Qatar, Bahrain, UAE, Oman, Saudi Arabia, Jordan, Lebanon, Egypt (middle east) tax rules and laws

Upload

robert-chambersCategory

view

224download

0description

Establishing a Property Tax System in Egypt

Robert Chambers Chief Risk Officer

Egyptian Mortgage Refinance Company Cairo, Egypt

1 | P a g e

Abstract

A property tax system is a subsystem of a political/governmental system resting between the government and the taxpayer. Government inputs into the system include property tax policy in the form of laws and regulations, oversight, budgetary requirements and other support to allow for transparency in the system. The market (taxpayer/society) side provides data including information about market activities. The property tax system uses its government provided authority and market inputs to formulate market value estimates, assessed values, property descriptions and tax liabilities.

Egypt, like many other developing economies, has a property tax system founded on antiquated principles and has not been modernized due to a lack of resources, public and political resistance, and the magnitude of the required effort. The foundation of a successful property tax system is a comprehensive, complete property records (cadastral) system.

Generally, property tax systems are dynamic and complex environments. Their main function is to determine who must pay property taxes and the share of total property taxes that each taxpayer should pay. Good land records improve efficiency and effectiveness in collecting land and property taxes by identifying landowners and their properties. A pilot project is recommended as a first step in the creation of a modern cadastral system where the specific property information is integrated with cadastral maps through Geographic Information System (GIS) technology. A mass appraisal system requires effective managers, current technology and skilled appraisers.

Taxpayers must accept the value estimates as reasonable and have confidence in the system. Administration of the valuation program must be efficient. Standardized procedures, quality control, effective public information programs, and attention to consistency help achieve these goals.

2 | P a g e

(Page Intentionally Left Blank)

3 | P a g e

Table of Contents

Introduction ............................................................................................................................................. 4

Section I: The Theory of Market Based Property Tax Systems ................................................................. 5

A. The Property Tax System Environment: ....................................................................................... 5

Figure 1: The Property Tax System Environment ............................................................................ 5

B. Real Property Assessment System ................................................................................................ 6

B.1 Elements: ............................................................................................................................. 6

B.2 Functions: ............................................................................................................................ 6

B.3 Phases: ................................................................................................................................. 6

B.4 Linkages: ............................................................................................................................. 7

Figure 2: Typical Property Tax System ........................................................................................... 7

Section II: The Real World .................................................................................................................... 8

A. The Taxpayer ............................................................................................................................... 8

B. Sources of Valuation Information ................................................................................................. 8

C. Basis of Valuation .......................................................................................................................... 9

C.1 Market Value Approach ............................................................................................................ 9

C.2 Income Value Approach ........................................................................................................... 9

C.3 Unit Approach ........................................................................................................................... 9

C.4 Other Approaches .................................................................................................................... 10

D. Revaluations .......................................................................................................................... 10

E. Indexation .................................................................................................................................. 10

F. Exemptions and Tax Relief ........................................................................................................... 11

G. Tax Appeal Systems .................................................................................................................... 11

H. Tax Collection and Payment ....................................................................................................... 12

Section III: Recommendations for Egypt ........................................................................................... 12

Current Conditions ............................................................................................................................ 12

B. Development of a Modern Cadastral System .................................................................................. 12

C. First Steps ..................................................................................................................................... 13

D. Conclusions ................................................................................................................................. 13

Works Cited .......................................................................................................................................... 14

Appendix A: ........................................................................................ Error! Bookmark not defined.

Appendix B ......................................................................................... Error! Bookmark not defined.

4 | P a g e

Introduction

Under the current tax system in Egypt, periodic real estate tax revenue is generated from agricultural and urban properties based on their rental values. The Real Estate Tax Authority determines rental values. The rent estimation is based on the personal expertise of the authority personnel, where they define the rent as a percentage of the estimated cost of a building. The system has not been modernized with available technologies and property records are often incomplete or missing.

The foundation of a successful property tax system is a complete, comprehensive property records (cadastral) system.

Good land records improve efficiency and effectiveness in collecting land and property taxes by identifying landowners and their properties. Property taxes are relatively easy to collect in contrast, for example, to personal income taxes where earnings can be hidden. It is not possible to hide a piece of land or building although it is possible to conceal the records of such a property.

A real property assessment system is just one component of a property tax system and real estate valuation is a subcomponent of the property assessment system. Generally, property tax systems are dynamic and complex environments. Their main function is to determine who must pay property taxes and the share of total property taxes that each taxpayer should pay. The focus of this concept paper is on market value-based systems and mass appraisal.

5 | P a g e

Section I: The Theory of Market Based Property Tax Systems

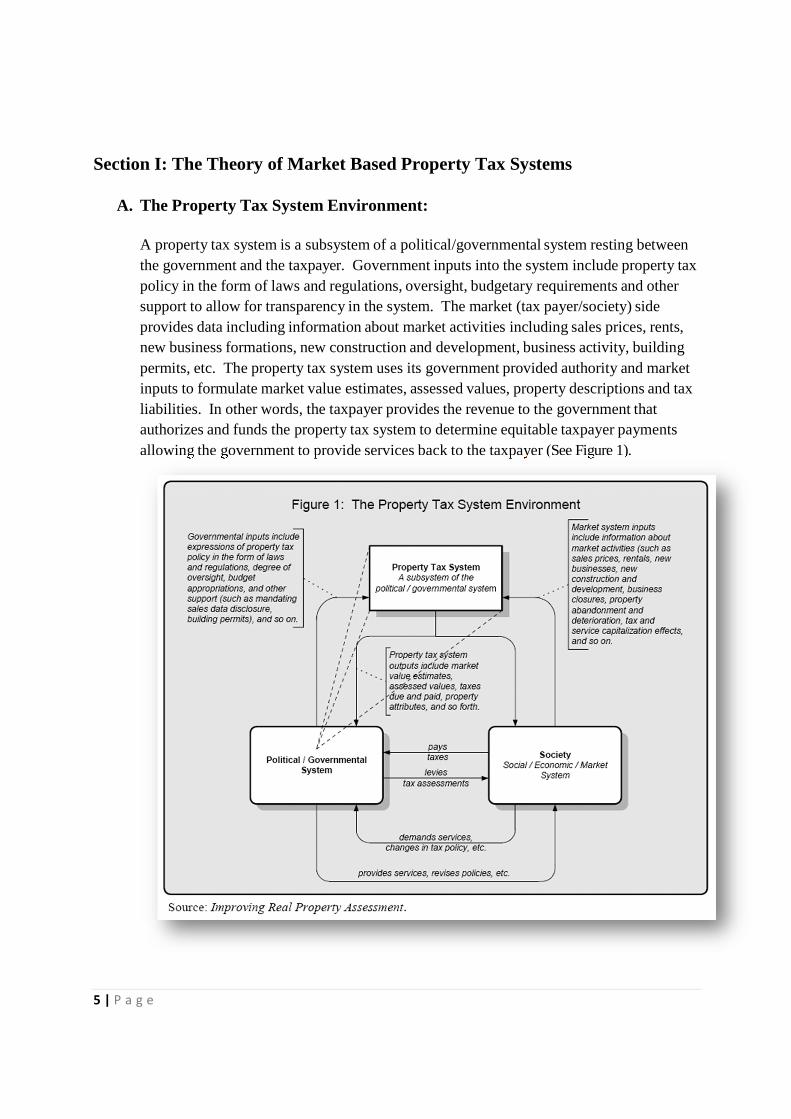

A. The Property Tax System Environment:

A property tax system is a subsystem of a political/governmental system resting between the government and the taxpayer. Government inputs into the system include property tax policy in the form of laws and regulations, oversight, budgetary requirements and other support to allow for transparency in the system. The market (tax payer/society) side provides data including information about market activities including sales prices, rents, new business formations, new construction and development, business activity, building permits, etc. The property tax system uses its government provided authority and market inputs to formulate market value estimates, assessed values, property descriptions and tax liabilities. In other words, the taxpayer provides the revenue to the government that authorizes and funds the property tax system to determine equitable taxpayer payments allowing the government to provide services back to the taxpayer (See Figure 1).

Figure 1: The Property Tax System Environment

6 | P a g e

B. Real Property Assessment System

A real property assessment system is made up of elements, functions, phases and linkages.

B.1 Elements:

Property tax systems consist of people, legislatively enabled policies, technology, data and processes. The legislative and regulatory framework of a property tax system should articulate policy choices, provide the basis for their success and assign responsibilities. Laws, regulations and court decisions establish the legal framework.

B.2 Functions:

A property tax system identifies and links taxpayers to taxable property. It produces tax assessments and, it collects taxes. If any of the three functions are not done properly, tax equality will suffer, revenue generation will most likely suffer and public confidence will erode. A successful property tax system is an equitable one. The fair and equitable apportionment of property tax requires careful planning, efficient use of resources, sufficient data, and, in ad valorum based systems an automated mass appraisal program capable of producing accurate, defensible market based valuations. Along with accurate and equitable valuations, exemptions and other tax relief measures must be applied. Assessment notices and tax bills must be delivered to taxpayers. Taxpayers must be allowed to review their assessments and appeal against them. Appeals need to be processed. Tax payments must be received, accounted for and deposited. Taxpayers must be provided with sufficient information to feel comfortable in the process. The main components of a property tax system are an administrative component, an assessment component and a collection component. The administrative component controls the other two. It dictates powers and responsibilities including the power to tax property. It provides resources and controls and how they are used. The assessment component determines who is to pay a tax and the size of each taxpayer's share. The assessment component may include a valuation system. The collection component bills, receives, accounts for, and distributes property tax payments. It also has the responsibility to ensure compliance.

B.3 Phases:

This is the time dimension of the system. Tax systems are dynamic, not static. Taxation occurs in periodic (usually annual) cycles. Often there are longer intervals between revaluations.

7 | P a g e

B.4 Linkages:

There are the linkages among the property tax system, its stakeholders and other systems. There are internal linkages including assessments, collections and administration. External linkages include taxpayers, the cadastral system, building authorities and real estate professionals. Figure 2: Typical Property Tax System

External Linkage

Source: Lincoln Institute of Land Policy

The main function of a property tax system is to determine who must pay property taxes and each taxpayer’s share. A mass appraisal system requires effective managers, current technology and skilled valuers. Taxpayers must accept the value estimates as reasonable and have confidence in the system. Administration of the valuation program must be efficient. Standardized procedures, quality control, effective public information programs and attention to consistency help achieve these goals.

8 | P a g e

Section II: The Real World

A. The Taxpayer

In most jurisdictions, property taxes are payable by the property owner. In the case of the non-owner occupied property, the owner pays the tax. In some jurisdictions, both the owner and tenant, usually at different rates, pay the property tax. In the property tax systems in emerging economies where the tax is the responsibility of the property owner, a special provision is typically made where, when the state remains the owner of residential or commercial property prior to its return to its former owners or privatization, then the tenant is the taxpayer. Generally, in these jurisdictions, the state is exempt from property taxes and the special provision is seen as a means of ensuring a fair and equitable tax base.

B. Sources of Valuation Information

Many countries have some form of cadastral system for the recording of property related information. The nature and implementation of such systems varies considerably from being a series of different registers administered at various levels of government to a single register administered at the national level. Most countries rely on the use of Computer Assisted Mass Appraisal systems (CAMA) for the storage and processing of information. As part of the assessment process there will typically be an exchange of information between the different levels of government involved and taxpayers will often be requested to supply additional information where appropriate. Even in jurisdictions that have adopted a self-assessment system, central information systems are used to ensure that the information given by the taxpayer is accurate. In these countries, the tax authorities typically have the right to challenge the valuation and substitute their own. The rights of the taxpayer to access centrally held information differs considerably between countries ranging from no rights to being sent notices when a new valuation or alteration is made. In addition, valuation calculations and data may also be made available at the request of the taxpayer. Many countries link their cadastre (or equivalent) to other taxes. For example, the transfer of property whether by sale, gift or inheritance cannot be registered until the cadastre has been updated.

9 | P a g e

C. Basis of Valuation

Three main approaches typically applied for property tax valuation are utilized.

C.1 Market Value Approach

This is normally based on the market value of the property as of a specific date. This may be a current date such as the start of the tax year or as of the date of assessment/reassessment. Market value is usually defined on the basis of a property’s highest and best use. This approach may give rise to potential valuation issues where a property is used for a purpose other than its highest and best use. It may be possible in some cases for the taxpayer to dispute what the highest and best use is, as well as raise arguments as to the value of the current use.

C.2 Income Value Approach

This is normally based on the market rental value of the property as of a specified date. Some jurisdictions specify a baseline date some time before the new rental values come into effect to allow consideration of all market data available before arriving at their valuations. The market rental value may be restricted as to the assumptions that can be made with regard to considerations such as highest and best use. In some jurisdictions, it is not permitted to assume a change of use of a property to a higher and better use nor is one permitted to assume even minor physical changes to the property. The rationale for the approach is that the tax is levied on the tenant and the amount of tax is based on the use to which the property is actually put, not its potential value. One problem that arises with the use of a rental approach is in those instances where some form of rent control restricts the rental value and hence distorts the basis of valuation. The cost approach which is related to the cost of construction is sometimes used and a certain percent of the cost represents rental value. One must not underestimate the considerable difficulties of relating cost to rental value and testing that the resulting value is in line with the market.

C.3 Unit Approach

The unit approach does not relate to a property’s value, neither market nor rental but rather to its size. The tax is then levied at a prescribed rate per square meter or per unit, which may vary depending on the use of the property. These rates may be loosely based on rental or market values but are more often an arbitrary rate fixed by the appropriate

10 | P a g e

taxation authorities. This approach is more common in emerging economies where markets and record systems are less developed and market data is scarce. In most cases, it is the intention of the property tax system to change to a value based system when conditions allow. Often emerging economies have adopted the unit approach due to a lack of property and market information, a limited and restricted property market as well as insufficient resources to enable the development of market based systems. The move to a value based system will typically take place when resources and circumstances permit.

C.4 Other Approaches

Numerous other approaches are applied across the world. One is that of the market value banding approach This approach is based on property being assigned to a specific group rather than valuing each individual property. Another approach is indexing where a specific type of property is valued based on a property value index.

D. Revaluations

In order for the property tax system to remain fair and equitable, parcels must be reassessed on a periodic basis. There are certain problems associated with the lack of a regularly updated tax base. Many countries have either no provision for regular revaluations of the tax base or have postponed such revaluations. As a result, the tax base bears little resemblance to the value on which it is stated to have been based, be it market or rental value. The lack of an up-to-date tax base undermines the taxpayer’s confidence in the tax system and can have other unexpected consequences. For example, other taxes or legislation may be linked directly or indirectly the annual property tax assessment. For example, compensation to tenants for improvements to rented property or for loss of tenure is related to a multiplier of the assessed value. In cases of mandatory purchase, compensation is again related to the assessed value. In other countries, the amount of gift tax is related to the annual property tax assessment. In these cases, the assessed market value is taken to be the value of the gift thus removing the need for an additional valuation of the property at the time of making the gift.

E. Indexation

Many countries have attempted to overcome the problems associated with infrequent revaluations by some form of indexation. Where annual indexation between regular revaluations of say 4 or 5 years may ensure a relatively accurate tax base its use becomes

11 | P a g e

more questionable when the base has not been updated for 10 or 20 years. The position is made far worse, where the property market is changing rapidly. Market Values and market rents of property can be increased annually by an index to ensure the owner/tenant is paying a tax based on the market value or rental value of the property. In most countries, a consumer price based index is often adopted. No index can truly be applicable for all areas of the country where values are changing at different rates in different geographic areas. For local taxation purposes, the same issues apply. Any index adopted needs to be closely related to the property market in that location and for the specific property type. In most cases, the index is a single figure applied across the whole of the country and for all types of property. This can lead to further distortions when comparing the real values to assessment values.

F. Exemptions and Tax Relief

While there can be many variations, the subject of exemptions can be considered from two perspectives:

• Exemptions given due to the nature of the taxpayer

• Exemptions given due to the nature of the property Countries may adopt either or both approaches. Some common features can be identified as to the types of properties where some form of relief or exemptions may be granted. Examples include land owned by the state and used for providing public services, such as schools, hospitals, cemeteries etc., land and property used for religious purposes, historic buildings and agricultural land. With regard to taxpayer exemptions, they can include tax relief for the elderly, economically disadvantaged and the disabled. Tax relief in the form of either a separate rate or residential exclusion is typically applied. Most countries have developed systems that satisfy their individual needs and are often closely linked with other forms of taxation or state aid and benefits.

G. Tax Appeal Systems

Most countries have some form of system by which the taxpayer may challenge the tax assessment. Many jurisdictions allow an informal approach to the taxing authority where differences may be resolved without the need for a more formal approach. Where a formal approach is required, two approaches seem common. One is where the appeal is dealt with as part of the general tax appeal process and will go through the public court system. The second is where the appeal is dealt with in courts and hearings established especially

12 | P a g e

for tax appeal purposes. The challenge of a tax assessment or valuation typically does not postpone the payment of the tax in the specific jurisdiction.

H. Tax Collection and Payment

Generally, there are two approaches for tax collections. One is where the tax is collected by a national tax administration often as part of the income tax process. Where this occurs, it is recognized that the taxes are not considered an income tax but the approach is used on the grounds of ease of collection for both the taxpayer and the tax collectors. This approach also has the advantage that it can be linked with any national tax relief and benefits which the taxpayer may be entitled. The second is where the tax is paid directly to the local tax authorities. These authorities may also act on behalf of lower tier authorities with respect to tax collection. In these cases, taxpayers can usually pay the tax in a series of installments. There is a wide range of different approaches to payment by installments as regards both the timing and the amount of each installment.

Section III: Recommendations for Egypt

Current Conditions

It does not appear that Egypt has a comprehensive and equitable property tax system. Based on preliminary research, it appears periodic property tax revenue is generated from agricultural and urban properties based on their rental values. Rental values are determined by The Real Estate Tax Authority. The estimate of rent is based on the personal expertise of the tax authority personnel, where rent is often defined as a percent of the estimated cost of building. The system has not been modernized with available technologies and property records are often incomplete or missing. The foundation of a successful property tax system is a comprehensive, complete property records cadastre and use of CAMA technologies.

B. Development of a Modern Cadastral System

The foundation of a fair and equitable property tax system is a modern property information system including accurate land and building descriptions and spatial database. The Egyptian government is encouraging the development of a real estate and mortgage industry as well as foreign investments. One-step in this development is the completion of modern cadastre, including both spatial data, individual property descriptions and legal and administrative attributes. The efforts to reach this goal on a

13 | P a g e

national basis will be substantial. There must be coordination and co-operation between all government authorities involved. Once a modern, comprehensive system in its place with accurate property information, a fair and equitable property tax system can be implemented.

C. First Steps

A pilot project should be developed to create a local modern cadastral system where the specific property information is integrated with cadastral maps through GIS technology. A specific geographic area should be identified where property ownership can, for the most part, be clearly defined. The pilot project area can then be mapped and descriptive property and ownership information can be compiled. If the authorities decide to adopt a market based system (vs. a unit-based system), market data must also be compiled in the project area. Once the pilot project is completed, it can be expanded to a broader geographic area.

D. Conclusions

Egypt, like many other developing economies, has a property tax system founded on antiquated principles and has not been modernized due to a lack of resources, public and political resistance, and the magnitude of the required effort. The foundation of a successful property tax system is a comprehensive, complete property records cadastral system. A pilot project is recommended as a first step in the creation of a modern cadastral system where the specific property information is integrated with cadastral maps through GIS technology. Generally, property tax systems are dynamic and complex environments. Their main function is to determine who must pay property taxes and the share of total property taxes that each taxpayer should pay. Good land records improve efficiency and effectiveness in collecting land and property taxes by identifying landowners and their properties. A mass appraisal system requires effective managers, current technology and skilled appraisers. Taxpayers must accept the value estimates as reasonable and have confidence in the system. Administration of the valuation program must be efficient. Standardized procedures, quality control, effective public information programs, and attention to consistency help achieve these goals.

14 | P a g e

Works Cited

Almy, R. (2000). A Survey of Property Taxation Systems in Europe. London: Lincoln Institute of Land Policy.

Almy, R. (2002). Real Property Assessment System. Cambridge: Lincoln Institute of Land Policy.

Baker & McKenzie. (2000). 1999 Survey of Effective Tax Burdensin the European Union, Real Estate Investment in Central and Eastern Europe. Chicago: Price, Waterhouse, Coopers.

Brzeski, J. (2001). Europe in Transition: Property Taxation Challenges in Central and Eastern Europe. Washington D.C.: World Bank.

Gloudemans, R. (1999). Mass Appraisal of Real Property. Chicago: International Association of Assessing Officers.

Hepworth, M. (1991). Pros and Cons of Local Taxation. Cambridge: Institute of Revenue Rating and Valuation.

Joseph Eckert, R. G. (1978). Improving Real Property Assessment: A Reference Manual. Chicago: International Association of Assessment Officers.

Kelly, R. (2000). Property Taxation in East Africa: The Tale of Three Reforms. Nairobi: Shelter Afrique.

Snarski, R. D. (2007). Technical Communications in the Information Age. Acton: Copley Custom Textbooks.