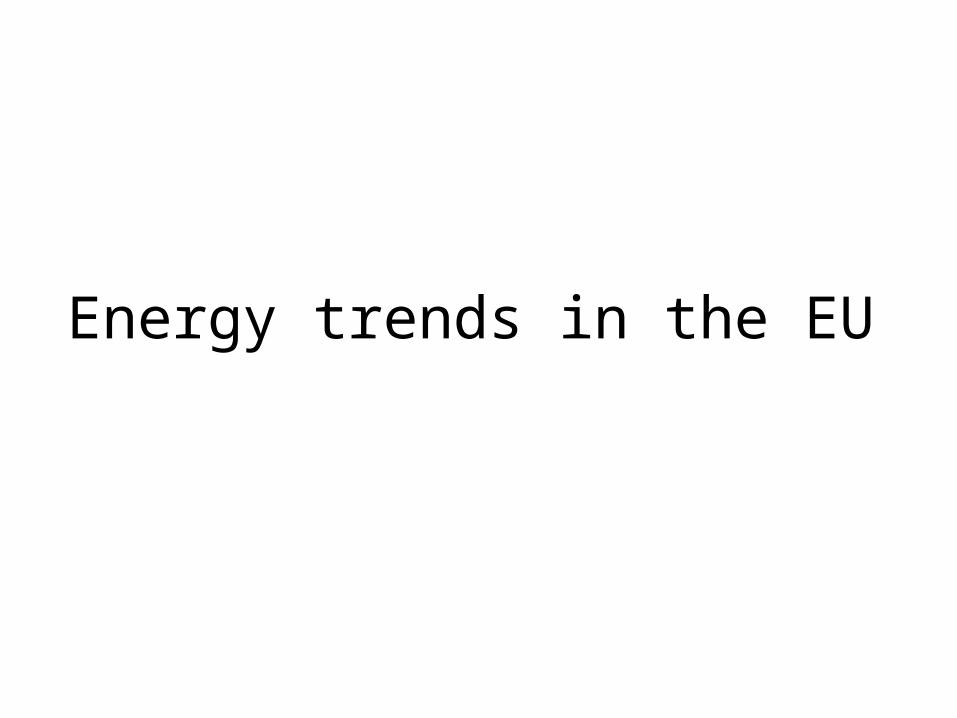

EU energy among Lisbon, Moskow and Kyoto

27

EU energy among Lisbon, Moskow and Kyoto Dr.Ionut PURICA IPE Academy of Romania

-

Upload

aileen-rodriguez -

Category

Documents

-

view

19 -

download

4

description

EU energy among Lisbon, Moskow and Kyoto. Dr.Ionut PURICA IPE Academy of Romania. Topics for discussion. Energy Trends in EU Energy Market in a regional context Surrounded – integrated corporate action New Technologies – real options Some Romanian data Conclusions. - PowerPoint PPT Presentation

Transcript of EU energy among Lisbon, Moskow and Kyoto

EU energy among Lisbon, Moskow and Kyoto

Dr.Ionut PURICA

IPE Academy of Romania

Topics for discussion

• Energy Trends in EU

• Energy Market in a regional context

• Surrounded – integrated corporate action

• New Technologies – real options

• Some Romanian data

• Conclusions

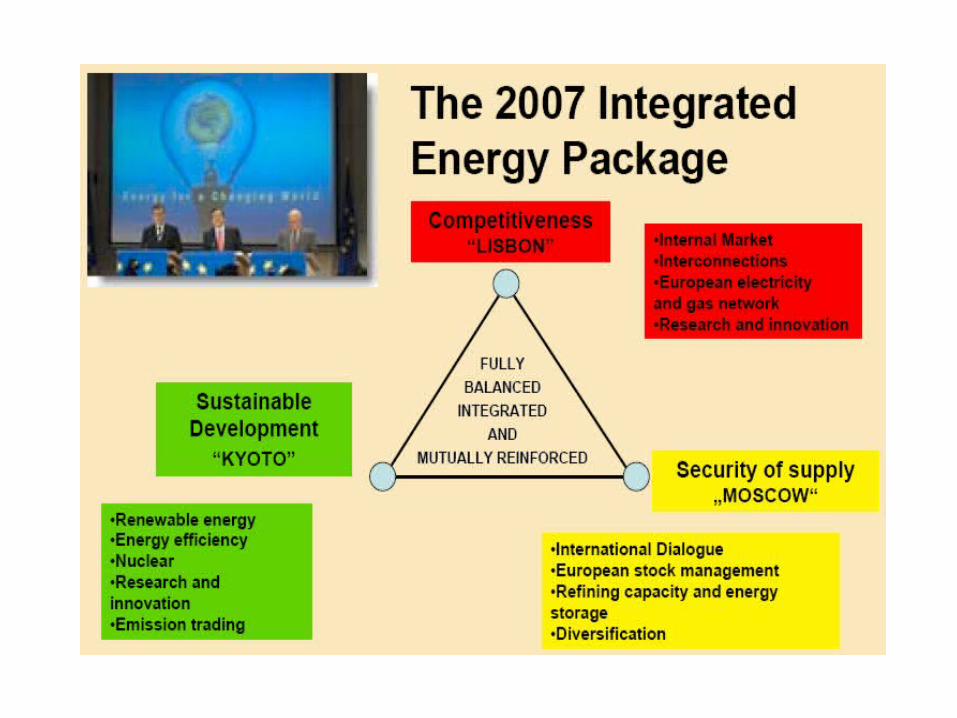

Energy trends in the EU

Buy yourself a small generator

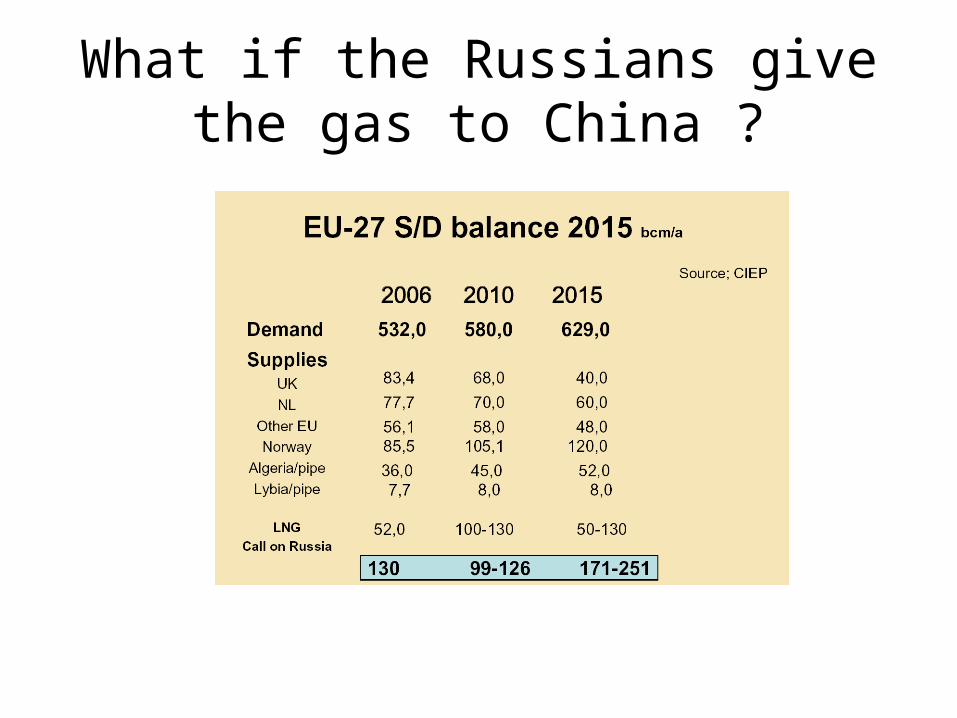

What if the Russians give the gas to China ?

Energy Market in a regional context

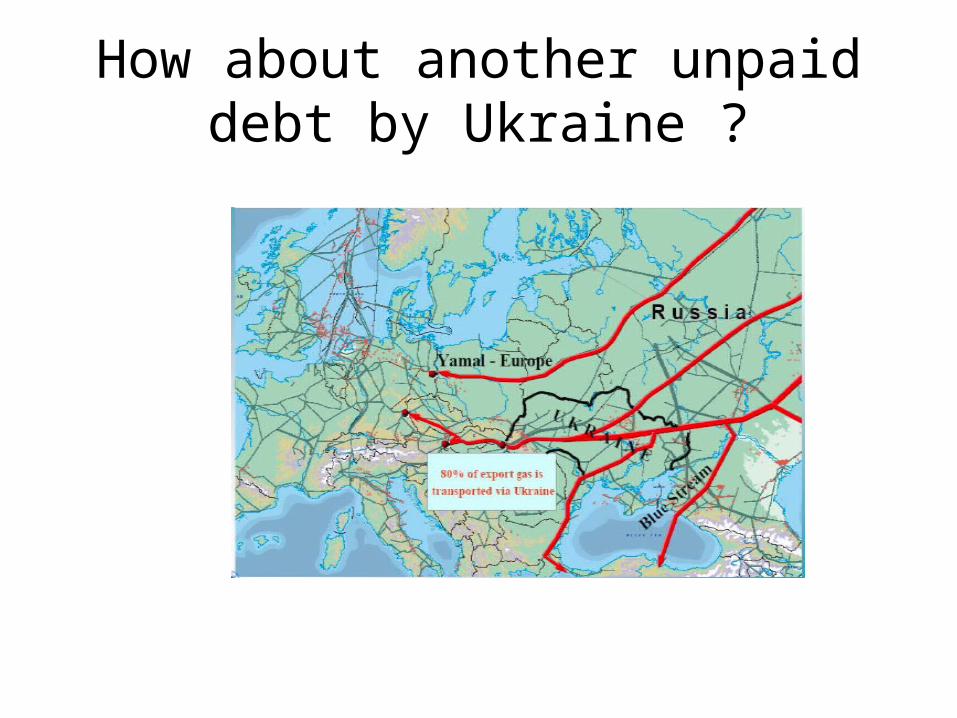

How about another unpaid debt by Ukraine ?

New Infrastructure towards the EU-27(bcm/a)Pipelines,Existing (2006), under construction/planned (2015)• Russia– EU-2006: 176– 2015: - FRG +55, Bulgaria +30• Norway– EU-2006: 128– 2015: UK +11, TBD:<20, Swe/DK:+8• Algeria– EU-2006: 40– 2015: Spain +13, Italy +13• Lybia– EU-2006: 9• Iran/Caspian– 2015: Bulgaria 23Total (2006) 344 – (2015) +92-173

Complex traffic risks in the Baltic both surface and submarine

State of health of NABUCO

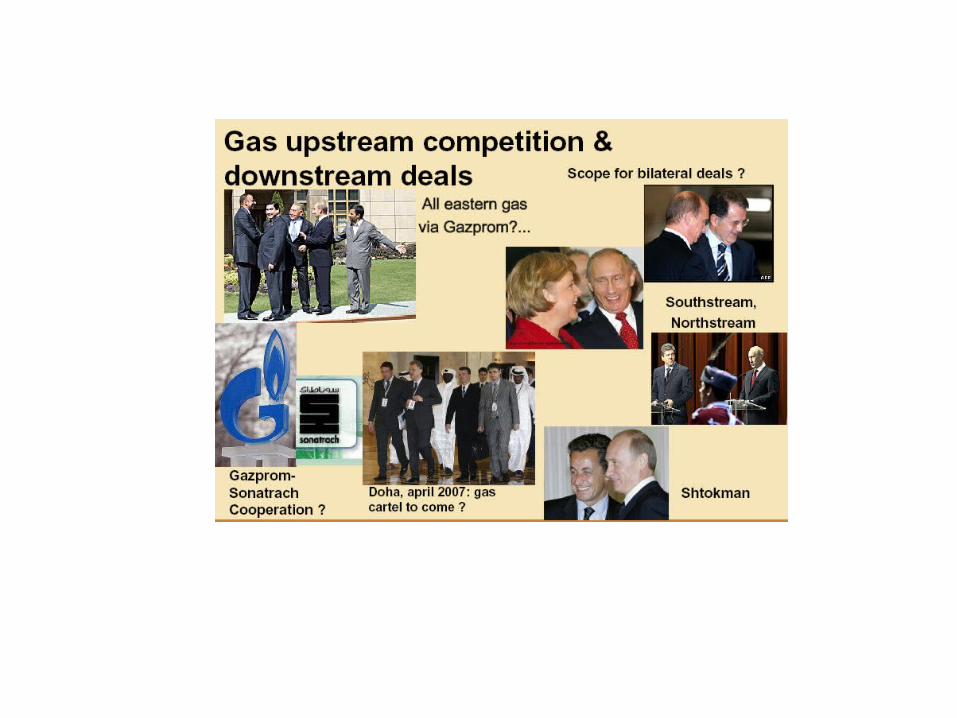

Surrounded – integrated corporate action

North Stream operational at end 2011; South Stream allowed by Turkey to pass in its waters in Dec.2011:“Best Christmas present to Russia”- Vladimir Putin

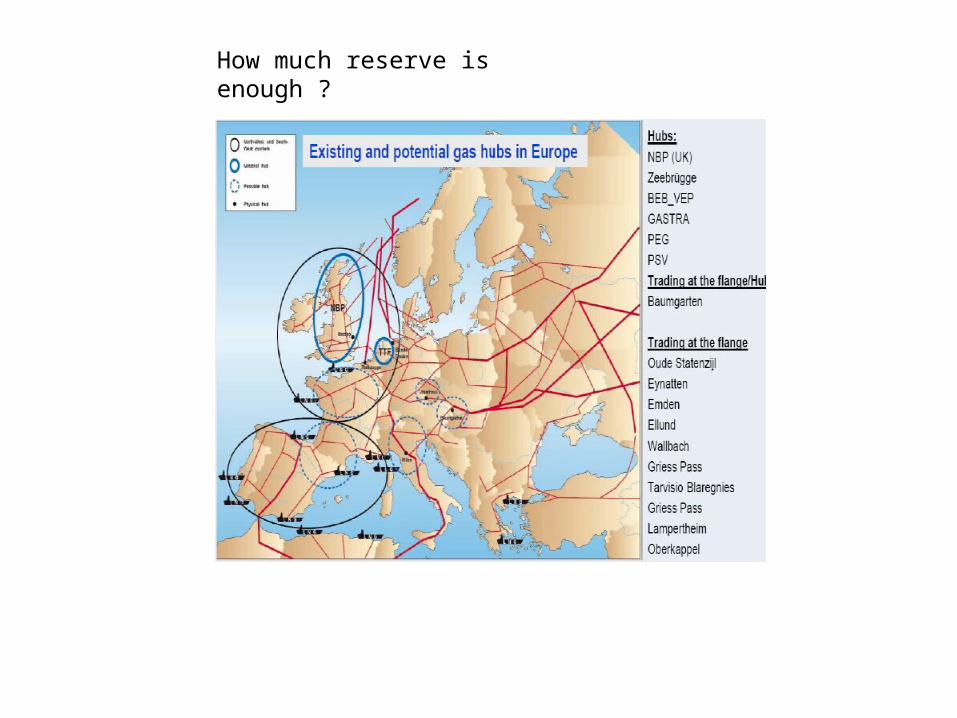

How much reserve is enough ?

LNG gas capacityLikely/possible

2007 2010 2015

Belgium 6,5 9,1 9,1

France 15,6 23,9 26,4-59,4

UK 9,0 44,0 49,7-54,7

NL 0,0 1,0 17,0-27,0

Italy 3,5 16,5 23,5-47,5

Spain 50,5 57,3 64,3

Portugal 5,5 5,5-8,5 5,5-8,5

Greece 2,6 2,6 2,6

Ireland 0,0 0,0 2,5

Croatia 0,0 0,0 10,0

Germany 0,0 5,0 10,0

Total 93,2 159,8-167,8 198-299,5

Gas Markets in Europe

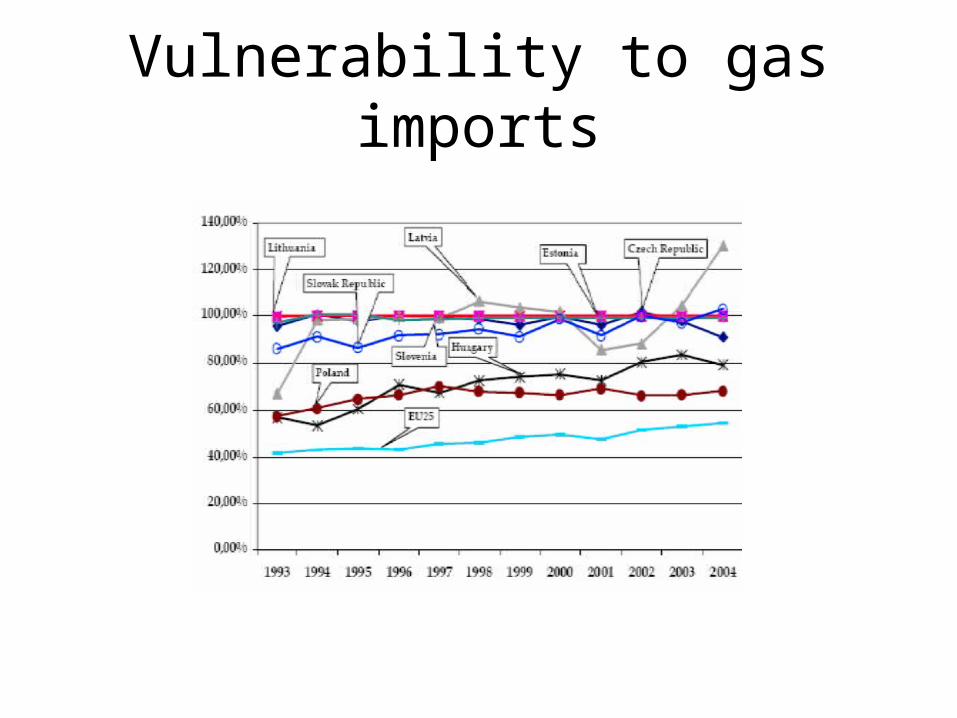

Vulnerability to gas imports

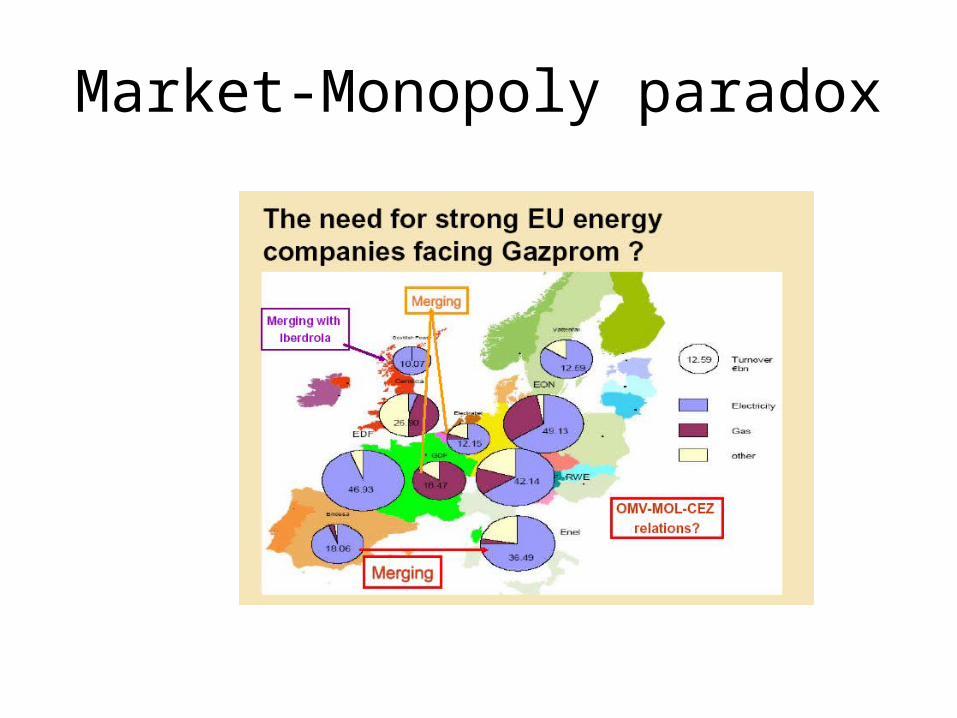

Market-Monopoly paradox

New Technologies – real options

How to reduce CO2 without more gas consumption?

Nuclear Power in the World

-5

0

5

10

15

20

25

30

35

40

45

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

Inc

rem

en

tal n

uc

lea

r p

ow

er

ca

pa

cit

y

ad

dit

ion

s in

GW

e

-300

0

300

600

900

1,200

1,500

1,800

2,100

2,400

2,700

To

tal n

uc

lea

r p

ow

er

ge

ne

rati

on

in T

Wh

Nuclear power in electricity generation

0

10

20

30

40

50

60

70

80

FRANCE

LITH

UANIA

SLOVAKIA

BELGIU

M

SWEDEN

UKRAINE

BULGARIA

SWIT

ZERLA

ND

SLOVENIA

ARMENIA

S. KOREA

HUNGARY

GERMANY

CZECH R

EP

JAPAN

FINLA

ND

SPAIN

TAIW

ANUSA

UK

RUSSIA

CANADA

ROMANIA

ARGENTINA

S. AFR

ICA

MEXIC

O

NETHERLA

NDS

BRAZIL

INDIA

PAKISTAN

CHINA

Pe

rce

nta

ge

of

ele

ctr

icit

y f

rom

nu

cle

ar

po

we

r

Should we begin to ‘Think Big’ ?

Have we got enough time ?

Conclusions

• EU energy strategy should be viewed at continental level

• Environmental measures should include technologies not only markets

• North-South view may shed new solutions in the East of the EU

• Global corporate strategy needed for energy companies

• Development within 3 x 20%: mobilizing local domain objectives without a global view

The road ahead for EU energy

Be it that you live interesting times (Chinese curse)