European DataWarehouse · 2018-09-26 · New Securitisation Regulation (EU) 2017/2402 Information...

21

European DataWarehouse Gap Analysis 2.0 | 24 th September 2018

Transcript of European DataWarehouse · 2018-09-26 · New Securitisation Regulation (EU) 2017/2402 Information...

Corporate Presentation – October 2014

European DataWarehouse

Gap Analysis 2.0 | 24th September 2018

Agenda

1. New Securitisation Regulation (EU) 2017/2402 - Information to be disclosed

2. Summary of Gap Analysis 2.0

3. Gap Analysis of the ECB RMBS Template vs. the ESMA draft Residential Real Estate Underlying Exposures Template

4. Annexes

September 2018 European DataWarehouse GmbH 2

New Securitisation Regulation (EU) 2017/2402 Information to be Disclosed

September 2018 European DataWarehouse GmbH 3

Regulation Timeline: Where Are We Now?

September 2018 4European DataWarehouse GmbH

European Commission legislative proposal

November 26th

2014

Political deal on new RegulationMay 30th 2017

Publication in the Official

JournalDecember 28th

2017

Entry into force of the

RegulationJanuary 17th

2018

ESMA Consultation on Securitisation

Repository1st semester

2018

ESMA submitted

RTS/ITS on disclosure

requirements to EC on August

22nd 2018

Application of the

Securitisation Regulation

January 2019

We are here

Level 1 of the Process

A new Securitisation Regulation (EU) 2017/2402 was published on 28th December 2017 in the European Union OfficialJournal. It will apply in January 2019.

The regulation has two parts:• The first part of the regulation provides a common set of rules that apply to all securitisations• The second part of the regulation defines the criteria that qualify for Simple, Transparent and Standardised (STS)

securitisation

According to the regulation all securitisations should comply with the following disclosure requirements and all publicsecuritisations should make this information available to a securitisation repository:• Loan Level Data templates for the most prominent asset classes• Standardised Investor Reports for all securitisations• Additional documentation (incl. new standardised templates for inside information and significant events)

Other technical Standards shall be submitted to the CommissionBefore January

18th 2019

Level 2 of the Process

September 2018 5

* The full text of Level 1 of the regulation is available at http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32017R2401

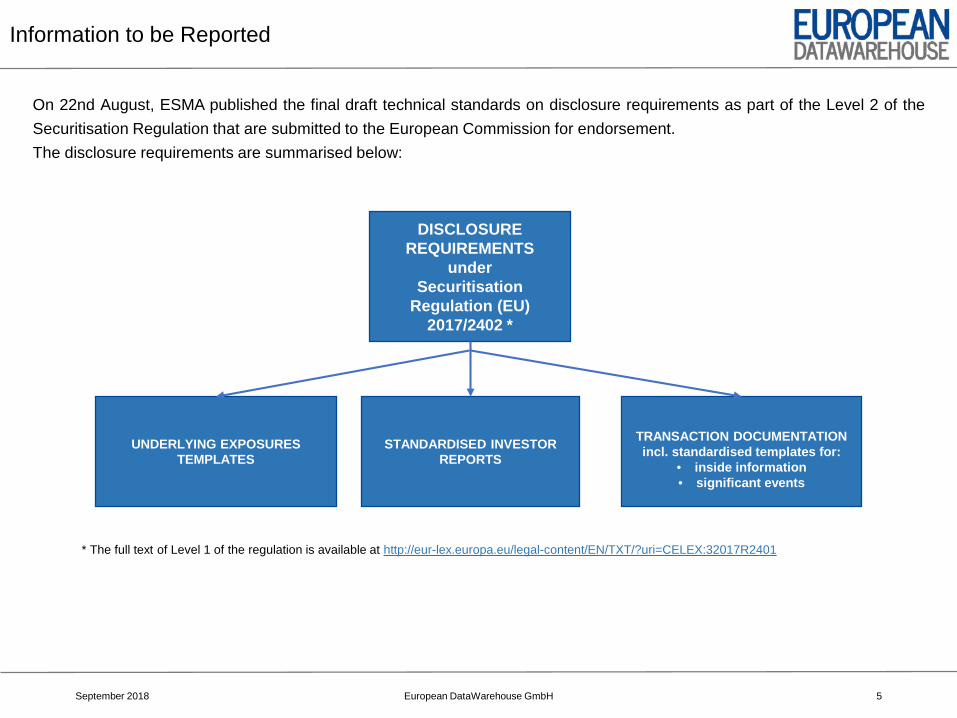

Information to be Reported

European DataWarehouse GmbH

DISCLOSURE REQUIREMENTS

under Securitisation

Regulation (EU) 2017/2402 *

TRANSACTION DOCUMENTATIONincl. standardised templates for:

• inside information • significant events

STANDARDISED INVESTOR REPORTS

UNDERLYING EXPOSURES TEMPLATES

On 22nd August, ESMA published the final draft technical standards on disclosure requirements as part of the Level 2 of theSecuritisation Regulation that are submitted to the European Commission for endorsement.The disclosure requirements are summarised below:

ED Aims to Become the First Securitisation Repository Under the Regulation

September 2018 European DataWarehouse GmbH 6

According to Article 7 (2) of Regulation (EU) 2017/2402,“the originator, sponsor and securitisation special purposeentity (SSPE) shall make the information for a securitisationtransaction available by means of a securitisation repository”

All securitisation repositories seeking to be designated will besupervised by ESMA

Summary of Gap Analysis 2.0

September 2018 European DataWarehouse GmbH 7

Gap Analysis 2.0

September 2018 European DataWarehouse GmbH 8

Key Differences

According to the ESMA Final Report on Disclosure Requirements under the Securitisation Regulation *, the ESMA proposed underlying exposures templates are built on the existing ECB ABS loan-level data templates.

The key differences are highlighted below:

September 2018 European DataWarehouse GmbH 9

Format changes

Addition/Removal of fields

Regulatory fields

Risk-related fields

Arrears information

Energy Performance

Change in the structure

No Data Allowance

Static vs. dynamic

* The ESMA Final Report on Technical standards on disclosure requirements under the Securitisation Regulation: https://www.esma.europa.eu/sites/default/files/library/esma33-128-474_final_report_securitisation_disclosure_technical_standards.pdf

No Data Options

September 2018 European DataWarehouse GmbH 10

New ESMA proposed “No Data” options:

Current ECB “No Data” options:

Source: ESMA Final Report on disclosure requirements

No Data Option Explanation

ND1 Data not collected as not required by the lending or underwriting criteria

ND2 Data collected on underlying exposure application but not loaded into the originator’s reporting system

ND3 Data collected on underlying exposure application but loaded onto a separate system from the originator’s reporting system

ND4-YYYY-MM-DD

Data collected but will only be available from YYYY-MM-DD (YYYY-MMDD shall be completed)

ND5 Not applicable

Source: ECB website https://www.ecb.europa.eu/paym/coll/loanlevel/implementation/html/index.en.html

Securitisation Item Types and Codes

September 2018 European DataWarehouse GmbH 11

Source: ESMA Final Report on disclosure requirements

New reporting templates proposed by ESMA

• CLO securitisations

• Esoteric

• Non-Performing Exposures

• Investor Report

• Inside information

• Significant Event

Item codes

When reporting the information to the securitisation repository, the reporting entity should provide the respective item code (see table) for each document

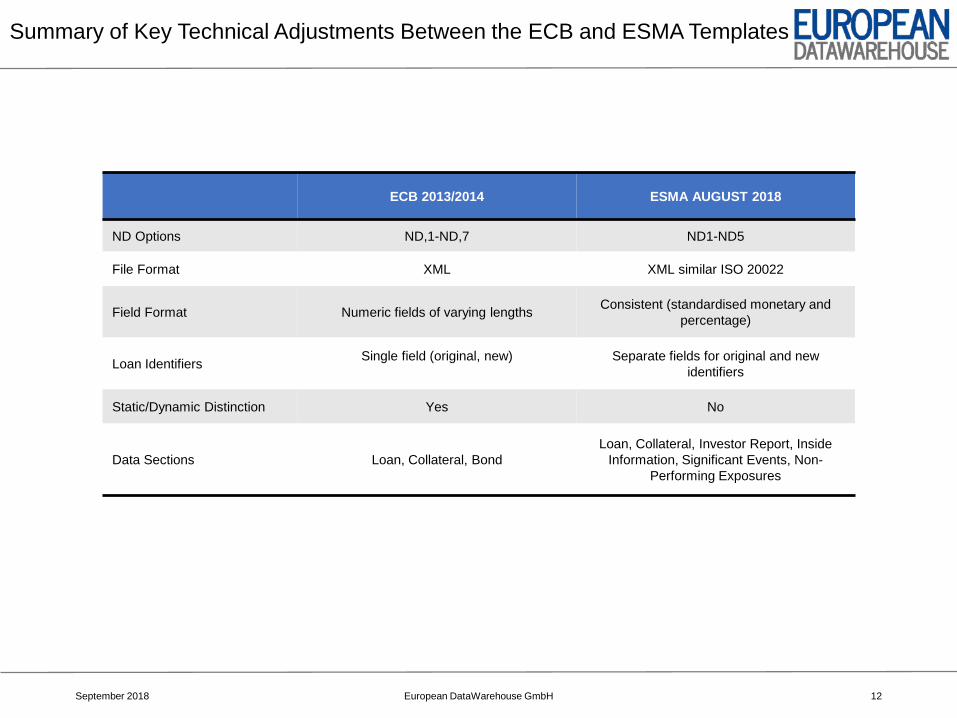

Summary of Key Technical Adjustments Between the ECB and ESMA Templates

September 2018 European DataWarehouse GmbH 12

ECB 2013/2014 ESMA AUGUST 2018

ND Options ND,1-ND,7 ND1-ND5

File Format XML XML similar ISO 20022

Field Format Numeric fields of varying lengths Consistent (standardised monetary and percentage)

Loan Identifiers Single field (original, new) Separate fields for original and new identifiers

Static/Dynamic Distinction Yes No

Data Sections Loan, Collateral, BondLoan, Collateral, Investor Report, Inside

Information, Significant Events, Non-Performing Exposures

September 2018 European DataWarehouse GmbH 13

Gap Analysis of the ECB RMBS Template vs. the ESMA draft Residential Real Estate

Underlying Exposures Template

ED Gap Analysis 2.0 and Methodology

Key points highlighted in the ED Gap Analysis 2.0 between the ECB ABS loan-level data templates and the proposed ESMA templates as of 22 August 2018

• Dropped fields

• New fields

• Changes to existing fields− Changes in definition

− No changes

− Format changes

− Changes in definition but same input

September 2018 European DataWarehouse GmbH 14

Residential Number of data fields

ECB mandatory fields 55

ECB optional fields 102

ESMA fields 108

Dropped ECB mandatory fields 10

Dropped ECB optional fields 80

New fields 42

Mandatory fields existing in both templates 45

ECB optional fields changing to mandatory 22

Merged fields 1

ECB fields that changed format 29

ECB fields that change from loan section to collateral section 15

Source: ED Calculations

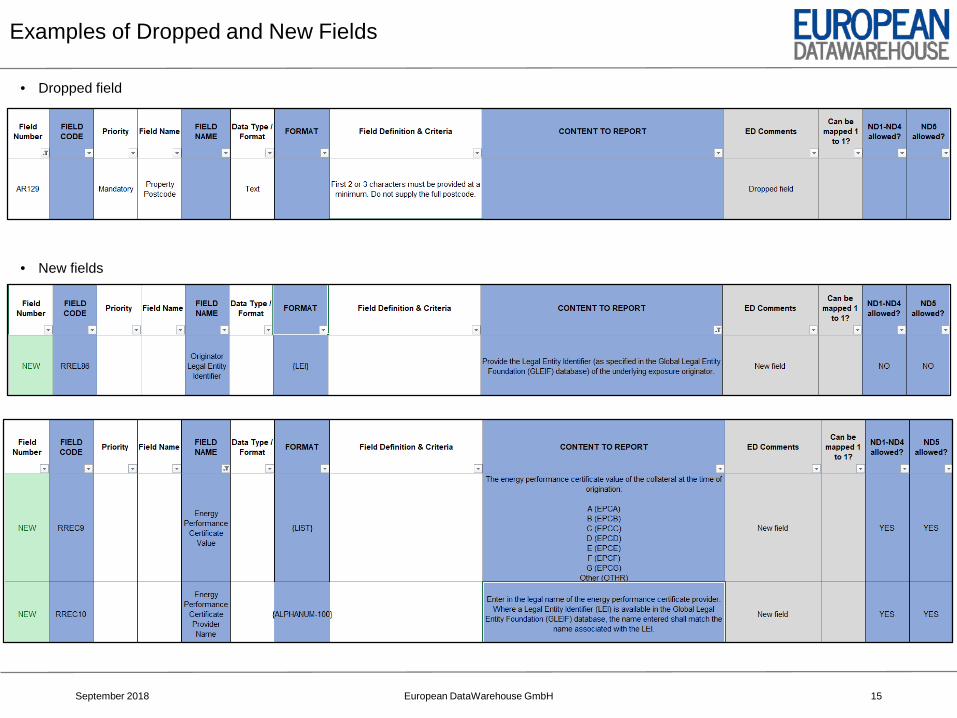

Examples of Dropped and New Fields

• Dropped field

• New fields

September 2018 European DataWarehouse GmbH 15

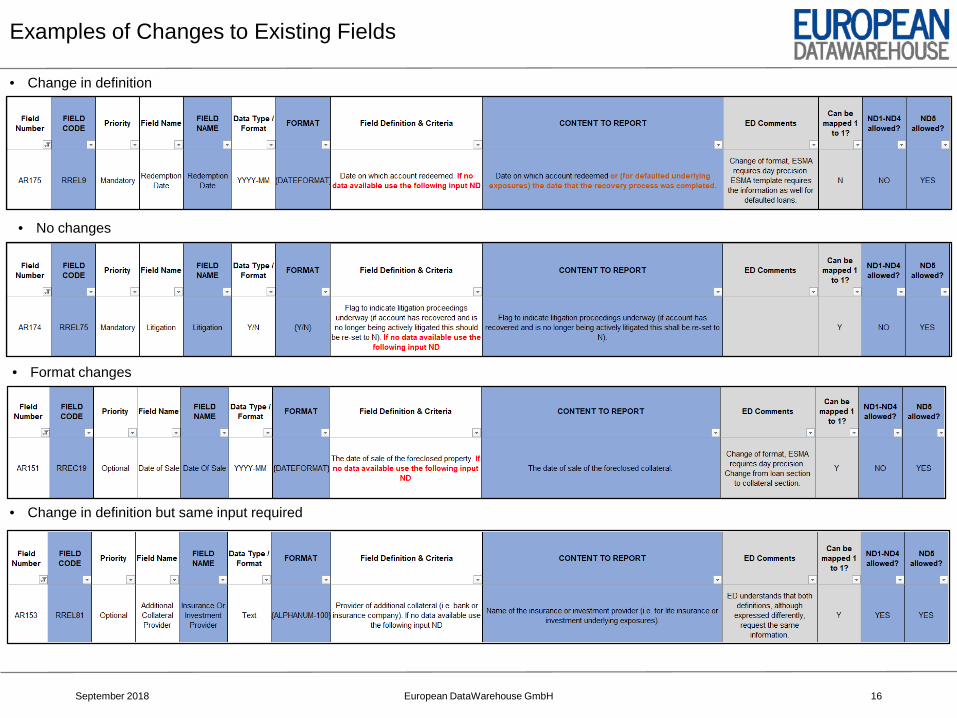

Examples of Changes to Existing Fields

September 2018 European DataWarehouse GmbH 16

• Change in definition

• No changes

• Change in definition but same input required

• Format changes

Transition from the ECB RMBS to the Final ESMA Template for Residential Real Estate Underlying Exposures

September 2018 European DataWarehouse GmbH 17

Source: ED Calculations

Contact Details for Gap Analysis

September 2018 European DataWarehouse GmbH 18

+49 (0) 69 50986 9017

ANNEX

September 2018 European DataWarehouse GmbH 19

Upcoming Webinars and Workshops on the Securitisation Regulation

Webinar schedule:

24 October: Auto ABS

20 November: SME/Corp/CLO

10 December: All other Asset Classes

Workshop schedule:

25 October: Lisbon, Portugal

05 November: London, United Kingdom

13 November: Milan, Italy

15 November: Madrid, Spain

22 November: Dublin, Ireland

September 2018 European DataWarehouse GmbH 20

September 2018 European DataWarehouse GmbH 21

This presentation (the “Presentation”) has been prepared by European DataWarehouse GmbH (the “Company”) and is being made available for information purposes only.

The Presentation is strictly confidential and any disclosure, use, copying and circulation of this Presentation is prohibited without the consent from the Company.

Information in this Presentation, including forecast financial information, should not be considered as advice or a recommendation toinvestors or potential investors in relation to holding, purchasing or selling securities or other financial products or instruments and does nottake into account your particular investment objectives, financial situation or needs. No representation, warranty or undertaking, express orimplied, is made as to the accuracy, completeness or appropriateness of the information and opinions contained in this Presentation.Under no circumstances shall the Company have any liability for any loss or damage that may arise from the use of this Presentation or theinformation or opinions contained herein.

Certain of the information contained herein may include forward-looking statements relating to the business, financial performance andresults of the Company and/or the industry in which it operates. Forward-looking statements concern future circumstances and results andother statements that are not historical facts, sometimes identified by the words “believes”, expects”, “predicts”, “intends”, “projects”, “plans”,“estimates”, “aims”, “foresees”, “anticipates”, “targets”, “may”, “will”, “should” and similar expression.The forward-looking looking statements, contained in this Presentation, including assumptions, opinions and views of the Company or cited from third party sources are solely opinions and forecasts which are uncertain and subject to risks.

Disclaimer

Disclaimer