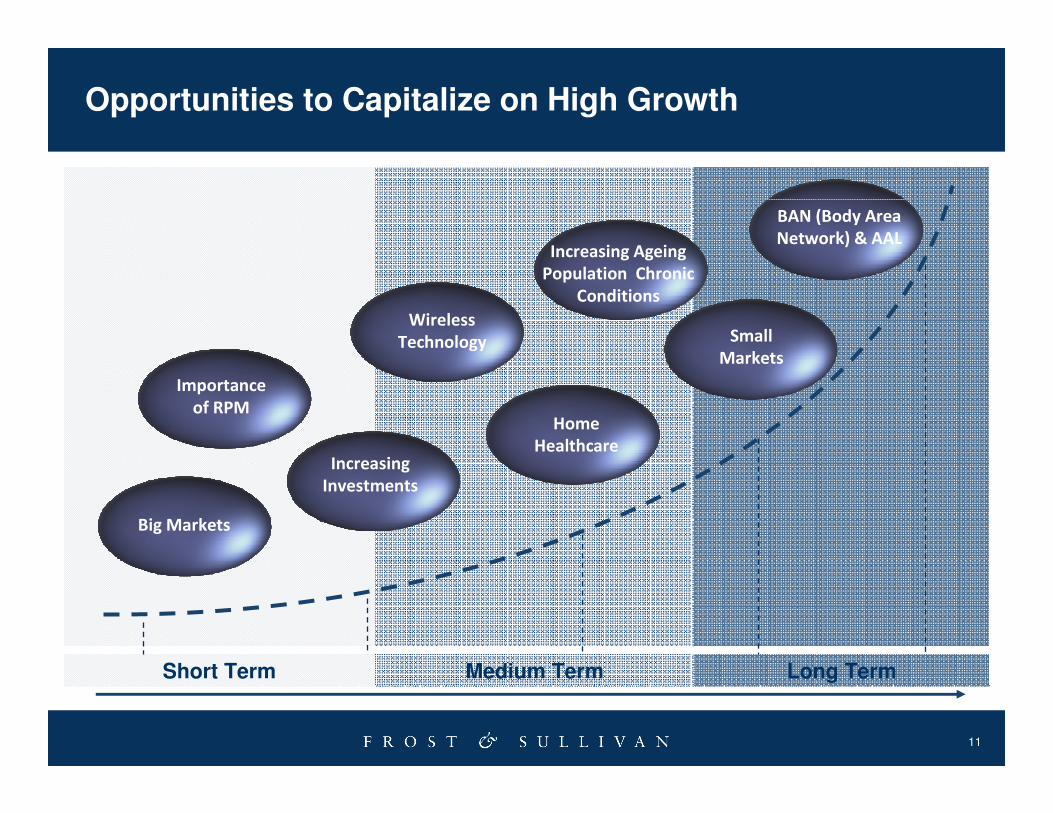

Opportunities to Capitalize on High Growth

Short Term Medium Term Long Term

Big Markets

BAN (Body Area

Network) & AAL

Increasing

Investments

Home

Healthcare

Importance

of RPM

Wireless

Technology

Increasing Ageing

Population Chronic

Conditions

Small

Markets

12

Recommendations

Short Term Recommendations

Long Term Recommendations

� Customize products to suit customer needs.

� Channel the services and devices to UK and Germany markets to achieve better results.

� Services including Audio / video consultation and Health management devices are likely to provide a good platform for growth. Targeting them will provide better margins.

� Target smaller markets by adopting various distribution methods.

� Technologically sound and open platform devices that are compatible with most communication systems will help in expanding the customer base.

� Cost-competitiveness will hold prominence in the business strategies that will be devised.

13

Next Steps

� Request a strategic approach document for a Growth Partnership Service or Growth Consulting Service to support you and your team to accelerate the growth of your company.

([email protected]) +44 (0)20 7343 8383

� Join us at our annual Growth, Innovation and Leadership 2011: A Frost & Sullivan Global Congress on Corporate Growth

(www.gil-global.com)

� Register for the next Chairman’s Series on Growth:

The CEO’s Perspective on Innovation: How Creativity Fosters Growth

14 July 2010 10:00 AM BST (www.frost.com/growthEU)

� Register for Frost & Sullivan’s Growth Opportunity Newsletter and keepabreast of innovative growth opportunities (www.frost.com/news)

14

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by taking our survey.

What would you like to see from Frost & Sullivan?

15

Find us @Frost_Sullivan on Twitter

Frost & Sullivan on Twitter and Facebook

Become a fan of Frost & Sullivan on Facebook

16

For Additional Information

Katja Feick

Corporate Communications

Healthcare

0049 (0) 69 7703343

Noel Anderson

European Vice President

New Business Development

+44 (0)207 343 8389

Siddharth Saha

Director of Research

Healthcare

+ 44 (0) 207 343 8374