ESB-1442-1211. From Health Care Reform This is only a brief summary that reflects our current...

32

ESB-1442-1211

-

Upload

myles-lindsey -

Category

Documents

-

view

213 -

download

0

Transcript of ESB-1442-1211. From Health Care Reform This is only a brief summary that reflects our current...

ESB-1442-1211

ESB-1442-1211

MANAGING NEW ADMINISTRATIVE

OBLIGATIONSFrom Health Care Reform

This is only a brief summary that reflects our current understanding of select provisions of the law, often in the absence of regulations. All of the interpretations contained herein are subject to change as the appropriate agencies publish additional guidance.

ESB-1442-1211

• Provide a road map for Health Care Reform• Gain an understanding of the key

administrative obligations affecting employers• Develop an immediate action plan

OBJECTIVES

ESB-1442-1211

SETTING THE STAGE

• 1,000 pages of legislation drafted and enacted very quickly

• Rules are still being developed– Federal agency guidance– Role of states

ESB-1442-1211

• Plan design mandates• Health FSA/HRA/HSA provisions• Plan sponsorship provisions• Administrative requirements

HCR ROADMAP

ESB-1442-1211

• Notice and disclosure requirements • Enrollment provisions• Reporting obligations• Nondiscrimination testing• Fee payment

ADMINISTRATIVE REQUIREMENTS

ESB-1442-1211

• Grandfathered plans must maintain records documenting the terms of coverage in effect on March 23, 2010

• Must be available to agencies and participants upon request

• Must be sent to any new insurance carrier

DOCUMENTATION OF GRANDFATHERED STATUS

ESB-1442-1211

• Grandfathered plans must include notice of grandfathered status in all benefit summaries

• Model language available• Effective for plan years on/after March 23,

2010

NOTICE OF GRANDFATHERING

ESB-1442-1211

• 1st plan year on/after Sept. 23, 2010:– Lifetime limits– Adult child eligibility

• All plan years on/after Sept. 23, 2010:– Right to select PCP– Direct access to OB/GYN– Model language available

PATIENT PROTECTION NOTICES

ESB-1442-1211

• 1st plan year on/after Sept. 23, 2010 • Required to offer a minimum of 30 days for

open enrollment– Special enrollment applied for individuals excluded

from coverage due to the imposition of lifetime limits or age

• Individuals and family members could enroll

30-DAY ENROLLMENT

ESB-1442-1211

• Fully-insured non-grandfathered plans may not discriminate in favor of highly compensated individuals

• Self-funded plans are currently subject to similar rules, regardless of grandfathered status

NONDISCRIMINATIONTESTING

ESB-1442-1211

• Effective for plan years on/after Sept. 23, 2010– IRS has delayed enforcement pending publication

of regulations• Nondiscrimination testing may be required

NONDISCRIMINATIONTESTING (CONT’D)

ESB-1442-1211

• Non-grandfathered plans must make disclosures to HHS and public– E.g., claims payment policies, enrollment data,

financial disclosures, cost-sharing• Effective for plan years on/after Sept. 23, 2010

– Regulations are expected to clarify required content and effective date

TRANSPARENCY DISCLOSURES

ESB-1442-1211

• Plan sponsors and insurers must pay a fee to help fund comparative effectiveness research– $1 per individual for 1st plan year after Sept. 30, 2011– $2 per individual for the next year– Increases based on percentage increase in per capital

National Health Expenditures in subsequent years• Watch for details on how/when to pay

COMPARATIVE EFFECTIVENESS RESEARCH FEE

ESB-1442-1211

• Effective for the 2012 tax year– Employers that filed fewer than 250 W-2s in 2011

are not required to report until future notice• Must report health care costs, including:

– Employer and employee contributions– Pre-tax and after-tax contributions in most cases

W-2 REPORTING

ESB-1442-1211

• 4 methods to calculate cost of coverage:– Premium Charged Method– COBRA Applicable Premium Method– Modified COBRA Premium Method– Composite Rate

W-2 REPORTING (CONT’D)

ESB-1442-1211

Coverage subject to W-2 reporting Coverage exempt from W-2 reportingEmployer- sponsored group health coverage HRA Allocations

Employer contributions to Health FSA Employee contributions to a Health FSA*

Gap Coverage Health Savings Account contributions

Hospital Indemnity Coverage if pre-tax Archer MSA contributions

Fixed Indemnity Coverage if pre-tax Stand Alone Dental Coverage

Specified Disease Coverage (e.g., cancer, critical illness) if pre-tax

Stand Alone Vision Coverage

On-site clinic Long Term Care Coverage

Employer-sponsored wellness Disability Coverage

Accident, including AD&D

* Requires an additional calculation

W-2 REPORTING (CONT’D)

ESB-1442-1211

• Action Steps– Contact payroll – Determine which coverages are reportable– Determine reportable cost– Calculate amount to report per employee

• Worksheet is available at www.HCReducation.com/W2reporting

W-2 REPORTING (CONT’D)

ESB-1442-1211

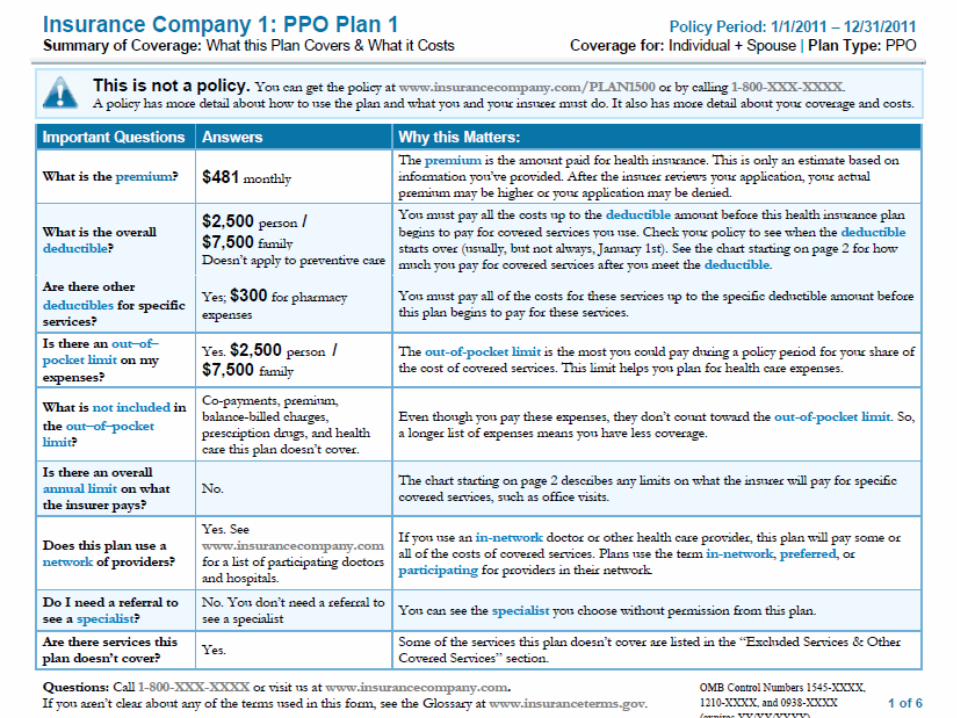

• Plan sponsor must provide a Summary of Benefits and Coverage (SBC) and Uniform Glossary to plan participants

• Fill in template • Distribute with enrollment materials, following

special enrollment events, and upon request• Required after final regulations are published

SUMMARY OF BENEFITS AND COVERAGE

ESB-1442-1211

ESB-1442-1211

ESB-1442-1211

• If make certain modifications to health plan coverage not reflected in distributed SBC

• Must send notice of changes 60 days in advance of effective date

• May simply distribute updated SBC• Required after final regulations are published

ADVANCE NOTICE OFBENEFIT CHANGES

ESB-1442-1211

• Employers must provide information about the state Exchanges– To all employees by March 1, 2013– To all subsequent new hires

• Model language will likely be provided• If plan’s actuarial value is less than 60%, must

describe availability of premium assistance

NEW HIRE INFORMATION

ESB-1442-1211

• Plan sponsors of non-grandfathered plans must report on certain quality-related programs– E.g., disease management

• Must be issued annually to HHS and to employees during open enrollment

• Effective date to be established by regulations

QUALITY REPORTING

ESB-1442-1211

• Plan sponsors with 200+ full-time employees must automatically enroll newly eligible full-time employees

• Must provide notice • Employees may opt out• Effective date to be established by

regulations, expected to be published by 2014

AUTOMATIC ENROLLMENT

ESB-1442-1211

• Effective January 1, 2014• Employers with 50+ full-time employees must

report extensive details about the employer’s health coverage and workforce to the IRS

• Certain reporting is also required for smaller employers that provide minimum essential coverage

COVERAGE AND WORKFORCE REPORTING

ESB-1442-1211

• Frequency is to be determined• Must provide a written statement to each

employee named in the return each year

COVERAGE AND WORKFORCE REPORTING (CONT’D)

ESB-1442-1211

• Effective 2018: 40% non-deductible excise tax • Imposed on aggregate value of health

coverage that exceeds threshold amounts• Plan sponsors must:

– Calculate value of coverage on a per month basis– Notify entity required to pay and IRS

CADILLAC TAX REPORTING

ESB-1442-1211

• General thresholds: – $10,200 individual coverage– $27,500 family coverage

• Indexed for inflation• Applies for specified health coverage

CADILLAC TAX (CONT’D)

ESB-1442-1211

• Ensure benefit summaries include required notices– Grandfathered status– Selection PCP– Direct access to OB/GYNs

• Maintain documentation supporting grandfathered status

ACTION PLAN

ESB-1442-1211

• Create a plan for complying with the W-2 reporting requirements

• Watch for guidance on:– Paying comparative effectiveness research fee– Nondiscrimination rules– Transparency disclosures– Summary of Benefits and Coverage distribution

ACTION PLAN (CONT’D)

ESB-1442-1211

Thank you!This is only a brief summary that reflects our current understanding of select provisions of the law, often in the absence of regulations. All of the interpretations contained herein are subject to change as the appropriate agencies publish additional guidance.