Ericsson strategy – Global trends for local...

20

Ericsson strategy – Global trends for local markets Torbjörn Nilsson Senior Vice President, Strategy & Product Management

Transcript of Ericsson strategy – Global trends for local...

Ericsson strategy –Global trends for local markets

Torbjörn NilssonSenior Vice President, Strategy & Product Management

2005-09-72

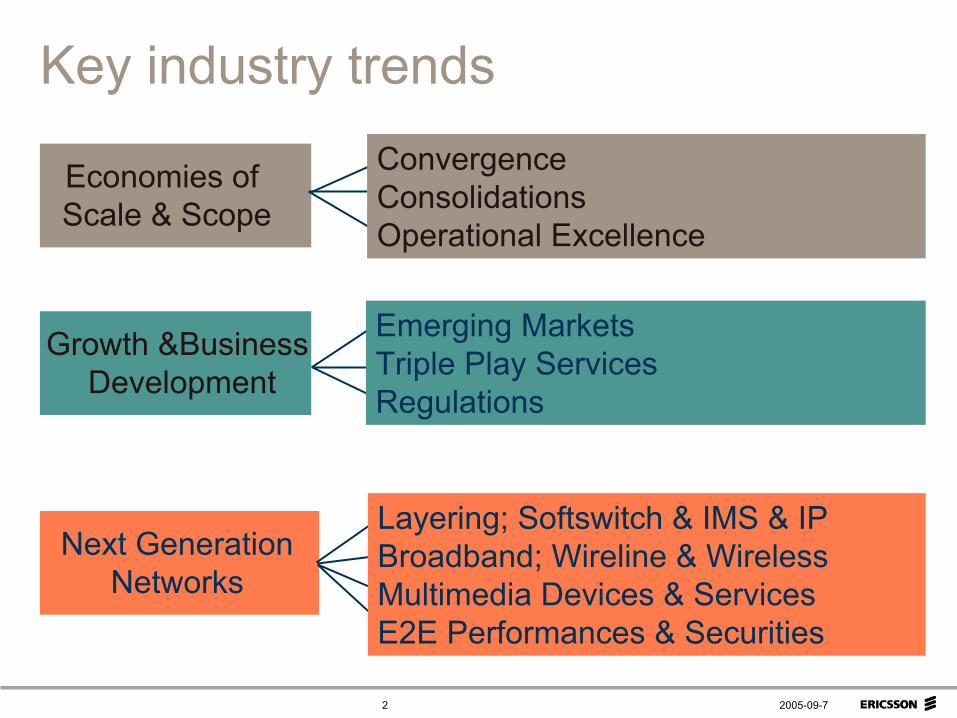

Key industry trends

Economies of Scale & Scope

Growth &Business Development

Next GenerationNetworks

Emerging MarketsTriple Play ServicesRegulations

Layering; Softswitch & IMS & IP Broadband; Wireline & Wireless Multimedia Devices & ServicesE2E Performances & Securities

Convergence ConsolidationsOperational Excellence

2005-09-73

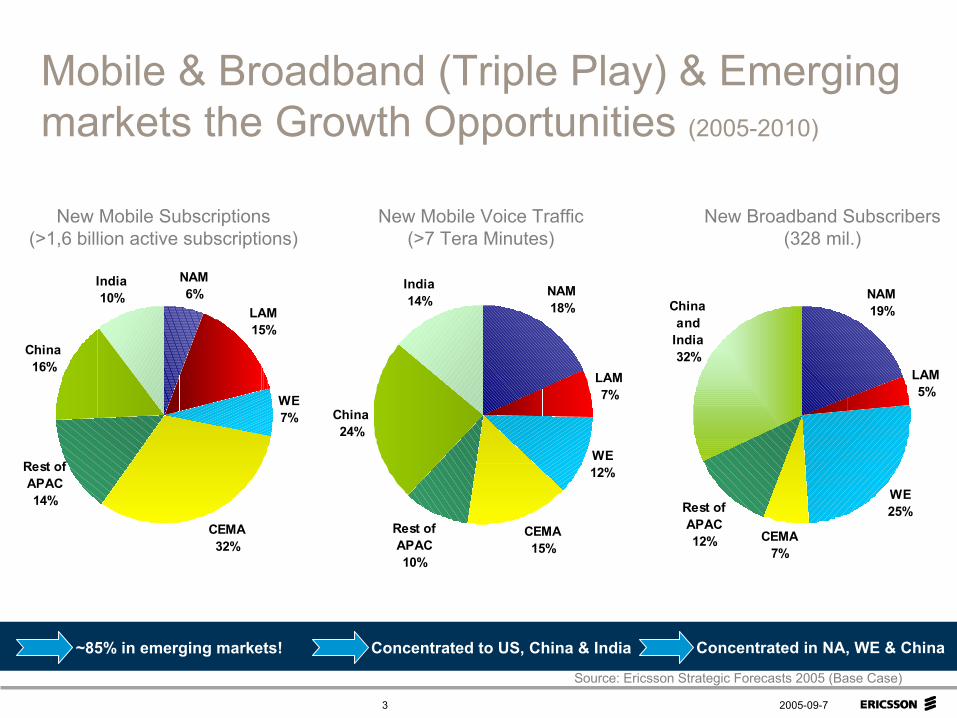

Mobile & Broadband (Triple Play) & Emerging markets the Growth Opportunities (2005-2010)

New Mobile Voice Traffic (>7 Tera Minutes)

Source: Ericsson Strategic Forecasts 2005 (Base Case)

New Mobile Subscriptions (>1,6 billion active subscriptions)

New Broadband Subscribers(328 mil.)

~85% in emerging markets! Concentrated to US, China & India Concentrated in NA, WE & China

NAM18%

LAM7%

WE12%

CEMA15%

Rest of APAC10%

China24%

India14%

NAM6%

LAM15%

WE7%

CEMA32%

Rest of APAC14%

China16%

India10% NAM

19%

LAM5%

WE25%

CEMA7%

Rest of APAC12%

China and

India32%

2005-09-74

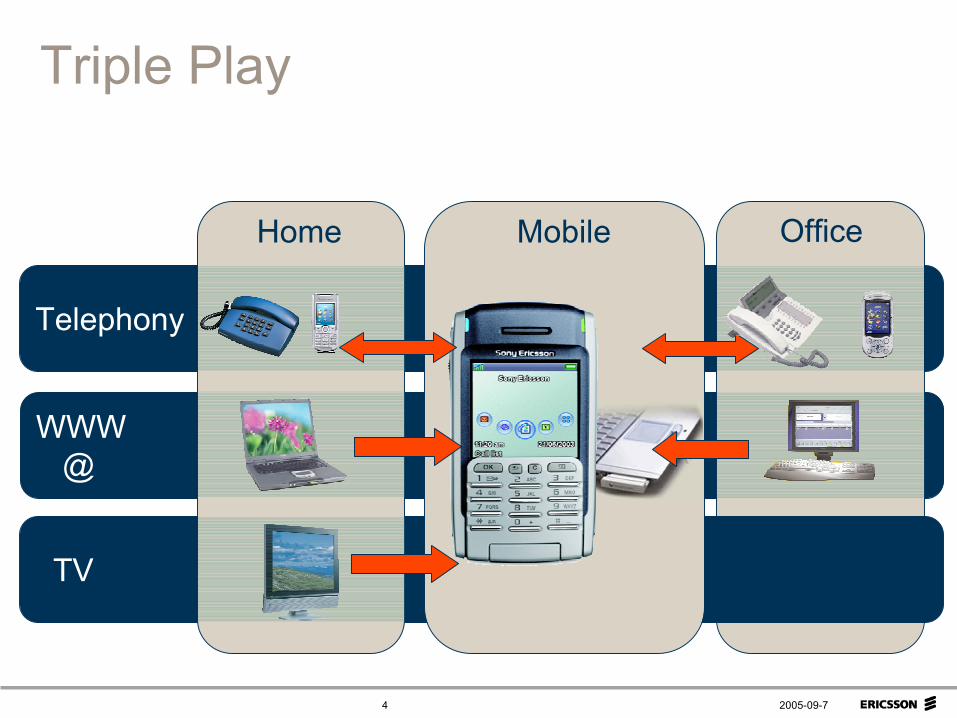

Telephony

WWW@

Office

TV

MobileHome

Triple Play

2005-09-75

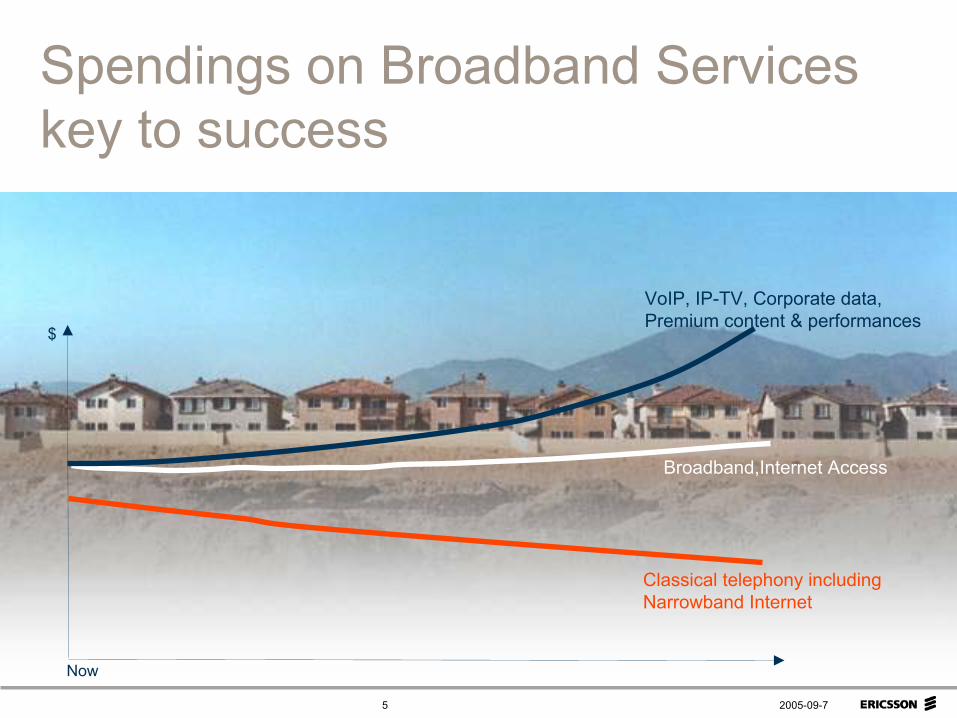

Spendings on Broadband Services key to success

VoIP, IP-TV, Corporate data, Premium content & performances

Broadband,Internet Access

Now

$

Classical telephony includingNarrowband Internet

2005-09-76

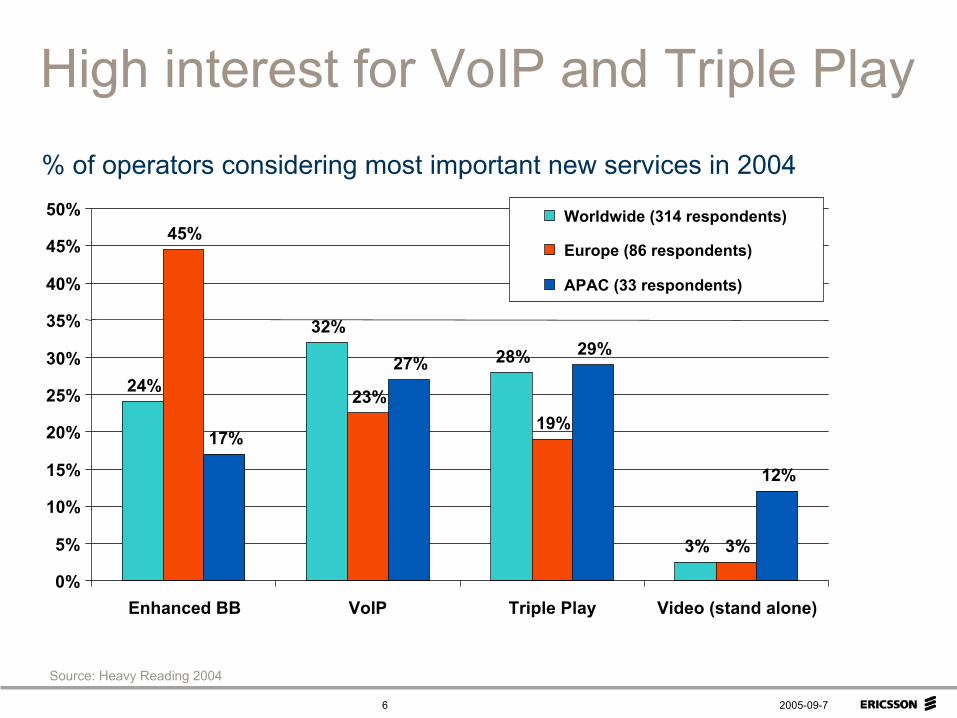

High interest for VoIP and Triple Play

24%

32%28%

3%

45%

23%19%

3%

17%

27%29%

12%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Enhanced BB VoIP Triple Play Video (stand alone)

Worldwide (314 respondents)

Europe (86 respondents)

APAC (33 respondents)

% of operators considering most important new services in 2004

Source: Heavy Reading 2004

2005-09-77

Broadband everywhere

2005-09-78

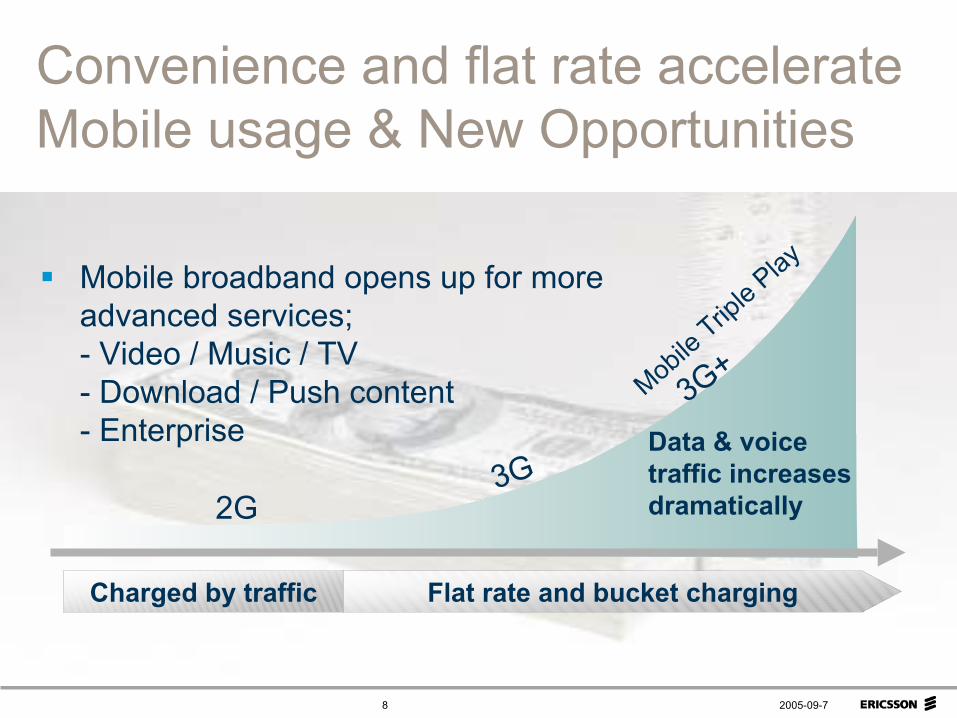

Convenience and flat rate accelerate Mobile usage & New Opportunities

Data & voice traffic increases dramatically

Charged by traffic Flat rate and bucket charging

Mobile broadband opens up for more advanced services;- Video / Music / TV- Download / Push content- Enterprise

Mobile Trip

le Play

2G3G

3G+

2005-09-79

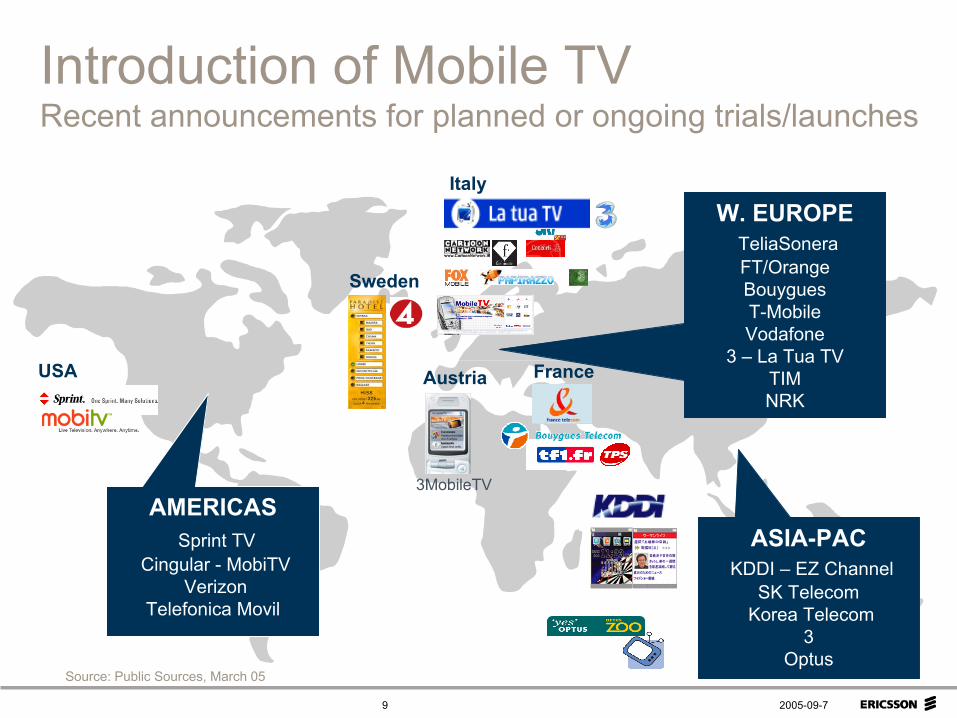

Introduction of Mobile TVRecent announcements for planned or ongoing trials/launches

Source: Public Sources, March 05

AMERICASSprint TV

Cingular - MobiTV Verizon

Telefonica Movil

W. EUROPETeliaSoneraFT/Orange BouyguesT-MobileVodafone

3 – La Tua TVTIMNRK

ASIA-PACKDDI – EZ Channel

SK Telecom Korea Telecom

3Optus

France

Sweden

Austria

3MobileTV

USA

Italy

2005-09-710

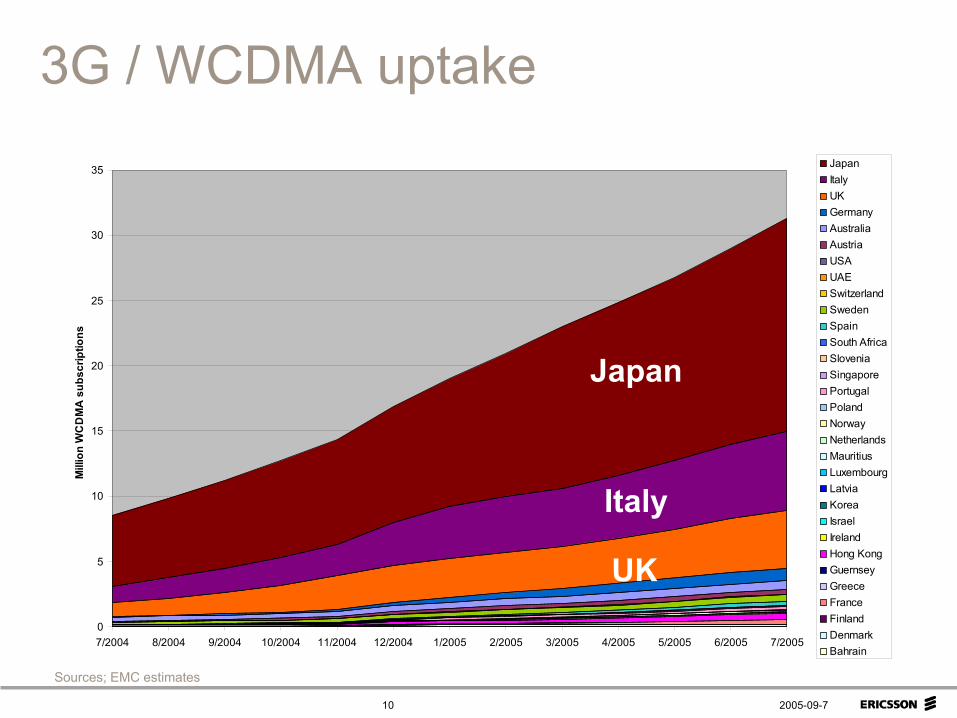

3G / WCDMA uptake

0

5

10

15

20

25

30

35

7/2004 8/2004 9/2004 10/2004 11/2004 12/2004 1/2005 2/2005 3/2005 4/2005 5/2005 6/2005 7/2005

Mill

ion

WC

DM

A s

ubsc

riptio

ns

JapanItalyUKGermanyAustraliaAustriaUSAUAESwitzerlandSwedenSpainSouth AfricaSloveniaSingaporePortugalPolandNorwayNetherlandsMauritiusLuxembourgLatviaKoreaIsraelIrelandHong KongGuernseyGreeceFranceFinlandDenmarkBahrain

Japan

Italy

UK

Sources; EMC estimates

2005-09-711

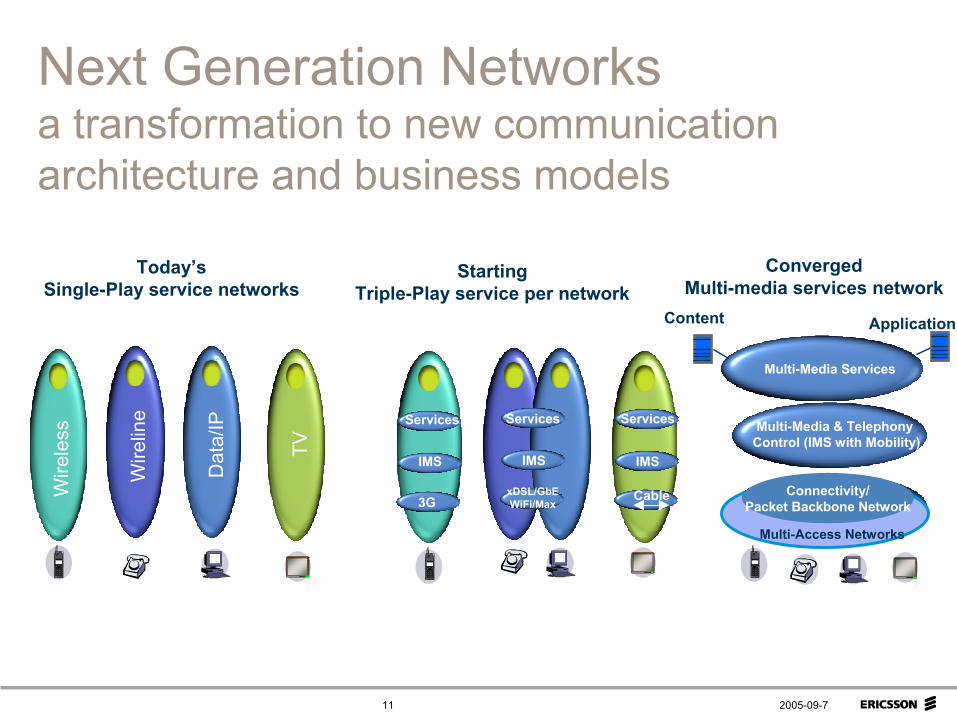

Today’sSingle-Play service networks

Dat

a/IP

Wire

less

Wire

line C

able

TV

Next Generation Networks a transformation to new communication architecture and business models

ApplicationContent

Connectivity

Multi-Media & Telephony Control (IMS with Mobility)

Multi-Media Services

Connectivity/Packet Backbone Network

Multi-Access Networks

TVStarting

Triple-Play service per network

3G

IMS IMS IMS

xDSL/GbEWiFi/Max

Cable

Services Services Services

ConvergedMulti-media services network

2005-09-712

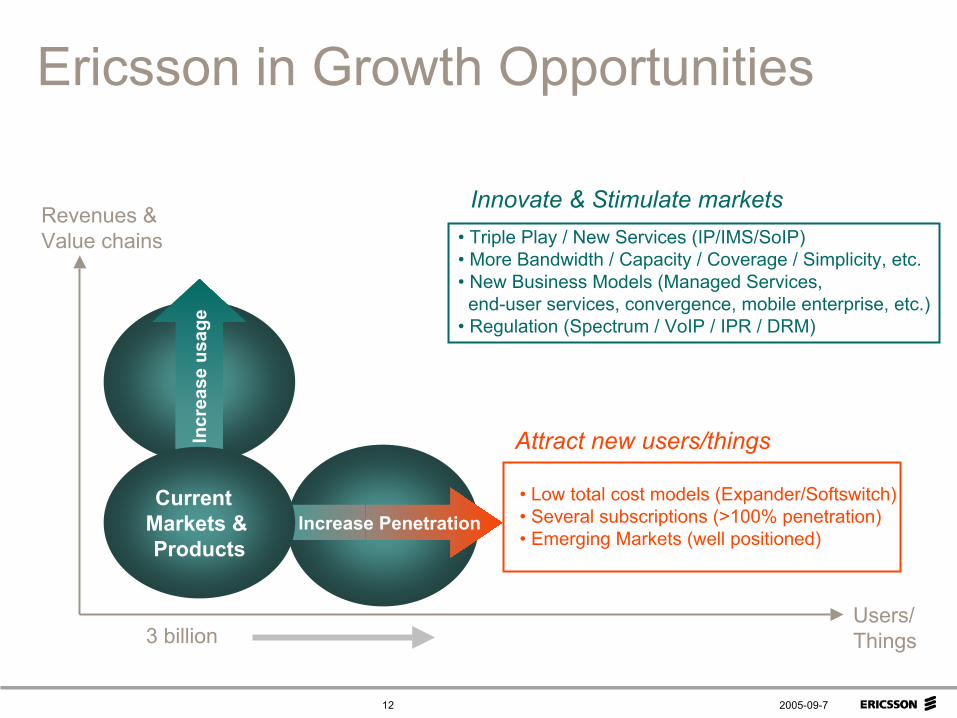

Ericsson in Growth Opportunities

Incr

eas e

usa

ge

Increase Penetration

Revenues &Value chains

Users/Things3 billion

Innovate & Stimulate markets• Triple Play / New Services (IP/IMS/SoIP)• More Bandwidth / Capacity / Coverage / Simplicity, etc.• New Business Models (Managed Services, end-user services, convergence, mobile enterprise, etc.)

• Regulation (Spectrum / VoIP / IPR / DRM)

Attract new users/things

• Low total cost models (Expander/Softswitch)• Several subscriptions (>100% penetration)• Emerging Markets (well positioned)

CurrentMarkets & Products

2005-09-713

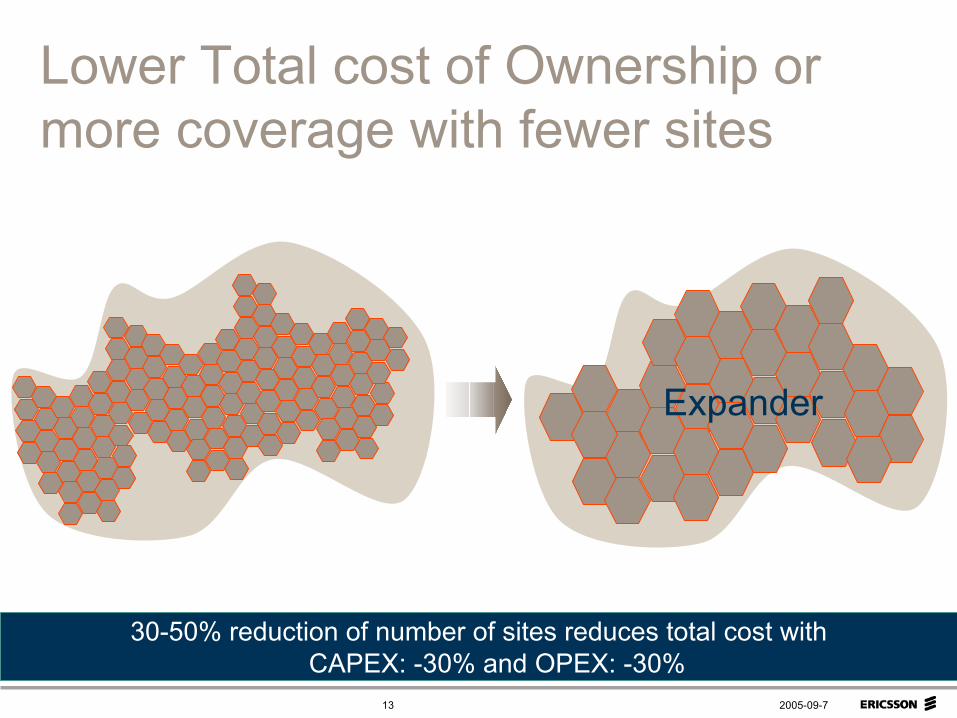

30-50% reduction of number of sites reduces total cost withCAPEX: -30% and OPEX: -30%

Lower Total cost of Ownership or more coverage with fewer sites

Expander

2005-09-714

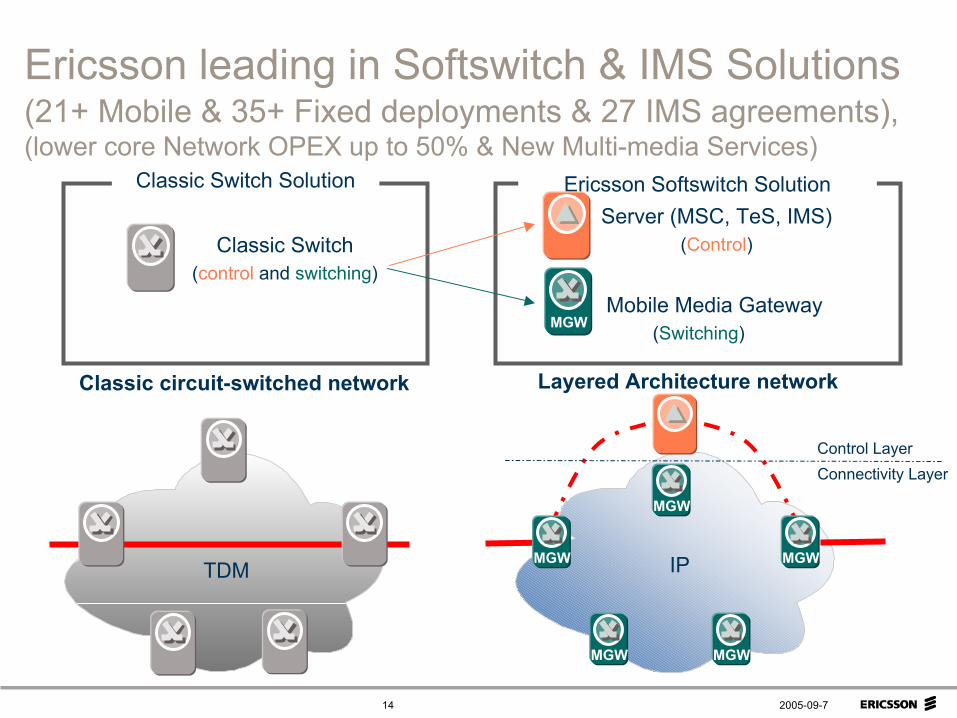

Ericsson leading in Softswitch & IMS Solutions(21+ Mobile & 35+ Fixed deployments & 27 IMS agreements), (lower core Network OPEX up to 50% & New Multi-media Services)

Classic Switch(control and switching)

Classic Switch SolutionServer (MSC, TeS, IMS)

(Control)

Mobile Media Gateway(Switching)

Ericsson Softswitch Solution

MGW

TDM IP

Control LayerConnectivity Layer

Classic circuit-switched network Layered Architecture network

MGW

MGW MGW

MGW

MGW

2005-09-715

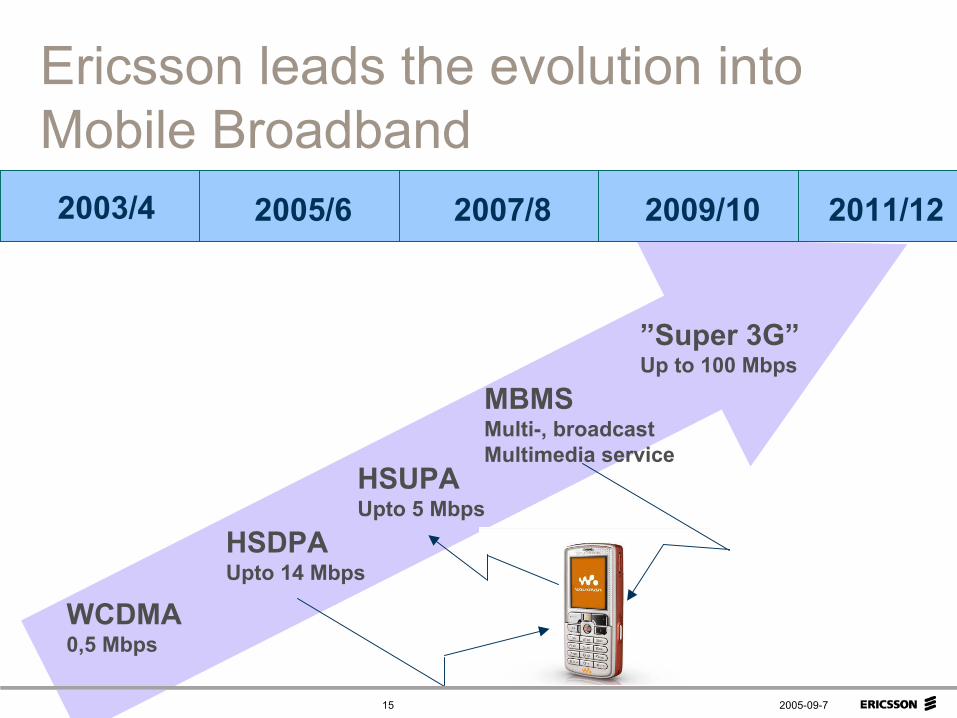

WCDMA0,5 Mbps

HSDPAUpto 14 Mbps

2005/6 2009/102003/4 2007/8 2011/12

HSUPAUpto 5 Mbps

”Super 3G”Up to 100 Mbps

MBMSMulti-, broadcast Multimedia service

Ericsson leads the evolution into Mobile Broadband

2005-09-716

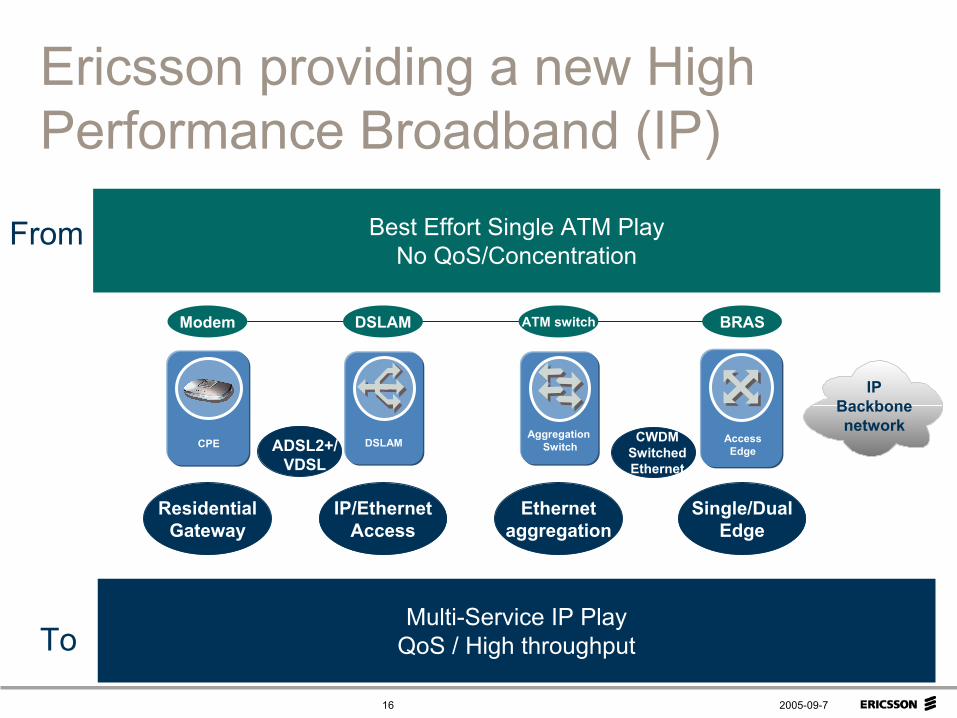

Ericsson providing a new High Performance Broadband (IP)

CPE DSLAMAggregation

SwitchAccessEdge

Modem DSLAM ATM switch BRAS

Best Effort Single ATM PlayNo QoS/Concentration

Multi-Service IP PlayQoS / High throughput

ResidentialGateway

IP/EthernetAccess

Ethernetaggregation

Single/DualEdge

From

To

IPBackbonenetwork

ADSL2+/VDSL

CWDMSwitchedEthernet

2005-09-717

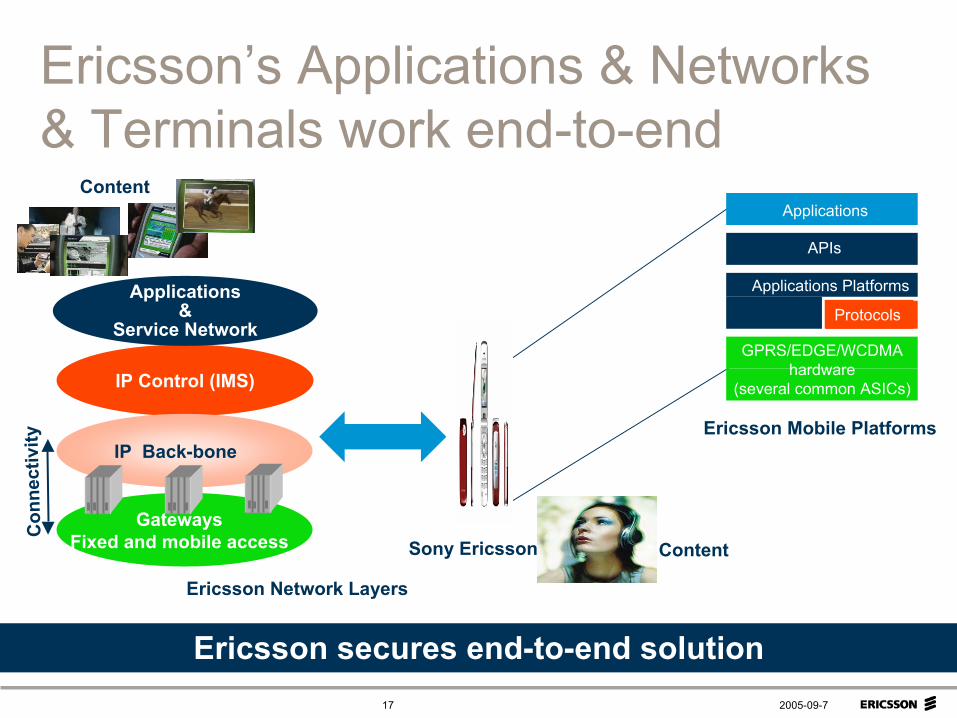

Ericsson’s Applications & Networks & Terminals work end-to-end

Ericsson secures end-to-end solution

Ericsson Network Layers

Sony Ericsson

Ericsson Mobile Platforms

Applications

APIs

Applications Platforms

Protocols

GPRS/EDGE/WCDMAhardware

(several common ASICs)IP Control (IMS)

IP Back-bone

GatewaysFixed and mobile access

Applications&

Service Network

Content

Con

nect

ivity

Content

2005-09-718

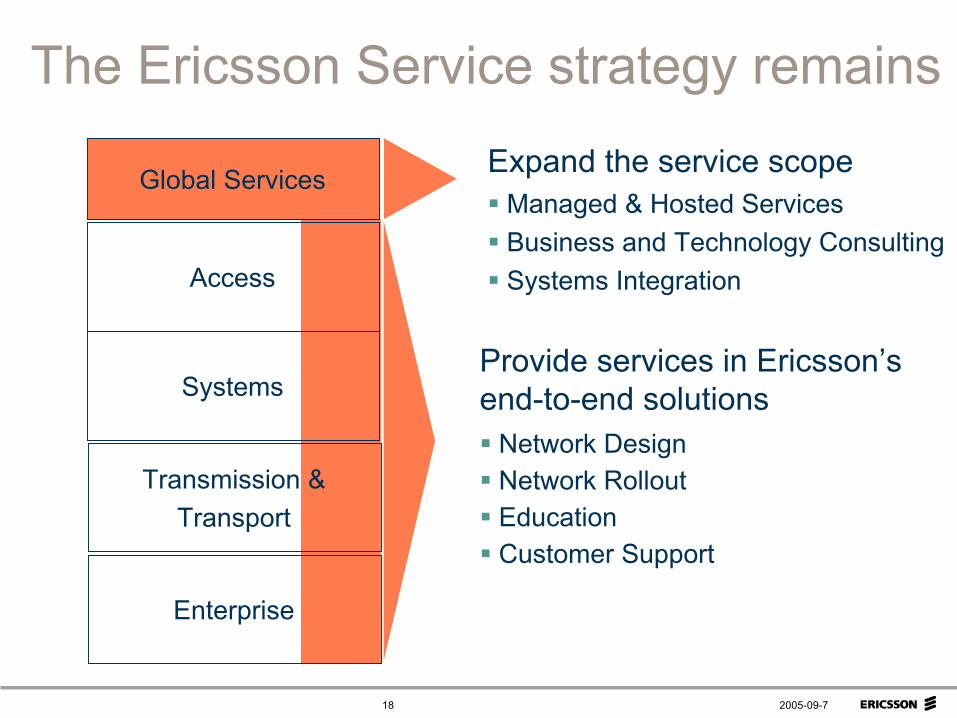

Global Services

Access

Expand the service scopeManaged & Hosted ServicesBusiness and Technology ConsultingSystems Integration

Provide services in Ericsson’send-to-end solutions

Network DesignNetwork RolloutEducationCustomer Support

The Ericsson Service strategy remains

Systems

Transmission &Transport

Enterprise

2005-09-719

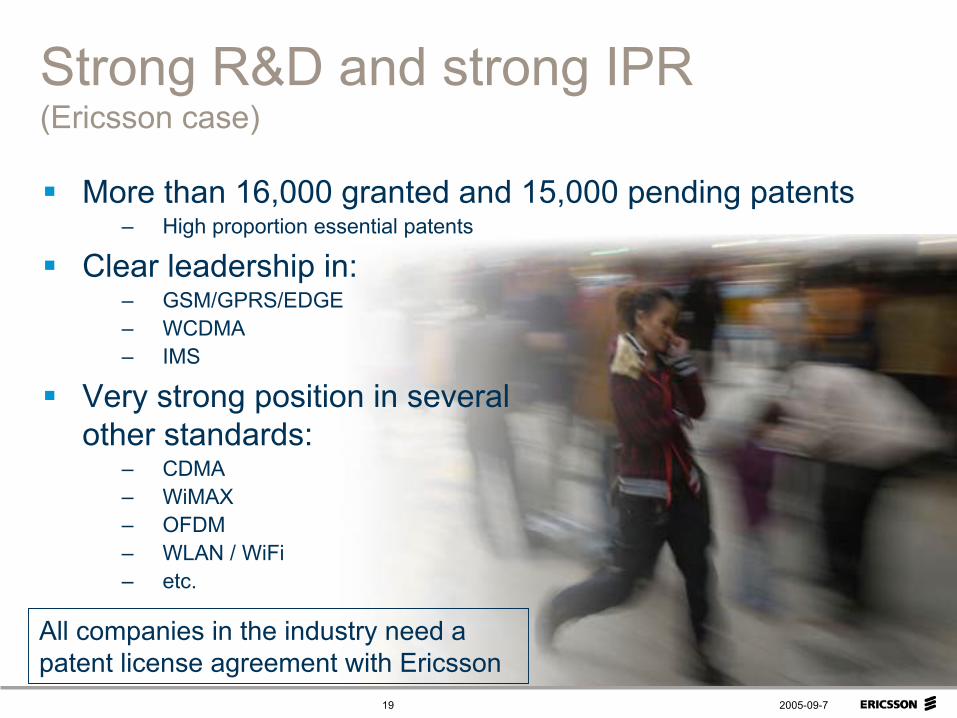

Strong R&D and strong IPR(Ericsson case)

More than 16,000 granted and 15,000 pending patents– High proportion essential patents

Clear leadership in:– GSM/GPRS/EDGE– WCDMA– IMS

Very strong position in severalother standards:

– CDMA– WiMAX– OFDM– WLAN / WiFi– etc.

All companies in the industry need a patent license agreement with Ericsson

2005-09-720