Major and Minor Music Compared to Excited and Subdued Speech (2009)

Equity & Debt Strategy

Mid July – August’ 2019

Equity Market Update &

Equity MF Strategy

Confidential | 3

Equity Strategy - Highlights of the month

Exhibit 1: India has significantly under-performed global markets

in June and post budget in July

Exhibit 2: Declining bond yields has made relative valuations of

equities slightly less expensive

Nifty earnings yield = 1 / Nifty Fwd PE

Source: Bloomberg; All data are as of 22nd July 2019

Exhibit 1:-• Indian markets have reversed their CYTD out-performance in the month of June

and post the budget in July. Some of the uncertainty regarding FPI taxationseems to have spooked market participants.

• Commentary from some companies which have declared results so far have notbeen very strong either and has raised concerns on the strength of the earningsrecovery. Midcap stocks have continued to under-perform large caps.

• While the domestic weakness could continue for the next two quarters orlonger, the fact that these realities are getting reflected in stock prices makesthe current market conditions less risky. In contrast, prior to elections marketswere largely ignoring signs of a slowdown and expecting ample liquidity andstimulus to support prices.

Exhibit 2:-• The gap between 10 Yr. Govt. Bond Yield & Nifty Earnings Yield has

declined from the peak of ~2.7% during Sept’2018 to ~0.7% currently –which is lowest level since June 2017. A major part of the currentnarrowing of the gap has happened post budget announcement due todecline in 10 Yr. Govt. Bond Yield.

• The yield gap was negative during July’05-Feb’06, Sep’08-May’09, May’13-June’13 & Nov’16-Dec’16 all of which were very lucrative entry points forequities – the last two being a very short window.

• A high yield gap indicates that an equity investor is relatively better offearning risk-free returns than taking equity risk. While the gap is not yetnegative which would indicate extreme pessimism, the current level doesnot indicate a dangerous euphoria either.

-6

-4

-2

0

2

4

0.00

3.00

6.00

9.00

12.00

15.00Yield Gap (%) Nifty Earnings Yield % 10 Yr Govt. Bond Yield %

8.2%

5.4%

4.0%4.9%

7.7%

2.6%

0.3%

6.7%

1.0%

-4.3%

-0.4%

3.6%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%Market performance from 1st Jun to 22nd Jul 2019

Confidential | 4

Equity Strategy - Highlights of the month

Exhibit 4: While midcaps have outperformed large-caps over the

long term, they are prone to cycles of out / under-performance

Exhibit 3: The Nifty stocks which have outperformed in the last 1 year

have also seen a sharp correction post Budget (except RIL)

Exhibit 4:-• Markets have seen a series of controlled explosions in individual companies

due to issues ranging from auditor resignations to panics caused bypledged shares. Some mid-caps have seen severe price reactions toquarterly results which were below market estimates.

• Over the last month, the weak sentiment in large-caps have affected mid-caps even more, creating opportunity for bottom-up stock pickers. Theimmediate effect though has been significant price erosions acrossportfolios. As market participants recover and re-asses their investmentthesis, selective buying should emerge.

• We see this is a natural progression of the third mid-cap cycle in the last~15 years. Extreme apathy for mid & small-cap stocks in late 2013 set thestage for a strong bull market. However, the timing is always hard to call.

Exhibit 3:-• The leaders of the recent past saw a sell-off post the budget. The high

valuations came off a bit and the earnings outlook for some of thesecompanies have also weakened given the muted commentary on quarterlyresults.

• Financials have corrected post commentary by some banks like RBL Bank, DCBBank & HDFC Bank and Bajaj Finance. The managements struck a cautiousnote and highlighted risks in some segments of their loan book. Markets arealso now expecting a moderation in Bajaj Finance’s growth momentum.

• With the recent price correction in these stocks and weak performance ofstocks like Page Industries, Eicher Motors, & Maruti for quite some time now,many stocks are beginning to reflect lower earnings expectations, if not lowvaluations.

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50 3 year returns of Nifty Midcap 100 / 3 year returns of Nifty 100

Apr-09, Aug-13, 0.77

Oct-16, 1.46

July-19, 0.85

Source: Bloomberg; All data are as of 22nd July 2019

-5.8%

-14.1%

-3.8%

-9.7%

-16.4%

-2.5%

-5.6%

-15.3%

0.0%

-9.8%

-18.0%

-15.0%

-12.0%

-9.0%

-6.0%

-3.0%

0.0%

ICIC

I Ban

k

Baj

aj F

inan

ce

UP

L

Axi

s B

ank

Tita

n

Wip

ro

Stat

e B

ank

of

Ind

ia

Baj

aj F

inse

rv

Rel

ian

ceIn

du

stri

es

L&T

Performance during 5th July to 22nd July

Confidential | 5

Market Performance: Domestic Markets witnessed sharp sell-off in the aftermath of the Union Budget

Source: Bloomberg; All data are as of 22th July 2019

Market Performance: Domestic markets witnessed a sharp sell-off post

the budget; subdued Q1 FY20 earnings have also contributed to the fall

Sectoral Indices: Most of the indices have fallen post the budget;

Banking & Auto Indices have seen the sharpest fall

Top 10 Nifty stocks: The Nifty stocks which have outperformed in the last

1 year have also seen a sharp correction post Budget (except RIL)10 Yr Govt. Bond Yield: 10 yr Yield rallied as a result of the Govt’s

announcement to borrow overseas; reducing the supply in domestic market

-4.2% -4.5% -4.1%

-7.2% -7.1%-8.0%-7.0%-6.0%-5.0%-4.0%-3.0%-2.0%-1.0%0.0%

Nifty Index Nifty 500 Index S&P BSE 200Index

Nifty Midcap 100Index

S&P BSE SmallCap Index

Performance during 5th July to 22nd July

-0.7%

-4.0%

-6.8%-8.3%

-7.2%

-0.4%

2.5%

-7.7%

-9.6%

-3.6%

-12.0%

-9.0%

-6.0%

-3.0%

0.0%

3.0%

6.0%

Nifty ITIndex

NIFTYFMCGIndex

NIFTYFinancialServices

Index

NIFTYAutoIndex

NIFTYBankIndex

NIFTYMediaIndex

NIFTYPharma

Index

NIFTYPrivateBankIndex

NIFTYPSU Bank

Index

NIFTYRealtyIndex

Performance during 5th July to 22nd July

6.70

6.43

6.10

6.20

6.30

6.40

6.50

6.60

6.70

6.80

5-Jul 8-Jul 11-Jul 14-Jul 17-Jul 20-Jul

10 Year Govt Bond Yield

-5.8%

-14.1%

-3.8%

-9.7%

-16.4%

-2.5%

-5.6%

-15.3%

0.0%

-9.8%

-18.0%

-15.0%

-12.0%

-9.0%

-6.0%

-3.0%

0.0%

ICICIBank

BajajFinance

UPL Axis Bank Titan Wipro StateBank of

India

BajajFinserv

RelianceIndustries

L&T

Performance during 5th July to 22nd July

Confidential | 6

Market Performance: Markets fell in June-July; underperforming global markets; tepid Q1 earnings have also contributed to the downfall

Index Performance1st July to 22nd July

Till 30th June’2019

1m 3m 6m 12m CYTD

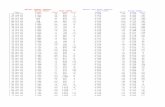

US S&P 500 1.2% 6.9% 3.8% 17.3% 8.2% 17.3%

UK FTSE 100 1.6% 3.7% 2.0% 10.4% -2.8% 10.4%

Japan Nikkei 225 0.7% 3.3% 0.3% 6.3% -4.6% 6.3%

Germany (DAX) -0.8% 5.7% 7.6% 17.4% 0.8% 17.4%

Singapore Straits 1.1% 6.5% 3.4% 8.2% 1.6% 8.2%

Korea KOSPI -1.7% 4.4% -0.5% 4.4% -8.4% 4.4%

Malaysia KLCI -1.0% 1.3% 1.7% -1.1% -1.1% -1.1%

Brazil IBOV 2.5% 4.1% 5.8% 14.9% 38.8% 14.9%

Russia MOEX -2.7% 3.8% 10.8% 16.7% 20.5% 16.7%

India SENSEX -3.5% -0.8% 1.9% 9.2% 11.2% 9.2%

China SHCOMP -3.1% 2.8% -3.6% 19.4% 4.6% 19.4%

Indonesia Jakarta 1.2% 2.4% -1.7% 2.6% 9.6% 2.6%

Broader Markets1st July to 22nd July

Till 30th June’2019

1m 3m 6m 12m CYTD

Nifty-50 -3.6% -1.1% 1.4% 8.5% 10.0% 8.5%

Nifty-500 -4.1% -1.5% -0.1% 5.3% 5.4% 5.3%

S&P BSE 200 -4.1% -1.2% 0.4% 5.9% 6.9% 5.9%

Nifty Midcap 100 -7.4% -1.7% -3.3% -1.2% -2.9% -1.2%

S&P BSE Smallcap -7.7% -4.2% -5.2% -3.2% -11.2% -3.2%

Market Performance: India has underperformed most global

markets in the period of June-July

Sectoral Indices: Auto Sector has seen a battering due to no major relief

in the budget; banks are falling post Q1 commentaries of some banks

Currency: INR appreciated against the USD in June-July; Dollar

weakened against other currencies as well in June-July

Source: Bloomberg; All data are as of 22nd July 2019

-4.34%-3.76%

-4.32%

-11.63%

-6.64% -6.61%

-3.92%

-8.30%-7.54%

-3.73%

-15.00%

-12.00%

-9.00%

-6.00%

-3.00%

0.00%

Nifty IT NiftyFMCG

NiftyFinancialServices

NiftyAuto

NiftyBank

NiftyMedia

NiftyPharma

NiftyPrivateBank

NiftyPSUBank

NiftyRealty

1st June to 22nd July Performance

92

93

94

95

96

97

98

67

69

71

73

75 INR/USD US Dollar Index Spot Rate

Confidential | 7

Market Valuation & Earnings: Trailing PE of the Nifty is near all time highs thanks

to a low earnings base | Discount Between Mid caps and Large Caps deepens

Trailing PE: FY19 earnings were fairly weak for the index driven by

large drags from a few heavyweights

Forward PE: Earnings for the index should improve substantially in FY20

and FY21 as the corporate facing banks revert to normalized profitability

Relative Valuations: Nifty Midcap 100 Index now trades at 14.6 times

forward PE vs Nifty’s 18.10 times forward PE, reflecting a ~24% discount

Nifty Earnings: FY20 earnings growth for the index is expected to

be a sharp 35.3% on the back of a disappointing FY19

24% discount

25.3431

0

5

10

15

20

25

30

Jun

-01

Jun

-02

Jun

-03

Jun

-04

Jun

-05

Jun

-06

Jun

-07

Jun

-08

Jun

-09

Jun

-10

Jun

-11

Jun

-12

Jun

-13

Jun

-14

Jun

-15

Jun

-16

Jun

-17

Jun

-18

Jun

-19

Nifty Trailing 12M PE ratio

0

5

10

15

20

25Nifty 1 Year Forward PE ratio

Significant expansion in valuations post the GFC across the world

460 459

620

734

400

500

600

700

800

FY18 EPS FY19 EPS FY20E EPS FY21E EPS

Nifty EPS

-0.3%

35.3%

18.3%

Source: Bloomberg; All data are as of 22nd July 2019

0

5

10

15

20

25

30Nifty 1 Year Forward PE ratio

Nifty Midcap 100 One Year Forward PE ratio

Confidential | 8

Flows: Multi Cap & Large Cap Funds did see strong inflows during June; Equity

inflows on a whole picked up pace post the election results

FPI Flows: Foreign investor flows have been strong over the last few months. So far in CY2019, the FPI inflows into Equity have been to the tune of INR 78,647 crores

Domestic Flows: For last 7 Months (except March), inflows into Equity Mutual Funds have been negative if we exclude SIPs. Multi Cap & Large Cap Funds saw decent inflows in June with their contribution being ~44% of the total Net Equity Inflows in comparison to ~14% in May

INR Cr

Note: Net Equity Inflows includes Open & Closed Ended Equity Funds including ELSS excluding ETFs

13781

-11423

11654

-5552-10060

-4831

2264 1775

-10825

-28921

5981 3143

-4262

17220

33981

21193

79202596

-40000

-30000

-20000

-10000

0

10000

20000

30000

40000

Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Jan-19 Feb-19 Mar-19 Apr-19 May-19 Jun-19

FPI Equity Inflows (INR Crs)

11171 113509660 9452

8375

1117212622

8414

6606 61585122

11756

42294968

75856690 7304 7554 7554 7658 7727 7985 7985 8022 8064 8095 8055 8238 8183 8122

0

5000

10000

15000

Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Jan-19 Feb-19 Mar-19 Apr-19 May-19 Jun-19

Net Equity Inflows SIP Flows

Source: NSE, AMFI; All data are as of 30th June 2019

Confidential | 9

India’s Industrial Production : Industrial Output increased by 3.1% in

May mainly on account of improvement in power generation

Macro Indicators: GDP growth slowed in March quarter; manufacturing activity softened a bit in June while services continued to slip

Real GDP growth Rate : Q4 GDP grew at a 5 year low of 5.8%;

GDP growth rate for FY19 is 6.8%

India Manufacturing PMI : Growth was led by consumer goods;

Capital goods did not see any see any significant rise in output

Services PMI : Survey participants blamed unfavourable taxation* &

increased compliance cost in the GST era for the contraction in

activities

7

6

6.8

7.7

8.1 8

7

6.6

5.8

5

6

7

8

9

Mar-17 Jun-17 Sep-17 Dec-17 Mar-18 Jun-18 Sep-18 Dec-18 Mar-19

Real GDP Growth Rate%

51.651.2

53.1

52.3

51.7

52.2

53.1

54

53.2

53.954.3

52.6

51.8

52.7

52.1

49

50

51

52

53

54

55India Manufacturing PMI

51.4

49.6

52.6

54.2

51.550.9

52.2

53.753.2

52.2 52.552

5150.2

49.6

47

48

49

50

51

52

53

54

55India Services PMI

*Under GST, services are taxed at 18%, higher than 15% levied earlier

3.09%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

Jan

-18

Feb

-18

Mar

-18

Ap

r-1

8

May

-18

Jun

-18

Jul-

18

Au

g-1

8

Sep

-18

Oct

-18

No

v-1

8

De

c-1

8

Jan

-19

Feb

-19

Mar

-19

Ap

r-1

9

May

-19

IIP YoY%

Source: NSE, AMFI; All data are as of 30th June 2019

Confidential | 10

Passenger Vehicles Domestic: Car market; primarily driven by urban

disposable income, is indicating severe stress in job & loan finance market

Domestic Highlights: CPI rose due to increase in food prices; core CPI continued to moderate | Govt. missed the tax collections target for FY19 by over 1 lac crores

CPI Inflation : CPI Inflation hit eight-month high at 3.18% in June mainly

due to rise in food prices; core CPI continued to remain subdued

Two Wheelers Domestic :Higher insurance costs & lack of liquidity due to the NBFC

situation have driven the slowdown in two-wheelers

13 months 12 months 7 months

Source: NSE, AMFI, Bloomberg; All data are as of 30th June 2019

999.36

Apr18

May18

Jun18

Jul 18 Aug18

Sep18

Oct18

Nov18

Dec18

Jan19

Feb19

Mar19

Apr19

May19

Jun19

900

920

940

960

980

1000

1020

1040

1060

1080

1100

1120

1140GST Collections (Rs Bn)

GST collections: The collections have come below INR 1 lac crores in

the month of June

3.18

4.33

2.21

0

1

2

3

4

5

6

Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18 Feb-19 May-19

CPI Inflation % CPI Inflation (Urban) CPI Inflation (Rural)

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0% Domestic Passenger Vehicles Sales YoY%

17 months12 months

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0% Domestic Two-Wheeler Sales YoY%

Confidential | 11

Global Macro: US treasury yields price-in rate cuts from the Fed in response to a slowing economy

US FOMC Dots Median of the Longer Run Projections: This data is taken from the Projection Materials, released at the end of every FOMC meeting

US Treasury Yields: Bond markets are anticipating a significant slowdown in US growth and price in rate cuts by the Fed

US CPI: Core CPI at 2.1% YoY in June was more than expectations; reduces the chance of a 50 bps rate cut by Fed

US GDP Growth rate: US GDP grew at a faster face than expected in the first quarter; expectation was 2.5%

Median of the FOMC’s projections for the Federal Reserve’s target overnight rate over their longer term

0

1

2

3

4

5

Jun-08 Jun-09 Jun-10 Jun-11 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16 Jun-17 Jun-18 Jun-19

US 10 Yr Govt. Bond Yield

More than 100 bps fall since it made its high in Oct’2018

2.5

2.00

2.50

3.00

3.50

4.00

Jun-15 Dec-15 Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Dec-18 Jun-19

US FOMC Dots Median of the Longer Run Projections

-1.00

0.00

1.00

2.00

3.00

4.00

Jun-15 Dec-15 Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Dec-18 Jun-19

US CPI YoY%

Source: Bloomberg; All data are as of 30th June 2019

3.10

0.00

1.00

2.00

3.00

4.00

5.00

Mar-15 Sep-15 Mar-16 Sep-16 Mar-17 Sep-17 Mar-18 Sep-18 Mar-19

United States GDP YoY%

Confidential | 12

Global Macro: China’s GDP grew at the weakest pace in past 27 years; ECB and BOJ assets continues to expand

ECB Assets:The European Central Bank continues to maintain an accommodative monetary policy given the continued weak growth

China GDP Growth: China’s GDP grew at a faster pace than expected in the first quarter; expectation was 6.3%

US Fed Assets: US will slow the slimming of the Balance Sheet by September which should help in stimulating the economy by injecting liquidity

Bank of Japan Assets:BOJ has been in the realm of unconventional monetary policy since 1999 and has expanded its ETF purchases repeatedly

6.2

5.80

6.20

6.60

7.00

7.40

Mar

-15

Jun

-15

Sep

-15

De

c-1

5

Mar

-16

Jun

-16

Sep

-16

De

c-1

6

Mar

-17

Jun

-17

Sep

-17

De

c-1

7

Mar

-18

Jun

-18

Sep

-18

De

c-1

8

Mar

-19

Jun

-19

China GDP YoY%

4693

0

1000

2000

3000

4000

5000ECB Assets (Euro Bns)

Source: Bloomberg; All data are as of 30th June 2019

0

1000000

2000000

3000000

4000000

5000000 US Fed Assets (USD Mns)

0

100000

200000

300000

400000

500000

600000 Bank of Japan Assets (JPY Bns)

Confidential | 13

10,199

10,494

10,935

11,377

9000

9500

10000

10500

11000

11500

12000

12500

13000

Jul '19 Sep '19 Dec '19 Mar '20

Current Nifty level(11,350)

10.1% Downside(Immediate)

Equity allocation of INR 100 Jul-19 Aug-19 Sep-19 Oct-19 Total

• Staggered deployment of INR 90• Hold INR 10 in cash; deployment basis market level & outlook

22.5 22.5 22.5 22.5 90.00

Risk-Reward ratio unfavourable at current Nifty level, and there is concern on the strength of earnings recovery with domestic weakness expected to continue over 1-2 quarters, we therefore continue to maintain “10% Underweight” stance on equities

9.9% Upside(By Mar 20)

Equity Deployment Strategy10% underweight on equities to hold in cash, 90% to be deployed in staggered manner

Confidential | 14

India Equities: Valuations & Strategy – 10% Underweight Stance Continues

Indian markets touched all time highs at the start of June, however it gave up all its gains post budget in July. Last month, Indianmarkets had outperformed global markets post the decisive mandate to the NDA government, however most of these gains havebeen washed out post the budget. Some uncertainty regarding FPI taxation seems to have spooked market participants.

On the global front, post the G20 summit, US and China agreed to keep trade war from escalating and restart trade negotiations.The US Fed left interest rates on hold and signaled a rate cut in the near future.

Midcap stocks have continued to under-perform large caps. The high valuations came off a bit and the earnings outlook for someof these companies have also weakened given the muted commentary on quarterly results. While the domestic weakness couldcontinue for the next two quarters or longer, the fact that these realities are getting reflected in stock prices makes the currentmarket conditions less risky. In contrast, prior to elections markets were largely ignoring signs of a slowdown and expecting ampleliquidity and stimulus to support prices.

With the General Elections & Budget behind us now, crude prices, consumption slump along with global growth concerns takefront seat now. Therefore we maintain our stance of “10% Underweight” on equities. For fresh corpus, we recommendstaggering 90% deployment in next 4 months while keeping 10% as dry powder for deploying opportunistically.

Mutual Funds: As domestic liquidity continues to drive markets, we advise new investments to be staggered in Mutual Funds viaSIPs/STPs.Recommended allocation within equity mutual funds is as under:

• 50% Large Cap allocation

• 50% Multi Cap allocation (such funds currently have a bias toward large cap)

• 5%-10% Mid Cap allocation (only for Moderate, Growth and Aggressive risk profiles)

• For investors who want equity exposure but have low appetite for volatility, they can take equity exposure throughAggressive Hybrid Funds. Such funds have around 25% to 30% of their portfolio into Debt instruments which providescushion to the portfolio return during market volatility.

Source: EPS Estimates by KIE

Confidential | 15

Recommended Equity Funds’ Performances

Source: MFI ExplorerReturns are CAGR as on July 23, 2019 and for Regular Plans with Growth option. Corpus size is as on July, 2019.

Scheme Name Corpus (In crs.) 1 Year 3 Years 5 Years Investor Suitability

Large Cap Funds

Aditya Birla Sun Life Frontline Equity Fund 21,664 0.44 7.71 9.32 All Risk Profiles except Secure

Axis Bluechip Fund 6,303 1.16 12.88 10.89 All Risk Profiles except Secure

HDFC Top 100 Fund 17,912 10.53 11.54 9.40 All Risk Profiles except Secure

ICICI Prudential Bluechip Fund 22,117 3.13 9.93 10.02 All Risk Profiles except Secure

Mirae Asset Large Cap Fund 13,618 6.08 12.60 13.12 All Risk Profiles except Secure

UTI Nifty Next 50 Index Fund 395 -5.32 - - All Risk Profiles except Secure

Large & Mid Cap Funds

IDFC Core Equity Fund 2,970 -2.86 8.22 9.60 All Risk Profiles except Secure

Invesco India Growth Opportunities Fund 1,539 -2.68 10.57 11.21 All Risk Profiles except Secure

Multi Cap Funds (Multi Cap/ Value/ Focused/ Dividend Yield/ Contra)

Axis Focused 25 Fund 8,044 -6.40 12.70 12.82 All Risk Profiles except Secure

HDFC Equity Fund 23,688 10.02 11.38 9.23 All Risk Profiles except Secure

Kotak Standard Multicap Fund 25,845 2.58 11.15 13.67 All Risk Profiles except Secure

Mid & Small Cap Funds (Mid Cap/Small Cap)

HDFC Small Cap Fund 8,427 -7.51 10.96 13.18 All Risk Profiles except Secure

Kotak Emerging Equity Scheme 4,501 -3.02 7.34 14.21 All Risk Profiles except Secure

L&T Midcap Fund 5,026 -9.30 8.80 13.35 All Risk Profiles except Secure

Thematic/Sectoral Funds

Sundaram Rural and Consumption Fund 2,251 -6.45 6.89 12.60 All Risk Profiles except Secure

Sundaram Services Fund 1,217 - - - All Risk Profiles except Secure

Solution Oriented - Retirement Funds

Tata Retirement Savings Fund - Moderate Plan 1,092 -3.91 9.41 12.49 All Risk Profiles except Secure

Solution Oriented - Children's Funds

HDFC Children’s Gift Fund 2,840 2.44 9.63 10.45 All Risk Profiles except Secure

ICICI Prudential Child Care Fund (Gift Plan) 645 4.22 7.52 8.45 All Risk Profiles except Secure

Indices

Nifty 2.22 9.87 7.76

Confidential | 16

Recommended Hybrid Funds’ Performances

Scheme Name Corpus (In crs.) 1 Year 3 Years 5 Years Investor Suitability

Aggressive Hybrid Funds

Aditya Birla Sun Life Equity Hybrid '95 12,663 -1.67 5.85 9.22 All Risk Profiles except Secure

L&T Hybrid Equity Fund 9,044 -1.48 6.78 10.10 All Risk Profiles except Secure

Reliance Equity Hybrid Fund 10,833 -2.56 6.82 8.84 All Risk Profiles except Secure

SBI Equity Hybrid Fund 29,832 6.75 9.73 11.24 All Risk Profiles except Secure

Balanced Advantage Funds (Balanced Advantage OR Dynamic Asset Allocation)

ICICI Prudential Balanced Advantage Fund 28,709 5.74 8.10 9.41 All Risk Profiles except Secure

Kotak Balanced Advantage Fund 2,879 - - - All Risk Profiles except Secure

Indices

Nifty 2.22 9.87 7.76

Source: MFI ExplorerReturns are CAGR as on July 23, 2019 and for Regular Plans with Growth option. Corpus size is as on July, 2019.

Debt Market Update &

Debt MF Strategy

Confidential | 18

Indicators

Policy Expectation

• With growth in Q4FY19 moderating to 5Y low, inflation inJune continuing to remain below estimates andgovernment maintaining fiscal prudence in budget; thereis case for 25bps rate cut in August

• Market expectations of repo rate trajectory reflected by1Y OIS (currently at 5.41%) also indicate it pricing in atleast 25 bps cut

Inflation

• CPI inflation rose to 3.18% in June from 3.05% in May continuing to remain below estimates

• RBI’s inflation estimates stands at 3.0-3.1% for 1HFY20 and at 3.5-3.8% 2HFY20

• Risks remain broadly balanced as reducing core inflation and rising food inflation trajectory expected to converge in near term

• INR currently at 68.8/$ (up from ~69.7/$ in June end); has been buoyed by debt flows from FPI

• Near term moves likely to be volatile with global liquidity attracted to debt markets while risk sentiments weighed down by global growth concerns & FPI reaction to higher surcharge introduced in budget

Corporate and G-Sec Benchmark Yield• 10Y G-sec (now at 6.36%) rallied 50+ bps since June

end• 10Y segment has outperformed related to all other

parts of the curve. Partial profit booking and reversal likely. Likely to consolidate.

Liquidity• Banking system liquidity has improved significantly with

average levels now near INR 1.5L Cr• Govt using external borrowing (INR 0.7L Cr) has helped

reduce supply pressure causing the recent rally

INR

G-Sec Supply• Govt borrowings unchanged at INR 7.1L Cr (gross) and

INR 4.73L Cr (net) drove away apprehension on incremental borrowing

• Announcement to partly use offshore route (10% of gross borrowing) reduced concerns on supply

Debt Market: Key Variables

Source: Bloomberg, KIE

Global Trends• US 10Y stands at 2.047% below 3M yields at 2.051% with

increasing expectations of rate cuts by the Fed• Globally interest rates have fallen due to concerns of

slowdown; aggregate negative yielding debt increased from $11.01 to $13.05 Tn in 1 month; leading to incremental debt flows to EMs

Fiscal Policy• Government adhered to fiscal consolidation by lowering

fiscal deficit target to 3.3% against market expectations of 3.4%+

Confidential | 19

Global yields soften across the curve; negative yields helped flows in EMs leading to sharp rally

Note: As of 19th June 2019, Source: Bloomberg

Jan-19 Feb-19 Mar-19 Apr-19 May-19 Jun-19 Jul-19

7.00

8.00

9.00

10.00

11.00

12.00

13.00

14.00Aggregate Negative Yielding Debt ($ Tn)

Aggregate negative yielding debt has increased sharply in

FYTD20 from ~$10 tn to $13 tn

99

4740

56

154

IndiaIndonesiaKoreaThailandBrazil

0

20

40

60

80

100

120

140

160

180

Bp

s

India

Flows to EM increased with sharp rally in 10Y curve across

countries since April 2019

2.051 2.047

1.50

1.70

1.90

2.10

2.30

2.50

2.70

2.90

3M 6M 1Y 2Y 3Y 5Y 7Y 10Y 30Y

% Y

ield

US Treasury (Current Yields)

US Treasury (3M earlier)

US 10Y yields below 3M as expectations of rate cut in July policy

strengthened with Fed officials indicating accommodative policy

ItalySpainFranceJapanGermanySwitzerland

Globally yields continued to fall with several points of yield curve

in negative territory (shown in blue below) in Europe & Japan

6M1Y2Y3Y4Y5Y6Y7Y8Y9Y

10Y15Y30Y

Fall in 10Y yields since April 2019

Confidential | 20

With GDP growth slowing, inflation continuing to remain benign Government sticks to fiscal numbers

3.183.10E3.50E

4.09

2.37

Jun18

Jul18

Aug18

Sep18

Oct18

Nov18

Dec18

Jan19

Feb19

Mar19

Apr19

May19

Jun19

Sep19

Mar20

-3.00

-2.00

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00CPI (YoY%) Core Inflation Food Inflation

Core inflation continued to moderate for 8th straight month

owing to weak demand; food inflation rose from 2.03% to 2.37%

Note: As of 19th July 2019, Source: Bloomberg, PTI

7.2E

6.7E

5.8

6.67.0

8.07.77.7

Mar 20Sep 19Mar 19Dec 18Sep 18Jun 18Mar 18Dec 17

4.00

5.00

6.00

7.00

8.00

9.00 Real GDP Growth Rate (% YoY)

India’s GDP growth moderated to 5.8% in Q4FY19 while FY19

GDP growth rate was 6.8%

4.6

4.13.9

3.5 3.53.3 3.3E

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

2014 2015 2016 2017 2018 2019 2020

Fiscal consolidation maintained in budget with target at 3.3%

against market expectations of 3.4%+

7.59

6.88

6.36

6.00

6.20

6.40

6.60

6.80

7.00

7.20

7.40

7.60

7.80

8.00

Jan-19 Feb-19 Mar-19 Apr-19 May-19 Jun-19 Jul-19

% Y

ield

10Y G-sec yields

10Y G-sec rallied as govt. gave comfort on supply – demand

dynamics with fiscal at 3.3% & partially borrowing through offshore

Confidential | 21

Liquidity in Debt markets improved with FPI flows turning positiveRBI OMOs and offshore borrowing supports liquidity

14.7

19.2

27.2 27.8

33.035.6 36.9

China India South Korea Russia Thailand Brazil Indonesia

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00 External Debt (% of GDP)

India’s external debt to GDP ratio is among the lowest globally;

offshore funding of Govt borrowing to help debt markets

2,521

-6,745

22,987

-6,529

7,560

CYTD2019CY2018CY2017CY2016CY2015

-10,000

-5,000

0

5,000

10,000

15,000

20,000

25,000

US

D M

illi

on

FII flows have turned positive to Indian debt markets in

CYTD19

1498.74

-1000

0

1000

2000

17-Jun 27-Jun 7-Jul 17-JulAm

ou

nt

in R

s. B

n

Banking system liquidity improved significantly from negative in

the past 3-6 months to now at a comfortable surplus of INR 1.5L Cr

10,000

20,000

20,000

36,000

52,000

50,000

50,000

37,500

60,000

35,000

25,000

12,500

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

May18

Jun18

Sep18

Oct18

Nov18

Dec18

Jan19

Feb19

Mar19

Apr19

May19

Jun19

RBI has infused INR 87,500 Cr till date in FY20 through

USD/INR swaps and OMOs

Rs cr

Note: As of 19th June 2019, Source: Bloomberg, RBI

Confidential | 22Note: As of 19th June 2019, Source: Bloomberg, RBI

7.63

5.75

Ju

l 19

Ju

n 1

9

Ap

r 19

Ma

r 19

Fe

b 1

9

Dec 1

8

No

v 1

8

Oct

18

Au

g 1

8

Ju

l 18

Ju

n 1

8

Ap

r 18

Ma

r 18

Jan

18

Dec 1

7

No

v 1

7

Oct

17

Au

g 1

7

Ju

l 17

Ju

n 1

7

Ma

y 1

7

Ma

r 17

Fe

b 1

7

Jan

17

5.00

5.50

6.00

6.50

7.00

7.50

8.00

8.50

9.00

9.501 Yr CP Repo

With yields coming off across the curve; 1Y CPs continued to

look attractive with spread of 188 bps over repo

GST collections slowing is a concern to fiscal targets; Oil prices have been volatile in FYTD20 though remaining range bound this month

834,733

185,007 111,540

38,970

670,167

185,057

106,919 38,578

Liquid Funds Short Term Funds Credit Funds Gilt / DynamicFunds

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

INR

Cro

res

May-19 Jun-19

Short term funds’ AUM remained flat while credit funds saw

~5k Cr outflows

999.36

Apr18

May18

Jun18

Jul18

Aug18

Sep18

Oct18

Nov18

Dec18

Jan19

Feb19

Mar19

Apr19

May19

Jun19

900

950

1000

1050

1100

1150 GST Collections (Rs Bn)

GST collections in April reached all-time high, increasing

hopes of meeting FY20 expectations

Rs bn

62.18

Jul 19Jun 19May 19Apr 19

58

60

62

64

66

68

70

72

74

76 Brent Oil ($/bbl)

Oil prices have been in $62-67/bbl in July due to global slowdown;

however risks remain with escalating crisis in Middle East

Confidential | 23

Debt Funds Performance – Last 1 YearStrong performance shown by long end strategies on back of sharp fall in yieldsCredit risk funds weighed down by downgrades and defaults

7.3

7

7.2

7

6.5

9

9.0

2

5.9

6

10

.45

14

.94

LIQ

UID

F

UN

DS

ULT

RA

S

HO

RT

/LO

W

DU

RA

TI

ON

…

AR

BIT

RA

GE

F

UN

DS

SH

OR

T

TE

RM

F

UN

DS

ME

DIU

M A

ND

C

RE

DIT

R

ISK

F

UN

DS

DY

NA

MIC

F

UN

DS

GIL

T

FU

ND

S

PERFORMANCE COMPARISON

Note: As of 17th June 2019, Source: MFI

Confidential | 24

24

Tenors G-Sec AAA - PSU AAA- Corp AA+ AA AA- A+

3M 5.76 6.45 6.70 6.94 7.21 7.64 8.09

6M 5.81 6.59 6.83 7.07 7.35 7.78 8.23

1Y 5.84 6.92 7.27 7.44 7.71 7.91 8.36

3Y 6.24 7.01 7.47 7.70 7.96 8.06 8.51

5Y 6.33 7.25 7.74 7.85 8.08 8.16 8.61

7Y 6.48 7.39 7.81 7.96 8.19 8.18 8.63

10Y 6.36 7.35 7.89 8.02 8.27 8.21 8.66

15Y 6.75 7.36 8.11 8.11 8.44 8.23 8.68

Credit SpreadsWhile yields have come off sharply, benign rate environment holds good for high quality short end bonds

Note: As of 19th July 2019, Source: Bloomberg

Confidential | 25

India Fixed Income: Strategy

With growth in Q4FY19 moderating to 5Y low, inflation in June continuing to remain below estimates and government maintaining fiscal prudence in budget; the case for 25bps rate cut in August policy has strengthened.

G-sec demand – supply apprehensions have reduced with borrowing remaining unchanged and announcement of partially routing (~10% of gross) them through the external borrowing

Risks: Global risk-off environment, crude prices, fiscal slippage, sharp unfavourable currency movement, call-off of sovereign bond issue

We reiterate that the current environment calls for a “caution” in credit space. Therefore we suggest no allocation to “Credit Funds” and predominate allocation to AAA oriented funds.

Investment Focus: We recommend to maintain overweight on short/medium term strategies. Remain high quality focused. 1 to 5 year corporate bonds, most

preferred.

Best played through roll-down strategies or 3 year high quality Fixed Maturity Plans (FMPs). Also selective allocation to active short term funds is advised.

Clients with a long investment horizon of at least 10 years, may look to lock in yields in high quality 10 Year roll down or hold to maturity (HTM) funds.

Source : AMCs, other Financial websites

Confidential | 26

Recommended Debt Funds’ Performances

Scheme NameCorpus (In

crs.)6m 1Yr 2Yr Investor Suitability

Short Term 1-3 yrs (Corporate Bond/ Banking & PSU/Short Duration)

Tier IAditya Birla Sun Life Corporate Bond Fund 15,662 10.94 10.15 7.50 All Risk Profiles except SecureHDFC Short Term Debt Fund 7,992 10.02 9.17 7.34 All Risk Profiles except SecureICICI Prudential Banking & PSU Debt Fund 5,930 11.88 9.45 6.48 All Risk Profiles except SecureICICI Prudential Short Term Fund 8,680 10.28 8.97 6.42 All Risk Profiles except Secure

Tier IIAxis Banking & PSU Debt Fund 6,530 11.12 10.44 8.21 All Risk ProfilesIDFC Banking & PSU Debt Fund 6,718 12.41 11.26 7.87 All Risk ProfilesL&T Triple Ace Bond Fund 1,197 19.17 13.80 8.11 All Risk ProfilesL&T Banking and PSU Debt Fund 785 9.64 8.50 6.57 All Risk ProfilesSundaram Corporate Bond Fund 662 12.33 10.65 6.16 All Risk Profiles

Dynamic Debt (Medium to Long Duration/ Dynamic Bond/Gilt)Tier I

ICICI Prudential All Seasons Bond Fund 2,750 12.54 10.14 6.10 All Risk Profiles except SecureReliance Gilt Securities Fund 1,040 20.43 16.37 7.83 All Risk Profiles except SecureSBI Magnum Gilt Fund 1,524 22.80 15.62 6.93 All Risk Profiles except Secure

Tier II

Aditya Birla Sun Life Active Debt Multi Manager FoF Scheme 11 8.14 5.08 6.72 All Risk Profiles except SecureICICI Prudential Bond Fund 3,279 12.46 10.24 5.93 All Risk Profiles

Source: MFI ExplorerReturns are CAGR as on July 23, 2019 and for Regular Plans with Growth option. Corpus size is as on June, 2019.

Confidential | 27

DisclaimerThe aforesaid is for information purposes only and should not be construed to be investment advice under SEBI (Investment Advisory) Regulations.

In the preparation of the material contained in this document, Kotak Mahindra Bank has used information that is publicly available, including information developed in-house. Some of the material used in the document may have been obtained from members/persons other than the Kotak Mahindra Bank and/or its affiliates and which mayhave been made available to Kotak Mahindra Bank and/or its affiliates. Information gathered & material used in this document is believed to be from reliable sources. KotakMahindra Bank however does not warrant the accuracy, reasonableness and/or completeness of any information. For data reference to any third party in this material nosuch party will assume any liability for the same. Kotak Mahindra Bank and/or any affiliate of Kotak Mahindra Bank does not in any way through this material solicit any offerfor purchase, sale or any financial transaction/commodities/products of any financial instrument dealt in this material. All recipients of this material should before dealingand or transacting in any of the products referred to in this material make their own investigation, seek appropriate professional advice

We have included statements/opinions/recommendations in this document which contain words or phrases such as "will", "expect" "should" and similar expressions orvariations of such expressions, that are "forward looking statements". Actual results may differ materially from those suggested by the forward looking statements due torisks or uncertainties associated with our expectations with respect to, but not limited to, exposure to market risks, general economic and political conditions in India andother countries globally, which have an impact on our services and / or investments, the monetary and interest policies of India, inflation, deflation, unanticipatedturbulence in interest rates, foreign exchange rates, equity prices or other rates or prices, the performance of the financial markets in India and globally, changes indomestic and foreign laws, regulations and taxes and changes in competition in the industry. By their nature, certain market risk disclosures are only estimates and could bematerially different from what actually occurs in the future. As a result, actual future gains or losses could materially differ from those that have been estimated

Kotak Mahindra Bank (including its affiliates) and any of its officers directors, personnel and employees, shall not liable for any loss, damage of any nature, including but notlimited to direct, indirect, punitive, special, exemplary, consequential, as also any loss of profit in any way arising from the use of this material in any manner. The recipientalone shall be fully responsible/ are liable for any decision taken on the basis of this material. The investments discussed in this material may not be suitable for all investors.Any person subscribing to or investing in any product/financial instruments should do so on the basis of and after verifying the terms attached to such product/financialinstrument. Financial products and instruments are subject to market risks and yields may fluctuate depending on various factors affecting capital/debt markets. Please notethat past performance of the financial products and instruments does not necessarily indicate the future prospects and performance thereof. Such past performance mayormay not be sustained in future. Kotak Mahindra Bank (including its affiliates) or its officers, directors, personnel and employees, including persons involved in thepreparation or issuance of this material may; (a) from time to time, have long or short positions in, and buy or sell the securities mentioned herein or (b) be engaged in anyother transaction involving such securities and earn brokerage or other compensation in the financial instruments/products/commodities discussed herein or act as advisoror lender / borrower in respect of such securities/financial instruments/products/commodities or have other potential conflict of interest with respect to anyrecommendation and related information and opinions. The said persons may have acted upon and/or in a manner contradictory with the information contained here. Nopart of this material may be duplicated in whole or in part in any form and or redistributed without the prior written consent of Kotak Mahindra Bank. This material is strictlyconfidential to the recipient and should not be reproduced or disseminated to anyone else

This material is not a research report as per the SEBI (Research Analyst) Regulations, 2014. We may or may not have any relation with Kotak AMC.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.