eSmart Tax issue 7

32

THE DIGITAL BUSINESS AND WEALTH MANAGEMENT MAGAZINE eSmartTax April // May // June 2009 A BUDGET FOR BUSINESS BUDGET 2009 AT A GLANCE TAXING TIMES The corporate survival guide making the right decisions in today’s challenging business environment introduction of a new penalty regime 2009/10 tax tables what do the numbers mean to you? Tackling a potential inheritance tax issue now is a great time to discuss your problem with us Weathering the current economic downturn a significant contribution to the continued health of your business A major opportunity to limit tax crystallising losses could work to your advantage Budget 2009 small-scale initiatives Value Added Tax alleviating short term pressure on companies

-

Upload

steve-wright -

Category

Documents

-

view

226 -

download

2

description

The digital tax news magazine

Transcript of eSmart Tax issue 7

THE DIGITAL BUSINESS AND WEALTH MANAGEMENT MAGAZINE

eSmartTaxApril // May // June 2009

A BUDGET FOR BUSINESS BUDGET 2009 AT A GLANCE TAXING TIMES

The corporatesurvival guide

making the right decisions in today’s

challenging business environment

introduction of a new penalty regime

2009/10 tax tableswhat do the numbers mean to you?

Tackling a potential inheritance tax issuenow is a great time to discuss your problem with us

Weathering the current economic downturna significant contribution to the continued health of your business

A major opportunity

to limit taxcrystallising losses could work to your advantage

Budget 2009small-scale initiatives

Value Added Tax

alleviating short term pressure on companies

Welcome to the latest issue of our business and wealth management magazine. Inside this issue we look at the relatively small-scale initiatives announced for business by the chancellor Alistair Darling during Budget 2009. The announcements included a new £750m strategic investment fund, reforms to the taxation of foreign profits, a boost to capital allowances to encourage new investment and a number of energy-related measures. Turn to pages 5 and 6 to read our Budget 2009 business coverage.

The fall in the value of assets such as shares, buy-to-let properties and holiday homes to their lowest levels in years, combined with capital gains being taxed at its lowest rate in 40 years, may be prompting more and more taxpayers to give away surplus assets to minimise future inheritance tax (IHT) bills. If you are considering tackling a potential IHT issue we consider your options on page 9.

Since the start of this current tax year, on page 13 we consider the significant changes in taxation and benefits that now apply and on page 24 the introduction of a new Value Added Tax (VAT) penalty regime.

At the time of publishing, the global financial crisis and events are changing very quickly, and some further changes are likely to have occurred by the time you read this issue. A full content listing appears on page 3.

inside this

issue

02

Content of the articles featured in this publication is for your general information and use only and is not intended to address your particular requirements or constitute a full and authoritative statement of the law. They should not be relied upon in their entirety and shall not be deemed to be, or constitute advice. Although endeavours have been made to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No individual or company should act upon such information without receiving appropriate professional advice after a thorough examination of their particular situation. We cannot accept responsibility for any loss as a result of acts or omissions taken in respect of any articles.

14

0508

13

1710To discuss your specific

requirements or to obtain further information, please contact us.

If you would like us to email a copy of our digital magazine to someone you know, please email us with their details and we’ll send them a copy.

1905

060808

10

09

1113

14

16

18

18

18

20

20

22

24

28

26

28

29

3006

Inside this issueBudget 2009 small-scale initiativesAlleviating short term pressure on companies

Budget 2009 at a glanceWere you a winner or a loser?

A Budget for business? The highlights

Corporate Financial PlanningObjective professional advice

Tackling a potential inheritance tax issueNow is a great time to discuss your problem with us

2009/10 tax tablesWhat do the numbers mean to you? Taxing timesTax facts

Significant changes in taxation and benefitsHow the new rules could affect your finances

Self-Invested Personal PensionsYour questions answered

Struggling to maintain cashflow levels? A guide to making sure your business gets paid on time

A major opportunity to limit taxCrystallising losses could work to your advantage

Self-employmentNew penalties if you are late in notifying HMRC that you have commenced self-employment

Credit levels continue to declineSmall and medium-sized businesses don’t expect the situation to improve in the next quarter

Corporate fundingOne solution for small firms experiencing real cash flow difficulties

Weathering the current economic downturnA significant contribution to the continued health of your business

Small firms struggle with UK tax lawsThree quarters find it difficult to find information about regulations

The corporate survival guideMaking the right decisions in today’s challenging business environment

Value Added TaxIntroduction of a new penalty regime

Looking to raise money in the recession? In such a competitive market it’s vital to be well prepared

Research and DevelopmentTax incentives encourage innovation in the UK

VAT GlossaryThese are some definitions of common VAT terms that HMRC uses

Legal structuresPutting your business on a proper footing

Getting in good shape to survive the downturnKey areas around which small businesses should consider taking action

03

If you would like us to email a copy of our digital magazine to someone you know, please email us with their details and we’ll send them a copy.

Explore your business and wealth management options...tell us what you need?

Click Here *

APRIL / MAY / JUNE 2009 05

David Frost, director general of the British Chambers of Commerce, added: “There are some good measures for business at a micro level, but we still think Darling’s forecasts are over-optimistic. What has really taken people aback is the sheer scale of borrowing and worry about how it will be clawed back.”

Gilbert Toppin, chief executive of the EEF manufacturers’ federation, said: “Given the most difficult economic conditions for a generation, the chancellor has gone some way towards alleviating short term pressure on companies. However, the growth forecasts look overly optimistic and there

is a serious danger that if these fail to come to fruition business will pay the price in higher taxes.”

Business is likely to be moderately pleased with a doubling of the main capital allowance for investment to 40 per cent in 2009/10. A two-year extension of provisions to allow

companies to carry forward tax losses over three years was also announced.

In addition there will be a top-up scheme for companies that have had difficulty getting adequate trade credit insurance, but the chancellor ignored pleas from some business organisations for a scheme to subsidise the wages of workers on short time. Tax credits were already boosting the earnings of staff on shorter hours, he said.

He gave the motor industry a £2,000 cash incentive to trade in 10-year-old cars for new ones, but insisted that car companies must bear half the cost.

Budget 2009 small-scale initiativesAlleviating short term pressure on companies

There were relatively small-scale initiatives announced for business by the chancellor Alistair Darling during Budget 2009. The announcements included a new £750m strategic investment fund, reforms to the taxation of foreign profits, a boost to capital allowances to encourage new investment, plus a number of energy-related measures including incentives to advance production from small North Sea oil fields and to encourage offshore wind farms.

NeeD MORe INFORMATION?PLEASE CONTACT US WITH YOUR ENQUIRY.

Business is likely to be moderately pleased with a doubling of the main capital allowance for investment to 40 per cent in 2009/10.

If you would like us to email a copy of our digital magazine to someone you know, please email us with their details and we’ll send them a copy.

The economy is forecast to contract by 3.5pc in 2009, but growth is expected to resume “towards the end of the year” according to the chancellor.

Take a look at our guide and see how your finances could be affected by Budget 2009.

Budget 2009 highlights The Economy – GrowthThe UK economy contracted by 1.6pc in the last quarter of 2008. GDP growth for the year as a whole expected to be -3.5pc.

Growth forecast of 1.25pc in 2010. From 2011, the economy will continue to recover with growth of 3.5pc from then on. In future years the economy will recover towards a trend rate of growth of around 2.75pc.

Inflation is expected to reach 1pc by the end of this year. The Bank of England inflation target remains unchanged at 2pc. RPI inflation is forecast to remain negative, falling to minus-3pc by September, before moving back above zero next year.

The Economy - Borrowing UK figures for public sector net borrowing will be £175bn this year, 12.4pc of GDP. From 2010, borrowing will fall to £173bn, then £140bn, £118bn and £97bn.

As a share of GDP, borrowing will be 11.9pc next year, 9.1pc in 2011/12, then 7.2pc in 2012/13 and 5.5pc in 2013/14.

UK net debt, including the cost of stabilising the banking system, will as a share of GDP increase from 59pc this year to 68pc next year, 74pc in 2011/12, then 78pc and 79pc in subsequent years. It will stabilise and then begin to fall in 2015/16.

The UK’s current deficit is expected to halve within four years.

Income tax New 50pc tax rate introduced for those earning more than £150,000 to take effect from April 6, 2010.

Personal allowances to be fully withdrawn for those with incomes over £100,000 from April 6, 2010.

No income tax increases this year.

Pensions From April 2011, pension tax relief for those with incomes over £150,000 will be restricted so it is gradually tapered to the 20pc rate.

Basic state pension increased by at least 2.5pc, regardless of the Retail Price Index.

Capital disregard on Pension Credit is to be raised from £6,000 to £10,000 from November 2009.

Education £250m will be provided this year and £400m in 2010/11 for an additional 54,000 places in sixth form and further education colleges, with consequential provisions for Scotland, Wales and Northern.

06

Were you a winner or a loser?

Budget 2009 at a glance

APRIL / MAY / JUNE 2009

The chancellor Alistair Darling unveiled plans during his second Budget Report to increase taxes for the highest paid, rein in public spending and substantially increase borrowing to restore the public finances.

07APRIL / MAY / JUNE 2009

Housing The stamp duty holiday on properties sold for less than £175,000 will be extended until the end of 2009.

An extra £80m is to be given to the HomeBuy Direct, the government’s shared equity mortgage scheme.

An extra £1bn will be provided to help homeowners and boost housing.

A scheme will be introduced to guarantee securities backed by mortgages in a bid to increase lending.

£500m of extra financial support will be provided for housing projects, including £100m for councils to build new energy-efficient housing.

£50m to accelerate the modernisation of housing for military families.

Environment£435m extra support for energy efficiency measures for homes, businesses and public places.

Additional £1bn to help combat climate change by supporting low-carbon industries and green jobs.

£525m of new support will be given over the next two years for offshore wind projects.

£405m to encourage low-carbon energy and advanced green manufacturing in Britain to drive new technology and investment in small-scale projects.

Most energy-efficient new power stations using combined heat and power (CHP) technology to be exempt from climate change levy.

Jobs An additional £1.7bn for Job Centre Plus and the New Deal is to be provided.

Additional support for people who have been out of work for 12 months.

From next January everyone under the age of 25 who has been jobless for 12 months will be offered a job or a place in training.

£260m of new money allocated for training and subsidies for young people to help them gain skills and experience.

Statutory redundancy pay will increase from £350 to £380 a week.

WelfareThe child element of the Child Tax Credit to increase by £20 from April next year.

£100 extra for child trust fund vouchers for new babies with disabilities, extra £200 for those with severe disabilities.

Grandparent care for young relatives to count towards basic state pension.

Last year’s increase in winter fuel allowance to be extended for another year, £250 for over-60s and £400 for over-80s.

SavingsAnnual Individual Savings Account limit to be increased from £7,200 to £10,200, half of which can be invested in cash. New limit introduced this year for over-50s, next year for all other savers.

Pensioners Pensioners’ Winter Fuel Allowance is to be kept at the higher level of £250 for over-60s and £400 for over-80s for another year.

Tax avoidance The aim is to raise £1bn of

extra revenue over the next three years by closing tax loopholes and schemes.

Government Efficiency savings from 2011 are expected to give a further £9bn of additional savings a year by 2013/14.

Financial services Treasury paper to be published with recommendations for wide-ranging reform of financial services, including action to reduce the impact of the failure of financial firms.

MotoringA car scrappage scheme introduced from this May to provide motorists with a £2,000 discount on new vehicles bought when they trade in cars over 10 years old. The scheme will end in March 2010.

Other announcements Alcohol duties increased by 2pc.

Tobacco duty increased by 2pc.

Fuel duty will increase by 2p per litre in September and then by 1p a litre above indexation each April for the next four years.

A Budget for business?

APRIL / MAY / JUNE 200908

Reacting to the Chancellor’s Budget speech, Richard Lambert, CBI Director-General, said:

”We are disappointed that the chancellor had nothing to say on next year’s increase in National Insurance Contributions for employers which is a tax on jobs, and he has not reversed the policy on empty properties.

“Rates on empty property have forced companies to cut staff, and can make the difference between surviving the downturn and going to the wall.

“The government should also look at postponing the reintroduction of the 17.5pc VAT rate by a month to cover the New Year sales period.”

Business highlights at a glance

Loss-making companies can reclaim taxes paid on profits made in the past three years to November 2010.

Extension of scheme allowing businesses to defer tax bills.

Support for companies’ cashflow, with a top-up trade credit insurance scheme to match private sector trade credit insurance provision.

Businesses’ main capital allowance rate doubled to encourage firms to bring forward investment.

New £750m investment fund to provide financial support to emerging technologies and regionally important sectors in advances businesses.

Enhanced tax relief to support investment of £50bn this year, including £10bn to support the communications sector and extend the broadband network.

Incentives to encourage smaller North Sea oil fields to be brought into production.

During this period of economic downturn it’s crucial that all businesses consider their corporate financial planning requirements. Talk to us about our comprehensive planning service designed to meet the distinct and changing needs of you and your business.

We can assess and recommend planning actions to enhance and protect your business interests.

n Comprehensive planning servicen Corporate Financial Planning Review and Advice n Pre year end profit extraction and Directors Remuneration/

Dividends n Exit Tax Planning n Directors Pensions and Small Self Administered Schemes n Shareholder Protection and Keyman Insurance n Employee Benefits n Employee Share Schemes n Business Insurance

Whatever the size of your business, if you require objective professional advice on corporate financial planning, please contact us for further information.

The highlights

Corporate Financial Planning

If you would like us to email a copy of our digital magazine to someone you know, please email us with their details and we’ll send them a copy.

NeeD MORe INFORMATION?PLEASE CONTACT US WITH YOUR ENQUIRY.

APRIL / MAY / JUNE 2009 09

TThis current slump in asset values may present appropriate taxpayers with a rare

opportunity to pass on assets while paying substantially reduced capital gains tax (CGT). The reduction in the CGT rate from up to 40pc to a flat rate of 18pc in April last year will also reduce the potential tax bill on assets gifted away. For lifetime gifts, the value of assets for IHT purposes is determined at the time they are given away, so while valuations are low, it is worth considering the advantages of gifting assets now.

So long as the gift is an outright gift to an individual and the donor

survives seven years after making the gift, there will be a significant long-term tax saving. And with the IHT rate at 40pc, the long-term tax saving could be very significant. If there is a risk that IHT becomes due on gifts made

prior to death, it is important for taxpayers to consider making gifts while asset values are low.

Lifetime gifts use up the nil-rate band first upon death within 7 years. This will affect the allowances and the actual tax paid on the estate. The nil-rate band is the amount up to which an estate will have no IHT to pay and is currently if you are single £325,000 (2009/10), or are married or in a civil partnership £650,000 (2009/10).

Inheritance tax glossary…the basics Assets Generally, everything that you own.

Beneficiary A person, or organisation, to whom you leave a gift in your Will.

Estate The total sum of your possessions, including property and money, left at your death once any debts have been paid.

Inheritance tax (IHT) The 40pc tax paid on an estate that is over the nil-rate band threshold. The current 2009/10 threshold is £325,000 for an individual. Married couples or those in a civil partnership have a combined threshold of £650,000.

Intestate The term for someone dying without having a Will in place. In this case the Rules of Intestacy will decide to whom your estate is passed.

Nil rate band The amount of your estate on which IHT is not payable. For the tax year 2009/10 this is £325,000, and for married couples or those in a civil partnership £650,000.

Potentially exempt transfer A gift made during one’s lifetime that is exempt from IHT should the donor live for seven years after making the gift.

Trust An arrangement you can make in your Will to administer part of your assets after your death.

Will A form of instruction as to how someone wishes to dispose of their assets on death.

Tax benefits may vary as a result of

statutory change and their value will

depend on individual circumstances.

Thresholds, percentage rates

and tax legislation may change in

subsequent finance acts.

Tackling a potential IHT issueNow is a great time to discuss your problem with us

The fall in the value of assets such as shares, buy-to-let properties and holiday homes to their lowest levels in years, combined with capital gains being taxed at its lowest rate in 40 years, may be prompting more and more taxpayers to give away surplus assets to minimise future inheritance tax (IHT) bills. If you are considering tackling a potential IHT issue, now is a great time to discuss this with us.

Taxpayers waste £190m every year on unnecessary IHT payments, according to financial research company Defaqto.

If you wish to discuss how we could help you mitigate a potential IHT liability and safeguard the wealth of your estate for your heirs, now is the perfect time to consider the options available to you. For more information, please contact us.

APRIL / MAY / JUNE 200910

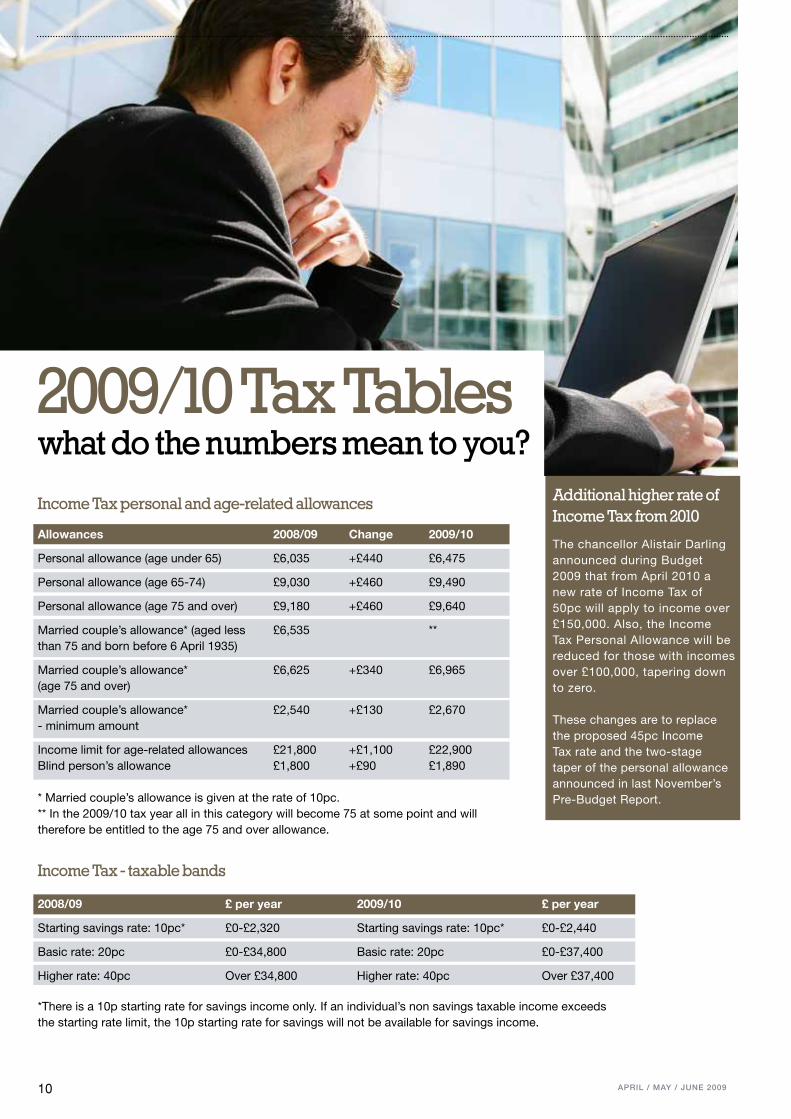

2009/10 Tax Tableswhat do the numbers mean to you?

Income Tax personal and age-related allowances

Allowances 2008/09 Change 2009/10

Personal allowance (age under 65) £6,035 +£440 £6,475

Personal allowance (age 65-74) £9,030 +£460 £9,490

Personal allowance (age 75 and over) £9,180 +£460 £9,640

Married couple’s allowance* (aged less £6,535 **than 75 and born before 6 April 1935)

Married couple’s allowance* £6,625 +£340 £6,965(age 75 and over)

Married couple’s allowance* £2,540 +£130 £2,670- minimum amount

Income limit for age-related allowances £21,800 +£1,100 £22,900Blind person’s allowance £1,800 +£90 £1,890

* Married couple’s allowance is given at the rate of 10pc.** In the 2009/10 tax year all in this category will become 75 at some point and will therefore be entitled to the age 75 and over allowance.

Additional higher rate of Income Tax from 2010

The chancellor Alistair Darling announced during Budget 2009 that from April 2010 a new rate of Income Tax of 50pc will apply to income over £150,000. Also, the Income Tax Personal Allowance will be reduced for those with incomes over £100,000, tapering down to zero.

These changes are to replace the proposed 45pc Income Tax rate and the two-stage taper of the personal allowance announced in last November’s Pre-Budget Report.

Income Tax - taxable bands

2008/09 £ per year 2009/10 £ per year

Starting savings rate: 10pc* £0-£2,320 Starting savings rate: 10pc* £0-£2,440

Basic rate: 20pc £0-£34,800 Basic rate: 20pc £0-£37,400

Higher rate: 40pc Over £34,800 Higher rate: 40pc Over £37,400

*There is a 10p starting rate for savings income only. If an individual’s non savings taxable income exceeds the starting rate limit, the 10p starting rate for savings will not be available for savings income.

APRIL / MAY / JUNE 2009 11

New VAT flat rate scheme guidance New guidance has been issued by HM Revenue & Customs (HMRC) on the VAT flat rate scheme and, in particular, changes have been introduced concerning businesses wishing to deregister. Businesses should consider whether or not they may be better-off by operating within the Scheme.

The main aim of the Flat Rate Scheme is to reduce the cost of complying with VAT obligations by simplifying the VAT calculation for small businesses; instead of paying HMRC the total VAT charged on invoices minus any input VAT that may be reclaimed, businesses are charged a fixed percentage of their gross turnover and pay that amount to HMRC each year.

New HMRC enforcement powersHMRC “believe that it is reasonable to expect a person who encounters a transaction or other event with which they are not familiar, to take care to check the correct tax treatment, or seek suitable advice. We expect people to take their tax seriously.”

As an incentive to ensuring that a taxpayer takes tax seriously, HMRC now have the following powers:

Three new powers to gather informationWritten notice may be given to a person requiring them to provide information or produce documentation reasonably required for the purpose of checking their tax position. Information includes explanations, schedules or documents which may be more than six years old, and/or which do not already exist.

A third party notice may be given to a person requiring them to provide information or produce documents reasonably required for the purpose of checking another person’s tax position.

An “Identity Unknown Notice” may be given to a person requiring them to provide information or produce documentation reasonably required for the purposes of checking the UK tax position of an unknown individual or a class of persons whose identities are unknown.

Compliance check powersPowers to enter business premises and inspect the premises (but not by forced entry), business assets and statutory records. Where an information notice has been issued, these documents may be required for inspection at the same time. An inspection will only take place if “reasonably required to establish the tax position” of the taxpayer.

Usually inspections will be by mutually agreed appointment, but HMRC do have powers to make unannounced visits where they establish that there may be a strong risk that business assets or documents may be removed or destroyed.

The new rules also apply to inspection of a residential property which is partly used for business purposes. HMRC’s powers do not extend to the inspection of premises used solely as a dwelling.

Penalties for inaccuraciesTaxpayers, who file incorrect tax returns (on or after 1st April 2009 for periods starting on or after 1st April 2008), or need to pay more tax or repay a refund as a result of an enquiry, may be charged a penalty.

Penalties will apply unless the taxpayer takes “reasonable care.”

This will include keeping accurate records, understanding the position and informing HMRC about any error.

The new regime is intended to discourage concealment of inaccuracies. Mitigation of penalties is based on the quality of the disclosure, which includes giving information and helping HMRC regarding the inaccuracy. Reduced penalties will apply if an unprompted disclosure is made.

Internal review processA new review process operated internally in respect of most HMRC decisions. The taxpayer or his agent may request a review of the decision, and that review will be undertaken by a specially trained member of HMRC staff, who is independent of the individual working on the case.

The intention is to provide a fresh pair of eyes, a more cost effective means of resolving disputes and an additional safeguard. If agreement is still not achieved as a result of the review, the option of progressing matters to a Tribunal is available.

The Tax Tribunal ProcessThe General and Special Commissioners are replaced by a new Tribunal service operated by the Ministry of Justice. The new service replaces the separate system for direct taxes and VAT. There is the First Tier Tribunal and the Upper Tier Tribunal. The new appeal hearings will fall into four categories: Complex, Standard, Basic and Paper.

Taxing times Tax facts

NeeD MORe INFORMATION?PLEASE CONTACT US WITH YOUR ENQUIRY.

We serve a wide range of business clients...and we’re passionate about providing tailored advice.Our range of corporate services are extensive, including financial guidance and assistance for organisations.

Contact us to discuss how we could take away your tax headache, or visit our website for further information.

APRIL / MAY / JUNE 2009 13

Since the start of this current tax year on April 6, there have been some significant changes in taxation

and benefits that now apply. In September last year, Alistair Darling, the chancellor, raised the annual personal allowance, the amount that you can earn before you pay tax for those under the age of 65 to £6,035. This was to compensate those people who had been disadvantaged after the abolition of the 10p tax rate.

During this current 2009/10 tax year, if you are under the age of 65 the allowance has been increased to £6,475. In addition there has also been a £5-a-week rise in the starting point for paying primary Class 1 national insurance contributions (Lower earnings limit), from £90 (£4,680 a year) to £95 (£4,940).

There is also an increase in the personal allowance and the starting point for national insurance, plus an additional rise in the higher-rate threshold, to £37,400, for higher-rate taxpayers.

However, this is set to change next year following the chancellor’s announcement delivered during the Budget Report on April 22. The previously planned introduction of a new 45pc income tax rate from April 2011, on income over £150,000 will now be brought forward by a year and the rate will increase to 50pc.

In addition, the personal tax allowance will be withdrawn for those earning more than £100,000 from next April, instead of a year later. From April 2011, the exchequer also intends to restrict pension tax relief for those with incomes above £150,000.

How the new rules could affect your finances

Significant changes in taxation and benefits

News

Whatever the size of your business, if you require objective professional advice on corporate financial planning and employee benefits, please contact us for further information.

In September last year, Alistair Darling, the

chancellor, raised the annual personal allowance, the amount that you can earn before you pay tax for those under the age of 65 to £6,035.

NeeD MORe INFORMATION?PLEASE CONTACT US WITH YOUR ENQUIRY.

APRIL / MAY / JUNE 200914

SelF-InveSTed PerSonal PenSIonS Your questions answered

Changes to the pension rules in April 2006 (known as ‘A-Day’) enabled

individuals to invest higher contribution levels and made it easier to set up a Self-Invested Personal Pension (SIPP), a tax-efficient wrapper into which you can put a range of investments chosen by you to achieve your future personal financial goals.

SIPPs are personal pensions which allow more sophisticated investors to choose where you want your retirement savings to be invested, instead of leaving a pension company to make the decisions. You can hold a wide variety of investments in a SIPP,

from investment funds and shares to commercial property and futures and options.

When you reach retirement, you can take an income direct from your pension fund, in the form of a so-called ‘unsecured pension,’ which may give you greater control over how and when you take income from your fund.

SIPPs share the same benefits as personal and stakeholder pensions. They enjoy tax relief at either basic or higher rate tax, your contributions will accumulate and from the age of 50 (or 55 after 2010) you can claim a tax-free lump sum and income from your SIPP. The tax treatment

will depend on your individual circumstances and may be subject to change in the future.

Q: Who can take out a SIPP?A: You can take out a SIPP even if you are already contributing to another pension, such as an occupational (company) pension scheme, providing you don’t exceed the maximum pension contribution limits. But it is important to be sure that you are really going to make use of the investment freedom a SIPP offers and that it makes financial sense for you to do so as some SIPPs could be more expensive than other types of pensions.

It’s not something we usually contemplate during our working lives, but many of us could spend almost a third of our life in retirement. Even if your retirement isn’t on the near horizon it’s never too early to start planning. A pension is one of the most effective ways to save for your future because of the tax benefits they offer.

APRIL / MAY / JUNE 2009 15

Q: How much can I contribute to a SIPP?A: It is generally recommended that you should have an existing pension fund of around £50,000 to transfer or invest lump sums of several thousand pounds a year.

Since April 2006, the maximum amount that you can contribute to your pension each year and qualify for tax relief is the equivalent of 100 per cent of your taxable earnings (called net relevant earnings), subject to an annual limit of £245,000 and an overall lifetime limit for your pension pot of £1.75m. (These are the limits for the tax year 2009/10 and will be increased in future tax years).

A reason why people may wish to consider transferring their previous pension policies into a SIPP is to consolidate their retirement savings in one place and thereby benefiting from easier administration and the possibility of more cost-effective charges.

Q: What investments can I include in a SIPP?A: These are the main investments permitted, that can be included in a SIPP:

n Deposit accounts (in any currency providing they are with a UK deposit taker)

n Government securities and other fixed interest stocks

n Unit trusts n Open ended investment

companies (OEICs) n Investment trusts n Insurance funds n UK stocks and shares

including shares listed on the Alternative Investment Market (AIM)

n Overseas stocks and shares quoted on a Recognised Stock Exchange

n Unquoted shares n Commercial property n Ground rents in respect of

commercial property n Traded endowment

policies n Permanent Interest

Bearing Shares (PIBS) n Warrants n Futures and Options

Q: How much could I expect to receive from a SIPP?A: The amount of pension you receive at retirement from a SIPP will depend on how much you invest, the growth of your investments, how much is deducted in charges and annuity rates (if you decide to convert your fund into an annuity at age 75).

SIPPs offer a wider range of investment options compared with personal and stakeholder pensions. You receive income tax relief on your contributions and the investments in your SIPP grow virtually tax-free. You can take a tax-free lump sum, plus an income from your SIPP between the ages of 50 and 75, although from 2010 the minimum age at which you can take retirement benefits increases to 55.

Q: How can I invest in property via a SIPP?A: One of the attractions of SIPPs is that they can be used to invest and develop commercial property, such as offices, industrial units or shops. Your pension fund does not even have to be large enough to buy a property outright as you can borrow up to 50 per cent of the fund’s net value. It is not

possible to invest directly in residential property via a SIPP, although a commercial property with a residential element such as a caretaker’s flat may be permitted.

By far the greatest demand for property investment within a SIPP is from small business people who want to buy their own business premises. Changes to the pension rules in April 2006 mean such purchases are now possible even if the property is already owned by the investor or someone connected to them.

Buying your own business premises within a SIPP can have several tax advantages. The rent paid into your SIPP is free of tax because it is a tax deductible expense. There will be no capital gains tax to pay on the property when it is sold within the pension fund and if you die before age 75 and before you start drawing your pension, your beneficiaries can receive the proceeds of the sale of the property free of inheritance tax.

Q: How do I move my existing pensions into a SIPP?A: If you contact your chosen SIPP provider and give them details of your previous pensions, they will arrange for the transfer of your funds into your SIPP. However, it is vital to take professional advice first.

Your previous pensions may also include guaranteed annuity rates which could give you a higher pension than would be available if you were to switch, or there may be a large penalty for transferring.

If you are considering switching from an occupational scheme, you may also be at risk giving up some valuable benefits such as spouse’s and dependants’

pensions as well as ill health and early retirement benefits.

If part of your pension has been built up from National Insurance rebates as a result of being opted out of the State Earnings Related Pension Scheme (SERPs) or the State Second Pension (S2P), these funds cannot currently be transferred into a SIPP but must be invested into an insurance plan.

Q: What are the alternatives to a SIPP?A: If your main concern is to be able to spread your pension savings among a variety of different investment groups rather than being tied to one set of funds offered by your pension company, a cheaper solution than a SIPP could be an ordinary personal pension where you are offered a wide choice of external managers.

The value of investments and the income from them can go down as well as up and you may not get back

your original investment. Past performance is not a guide to future performance. Tax

benefits may vary as a result of statutory change and their

value will depend on individual circumstances. Thresholds,

percentage rates and tax legislation may change in subsequent finance acts.

Planning for a successful retirement requires professional advice to ensure that you fully achieve your retirement goals. For more information about the services we provide and the options available to you, please contact us.

APRIL / MAY / JUNE 200916

Struggling to maintain cashflow levels?A guide to making sure your business gets paid on time

APRIL / MAY / JUNE 2009 17

35pc of the businesses surveyed estimated that late payments cost them in excess of £10,000 a year both in terms of bank charges and the administrative costs of chasing payments, even before the additional practical difficulties of day-to-day cashflow control are taken into account.

The average amount owed in late payments rose by a third in 2008, bringing the average amount owed by UK companies to around £40,000.

Initiatives that business owners can implement to address this issue:

1. Agree realistic payment terms upfrontStandard credit terms should be defined by how quickly you have to pay for materials and provide services; payment terms should be part of standard terms and conditions, contracts and every invoice.

2. Make it easy to be paidThose with difficult payment processes are more likely to be affected, ensure clarity as to whom payments should be made to, how they should be made and provide bank details to accept BACS payments.

3. Credit check new customersBackground checks on new customers will help with your planning and decision-making with regard to the provision of any services. Credit reference agencies offer a valuable source of information, while you can also consider insuring trade debts.

4. Have a clear procedure for credit controlEnsure communication lines are kept open and a clear procedure for credit control is maintained, polite but insistent reminder letters should be sent on a regular and consistent basis.

5. Don’t be afraid to take actionLate payment is a significant threat to your business and should be reacted to as such - chasing late payments is vital to survival in the current climate. It is also important to know who to chase for late payments and leave a trail by using email and faxes in case you have to take collective action.

NeeD MORe INFORMATION?PLEASE CONTACT US WITH YOUR ENQUIRY.

More than 60pc of entrepreneurs are struggling to maintain cashflow

levels due to delays or defaults on the payment of creditors’ bills,

according to research by Tenon Recovery.

If you would like us to email a copy of our digital magazine to someone you know, please email us with their details and we’ll send them a copy.

APRIL / MAY / JUNE 200918

A major opportunity to limit tax

The current economic climate could offer a major opportunity for people to limit their tax bills and crystallise losses by turning them to their advantage and passing on share portfolios and property to children to help avoid capital gains tax (CGT).

Gifts from parents to children usually incur CGT if they have risen in value, but no tax is levied if the value falls, meaning families are able to give away second homes and shares without having to pay tax.

If your profits have fallen below the CGT allowance or fallen into negative territory, crystallising them could reduce your tax bill.

If you have made a capital loss on your share portfolio, this can generally be carried forward indefinitely to offset against future gains, however, you must notify HM Revenue & Customs of losses within five years.

Crystallising losses could work to your advantage

A change in the penalty you will pay if you are late in notifying HM Revenue & Customs (HMRC) that you have commenced self-employment was introduced from April 6.

Up until this date, the penalty was £100 and you had 3 months following the commencement of trade to let HMRC know that you have become self employed.

New penalties for late notification of self-employmentFrom April 6 the rules have been changed as follows:

Anyone who ceases or becomes liable for Class 2 or Class 3 contributions must notify HMRC immediately.

A penalty may be levied (between 30pc and 100pc of the “lost

contributions”) if notice is not given by 31 January following the end of the tax year in which you become liable.

There will be no penalty if you have a reasonable excuse for the late notification.

The new HMRC penalty system has been drawn up to encourage people to take more care when submitting tax returns and other documents, as well as to deter deliberate under-assessment of tax liabilities.

New penalties if you are late in notifying HMRC that you have commenced self-employment

Self-employmentNews

If you would like us to email a copy of our digital magazine to someone you know, please email us with their details and we’ll send them a copy.

NeeD MORe INFORMATION?PLEASE CONTACT US WITH YOUR ENQUIRY.

Despite a raft of government measures small and medium-sized businesses have reported that the availability of credit has continued to decline and that they don’t expect the situation to improve in the next quarter.

According to the second monthly Confederation of British Industry (CBI) Access to Finance Survey 60pc of firms who sought new or renewed finance found that its availability had declined over the last three months.

40pc of companies reported that they had not experienced a change in the availability of accessing finance, but none of the businesses surveyed saw an improvement in the situation in the last quarter.

60pc of firms who sought new or renewed finance found that its availability had declined over the last three months.

Small and medium-sized businesses don’t expect the situation to improve in the next quarter

Credit levels continue to decline

APRIL / MAY / JUNE 2009 19

As the challenging economic climate takes a firm hold, the gap between companies issuing an invoice and receiving payment is lengthening, causing many small firms to experience real cashflow difficulties.

Research from the Asset Based Finance Association (ABFA) in December 2008, found that 28pc of small companies reported payment periods of 40-49 days, compared to just 23pc that are still receiving payment in the more normal period of 30-39 days.

Delayed payments add to the pressure currently felt by businesses and may prevent company expansion, or in the worst case scenario, cause the business to fail. This is where factoring can help.

Factoring is one solution that could provide a business with many benefits, including increasing cashflow. Factoring is where a business sells its invoices to another firm and can provide a much needed cash injection and provide almost instant working capital.

As a result of the credit crunch, with banks lending less, the flexibility of factoring can be a key advantage. Whereas a loan is based on the company’s asset backing, factoring looks at the value of invoices, providing funding to those clients with successful sales orders.

Once an invoice has been issued, up to 85pc of the value can be advanced to the company with the remaining balance being transferred once the debtor has paid.

The amount of funding needed by a company can fluctuate according to the business it is conducting. So, if there are seasonal peaks in cashflow, funding requirements will alter, and factoring could meet these needs. Or, if the turnover of the company is growing, the cash facility grows with it, unlike a bank overdraft which can be reduced or withdrawn at any time.

The factor takes on the responsibility of running and maintaining the sales ledger and thereby becomes an extension of the seller’s accounts

department. Many smaller firms do not have the resources for a specialist accounts team and it can by helpful to the business to have the ledger run by experienced personnel, and freeing up staff to concentrate on other areas of the business.

The cost of factoring is very similar to a normal bank overdraft rate, which tends to be about 3pc over the base rate. Figures from the ABFA show that this form of corporate funding continues to grow and dominate the funding market.

Corporate fundingOne solution for small firms experiencing real cashflow difficulties

If you would like us to email a copy of our digital magazine to someone you know, please email us with their details and we’ll send them a copy.

NeeD MORe INFORMATION?PLEASE CONTACT US WITH YOUR ENQUIRY.

APRIL / MAY / JUNE 200920

New research for the AAT, the professional education and membership body for accounting staff, found that an unnecessarily complex tax regime and a lack of finance training is compounding the impact of the recession, at a time when this sector, considered the ‘backbone’ of the economy, needs to make every penny count.

Common mistakes which cost firms cash include incurring fines for late filing of accounts, failing to claim Business Rate Relief and ignorance of opportunities such as the ‘Time to Pay’ scheme, which allows those companies unable to pay their tax bill to spread payments.

Business rates are the third largest cost to SMEs per annum and rate relief could be worth up to £1200 per firm. Despite this, over £400m of Business Rates Relief goes unclaimed each year, in large part because firms are not aware of the opportunity.

Small businesses also have to pay a 5pc surcharge if they are three months late in paying.

238,699 British companies filed their accounts late in 2007, an increase of 25pc since 2003, and the trend is expected to continue in 2009 as firms struggle in a recessionary climate. Fines for late filing increased dramatically in January 2009, with companies now being charged £150 for forms submitted up to four weeks late, or £375 if this period extends to three months.

Small businesses also have to pay a 5pc surcharge if they are three months

late in paying. In addition, fines automatically double if firms are found to have submitted the previous year’s returns late.

There is still some ignorance about the ‘Time to Pay’ scheme, which was introduced in November 2008 and is administered by HMRC Business Payment Support Service. Only 60,000 businesses, out of a potential 4.7m, have arranged to spread their tax burden with HMRC.

A 2007 survey by HBOS, found that 75pc of small businesses were run by directors with no financial training and 55pc of SME business owners, with sole responsibility for financial matters within their firm did so without any form of external professional financial assistance.

The British Bankers’ Association has compiled this list to help businesses to weather the current economic downturn. n Plan your cashflow

requirements carefully and allow for any differences in the payment terms you receive from your suppliers and those you give to your customers.

n When you prepare your cashflow forecast, undertake a ‘what-if’ analysis. What happens if sales are 10pc less than the forecast? What happens if raw materials increase in price by 20pc? You can then forecast the worst-case finance requirement which mitigates the need to go back to your bank for more funding.

n Review your actual cashflow regularly, at least every month. Check that it is in line with your forecast and act quickly if it is not.

n Think carefully about who you do business with and don’t become too dependent on one customer.

n Invoice your customers promptly and accurately and follow up to check they have paid. Offer an incentive to pay early.

n If you think you might have a cash flow problem, speak to your bank immediately. They might be able to help and the earlier you speak to them, the more options available there could be.

n Be open and realistic with all the facts. That way, you will have a solid base for the banking relationship you will need in the future. Most of all understand your business plan and then monitor progress through it so you can exploit success and limit problems.

n Review all of your costs and look for ways to be more efficient. Cut down unnecessary expenditure and strip out as much as you sensibly can.

Small firms struggle with UK tax lawsThree quarters find it difficult to find information about regulationsA lack of financial experience, one of the world’s most complex tax systems and a lack of clarity from the government are causing small firms to struggle with tax law, say the AAT. Cash-strapped small businesses are losing out on the chance to defer a potential £7.7bn of tax payments due to poor finance skills and a failure to seek out professional advice.

Weathering the current economic downturnA significant contribution to the continued health of your business

News

If you would like us to email a copy of our digital magazine to someone you know, please email us with their details and we’ll send them a copy.

APRIL / MAY / JUNE 2009 21

APRIL / MAY / JUNE 200922

Know what is going on in your businessYou cannot make the right decisions on cost unless you know what is going on in your business. Make robust forecasting and scenario analysis a key priority. Understand potential scenarios and your contingencies for responding to them.

Understand the viability of your key suppliers and customersIn today’s challenging business environment, it is important to understand the viability of your key suppliers and customers. How are you managing your counterparty risk? What happens if one of your key customers goes out of business? How is the relationship with your banks, your pension fund trustees, credit insurers, or your shareholders?

Know what drives cost in your businessMake sure that you have a clear understanding on what drives cost in your business and what cost can be taken out of the business. Evaluate whether you are being as thorough as you can be.

Evaluate your cost baseDon’t panic and ‘slash and burn,’ panic destroys value. As you evaluate your cost base, move swiftly to remove waste but don’t use cost avoidance as a substitute for achieving lasting, wholesale efficiencies. Be very careful about removing costs that are close to your customer, losing sales can more than cover any gains made from cost savings.

Make your business more agileIf you want to achieve cost leadership think about how your organisation could do business in a more agile, efficient way. Think innovatively about delivery, could you outsource or joint venture part of your value chain? What about off-shoring, management de-layering or even joint venturing with your competition to save costs in certain areas? The appetite of your competitors to collaborate may be very different now compared to only a year ago.

Long term value creation and survivalManagement teams are beginning to realise that taking out £1 of cost can be equal to

generating £9 of new sales and are prioritising their attention accordingly. The challenge of delivering a low cost business model demands a new focus on cost from the board down. Cost is the route to long term value creation and survival.

Understand the cash dynamics of your businessIn the current market where cash is king, understanding the cash dynamics of spend can be as important as the impact on the bottom line. Make cash a key component of your cost optimisation approach.

Relentless, ongoing focus and determinationTruly optimising costs requires relentless, ongoing focus and determination. Given the size and scale of the challenge ahead, organisations can not afford to have any confusion about roles and responsibilities. Initiatives need to be led from the top and should not be delegated down.

Source: KPMG

The corporate survival guideMaking the right decisions in today’s challenging business environment

If you would like us to email a copy of our digital magazine to someone you know, please email us with their details and we’ll send them a copy.

The recession and economic downturn has subjected organisations to be even more disciplined about keeping a watchful eye on the key fundamentals of running their businesses. Take a look and see if your business could be focusing on any other areas.

Financial services, taxes and wealth management for individuals...do you need a professional assessment of your situation? If you want to organise your financial affairs, particularly where it involves taxation – don’t leave it to chance.

Contact us to discuss your requirements, and we’ll help you navigate this complicated area.

APRIL / MAY / JUNE 200924

Value Added Tax Introduction of a new penalty regime

This April marked the introduction of a new Value Added Tax (VAT) penalty regime. The legislation has

been in place since the Finance Act of 2007, and covers a range of tax regimes. Currently, it applies to errors made in respect of VAT, Income Tax, PAYE, CGT, NICs, Corporation Tax, and the Construction Industry Scheme.

The penalty applies in two situations, firstly where there is a failure to notify an under-assessment. This will arise where a taxpayer is required to submit a VAT Return, fails to do so, and is sent an estimated assessment. If the assessment understates his liability, and he fails to take ‘reasonable steps’ to tell Customs his correct liability within 30 days, then the penalty will be triggered.

Secondly, if a person submits a document which contains an error. In particular, this will apply to a VAT Return, and to a Voluntary Disclosure form. However, the legislation is widely drafted, and includes ‘any document which is likely to be relied upon by HM Revenue & Customs (HMRC) to determine a taxpayer’s liability. Thus, a D-I-Y claim, an 8th or 13th Directive claim, or even a letter of explanation, would be covered by the penalty provisions.

HMRC detail three categories of inaccuracy. These are significant, as each has its own range of penalty percentages. If an inaccuracy is found to fall within a lower band, then a lower penalty rate will apply. Where the taxpayer has taken ‘reasonable care,’ even though an error has been made, then no penalty will apply.

n An error, when reasonable care not taken: 30pc;

n An error which is deliberate, but not concealed: 70pc;

n An error, which is deliberate and concealed: 100pc.

The legislation provides that if a person takes ‘reasonable care,’ then no penalty is due. There is no definition of ‘reasonable care.’ HMRC have said that they would not expect the same level of knowledge or expertise from a self-employed person, as from a large corporation.

HMRC expect that, where an issue is unclear, advice is sought, and a record maintained of that advice. They also expect that, where an error is made, it is adjusted, and HMRC notified promptly. They have specifically stated that merely to adjust a Return will not constitute a full disclosure of an error. Therefore a penalty may still be applicable.

The amount of the penalty is calculated by applying the appropriate penalty rate (above) to the ‘Potential Lost Revenue’ or PLR. This is essentially the additional amount of VAT due or payable, as a result of the inaccuracy, or the failure to notify an under-assessment. Special rules apply where there are a number of errors, and they fall into different penalty bands.

The percentage penalty may be reduced by a range of ‘defences:’

n Telling; this includes admitting the document was inaccurate, or that there was an under-assessment, disclosing the inaccuracy in full, and explaining how and why the inaccuracies arose;

n Helping; this includes giving reasonable help in quantifying the inaccuracy, giving positive assistance rather than passive acceptance, actively engaging in work required to quantify the inaccuracy, and volunteering any relevant information;

n Giving Access; this includes providing documents, granting requests for information, allowing access to records and other documents.

APRIL / MAY / JUNE 2009 25

Further, where there is an ‘unprompted disclosure’ of the error, HMRC have power to reduce the penalty further. This measure is designed to encourage businesses to review their own VAT Returns.

A disclosure is unprompted if it is made at a time when a person had no reason to believe that HMRC have discovered or are about to discover the inaccuracy. The disclosure will be treated as unprompted even if at the time it is made, the full extent of the error is not known, as long as fuller details are provided within a reasonable time.

There is some guidance on the line between unprompted and prompted disclosures. In particular, where Customs have contacted the business to make a compliance check, or have arranged a visit, then any disclosure will be prompted, and a higher rate of penalty will apply.

HMRC have included a provision whereby a penalty can be suspended for up to 2 years. This will occur for a careless inaccuracy, not a deliberate inaccuracy. HMRC will consider suspension of a penalty where, given

the imposition of certain conditions, the business will improve its accuracy. The aim is to improve future compliance, and encourage businesses which genuinely seek to fulfil their obligations.

HMRC have an internal reconsideration procedure, where a business should apply to in the first instance. If the outcome is not satisfactory, the business can pursue an appeal to the Tribunal. A business can appeal whether a penalty is applicable, the amount of the penalty, a decision not to suspend a penalty, and the conditions for suspension. A new Tribunal structure is also being put into place.

HMRC have amended s77 of the VAT Act 1994, to extend the normal time limit for penalties to 4 years. Additionally, where there is deliberate action to evade VAT, the 20 year limit applies. In particular, this applies to a loss of VAT which arises as a result of a deliberate inaccuracy in a document submitted by that person.

Other penalties, for example, for failure to notify registration, failure to notify change in material change of supplies, failure to notify acquisition of goods, or unauthorised issue of invoices showing VAT, will come into force in April 2010. FA08, Sch 41 contains the appropriate provisions. This also provides new penalties for Insurance Premium Tax, Aggregates Levy, Climate Change Levy, Landfill Tax, Air Passenger Duty, amongst others.

This April marked the introduction of a new Value Added Tax (VAT) penalty regime. The legislation has been in place since the Finance Act of 2007, and covers a range of tax regimes.

NeeD MORe INFORMATION?PLEASE CONTACT US WITH YOUR ENQUIRY.

APRIL / MAY / JUNE 200926

Despite the credit crunch, there is still some money available for businesses looking for additional finance. But in such a competitive market it’s vital to be well prepared.

Is it still possible in the current climate to raise new investment for your company? Are venture capitalists and angel investors closed for business? Where can you get additional finance?

According to Aegis Corporate Strategy it is still possible to raise finance for both established businesses and early-stage companies. However, there is a lot less cash around than there was 12 months ago so businesses need to have a high quality business plan and put forward a compelling case.

A number of the larger venture capital companies that invest between £1m and £10m in early-stage companies still have substantial resources available. However, investors are very choosy and often focused on specific sectors so it’s vital you’re well prepared before you approach them.

The market for equity of less than £1m has been very badly affected. Traditionally this has been provided by venture capital trusts (VCTs) and business angels. There is a dramatic reduction in the finance available from both of these groups. Business angels will normally look for EIS (tax) relief on their investment. It is worth remembering that there is a much higher appetite for EIS opportunities in March and October as angels look to maximise their tax relief.

Financing increased working capital requirements caused by reduced sales,

however, is extremely difficult. In some cases where the banks have refused to provide additional finance, venture capitalists will bridge the gap but this is very expensive for shareholders.

While the new government measures will hopefully increase lending, it is going to be a number of years before we will be able to negotiate loans at the same level and conditions that were achieved in 2007 and early 2008. In the interim, management should explore options such as invoice discounting and a mezzanine loan before looking for equity.

The number of banks providing new loans for buyouts and acquisitions has fallen dramatically. Deals in excess of £50m are particularly difficult if additional banking is required. There is still an appetite for smaller deals but fees and margins charged are often at least 100 per cent higher than 12 months ago.

If you are contemplating an acquisition or buyout talk to a number of banks at an early stage to assess the level of borrowing you can get. Then look at alternative financing to bridge the gap.

Will the vendor agree to a deferred payment? Will they retain an equity stake that can be bought out at an agreed price at a later date? Will they reinvest alongside a venture capitalist? Will they provide a mezzanine loan to bridge the gap? Most importantly, will they reduce the price? Remember there are fewer options available to vendors these days and this should help you to agree a better or more flexible deal.

In such a competitive market it’s vital to be well prepared

Looking to raise money in the recession?

Enterprise

If you would like us to email a copy of our digital magazine to someone you know, please email us with their details and we’ll send them a copy.

NeeD MORe INFORMATION?PLEASE CONTACT US WITH YOUR ENQUIRY.

Looking to raise money in the recession?

Financial planning is our business...we’re passionate about making sure your finances are in good shape.Our range of personal financial planning services is extensive, covering all areas from pensions to taxation and inheritance matters to tax-efficient investments.

Contact us to discuss your current situation, and we’ll help get your finances in good shape.

APRIL / MAY / JUNE 200928

Did you know that generous Research and Development (R&D) tax incentives are available to encourage innovation in the UK? If your company is developing new products, processes, materials or services, there is a good chance that you will be able to claim R&D relief.

The new filing deadline for R&D claims significantly

reduces the time available to make and submit claims. R&D claims have to be made by the first anniversary of the filing deadline for the company’s tax return (normally 2 years). Companies need to start planning early to optimise the amount that can be claimed before the filing deadline.

Tax incentives encourage innovation in the UK

Research and Development

accounting period: see tax period acquisitions: goods brought into the UK from other EU countries, sometimes known as imports corporate body: an incorporated body such as a limited company, limited liability partnership, friendly, industrial or provident society distance sales: where a business in one EU country sells and ships goods directly to consumers in another EU country, e.g. Internet or mail-order sales input tax: the VAT you pay on your purchases output tax: the VAT you charge on your sales place of supply: the country where a supply of goods or services is said to be made for VAT purposes self-billing: your customer issues your VAT invoice and sends a copy to you with their payment

supply: selling or otherwise providing goods or services, including barter and some free provision supply of goods: when exclusive ownership of goods passes from one person to another taxable person: any business entity that buys or sells goods or services and is required to be registered for VAT, this can be an individual, partnership, company, club, association or charity taxable supplies: all goods and services you sell or otherwise supply which are liable to VAT at the standard, reduced or zero rate - whether or not you are registered for VAT taxable turnover: the total value excluding VAT of the taxable supplies you make in the UK (excludes capital items like buildings, equipment, vehicles or exempt supplies)

tax period: the period of time covered by your VAT Return, usually quarterly tax point: the date when VAT has to be accounted for, for goods, this is usually when you send the goods to a customer or when they take them away, for services, this is usually when the service is performed time of supply: see tax point

VAT glossaryThese are some definitions of common VAT terms that HMRC uses:

NeeD MORe INFORMATION?PLEASE CONTACT US WITH YOUR ENQUIRY.

If you would like us to email a copy of our digital magazine to someone you know, please email us with their details and we’ll send them a copy.

APRIL / MAY / JUNE 2009 29

To put your business on a proper footing with HM Revenue & Customs (HMRC) and other authorities, you need to make sure that it has the right legal structure. It’s worth thinking carefully about which structure best suits the way that you do business, as this will affect:

n the tax and National Insurance that you pay

n the records and accounts that you have to keep

n your financial liability if the business runs into trouble

n the ways your business can raise money

n the way management decisions are made about the business

There are several structures to choose from, depending on your situation. If you are not sure which legal structure would best suit your business, it’s important to seek professional advice.

Overview of legal structures

Sole traderThe advantages of being a sole trader include independence, ease of set up and running, and the fact that all the profits go to you.

The disadvantages include a lack of support, unlimited liability and the fact that you are personally responsible for any debts run up by your business.

PartnershipThe advantages of being in a partnership include its ease of set up and running, and the range of skills and experience that the partners can bring to the business.

On the other hand, problems can occur when there are disagreements between partners. There is unlimited liability and, as a partner, you are personally responsible for any debts that the business runs up.

Limited liability partnership (LLP)LLPs retain the flexibility of a partnership and your personal liability is limited. There is no restriction on the number of members, but at least two must be “designated members” - the law places extra responsibilities on them.

The formation of an LLP is more complex and costly than that of a partnership and problems can occur when there are disagreements between the members. If the number of partners is reduced, and there are fewer than two designated members, then every member is deemed to be a designated member.

Limited liability companyIn a limited liability company your personal financial risk will be restricted to how much you invest in the business and any guarantees you have given in order to obtain financing.

However, you should remember that this type of company also brings a range of extra legal duties, including the maintenance of the company’s public records, e.g. for the purpose of the filing of accounts.

FranchiseThe major advantage of a franchise is that it takes advantage of the success of an established business and support networks.

However, your freedom to manage the business is limited by the terms of the franchise agreement. Also franchisees often pay a share of their turnover to the franchiser, which reduces overall profits.

Social enterprisesSocial enterprises are businesses that trade for a social purpose and represent a diverse and growing range of business activity across the UK.

Putting your business on a proper footing

Legal structures

NeeD MORe INFORMATION?PLEASE CONTACT US WITH YOUR ENQUIRY.

If you are considering setting up your own business and would like to discuss the options available, please contact us for further information.

APRIL / MAY / JUNE 200930

Getting in good shape to survive the downturnKey areas around which small businesses should consider taking action

No two companies are the same and some businesses will already be doing some of the following well. If you can tick off all these actions, you should be in good shape to survive the downturn.

Get closer to customers and suppliersBusinesses with a limited number of key customers and suppliers need to be very careful. If one of these becomes insolvent it can be catastrophic. So you

should monitor these key customers’ behaviour in orders, sales, trading trends and business projections.

Most importantly, check their payment performance. Feedback from staff dealing with these customers can be invaluable in identifying signs that a customer is in financial distress or considering moving to another supplier. The same applies to key suppliers. Stress-test your business by asking

what the effects of a key customer or supplier ceasing to trade would be.

If you feel your business is heading for trouble it is better to take advice early. Insolvency practitioners complain that companies leave talking to them until the most likely outcome is administration.

Better credit managementDuring this recession active credit management is vital. This applies

Firms of all sizes and from all sectors need to focus on their cashflow to ensure that they survive and even flourish following this recession. The following points offer key areas around which small businesses should consider taking action.

APRIL / MAY / JUNE 2009 31

throughout the process, from vetting existing and potential new customers by taking out regular credit checks through to securing payment. Late payment is a particular issue in this recession and managing your receivables should be a high priority. Some key questions to ask are:

n Do you have payment terms? Do these include charging interest on late payment?

n Are the terms accepted by your customers?

n Do you get regular credit checks? n Is there one person who is

responsible for collecting receivables?

n What happens if customers go beyond your terms?

n Is there a procedure for the directors to get involved in pressuring customers to pay?

n How frequently is the aged debtors list reviewed by a director?

n What is the procedure for taking legal action to recover debts?

Manage cashflowThere is unlikely to be a time in your company’s life when managing cashflow is more important. The basis of cashflow management is having a system whereby the directors receive daily information on the cash position, either in terms of balances at the bank or how much of the overdraft facility is unused.

In addition, there must be regular forecasts of how the available facilities will change in the next week, month, quarter and year. These should be prepared on spreadsheets and with an automated cash flow management system it is a simple task to change assumptions.

Improve management reportingWith the recession making access to finance difficult, many businesses are concerned enough to want information on their trading performance quicker than they have had in the past. Businesses that produce monthly accounts late in the month, leave directors and finance providers lacking important up-to-date information on their position.

But there are steps that can be taken to improve reporting deadlines, some requiring relatively small outlays. The main thing is often to make shorter timescales a greater priority. Benefits include quicker and better information on which to base decisions; better informed stakeholders, including finance providers; a more professional image when dealing with customers, suppliers and finance providers; more time for interrogation of the figures; and fewer surprises at the year-end. Finally, if your month-end reporting procedures are slick, producing the annual accounts at the end of the year should also be a straightforward routine.

Control gross margin and costsBusinesses can improve gross margin by increasing selling prices; reducing the cost of purchased direct materials; improving the sales mix; reducing waste, write-offs and pilferage of stock; and introducing special lines or temporary products.

Some of these may be quickly discounted but it is worthwhile asking if they might be an option for you. It is also important to review both current and planned capital expenditure which can yield cashflow savings and improve profitability.

Strategy, marketing and product developmentRecessions tend to affect different business sectors to different degrees. Time spent on developing new products and markets can yield significant benefits, including reducing reliance on a few customers or one sector, entry into higher added-value products and increased gross margins. It can also increase your attractiveness to new equity providers once the recession is over.

Consider how your competitors are faring and how are they likely to respond to the current crisis. Intelligence from staff, suppliers and customers on competitors can help identify potential opportunities.

Build relationships with finance providersEven if your business currently has no borrowings or is operating well within the limits of its facilities, spending time with your current and potential new finance

providers will be worthwhile. Some new SME finance schemes

have recently been announced by the government while businesses which might require fresh equity capital to finance new marketing or product development, or to recapitalise after the recession, should find out what small scale equity schemes are available from business angels, regional development agencies and more formal private equity funds.

Ensure your business is appropriately financedCompanies seeking finance invariably think of a term loan (for a fixed period) or an overdraft. But it is important to make the finance appropriate to the purpose for which it is required.

Although overdrafts provide flexible finance for working capital, they are repayable on demand. Factoring and invoice discounting, if appropriate, could be an alternative solution for your business as they can yield a bigger percentage advance than an overdraft based on debtors.

Minimise tax paymentsYou should take professional advice to ensure that you have availed yourself of all the legitimate ways of reducing a tax liability, such as using all capital allowances and including all allowable expenses.

If your forecasts suggest that the business may have difficulty paying the taxes you should take advice before approaching HM Revenue & Customs (HMRC) for proposals to pay by instalments.

In the 2008 Pre-Budget report, chancellor Alistair Darling announced that HRMC had launched a new business payment support service to help businesses finding it difficult to make tax payments on time, including corporation tax, VAT, PAYE and national insurance contributions. This scheme following Budget 2009 has now been extended. Businesses experiencing temporary financial difficulties or needing more time to pay an outstanding tax bill can agree a timetable of payments that they will be able to afford.

Source: Institute of Chartered Accountants in England and Wales

Content of the articles featured in this publication is for your general information and use only and is not intended to address your particular requirements or constitute a full and authoritative statement of the law. They should not be relied upon in their entirety and shall not be deemed to be, or constitute advice. Although endeavours have been made to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No individual or company should act upon such information without receiving appropriate professional advice after a thorough examination of their particular situation. We cannot accept responsibility for any loss as a result of acts or omissions taken in respect of any articles.

Produced by Goldmine Publishing Limited • Prudence Place • Luton • Bedfordshire • LU2 9PE

Insolvency issues designed to guide you through the maze of options...is your business facing serious financial difficulties?Professional advice for directors considering the options for restructuring and turning around their business.

Contact us to discuss the best way to deal with your responsibilities, don’t leave it until it’s too late.

Articles are copyright protected by Goldmine Publishing Limited 2009. Terms and conditions apply. Unauthorised duplication or distribution is strictly forbidden.