Essentials of Estate Planning: What You Need to Know Presented by: Joseph D. Serrano.

28

Essentials of Estate Planning: What You Need to Know Presented by: Joseph D. Serrano

-

Upload

curtis-patrick -

Category

Documents

-

view

215 -

download

0

Transcript of Essentials of Estate Planning: What You Need to Know Presented by: Joseph D. Serrano.

Essentials of Estate Planning:

What You Need to Know

Presented by:Joseph D. Serrano

2

• Estate planning is a process.

• After having been created, your plan should be monitored, re-evaluated, and updated regularly.

• You are the one in control of the entire process.

3

INITIAL QUESTIONS

• Do you care who receives your assets when you die?

• Do you want someone to handle your children's assets if you die while they are still minors?

• Do you care who will raise your children in the event of your death?

• Do you wish to minimize the taxes owed on your estate, as well as the burden upon your heirs as to paying them?

• Do you care about who will manage your assets if you become disabled?

4

• Your Estate Planning Team, which consists of:– Your Family– Your Accountant– Your Financial Planner– Your Estate Planning Attorney– Your Religious Advisor

Who will help me put together my estate plan?

5

What is my “estate”?• Your estate is simply everything you own.• It includes:

– your home– other real estate– frequent flyer miles– bank accounts– investments– retirement benefits from your employer– IRAs– insurance policies– collectibles– personal belongings (such as jewelry)– business interests

What is my “estate”?

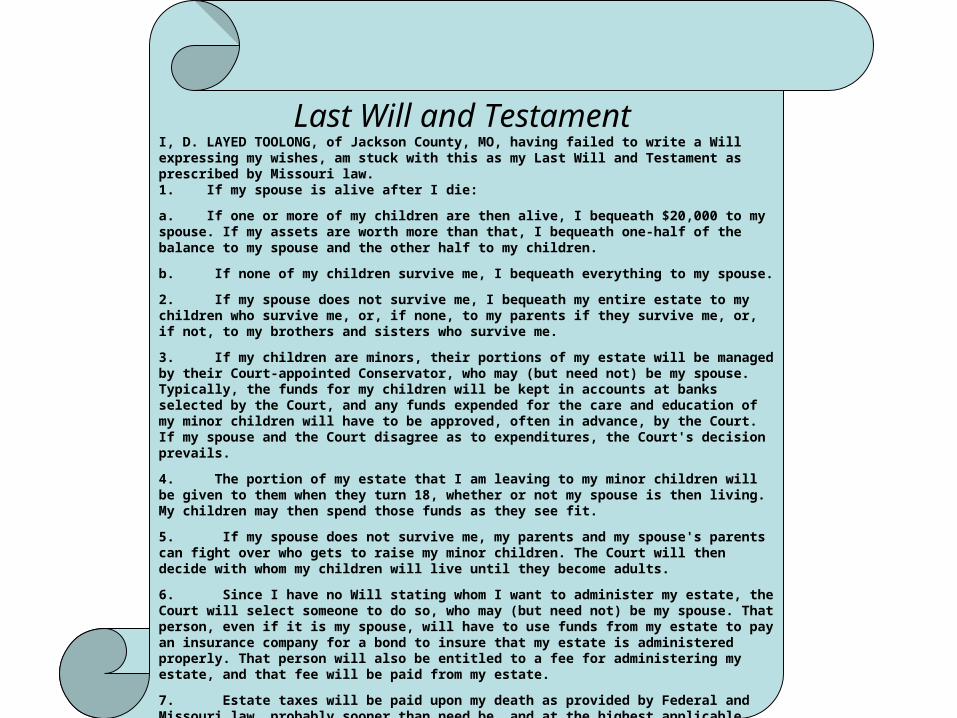

Last Will and Testament I, D. LAYED TOOLONG, of Jackson County, MO, having failed to write a Will expressing my wishes, am stuck with this as my Last Will and Testament as prescribed by Missouri law.1. If my spouse is alive after I die:

a. If one or more of my children are then alive, I bequeath $20,000 to my spouse. If my assets are worth more than that, I bequeath one-half of the balance to my spouse and the other half to my children.

b. If none of my children survive me, I bequeath everything to my spouse.

2. If my spouse does not survive me, I bequeath my entire estate to my children who survive me, or, if none, to my parents if they survive me, or, if not, to my brothers and sisters who survive me.

3. If my children are minors, their portions of my estate will be managed by their Court-appointed Conservator, who may (but need not) be my spouse. Typically, the funds for my children will be kept in accounts at banks selected by the Court, and any funds expended for the care and education of my minor children will have to be approved, often in advance, by the Court. If my spouse and the Court disagree as to expenditures, the Court's decision prevails.

4. The portion of my estate that I am leaving to my minor children will be given to them when they turn 18, whether or not my spouse is then living. My children may then spend those funds as they see fit.

5. If my spouse does not survive me, my parents and my spouse's parents can fight over who gets to raise my minor children. The Court will then decide with whom my children will live until they become adults.

6. Since I have no Will stating whom I want to administer my estate, the Court will select someone to do so, who may (but need not) be my spouse. That person, even if it is my spouse, will have to use funds from my estate to pay an insurance company for a bond to insure that my estate is administered properly. That person will also be entitled to a fee for administering my estate, and that fee will be paid from my estate.

7. Estate taxes will be paid upon my death as provided by Federal and Missouri law, probably sooner than need be, and at the highest applicable rates.

In Witness Whereof, not having cared enough to properly execute a document setting forth my desires, I wind up with this as my Will. /signed/ D. Layed Toolong

7

Who are the key persons in your Will?

• Family, friends and, if appropriate, charitable organizations

• Guardians• Executors• Trustees

8

Lifetime Documents

• Powers of Attorney:– Durable Powers of Attorney– Springing Powers of Attorney

• Health Care Proxies/Living Wills• HIPAA Releases

9

Death and Taxes

• For transfers at death: Federal exemption is presently $2,000,000 (scheduled to increase to $3,500,000 by 2009)

• For lifetime gifts: Federal gift exemption is frozen at $1,000,000

• State estate, inheritance and gift tax laws vary and have to be taken into account separately

10

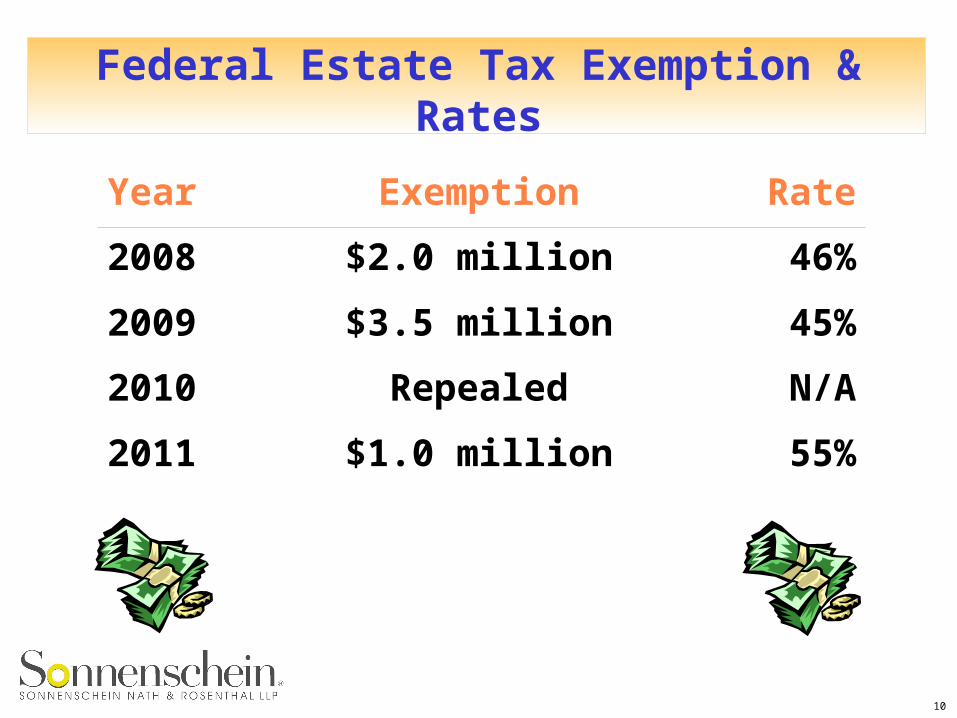

Federal Estate Tax Exemption & Rates

Year Exemption Rate

2008 $2.0 million 46%

2009 $3.5 million 45%

2010 Repealed N/A

2011 $1.0 million 55%

11

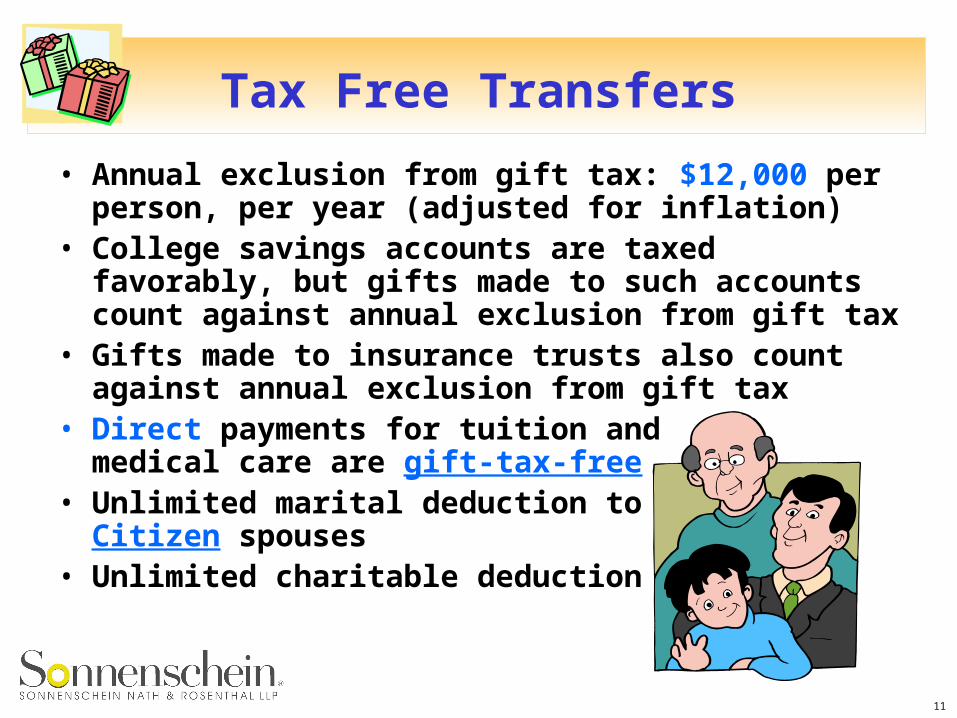

Tax Free Transfers

• Annual exclusion from gift tax: $12,000 per person, per year (adjusted for inflation)

• College savings accounts are taxed favorably, but gifts made to such accounts count against annual exclusion from gift tax

• Gifts made to insurance trusts also count against annual exclusion from gift tax

• Direct payments for tuition andmedical care are gift-tax-free

• Unlimited marital deduction to Citizen spouses

• Unlimited charitable deduction

12

State Estate and Inheritance Taxes

• Before 2001, state death taxes were relatively uniform, and (usually) were fully credited against the federal estate tax.

• The federal credit for state death taxes has been phased out and replaced by a deduction.

• Overall, death taxes in many states appear to be higher than they were before. They vary with the residence of the decedent and the situs of the assets.

The Federal Estate Tax for CouplesWith Assets of $4,000,000 or Less

(Death in 2008)

14

Example 1Spouse A has assets of $4,000,000; Spouse B has assets of $0. Spouse A dies first with a Will leaving everything to Spouse B (or everything is held in joint names):

A. When Spouse A dies:

Spouse A’s assets $4,000,000

Less federal estate tax 0

Amount passing to Spouse B $4,000,000

Spouse B’s assets 0

Assets supporting Spouse B $4,000,000

B. When Spouse B dies:

Spouse B’s assets $4,000,000

Less federal estate tax 920,000

Amount passing to children $3,080,000

15

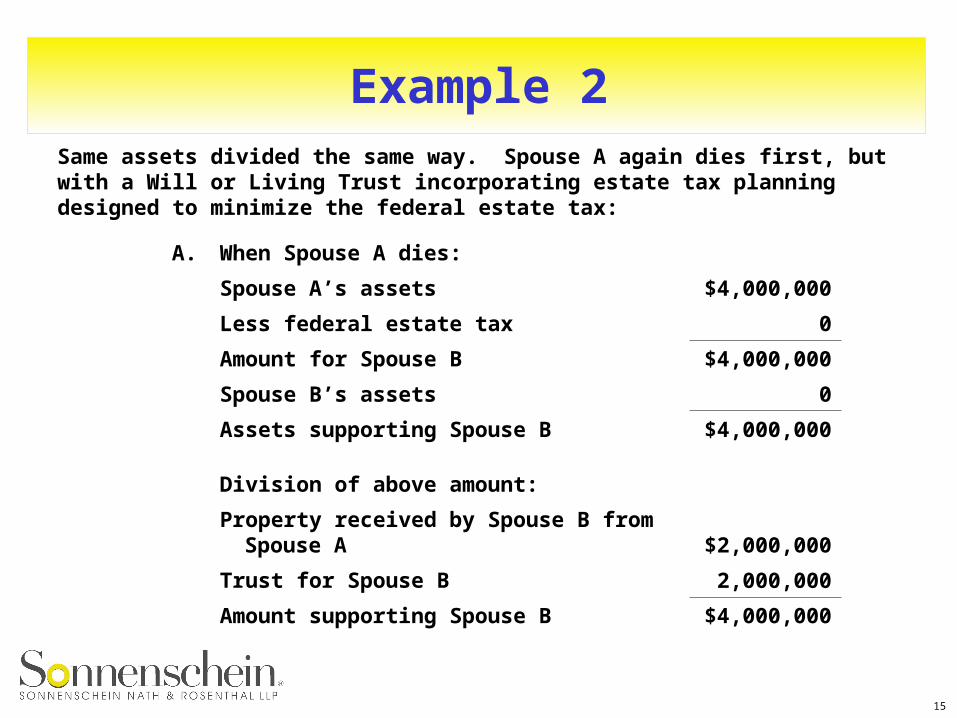

Example 2Same assets divided the same way. Spouse A again dies first, but with a Will or Living Trust incorporating estate tax planning designed to minimize the federal estate tax:

A. When Spouse A dies:

Spouse A’s assets $4,000,000

Less federal estate tax 0

Amount for Spouse B $4,000,000

Spouse B’s assets 0

Assets supporting Spouse B $4,000,000

Division of above amount:

Property received by Spouse B from Spouse A $2,000,000

Trust for Spouse B 2,000,000

Amount supporting Spouse B $4,000,000

16

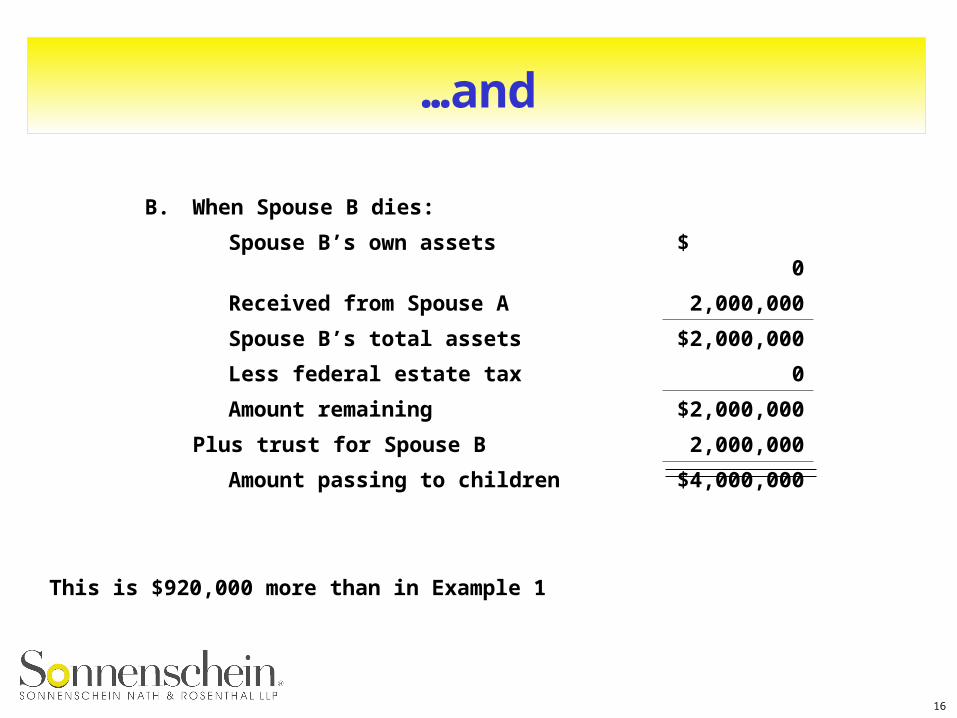

B. When Spouse B dies:

Spouse B’s own assets $ 0

Received from Spouse A 2,000,000

Spouse B’s total assets $2,000,000

Less federal estate tax 0

Amount remaining $2,000,000

Plus trust for Spouse B 2,000,000

Amount passing to children $4,000,000

…and

This is $920,000 more than in Example 1

17

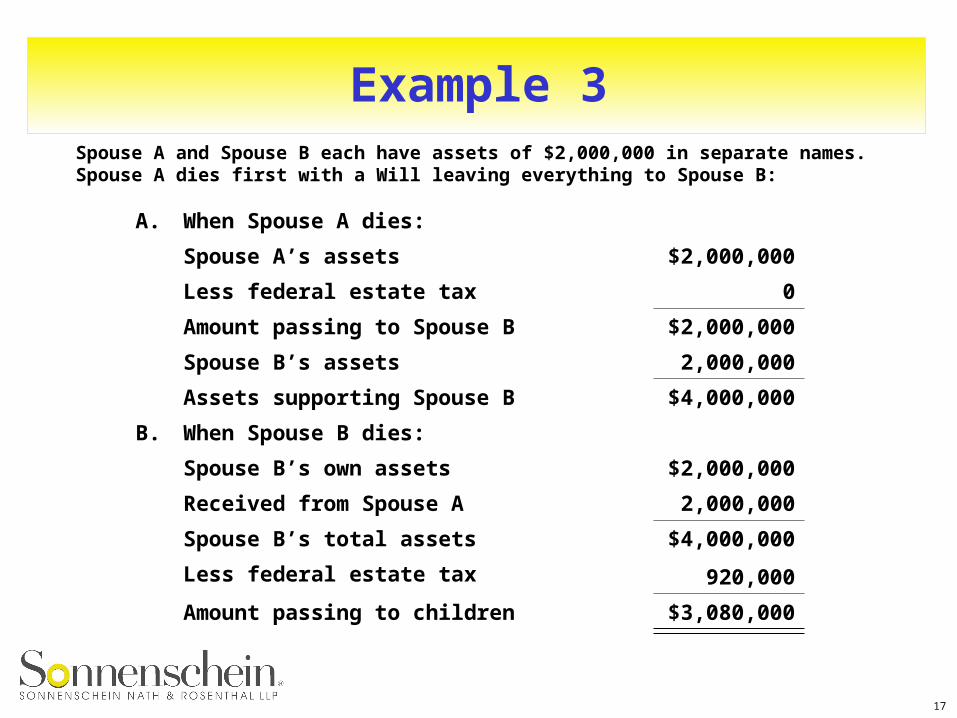

Example 3Spouse A and Spouse B each have assets of $2,000,000 in separate names. Spouse A dies first with a Will leaving everything to Spouse B:

A. When Spouse A dies:

Spouse A’s assets $2,000,000

Less federal estate tax 0

Amount passing to Spouse B $2,000,000

Spouse B’s assets 2,000,000

Assets supporting Spouse B $4,000,000

B. When Spouse B dies:

Spouse B’s own assets $2,000,000

Received from Spouse A 2,000,000

Spouse B’s total assets $4,000,000

Less federal estate tax 920,000

Amount passing to children $3,080,000

18

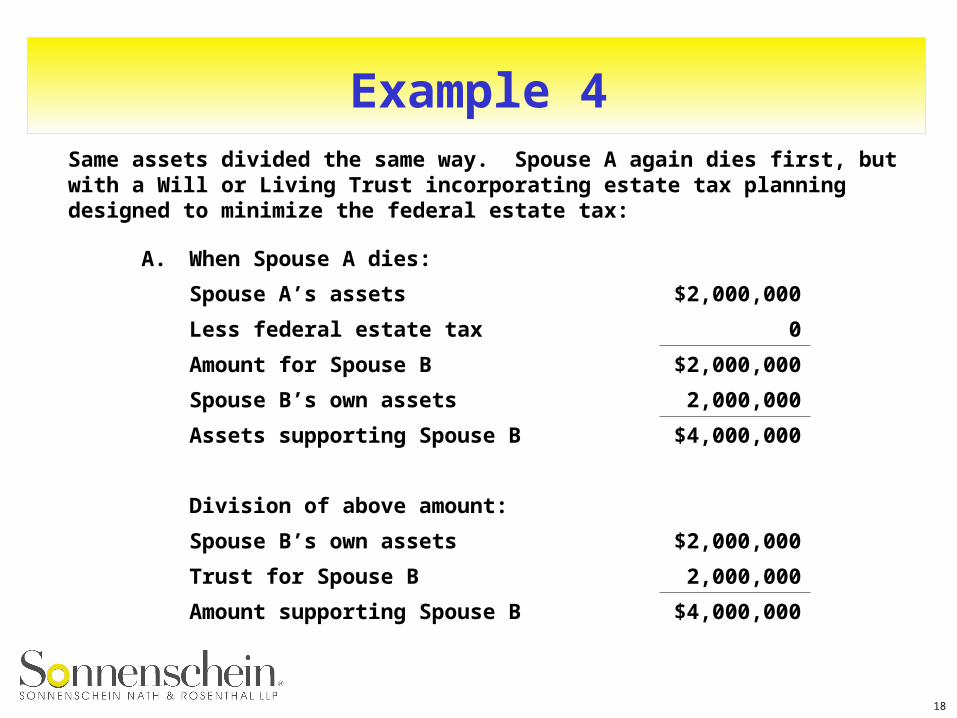

Example 4Same assets divided the same way. Spouse A again dies first, but with a Will or Living Trust incorporating estate tax planning designed to minimize the federal estate tax:

A. When Spouse A dies:

Spouse A’s assets $2,000,000

Less federal estate tax 0

Amount for Spouse B $2,000,000

Spouse B’s own assets 2,000,000

Assets supporting Spouse B $4,000,000

Division of above amount:

Spouse B’s own assets $2,000,000

Trust for Spouse B 2,000,000

Amount supporting Spouse B $4,000,000

19

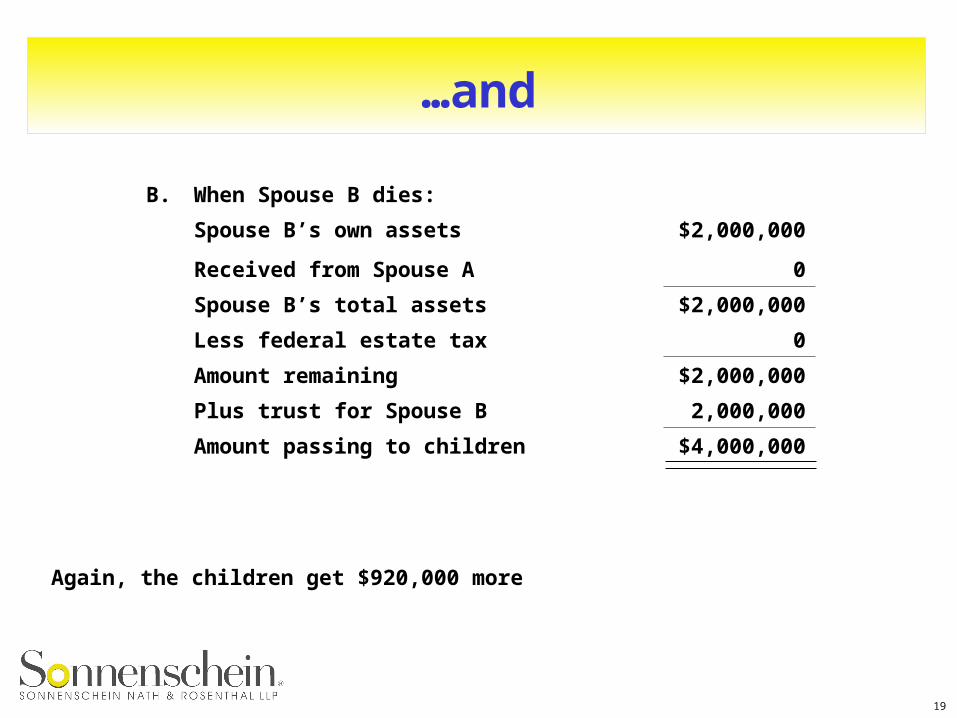

B. When Spouse B dies:

Spouse B’s own assets $2,000,000

Received from Spouse A 0

Spouse B’s total assets $2,000,000

Less federal estate tax 0

Amount remaining $2,000,000

Plus trust for Spouse B 2,000,000

Amount passing to children $4,000,000

…and

Again, the children get $920,000 more

20

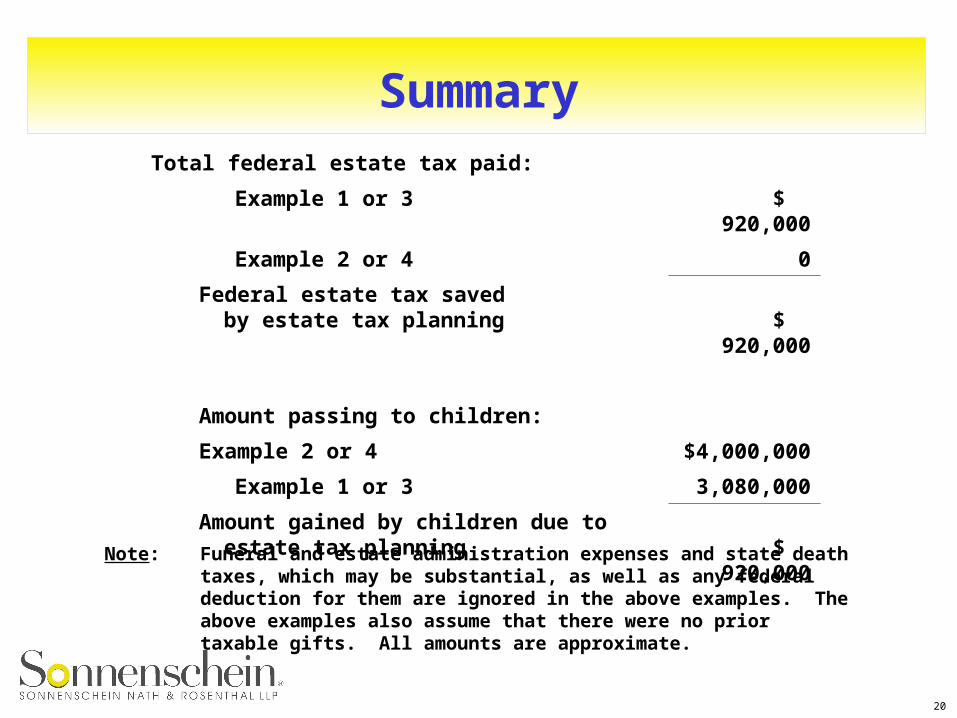

SummaryTotal federal estate tax paid:

Example 1 or 3 $ 920,000

Example 2 or 4 0

Federal estate tax saved by estate tax planning $ 920,000

Amount passing to children:

Example 2 or 4 $4,000,000

Example 1 or 3 3,080,000

Amount gained by children due to estate tax planning $ 920,000

Note: Funeral and estate administration expenses and state death taxes, which may be substantial, as well as any federal deduction for them are ignored in the above examples. The above examples also assume that there were no prior taxable gifts. All amounts are approximate.

Would you rather leave Would you rather leave $920,000$920,000

to your childrento your childrenor to youror to your

“Uncle Sam”“Uncle Sam”??

22

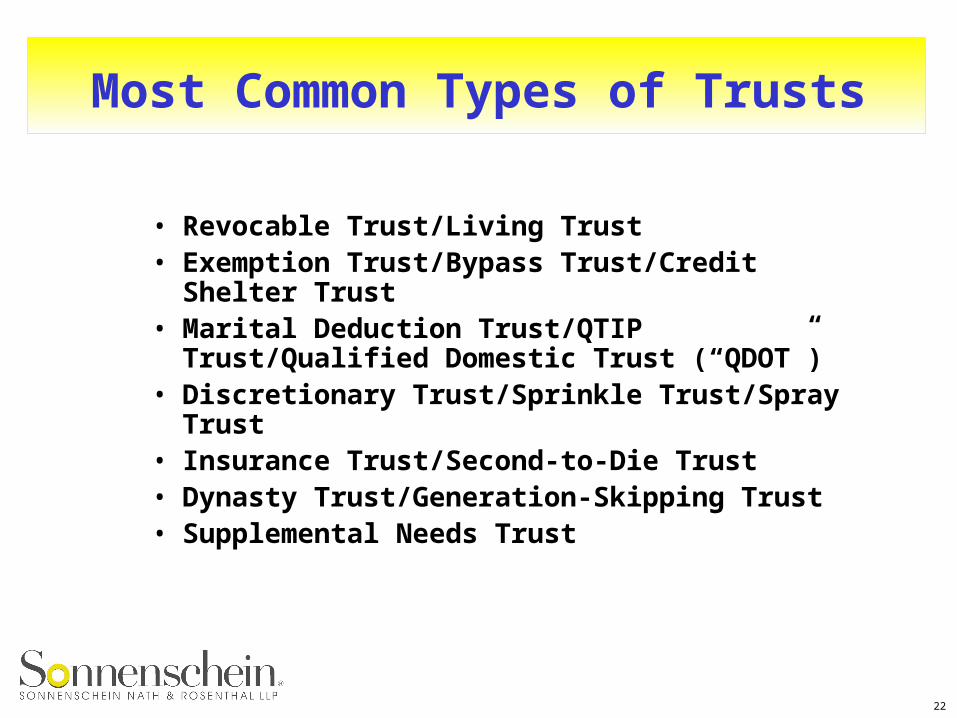

Most Common Types of Trusts

• Revocable Trust/Living Trust• Exemption Trust/Bypass Trust/Credit Shelter

Trust• Marital Deduction Trust/QTIP Trust/Qualified

Domestic Trust (“QDOT”)• Discretionary Trust/Sprinkle Trust/Spray Trust• Insurance Trust/Second-to-Die Trust• Dynasty Trust/Generation-Skipping Trust• Supplemental Needs Trust

23

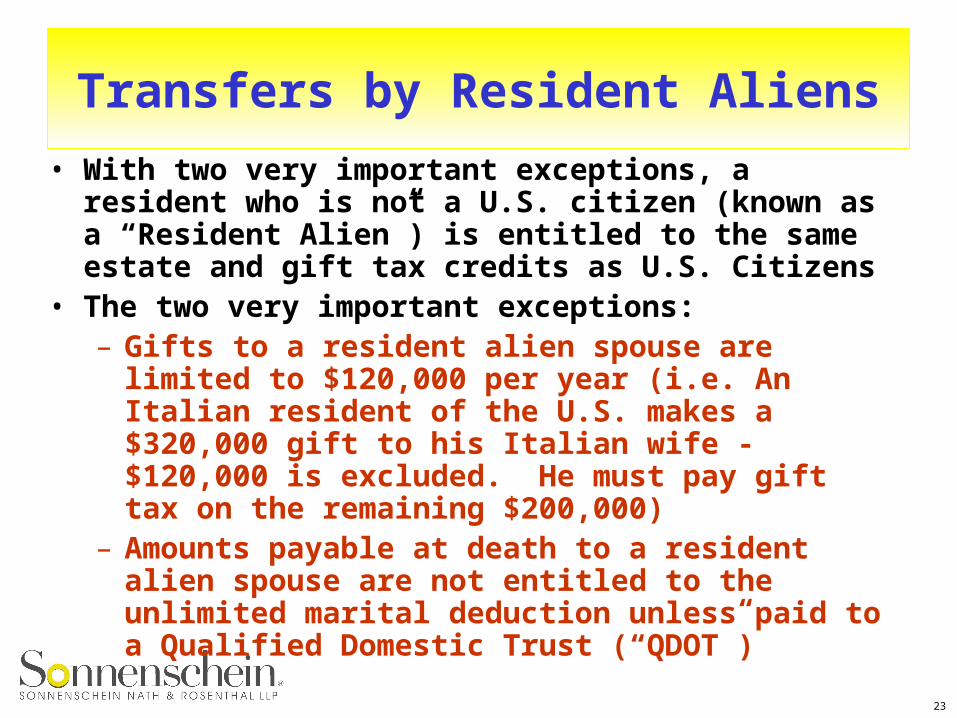

Transfers by Resident Aliens

• With two very important exceptions, a resident who is not a U.S. citizen (known as a “Resident Alien”) is entitled to the same estate and gift tax credits as U.S. Citizens

• The two very important exceptions:– Gifts to a resident alien spouse are limited to

$120,000 per year (i.e. An Italian resident of the U.S. makes a $320,000 gift to his Italian wife - $120,000 is excluded. He must pay gift tax on the remaining $200,000)

– Amounts payable at death to a resident alien spouse are not entitled to the unlimited marital deduction unless paid to a Qualified Domestic Trust (“QDOT”)

24

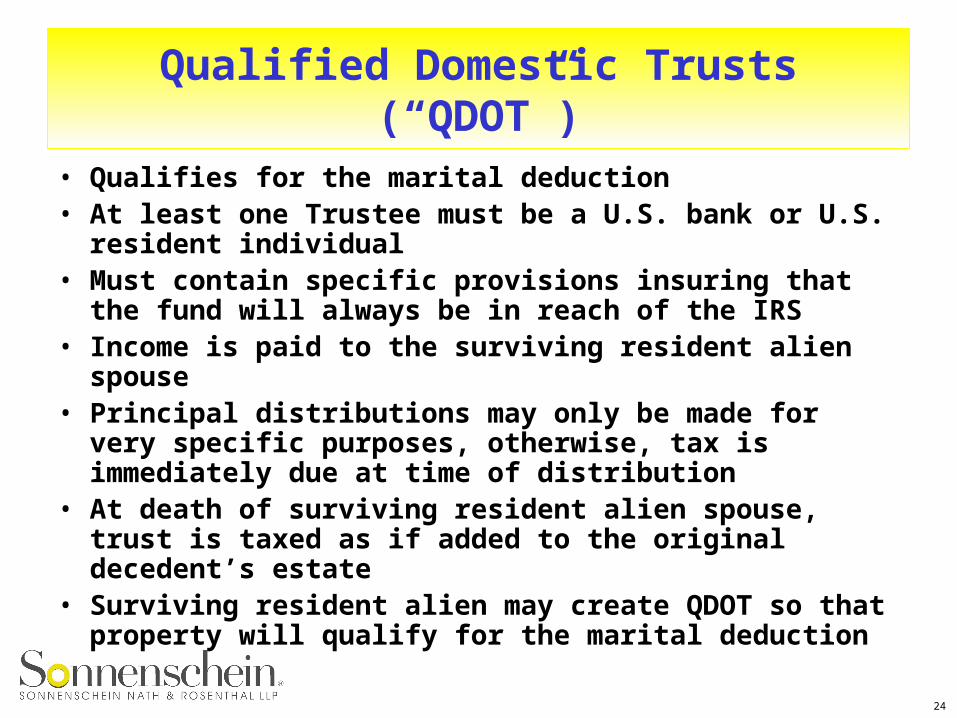

Qualified Domestic Trusts(“QDOT”)

• Qualifies for the marital deduction• At least one Trustee must be a U.S. bank or U.S.

resident individual• Must contain specific provisions insuring that the fund

will always be in reach of the IRS• Income is paid to the surviving resident alien spouse• Principal distributions may only be made for very

specific purposes, otherwise, tax is immediately due at time of distribution

• At death of surviving resident alien spouse, trust is taxed as if added to the original decedent’s estate

• Surviving resident alien may create QDOT so that property will qualify for the marital deduction

25

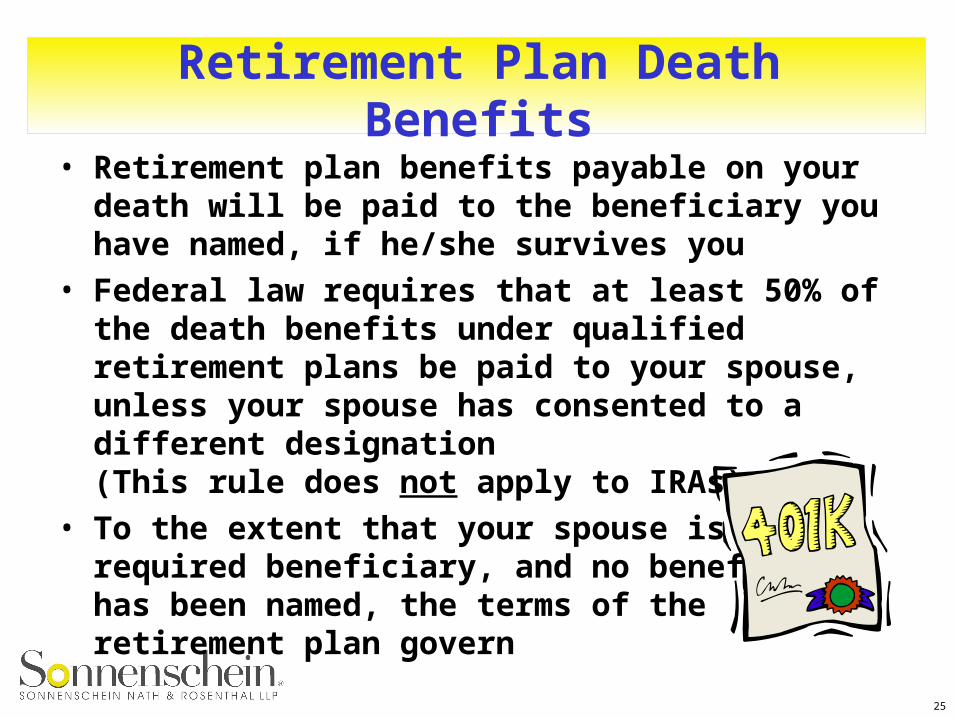

Retirement Plan Death Benefits

• Retirement plan benefits payable on your death will be paid to the beneficiary you have named, if he/she survives you

• Federal law requires that at least 50% of the death benefits under qualified retirement plans be paid to your spouse, unless your spouse has consented to a different designation (This rule does not apply to IRAs)

• To the extent that your spouse is not a required beneficiary, and no beneficiary has been named, the terms of the retirement plan govern

26

Three Primary Goalsof Retirement Planning

• Identify funds needed and available for retirement income

• Evaluate savings and investment strategies needed to meet retirement income objectives

• Integrate retirement plans into income and estate tax planning

27

Tax Planning at Retirement

• Defer income taxes for as long as possible

• Maintain as much flexibility as possible with respect to investments and distributions

• Minimum distribution rules during life

28

Tax Planning at First Death

• Qualify benefits for Federal estate tax marital deduction

• Consider how to take advantage of the exemptionif retirement plans constitute a majority of estate assets

• Continue income tax deferral and flexibility– Spousal IRA rollover– Long term post death payout

• Minimum distribution rules at death