Equity Research on Cement Sector

85

Equity Research on Cement Sector PROJECT REPORT ON EQUITY RESEARCH ON CEMENT SECTOR IN BIRLA SUN LIFE INSURANCE COMPANY LTD. SUBMITTED IN PARTIAL FULFILMENT OF THE REQUIREMENT OF MASTER OF MANAGEMENT STUDIES BY GURPREET SINGH SALUJA ROLL NO. : 2010129 MMS-II (SEM III) YEAR 2010-2012 Page 1

Transcript of Equity Research on Cement Sector

Equity Research on Cement Sector

PROJECT REPORT ON

EQUITY RESEARCH ON CEMENT SECTORIN

BIRLA SUN LIFE INSURANCE COMPANY LTD.

SUBMITTED IN PARTIAL FULFILMENT OF THE REQUIREMENT OF

MASTER OF MANAGEMENT STUDIES

BY

GURPREET SINGH SALUJA

ROLL NO. : 2010129

MMS-II (SEM III)

YEAR 2010-2012

Page 1

Equity Research on Cement Sector

LALA LAJPATRAI INSTITUTE OF MANAGEMENT MAHALAXMI, MUMBAI - 400034

PROJECT REPORT ON

EQUITY RESEARCH ON CEMENT SECTOR

In

BIRLA SUN LIFE INSURANCE COMPANY LTD.

SUBMITTED IN PARTIAL FULFILMENT OF THE REQUIREMENT OF

MASTER OF MANAGEMENT STUDIES

BY

GURPREET SINGH SALUJA

ROLL NO. : 2010129

MMS-II (SEM III)

YEAR 2010-2012

Page 2

Equity Research on Cement Sector

LALA LAJPATRAI INSTITUTE OF MANAGEMENT MAHALAXMI, MUMBAI - 400034

SUMMER INTERNSHIP PROJECT

SUBMITTED BYGURPREET SINGH SALUJA

ROLL NO. : 2010129MMS – II (SEM III)

Year 2010-2012

Page 3

Equity Research on Cement Sector

Page 4

Equity Research on Cement Sector

Page 5

Equity Research on Cement Sector

CertifiCate

This is to certify that the project work titled “Equity Research on Cement Sector” is a summer internship work carried out by Mr. Gurpreet Singh Saluja.The project was completed for “Birla Sunlife Insurance Company Ltd.”, under the guidance of Mr. Nikesh Ruparel.I further certify that the said work has not been submitted in the part or in full, to any other University.

Date:

____________________ ____________________ Prof. Arati Kale Dr V.B. AngadiProject Guide Director,

Lala Lajpatrai Institute of Management

Page 6

Equity Research on Cement Sector

DECLARATION

I, Mr. Gurpreet Singh Saluja, student of Lala Lajpatrai Institute of Management of MMS II (Semester III) hereby declare that I have completed the summer internship project on Equity Research on Cement Sector with Birla Sunlife Insurance Company Ltd. in the Academic year 2010-2012. The information submitted is true & original to the best of my knowledge.

Signature of the student

Page 7

Equity Research on Cement Sector

ACKNOWLEDGEMENT

At the outset of this project, I would like to express my profound thanks to a few people without whose help, completion of this project would not have been possible.

First and foremost, I would like to express sincere thanks to Birla Sunlife Insurance Company Ltd. for giving me this opportunity to work with them.The list is endless but to name a few special people, I would like to thank Mr.Nikesh Ruparel for being extremely supportive and guiding me throughout my internship and giving me constant motivation and expert advice.

I would also like to thank the entire Birla Sunlife Insurance Department for providing me their precious time and making this internship a successful learning experience.

I am very grateful to Dr. Angadi, Directorof Lala Lajpat Rai Institute of Management, for giving me the opportunity to do this project in Birla Sunlife Insurance Company Ltd. My sincere thanks to Prof. Arati Kale for her valuable guidance and advice in completing this project.

I would also like to thank Prof. Narendran and Prof. Avni Pramod for being an excellent mentor and helping me whenever I approached him/her.

Last but not the least; I take pride in thanking my family, siblings and friends for their much valued support..

Page 8

Equity Research on Cement Sector

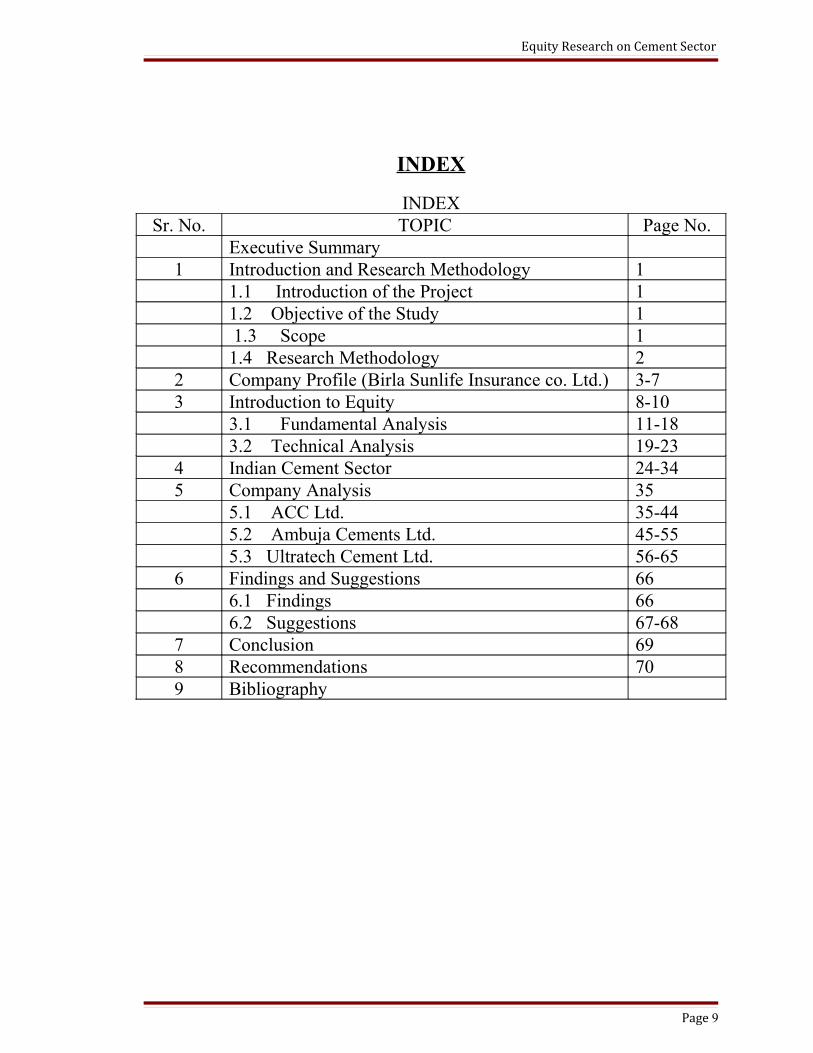

INDEX

INDEXSr. No. TOPIC Page No.

Executive Summary1 Introduction and Research Methodology 1

1.1 Introduction of the Project 11.2 Objective of the Study 1 1.3 Scope 11.4 Research Methodology 2

2 Company Profile (Birla Sunlife Insurance co. Ltd.) 3-73 Introduction to Equity 8-10

3.1 Fundamental Analysis 11-183.2 Technical Analysis 19-23

4 Indian Cement Sector 24-345 Company Analysis 35

5.1 ACC Ltd. 35-445.2 Ambuja Cements Ltd. 45-555.3 Ultratech Cement Ltd. 56-65

6 Findings and Suggestions 666.1 Findings 666.2 Suggestions 67-68

7 Conclusion 698 Recommendations 709 Bibliography

Page 9

Equity Research on Cement Sector

EXECUTIVE SUMMARY

Indian economy being one of the fastest developing economies in the world, companies

in India are growing at faster rate as compared to their growth rate a decade back. Many

Indian Companies are expanding their business globally with mergers and acquisitions.

Thus Indian equity markets today are attracting investors from around the world to take

advantage of India’s growth story.

As companies grow their shareholders are benefitted with good dividend and capital

appreciation on investment in equity shares of such companies. Number of companies

listed in stock exchange (BSE & NSE) has been increasing every year with new IPO’s

coming in the market.

In India people are realizing that equity has potential to give highest return as compared

to other investment avenues however people do not have proper knowledge in which

stock to invest their hard earned money to get good returns. They just invest on the basis

of tips given by brokers or friends which is not correct. The penetration of retail investors

in the Indian Markets is just around 5%, which means that the Indian investor is not able

to take the maximum advantage of India’s growth.

This report is meant to narrow down this gap between retail investors and equity markets

by simplifying the basic investment strategies and give a basic understanding of how

stocks are analysed for investment using the the theories of fundamental and technical

analysis

Equity Research helps the investor to know about the value, risk & volatility of the

covered security, and thus assist investors to decide whether to buy, hold, sell, sell short,

or simply avoid the security in question.

Page 10

Equity Research on Cement Sector

Fundamental analysis is very helpful to the investor, which is reflected in the investment

purpose. Fundamental analysis consist of three parts, they are economic, industry and

company. Any investors who go to systematic investment, he/she would like to know, the

complete scenario of the industry. If the industry looks positive then analyze various

companies in the sector. A Company is analyzed fundamentally to check its performance

and financial strength. With the help of this analysis investors comes to know whether to

make an investment in a particular stock.

In this report I have explained How to do fundamental analysis with analysis of cement

sector and few companies in the sector.

Page 11

Equity Research on Cement Sector

1. INTRODUCTION AND RESEARCH METHODOLOGY

1.1 INTRODUCTION OF THE PROJECT :

Equity Research is a subject which involves detailed knowledge of the share market. This

knowledge can be obtained through fundamental and technical analysis. Fundamental

Analysis looks into the company’s financial statements and key ratios to determine

whether a stock is worth buying or not. Fundamental Analysis is generally for long term

perspective. Technical Analysis make use of charts to determine the future price of a

particular stock. These analysis helps in making informed decisions which stock to buy,

hold or sell. This research report is prepared on cement sector in India and its three

companies namely ACC LTd, Ambuja Cements Ltd. and Ultratech Cement Ltd. and an

analysis is done in order to determine which company provides good returns to the

investors.

1.2 OBJECTIVE OF THE STUDY:

To acquire a deep knowledge of the Cement Sector through fundamental analysis.

• To assess the financial health & management effectiveness of the Company.

• To evaluate the share of the company ACC Ltd., Ambuja Cements Ltd. and

Ultratech Cement Ltd. on the basis of fundamental analysis.

• To find out how effectively resources are used within the enterprise

• To predict the future performance of the stocks and give suggestion on the same.

1.3 SCOPE:

The scope of project is limited to Understanding the basics of Fundamental analysis and

apply it to take a decision of investing in Cement Stocks.

Page 12

Equity Research on Cement Sector

1.4 RESEARCH METHODOLOGY:

Formation of the Problem

• Which significant ratios determine investment decision in share market ?

Collection of Data

Secondary Data:

The sources of secondary data are:

• Company Annual Report

• Internet-Websites

Research Limitation

• Information available on the websites was not updated.

• There was a limited time period to complete the project.

• This research is restricted to analysis of cement sector.

Page 13

Equity Research on Cement Sector

2. COMPANY PROFILE

Company Profile

Established in 2000, Birla Sun Life Insurance Company Limited (BSLI) is a joint venture

between the Aditya Birla Group, a well known and trusted name globally amongst Indian

conglomerates and Sun Life Financial Inc, leading international financial services

organization from Canada. The local knowledge of the Aditya Birla Group combined

with the domain expertise of Sun Life Financial Inc., offers a formidable protection for its

customers’ future.

With an experience of over 9 years, BSLI has contributed significantly to the growth and

development of the life insurance industry in India and currently ranks amongst the top 5

private life insurance companies in the country.

Page 14

Equity Research on Cement Sector

Known for its innovation and creating industry benchmarks, BSLI has several firsts to

its credit. It was the first Indian Insurance Company to introduce “Free Look Period”

and the same was made mandatory by IRDA for all other life insurance companies.

Additionally, BSLI pioneered the launch of Unit Linked Life Insurance plans amongst

the private players in India. To establish credibility and further transparency, BSLI also

enjoys the prestige to be the originator of practice to disclose portfolio on monthly basis.

These category development initiatives have helped BSLI be closer to its policy holders’

expectations, which gets further accentuated by the complete bouquet of insurance

products (viz. pure term plan, life stage products, health plan and retirement plan) that

the company offers.

Add to this, the extensive reach through its network of 600 branches and 175,000

empanelled advisors. This impressive combination of domain expertise, product range,

reach and ears on ground, helped BSLI cover more than 2 million lives since it

commenced operations and establish a customer base spread across more than 1500

towns and cities in India. To ensure that our customers have an impeccable experience,

BSLI has ensured that it has lowest outstanding claims ratio of 0.00% for FY 2008-09.

Additionally, BSLI has the best Turn Around Time according to LOMA on all claims

Parameters. Such services are well supported by sound financials that the Company has.

The AUM of BSLI stood at Rs. 8165 crs as on February 28, 2009, while as on March 31,

2009, the company has a robust capital base of Rs. 2000 crore.

Vision

To be a leader and role model in a broad based and integrated financial services business.

Mission

To help people mitigate risks of life, accident, health, and money at all stages and under

all circumstances.

Enhance the financial future of our customers including enterprises.

Values

Page 15

Equity Research on Cement Sector

Integrity, Commitment, Passion, Seamlessness, Speed

Management

The management team comprises of

• Mr. Kumar Mangalam Birla (Chairman)

• Mr.Niall O’Hare (Chief Actuarial Officer)

• Mr. Jayant Dua ( Managing Director and CEO)

A US $28 billion corporation, the Aditya Birla Group is in the league of Fortune 500

worldwide. It is anchored by an extraordinary force of 100,000 employees, belonging to

25 different nationalities. The group operates in 25 countries across six continents –

truly India's first multinational corporation.

Aditya Birla Group through Aditya Birla Financial Services Group (ABFSG), has a

strong presence across various financial services verticals that include life insurance,

fund management, distribution & wealth management, security based lending,

insurance broking, private equity and retail broking. The seven companies representing

ABFSG are Birla Sun Life Insurance Company, Birla Sun Life Asset Management

Company, Aditya Birla Money, Aditya Birla Finance, Birla Insurance Advisory &

Broking Services, Aditya Birla Capital Advisors and Apollo Sindhoori Capital

Investment. In FY 2008-09, the consolidated revenues of ABFSG from these businesses

crossed Rs. 4763 crore, registering a growth rate of 36%.

Sun Life Financial is a leading international financial services organisation providing a

diverse range of protection and wealth accumulation products and services to individuals

and corporate customers. Chartered in 1865, Sun Life Financial and its partners today

have operations in key markets worldwide, including Canada, the United States, the

United Kingdom, Ireland, Hong Kong, the Philippines, Japan, Indonesia, India, China

Page 16

Equity Research on Cement Sector

and Bermuda. As of December 31, 2008, the Sun Life Financial group of companies had

total assets under management of $381 billion.

Awards

At Birla Sun Life Insurance, winning is a way of life. Our innovative solutions and

customer-friendly services have been admired, appreciated and rewarded by customers

and the industry at large.

• Recruiting and Staffing Best in Class Awards.

• Outlook Money Awards 2004 BSLI - Best Life Insurer (Runner Up) 2004

TROPHY

• The 8th Asia Insurance Industry Awards 2004 - Birla Sun Life Insurance was

among the top five nominees in the category.

• The Indo-Canadian Business Chamber- BSLI awarded for its 'Successful

Performance' for 4 years April 2005.

• Birla Sun Life Insurance was presented 'The Hewitt Best Employers In India

Awards 2004' Trophy.

• Birla Sun Life Insurance was awarded 'The Great Place to Work Seminar Series

2007’ Presented by Anil Sachdev (Chairman & MD of Grow Talent Company

Page 17

Equity Research on Cement Sector

Ltd) Robert Levering (Co-founder Great Place to Work Institute) and Jehangir

Pocha (Business World Magazine).

• The Bhartiya Shiromani Puraskar awarded to BSLI at the seminar on "Economic

Development” New Delhi, on February 13, 2006. This is a Certificate of

Excellence for Enhancing the image of India presented by Dr. Bhishma Narain

Singh (Former Governor of Tamil Nadu & Assam) in association with the

"Institute of Economic Studies (IES)".

• Hewitt Best Employers in India 2004.

• Sponsorship Acknowledgement for - The Asia Insurance Review.

Future Business Continuity Plan

Birla Sun Life Insurance is one of the few Indian companies to have a fully operational

Business Continuity Plan (BCP) to ensure minimal impact to the organisation, its people,

and most importantly, its customers. Our Business Continuity Planning (BCP) Program is

a response plan which would ensure that in the event of a disaster we would be able to

restore and recover operations for critical processes within a predetermined time after the

disaster

BSLI’S Business Continuity Management Policy

To have a planned response in the event of any contingency ensuring recovery of critical

activities at agreed levels within agreed timeframe thereby complying with various

Page 18

Equity Research on Cement Sector

regulatory requirements and minimizing the potential business impact to BSLI.

Additionally to create a system that fosters continuous improvement of business

continuity management.

3. INTRODUCTION TO EQUITY

What is Equity?

In accounting and finance, equity is the residual claim or interest of the most junior class

of investors in assets, after all liabilities are paid. If valuations placed on assets do not

exceed liabilities, negative equity exists. In an accounting context, Shareholders' equity

(or stockholders' equity, shareholders' funds, shareholders' capital or similar terms)

represents the remaining interest in assets of a company, spread among individual

shareholders of common or preferred stock.

At the start of a business, owners put some funding into the business to finance assets.

This creates liability on the business in the shape of capital as the business is a separate

entity from its owners. Businesses can be considered to be, for accounting purposes, sums

of liabilities and assets; this is the accounting equation. After liabilities have been

accounted for, the positive remainder is deemed the owner's interest in the business.

This definition is helpful to understand the liquidation process in case of bankruptcy. At

first, all the secured creditors are paid against proceeds from assets. Afterward, a series of

creditors, ranked in priority sequence, have the next claim/right on the residual proceeds.

Ownership equity is the last or residual claim against assets, paid only after all other

creditors are paid. In such cases where even creditors could not get enough money to pay

their bills, nothing is left over to reimburse owners' equity. Thus owners' equity is

reduced to zero. Ownership equity is also known as risk capital, liable capital and equity.

Page 19

Equity Research on Cement Sector

What is Equity Shares?

Total equity capital of a company is divided into equal units of small denominations,

each called a share. For example, in a company the total equity capital of Rs 2,00,00,000

is divided into 20,00,000 units of Rs 10 each. Each such unit of Rs 10 is called a Share.

Thus, the company then is said to have 20, 00,000 equity shares of Rs 10 each. The

holders of such shares are members of the company and have voting rights.

Equity Investment

Equity investments generally refers to the buying and holding of shares of stock on a

stock market by individuals and firms in anticipation of income from dividends and

capital gain as the value of the stock rises. It also sometimes refers to the acquisition of

equity (ownership) participation in a private (unlisted) company or a startup (a company

being created or newly created). When the investment is in infant companies, it is

referred to as venture capital investing and is generally understood to be higher risk than

investment in listed going-concern situations.

How to invest in Equity Shares?

Investors can buy equity shares of a company from Security market that is from Primary

market or Secondary market.

The primary market provides the channel for sale of new securities. Primary market

provides opportunity to issuers of securities; Government as well as corporate, to raise

resources to meet their requirements of investment and/or discharge some obligation.

Investors can buy shares of a company through IPO (Initial Public Offering) when it is

first time issued to the public. Once shares are issued to the public it is traded in the

secondary market. Stock exchange only acts as facilitator for trading of equity shares.

Anyone who wishes to buy shares of a company can buy it from an existing shareholder

of a company.

Page 20

Equity Research on Cement Sector

Why should one invest in Equity in particular?

When you buy a share of a company you become a shareholder in that Company

.Equities have the potential to increase in value over time. It also provides your portfolio

with the growth necessary to reach your long term investment goals. Research studies

have proved that the equities have outperformed most other forms of investments in the

long term.

Equities are considered the most challenging and the rewarding, when compared to other

investment options. Research studies have proved that investments in some shares with a

longer tenure of investment have yielded far superior returns than any other investment.

However, this does not mean all equity investments would guarantee similar high returns.

Equities are high risk investments. One needs to study them carefully before investing

It is important for investors to note that while equity shares give highest return as

compared to other investment avenues it also carries highest risk therefore it is important

to find ‘ real value’ or ‘ intrinsic value’ of the security before investing in it. The

intrinsic value of a security being higher than the security’s market value represents a

time to buy. If the value of the security is lower than its market price, investors should

sell it.

To be able to value equity, we need to first understand how equity is to be analyzed.

Equity Share of any company can be analyzed through

• Fundamental Analysis

• Technical Analysis

Page 21

Equity Research on Cement Sector

3.1 FUNDAMENTAL ANALYSIS

Introduction

Fundamental analysis applied to the share market is a method of assessing whether a

company is a good investment using information from various sources such as financial

statements, company announcements, disclosures and economic and industry

reports.Fundamental analysis typically focuses on key statistics in a company's financial

statements to determine if the stock price is correctly valued.

Interpretation

Most fundamental information focuses on economic, industry, and company statistics.

The typical approach to analyzing a company involves four basic steps:

• Determine the condition of the general economy.

• Determine the condition of the industry.

• Determine the condition of the company.

• Determine the value of the company's stock.

Fundamental analysis includes:

• Economic analysis

• Industry analysis

Page 22

Equity Research on Cement Sector

• Company analysis

Economic Analysis

The economy is studied to determine if overall conditions are good for the stock market.

Is inflation a concern? Are interest rates likely to rise or fall? Are consumers spending? Is

the trade balance favorable? Is the money supply expanding or contracting? These are

just some of the questions that the fundamental analyst would ask to determine if

economic conditions are right for the stock market.

Industry Analysis

The company's industry obviously influences the outlook for the company. Even the best

stocks can post mediocre returns if they are in an industry that is struggling. It is often

said that a weak stock in a strong industry is preferable to a strong stock in a weak

industry.

Company Analysis

After determining the economic and industry conditions, the company itself is analyzed

to determine its financial health. This is usually done by studying the company's financial

statements. From these statements a number of useful ratios can be calculated. The ratios

fall under five main categories: profitability, price, liquidity, leverage, and efficiency.

When performing ratio analysis on a company, the ratios should be compared to other

companies within the same or similar industry to get a feel for what is considered

"normal."

Fundamental analysis looks at both ‘quantitative’ data (eg. revenue growth, margins and

financial ratios) and ‘qualitative’ data (eg. management strength, market position, patents

and proprietary technology).

Under this method, the company’s valuation is based on past performance, industry

trends, growth potential management and competition. Unlike the Efficient Market

Theory (EMT), which says that all information is already reflected in current prices and

Page 23

Equity Research on Cement Sector

therefore cannot be predicted, fundamental analysis believes that an intrinsic value may

be derived and that investors can profit by buying ‘undervalued’ shares and, where short

selling is allowed, selling ‘overvalued’ shares.

‘Undervalued’ shares are those that have a higher intrinsic valuation compared to the

current market price. Conversely, ‘overvalued’ shares are those with intrinsic valuations

less than the current market price. The assumption here is that in the long run, shares will

move towards the intrinsic valuation or the ‘correct price’.

Earnings

It is often said that earnings are the "bottom line" when it comes to valuing a company's

stock, and indeed fundamental analysis places much emphasis upon a company's

earnings. Simply put, earnings are how much profit (or loss) a company has made after

subtracting expenses. During a specific period of time, all public companies are required

to report their earnings on a quarterly basis through a 10-Q Report . Earnings are

important to investors because they give an indication of the company's expected

dividends and its potential for growth and capital appreciation. That does not necessarily

mean, however, that low or negative earnings always indicate a bad stock; for example,

many young companies report negative earnings as they attempt to grow quickly enough

to capture a new market, at which point they'll be even more profitable than they

otherwise might have been. The key is to look at the data underlying a company's

earnings on its financial statements and to use the following profitability ratios to

determine whether or not the stock is a sound investment.

Approaches to Fundamental Analysis

‘Top-down’ and ‘bottom-up’

There are two approaches to conducting fundamental analysis: top-down and bottom-up.

Both have their strengths and weaknesses and both have the same goal of choosing the

best companies for investment. The important thing is to use the approach that you are

comfortable with and which suits your investment style.

Page 24

Equity Research on Cement Sector

The bottom-up approach starts from the individual company before proceeding to the

general economic and market conditions. Advocates of this approach such as Warren

Buffett, Peter Lynch and Benjamin Graham primarily look for companies that are

financially healthy, have a strong track record of earnings growth and good prospects.

The general idea behind this is that there are the companies that can deliver profits in any

market environment and thrive even under difficult conditions. Industry and

macroeconomic factors are then considered, but are only secondary under this approach.

On the other hand, the top-down approach, as the name suggests, begins from the macro

level (general or broad) and ends at the micro level (specific). Under this approach, one

first looks at the global market conditions, then drills down to the state of a country’s

economy, then a specific sector and finally an individual company.

Fundamental Analysis Tools

Earnings Per Share:

Earnings Per Share = Net Earnings / Outstanding Shares

Earnings per share serve as an indicator of a company's profitability. An important aspect

of EPS that's often ignored is the capital that is required to generate the earnings (net

income) in the calculation. Two companies could generate the same EPS number, but one

could do so with less equity (investment) - that company would be more efficient at using

its capital to generate income and, all other things being equal would be a "better"

company. EPS plays major role in investment decision. One should look for high EPS

stocks and the higher the better is the stock. EPS comparison should be done from one

company to another which are in the same industry/sector and not from one company

from Auto sector and another company from IT sector.

There are three types of EPS numbers:

Trailing EPS - Trailing EPS means last year’s EPS which is considered as actual and for

ongoing current year.

Current EPS - Current EPS means which is still under projections and going to come on

Page 25

Equity Research on Cement Sector

financial year end.

Forward EPS - Forward EPS which is again under projections and going to come on

next financial year end

The EPS is helpful in comparing one company to another, assuming they are in the same

industry, but it alone doesn’t tell you the whole story of the company. For that

information, we need to look at some more ratios.

Price to Earnings Ratio:

The P/E looks at the relationship between the stock price and the company’s earnings.

The P/E is the most popular metric of stock analysis

You calculate the P/E by taking the share price and dividing it by the company’s EPS.

P/E = Stock Price / EPS

The P/E gives you an idea of what the market is willing to pay for the company’s

earnings. The higher the P/E the more the market is willing to pay for the company’s

earnings. Some investors read a high P/E as an overpriced stock and that may be the case,

however it can also indicate the market has high hopes for this stock’s future and has bid

up the price.

Conversely, a low P/E may indicate a “vote of no confidence” by the market or it could

mean this is a sleeper that the market has overlooked..

What is the “right” P/E? There is no correct answer to this question, because part of the

answer depends on your willingness to pay for earnings. The more you are willing to pay,

which means you believe the company has good long term prospects over and above its

current position, the higher the “right” P/E is for that particular stock in your decision-

making process. Another investor may not see the same value and think your “right” P/E

is all wrong.

Page 26

Equity Research on Cement Sector

Many investors try finding low P/E ratios stocks of high value growth companies and

make investments in such stocks which may prove real diamonds in future. Generally the

P/E ratios are compared of one company to other companies in the same sector/industry

and not in other industry before selecting any particular share.

Dividend Payout Ratio:

The Dividend Payout Ratio measures what a company’s pays out to investors in the form

of dividends.You calculate the DPR by dividing the annual dividends per share by the

Earnings Per Share.

DPR = Dividends Per Share / EPS

Growing companies will typically retain more profits to fund growth and pay lower or no

dividends. Companies that pay higher dividends may be in mature industries where there

is little room for growth and paying higher dividends is the best use of profits (utilities

used to fall into this group, although in recent years many of them have been

diversifying).

The payout ratio and the retained earning ratio are the indicators of the amount of

earnings that have been ploughed back in the business. The lower the payout ratio, the

higher will be the amount of earnings ploughed back in the business and vice versa. A

lower payout ratio or higher retained earnings ratio means a stronger financial position of

the company.

Dividend Yield:

The dividend yield of a company's stock offerings is the yearly total dividend payments

that the corporation makes divided by its market capitalization. The dividend yield can

also be expressed as dividend per share divided by the share price.

This is the return to shareholders based on current share prices (as determined by the

market).

Page 27

Equity Research on Cement Sector

Interpretation of Dividend Yield

High Dividend Yield Low Dividend Yield

Shows that stock is underpriced

(less than its real value)

- Indicates future dividend

payments may NOT be as high as

the current one

- Shows the company has been hit

hard in times of economic

depression and financial hardship

Shows that stock is overpriced

(more than its real value)

- Indicates future dividend

payments might actually be higher

than the current dividend payments

- Shows the company is relatively

financially stable

Return on Equity:

Return on Equity (ROE) is one measure of how efficiently a company uses its assets to

produce earnings. You calculate ROE by dividing Net Income by Book Value.

ROE = Net Income/ Book Value

A healthy company may produce an ROE in the 13% to 15% range. Like all metrics,

compare companies in the same industry to get a better picture. The investors favour the

company with higher ROE.

Return on Capital Employed:

Page 28

Equity Research on Cement Sector

This ratio shows the relationship between the profit earned before interest and tax and the

capital employed to earn such profit.

Return on Capital Employed

= Net Profit before Interest, Tax and Dividend/Capital Employed x 100

Where Capital Employed = Share Capital (Equity + Preference) + Reserves and Surplus

+ Long-term Loans – Fictitious Assets

Or

Capital Employed = Fixed Assets + Current Assets – Current Liabilities

Return on capital employed measures the profit, which a firm earns on investing a unit of

capital. The profit being the net result of all operations, the return on capital expresses all

efficiencies and inefficiencies of a business. This ratio has a great importance to the

shareholders and investors and also to management. To shareholders it indicates how

much their capital is earning and to the management as to how efficiently it has been

working. This ratio influences the market price of the shares. The higher the ratio, the

better it is.

Inventory Turnover Ratio

Cost of goods sold / Average inventory at cost

Usually a high inventory turnover/stock velocity indicates efficient management of

inventory because more frequently the stocks are sold, the lesser amount of money is

required to finance the inventory. A low inventory turnover ratio indicates an inefficient

management of inventory. A low inventory turnover implies over-investment in

inventories, dull business, poor quality of goods, stock accumulation, accumulation of

obsolete and slow moving goods and low profits as compared to total investment.

Page 29

Equity Research on Cement Sector

3.2 TECHNICAL ANALYSIS

Introduction

Should I buy today? What will prices be tomorrow, next week, or next year? Wouldn't

investing be easy if we knew the answers to these seemingly simple questions? technical

analysis has the answers to these questions.

Technical analysis is the process of analyzing a security's historical prices in an effort to

determine probable future prices. This is done by comparing current price action (i.e.,

current expectations) with comparable historical price action to predict a reasonable

outcome.

Simply put, technical analysis is the study of prices, with charts being the primary tool.

Technical analysts are sometimes referred to as chartists because they rely almost

exclusively on charts for their analysis.

Technical analysis is applicable to stocks, indices, commodities, futures or any tradable

instrument where the price is influenced by the forces of supply and demand. Price refers

to any combination of the open, high, low or close for a given security over a specific

timeframe. The time frame can be based on intraday (tick, 5-minute, 15-minute or

hourly), daily, weekly or monthly price data and last a few hours or many years.

Technicians, as technical analysts are called, are only concerned with two things:

• What is the current price?

• What is the history of the price movement?

Page 30

Equity Research on Cement Sector

The price is the end result of the battle between the forces of supply and demand for the

company's stock. The objective of analysis is to forecast the direction of the future price.

By focusing on price and only price, technical analysis represents a direct approach.

Technicians believe it is best to concentrate on what and never mind why. Why did the

price go up? It is simple, more buyers (demand) than sellers (supply). After all, the value

of any asset is only what someone is willing to pay for it.

Characteristics

Technical analysis employs models and trading rules based on price and volume

transformations, such as the relative strength index, moving averages, regressions, inter-

market and intra-market price correlations, cycles or, classically, through recognition of

chart patterns.

Technical analysis stands in contrast to the fundamental analysis approach to security and

stock analysis. Technical analysis "ignores" the actual nature of the company, market,

currency or commodity and is based solely on "the charts," that is to say price and

volume information, whereas fundamental analysis does look at the actual facts of the

company, market, currency or commodity. For example, any large brokerage, trading

group, or financial institution will typically have both a technical analysis and

fundamental analysis team.

Principles

Technicians say that a market's price reflects all relevant information, so their analysis

looks at the history of a security's trading pattern rather than external drivers such as

economic, fundamental and news events. Price action also tends to repeat itself because

investors collectively tend toward patterned behavior – hence technicians' focus on

identifiable trends and conditions.

The field of technical analysis is based on three assumptions:

Page 31

Equity Research on Cement Sector

• The market discounts everything.

• Price moves in trends.

• History tends to repeat itself.

The Market Discounts Everything

A major criticism of technical analysis is that it only considers price movement, ignoring

the fundamental factors of the company. However, technical analysis assumes that, at any

given time, a stock's price reflects everything that has or could affect the company -

including fundamental factors. Technical analysts believe that the company's

fundamentals, along with broader economic factors and market psychology, are all priced

into the stock, removing the need to actually consider these factors separately. This only

leaves the analysis of price movement, which technical theory views as a product of the

supply and demand for a particular stock in the market.

Price Moves in Trends

In technical analysis, price movements are believed to follow trends. This means that

after a trend has been established, the future price movement is more likely to be in the

same direction as the trend than to be against it. Most technical trading strategies are

based on this assumption.

History Tends To Repeat Itself

Another important idea in technical analysis is that history tends to repeat itself, mainly

in terms of price movement. The repetitive nature of price movements is attributed to

market psychology; in other words, market participants tend to provide a consistent

reaction to similar market stimuli over time. Technical analysis uses chart patterns to

Page 32

Equity Research on Cement Sector

analyze market movements and understand trends. Although many of these charts have

been used for more than 100 years, they are still believed to be relevant because they

illustrate patterns in price movements that often repeat themselves.

Other Usage

Technical analysis can be used on any security with historical trading data. This includes

stocks, futures and commodities, fixed-income securities, forex, etc. In this tutorial, we'll

usually analyze stocks in our examples, but keep in mind that these concepts can be

applied to any type of security. In fact, technical analysis is more frequently associated

with commodities and forex, where the participants are predominantly traders.

Now that you understand the philosophy behind technical analysis, we'll get into

explaining how it really works. One of the best ways to understand what technical

analysis is (and is not) is to compare it to fundamental analysis. We'll do this in the next

section.

Charting Terms and Indicators

Types of charts

OHLC "Bar Charts" — Open-High-Low-Close charts, also known as bar charts, plot

the span between the high and low prices of a trading period as a vertical line segment at

the trading time, and the open and close prices with horizontal tick marks on the range

line, usually a tick to the left for the open price and a tick to the right for the closing

price.

Candlestick chart — Of Japanese origin and similar to OHLC, candlesticks widen and

fill the interval between the open and close prices to emphasize the open/close

relationship. In the West, often black or red candle bodies represent a close lower than

the open, while white, green or blue candles represent a close higher than the open price.

Line chart — Connects the closing price values with line segments.

Page 33

Equity Research on Cement Sector

Point and figure chart — a chart type employing numerical filters with only passing

references to time, and which ignores time entirely in its construction.

Concepts

Resistance — a price level which acts as a ceiling above prices

Support — a price level which acts as a floor below prices

Breakout — the concept whereby prices forcefully penetrate an area of prior support or

resistance, usually, but not always, accompanied by an increase in volume.

Trending — the phenomenon by which price movement tends to persist in one direction

for an extended period of time

Average true range — averaged daily trading range, adjusted for price gaps

Chart pattern — distinctive pattern created by the movement of security prices on a

chart

Momentum — the rate of price change

Point and figure analysis — a priced-based analytical approach employing numerical

filters which may incorporate time references, though ignores time entirely in its

construction.

Overlays

Overlays are generally superimposed over the main price chart.

Resistance — an area that brings on increased selling

Support — an area that brings on increased buying

Trend line — a sloping line of support or resistance

Page 34

Equity Research on Cement Sector

Channel — a pair of parallel trend lines

Moving average — an average that lags behind the price action but filters out short term

movements.

4. CEMENT INDUSTRY

Industry Background

Pre Independence

The first endeavor to manufacture cement dates back to 1889 when a Calcutta based

company endeavored to manufacture cement from Argillaceous (kankar).

But the first endeavor to manufacture cement in an organized way commenced in

Madras. South India Industries Limited began manufacture of Portland cement in

1904.But the effort did not succeed and the company had to halt production.

Finally it was in 1914 that the first licensed cement manufacturing unit was set up by

India Cement Company Ltd at Porbandar, Gujarat with an available capacity of 10,000

tons and production of 1000 installed. The First World War gave the impetus to the

cement industry still in its initial stages. The following decade saw tremendous progress

in terms of manufacturing units, installed capacity and production. This phase is also

referred to as the Nascent Stage of Indian Cement Industry.

Page 35

Equity Research on Cement Sector

During the earlier years, production of cement exceeded the demand. Society had a

biased opinion against the cement manufactured in India, which further led to reduction

in demand. The government intervened by giving protection to the Industry and by

encouraging cooperation among the manufacturers.

In 1927, the Concrete Association of India was formed with the twin goals of creating a

positive awareness among the public of the utility of cement and to propagate cement

consumption.

Post Independence

The growth rate of cement was slow around the period after independence due to various

factors like low prices, slow growth in additional capacity and rising cost. The

government intervened several times to boost the industry, by increasing prices and

providing financial incentives. But it had little impact on the industry.

In 1956, the price and distribution control system was set up to ensure fair prices for both

the manufacturers and consumers across the country and to reduce regional imbalances

and reach self sufficiency.

Period of Restriction (1969-1982)

The cement industry in India was severely restrained by the government during this

period. Government hold over the industry was through both direct and indirect means.

Government intervened directly by exercising authority over production, capacity and

distribution of cement and it intervened indirectly through price control.

In 1977 the government authorized higher prices for cement manufactured by new units

or through capacity increase in existing units. But still the growth rate was below par.

In 1979 the government introduced a three tier price system. Prices were different for

cement produced in low, medium and high cost plants.

However the price control did not have the desired effect. Rise in input cost, reduced

profit margins meant the manufacturers could not allocate funds for increase in capacity.

Partial Control (1982-1989)

Page 36

Equity Research on Cement Sector

To give impetus to the cement industry, the Government of India introduced a quota

system in 1982.A quota of 66.60% was imposed for sales to Government and small real

estate developers. For new units and sick units a lower quota at 50% was affected. The

remaining 33.40% was allowed to be sold in the open market.

These changes had a desired effect on the industry. Profitability of the manufacturers

increased substantially, but the rising input cost was a cause for concern.

Post Liberalization

In 1989 the cement industry was given complete freedom, to gear it up to meet the

challenges of free market competition due to the impending policy of liberalization. In

1991 the industry was de licensed.This resulted in an accelerated growth for the industry

and availability of state of the art technology for modernization. Most of the major

players invested heavily for capacity expansion.To maximize the opportunity available in

the form of global markets, the industry laid greater focus on exports. The role of the

government has been extremely crucial in the growth of the industry.

Cement is one of the core industries which plays a vital role in the growth and expansion

of a nation. It is basically a mixture of compounds, consisting mainly of silicates and

aluminates of calcium, formed out of calcium oxide, silica, aluminium oxide and iron

oxide. The demand for cement depends primarily on the pace of activities in the business,

financial, real estate and infrastructure sectors of the economy. Cement is considered

preferred building material and is used worldwide for all construction works such as

housing and industrial construction, as well as for creation of infrastructures like ports,

roads, power plants, etc. Indian cement industry is globally competitive because the

industry has witnessed healthy trends such as cost control and continuous technology

upgradation.

Current Scenario

The Indian cement industry is the 2nd largest market after China. The cement industry in

India has received a great impetus from a number of infrastructure projects taken up by

the Government of India like road networks and housing facilities. While the Indian

Page 37

Equity Research on Cement Sector

cement industry enjoys a phenomenal phase of growth, experts reveal that it is poised

towards a highly prosperous future over the very recent years. The country’s cement

production is projected to grow at a compound annual growth rate (CAGR) of around 12

per cent during 2011-12 - 2013-14 to reach 303 million metric tonnes (MMT), as per the

RNCOS research report.

India’s cement industry has suffered two major setbacks recently. The largest domestic

supplier of coal to cement plants, Coal India Ltd, recently increased their prices by 30%.

In addition to this, the government’s 2011 Budget outlined a 2% hike in excise duty for

the already suffering cement sector. The two setbacks are likely to reduce profits in the

upcoming year. Despite a bad performance during the last four quarters, the cement

sector had started to turn around since December when the industry saw a gradual

increase of demand, in particular from the realty sector.

Indian cement industry comprises of 137 large and 365 mini cement plants. The large

plants employ 120,000 people, according to a recent report on the Indian cement industry

published by Cement Manufacturers Association (CMA).

Cement Production & Despatches (P)

Description Jan-11 Dec-10 Jan-102010-11 2009-10

(Apr-Jan)

Cement

Production14.52 13.59 14.65 136.51 130.85

Cement

Despatches14.47 13.60 14.59 135.56 130.09

Source: Cement Manufacturers' Association

Cement production during April to January 2010-11 was 136.51 million tonnes as

compared to 130.85 million tonnes during the same period for the year 2009-10.

Despatches were estimated at 135.56 million tonnes during April to January 2010-11

whereas during the same period for the year 2009-10, it stood at 130.09 million tonnes.

Page 38

Equity Research on Cement Sector

Key Drivers of Cement Industry

• Buoyant real estate market

• Increase in infrastructure spending

• Various governmental programmes like National Rural Employment Guarantee

• Low-cost housing in urban and rural areas under schemes like Jawaharlal Nehru

National Urban Renewal Mission (JNNURM) and Indira Aawas Yojana

Globalisation of Indian Cement Industry

Cement, being a bulk commodity, is a freight intensive industry and transporting it over

long distances can prove to be uneconomical. This has resulted in cement being largely a

regional play with the industry divided into five main regions viz. north, south, west, east

and the central region. While the southern region always had excess capacity in the past

owing to abundant availability of limestone, the western and northern regions are the

most lucrative markets on account higher demand and production shortfall. However,

with capacity addition taking place at a faster rate as compared to demand, prices have

remained southbound, especially in the recent past. Nevertheless, considering the

government's thrust on infrastructure long term demand remains intact.

Given the high potential for growth, quite a few foreign transnationals have been eyeing

the Indian markets and are planning to acquire domestic companies. Thus globalization

of Indian Cement Industry has led to many foreign companies engaging in mergers and

acquisitions of Indian cement companies. For example,

HeidelbergCement-IndoramaCementLtd.

Heidelberg Cement Company entered into an agreement for a 50% joint venture with the

Indorama Cement Ltd., situated in Mumbai, originally possessed by the Indorama S P

Lohia Group. Heidelberg Cement company is the leading German cement manufacturing

company. The Heidelberg Cement was set up in 1873 and has a long and prosperous

Page 39

Equity Research on Cement Sector

history. Being one of the best in the world the Heidelberg Cement Company has its bases

in different countries. The Heidelberg Cement Company has two manufacturing units in

India. A grinding plant in Mumbai and a cement terminal near Mumbai harbor. A clinker

plant is coming up in the state on Gujarat.

Holcim Cement - Gujarat Ambuja Cements(GACL)

Holcim Cement Company is among the leading cement manufacturing and supplying

companies in the world. It has increased its stake from 46.44 per cent to 50 per cent stake

in Ambuja Cement through the creeping acquisition route. It has also increased its stake

in ACC to reach 50.1 per cent.

Italcementi cement - Zuari Cement Limited

Italcementi Cement Company with the help of the Ciments Français, a subsidiary for its

global activities, has acquired shares of the famous Indian cement manufacturer - Zuari

Cement Limited. The acquisition was of 50% shareholding and the deal was of about 100

million Euros. Italcementi Cement is the 5th largest cement manufacturing company in

the world. The production capacity of the Italcementi cement company is about 70

million tons in a year. With the construction boom in India the company looks for a

stable future. In 2001 the Italcementi cement entered the Indian market scenario. It took

over the plant of the Zuari Cement Limited in Andhra Pradesh in southern India. The

joint venture earned revenues of around 100 million Euros and an operating profit of 4

million Euros.

Lafarge India is the subsidiary of the Lafarge Cement Company of France. It was

established in 1999 in India with the acquisition of the Tisco and the Raymond cement

plants. Lafarge Cement presently has three cement manufacturing units in India. One of

them is in Jharkhand which is used for the purpose of grinding and the other two are in

Chhattisgarh used for manufacturing. The Lafarge Cement Company was set up in the

year 1833 by Leon Pavin. Lafarge Cement Company situated in France is the leading

cement producing company in the world. It has plans for increasing the cement

production through technological innovations and maximization of the capacity of the

Page 40

Equity Research on Cement Sector

plant. It has a large network of distributors in the eastern part of India. The Lafarge

Cement Company is presently producing nearly 5.5 million tons of cement for the Indian

cement market.

During the first half of FY11, UltraTech Cement merged itself with Samruddhi Cement

to become the largest cement company in the country. Considering the long term growth

story, fair valuations, fragmented structure of the industry and low gearing, another wave

of consolidation would not come as a surprise.

Technological Advancements

Modernization and technology up-gradation is a continous process for any growing

industry and is equally true for the cement industry. At present, the quality of cement and

building materials produced in India meets international standards and benchmarks and

can compete in international markets. The productivity parameters are now nearing the

theoretical bests and alternate means. Substantial technological improvements have been

brought about and today, the industry can legitimately be proud of its state-of-the-art

technology and processes incorporated in most of its cement plants. This technology up

gradation is resulting in increased capacity, reduction in cost of production of cement.

SWOT Analysis

Strenghts:

• High Entry Barriers

Cement being a capital-intensive industry creates high entry barriers for the new

players. Moreover, the creation of distribution channel, acquisition of limestone

reserves etc makes entry of new players extremely difficult.

Weakness:

• Dependence on Government

Industry is highly dependent on government authorities for power supply. Cement

industry has been suffering from frequent power cuts.

Page 41

Equity Research on Cement Sector

• Increasing dependence on imported coal

Over the years, there has been deterioration in the quality of coal. In particular,

the ash content has increased implying lower calorific values for coal, and

improper and inefficient burning, etc. This has increased the dependence of

cement industry on imported coal. Poor port infrastructure and high volatility in

exchange rates creates concerns.

Oppurtunities:

• Growth from newer products - Ready to mix concrete

RMC is a value-added semi-finished product that results in a superior quality

concrete.Various advantages of RMC are quality control, eco friendly, greater

speed of construction, correct proportion of ingredients, lower wastage, reduce

manpower requirement etc. RMC is a high margin product as compared to site

mixed concrete (SMC). In India, RMC accounting for meager5% of cement

production that is converted to RMC as against 70% in developed countries.

Though India is the second largest cement manufacturer, it is among the lowest

cement consuming countries. In India per capita cement consumption is 122 kg,

which is far below the world average of approximately320 kg. With the growth of

economy, per capita cement consumption rises at brisk pace. It indicates there is a

potential for growth in cement industry.

Threats:

• Rising interest rate

Rising interest rates may impact housing demand and thereby affecting cement

demand and also capital expenditure.

• Substitutes

Bitumen and Engineering plastic have emerged as substitute of cement in road

and building construction.

Page 42

Equity Research on Cement Sector

Budget 2011:

The year 2010 was quite challenging for the entire cement industry. On the one hand,

demand off-take was weaker than expected due to lower realty and infrastructure

spending. Prolonged monsoons and logistical constraints further dampened the

construction activity. On the supply front, overcapacity continued to plague the industry.

Cement prices remained under pressure and caused margins to contract severely. The

industry is expected to end the current fiscal at about 75% capacity utilisation. And this

does not seem to be the end yet. The demand-supply mismatch is here to stay for quite

some time as the total industry cement capacity is expected to increase even further over

the next 18-24 months. Excess supply would reach its highest level (about 126 mtpa) in

FY13 with capacity going up to 393 mtpa. On the cost front, key raw material costs,

especially prices of coal show no signs of abating. Going forward, rising interest costs

remain a challenge for the construction industry. Much will depend on government’s

housing and infrastructure initiatives. Given this backdrop, over the next couple of years,

the margins of the cement companies will continue to remain under strain.

Budget Measures:

Incentives have been doled out for end users of cement such as the housing sector and

development of infrastructure.

• To replace excise with ad valorem duties on cement:

• In case of packaged cement, retail price per 50 kg bag not exceeding Rs 190 per

bag (equivalent to Rs 3,800 per tonne) would entail 10% ad valorem duty plus Rs

80 per tonne from Rs 290 per tonne earlier. In case of retail price per 50 kg bag

exceeding Rs 190 per bag, there would be an ad valorem duty of 10% plus Rs

160 per tonne from just 10% of retail sales price earlier.

• 10% ad valorem duty for all goods other than those cleared in packaged form.

• For cement clinker, there would be an ad valorem duty of 10% plus Rs 200 per

tonne from flat Rs 375 per tonne earlier.

Page 43

Equity Research on Cement Sector

• To reduce basic custom duty on two critical raw materials of the cement industry

viz. petcoke and gypsum to 2.5%

• Rate of minimum alternate tax (MAT) on book profits has been increased from

18% to 18.5%.

Budget Impact:

• Increased budgetary allocation towards infrastructural development and housing

is likely to boost demand for cement. Thus, cement manufacturers will continue to

benefit owing to increase in volumes.

• Impact of cut on customs duty on key raw materials such as petcoke and gypsum

would bring some relief to cement manufacturers who have been facing margin

pressures due to rising input costs.

• Cash dispensers and their parts have been fully exempted from basic customs

duty, to drive the financial inclusion agenda of the Government. This would result

in lower input cost and pressure on operating profit margin could marginally ease.

• The new excise duty structure will increase the tax incidence on the cement

industry.

Company Impact:

• With more incentives being spelled out for the infrastructure and housing sector,

cement manufacturers will continue to benefit. This is beneficial to all cement

companies, specifically the top layers catering to eastern region such as ACC and

Ultratech Cement.

• Lower duty on key materials will aid the profitability of large players like ACC,

Ambuja Cement and Ultratech Cement.

Future Ahead of Indian Cement Industry:

Page 44

Equity Research on Cement Sector

In the Budget 2011, with country's GDP pegged to grow ~8%+ annually going forward,

cement industry is likely to grow in double digit over long term and outlook for demand

remains positive. The cement industry is pushing for increased use of cement in highway

and road construction. The Ministry of Road Transport and Highways has planned to

invest US$ 354 billion in road infrastructure by 2012. Housing, infrastructure projects

and the nascent trend of concrete roads would continue to accelerate the consumption of

cement.

Increased infrastructure spending has been a key focus area. Finance Minister Pranab

Mukherjee has proposed to earmark US$ 47 billion for infrastructure development during

2011-12.

The infrastructure sector has received an impetus in the form of increased funds and tax

related incentives offered to attract investors for tapping the infrastructure opportunities

around the country. Introduction of tax free bonds, creation of infrastructure debt funds,

formulating a comprehensive policy for developing public private partnership projects are

some announcements which will give a fillip to the infrastructure sector which is the

backbone of any economy.

Page 45

Equity Research on Cement Sector

5. COMPANY ANALYSIS

5.1 ACC Ltd

ACC (ACC Limited) is India's foremost manufacturer of cement and concrete. ACC's

operations are spread throughout the country with 16 modern cement factories, more than

40 Ready mix concrete plants, 21 sales offices, and several zonal offices. It has a

workforce of about 9,000 persons and a countrywide distribution network of over 9,000

dealers.

Since inception in 1936, the company has been a trendsetter and important benchmark for

the cement industry in many areas of cement and concrete technology. ACC has a unique

track record of innovative research, product development and specialized consultancy

Page 46

Equity Research on Cement Sector

services. The company's various manufacturing units are backed by a central technology

support services centre - the only one of its kind in the Indian cement industry.

ACC has rich experience in mining, being the largest user of limestone. As the largest

cement producer in India, it is one of the biggest customers of the domestic coal industry,

of Indian Railways, and a considerable user of the country’s road transport network

services for inward and outward movement of materials and products.

Among the first companies in India to include commitment to environmental protection

as one of its corporate objectives, the company installed sophisticated pollution control

equipment as far back as 1966, long before pollution control laws came into existence.

Today each of its cement plants has state-of-the art pollution control equipment and

devices.

ACC plants, mines and townships visibly demonstrate successful endeavours in quarry

rehabilitation, water management techniques and ‘greening’ activities. The company

actively promotes the use of alternative fuels and raw materials and offers total solutions

for waste management including testing, suggestions for reuse, recycling and co-

processing.

ACC has taken purposeful steps in knowledge building. We run two institutes that offer

professional technical courses for engineering graduates and diploma holders which are

relevant to manufacturing sectors such as cement. The main beneficiaries are youth from

remote and backward areas of the country.

During the year ended December 31, 2010, it sold 20.984 million tons of cement and

0.120 million tons of clinker. The Company’s subsidiaries include ACC Concrete

Limited, Bulk Cement Corporation (India) Limited, ACC Mineral Resources Limited,

Lucky Minmat Limited, Encore Cements & Additives Private Limited, National

Limestone Co. Private Limited and National Limestone Co. Private Limited. In April

2010, the Company acquired 45% interest in Asian Concrete and Cements Private

Limited.

Page 47

Equity Research on Cement Sector

ACC has made significant contributions to the nation building process by way of quality

products, services and sharing expertise. Its commitment to sustainable development, its

high ethical standards in business dealings and its on-going efforts in community welfare

programmes have won it acclaim as a responsible corporate citizen. ACC’s brand name is

synonymous with cement and enjoys a high level of equity in the Indian market. It is the

only cement company that figures in the list of Consumer SuperBrands of India.

ACC Ltd recorded 2.13% YOY rise in dispatches for the month of December 2010.

Cement dispatch in December was 1.92 million tonnes as compared to 1.88 million tons a

year ago. Production of cement in December rose to 1.91 million tonnes as against 1.86

million tons in the corresponding period last year.

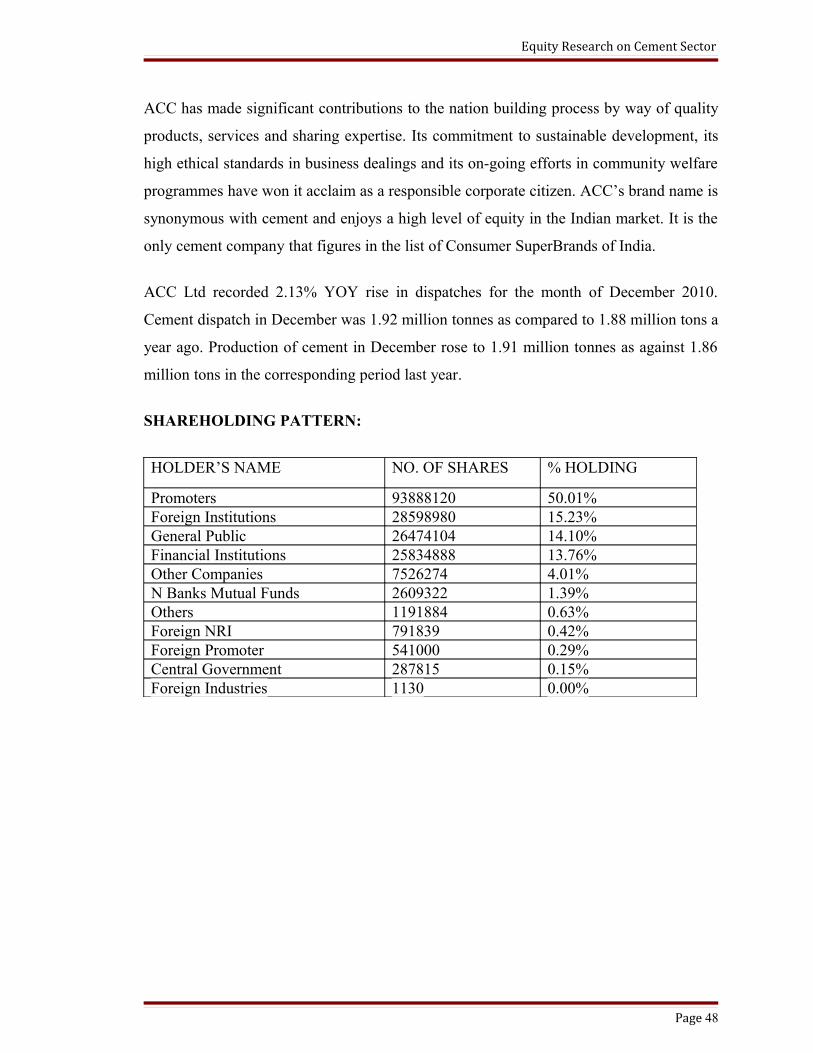

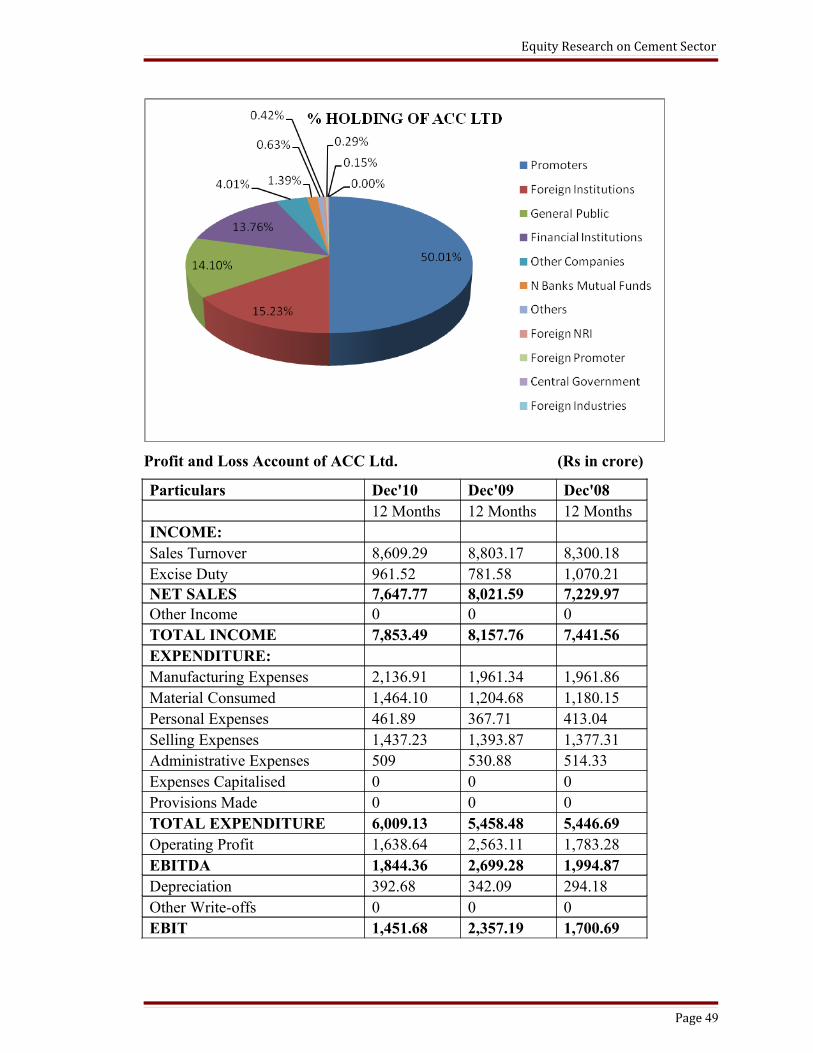

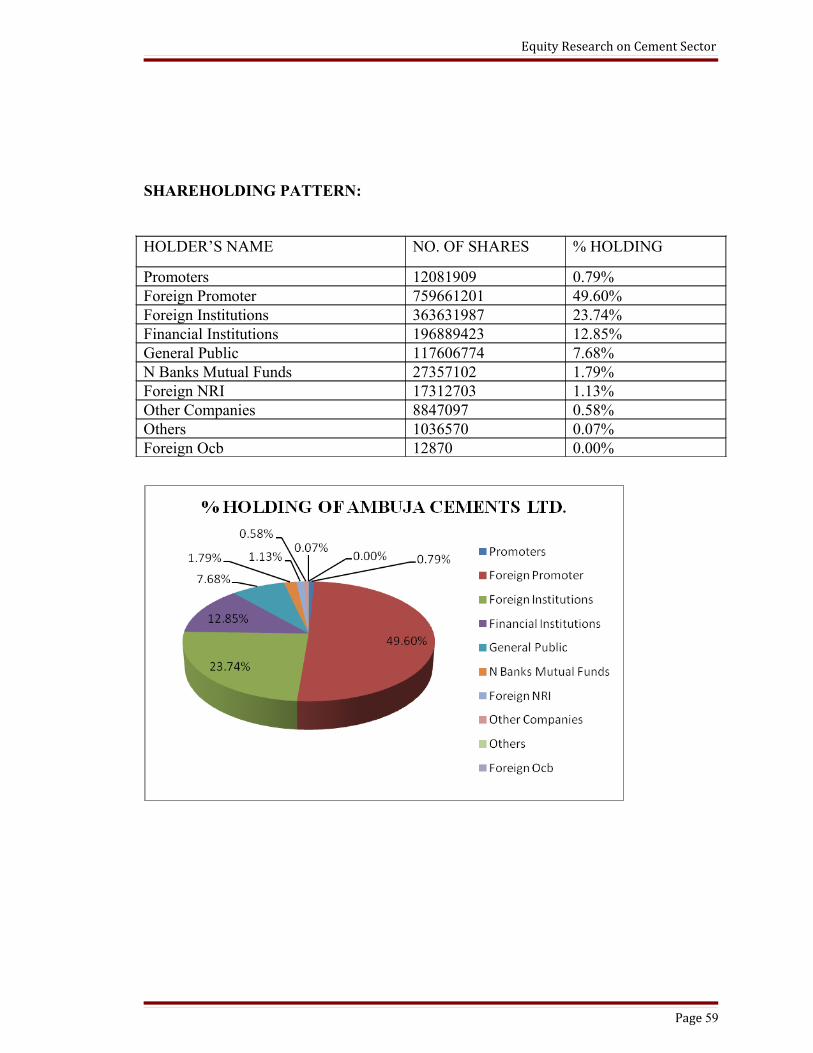

SHAREHOLDING PATTERN:

HOLDER’S NAME NO. OF SHARES % HOLDING

Promoters 93888120 50.01%Foreign Institutions 28598980 15.23%General Public 26474104 14.10%Financial Institutions 25834888 13.76%Other Companies 7526274 4.01%N Banks Mutual Funds 2609322 1.39%Others 1191884 0.63%Foreign NRI 791839 0.42%Foreign Promoter 541000 0.29%Central Government 287815 0.15%Foreign Industries 1130 0.00%

Page 48

Equity Research on Cement Sector

Profit and Loss Account of ACC Ltd. (Rs in crore)

Particulars Dec'10 Dec'09 Dec'08 12 Months 12 Months 12 MonthsINCOME: Sales Turnover 8,609.29 8,803.17 8,300.18Excise Duty 961.52 781.58 1,070.21NET SALES 7,647.77 8,021.59 7,229.97Other Income 0 0 0TOTAL INCOME 7,853.49 8,157.76 7,441.56EXPENDITURE: Manufacturing Expenses 2,136.91 1,961.34 1,961.86Material Consumed 1,464.10 1,204.68 1,180.15Personal Expenses 461.89 367.71 413.04Selling Expenses 1,437.23 1,393.87 1,377.31Administrative Expenses 509 530.88 514.33Expenses Capitalised 0 0 0Provisions Made 0 0 0TOTAL EXPENDITURE 6,009.13 5,458.48 5,446.69Operating Profit 1,638.64 2,563.11 1,783.28EBITDA 1,844.36 2,699.28 1,994.87Depreciation 392.68 342.09 294.18Other Write-offs 0 0 0EBIT 1,451.68 2,357.19 1,700.69

Page 49

Equity Research on Cement Sector

Interest 56.78 84.3 39.96EBT 1,394.90 2,272.89 1,660.73Taxes 424.15 688.93 524.6Profit and Loss for the Year 970.75 1,583.96 1,136.13Non Recurring Items (35.73) 1.23 41.25Other Non Cash Adjustments 185.92 21.54 35.39Other Adjustments -0.9 0 0.02REPORTED PAT 1,120.01 1,606.73 1,212.79KEY ITEMS Preference Dividend 0 0 0Equity Dividend 572.63 431.76 375.33Equity Dividend (%) 304.67 229.73 199.77Shares in Issue (Lakhs) 1,877.45 1,877.40 1,876.82EPS - Annualised (Rs) 59.66 85.58 64.62

Balance-Sheet of ACC Ltd. (Rs. In crore)

Particulars Dec'10 Dec'09 Dec'08Liabilities 12 Months 12 Months 12 MonthsShare Capital 187.95 188.02 187.88Reserves & Surplus 6,281.54 5,828.20 4,739.85Net Worth 6,469.49 6,016.22 4,927.73Secured Loans 518.05 559.74 450Unsecured Loans 5.77 7.18 32.03TOTAL LIABILITIES 6,993.31 6,583.14 5,409.76Assets Gross Block 8,076.95 6,826.27 5,835.67(-) Acc. Depreciation 2,994.51 2,667.98 2,365.97Net Block 5,082.44 4,158.29 3,469.70Capital Work in Progress. 1,562.80 2,156.21 1,602.86Investments. 1,702.67 1,475.64 679.08Inventories 914.98 778.98 793.27Sundry Debtors 178.28 203.7 310.17Cash And Bank 1,080.03 746.38 984.24Loans And Advances 752.41 714.55 779.76Total Current Assets 2,925.70 2,443.61 2,867.44Current Liabilities 2,627.84 2,558.73 2,245.39Provisions 1,652.46 1,091.88 963.93Total Current Liabilities 4,280.30 3,650.61 3,209.32

Page 50

Equity Research on Cement Sector

NET CURRENT ASSETS -1,354.60 -1,207.00 -341.88Misc. Expenses 0 0 0

TOTAL ASSETS (A+B+C+D+E) 6,993.31 6,583.14 5,409.76

Comments on Profit and Loss statement of ACC Ltd.

• Net Sales has increased by 10.95% in 2009 as compared to year 2008 but it has

reduced in the year 2010 by 4.66% compared to year 2009. This is due to

reduction in cement sales volumes.

• Raw Material consumption has increased by 2.08% in the year 2009. It has further

increased by 21.53% in 2010 as compared to 2009. This is because Average cost

of raw material has increased

• Personal Expenses reduced in the year 2009 by 10.97% as compared to the year

2008 but is has increased by 25.61% in the year 2010 as compared to the year

2009. This increase is due to Annual increase in salary and impact of revision in

wage agreement with the trade unions.

Page 51

Equity Research on Cement Sector

• Total expenditure has marginally increased in the year 2009 in comparison with

the year 2008. However in the year 2010 total expenditure has increased by

10.09% as compared to 2009.

• EBIT increased by 38.60% in 2009 as compared to 2008 but it decreased in the

year 2010 by 38.41% as compared to 2009. This is because of reduction in net

sales and increase in total expenditure.

• Interest expenses has decreased by 32.65% as compared to the year 2009 because

of repayment of Rupee Term loan of Rs. 50 crore (Rs. 200 Crore was repaid in

the month of Dec 2009).

• Reported PAT increased in 2009 by 32.48% as compared to 2008 but has reduced

in the year 2010 by 30.29% as compared to 2009 because of reduction in sales

and increase in expenditure.

Comments on Balance Sheet of ACC Ltd.

• Reserves and Surplus has increased by 22.09% in2009 as compared to 2008 but

has increased only by 7.78% in 2010 as compared to 2009.

• Secured Loans increased during 2009 by 24.39% as compared to 2008 but it

decreased in the year 2010 by 7.45% as compared to the year 2009. Secured

Loans decreased because of repayment of rupee term loan of Rs. 50 crore during

the current year.

Page 52

Equity Research on Cement Sector

• Unsecured Loans also decreased in 2009 by 77.58% as compared to 2008 and

further decreased in 2010 by 19.64% as comparedto previous year. This marginal

decrease is due to repayment of Rs. 3.03 as compared to previous year.

• Fixed Assets has increased by 19.85% in the year 2009 as compared to the year

2008 and further increased by 22.22% in the year 2010 as compared to 2009. This

increase is mainly due to mainly due to commissioning of Bargarh expansion /

modernization project, Wadi capacity expansion, captive power plants at Chanda

and Bargarh, grinding units at Kudithini and Thondebhavi and other

capitalizations.

• Capital work in progress decreased by 27.52% as compared to previous year

mainly due to capitalization of projects.

• Investments increased to a great extent in 2009 by 117.30% as compared to 2008.

It further increased in 2010 by 15.39% as compared to 2009. This increase is

because of increase in the investment of mutual funds as compared to previous

year. As on December 31, 2010 the company invested Rs. 1,307.56 Crore

(Previous Year Rs. 1,129.47 Crore) in mutual funds of its surplus cash. 100%

Investment in Encore Cement and Additives Private Limited, a Company engaged

in manufacturing and supply of ground Slag. 45% Investment in Asian Concretes

and Cements Private Limited, a Company engaged in cement grinding.

• Inventories decreased in 2009 by 1.80% but increased in the year 2010 by 17.46%

as compared to previous year. Stock-in-trade as on December 31, 2010 was higher

than the level of December 31, 2009 by Rs. 56.57 Crore. raw materials inventory

Page 53

Equity Research on Cement Sector

was higher by 50.45% due to increase in inventories of gypsum and slag.

Inventory of Coal increased by 44.28% as compared to previous year

• Sundry Debtors decreased by 34.33% in 2009 as compared to 2008 and it further

decreased to 12.48% in the year 2010 as compared to the year 2009 which

indicates collection period of ACC Ltd. has improved yoy.

• Loans and Advances decreased in 2009 as compared to 2008 but has increased in

2010 by 5.30% as compared to 2010.

• Current Liabilities increased by 13.95% in 2009 as compared to 2008 but has

marginally increased in 2010 by 2.70% as compared to previous year.

• Provisions has increased by 13.27% in 2009 when compared to 2008 but

increased further to 51.34% in the year 2010 as compared to previous year. This

increase is due to following reasons employee benefits provision has increased by

Rs. 22.99 crore on account of change in discount rate as well as change in

assumption for salary escalation rate. Proposed a one-time special Platinum

Jubilee final dividend of Rs. 7.50 per share. Higher Provision for income tax.

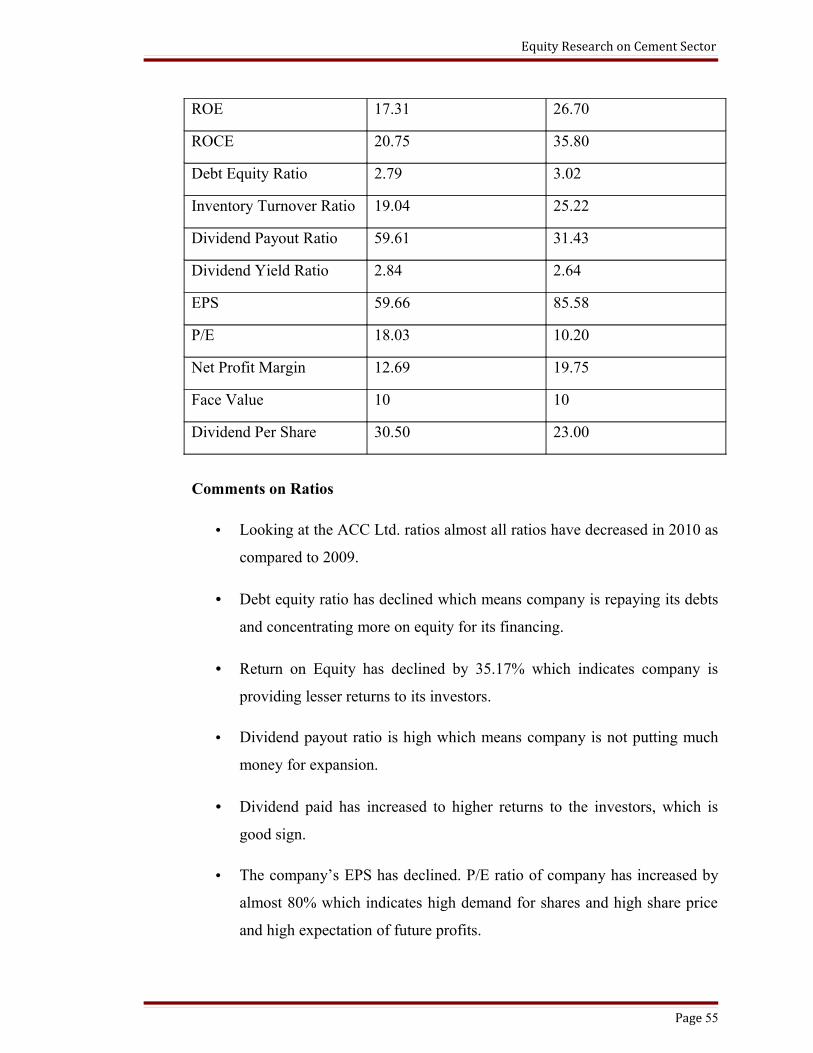

Ratios of ACC Cement

Ratios Year 2010 Year 2009

Page 54

Equity Research on Cement Sector

ROE 17.31 26.70

ROCE 20.75 35.80

Debt Equity Ratio 2.79 3.02

Inventory Turnover Ratio 19.04 25.22

Dividend Payout Ratio 59.61 31.43

Dividend Yield Ratio 2.84 2.64

EPS 59.66 85.58

P/E 18.03 10.20

Net Profit Margin 12.69 19.75

Face Value 10 10

Dividend Per Share 30.50 23.00

Comments on Ratios

• Looking at the ACC Ltd. ratios almost all ratios have decreased in 2010 as

compared to 2009.

• Debt equity ratio has declined which means company is repaying its debts

and concentrating more on equity for its financing.

• Return on Equity has declined by 35.17% which indicates company is

providing lesser returns to its investors.

• Dividend payout ratio is high which means company is not putting much

money for expansion.

• Dividend paid has increased to higher returns to the investors, which is

good sign.

• The company’s EPS has declined. P/E ratio of company has increased by

almost 80% which indicates high demand for shares and high share price

and high expectation of future profits.

Page 55

Equity Research on Cement Sector

ACC Ltd. Chart

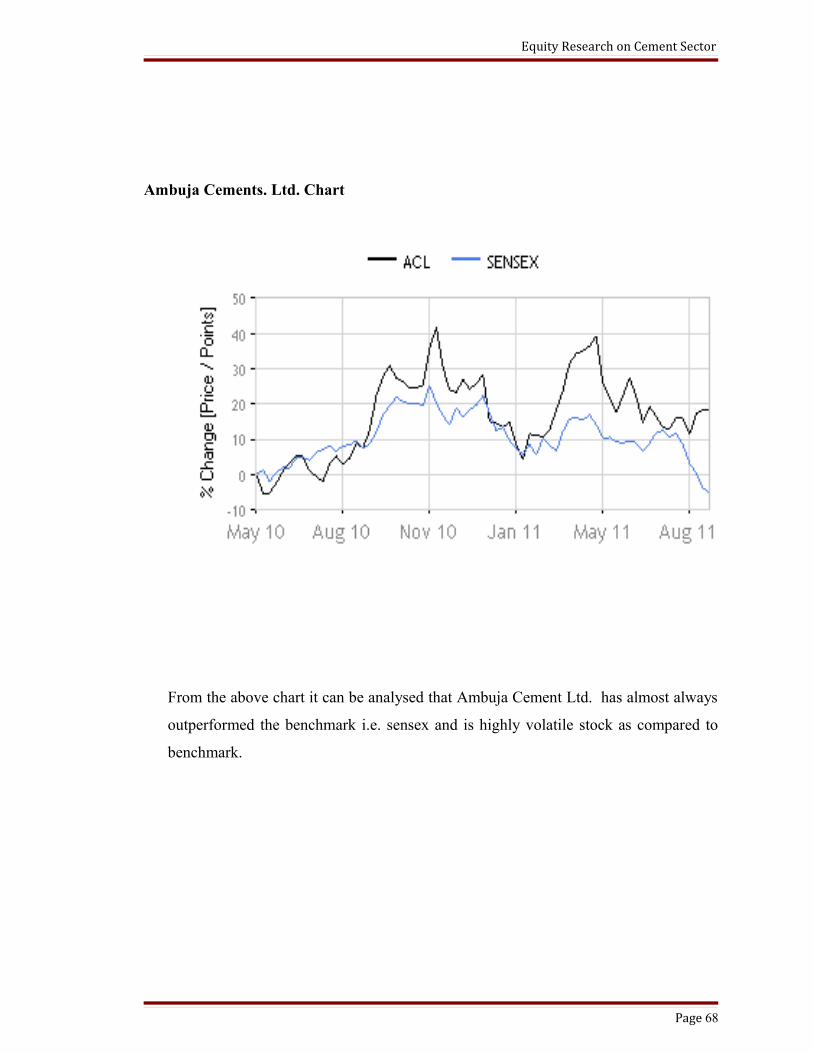

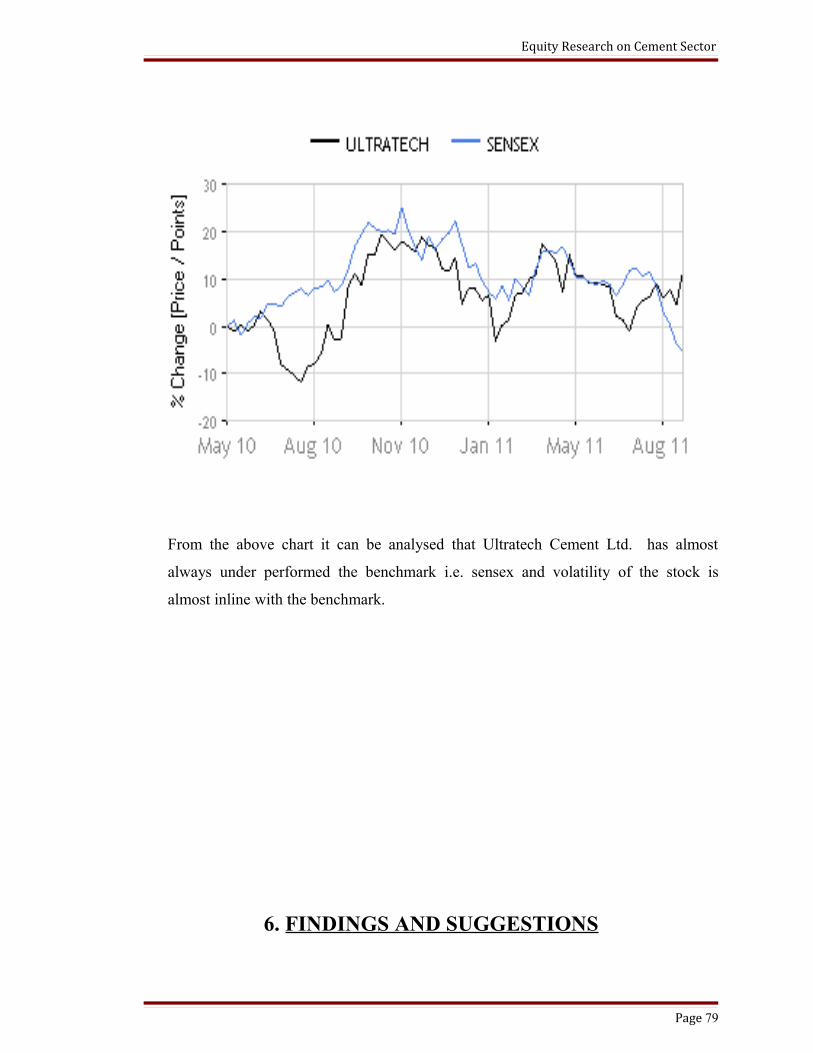

From the above chart it can be analysed that ACC Ltd. approximately till December

2010 has been in line with benchmark i.e. sensex and from January 2011 it has

outperformed the benchmark.

Page 56

Equity Research on Cement Sector

5.2 AMBUJA CEMENTS LTD.

Ambuja Cements Ltd. (ACL) is one of the leading cement manufacturing companies in

India. The company was incorporated in the year 1981 as Ambuja Cements Pvt Ltd and it

was rehabilitated into a public limited company on 19th March 1983 as Gujarat Ambuja

Cements Ltd The Company was founded by Narotam Sekhsaria in 1983 with a partner,

Suresh Neotia. Sekhsaria’s business acumen and leadership skills put the company on a

fast track to growth. The Company commenced cement production in 1986.

ACL has grown dynamically over the past decade. Its current cement capacity is about 25

million tonnes. The Company has five integrated cement manufacturing plants and eight