Residential Real Estate Closings: Essentials of Practice ...

Estate Planning

Key Concepts

Publish Date: July 2021

2

Estate Planning - Key Concepts

By

Danny C. Santucci

The author is not engaged by this text, any accompanying electronic media, or lecture in the render-ing of legal, tax, accounting, or similar professional services. While the legal, tax, and accounting issues discussed in this material have been reviewed with sources believed to be reliable, concepts discussed can be affected by changes in the law or in the interpretation of such laws since this text was printed. For that reason, the accuracy and completeness of this information and the author's opinions based thereon cannot be guaranteed. In addition, state or local tax laws and procedural rules may have a material impact on the general discussion. As a result, the strategies suggested may not be suitable for every individual. Before taking any action, all references and citations should be checked and updated accordingly.

This publication is designed to provide accurate and authoritative information in regard to the sub-ject matter covered. It is sold with the understanding that the publisher is not engaged in rendering legal, accounting, or other professional service. If legal advice or other expert advice is required, the services of a competent professional person should be sought.

—-From a Declaration of Principles jointly adopted by a committee of the American Bar Association and a Committee of Publishers and Associations.

Copyright July 2021

Danny Santucci

i

TABLE OF CONTENTS

CHAPTER 1 - Estate Planning .................................................................. 1-1 Build, Preserve & Distribute ...................................................................................................................... 1-2 Legal Documents ....................................................................................................................................... 1-3 Estate Planning Team ................................................................................................................................ 1-4

Attorney ............................................................................................................................................... 1-5 Accountant ........................................................................................................................................... 1-5 Insurance Agents ................................................................................................................................. 1-6 Financial Planner .................................................................................................................................. 1-6

Estate Administration ................................................................................................................................ 1-6 Probate Court....................................................................................................................................... 1-6 Executor ............................................................................................................................................... 1-7 Internal Revenue Service (IRS) ............................................................................................................. 1-9 Trustee ................................................................................................................................................. 1-9 Family Members .................................................................................................................................. 1-9

Things to Be Done When Death Occurs ........................................................................................ 1-9 Estate Planning Techniques & Devices ...................................................................................................... 1-10

Transfers within Probate ..................................................................................................................... 1-10 Disposition of Property without a Will ......................................................................................... 1-10 Disposition of Property with a Will ............................................................................................... 1-11

Transfers Outside Probate ................................................................................................................... 1-12 Joint Tenancy with Right of Survivorship ...................................................................................... 1-13 Tenancy in Common ..................................................................................................................... 1-13 Retirement Plan & Individual Retirement Accounts ..................................................................... 1-13 Life Insurance ................................................................................................................................ 1-13 Gifts ............................................................................................................................................... 1-13 Payable on Death Accounts (POD) ................................................................................................ 1-14

Transfers Using a Trust ........................................................................................................................ 1-14 Special Planning Tools .......................................................................................................................... 1-14

Spending ....................................................................................................................................... 1-14 Annual Gift Tax Exclusion .............................................................................................................. 1-15 Applicable Exclusion Amount ....................................................................................................... 1-17

Spousal Portability of Unused Exemption Amount ................................................................. 1-17 2010 Special Election .............................................................................................................. 1-18

Unlimited Marital Deduction ........................................................................................................ 1-18 Family Business Deduction - Expired ............................................................................................ 1-18 Installment Payment of Estate Taxes - §6166............................................................................... 1-18 Private Annuities ........................................................................................................................... 1-19

Regs Restrict Private Annuity Tax Benefits ............................................................................. 1-19 Installment Sale to Family Member .............................................................................................. 1-19

Self-Canceling Installment Notes ............................................................................................ 1-19 Irrevocable Life Insurance Trust ................................................................................................... 1-19 Special Valuation of Farms and Businesses - §2032A ................................................................... 1-22 Crummey Trusts ............................................................................................................................ 1-22 Charitable Remainder Trusts ........................................................................................................ 1-22 Minor Trusts ................................................................................................................................. 1-23 Family Limited Partnerships ......................................................................................................... 1-23

ii

Grantor Retained Income Trusts .................................................................................................. 1-23 Qualified Personal Residence Trusts (QPRTs) ......................................................................... 1-23 Grantor Retained Annuity Trusts (GRATs) .............................................................................. 1-24 Grantor Retained Unitrusts (GRUTs) ....................................................................................... 1-24

Buy-Sell Agreements ..................................................................................................................... 1-24 Estate Planning Facts ................................................................................................................................. 1-24

Family ................................................................................................................................................... 1-24 Property ............................................................................................................................................... 1-25

Domicile ........................................................................................................................................ 1-25 Objectives ............................................................................................................................................ 1-25 Existing Estate Plan .............................................................................................................................. 1-25

CHAPTER 2 - Estate & Gift Taxes ............................................................. 2-1 Federal Estate Tax...................................................................................................................................... 2-1

Changing Legislative Landscape ........................................................................................................... 2-2 Spousal Portability of Unused Exemption Amount - §2010(c)(2) ................................................. 2-3

Persons Subject to Federal Estate Tax ................................................................................................. 2-4 Applicable Exclusion Amount, Basic Computation & Rates ................................................................. 2-4

Progressive or Flat Rate ................................................................................................................ 2-4 2010 Special Election .................................................................................................................... 2-7

State Inheritance Tax ........................................................................................................................... 2-7 State Death Tax Credit Turns into Deduction – §2011 & §2058 ................................................... 2-7

Taxable Estate - §2051 ......................................................................................................................... 2-10 Gross Estate - §2031 ..................................................................................................................... 2-10

Owned Property - §2033 ......................................................................................................... 2-12 Interests Terminating At Death - Life Estates & Joint Tenancies ........................................ 2-12 Interests Created After Death............................................................................................. 2-13 Remainder Interests ........................................................................................................... 2-13

Dower & Curtsey - §2034 ........................................................................................................ 2-14 Community Property Comparison ...................................................................................... 2-14

Gifts within Three Years of Death - §2035 .............................................................................. 2-14 Transfers from Revocable Trusts ........................................................................................ 2-14

Retained Life Interest - §2036 ................................................................................................. 2-15 Retained Voting Rights ....................................................................................................... 2-16

Lifetime Transfers With Reversionary Interests - §2037 ......................................................... 2-16 Revocable Transfers - §2038 ................................................................................................... 2-17 Annuities - §2039 .................................................................................................................... 2-17 Joint Interests - §2040 ............................................................................................................. 2-18

Qualified Joint Interests Between Spouses - §2040(b) ....................................................... 2-18 Powers of Appointment - §2041 ............................................................................................. 2-19

Ascertainable Standard - The Safe Harbor Limitation ........................................................ 2-19 5/5 Power ........................................................................................................................... 2-20

Life Insurance - §2042 ............................................................................................................. 2-20 Incidents of Ownership ....................................................................................................... 2-22 Community Property Issue ................................................................................................. 2-22

Deductions from Gross Estate ...................................................................................................... 2-22 Estate Expenses & Claims - §2053 .......................................................................................... 2-24

Inclusion of Administrative Expenses on Non-Probate Assets ........................................... 2-24 Casualty & Theft Losses during Administration - §2054 ......................................................... 2-24 Charitable Transfers - §2055 (§170 & §2522) ......................................................................... 2-24

Immediate Contributions .................................................................................................... 2-25 Split-Interest Contributions ................................................................................................ 2-25

iii

Charitable Remainder Trusts .......................................................................................... 2-27 Charitable Lead Trusts .................................................................................................... 2-35

Insurance Related Contributions ........................................................................................ 2-35 Unlimited Marital Deduction - §2056 ..................................................................................... 2-35

Requirements ..................................................................................................................... 2-35 Net Value Rule .................................................................................................................... 2-36 Non-Citizen Spouse ............................................................................................................. 2-36

Qualified Domestic Trust ................................................................................................ 2-38 Gifts to Non-Citizen Spouses .......................................................................................... 2-39

Valuation .............................................................................................................................................. 2-40 IRS Valuation Explanation - §7517 ................................................................................................ 2-40 Alternate Valuation - §2032.......................................................................................................... 2-40 Special Valuation - §2032A ........................................................................................................... 2-41

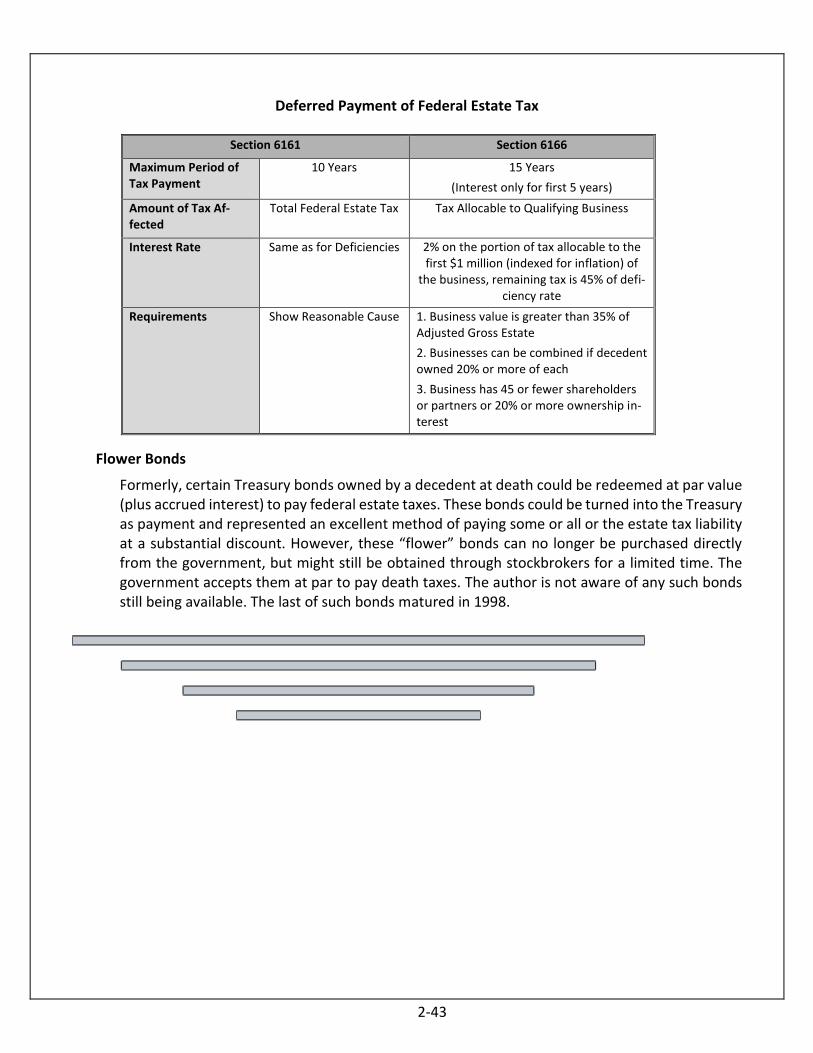

Estate Tax Return & Payment - §6018 ................................................................................................. 2-41 Installment Payment of Federal Estate Taxes - §6166.................................................................. 2-41

Computation ........................................................................................................................... 2-41 Eligibility & Court Supervision............................................................................................. 2-42

Closely Held Business .............................................................................................................. 2-42 Acceleration of Payment ......................................................................................................... 2-42

Flower Bonds ................................................................................................................................ 2-43 Tax Basis for Estate Assets - §1014 ...................................................................................................... 2-45

Community Property Cost Basis ................................................................................................... 2-46 Basis of Property Under the 2010 Special Election ....................................................................... 2-46

Property to Which the Modified Carryover Basis Rules Apply ................................................ 2-46 Limited Basis Increase for Certain Property ............................................................................ 2-47

GST Tax - §2601 ......................................................................................................................................... 2-48 Predeceased Parent Exception ..................................................................................................... 2-49 Exemption ..................................................................................................................................... 2-50

Allocation ................................................................................................................................ 2-50 Retroactive Allocation ........................................................................................................ 2-52

Gift Taxes - §2501 to §2524 ....................................................................................................................... 2-54 Gift Tax Computation ........................................................................................................................... 2-54 Calculation Steps .................................................................................................................................. 2-54 Applicable Exclusion............................................................................................................................. 2-55 Application ........................................................................................................................................... 2-55

Entity Rule ..................................................................................................................................... 2-55 Valuation .............................................................................................................................................. 2-55

Real Property ................................................................................................................................ 2-56 Stocks & Bonds ............................................................................................................................. 2-56 Annuities, Life Estates, Terms for Years, Remainders, & Reversions ............................................ 2-56

Split Gifts - §2513 ................................................................................................................................. 2-56 Community Property States.......................................................................................................... 2-57

Annual Exclusion .................................................................................................................................. 2-57 Per Donee/Per Year ...................................................................................................................... 2-58 Gifts in Excess of the Annual Exclusion ......................................................................................... 2-58 No Gift Tax .................................................................................................................................... 2-58 Gifts within 3 Years of Death ........................................................................................................ 2-58 Uniform Gifts to Minors Act ......................................................................................................... 2-59 Exception for Minor’s Trusts - §2503(b) & (c) ............................................................................... 2-59

Medical & Tuition Exclusion - §2503(e) ............................................................................................... 2-62 Qualifying Transfers ...................................................................................................................... 2-62

Interest-Free or Below-Market Loans .................................................................................................. 2-62 Gift Tax Marital Deduction ................................................................................................................... 2-62

iv

Nondeductible Terminable Interests ............................................................................................ 2-62 Gift Tax Charitable Deduction .............................................................................................................. 2-63

Partial Interests ............................................................................................................................. 2-64 Selecting Gift Property ......................................................................................................................... 2-65 Gift Advantages .................................................................................................................................... 2-65 Gift Disadvantages ............................................................................................................................... 2-66 Gift Tax Returns ................................................................................................................................... 2-66 Includibility of Gifts in the Estate ......................................................................................................... 2-66 Shifting Income & Gain ........................................................................................................................ 2-68

Gifts before Sale ........................................................................................................................... 2-68 Transfers into Trust Prior to Sale ............................................................................................ 2-68

Installment Obligations ................................................................................................................. 2-68 Transfer to Obligor at Death ................................................................................................... 2-69 Income in Respect of a Decedent ........................................................................................... 2-69

Reporting of Foreign Gifts - §6039(f) ............................................................................................ 2-70

CHAPTER 3 - Wills & Probate .................................................................. 3-1 What Is A Will? .......................................................................................................................................... 3-1

Provisions & Requirements .................................................................................................................. 3-1 Specific & General Bequests ......................................................................................................... 3-2 Residual Bequests ......................................................................................................................... 3-2 Conditional Bequests .................................................................................................................... 3-2 Executor ........................................................................................................................................ 3-2 Guardian ....................................................................................................................................... 3-3

Types of Wills ....................................................................................................................................... 3-3 Title Implications .................................................................................................................................. 3-4

Individual ...................................................................................................................................... 3-4 Joint Tenancy ................................................................................................................................ 3-5 Tenants in Common ...................................................................................................................... 3-7 Tenants by the Entirety................................................................................................................. 3-7 Community Property .................................................................................................................... 3-7

Tax Basis Advantage ................................................................................................................ 3-7 Untitled Assets .............................................................................................................................. 3-8

Changes to a Will ................................................................................................................................. 3-8 Advantages of a Will .................................................................................................................................. 3-8

Intestate Succession ............................................................................................................................ 3-9 Periodic Review .................................................................................................................................... 3-10 Continuing Business Operations .......................................................................................................... 3-11

Simple Will ................................................................................................................................................. 3-12 Probate ...................................................................................................................................................... 3-13

Advantages .......................................................................................................................................... 3-14 Disadvantages ...................................................................................................................................... 3-14 Probate Avoidance ............................................................................................................................... 3-15

Joint Tenancy ................................................................................................................................ 3-15 Community Property .................................................................................................................... 3-15 Totten Trust Accounts .................................................................................................................. 3-17 Life Insurance & Employee Benefits ............................................................................................. 3-17 Living Trusts .................................................................................................................................. 3-17

CHAPTER 4 - Trusts ................................................................................. 4-1 What is a Trust? ......................................................................................................................................... 4-1

v

Why a Trust? .............................................................................................................................................. 4-1 Types of Trusts ........................................................................................................................................... 4-3

Common Elements ............................................................................................................................... 4-3 Revocable Trust ................................................................................................................................... 4-3 Irrevocable Trusts ................................................................................................................................ 4-3 Testamentary Trust .............................................................................................................................. 4-4 Foreign Trusts - §679 ........................................................................................................................... 4-4 Family Trusts ........................................................................................................................................ 4-4 Medicaid Trust ..................................................................................................................................... 4-5 Living Trust ........................................................................................................................................... 4-5

Reversion ...................................................................................................................................... 4-5 Advantages of a Living Trust ......................................................................................................... 4-5 Disadvantages ............................................................................................................................... 4-6 Priority .......................................................................................................................................... 4-6

Pour-Over Will ......................................................................................................................... 4-6 Trust Taxation ............................................................................................................................................ 4-6

Income Tax ........................................................................................................................................... 4-6 Grantor Trusts - §671 to §678 ...................................................................................................... 4-6

Grantor Retained Income Trust .............................................................................................. 4-8 Revocable Trusts Included in Estate - §646 & §2652(b)(1) ........................................................... 4-9

Election for Income Tax Purposes ........................................................................................... 4-9 Irrevocable Trust Taxation ............................................................................................................ 4-10

Throwback Rules ..................................................................................................................... 4-10 Capital Gains ................................................................................................................................. 4-11 Deduction of Estate Planning Expenses ........................................................................................ 4-11 Deductibility of Death Expenses ................................................................................................... 4-11

Gift Tax ................................................................................................................................................. 4-11 Estate Tax ............................................................................................................................................. 4-13

Unlimited Marital Deduction ........................................................................................................ 4-14 Outright to Spouse .................................................................................................................. 4-14 Marital Deduction Trust .......................................................................................................... 4-14 Qualified Terminable Interest Property (QTIP) Trust .............................................................. 4-14

“A-B” Format................................................................................................................................. 4-16 “A-B-C” (QTIP) Format .................................................................................................................. 4-18 Valuation & Tax Basis .................................................................................................................... 4-19 Alternate Valuation....................................................................................................................... 4-21

Fundamental Provisions - Revocable Living Trust ..................................................................................... 4-21 Identification Clause ............................................................................................................................ 4-21 Recital Clause ....................................................................................................................................... 4-21 Property Transfer Clause ..................................................................................................................... 4-21 Income & Principal Clause ................................................................................................................... 4-21 Revocation & Amendment Clause ....................................................................................................... 4-22 Trustee Clause ...................................................................................................................................... 4-22

Trustee’s Acceptance .................................................................................................................... 4-22 Choice of a Trustee ....................................................................................................................... 4-22 Factors for Corporate Trustees ..................................................................................................... 4-22 Factors for Individual Trustees ..................................................................................................... 4-23

Trust Termination Clause ..................................................................................................................... 4-23

CHAPTER 5 - Post-Mortem Planning & Tax Return Requirements ........... 5-1 After Death Planning ................................................................................................................................. 5-1

Alternate Valuation Election ................................................................................................................ 5-1

vi

Special Use Valuation ........................................................................................................................... 5-1 Election to Defer Payment ................................................................................................................... 5-1 Final Medical Expenses ........................................................................................................................ 5-2 Administration Expenses ..................................................................................................................... 5-2 QTIP Election ........................................................................................................................................ 5-2 Disclaimers ........................................................................................................................................... 5-2

Federal Returns ......................................................................................................................................... 5-3 Form 1040 - Decedent’s Income Tax ................................................................................................... 5-3 Form 1041 - Estate’s Income Tax ......................................................................................................... 5-3 Form 706 - Decedent’s Estate Tax ....................................................................................................... 5-3 Carryover Basis Election & Information Return For 2010 .................................................................... 5-3

Decedent’s Estate Tax - Form 706 ............................................................................................................. 5-4 Filing Requirements ............................................................................................................................. 5-4 Paying the Estate Tax ........................................................................................................................... 5-5

Section 6161 ................................................................................................................................. 5-5 Section 6166 ................................................................................................................................. 5-6 Section 6163 ................................................................................................................................. 5-6

Overview of the Form 706 ................................................................................................................... 5-7 Definitions ..................................................................................................................................... 5-9

Preparing Form 706 ............................................................................................................................. 5-9 Form 706, Part 1, Page 1 - Decedent & Executor ......................................................................... 5-9 Form 706, Part 3, Page 2 - Elections by the Executor ................................................................... 5-9 Form 706, Part 4, Pages 2 & 3 - General Information ................................................................... 5-10 Schedule A, Page 5 - Real Estate ................................................................................................... 5-10 Schedule A-1, Pages 6 thru 9 - Section 2032A Valuation .............................................................. 5-10 Schedule B, Page 10 - Stocks and Bonds ....................................................................................... 5-11 Schedule C, Page 11 - Mortgages, Notes, and Cash ...................................................................... 5-11 Schedule D, Page 12 - Insurance on Decedent’s Life .................................................................... 5-11 Schedule E, Page 13 - Jointly Owned Property ............................................................................. 5-11 Schedule F, Page 14 - Other Miscellaneous Property .................................................................. 5-12 Schedule G, Page 15 - Transfers During Decedent’s Life .............................................................. 5-12 Schedule H, Page 15 - Powers of Appointment ............................................................................ 5-12 Schedule I, Page 16 - Annuities ..................................................................................................... 5-12 Schedule J, Page 17 - Funeral and Administration Expenses ........................................................ 5-12 Schedule K, Page 18 - Debts of Decedent, and Mortgages and Liens ........................................... 5-13 Schedule L, Page 19 - Net Losses During Administration and Expenses Incurred in Administering Property Not Subject to Claims .......................................................................................................................... 5-13 Schedule M, Page 20 - Bequests to Surviving Spouse................................................................... 5-14 Schedule O, Page 21 - Charitable Gifts and Bequests ................................................................... 5-14 Schedule P, Page 22 - Credit for Foreign Death Taxes .................................................................. 5-14 Schedule Q, Page 22 - Credit for Tax on Prior Transfers ............................................................... 5-14 Schedules R & R-1, Pages 23 thru 27 - Generation-Skipping Transfer Tax ................................... 5-14 Old Schedule T Gone - Qualified Family-Owned Business Interest .............................................. 5-14 Schedule U, Page 28 - Qualified Conservation Easement Exclusion ............................................. 5-14 Form 706, Part 5, Page 3 - Recapitulation .................................................................................... 5-15 Form 706, Part 6, Page 4 - Portability of Deceased Spousal Unused Exclusion (DSUE) ................ 5-15 Form 706, Part 2, Page 1 - Tax Computation ................................................................................ 5-15 Schedule PC, Pages 29 - 31 - Protective Claim for Refund ............................................................ 5-15

Discharge from Personal Liability......................................................................................................... 5-16 Estate Income Tax Return - Form 1041 ..................................................................................................... 5-18

Filing Requirements ............................................................................................................................. 5-18 Schedule K-1 ................................................................................................................................. 5-19

Tax Computation .................................................................................................................................. 5-19

vii

Exemption Deduction ................................................................................................................... 5-20 Contributions ................................................................................................................................ 5-20

Statute of Limitations........................................................................................................................... 5-20 Accounting Methods ............................................................................................................................ 5-20 Taxable Year ......................................................................................................................................... 5-20 Double, Split & Solo Deductions .......................................................................................................... 5-20

Decedent’s Final Income Tax Return - Form 1040 ..................................................................................... 5-23 Preceding Year Return ......................................................................................................................... 5-23 Filing Requirements ............................................................................................................................. 5-23

Refund .......................................................................................................................................... 5-23 Form 1310 ..................................................................................................................................... 5-23 Joint Return with Surviving Spouse .............................................................................................. 5-24

Request for Prompt Assessment.......................................................................................................... 5-24 Included Income .................................................................................................................................. 5-24

Partnership Income ...................................................................................................................... 5-25 S Corporation Income ................................................................................................................... 5-26 Self-Employment Income.............................................................................................................. 5-26 Community Income ...................................................................................................................... 5-26 Interest & Dividend Income .......................................................................................................... 5-26

Exemptions & Deductions .................................................................................................................... 5-27 Medical Expenses ......................................................................................................................... 5-27

Election for Decedent’s Expenses ........................................................................................... 5-27 Making the Election ............................................................................................................ 5-27 AGI Limit ............................................................................................................................. 5-28

Medical Expenses Not Paid By Estate ..................................................................................... 5-28 Insurance Reimbursements .................................................................................................... 5-28

Deduction for Losses..................................................................................................................... 5-28 At-Risk Loss Limits ................................................................................................................... 5-28 Passive Activity Rules .............................................................................................................. 5-29

Gift Tax Return - Form 709 ........................................................................................................................ 5-31 Penalties ............................................................................................................................................... 5-31 Filing ..................................................................................................................................................... 5-31

Extension of Time to File .............................................................................................................. 5-32 Extension of Time to Pay .............................................................................................................. 5-32

Split Gifts .............................................................................................................................................. 5-32 Special Applications & Traps ................................................................................................................ 5-33

Bargain Sales ................................................................................................................................. 5-33 Below Market Loans ..................................................................................................................... 5-33

Exception ................................................................................................................................. 5-34 Net Gifts ........................................................................................................................................ 5-34 Promises to Make a Gift ............................................................................................................... 5-34 Checks ........................................................................................................................................... 5-35 Stock Certificates .......................................................................................................................... 5-35 Promissory Notes .......................................................................................................................... 5-35 Powers of Appointment ................................................................................................................ 5-35

viii

Learning Objectives

After reading Chapter 1, participants will be able to:

1. Identify basic estate planning elements recognizing the importance of well-drafted legal documents and specify the key team participants including their roles in the estate plan-ning process.

2. Determine the major steps in the probate process, identify ways to make transfers out-side the probate system including the use of a trust, specify estate tax techniques that save death taxes while retaining maximum control, and identify estate-planning facts.

1-1

CHAPTER 1

Estate Planning

Everyone needs to do estate planning. Whether a person is a business owner or an employee, young or retired, wealthy or poor, people should plan their estate. Even those without assets need to deal with old age, possible conservatorship, health care directives, and funeral arrangements. Estate plan-ning is for everyone.

Since death is uncertain, everyone, young or old, should be ready for the contingency of death at any time. Even with the great advances in modern medicine, not everyone is lucky enough to grow old gracefully. None of us can, with certainty, predict the timing of our deaths. In estate planning, to-morrow may instantly become today.

Estate planning is more than just planning for death. It includes building an estate during a lifetime, then seeing that those assets are protected in an estate that can be passed to the next generation. It allows you the opportunity to control your success both during life and on death.

Thus, estate planning has three economic elements:

(1) Building the estate;

(2) Preserving the estate; and

(3) Distributing the estate.

1-2

Build, Preserve & Distribute

Estate planning is designing a program for effective wealth building, preservation, and disposition of property at the minimum possible tax cost. This process is much more than just planning for death. It is a commitment to yourself and your family.

Estate planning tries to encourage wealth building for everyone. Building an estate throughout life is part of estate planning.

When you start building an estate, you must preserve it at the same time. Preservation is the process of looking at the income and gift tax to minimize the overall tax burden for the total family unit.

Finally, once you have made and preserved an estate, you must determine how to distribute it to your heirs with the least possible death tax cost.

1-3

Legal Documents

For an estate plan to be effective, suitable and proper legal documents must be executed. The im-portance of well drafted legal documents cannot be overemphasized. Poor drafting and improper documentation will destroy any estate plan.

1-4

Legal instruments must be drafted by a competent attorney who knows estate planning techniques. Not all attorneys are qualified for estate planning work. For example, a specialist in real estate may not be knowledgeable on the latest estate planning developments.

Estate planning documents must be periodically reviewed due to tax and legal changes and to ascer-tain whether they continue to express the objectives of the estate owner. Such a review could bring about a modification in the plan that would produce significant benefits to the estate owner, while the neglect of such a review could be very costly.

Estate Planning Team

In estate planning, many professional skills are useful and a team effort will work best. Normally, the professionals most often involved in the estate planning process are:

(1) The attorney,

(2) The accountant,

(3) The insurance agent, and

(4) The financial planner.

There is one goal - the development of a comprehensive plan to accomplish the client’s financial and family objectives. Each member of the team has a job to do.

Estate Planning Team Assignments

Action Qualified Persons

Convincing a person to do estate planning

You (i.e., client or individual)

Spouse\

Attorney

Accountant

Financial Planner

Insurance Agent

Family Members

Friends

Analysis of Assets

Attorney

Accountant

You

Review of Present Plan

Attorney

Accountant

Financial Planner

Insurance Agent

Action Qualified Persons

Tax Analysis

Attorney

Accountant

Insurance Agent

1-5

Liquidity Requirements

Attorney

Accountant

Financial Planner

Insurance Agent

Legal Consequences Attorney

Changes in Estate Plan

You

Attorney

Accountant

Financial Planner

Insurance Agent

Putting Plan into Effect

Attorney

Accountant

Financial Planner

Insurance Agent

Follow Up

You

Attorney

Accountant

Financial Planner

Insurance Agent

Attorney

The attorney should decide whether suggestions, recommendations, and phases in the plan have legal substance and merit. A competent attorney must draft the legal documents that are the frame-work of an effective estate plan. Only a lawyer may legally practice law.

Note: Many people mistakenly believe that the attorney named in the estate planning documents must be used as the estate attorney at death. Even if the estate planning documents name an at-torney, most states deem this only a suggestion and not a requirement. There’s no reason to hire a lawyer if he or she is not the best choice.

Accountant

The accountant should know the financial affairs of the taxpayer, recognize the client’s need for po-tential estate planning1, and be knowledgeable with respect to income and estate tax laws. The ac-countant should also be able to advise on valuation problems and family income needs.

An accountant should file the final income tax return on behalf of the decedent. In addition, the estate will generally require an income tax return, as will any trusts formed under the estate plan. These are important functions for a good accountant.

1 The accountant is often the person on the team who has the responsibility to initiate the estate process.

1-6

Insurance Agents

Insurance agents are great motivators in getting persons involved in the estate planning process and can provide excellent advice and ideas. The agent should have specialized knowledge of the many forms of life insurance and know what various policies can and cannot do.

Financial Planner

The financial planner should be able to advise on investment return, asset management, and cash flow analysis. The financial planner should also know enough about insurance, estate taxes, and law to suggest possible solutions for the client to discuss with his or her accountant and attorney.

Estate Administration

There are other players in the total process of estate planning besides the “estate planning team.” These other participants can include:

(1) The Probate Court,

(2) An executor,

(3) The Internal Revenue Service, and

(4) A trustee.

Probate Court

The probate court is an important participant. It functions to:

(i) Oversee the executor and conserve the decedent’s assets,

(ii) Interpret the will, and

(iii) If there is no will, apply the laws of intestate succession.

The "probate estate" refers to any property subject to the authority of the probate court. Often it is good planning to avoid probate and there are several estate planning devices to do so.

Note: When one dies without a will, this is called dying intestate and the state writes a will for you by statute. Thus, under intestate succession, the probate estate is distributed to heirs based on a statutory distribution scheme.

Intestacy vs. Will

Intestacy Will

No expense of a will Appointment of guardian for mi-nors

No need to think about death Appointment of executor

Expense of a probate proceeding with an administrator

Potential expense of probate with an executor

Potential litigation Allocation of death taxes to heirs

1-7

Assignment of powers to executor to carry on business, sell assets

and make tax decisions

Elimination of bond for executor

Creation and exercise of powers of appointment

Bequests to relatives, heirs, and charities

Establishment of a testamentary trust

Can be used together with a living trust to avoid probate

Executor

An executor (man) or executrix (woman) is designated by the will to manage the assets and liabilities of the decedent. Normally, the executor is the surviving spouse or a close relative.

Being an executor is time consuming and often complex. The job may last from nine months up to several years. The duties of the executor include searching for assets, publishing notices to creditors, filing estate and income tax returns, paying expenses and liabilities, and distributing remaining assets (if any) to the beneficiaries. The executor is only in control of the probate assets.

1-8

1-9

Internal Revenue Service (IRS)

Obviously, the Internal Revenue Service is an interested participant. As many as four federal tax re-turns may be required after a person dies:

(1) An income tax return (Form 1040),

(2) An estate tax return (Form 706),

(3) An estate income tax return (Form 1041), and

(4) A gift tax return (Form 709).

Note: The tax departments of your state or local government may also have a role, depending on the inheritance tax laws of your domicile.

Trustee

If a trust has been created during the decedent’s lifetime (called inter vivos) or at death (called tes-tamentary), there will be a trustee named in the trust agreement to carry out the terms of the trust.

Family Members

The most immediate duties arising from the decedent’s death often fall on the shoulders of close family members. They have to deal with the practical and necessary tasks created when a loved one dies.

Things to Be Done When Death Occurs

1. Notify funeral parlor, funeral society, or other institution responsible for removing the body from the hospital.

Note: Request at least 10 death certificates. The funeral directors will usually handle such requests as a part of their duties.

2. Obtain and begin to implement any instructions the decedent left regarding his or her dispo-sition, including anatomical gifts or special funeral instructions.

3. Contact appropriate religious officials and proceed with funeral services or other planned dis-position.

4. Locate the Will, if any, and notify the executor.

Note: This may require access to safe deposit boxes. In many states, the next of kin may legally enter each box in the presence of a bank officer to retrieve legal papers such as wills, trusts, deeds, and burial instructions.

5. The executor should select and/or contact the estate lawyer.

6. Notify the immediate family, close friends, employer, and business colleagues of the death.

Note: When contacting relatives and friends confirm their addresses and telephone numbers.

7. Decide on an appropriate memorial for the decedent and notify acquaintances if flowers are to be omitted.

8. Prepare and deliver obituary to local newspapers, giving time and place of services.

9. Notify concerned persons too far away to attend the funeral.

10. Arrange for care of members of the family.

1-10

Note: This is a particular concern where there are minor children, an elderly spouse, a disabled dependent, or animals.

11. Determine if the decedent’s credit cards should be canceled.

12. Check carefully all death benefits.

13. Promptly check all debts and installment payments.

14. Notify utilities and landlord, if any.

15. Tell the post office where to send mail.

16. Determine the location of decedent’s vehicles and who has access to them.

Note: No one should be permitted to use the decedent’s vehicles except his or her surviving spouse. As legal owner, the decedent’s estate may be held liable for any accidents.

Estate Planning Techniques & Devices

While it is difficult to list all estate planning techniques and devices, the most popular can be cate-gorized by common use and objective rather than by tax code section. In fact, first approaching es-tate planning in this way will actually help your later understanding of the related tax issues that gave birth to most of these devices.

Transfers within Probate

Probate is the process through which legal title to property contained in the probate estate is trans-ferred from the decedent to the decedent’s heirs and beneficiaries. When a person dies with a will (testate), the probate court determines if the will is valid, hears any objections to the will, provides for the payment of creditors, and supervises the distribution of property by the personal representa-tive or executor according to the terms of the will. When an individual dies without a will (intestate) the probate court appoints an administrator who receives all claims, pays creditors, and distributes any remaining property according to the laws of the state in which the decedent died.

The “probate estate” refers to any property subject to the authority of the probate court. This prop-erty includes all solely owned property plus any other property that does not pass to someone else by operation of law.

Disposition of Property without a Will

If there’s no will, property in the probate estate is distributed according to the state law of intes-tacy. When an individual dies intestate, the probate court chooses a person responsible for ad-ministering the estate and distributing the probate assets. This person, called the administrator, may or may not have been the person you would’ve chosen. If there’s family bickering regarding the appointment of the administrator, the court often appoints a neutral party whose services must be paid from estate funds.

In addition, the probate estate is distributed to heirs based upon a statutory distribution scheme. While state laws vary greatly, most provide an allowance to be set aside for the surviving spouse and/or children. After this spousal set aside or if there is no spouse, the remaining probate estate, after payments of claims against the estate or debts of the decedent, is distributed in a variety of ways depending upon marital status, surviving heirs, and nature of the property.

1-11

Note: When there is a will, many states give the surviving spouse the ability to renounce the will and elect to take her intestate share provided by state law. Usually, the surviving spouse can take about one-third to one-half of the probate estate. This election procedure is meant to protect the surviving spouse from being disinherited by the predeceasing spouse.

Disposition of Property with a Will

A will is typically a written document that provides instructions for disposing of a person’s prop-erty upon his or her death. Upon the decedent’s death, the will must go through the probate process in order to have the instructions carried out. There are many reasons for having a will, including:

(1) The ability to dispose of your property other than through intestate succession;

(2) Nomination of your personal representative;

(3) Making specific bequests to individuals and charities;

(4) Appointment of guardians for minor children; and

(5) Apportionment of death taxes among heirs.

1-12

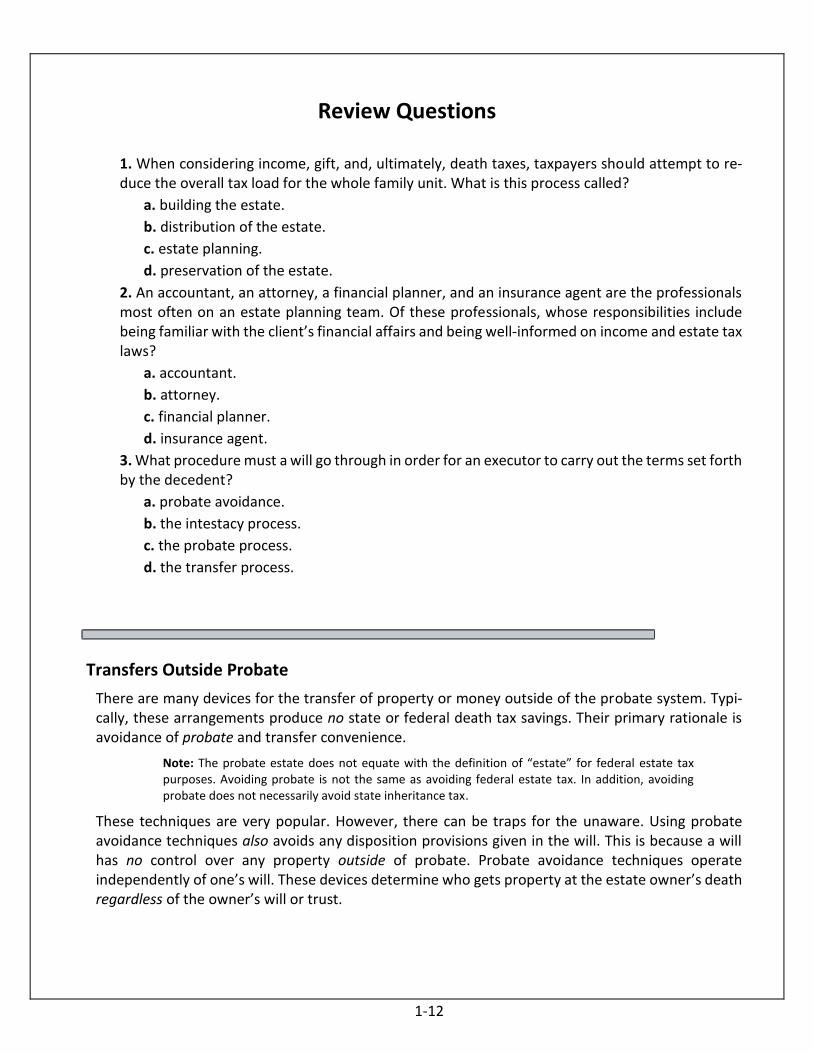

Review Questions

1. When considering income, gift, and, ultimately, death taxes, taxpayers should attempt to re-duce the overall tax load for the whole family unit. What is this process called?

a. building the estate.

b. distribution of the estate.

c. estate planning.

d. preservation of the estate.

2. An accountant, an attorney, a financial planner, and an insurance agent are the professionals most often on an estate planning team. Of these professionals, whose responsibilities include being familiar with the client’s financial affairs and being well-informed on income and estate tax laws?

a. accountant.

b. attorney.

c. financial planner.

d. insurance agent.

3. What procedure must a will go through in order for an executor to carry out the terms set forth by the decedent?

a. probate avoidance.

b. the intestacy process.

c. the probate process.

d. the transfer process.

Transfers Outside Probate

There are many devices for the transfer of property or money outside of the probate system. Typi-cally, these arrangements produce no state or federal death tax savings. Their primary rationale is avoidance of probate and transfer convenience.

Note: The probate estate does not equate with the definition of “estate” for federal estate tax purposes. Avoiding probate is not the same as avoiding federal estate tax. In addition, avoiding probate does not necessarily avoid state inheritance tax.

These techniques are very popular. However, there can be traps for the unaware. Using probate avoidance techniques also avoids any disposition provisions given in the will. This is because a will has no control over any property outside of probate. Probate avoidance techniques operate independently of one’s will. These devices determine who gets property at the estate owner’s death regardless of the owner’s will or trust.

1-13

Note: A trust only disposes of property that has been transferred to it. If no assets have been trans-ferred to a trust either during life or at death by the decedent’s will, no property will be controlled by the terms of trust.

Joint Tenancy with Right of Survivorship

When an asset is held in joint tenancy with right of survivorship, each joint tenant has an equal, undivided interest in the whole asset. In addition, a decedent’s share automatically shifts to the surviving joint tenant(s) at the moment of death by operation of law. In most situations, no fed-eral estate tax is saved. Fifty percent of any property held in such a manner with a spouse is included in the decedent’s estate. If the surviving joint tenant(s) is not the decedent’s spouse, 100% of the jointly held property is included in the decedent’s taxable estate, unless the surviving joint tenant(s) can prove actual contribution to the property.

Tenancy in Common

Tenancy in common is an arrangement in which each tenant takes an interest in the property. The interests owned by each co-tenant do not have to be equal. Each tenant can sell or bequeath his or her portion of the asset independent of the other tenant(s). Tenancy in common is fre-quently used for joint ownership of property among family members who are not spouses.

Retirement Plan & Individual Retirement Accounts

Naming a beneficiary to your retirement plan or individual retirement account (IRA) permits the benefits to go directly to the named beneficiary, bypassing probate. While at one time these funds enjoyed a special exclusion from the decedent’s estate, they are now generally includible in the decedent’s estate for federal estate tax purposes.

Note: Income tax planning has generally favored naming a spouse as the beneficiary even if the individual has a living trust. The spouse can take advantage of a variety of tax provisions which essentially treat the funds as the spouse’s own retirement account.

Life Insurance

When there is a named beneficiary other than the decedent’s estate, life insurance proceeds “spring” outside of probate. Proceeds from an insurance policy owned by the decedent that go to a named person as beneficiary are excluded from income tax. However, if the decedent owned the policy (or had any incidents of ownership), the proceeds are includible in the decedent’s fed-eral taxable estate even though the proceeds were payable to someone else.

Note: Frequently, an irrevocable insurance trust is used to avoid inclusion of the insurance proceeds in the decedent’s estate.

Gifts

Completed gifts made during one’s life avoid probate and in most cases federal estate tax. Essen-tially what has been given away is gone and is not includible in either the probate or federal estate. If a gift is given to a minor child, the transfer is typically made under the Uniform Transfers to Minors Act (UTMA) or the Uniform Gifts to Minors Act (UGMA). In such a case, the donor placing the asset in the name of a person called the “custodian” makes a gift of property or

1-14

money. Legal title is actually held by the minor. However, the custodian manages the asset until the minor becomes an adult at which time the property is turned over to the minor.

Note: If funds in such an account can be used to pay parental obligations for support, this may be considered taxable income to the parents. In addition, if a parent serves as custodian, such funds may be included in the parent’s estate should he or she predecease the child.

Payable on Death Accounts (POD)

Payable on death bank accounts are often referred to as “Totten” trusts. In either event, the account owner names a beneficiary (or payee) who automatically receives the account balance on the death of the owner. Until the owner dies, the beneficiary has no right to the account. In addition, the owner of the account can change the beneficiary or close the account at anytime. While such an account may be convenient and avoids probate, it saves no federal estate tax.

Transfers Using a Trust

A trust is a legal contract in which one party, the trustor, transfers property to a trustee for the ben-efit of one or more beneficiaries. While there are numerous types of trusts with a variety of charac-teristics, for estate planning purposes the most popular is the living revocable trust.

While a simple living trust will avoid probate, it does not necessarily save any federal income or es-tate taxes. From an income tax standpoint, it is typically classified as a “grantor” trust and the person creating the trust is taxable on its income. In addition, since the trust is typically revocable by the trustor, on the trustor’s death all assets in the trust are included in the trustor’s federal taxable es-tate.

For married couples, a popular type of trust is the “A-B” marital deduction trust. These trusts not only can avoid probate but also can reduce or avoid federal income and estate tax. This is accom-plished through the effective use of the marital deduction and the applicable exclusion amount. For example, such a trust can transfer tax-free to the couples’ heirs up to twice the applicable exclusion amount ($11,700,000 in 2021) plus the growth in up to one-half of their estate.

Note: Testamentary trusts are created by will at the time of the decedent’s death. As a result, tes-tamentary trusts require probate. This is a severe drawback with few offsetting advantages.

Special Planning Tools

The motivation to pass more wealth to survivors and save death taxes while retaining maximum control where possible has generated a variety of specialized estate planning tools. While many of the techniques listed below are more appropriately used for larger estates (i.e., those well in excess of the applicable exclusion amount), given the proper circumstances, they should be considered re-gardless of the size of the estate.

Spending

You may wish to simply spend and use up your estate for your own benefit. You earned it; you spend it. You do not have to leave it to anyone. However, most people are not so aggressive in reducing their estates.

1-15

Annual Gift Tax Exclusion

Up to $15,000 (in 2021) per donee per year can be given without gift tax consequences to each of an unlimited number of recipients. This amount is adjusted for inflation. In addition, an unlim-ited amount may be transferred free of gift tax for qualified tuition and medical expenses. Such gifts do not reduce the donor’s gift tax applicable exclusion amount ($5,000,000 in 2011; $5,120,000 in 2012; $5,250,000 in 2013; $5,340,000 in 2014; $5,430,000 in 2015; $5,450,000 in 2016; $5,490,000 in 2017; $11,180,000 in 2018; $11,400,000 in 2019; $11,580,000 in 2020; and $11,700,000 in 2021) and do not result in income tax to the recipient.

1-16

Gifting Tips

• Avoid Gifts of Future Interests

• Use Gift Splitting

• Make Direct Tuition or Medical

Expense Payments

• Don’t Give Appreciated Property

Shortly Before Death

• Don’t Give Property That May Drop in

Value

• Beware of Kiddie Backfire Tax

• Careful of Gifts of Mortgaged

Property

• Don’t Delay Lifetime Gifts

• Consider Crummy Trusts

• Beware of Generation Skips

• Beware of Transfers With Retained

Interests

• Watch COD on Life Insurance

• Give Power to Make Gifts in POA

• Careful of Donor as Trustee

1-17

The estate planning benefit of such gifts is a reduction in the taxable federal estate by both the original gift and any subsequent appreciation. For large estates, a pattern of gifts should be initi-ated early in order to transfer any substantial funds.

Applicable Exclusion Amount

The applicable exclusion amount is the size of an estate that can pass estate tax-free to one’s heirs. As a result of recent tax law, this amount has gradually risen over several years. In 2009, individuals could transfer a total of $3,500,000 in assets either during their lives or at death with-out paying any federal estate or gift tax. After applying this applicable exclusion amount the es-tate tax rate began at 45%. In 2010, the estate and generation-skipping transfer taxes were re-pealed.

However, in December of 2010, the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (“TRUIRJCA”) reinstated (subject to a special election for 2010) the es-tate and generation-skipping transfer taxes effective for decedents dying and transfers made af-ter December 31, 2009.

Note: This reenactment of the estate tax is in a complicated section of TRUIRJCA that sunsets cer-tain provisions of EGTRRA as if they had never been enacted.

For 2010 and 2011, the estate tax applicable exclusion amount was $5 million: for 2012 the ex-clusion was inflation indexed to $5.12 million. Amounts exceeding this exclusion amount were taxed at 35%. ATRA kept the inflation-indexed exclusion ($11.7 million in 2021) but, permanently increased the top estate, gift, and GST rate from 35% to 40% for transfers over the exclusion.

Spousal Portability of Unused Exemption Amount

Under TRUIRJCA, any applicable exclusion amount that remains unused as of the death of a spouse who dies after December 31, 2010 (the "deceased spousal unused exclusion amount"), is available for use by the surviving spouse, as an addition to such surviving spouse's applicable exclusion amount.

Note: The Act does not allow a surviving spouse to use the unused generation-skipping transfer tax exemption of a predeceased spouse.

If a surviving spouse is predeceased by more than one spouse, the amount of unused exclu-sion that is available for use by such surviving spouse is limited to the lesser of $11.7 million (in 2021) or the unused exclusion of the last such deceased spouse. This last deceased spouse limitation applies whether or not the last deceased spouse has any unused exclusion or the last deceased spouse's estate makes a timely election. A surviving spouse may use the pre-deceased spousal carryover amount in addition to such surviving spouse's own $11.7 (in 2021) million exclusion for taxable transfers made during life or at death.

Note: A deceased spousal unused exclusion amount is available to a surviving spouse only if an election is made on a timely filed estate tax return (including extensions) of the predeceased spouse on which such amount is computed, regardless of whether the estate of the predeceased spouse otherwise is required to file an estate tax return.

1-18

2010 Special Election