EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS WACHOVIA pg. 1 Upstream Master Limited...

26

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS WACHOVIA pg. 1 Upstream Master Limited Partnerships “A Wall Street Perspective” IPAA, January 2008 For certain non-U.S. institutional readers, this research is issued by Wachovia Securities International Limited, which is regulated in the U.K. by the Financial Services Authority. Wachovia Securities International Limited provides investment services in certain countries, and each has approved the contents of this document for viewing by approved parties in the country in which it does business. Not all investments or related services are available to residents of every country. Please consult your Financial Advisor or the Wachovia Securities office in your area for additional information. U.S. residents are directed to Wachovia.com for investment and related services. Yves Siegel, CFA (212) 214-5036 Michael Blum (212) 214-5037 Sharon Lui, CPA (212) 214-5035 Eric Shiu (212) 214-5038 Praneeth Satish (212) 214-8056 A publication of Wachovia Capital Markets, LLC Ronald Londe (314) 955-3829 Jeffrey Morgan, CFA (314) 955-6558

-

Upload

adonis-swift -

Category

Documents

-

view

216 -

download

2

Transcript of EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS WACHOVIA pg. 1 Upstream Master Limited...

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 1

Upstream Master Limited Partnerships

“A Wall Street Perspective”IPAA, January 2008

For certain non-U.S. institutional readers, this research is issued by Wachovia Securities International Limited, which is regulated in the U.K. by the Financial Services Authority. Wachovia Securities International Limited provides investment services in certain countries, and each has approved the contents of this document for viewing by approved parties in the country in which it does business. Not all investments or related services are available to residents of every country. Please consult your Financial Advisor or the Wachovia Securities office in your area for additional information. U.S. residents are directed to Wachovia.com for investment and related services.

Yves Siegel, CFA (212) 214-5036

Michael Blum (212) 214-5037

Sharon Lui, CPA(212) 214-5035

Eric Shiu (212) 214-5038

Praneeth Satish(212) 214-8056

A publication ofWachovia Capital

Markets, LLC

Ronald Londe(314) 955-3829

Jeffrey Morgan, CFA(314) 955-6558

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 2

Discussion Points

The Jury Is Still Out On Upstream MLPs Long-term sustainability has become a concern Unlike investors in Canadian royalty trusts, investors in upstream MLPs expect

sustainable distributions It is still unclear whether upstream MLPs are properly allocating adequate capital to

replace reserves and sustain distributions over the long term

Uncertainty Has Resulted In Some Headwinds For Recent Upstream MLP IPOs Market appears to be demanding a higher yield for new upstream MLP issues Issuers may pull or delay IPOs given the narrowing spread between upstream MLP

valuations and E&P C-Corp valuations

The Silver Lining Crude oil prices are at record levels and natural gas prices remain relatively strong While financing costs have increased, acquisitions will still likely get done

Closing Remarks

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 3

Source: FactSet, Standard & Poor’s, Wachovia Capital Markets, LLC

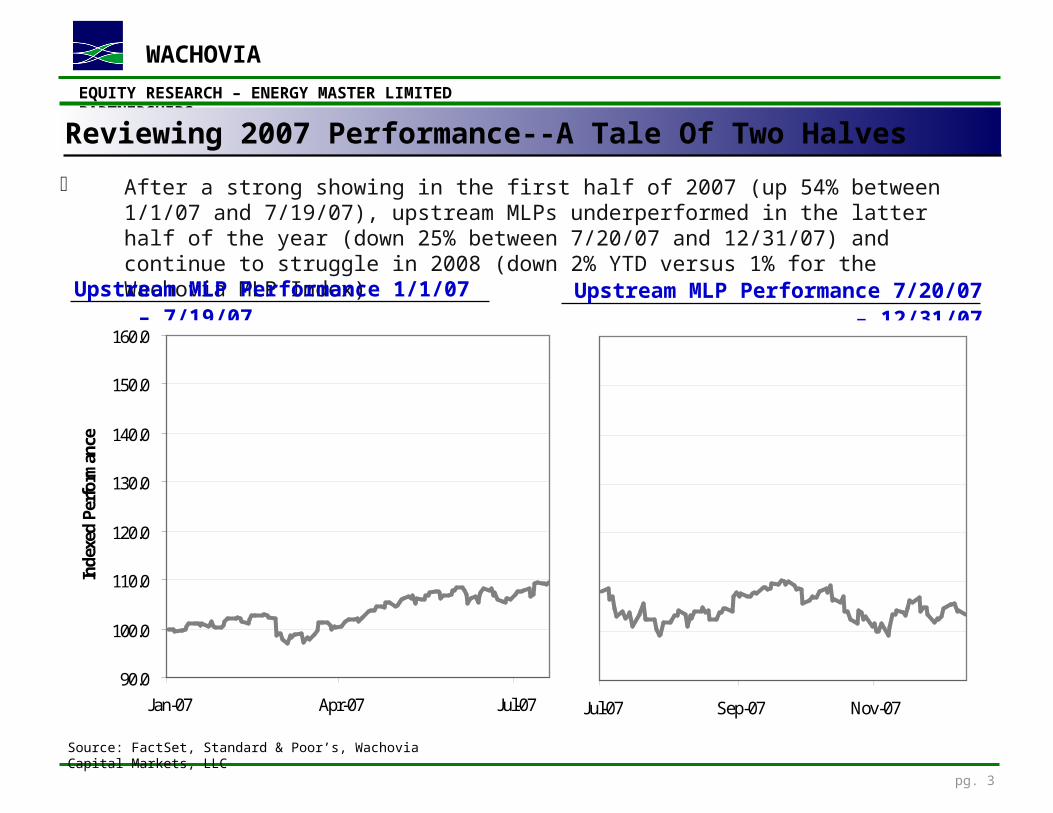

Reviewing 2007 Performance--A Tale Of Two Halves

After a strong showing in the first half of 2007 (up 54% between 1/1/07 and 7/19/07), upstream MLPs underperformed in the latter half of the year (down 25% between 7/20/07 and 12/31/07) and continue to struggle in 2008 (down 2% YTD versus 1% for the Wachovia MLP Index)

Upstream MLP Performance 1/1/07 – 7/19/07

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

Jan-07 Apr-07 Jul-07

Inde

xed

Perf

orm

ance

Upstream MLPs: +54%

S&P 500: +10%

WMLP Index: +20%

Upstream MLP Performance 7/20/07 – 12/31/07

Jul-07 Sep-07 Nov-07

Upstream MLPs: -25%

WMLP Index: -13%

S&P 500: -9%

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 4

Source: FactSet, Standard & Poor’s, Wachovia Capital Markets, LLC

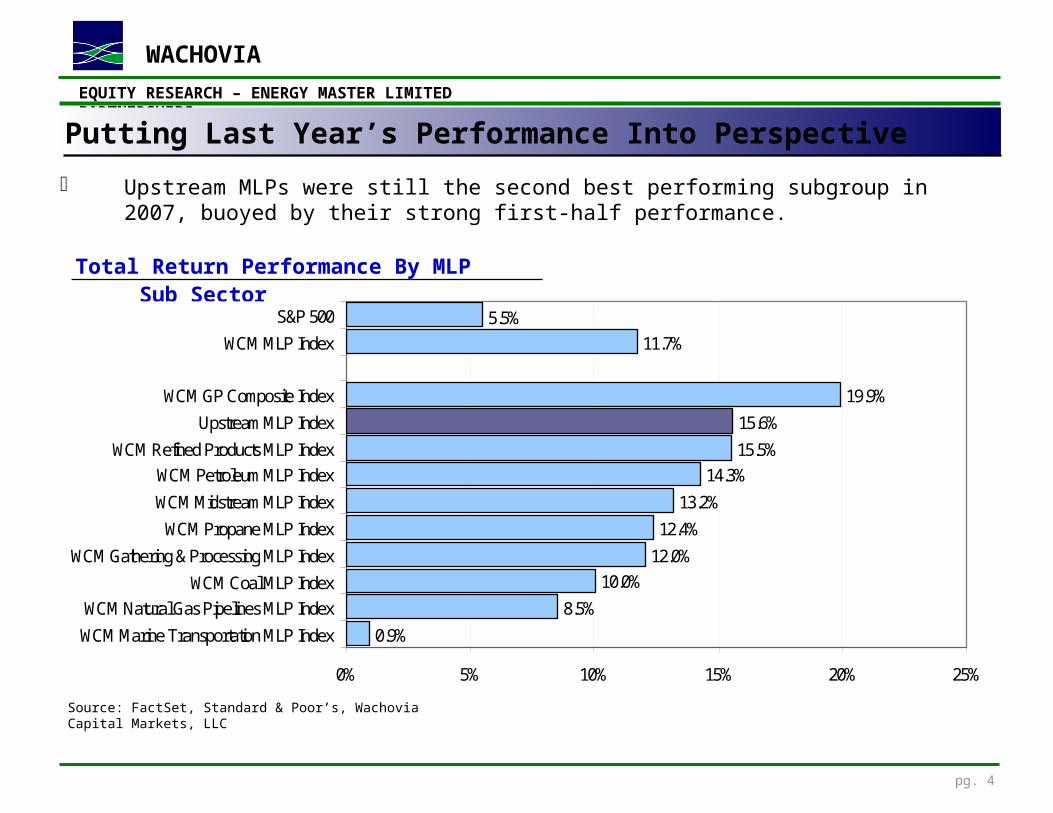

Putting Last Year’s Performance Into Perspective

Upstream MLPs were still the second best performing subgroup in 2007, buoyed by their strong first-half performance.

Total Return Performance By MLP Sub Sector

0.9%

8.5%

10.0%12.0%

12.4%

13.2%

14.3%15.5%

15.6%

19.9%

11.7%5.5%

0% 5% 10% 15% 20% 25%

WCM Marine Transportation MLP Index

WCM Natural Gas Pipelines MLP IndexWCM Coal MLP Index

WCM Gathering & Processing MLP Index

WCM Propane MLP Index

WCM Midstream MLP Index

WCM Petroleum MLP IndexWCM Refined Products MLP Index

Upstream MLP Index

WCM GP Composite Index

WCM MLP Index

S&P 500

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 5

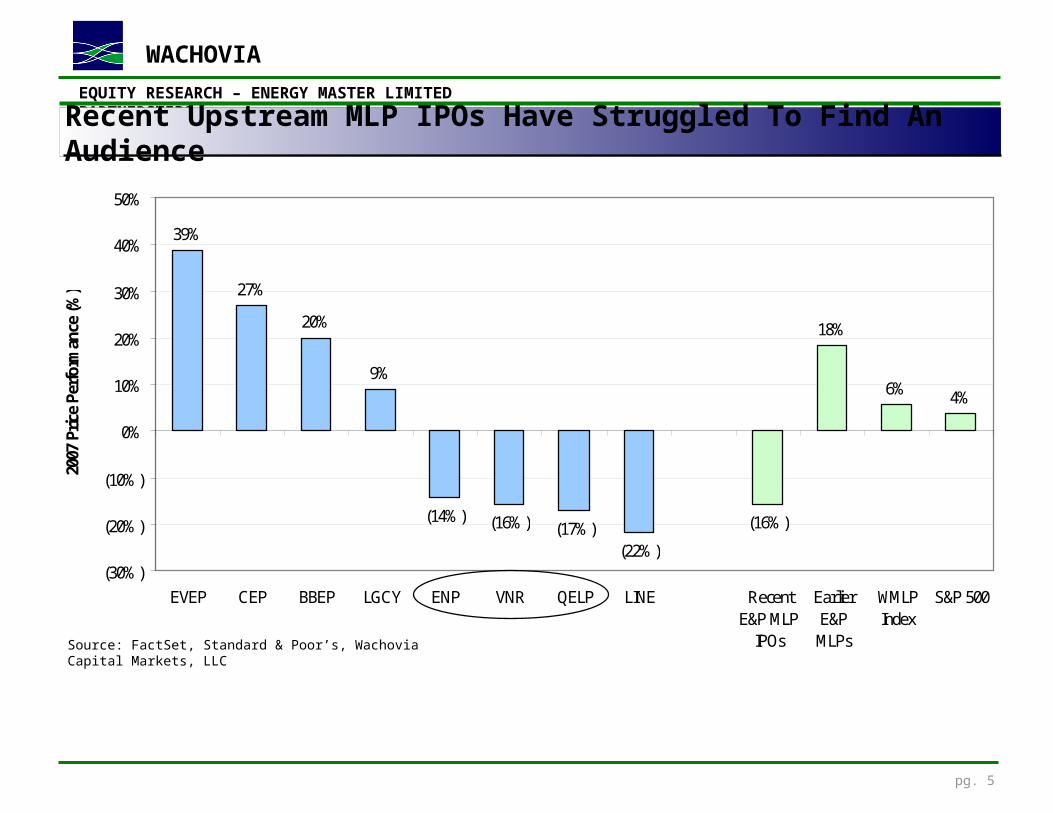

39%

27%

20%

9%

(14% ) (16% ) (17% )(22% )

(16% )

18%

6% 4%

(30% )

(20% )

(10% )

0%

10%

20%

30%

40%

50%

EVEP CEP BBEP LGCY ENP VNR QELP LINE RecentE&P MLP

IPOs

EarlierE&P

MLPs

WMLPIndex

S&P 500

2007

Pric

e Pe

rfor

man

ce (%

)

Recent Upstream MLP IPOs Have Struggled To Find An Audience

Source: FactSet, Standard & Poor’s, Wachovia Capital Markets, LLC

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 6

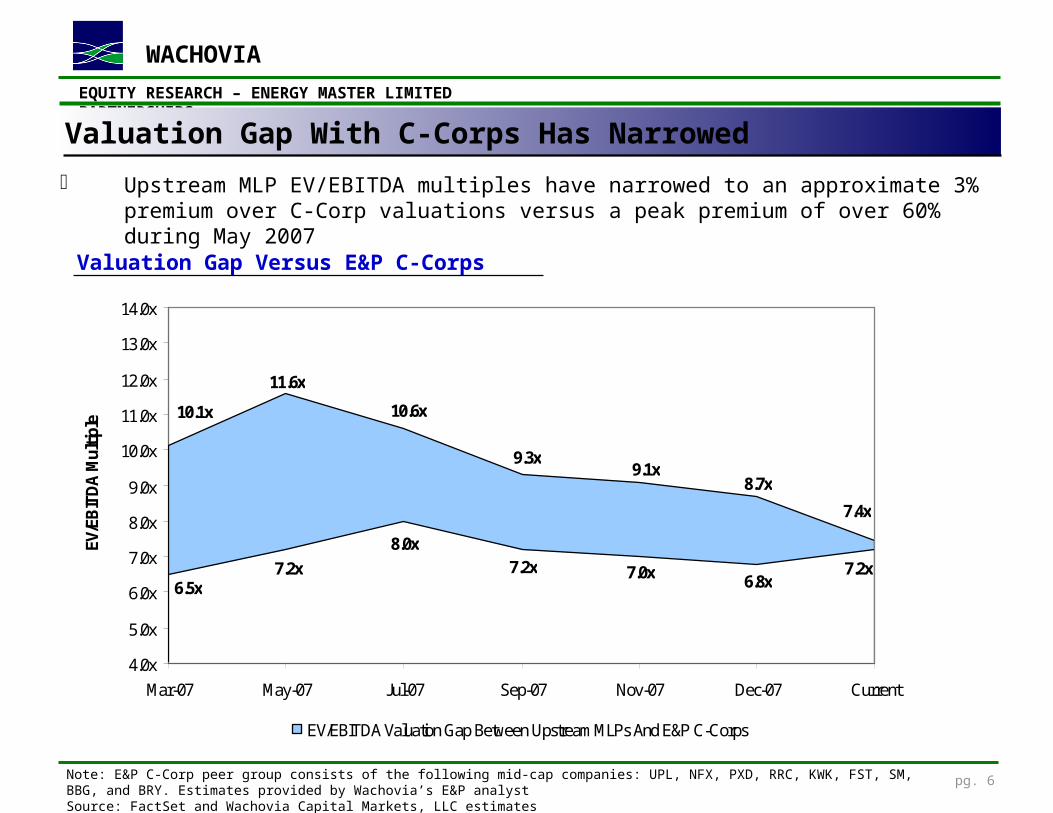

Upstream MLP EV/EBITDA multiples have narrowed to an approximate 3% premium over C-Corp valuations versus a peak premium of over 60% during May 2007

Valuation Gap With C-Corps Has Narrowed

Valuation Gap Versus E&P C-Corps

Note: E&P C-Corp peer group consists of the following mid-cap companies: UPL, NFX, PXD, RRC, KWK, FST, SM, BBG, and BRY. Estimates provided by Wachovia’s E&P analystSource: FactSet and Wachovia Capital Markets, LLC estimates

10.1x

11.6x

10.6x

9.3x9.1x

8.7x

7.4x

6.5x7.2x

8.0x7.2x 7.0x 6.8x

7.2x

4.0x

5.0x

6.0x

7.0x

8.0x

9.0x

10.0x

11.0x

12.0x

13.0x

14.0x

Mar-07 May-07 Jul-07 Sep-07 Nov-07 Dec-07 Current

EV/E

BIT

DA

Mul

tiple

EV/EBITDA Valuation Gap Between Upstream MLPs And E&P C-Corps

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 7

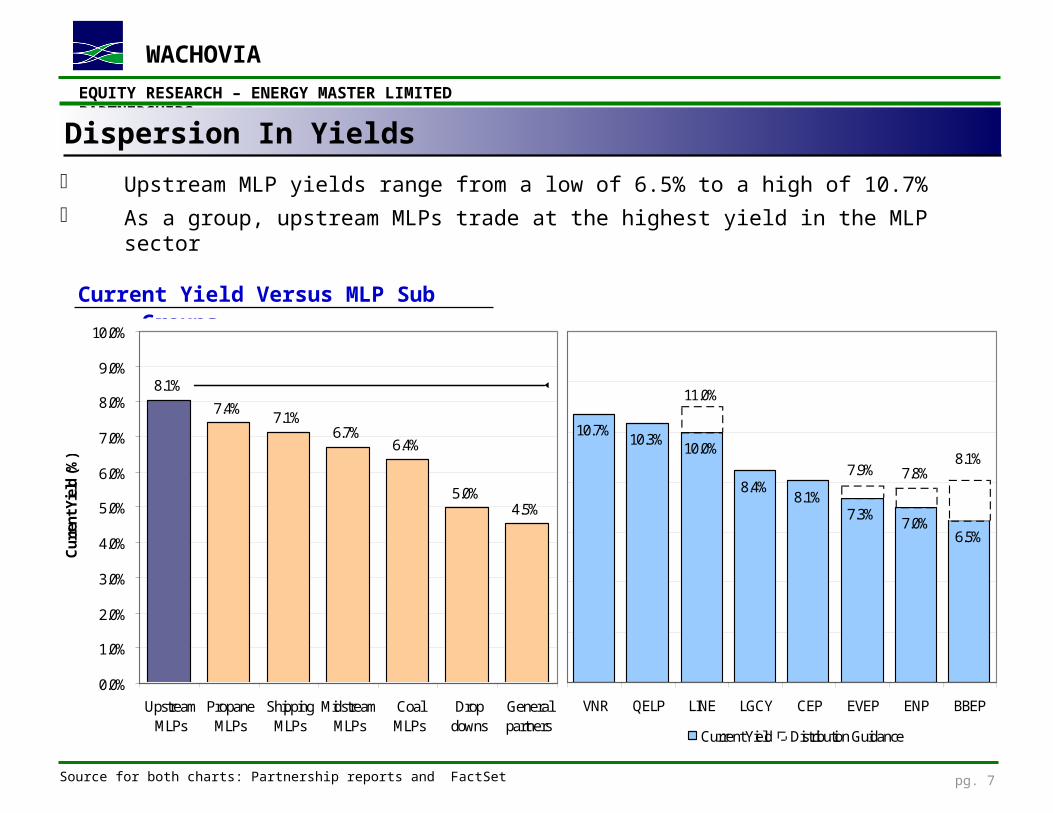

Upstream MLP yields range from a low of 6.5% to a high of 10.7% As a group, upstream MLPs trade at the highest yield in the MLP sector

Dispersion In Yields

Source for both charts: Partnership reports and FactSet

Current Yield Versus MLP Sub Groups

8.1%

7.4%7.1%

6.7%6.4%

5.0%4.5%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

UpstreamMLPs

PropaneMLPs

ShippingMLPs

MidstreamMLPs

CoalMLPs

Dropdowns

Generalpartners

Cur

rent

Yie

ld (%

)

10.7%10.3%

10.0%

8.4%8.1%

7.3%7.0%

6.5%

11.0%

8.1%7.8%7.9%

VNR QELP LINE LGCY CEP EVEP ENP BBEP

Current Yield Distribution Guidance

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 8

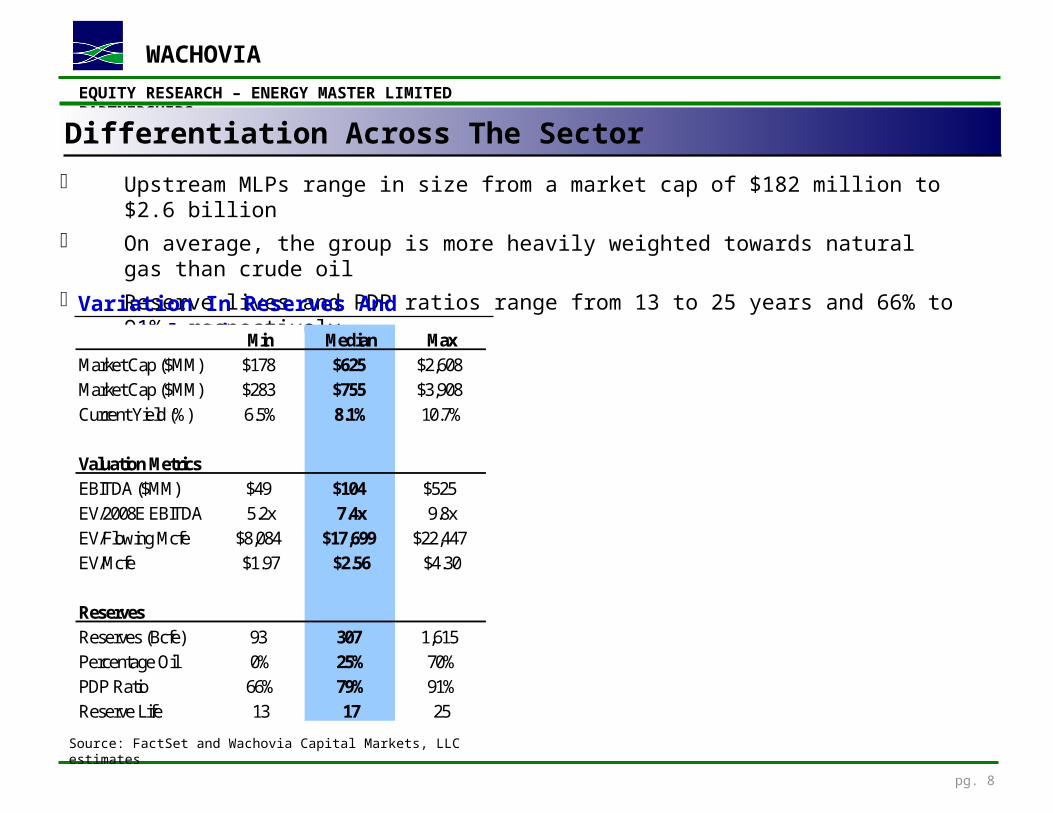

Upstream MLPs range in size from a market cap of $182 million to $2.6 billion On average, the group is more heavily weighted towards natural gas than crude oil Reserve lives and PDP ratios range from 13 to 25 years and 66% to 91%, respectively

Differentiation Across The Sector

Source: FactSet and Wachovia Capital Markets, LLC estimates

Variation In Reserves And ValuationMin Median Max

Market Cap ($MM) $178 $625 $2,608Market Cap ($MM) $283 $755 $3,908Current Yield (%) 6.5% 8.1% 10.7%

Valuation MetricsEBITDA ($MM) $49 $104 $525EV/2008E EBITDA 5.2x 7.4x 9.8xEV/Flowing Mcfe $8,084 $17,699 $22,447EV/Mcfe $1.97 $2.56 $4.30

ReservesReserves (Bcfe) 93 307 1,615Percentage Oil 0% 25% 70%PDP Ratio 66% 79% 91%Reserve Life 13 17 25

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 9

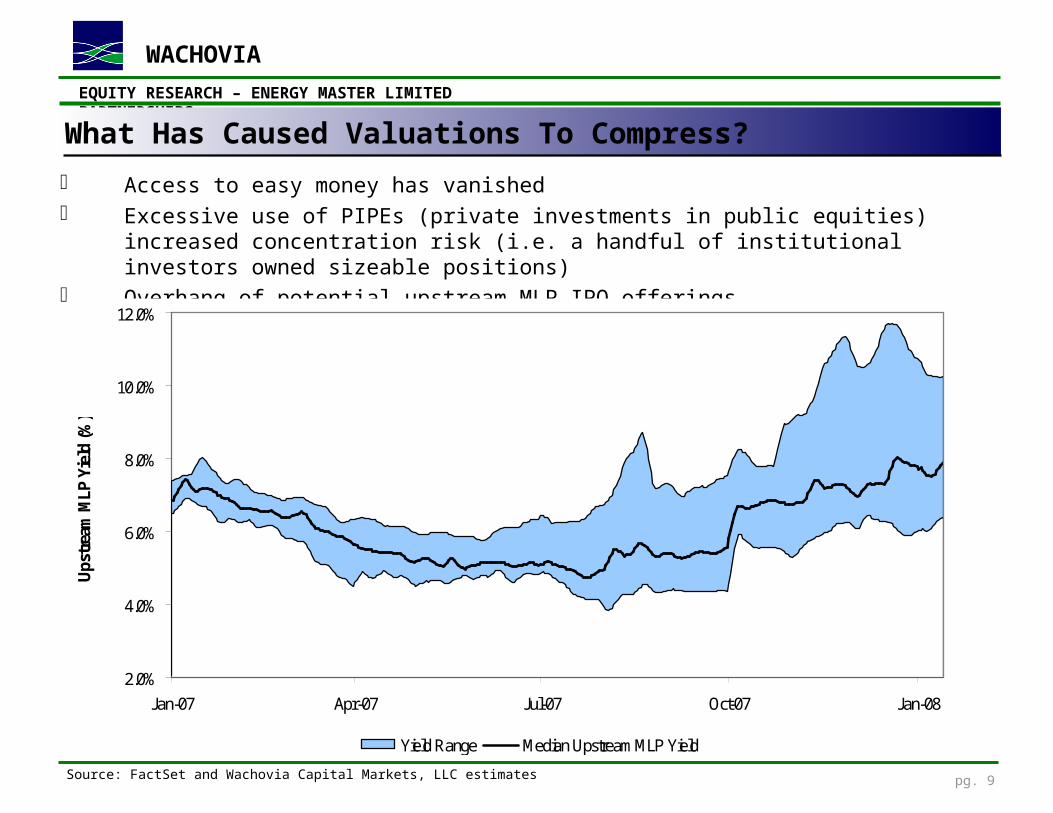

Access to easy money has vanished Excessive use of PIPEs (private investments in public equities) increased concentration risk (i.e. a handful of

institutional investors owned sizeable positions) Overhang of potential upstream MLP IPO offerings

What Has Caused Valuations To Compress?

Source: FactSet and Wachovia Capital Markets, LLC estimates

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08

Ups

trea

m M

LP Y

ield

(%)

Yield Range Median Upstream MLP Yield

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 10

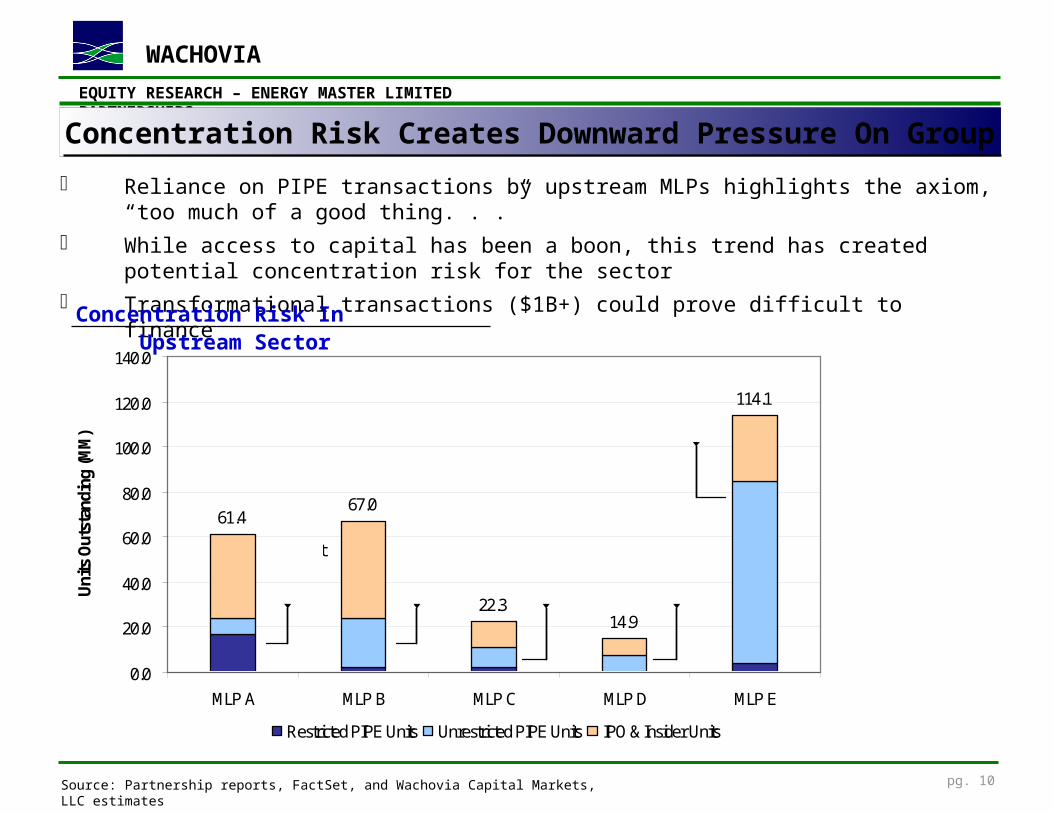

61.467.0

22.314.9

114.1

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

MLP A MLP B MLP C MLP D MLP E

Uni

ts O

utst

andi

ng (M

M)

Restricted PIPE Units Unrestricted PIPE Units IPO & Insider Units

PIPES represent

39% of total units

35% of total units

48% of total units

49% of total units

74% of total units

Concentration Risk Creates Downward Pressure On Group

Reliance on PIPE transactions by upstream MLPs highlights the axiom, “too much of a good thing. . .” While access to capital has been a boon, this trend has created potential concentration risk for the sector Transformational transactions ($1B+) could prove difficult to finance

Source: Partnership reports, FactSet, and Wachovia Capital Markets, LLC estimates

Concentration Risk In Upstream Sector

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 11

Upstream MLPs29%

Midstream50%

Other21%

Source for both charts: Partnership reports

2007 Was A Record Year For Equity Issuances

Equity Offerings By Sector

Historical Equity Offerings

MLPs raised approximately $14.6B of equity in 2007, versus $9.4B in 2006 and $5.6B in 2005 Approximately 59% of the equity raised in 2007 was via PIPE transactions Upstream MLPs raised $4.2B of equity in 2007, of which $3.7B was via PIPE transactions

$1,379$3,028

$8,549

$2,981

$4,598

$5,610

$9,415

$14,558

$3,756

$2,823

$1,259

$2,836

$3,781

$2,972

$0

$2,500

$5,000

$7,500

$10,000

$12,500

$15,000

2004 2005 2006 2007

Gro

ss E

quity

Pro

ceed

s ($

MM

)

IPOs Private Placements Public Secondaries

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 12

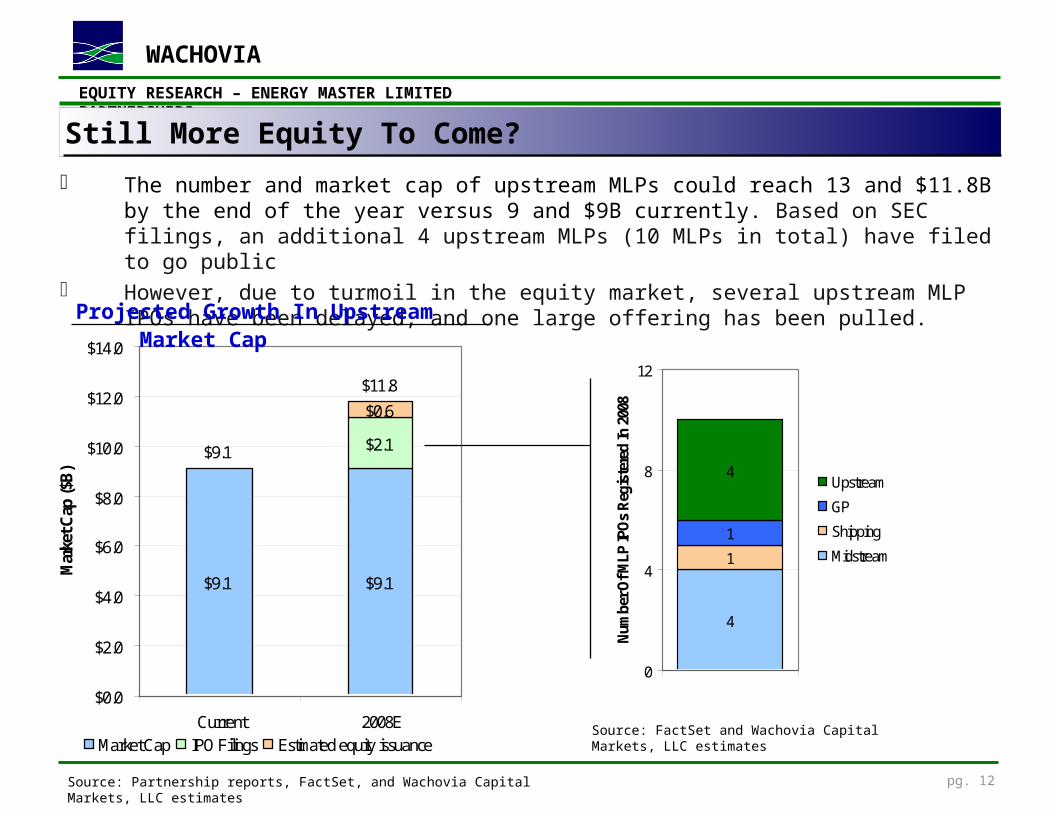

$9.1

$2.1

$0.6

$9.1

$11.8

$9.1

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

Current 2008E

Mar

ket C

ap ($

B)

Market Cap IPO Filings Estimated equity issuance

The number and market cap of upstream MLPs could reach 13 and $11.8B by the end of the year versus 9 and $9B currently. Based on SEC filings, an additional 4 upstream MLPs (10 MLPs in total) have filed to go public

However, due to turmoil in the equity market, several upstream MLP IPOs have been delayed, and one large offering has been pulled.

Still More Equity To Come?

Source: Partnership reports, FactSet, and Wachovia Capital Markets, LLC estimates

Source: FactSet and Wachovia Capital Markets, LLC estimates

Projected Growth In Upstream Market Cap

4

1

1

4

0

4

8

12

Num

ber O

f MLP

IPO

s R

egis

tere

d In

200

8

Upstream

GP

Shipping

Midstream

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 13

$2.3

0

$2.3

6 $2.6

8

$1.4

3

$3.8

0

$1.7

3

$2.4

2

$2.3

2

$2.3

8$2.5

9

$2.1

8 $2.4

4

$1.3

8

$3.4

9

$1.6

8

$2.4

3

$1.7

1

$2.6

1

$2.2

0

$1.7

7

$2.2

5

$1.4

0

$2.2

4

$1.7

2

$2.2

8

$1.6

0

$1.7

0

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

MLP A MLP B MLP C MLP D MLP E MLP F MLP G MLP H MLP I

$ Pe

r Uni

t

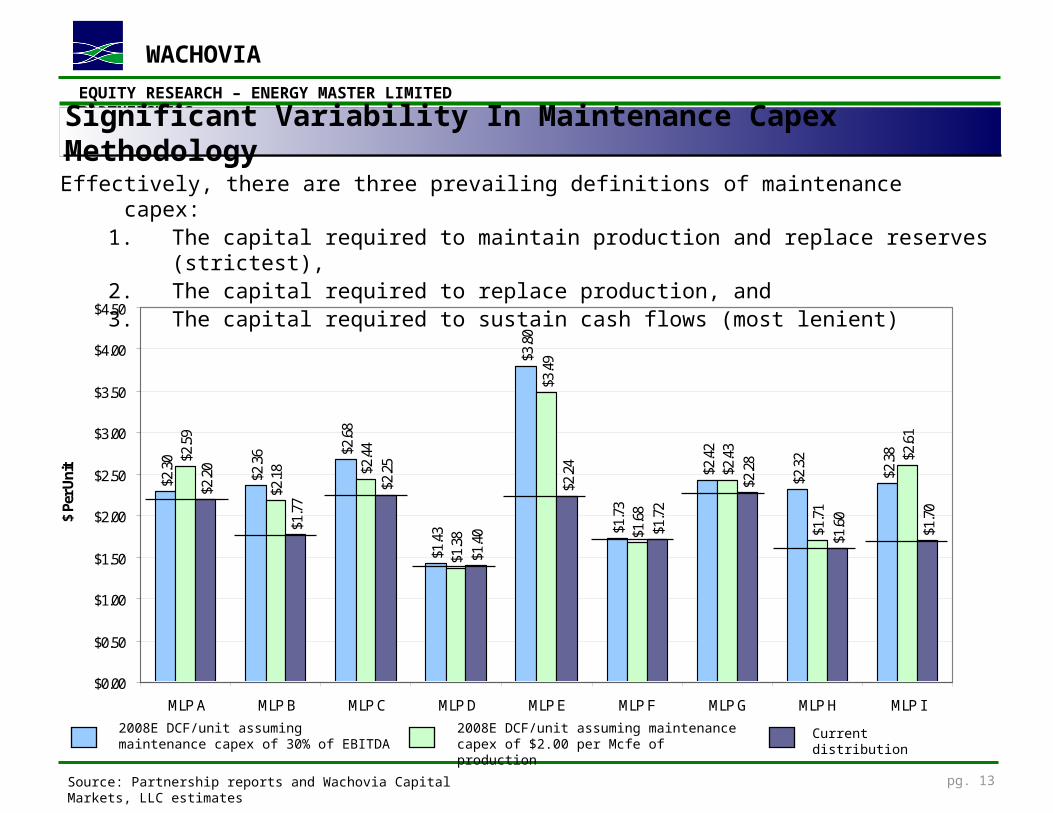

Effectively, there are three prevailing definitions of maintenance capex: 1. The capital required to maintain production and replace reserves (strictest), 2. The capital required to replace production, and 3. The capital required to sustain cash flows (most lenient)

Significant Variability In Maintenance Capex Methodology

Source: Partnership reports and Wachovia Capital Markets, LLC estimates

2008E DCF/unit assuming maintenance capex of 30% of EBITDA

2008E DCF/unit assuming maintenance capex of $2.00 per Mcfe of production

Current distribution

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 14

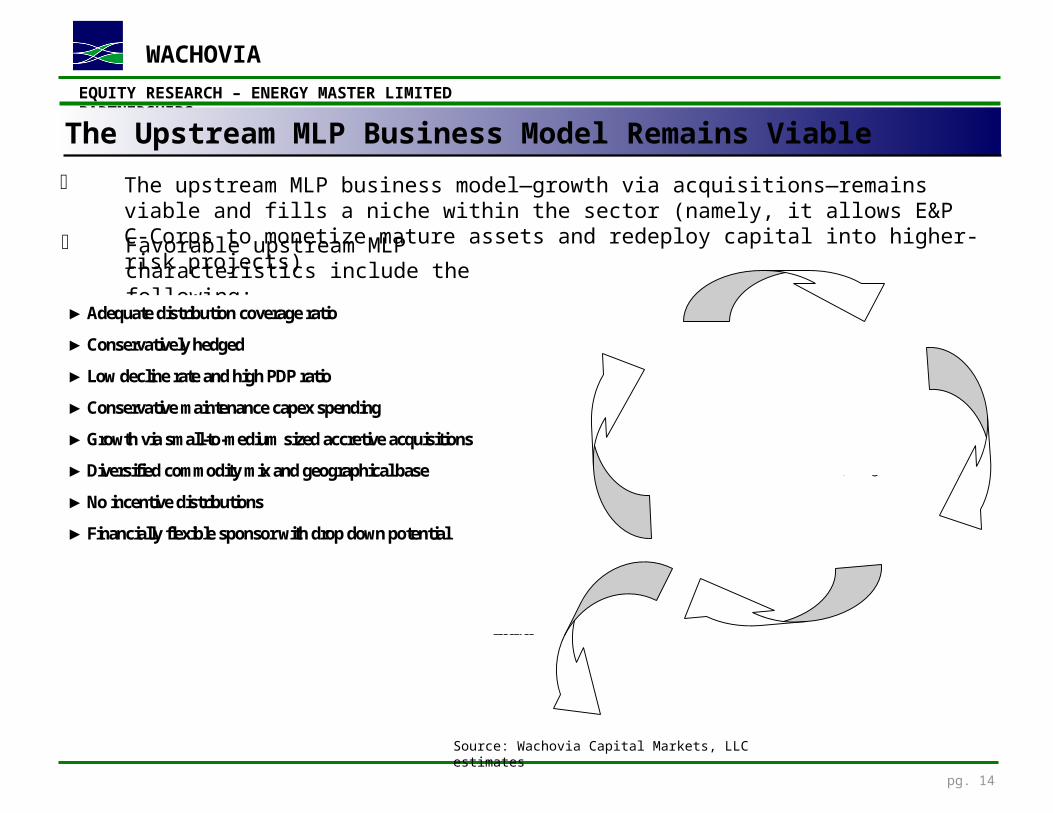

The upstream MLP business model—growth via acquisitions—remains viable and fills a niche within the sector (namely, it allows E&P C-Corps to monetize mature assets and redeploy capital into higher-risk projects)

The Upstream MLP Business Model Remains Viable

Source: Wachovia Capital Markets, LLC estimates

Oil & Gas Company (C-Corp) discovers new

reserves via exploratory drilling

Oil & Gas Company develops reserves and captures higher initial

production and cash flow (and higher decline rates)

Oil & Gas Company sells the mature reserves to an Upstream MLP after production rates have declined to a more manageable

and stable level (5-6%)

Oil & Gas Company redeploys capital

received from MLP

Common unitholders receive distributions

Upstream MLP distributes predictable cash flow to unitholders from proved

developed producing reserves

Favorable upstream MLP characteristics include the following:

►Adequate distribution coverage ratio

►Conservatively hedged

►Low decline rate and high PDP ratio

►Conservative maintenance capex spending

►Growth via small-to-medium sized accretive acquisitions

►Diversified commodity mix and geographical base

►No incentive distributions

►Financially flexible sponsor with drop down potential

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 15

$0

$20

$40

$60

$80

$100

$120

2000 2001 2002 2003 2004 2005 2006 2007 2008

Fron

t Mon

th N

YMEX

Cru

de O

il Pr

ice

($/B

bl)

$0

$2

$4

$6

$8

$10

$12

$14

$16

2000 2001 2002 2003 2004 2005 2006 2007 2008

Fron

t Mon

th N

YMEX

Nat

ural

Gas

Pric

e ($

/Mcf

e)

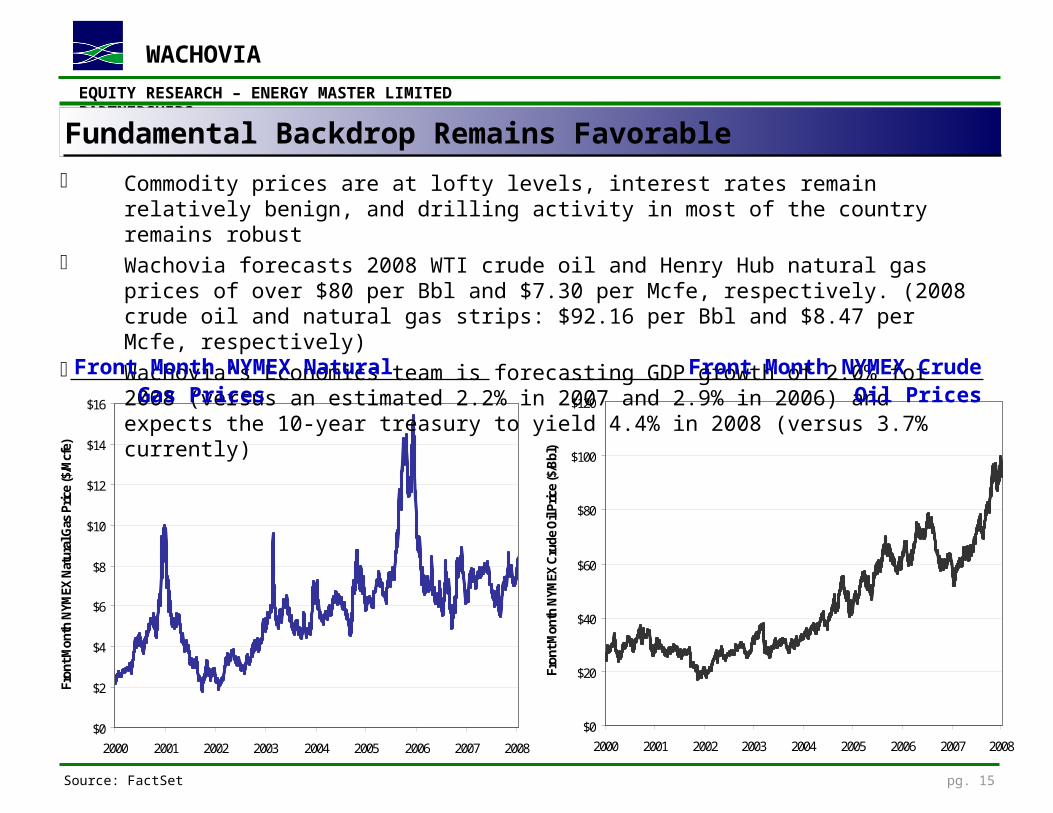

Commodity prices are at lofty levels, interest rates remain relatively benign, and drilling activity in most of the country remains robust

Wachovia forecasts 2008 WTI crude oil and Henry Hub natural gas prices of over $80 per Bbl and $7.30 per Mcfe, respectively. (2008 crude oil and natural gas strips: $92.16 per Bbl and $8.47 per Mcfe, respectively)

Wachovia’s Economics team is forecasting GDP growth of 2.0% for 2008 (versus an estimated 2.2% in 2007 and 2.9% in 2006) and expects the 10-year treasury to yield 4.4% in 2008 (versus 3.7% currently)

Source: FactSet

Fundamental Backdrop Remains Favorable

Front Month NYMEX Natural Gas Prices Front Month NYMEX Crude Oil Prices

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 16

$101

$256$121

$1,521

$2,470

$172

$1,521

$70

$880

$0

$600

$1,200

$1,800

$2,400

$3,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Ups

trea

m M

LP A

cqui

sitio

n Sp

endi

ng, $

MM

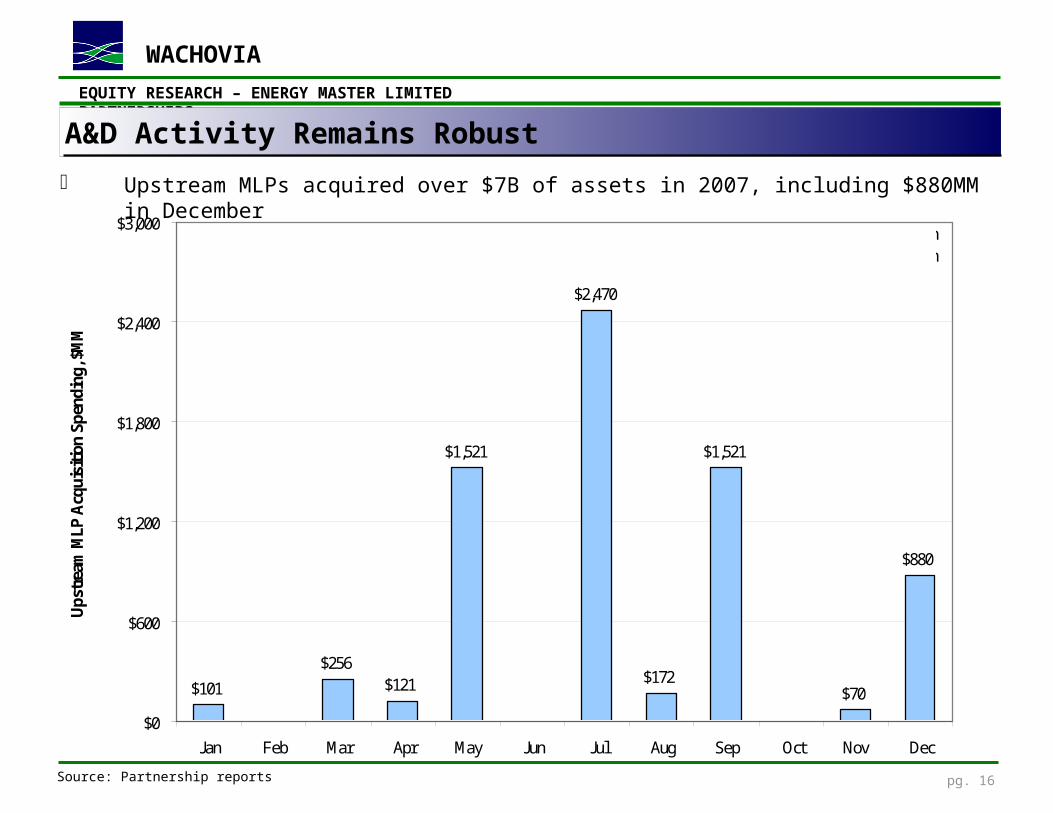

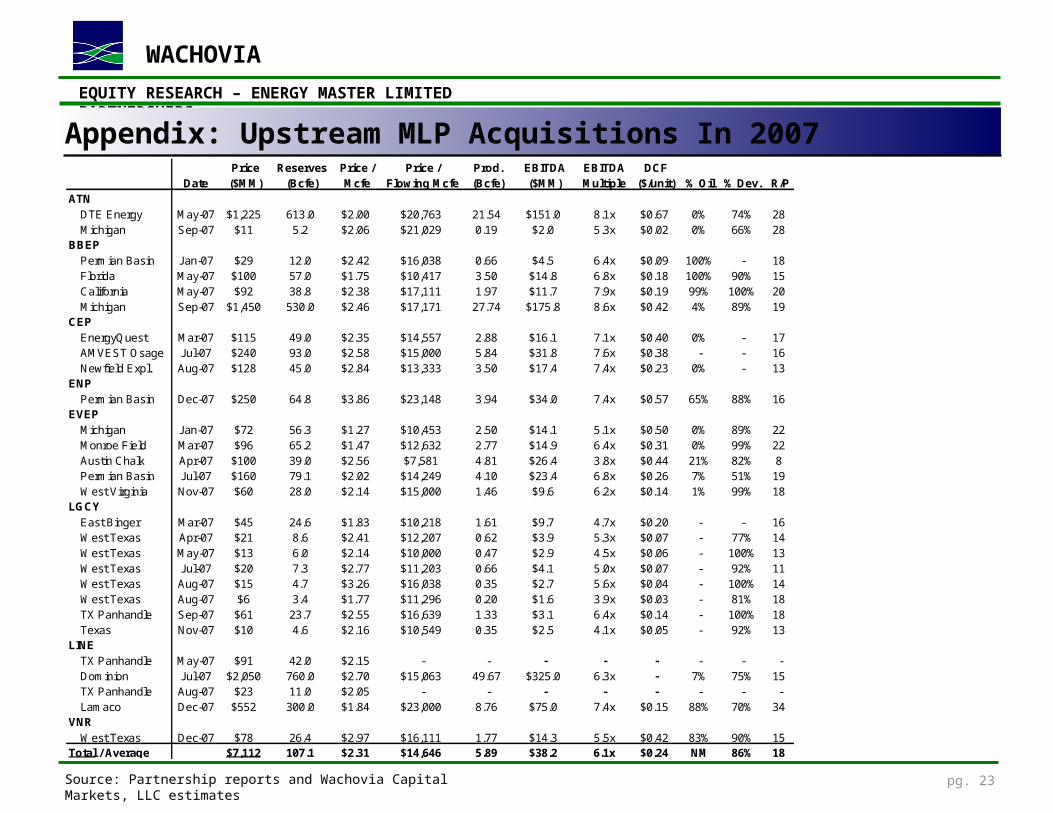

Median size: $84 millionLargest acq: $2.1 billionNo. of transactions: 28Price per Mcfe: $2.31

Upstream MLPs acquired over $7B of assets in 2007, including $880MM in December

A&D Activity Remains Robust

Source: Partnership reports

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 17

$2,602

$603$483

$337$174 $156

$2,757

$1.95

$2.27

$2.58 $2.59

$2.13$2.25

$1.81

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

Antrim Shale Midcontinent West Texas CherokeeBasin

Other TexasPanhandle

Appalachia

Tota

l ($M

M)

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

Ave

rage

Pric

e / M

cfe

Mul

tiple

Total Acquisition Spending (Left Axis) Price / Mcfe (Right Axis)

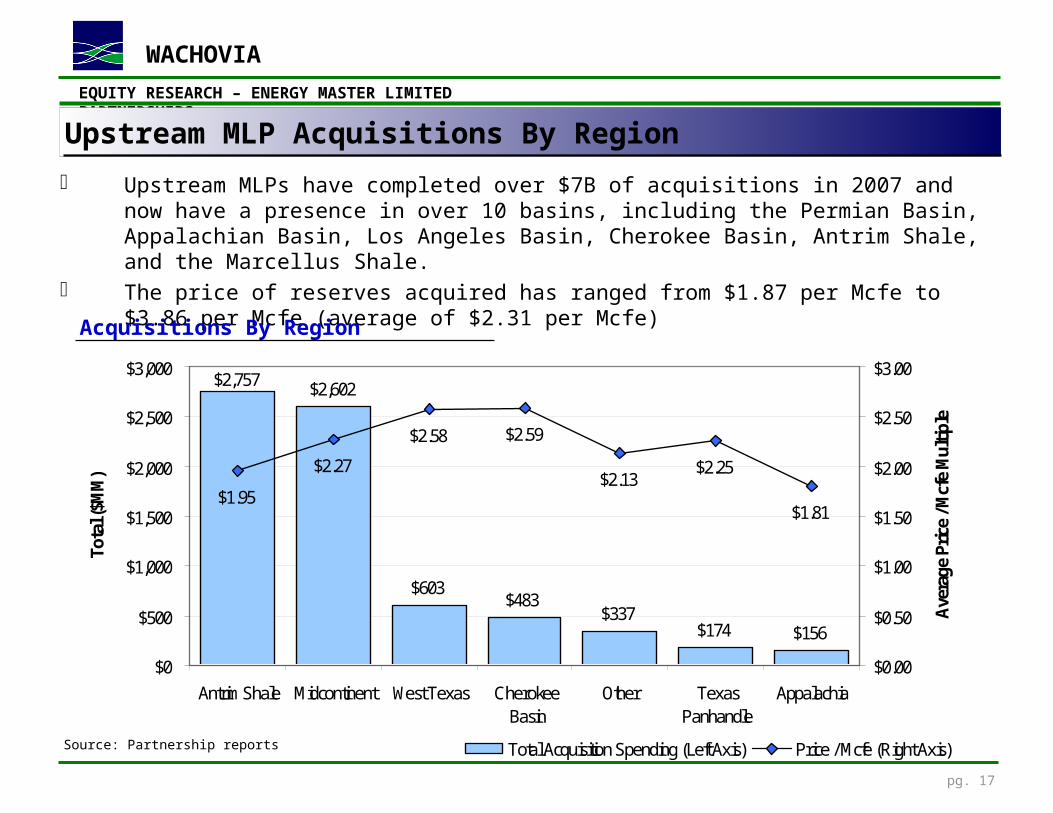

Upstream MLPs have completed over $7B of acquisitions in 2007 and now have a presence in over 10 basins, including the Permian Basin, Appalachian Basin, Los Angeles Basin, Cherokee Basin, Antrim Shale, and the Marcellus Shale.

The price of reserves acquired has ranged from $1.87 per Mcfe to $3.86 per Mcfe (average of $2.31 per Mcfe)

Upstream MLP Acquisitions By Region

Source: Partnership reports

Acquisitions By Region

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 18

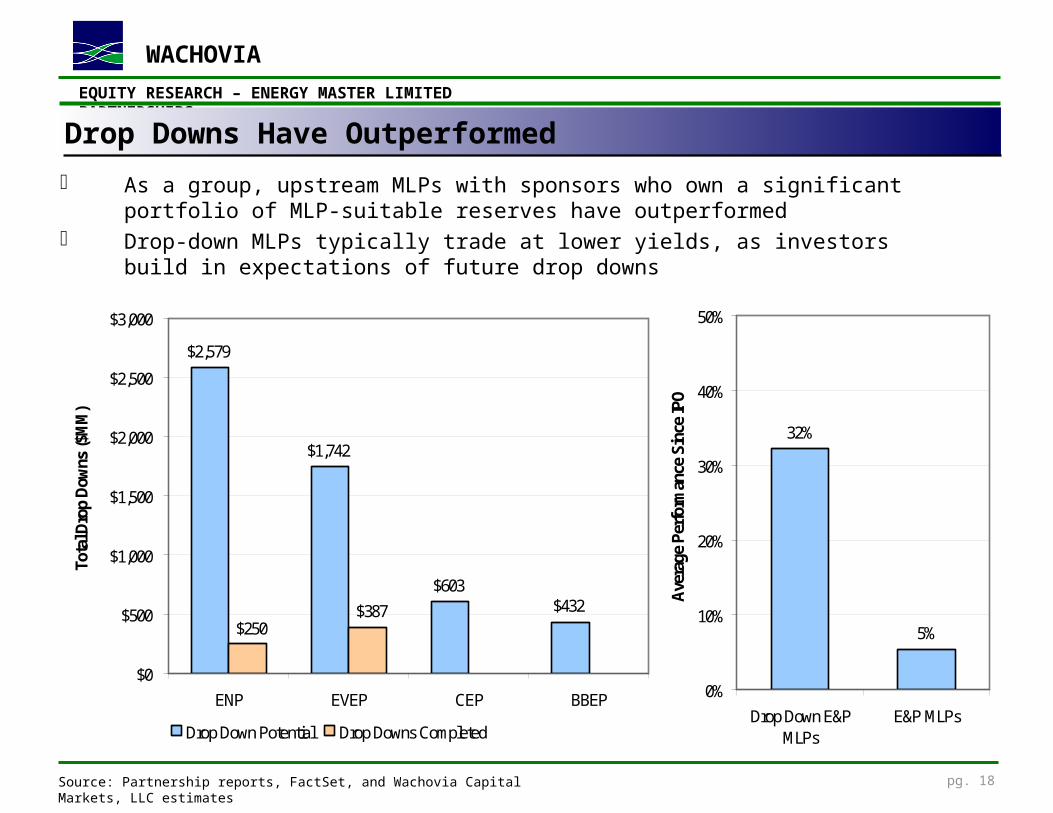

As a group, upstream MLPs with sponsors who own a significant portfolio of MLP-suitable reserves have outperformed

Drop-down MLPs typically trade at lower yields, as investors build in expectations of future drop downs

Drop Downs Have Outperformed

Source: Partnership reports, FactSet, and Wachovia Capital Markets, LLC estimates

$2,579

$1,742

$603$432$387

$250

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

ENP EVEP CEP BBEP

Tota

l Dro

p D

owns

($M

M)

Drop Down Potential Drop Downs Completed

32%

5%

0%

10%

20%

30%

40%

50%

Drop Down E&PMLPs

E&P MLPs

Ave

rage

Per

form

ance

Sin

ce IP

O

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 19

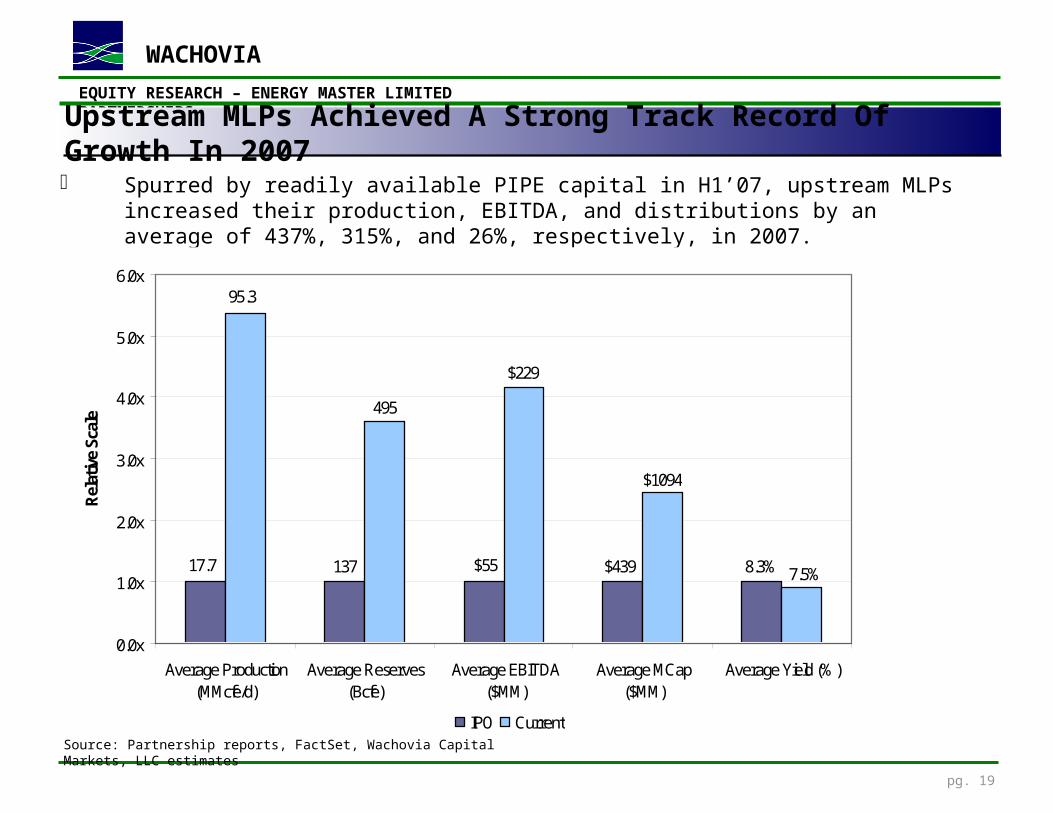

Spurred by readily available PIPE capital in H1’07, upstream MLPs increased their production, EBITDA, and distributions by an average of 437%, 315%, and 26%, respectively, in 2007.

Upstream MLPs Achieved A Strong Track Record Of Growth In 2007

Source: Partnership reports, FactSet, Wachovia Capital Markets, LLC estimates

17.7 $55137 $439 8.3%

95.3

$229

$1094

495

7.5%

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

Average Production(MMcfe/d)

Average Reserves(Bcfe)

Average EBITDA($MM)

Average MCap($MM)

Average Yield (% )

Rel

ativ

e Sc

ale

IPO Current

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 20

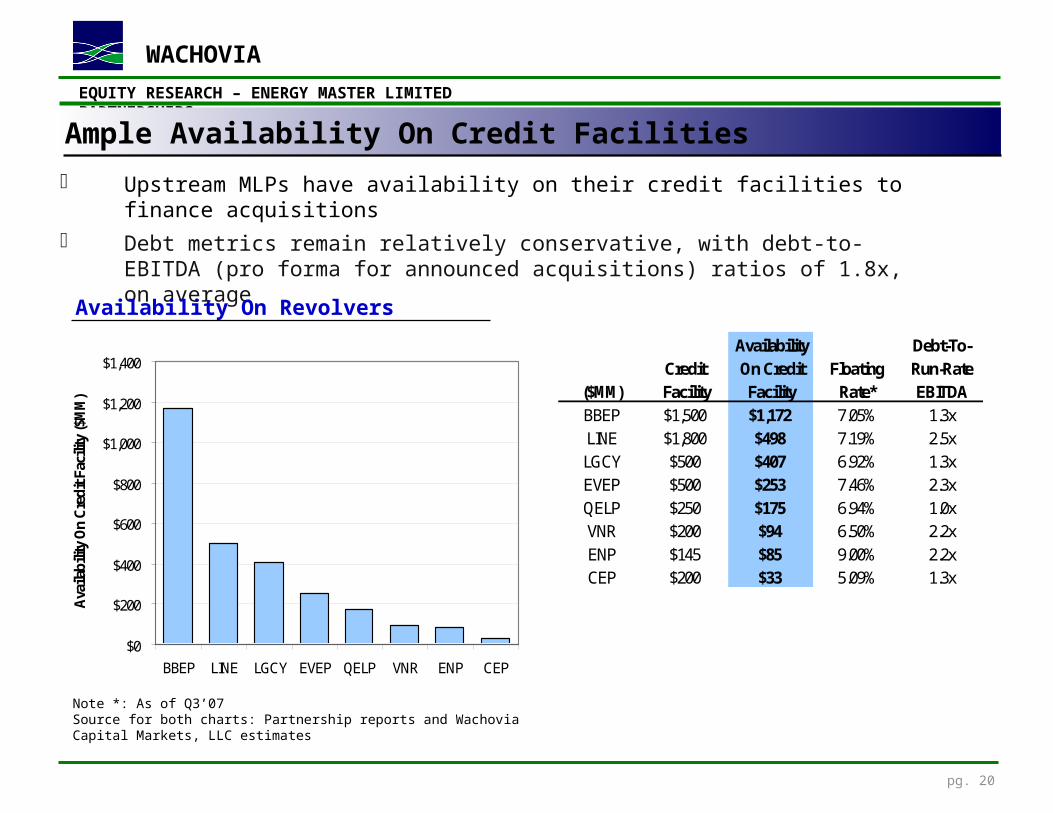

Upstream MLPs have availability on their credit facilities to finance acquisitions Debt metrics remain relatively conservative, with debt-to-EBITDA (pro forma for announced

acquisitions) ratios of 1.8x, on average

Ample Availability On Credit Facilities

Note *: As of Q3’07Source for both charts: Partnership reports and Wachovia Capital Markets, LLC estimates

Availability On Revolvers

Availability Debt-To-Credit On Credit Floating Run-Rate

($MM) Facility Facility Rate* EBITDABBEP $1,500 $1,172 7.05% 1.3xLINE $1,800 $498 7.19% 2.5xLGCY $500 $407 6.92% 1.3xEVEP $500 $253 7.46% 2.3xQELP $250 $175 6.94% 1.0xVNR $200 $94 6.50% 2.2xENP $145 $85 9.00% 2.2xCEP $200 $33 5.09% 1.3x

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

BBEP LINE LGCY EVEP QELP VNR ENP CEP

Ava

ilabi

lity

On

Cre

dit F

acili

ty ($

MM

)

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 21Source: FactSet and Wachovia Capital Markets, LLC estimates

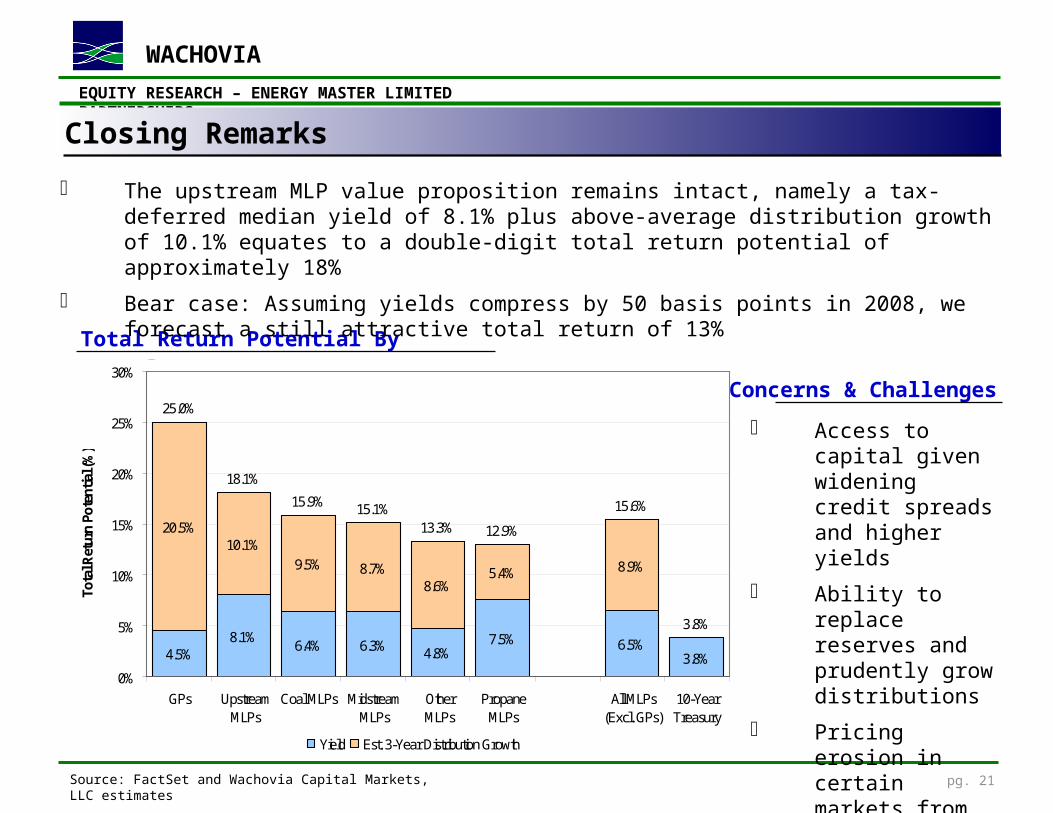

Closing Remarks

Total Return Potential By Sector

Higher Risk

The upstream MLP value proposition remains intact, namely a tax-deferred median yield of 8.1% plus above-average distribution growth of 10.1% equates to a double-digit total return potential of approximately 18%

Bear case: Assuming yields compress by 50 basis points in 2008, we forecast a still attractive total return of 13%

Concerns & Challenges

Access to capital given widening credit spreads and higher yields

Ability to replace reserves and prudently grow distributions

Pricing erosion in certain markets from the start-up of Rockies Express

4.5%8.1%

6.4% 6.3% 4.8%7.5% 6.5%

3.8%

20.5%10.1%

9.5% 8.7%8.6%

5.4% 8.9%

25.0%

18.1%

15.9% 15.1%13.3% 12.9%

15.6%

3.8%

0%

5%

10%

15%

20%

25%

30%

GPs UpstreamMLPs

Coal MLPs MidstreamMLPs

OtherMLPs

PropaneMLPs

All MLPs(Excl. GPs)

10-YearTreasury

Tota

l Ret

urn

Pote

ntia

l (%

)

Yield Est. 3-Year Distribution Growth

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 22

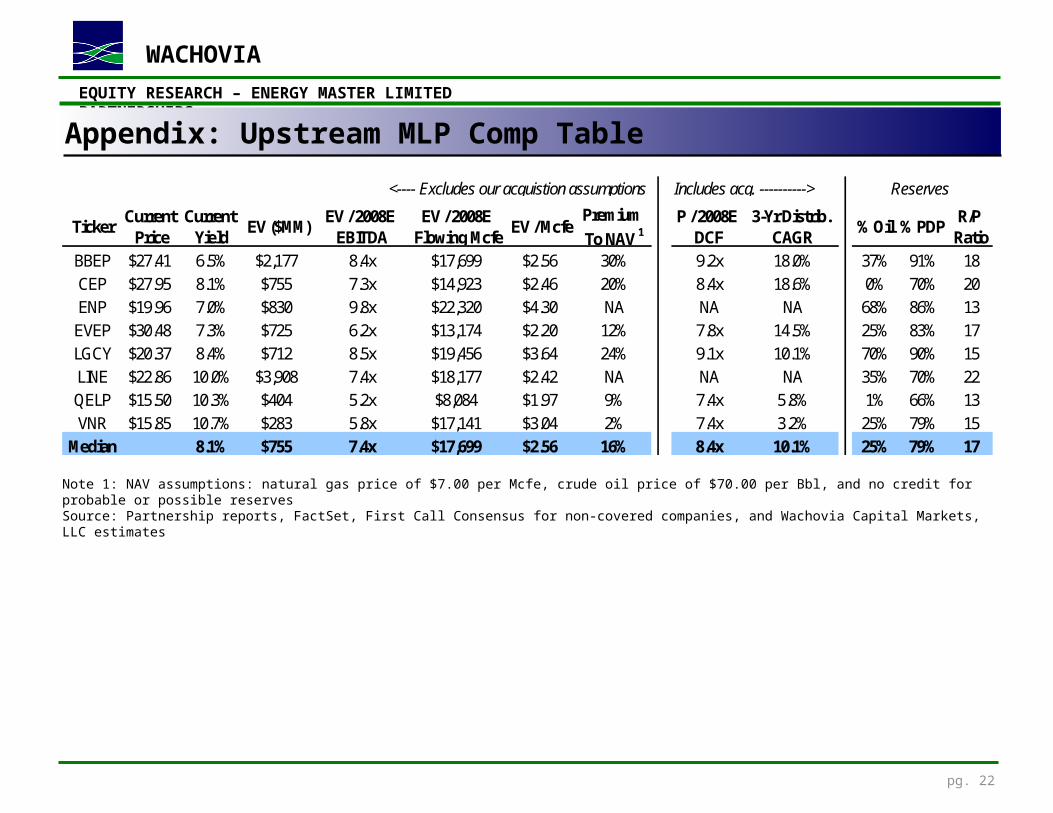

Appendix: Upstream MLP Comp Table

Note 1: NAV assumptions: natural gas price of $7.00 per Mcfe, crude oil price of $70.00 per Bbl, and no credit for probable or possible reservesSource: Partnership reports, FactSet, First Call Consensus for non-covered companies, and Wachovia Capital Markets, LLC estimates

<---- Excludes our acquistion assumptions Includes acq. ----------> Reserves Maintenance capex

TickerCurrent

PriceCurrent

YieldEV ($MM)

EV / 2008E EBITDA

EV / 2008E Flowing Mcfe

EV / McfePremium

To NAV 1P / 2008E

DCF3-Yr Distrib.

CAGR% Oil % PDP

R/P Ratio

BBEP $27.41 6.5% $2,177 8.4x $17,699 $2.56 30% 9.2x 18.0% 37% 91% 18CEP $27.95 8.1% $755 7.3x $14,923 $2.46 20% 8.4x 18.6% 0% 70% 20ENP $19.96 7.0% $830 9.8x $22,320 $4.30 NA NA NA 68% 86% 13

EVEP $30.48 7.3% $725 6.2x $13,174 $2.20 12% 7.8x 14.5% 25% 83% 17LGCY $20.37 8.4% $712 8.5x $19,456 $3.64 24% 9.1x 10.1% 70% 90% 15LINE $22.86 10.0% $3,908 7.4x $18,177 $2.42 NA NA NA 35% 70% 22QELP $15.50 10.3% $404 5.2x $8,084 $1.97 9% 7.4x 5.8% 1% 66% 13VNR $15.85 10.7% $283 5.8x $17,141 $3.04 2% 7.4x 3.2% 25% 79% 15

Median 8.1% $755 7.4x $17,699 $2.56 16% 8.4x 10.1% 25% 79% 17

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 23

Appendix: Upstream MLP Acquisitions In 2007

Source: Partnership reports and Wachovia Capital Markets, LLC estimates

Price Reserves Price / Price / Prod. EBITDA EBITDA DCFDate ($MM) (Bcfe) Mcfe Flowing Mcfe (Bcfe) ($MM) Multiple ($/unit) % Oil % Dev. R/P

ATNDTE Energy May-07 $1,225 613.0 $2.00 $20,763 21.54 $151.0 8.1x $0.67 0% 74% 28Michigan Sep-07 $11 5.2 $2.06 $21,029 0.19 $2.0 5.3x $0.02 0% 66% 28

BBEPPermian Basin Jan-07 $29 12.0 $2.42 $16,038 0.66 $4.5 6.4x $0.09 100% - 18Florida May-07 $100 57.0 $1.75 $10,417 3.50 $14.8 6.8x $0.18 100% 90% 15California May-07 $92 38.8 $2.38 $17,111 1.97 $11.7 7.9x $0.19 99% 100% 20Michigan Sep-07 $1,450 530.0 $2.46 $17,171 27.74 $175.8 8.6x $0.42 4% 89% 19

CEPEnergyQuest Mar-07 $115 49.0 $2.35 $14,557 2.88 $16.1 7.1x $0.40 0% - 17AMVEST Osage Jul-07 $240 93.0 $2.58 $15,000 5.84 $31.8 7.6x $0.38 - - 16Newfield Expl. Aug-07 $128 45.0 $2.84 $13,333 3.50 $17.4 7.4x $0.23 0% - 13

ENPPermian Basin Dec-07 $250 64.8 $3.86 $23,148 3.94 $34.0 7.4x $0.57 65% 88% 16

EVEPMichigan Jan-07 $72 56.3 $1.27 $10,453 2.50 $14.1 5.1x $0.50 0% 89% 22Monroe Field Mar-07 $96 65.2 $1.47 $12,632 2.77 $14.9 6.4x $0.31 0% 99% 22Austin Chalk Apr-07 $100 39.0 $2.56 $7,581 4.81 $26.4 3.8x $0.44 21% 82% 8Permian Basin Jul-07 $160 79.1 $2.02 $14,249 4.10 $23.4 6.8x $0.26 7% 51% 19West Virginia Nov-07 $60 28.0 $2.14 $15,000 1.46 $9.6 6.2x $0.14 1% 99% 18

LGCYEast Binger Mar-07 $45 24.6 $1.83 $10,218 1.61 $9.7 4.7x $0.20 - - 16West Texas Apr-07 $21 8.6 $2.41 $12,207 0.62 $3.9 5.3x $0.07 - 77% 14West Texas May-07 $13 6.0 $2.14 $10,000 0.47 $2.9 4.5x $0.06 - 100% 13West Texas Jul-07 $20 7.3 $2.77 $11,203 0.66 $4.1 5.0x $0.07 - 92% 11West Texas Aug-07 $15 4.7 $3.26 $16,038 0.35 $2.7 5.6x $0.04 - 100% 14West Texas Aug-07 $6 3.4 $1.77 $11,296 0.20 $1.6 3.9x $0.03 - 81% 18TX Panhandle Sep-07 $61 23.7 $2.55 $16,639 1.33 $3.1 6.4x $0.14 - 100% 18Texas Nov-07 $10 4.6 $2.16 $10,549 0.35 $2.5 4.1x $0.05 - 92% 13

LINETX Panhandle May-07 $91 42.0 $2.15 - - - - - - - -Dominion Jul-07 $2,050 760.0 $2.70 $15,063 49.67 $325.0 6.3x - 7% 75% 15TX Panhandle Aug-07 $23 11.0 $2.05 - - - - - - - -Lamaco Dec-07 $552 300.0 $1.84 $23,000 8.76 $75.0 7.4x $0.15 88% 70% 34

VNRWest Texas Dec-07 $78 26.4 $2.97 $16,111 1.77 $14.3 5.5x $0.42 83% 90% 15

Total / Average $7,112 107.1 $2.31 $14,646 5.89 $38.2 6.1x $0.24 NM 86% 18

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 24

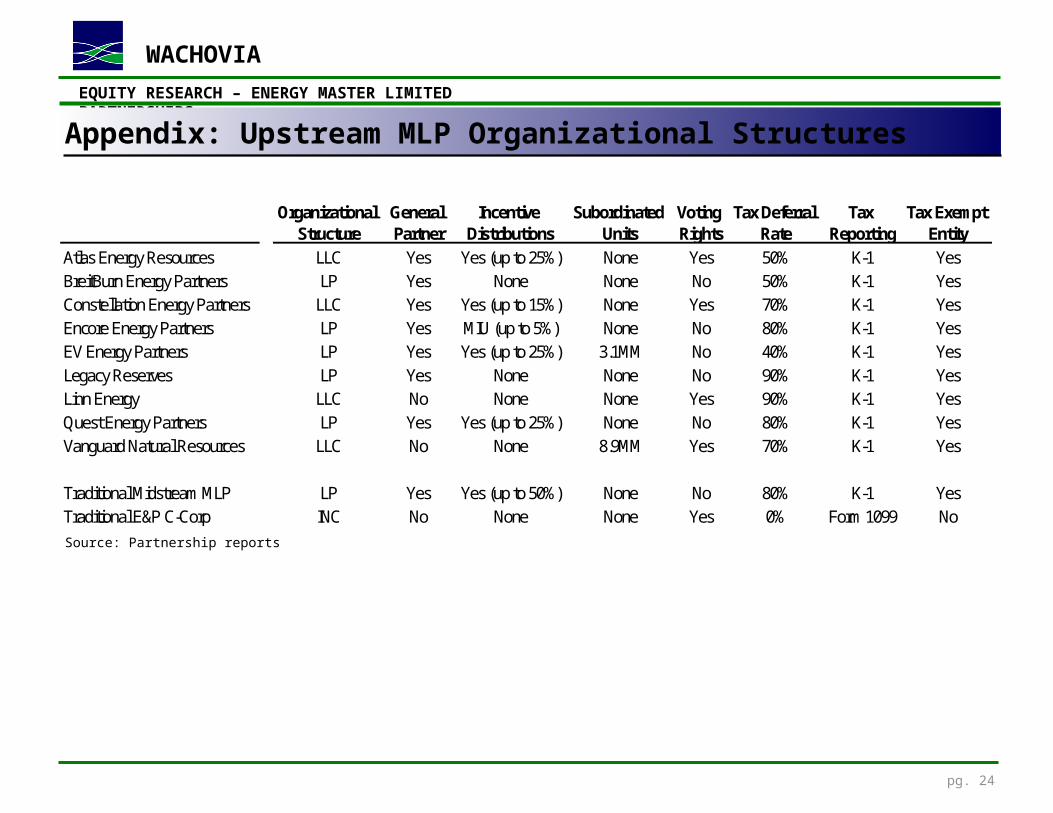

Appendix: Upstream MLP Organizational Structures

Source: Partnership reports

Organizational Structure

General Partner

Incentive Distributions

Subordinated Units

Voting Rights

Tax Deferral Rate

Tax Reporting

Tax Exempt Entity

Atlas Energy Resources LLC Yes Yes (up to 25%) None Yes 50% K-1 YesBreitBurn Energy Partners LP Yes None None No 50% K-1 YesConstellation Energy Partners LLC Yes Yes (up to 15%) None Yes 70% K-1 YesEncore Energy Partners LP Yes MIU (up to 5%) None No 80% K-1 YesEV Energy Partners LP Yes Yes (up to 25%) 3.1MM No 40% K-1 YesLegacy Reserves LP Yes None None No 90% K-1 YesLinn Energy LLC No None None Yes 90% K-1 YesQuest Energy Partners LP Yes Yes (up to 25%) None No 80% K-1 YesVanguard Natural Resources LLC No None 8.9MM Yes 70% K-1 Yes

Traditional Midstream MLP LP Yes Yes (up to 50%) None No 80% K-1 YesTraditional E&P C-Corp INC No None None Yes 0% Form 1099 No

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 25

To view price charts for all companies rated in this document, please go to www.wachoviaresearch.com or write to 7 Saint Paul Street, 1st Floor, MD5202, Baltimore, MD 21202

ATTN: Research Publications Additional Information Available Upon Request

I certify that:1) All views expressed in this research report accurately reflect my personal views about any and all of the subject securities or issuers discussed; and

2) No part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by me in this research report.

Wachovia Capital Markets, LLC maintains a market in the common stock of BreitBurn Energy Partners L.P., EV Energy Partners, L.P., Legacy Reserves, L.P., Quest Energy Partners, L.P.Wachovia Capital Markets, LLC or its affiliates managed or comanaged a public offering of securities for Legacy Reserves, L.P., Quest Energy Partners, L.P., Vanguard Natural Resources, LLC within the past 12 months.Wachovia Capital Markets, LLC or its affiliates intends to seek or expects to receive compensation for investment banking services in the next three months from BreitBurn Energy Partners L.P., Constellation Energy Partners LLC, EV Energy Partners, L.P., Legacy Reserves, L.P., Quest Energy Partners, L.P., Vanguard Natural Resources, LLC.Wachovia Capital Markets, LLC or its affiliates received compensation for investment banking services from BreitBurn Energy Partners L.P., Constellation Energy Partners LLC, EV Energy Partners, L.P., Legacy Reserves, L.P., Quest Energy Partners, L.P., Vanguard Natural Resources, LLC in the past 12 months.Wachovia Capital Markets, LLC and/or its affiliates, have beneficial ownership of 1% or more of any class of the common stock of BreitBurn Energy Partners L.P.BreitBurn Energy Partners L.P., Constellation Energy Partners LLC, EV Energy Partners, L.P., Legacy Reserves, L.P., Quest Energy Partners, L.P., Vanguard Natural Resources, LLC currently is, or during the 12-month period preceding the date of distribution of the research report was, a client of Wachovia Capital Markets, LLC. Wachovia Capital Markets, LLC provided investment banking services to BreitBurn Energy Partners L.P., Constellation Energy Partners LLC, EV Energy Partners, L.P., Legacy Reserves, L.P., Quest Energy Partners, L.P., Vanguard Natural Resources, LLC.Wachovia Capital Markets, LLC received compensation for products or services other than investment banking services from Quest Energy Partners, L.P. in the past 12 months.

Wachovia Capital Markets, LLC does not compensate its research analysts based on specific investment banking transactions. WCM’s research analysts receive compensation that is based upon and impacted by the overall profitability and revenue of the firm, which includes, but is not limited to investment banking revenue.STOCK RATING1 = Outperform: The stock appears attractively valued, and we believe the stock's total return will exceed that of the market over the next 12 months. BUY2 = Market Perform: The stock appears appropriately valued, and we believe the stock's total return will be in line with the market over the next 12 months. HOLD3 = Underperform: The stock appears overvalued, and we believe the stock's total return will be below the market over the next 12 months. SELLSECTOR RATINGO = Overweight: Industry expected to outperform the relevant broad market benchmark over the next 12 months.M = Market Weight: Industry expected to perform in-line with the relevant broad market benchmark over the next 12 months.U = Underweight: Industry expected to underperform the relevant broad market benchmark over the next 12 months.VOLATILITY RATINGV = A stock is defined as volatile if the stock price has fluctuated by +/-20% or greater in at least 8 of the past 24 months or if the analyst expects significant volatility. All IPO stocks are automatically rated volatile within the first 24 months of trading.As of: January 15, 2008

47% of companies covered by Wachovia Equity Research are rated Outperform. Wachovia Capital Markets, LLC has provided investment banking services for 40% of its Equity Research Outperform-rated companies.52% of companies covered by Wachovia Equity Research are rated Market Perform. Wachovia Capital Markets, LLC has provided investment banking services for 32% of its Equity Research Market Perform-rated companies.2% of companies covered by Wachovia Equity Research are rated Underperform. Wachovia Capital Markets, LLC has provided investment banking services for 21% of its Equity Research Underperform-rated companies.

EQUITY RESEARCH – ENERGY MASTER LIMITED PARTNERSHIPS

WACHOVIA

pg. 26

Additional Disclosures For International Clients

For additional disclosure information please go to: www.wachoviaresearch.comThe securities and related financial instruments described herein may not be eligible for sale in all jurisdictions or to certain categories of investors. For certain non-U.S. institutional readers (including readers in the EEA), this report is distributed by Wachovia Securities International Limited. For the purposes of Section 21 of the U.K. Financial Services and Markets Act 2000, this report has been approved by Wachovia Securities International Limited. This research is not intended for, and should not be relied on by, private customers. Please consult your Financial Advisor or the Wachovia Securities office in your area for additional information. U.S. residents are directed to wachovia.com for investment and related services.

For Wachovia Securities International Limited's policy for managing conflicts of interest in connection with research, please go to: www.wachoviaresearch.com/conflicts

Important Information for Japanese RecipientsThis material is distributed in Japan by Wachovia Securities (Japan) Co., Ltd., a foreign securities company registered with the Financial Services Agency in Japan.

Important Information for Australian RecipientsWachovia Capital Markets, LLC ("WCM”) is exempt from the requirements to hold an Australian financial services license in respect of the financial services it provides to wholesale clients in Australia. WCM is a registered broker-dealer registered with the U.S. Securities and Exchange Commission, and a member of the New York Stock Exchange, the National Association of Securities Dealers, Inc. and the Securities Investor Protection Corp. WCM is regulated under U.S. laws which differ from Australian laws. Any offer or documentation provided to you by WCM in the course of providing the financial services will be prepared in accordance with the laws of the United States and not Australian laws.

Additional DisclosuresWCM is a U.S. broker-dealer registered with the U.S. Securities and Exchange Commission and a member of the New York Stock Exchange, the National Association of Securities Dealers, Inc., and the Securities Investor Protection Corp. Wachovia Securities International Limited is a U.K. incorporated investment firm authorized and regulated by the Financial Services Authority.

This report is for your information only and is not an offer to sell, or a solicitation of an offer to buy, the securities or instruments named or described in this report. Interested parties are advised to contact the entity with which they deal, or the entity that provided this report to them, if they desire further information. The information in this report has been obtained or derived from sources believed by Wachovia Capital Markets, LLC, to be reliable, but Wachovia Capital Markets, LLC, does not represent that this information is accurate or complete. Any opinions or estimates contained in this report represent the judgement of Wachovia Capital Markets, LLC, at this time, and are subject to change without notice. Wachovia Capital Markets, LLC, and its affiliates may from time to time provide advice with respect to, acquire, hold, or sell a position in, the securities or instruments named or described in this report. For the purposes of the U.K. Financial Services Authority's rules, this report constitutes impartial investment research. Each of Wachovia Capital Markets, LLC, and Wachovia Securities International Limited is a separate legal entity and distinct from affiliated banks. Copyright © 2008 Wachovia Capital Markets, LLC.

SECURITIES: NOT FDIC-INSURED/NOT BANK-GUARANTEED/MAY LOSE VALUE