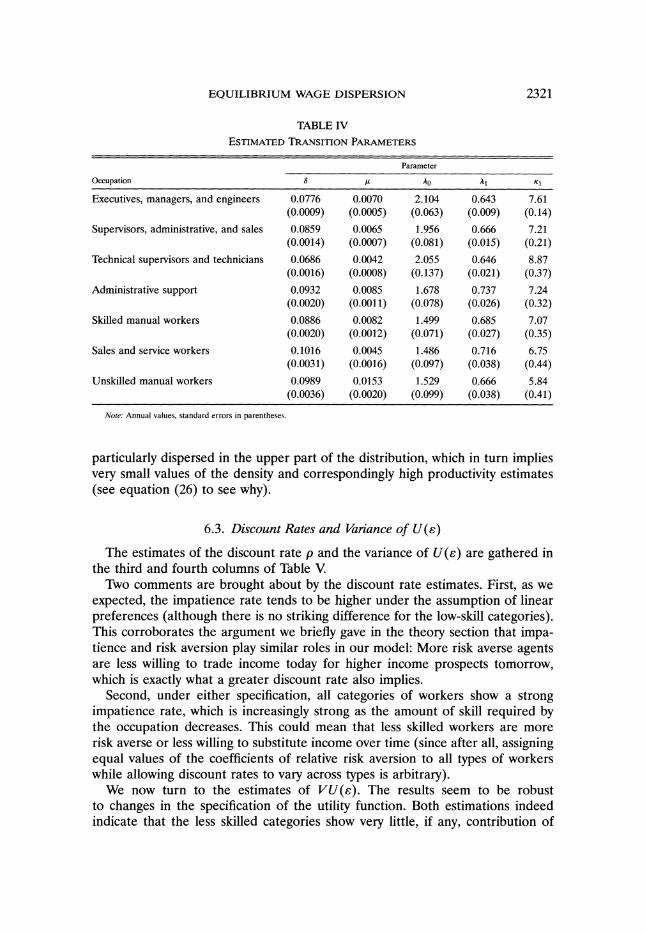

Equilibrium Wage Dispersion with Worker and Employer ... · an earlier contribution (Postel-Vinay...

57

Equilibrium Wage Dispersion with Worker and Employer Heterogeneity Author(s): Fabien Postel-Vinay and Jean-Marc Robin Source: Econometrica, Vol. 70, No. 6 (Nov., 2002), pp. 2295-2350 Published by: The Econometric Society Stable URL: http://www.jstor.org/stable/3081988 . Accessed: 31/03/2011 11:47 Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at . http://www.jstor.org/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unless you have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and you may use content in the JSTOR archive only for your personal, non-commercial use. Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at . http://www.jstor.org/action/showPublisher?publisherCode=econosoc. . Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed page of such transmission. JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. The Econometric Society is collaborating with JSTOR to digitize, preserve and extend access to Econometrica. http://www.jstor.org

Transcript of Equilibrium Wage Dispersion with Worker and Employer ... · an earlier contribution (Postel-Vinay...

Equilibrium Wage Dispersion with Worker and Employer HeterogeneityAuthor(s): Fabien Postel-Vinay and Jean-Marc RobinSource: Econometrica, Vol. 70, No. 6 (Nov., 2002), pp. 2295-2350Published by: The Econometric SocietyStable URL: http://www.jstor.org/stable/3081988 .Accessed: 31/03/2011 11:47

Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unlessyou have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and youmay use content in the JSTOR archive only for your personal, non-commercial use.

Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at .http://www.jstor.org/action/showPublisher?publisherCode=econosoc. .

Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printedpage of such transmission.

JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

The Econometric Society is collaborating with JSTOR to digitize, preserve and extend access to Econometrica.

http://www.jstor.org

Econometrica, Vol. 70, No. 6 (November, 2002), 2295-2350

EQUILIBRIUM WAGE DISPERSION WITH WORKER AND EMPLOYER HETEROGENEITY

BY FABIEN POSTEL-VINAY AND JEAN-MARC ROBIN'

We construct and estimate an equilibrium search model with on-the-job-search. Firms make take-it-or-leave-it wage offers to workers conditional on their characteristics and they can respond to the outside job offers received by their employees. Unobserved worker productive heterogeneity is introduced in the form of cross-worker differences in a "com- petence" parameter. On the other side of the market, firms also are heterogeneous with respect to their marginal productivity of labor. The model delivers a theory of steady- state wage dispersion driven by heterogenous worker abilities and firm productivities, as well as by matching frictions. The structural model is estimated using matched employer and employee French panel data. The exogenous distributions of worker and firm hetero- geneity components are nonparametrically estimated. We use this structural estimation to provide a decomposition of cross-employee wage variance. We find that the share of the cross-sectional wage variance that is explained by person effects varies across skill groups. Specifically, this share lies close to 40% for high-skilled white collars, and quickly decreases to 0% as the observed skill level decreases. The contribution of market imperfections to wage dispersion is typically around 50%.

KEYWORDS: Labor market frictions, wage dispersion, log wage variance decomposition.

1. INTRODUCTION

WHY DO WAGES DIFFER across identical workers? Why do firm characteristics matter? What is the source of the wage dispersion that firm and worker char- acteristics cannot explain? To address these basic three questions, we construct and estimate an equilibrium model of the labor market with worker- and firm- heterogeneous match productivities and on-the-job search. Search frictions are indeed a cause of market imperfection, which in theory resolves the three ques- tions altogether: Wages differ across firms because search frictions are a source

1 We are grateful for comments received from conference participants at the "search and matching" conference held at the University of Iowa (Aug. 2000), the Econometric Society World Meeting in Seattle (Aug. 2000), the "assignment and matching models" conference held at the Tinbergen Insti- tute (Dec. 2000), and from seminar participants at Boston University, New York University, Brown, Yale, University of Minnesota, University of Wisconsin, Northwestern, CREST, Paris-Jourdan, Uni- versite d'Evry, University of Aarhus, Universite Catholique de Louvain, LSE, Oxford, and Univer- sity College London. Discussions with Jim Albrecht, Ken Burdett, Melvyn Coles, Chris Flinn, Sam Kortum, Francis Kramarz, Dale Mortensen, and Gerard Van den Berg led to significant improve- ments in the paper. Special thanks are due to Zvi Eckstein for his numerous and insightful com- ments on preliminary versions of this paper. We are also grateful to the journal co-editor and two anonymous referees for the outstanding quality and constructiveness of their reports. The customary disclaimer naturally applies.

2295

2296 F. POSTEL-VINAY AND J.-M. ROBIN

of inefficiency, allowing less efficient firms to survive. Search frictions leave mar- ket power to employers, whereby more efficient firms extract higher rents. On- the-job search forces employers to grant their employees wage raises randomly over time, so that wages differ across identical employer-employee pairs.

In our model, unemployed workers search for a job and employees search for a better job. Workers differ in ability and firms differ in the marginal pro- ductivity of efficient labor. Workers and firms are imperfectly informed about the location of worker and firm types, which precludes optimal assignments as in standard marriage models. Yet, when two agents meet, both are immediately informed about each other's types. Employers have all the bargaining power and offer unemployed workers their reservation wage. The equilibrium nonetheless differs from Diamond's monopsony model as search on the job allows employees to locate alternative employers, whom they can bring into Bertrand price com- petition with their current employer. This competition either results in a wage rise or in job mobility, the poaching employer paying the worker a wage that can even be less than his/her current wage if the option value of turning down the best offer that the current employer can make-the marginal productivity-in exchange of a greater potential best offer-the marginal productivity at the new job-is large enough. Our model thus not only generates tenure effects but also job-to-job mobility with wage cuts.

The main prediction of the model however pertains to the cross-sectional dis- tribution of earnings. We show that log earnings are the sum of a worker-specific contribution to match productivity and a firm-specific component that closely interacts with a statistical summary of the last wage mobility that the worker enjoyed and that typically characterizes the effect of frictions. The worker effect is independent of the firm and the friction effects because employers do not sort workers by their characteristics thanks to the assumption of perfect substitutabil- ity of worker abilities. But it happens that the firm effect and the friction effect are not independent as more productive firms have stronger market power and thus suffer less from the Bertrand competition.

We use a rich panel of matched employer-employee data to estimate our model semi-nonparametrically. By that we mean that the econometric model is only parametric when the theory requires specific parameters (discount rates, job offer arrival rates, etc.), and is nonparametric as far as the distributions of firm and worker heterogeneities, exogenous to the model, are concerned.2

Although the three components of the steady-state earnings distribution are not independent, we proceed to a decomposition of the variance of earnings into three separate components by allocating the total within-firm variance of earn- ings that is not explained by worker heterogeneity to market frictions and all the between-firm variance to the firm effect. This wage variance decomposition is

2 The estimation of these distributions and model parameters uses data on spell durations and hardly more than a cross-section of the wage data. Most of the dynamic dimension of the wage data can then be used for out-of-sample fit analysis. Taking account of the fact that the model features no idiosyncratic productivity shocks, we conclude that it gives satisfactory predictions of wage variations with and without employer change.

EQUILIBRIUM WAGE DISPERSION 2297

undoubtedly the main empirical result of this paper. We find that the share of the total log wage variance explained by person effects lies around forty percent for managers, and quickly drops as the observed skill level decreases. The con- tribution of the person effect is estimated to be zero for the three lower-skilled worker categories, out of seven categories. Either there is no unobserved ability differences for low skilled workers, or some unmodelled institution, like collec- tive agreements or minimum wages, forbids the individualization of wages.

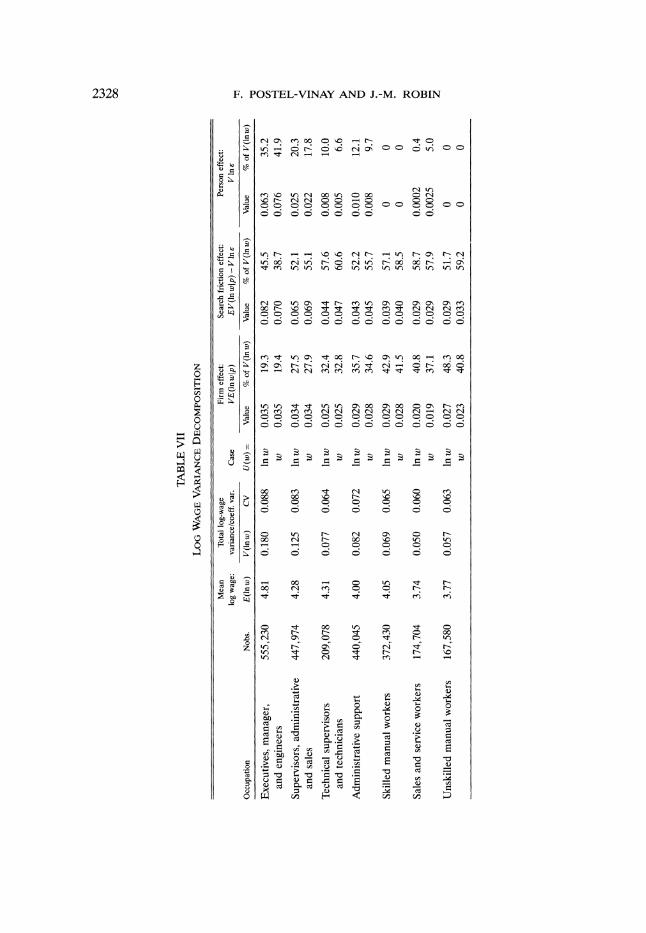

The estimation of a structural equilibrium search model to quantify the con- tribution of market frictions to the wage variance is the principal novelty of this paper. This contrasts with the work of Abowd, Kramarz, and Margolis (1999, hereafter AKM)3 who estimate a log-wage equation with firm and worker effects using the same data but over a different period of time. They find that unmea- sured individual heterogeneity accounts for more or less fifty percent of the total variance of log wages, while firm heterogeneity accounts for another thirty per- cent, the remaining twenty percent being left unexplained. Why is our estimate of the person effect so much smaller? We answer: because of labor market fric- tions. Endogenous worker mobility through the sequential sampling of alterna- tive job offers creates earnings differentials across identical workers working at identical firms. A "lucky" or "senior" worker who has gotten one more job offer than his "unlucky" or "junior" alter ego has also gotten one extra opportunity to bargain for a higher wage. Estimating a static error component model when the data generating process is dynamic will therefore attribute all historical differ- ences (in the states of individual wage trajectories at the first observation date) to person effects. We find that the explanatory power of historical differences is far from negligible (forty to sixty percent of total wage variance, depending on the skill category).

Lastly, thanks to the flexibility of the matching technology that we first posit, the model has interesting suggestions about the anatomy of the process through which workers and firms are matched together. Most empirical equilibrium search models make the assumption of random matching by which all firms have the same probability of being contacted by job seekers whatever their size.4 Here we use firm size data to come up with a measure of the firms' "recruiting effort" and find that it is in a decreasing relationship with the firms' productivities: more productive firms devote less effort to hiring, which naturally makes them less efficient in contacting potential new employees. On the other hand, since they generate ceteris paribus higher match surpluses, they are more likely to attract the workers that they do contact. Those two opposing forces sum up to a hump- shaped relationship between productivity and firm size.

Having motivated our research and announced our main results, we end the introductory part of the paper with a review of the related literature. The rest of

3See also Abowd and Kramarz (2000), and Abowd, Finer, and Kramarz (1999) for a similar descriptive analysis on US data.

4 See Burdett and Vishwanath (1988) and Mortensen (1998, 1999) for theoretical explorations of alternative matching hypotheses.

2298 F. POSTEL-VINAY AND J.-M. ROBIN

the paper will be divided into five parts: Section 3 details the theoretical model, Section 4 describes the data, Section 5 details the structural estimation proce- dure, Section 6 reports and discusses the estimation results, and in Section 7, we proceed to dynamic simulations. A final section concludes on the successes and failures of our model, and points to some ideas to improve on the latter. Proofs and technical details are gathered in a final Appendix.

2. RELATED LITERATURE

The wage setting mechanism assumed in this paper was already explored in an earlier contribution (Postel-Vinay and Robin (1999)) and a somewhat similar idea was independently developed by Dey and Flinn (2000). The model discussed in the present paper extends this earlier work in many directions. First, instead of making the standard assumption (in search models) that workers merely differ in their opportunity cost of employment, we also allow them to differ in ability. Second, the model exhibits a more flexible matching procedure than is usually posited by job search models (random matching). It finally provides an extended empirical treatment whereas our earlier paper was primarily focused on the the- oretical exploration of the idea of endogenous productivity determination a la Acemoglu and Shimer (1997) as a determinant of earnings dispersion.

The theoretical apparatus that we use mixes Burdett and Mortensen's (1998) ideas about on-the-job search with Burdett and Judd's (1983) ideas about instant between-firm competition for workers through job offer recall. As was shown by Burdett and Judd (1983), marginal productivity payments occur only if workers (searching for a job) can simultaneously apply to at least two would-be employ- ers. If job offers do not systematically arrive at least in pairs, then equilibrium wages are equal to neither marginal productivity nor reservation wages but are necessarily dispersed, even among identical workers and firms. Relatedly, Burdett and Mortensen (1998) show that dispersion in equilibrium wages occurs with sequential search if workers can search on the job. Limited or costly job search thus appears to be a self-reinforcing source of wage dispersion. Costly search gives firms monopsony power, which in turn motivates the workers' search activ- ity because there always remains a hope of finding a better-paying job.

Structural estimations of equilibrium models of the labor market with double productive heterogeneity are rather uncommon. In this field, the contributions most commonly cited use the Roy (1951) model of self selection and earnings inequality where heterogeneous and imperfectly substitutable workers sort them- selves across various sectors requiring sector-specific tasks (e.g., Heckman and Sedlacek (1985), Heckman and Scheinkman (1987), and Heckman and Honore (1990)). The original Roy model is Walrasian and thus abstracts from labor mar- ket frictions. As a result of perfect labor mobility between sectors, it does not deliver any observed worker mobility in equilibrium because all workers instanta- neously go to their elected sector and stay there forever. This is clearly at odds with empirical evidence and again pleads in favor of models like ours that take

EQUILIBRIUM WAGE DISPERSION 2299

account of the existing obstacles to labor mobility. Search frictions are incor- porated into the Roy model of self selection in a recent paper by Moscarini (2000), who mainly focuses on the differences in search strategies across workers. Although very promising, this approach still involves too much analytical com- plexity to be empirically implementable. Our model has the drawback of treating the search strategies as essentially exogenous, its advantage being its ability to deliver quantitatively realistic earnings distributions and wage dynamics that can be successfully confronted by the data.5

Finally, a number of equilibrium job search models with heterogeneous work- ers and/or firms have been estimated. This literature was initiated by Eckstein and Wolpin's (1990) celebrated estimation of the Albrecht and Axell (1984) model. Recent additions include the estimation of the Burdett and Mortensen (1998) model by Van den Berg and Ridder (1998), and Bontemps, Robin, and Van den Berg (1999, 2000) (see Mortensen and Pissarides (1998) for a survey).

3. THEORY

In this section we describe a non-Walrasian model of a labor market with search frictions that will be brought to the data in the following sections.

3.1. Setup

3.1.1. Workers and Firms

We consider the market for a homogeneous occupation (manual workers, administration employees, managers, . . . ) in which a measure M of atomistic workers face a continuum of competitive firms, with a mass normalized to 1, that produce one unique multi-purpose good.

Workers face a constant birth/death rate A, and firms live forever. Newborn workers begin their working life as unemployed. The unemployment rate of a given category of labor is denoted by u. The pool of unemployed workers is steadily fueled by layoffs that occur at the exogenous rate 8, and by the constant flow ,uM of newborn workers.

Workers are homogeneous with respect to the set of observable characteristics defining their occupation-or equivalently the particular market on which they operate-but may differ in their personal "abilities," which are not observed by the econometrician. A given worker's ability is measured by the amount ? of efficiency units of labor she/he supplies per unit of time. Ability or professional efficiency s can be thought of as a function of the individual's human capital. However it is not a choice variable and there is no human capital accumula- tion over the life-cycle. Newborn workers are assumed to draw their values of ?

randomly from a distribution with cdf H over the interval [Emin, Emaxl We only

5 The model proposed by Moscarini only has two types of jobs and therefore cannot deliver quan- titatively realistic wage dynamics. Increasing the number of job types, although in principle not par- ticularly difficult, has an enormous cost in terms of tractability.

2300 F. POSTEL-VINAY AND J.-M. ROBIN

consider continuous ability distributions and further denote the corresponding density by h.6

Firms differ in the technologies that they operate. We make the simplifying assumption of constant returns to labor. More specifically, we assume that firms differ by an exogenous technological parameter p, with cdf F across firms over the support [Pmin, pma]. This distribution is assumed continuous with density y. The marginal productivity of the match (8, p) of a worker with ability E and a firm with technology p is Ep. The total per period output of a type-p firm is consequently equal to p times the sum of its employees' abilities.

A type-E unemployed worker has an income flow of Eb, with b a positive con- stant, which he has to forgo from the moment he finds a job. Being unemployed is thus equivalent to working at a "virtual" firm of labor productivity equal to b that would operate on a frictionless competitive labor market, therefore paying each employee her marginal productivity, Eb.7 We think of b as some measure of the unemployed workers' "bargaining power." Intuitively, the more produc- tive this virtual firm is, the more rent the workers can extract from their future matches with "actual" employers.

Workers discount the future at an exogenous and constant rate p > 0 and seek to maximize the expected discounted sum of future utility flows. The instanta- neous utility flow enjoyed from a flow of income x is U(x).8 Firms seek to min- imize wage costs.

At this point we should emphasize a fundamental assumption of this model, which is that of complete information. In particular, all heterogeneous agent types are perfectly observed by everyone in the economy, even though some of them are not observable by the econometrician. All wages and job offers are also perfectly observed and verifiable. The importance of this assumption will become clear when we discuss the wage formation mechanism below.

3.1.2. Matching

Firms and workers are brought together pairwise through a (possibly two- sided) search process, which takes time, is sequential, and is random.

Specifically, unemployed workers sample job offers sequentially at a Poisson rate AO. As in the original Burdett and Mortensen (1998) paper (hereafter BM), employees may also search for a better job while employed. The arrival rate of offers to on-the-job searchers is A1. The type p of the firm from which a given offer originates is assumed to be randomly selected in [Pmin, Pmax] according to

6 We fully characterize unobserved individual productive heterogeneity by a scalar index. This is a strong restriction that greatly simplifies both theory and estimation. For a recent attempt at con- structing an assignment model a la Roy with both search frictions and a bi-dimensional heterogeneity of workers, see Moscarini (2000).

7 The-admittedly restrictive-assumption that a worker's productivities "at home" and at work are both proportional to s greatly simplifies the upcoming analysis.

8 We rule out intertemporal transfers and savings and assume incomplete insurance markets. Risk averse individuals who want to smooth consumption over time would want to save and borrow. But this is a source of additional complexity with which we cannot yet cope.

EQUILIBRIUM WAGE DISPERSION 2301

a sampling distribution with cdf F (and F 1- F) and density f . The sampling distribution is the same for all workers irrespective of their ability or employment status.

The common usage in the job search literature is to assume a particular "matching technology" that precisely connects the sampling distribution to the distribution of firm types. Two extreme benchmark cases are the assumption of random matching (all firms have an equal probability of being sampled, implying f (p) = y(p); see BM, among others), and that of balanced matching (the proba- bility of being sampled is proportional to firm size, implying f (p) = ?(p), where ?(p) denotes the density of firm types in the population of employed workers; see Burdett and Vishwanath (1988).9 We stand somewhere in between those two extremes as we assume no a priori connection between the probability density of sampling a firm of given type p, f (p), and the density y(p) of such firms in the population of firms.

Assuming that all workers have the same sampling distribution independently of their ability and employment status may seem somewhat disputable. A possi- ble rationale is that it would go against anti-discrimination regulations for a firm to post an offer specifying a range of acceptable values of worker types, except for those that have been agreed upon by the collective agreements defining the marketed occupation. Our assumption typically rules out the existence of help- wanted ads reading "Economist wanted; three-digit-IQed applicants only." How- ever, it does not imply that employers do not discriminate between workers since we shall assume that employers condition their wage offers on worker character- istics. Firms are therefore unable to select workers ex ante, but they can do so ex post.

One may think of the search process as follows: workers go to job agencies and take the job offers posted by the highest p firms, because higher p's generate higher surpluses (see below). The probability for a given worker to contact a firm of a given p thus only depends on the number of ads posted by these firms. The sampling weights f (p)/Iy(p) can be interpreted as the average flows of ads posted by firms of productivity p per unit of time (or, more loosely as their "hiring effort"). This hiring effort is likely to be a decision variable of the firms. Yet, we only consider here the partial equilibrium conditional on a given distribution of these ratios across firms. We leave these ratios unrestricted and provide no theory to endogenize them. We just refer to two recent papers by Mortensen (1998, 1999) that bring together the search and matching strands of the microeconomic and macroeconomic literature on labor in a way that provides foundations for the individual employer/employee match formation process we assume here.10

9 Mortensen and Vishwanath (1994) also analyze a form of matching that mixes random matching and balanced matching by assuming that workers draw offers either by contacting firms (as under random matching) with a given probability, or by contact with employees (as under balanced match- ing) with one minus this probability.

10 Mortensen (1999) also considers another extension of the BM equilibrium search model. Work- ers are allowed to choose the effort they put into search according to their current state (unemployed

2302 F. POSTEL-VINAY AND J.-M. ROBIN

3.1.3. Wage Setting

We make the following important four assumptions on wage strategies: (i) Firms can vary their wage offers according to the characteristics of the

particular worker they meet. (ii) They can counter the offers received by their employees from competing

firms. (iii) Firms make take-it-or-leave-it wage offers to workers. (iv) Wage contracts are long-term contracts that can be renegotiated by

mutual agreement only. The first two assumptions are a departure from the standard BM model. They

naturally arise from the assumption of perfect information about the individual characteristics of matching counterparts. This is a disputable assumption. Yet, recruitment interviews definitely reveal some information about worker ability. Moreover, even in countries like France where strict regulations constrain the firms' layoff policies, the labor legislation generally allows for probationary peri- ods during which firms are free to let go their hirees at no (or minimal) cost. We therefore claim that perfect information is a valid alternative to the blindness of interacting agents in the BM model.

Second, even if information is perfect, there might exist limits to the extent to which firms can vary the wage they offer to workers. These limits could be legal restrictions like a minimum wage decided by the government or negotiated by trade unions. We leave to further work the analysis of the effects of such restric- tions on the wage setting mechanism. Although we recognize the importance of these effects, analyzing them within the context of a general dynamic equilibrium model is a complex problem that we shall not attack here.

Third, when an employee receives an outside offer of a wage greater than her current wage but lower than her marginal productivity, there is no reason why her current employer should let her leave the firm although such passive behavior is clearly suboptimal.1" Thus combining assumptions (i) and (ii), one sees that certain outside offers can be a source of wage increases within the firm for the employee who receives them.

The last two assumptions are more standard. Assumption (iii) imposes that workers have no bargaining power (in the sense of a Nash bargaining model). It is a restrictive assumption, usual though it may be in the equilibrium search literature.12 Assumption (iv) only ensures that a firm cannot unilaterally cancel

or not) and wage. Assuming a convex search cost results in a job offer arrival rate A1 that is a decreasing function of the current wage. This is an interesting extension of the basic model, which we do not consider in this paper as it would considerably increase the mathematical complexity of the equilibrium.

11 Firms could nonetheless be willing to avoid moral hazard problems with the rest of their employ- ees, for example by committing themselves not to matching outside offers in order to reduce their workers' search intensity and turnover. For a preliminary look into this problem, see Postel-Vinay and Robin (2001).

12 In a recent paper, Dey and Flinn (2000) consider a very similar setup in which, in addition, firms do not have all the bargaining power. Bringing together Nash bargaining and Bertrand competition is certainly a very interesting extension to consider in future work.

EQUILIBRIUM WAGE DISPERSION 2303

a promotion obtained by one of its employees after having received an outside job offer, once the worker has turned down that offer. It follows that wage cuts within the firm are not permitted. In the same line of ideas, note that there is no endogenous firing motive on this market because nothing can change in the firm's environment that would make a wage contract cease to be profitable to the firm if it previously was.

3.2. Wage Contracts

We now exploit the preceding series of assumptions to derive the precise values of the wage resulting from the various forms of employer-employee contacts.

The lifetime utility of an unemployed worker of type s is denoted by VO(E) and that of the same worker when employed at a firm of type p and paid a wage w is V(e, w, p). A type-p firm is able to employ a type-s unemployed worker if the match is productive enough to at least compensate the worker for his for- gone unemployment income, i.e. sp > sb. Therefore, the lower support of the distribution of marginal productivities of labor (mpl), Pmin, has to be no less than b, for a firm less productive than b would never attract any worker. When- ever that condition is met, any type-p firm will want to hire any type-? unem- ployed worker upon "meeting" him on the search market. To this end, the type-p firm optimally offers to the type-s unemployed worker the wage f0(s, p) that exactly compensates this worker for his opportunity cost of employment, which is defined by

(1) V(e, X0(?, P), P) = Vo(e).

Because a given employed worker's future employment prospects depend on both the type of firm at which he works and his personal ability, the minimum wage at which a type-s unemployed worker is willing to work at a given type-p firm depends on p and s, as shown by equation (1).

When a type-p firm's employee receives an outside offer from a type-p' firm, both firms enter a Bertrand competition won by the most productive firm. Con- sider this sort of auction over a worker s by a firm of productivity p and one of productivity p' > p. Since it is willing to extract a positive marginal profit out of every match, the best the firm of type p can do for its employee is to set his wage exactly equal to sp. The highest level of utility the worker can attain by staying at the type-p firm is therefore V(e, sp, p). Accordingly, he accepts to move to a potentially better match with a firm of type p' if the latter offers at least the wage f(s, p, p') defined by

(2) V(e, (s, p, p'), p') = V(e, Sp, p)-

Any less generous offer on the part of the type-p' firm is successfully countered by the type-p firm. Now, if p' is less than p, then 0(s, p, p') > sp', in which case the type-p' firm will never raise its offer up to this level. Rather, the worker will

2304 F. POSTEL-VINAY AND J.-M. ROBIN

stay at his current firm, and be promoted to the wage 4(e, p', p) that makes him indifferent between staying and joining the type-p' firm.

The precise value of 4(.) is derived in Appendix A.1 as:

(3) U()(E, P, P')) = U(EP) - f

| F(x)U '(x) dx.

Note that in comparison to standard search theory, we get an explicit definition of 4(e, p, p') from (3) instead of an implicit definition as the solution to an integral equation. This will greatly simplify the numerical computations in the empirical analysis.

Expression (3) has some rather intuitive features. The wage paid by firm p' is less than the maximal wage firm p can afford to pay, i.e. the marginal productiv- ity of the match sp. The difference between the two, measured by the integral term in (3) represents the option value of turning down the type-p firm to work at the type-p' firm. This option value increases with the productivity difference ?(p'- p). Workers indeed accept lower wages to work at more productive firms because, sp being an upper bound on any wage offer resulting from the compe- tition between the incumbent employer p and any challenger p', workers agree to trade a lower wage now for increased chances of higher wages tomorrow. It is thus more difficult to draw a worker out of a more productive firm, and equiv- alently workers are more easily willing to work at more productive firms. The option value further positively depends on the frequency of outside offers (A1) and the likelihood of high-p draws.'3 Symmetrically, it negatively depends on the overall job termination rate 8 + At, which tends to reduce the probability that an outside wage offer arrives before the match breaks up. Finally, the amount of intertemporal transfer negatively depends on the discount rate and the coeffi- cient of relative risk aversion. More myopic and more risk-averse individuals are indeed less keen on accepting such risky transfers.14

Finally, we also show in Appendix A.1, thanks to the assumption that the value of nonmarket time Eb has the same form as match productivities, that the wage offered by a firm of type p to a type-s unemployed worker is 40(E, p) = 0(s, b, p). Unemployed workers of all types are thus prepared to work for a wage 00 that is less than the opportunity cost of employment sb for the same intertem- poral arbitrage motive. Moreover, the reservation wage does not depend on the arrival rate of offers AO. In conventional search theory, reservations wages do depend on AO, because the wage offers are not necessarily equal to the reserva- tion wage. A longer search duration may thus increase the value of the eventually accepted job. Here, this does not happen: Firms always offer their reservation

13 For two sampling distributions F, and F2, if F, first-order stochastically dominates F2, then the wedge U(sp) - U(O(s, p, p')) is greater for F, than for F2.

14 These two concepts, time discounting and risk aversion, play a somewhat similar role in this model. Less risk averse individuals will have similar trajectories to more risk averse workers if they are at the same time more myopic. This conjecture will be corroborated by the empirical analysis below.

EQUILIBRIUM WAGE DISPERSION 2305

wages to workers. Therefore, there is no gain to expect from rejecting an offer and waiting for the following one.

We end this section by showing the form that equation (3) takes if the utility function is of the CRRA type:

(4) U(x) = l - , (if a > 0, a 0 1),

Inx (ifa=1),

where a, the rate of relative risk aversion, is between 0 and +oo. Equation (3) then becomes

(5) In 4(s, p, p')

ln ? + In 4(1, p, p')

ln ? ? 1 - ln[pl a- f p F(x)x -dx] (if a > 0, a 7 1),

ln ? + lnp _-,4/f F(X) ?x (if a= 1),

for any a. In this particular case of CRRA preferences, the model thus natu- rally delivers a log-linear decomposition of wages clearly separating the effect of ability on one side (ln s) and the effect of labor market history on the other

(ln 4(1, p, p')).

3.3. Wage Dynamics and Job Mobility

The following mobility patterns then naturally emerge from these wage setting mechanisms and are rigorously proven in Appendix A.1. Let us first define the threshold firm type q(e, w, p) by the equality

0(s, q(e, w, p), p) = w.

Given that 4(s, p', p) is an increasing function of p', it follows that 4(s, p', p) < w for all p' < q(e, w, p). The value q(e, w, p) is therefore the minimal mpl p' such that the Bertrand competition between firm p and firm p' for worker ? raises the worker's wage above w.

Now, consider a worker of type s currently employed by a firm of type p at wage w, and let this worker be contacted by a firm of type p'. Only one of the following three cases can occur:

(i) p' < q(e, w, p), and nothing changes. [The worker does not gain any- thing from this contact because the type-p incumbent employer could attract the worker out of a type-p' firm for a lower wage than w.]

(ii) p > p' > q(e, w, p), and the worker obtains a wage raise (s, p', p) - w > 0 from his/her current employer. [The current employer can match any offer of the challenging firm and the worker profits from the Bertrand competition between p and p' by getting a wage raise in firm p equivalent in present value terms

2306 F. POSTEL-VINAY AND J.-M. ROBIN

to being paid his marginal productivity sp' in the type-p' firm. Note that it is a dominant strategy for the weaker firm p' to challenge firm p. Indeed p' loses nothing if p counters and wins the worker if not.]

(iii) p' > p, and the worker moves to firm p' for a wage 4(e, p, p') that may be greater or smaller than w. [Firm p is no match to p' and loses its employee to firm p' at a wage that is equivalent to being paid at his previous marginal productivity Ep. If p' is large enough the worker may even accept a wage cut to move to p' (this happens whenever O(E, p, p') < w).]

The wage setting mechanism that we assume in this paper delivers interesting earnings profiles. First, individual within-firm wage-tenure profiles are nonde- creasing and concave in expectation terms. A longer tenure increases the prob- ability of receiving a good outside offer. On the other hand, workers with long tenures have on average received more offers and consequently earn higher wages. They are therefore less likely to receive an attractive offer that would result in a promotion.'5 Second, the model can generate firm-to-firm worker movements with wage cuts when the tenure profile in the new firm is expected to be increasing over a very long time span.

Comments about the similarities and differences between the wage equation generated by our model and a standard human-capital-theory-based wage equa- tion can be made at this point to help clarify the discussion. First note that the reason for which wages increase with tenure in our model is similar to a standard optimal contract type of explanation. In a standard Beckerian story, specific and general human capital accumulation by workers makes them increasingly valu- able to their employers as their seniority increases (see e.g. Topel (1991)). Since general human capital is portable across firms, senior workers also have higher alternative wages. It is then optimal for the employers to offer upward sloping wage-tenure contracts in order to prevent excessive turnover. Thus in fine, it is between-firm competition on the labor market that forces wages to increase with tenure.

In our model firm competition forces employers to grant wage raises to their employees through the mechanism of Bertrand competition. Consider the sequence of wages a worker of ability s obtains in our model in a same firm with mpl p when his/her tenure t varies: they are all of the form of f(E, qt, p). The effect of tenure is entirely reflected by the sequence of productivities qt of all the less productive employers that the worker was able to bring into competition with his/her incumbent employer.

Over a worker's lifetime, the sequence of p values marks the effect of experi- ence as reflected by job-to-job mobility.16 Ultimately then, even though there is

15 Formally, let w(t) denote the stochastic process (jump process) of wages indexed by tenure (conditional on the worker's s and the employer's p). We have

E[w(t + dt)-w(t)Iw(t) = w, no job mobility] = At dt E[max{(s, p', p)-w, O}Ip' < p]. Expected within-firm wage trajectories are therefore continuously increasing and concave as the above expression is positive, tends to zero with dt and decreases with w.

16 This interpretation works up to the fact that, in our model, unemployment acts as a "reset button" for experience since falling into unemployment is like going back to a firm with very low

EQUILIBRIUM WAGE DISPERSION 2307

no human capital accumulation in our model, workers can gradually find better technological support to their innate ability by climbing the ladder of p's, This source of wage dispersion is usually neglected in Mincerian models.17

3.4. Steady-state Equilibrium

The focal point of this section is the equilibrium distribution of wages, i.e. the distribution of wages that can be estimated from a cross-section of individual wages. We know from what precedes that an employee of type E of a firm of type p is currently paid a wage w that is either equal to 4(s, b, p) if w is the first salary after unemployment, or is equal to 4(s, q, p), with p < q < p, if the last wage mobility is the outcome of a price competition between the incumbent employer and another firm of type q. The cross-sectional distribution of wages therefore has three components: a worker fixed effect (s), an employer fixed effect (p), and a random effect (q) that characterizes the most recent wage mobility. The aim of this section is to determine the joint distribution of these three components.

In a steady state a fraction u of workers is unemployed and a density ?(e, p) of type-s workers is employed at type-p firms. Let e(p) = f'm f(., p) de be the density of employees working at type-p firms. The average size of a firm of type p is then equal to Me(p)/y(p). We denote the corresponding cdfs with capital letters L(s, p) and L(p), and we denote as G(wIs, p) the cdf of the (not absolutely continuous, as we shall see) conditional distribution of wages within the pool of workers of ability s within type-p firms.

We now proceed to the derivation of these different distributional parame- ters by increasing order of complexity. The steady state assumption implies that inflows must balance outflows for all stocks of workers defined by a status (unem- ployed or employed), a personal type s, a wage w, an employer type p. The relevant flow-balance equations are spelled out in Appendix A.2. They lead to the following series of definitions:

* Unemployment rate:

(6) u += a ? A0

* Distribution of firm types across employed workers: The fraction of workers employed at a firm with mpl less than p is

(7) L( F) ( p)

productivity b < Pmin This could still be interpreted as an extreme form of human capital depre- ciation caused by the occurrence of an unemployment spell. Moreover, this depreciation could be made less extreme by making unemployment income proportional to past wages.

17 Although we suspect that it would be empirically difficult to tell apart the share of the returns to experience due to increasing knowledge from that due to better available technologies without precise information on firms' technologies, a promising avenue for future research would be to embed explicit human capital accumulation into an equilibrium model of labor market frictions with both heterogeneous workers and heterogeneous firms. In this spirit, an extension of our model that deserves consideration is one in which individual ability could evolve over time.

2308 F. POSTEL-VINAY AND J.-M. ROBIN

and the density of workers in firms of type p follows from differentiation as

(8) f(p) = 1 + K, _ (p)1

with K1 = Al/(S + /) * Within-firm distribution of worker types: The density of matches (?, p) is

(9) f(s, p) = h(s)t(p).

* Within-firm distribution of wages: The fraction of employees of ability ? in firms with mpl p is

/10) G1 + KjF(p) 2 1 + K,L[q(8, w, p)] 2

(10) Gwis, x 1+ KlF[q(8, w, p)] 1k 1+ K,L(p) 2 Equation (6) is standard in equilibrium search models (see BM) and merely

relates the unemployment rate to unemployment in- and outflows. Equation (7) is a particularly important empirical relationship as it will allow

us to back out the sampling distribution F from its empirical counterpart L.18 Steady-state equilibrium conditions thus provide structural solutions to standard selectivity problems in empirical models of the labor market, as they relate the distribution of unobservables to that of observables. They allow for nonparamet- ric analyses when standard models for censored data rest on strong parametric or semiparametric, more or less ad hoc, assumptions.

The equilibrium average size of a firm of productivity p is Mf(p)/y(p). Equa- tion (8) implies that it is the product of two terms:

(11) MEm(p) M(1+ K1) f(p)

y(p) [1+K1F(p)]2 y(p)

The first term in the right-hand-side multiplication, M(1 + K1)/[1 + K1F(p)]2, increases with p, meaning that the higher p, the easier it is for a firm to win the Bertrand game: high-productivity firms have more market power and should be thus bigger. The second term, f (p)/y(p), is the hiring effort of a firm of type p. The way hiring effort varies with p is unspecified by the model, but one easily imagines that convex hiring cost could make it a decreasing function of p. The model therefore does not constrain firm sizes to be necessarily increasing with firm productivities as it would be the case with random matching (f (p) = y(p)). Nor does the most productive firm p necessarily drain the whole workforce, as would be implied by balanced matching (f(p) = ?(p) forces F(p) = 1).

Equation (9) implies that, under the model's assumptions, the within-firm dis- tribution of individual heterogeneity is independent of firm types. Nothing thus prevents the formation of highly dissimilar pairs (low s, high p, or low p, high s)

18 It is exactly the same equilibrium relationship as between the distribution of wage offers and the distribution of earnings in the BM model.

EQUILIBRIUM WAGE DISPERSION 2309

if profitable to both the firm and the worker. This results from the assumptions of constant returns to scale, scalar heterogeneity, and undirected search. Given that all operating firms have p > b and since it never happens that p beats p' for some s's and p' beats p for some others, all possible matches generate a positive surplus and there will always exist a wage acceptable for every worker-firm pair.

This result doesn't rule out assortative matching of workers and firms in a general sense: remember that we are considering a labor market for one partic- ular occupation. Going back to the labor market as a whole, it may very well be the case that the within firm distributions of the marketed professions vary sig- nificantly across firms. Our model merely predicts the absence of sorting within occupations.19

Finally, equation (10) expresses the conditional cdf of wages in the population of type-8 workers hired by a type-p firm. What the pair of equations (9, 10) shows is that a random draw from the steady-state equilibrium distribution of wages is a value 4(s, q, p) where (e, p, q) are three random variables such that:

(i) s is independent of (p, q), (ii) the cdf of the marginal distribution of s is H over [Emin, ?max], (iii) the cdf of the marginal distribution of p is L over [pminlPmai' and (iv) the cdf of the conditional distribution of q given p is G(. lp) over {b} U

[Pmin, P] such that

G(qlp) G(4(s, q, p)|E, p)

[1 + K,F(p)]2

[1+ K1F(q)]2

for all q E {b} U [Pmin, p]. The latter distribution has a mass point at b and is otherwise continuous over the interval [Pmin, P].

An interesting feature of the steady-state distribution of the triple (?, q, p) is that it does not depend on the form of the utility function.

3.5. Implications for the Decomposition of Log-wage Variance

Our goal in this final section of the theory part of the paper is to use what we have so far learned from the model about the distribution of wages to provide a fully interpretable decomposition of the cross-worker variance of (log) wages.

19 This result finds some empirical support. The somewhat limited available evidence about the correlation between worker and firm productive heterogeneity components indeed shows that the degree of sorting is in any case small, controlling for observed worker heterogeneity. AKM estimate a correlation between firm and worker effects of 0.08 in the French DADS panel (order-dependent estimation of the correlation between a and 4 in Table VI), and Abowd, Finer, Kramarz (1999) find essentially 0 using the Washington State Ul data. This result has recently been updated by Abowd and Kramarz (2000) who find that this overall absence of correlation between person and firm effects results from the addition of two opposite effects which cancel each other out: person effects and industry effects are positively correlated between industries but negatively correlated within industries.

2310 F. POSTEL-VINAY AND J.-M. ROBIN

We showed in the preceding section that all wages were particular realizations of a random variable 4(8, q, p), with (?, q, p), drawn as indicated at the end of Section 3.4. We also showed that, provided that the utility function is of the CRRA form (4), wages are proportional to worker types (equation (5)). The following identities immediately follow from those considerations:

E(lnwlp) = Elns+E[ln40(1, q, p)lp],

V(ln wlp) = V ln s + V[ln b(1, q, p)Ip],

where the expectations and variances are taken with respect to the relevant steady-state equilibrium distributions, as described in Section 3.4. A natural decomposition of the total variance of log wages thus arises from our model as follows:

(12) Vlnw=EV(lnwlp)+ VE(lnwjp)

= Vlns + VE(lnwlp) + (EV(lnwlp) - Vlns)

= Vlns +VE[ln4(1,q,p)1p] +EV[lnq(1,q,p)jp].

Person effect Firm effect Effect of market frictions

The first term (V ln s) in this decomposition is obviously interpreted as the con- tribution of dispersion in unobserved individual ability. We shall therefore refer to it as the "person effect." The second term (VE(ln wjp)) is the between-firm wage variance. It reflects the fact that some firms pay higher wages on average and thus contribute to individual wage dispersion. Even though this is admittedly abusive since q and p are not independent, it is also quite natural to label this term the "firm effect." The third term (EV(ln wIp) - V ln s) is the share of the within-firm wage variance which is not due to dispersion in individual ability. Its origin is clearly identified in the model: the reason why two workers of identical types working at identical firms can earn different wages is that the two work- ers had different draws of alternative wage offers. This particular source of wage dispersion is therefore the fact that firms compete to attract workers on a fric- tional labor market. Hence the name "effect of market frictions" that we give to the corresponding term in our log-wage variance decomposition.

4. DATA

4.1. The DADS Panel

The De'clarations Annuelles des Donne'es Sociales dataset is a large collection of matched employer-employee informations collected by the French Statistical Institute INSEE (Institut National de la Statistique et des Etudes Economiques- Division des Revenues). The data are based on mandatory employer reports of the earnings of each salaried employee of the private sector subject to French payroll taxes over one given year. (See AKM for a complete description of the DADS data.) Each yearly observation includes an identifier that corresponds to

EQUILIBRIUM WAGE DISPERSION 2311

the employee and an identifier that corresponds to the establishment. We also have information on the timing in days of the individual's employment spell at the establishment, as well as the number of hours worked during that spell. Each observation also includes, in addition to the variables listed above, the sex, month, year, and place of birth, occupation, total net nominal earnings over the year, and annualized gross nominal earnings over the year for the individual, as well as the location-region, departement ("district"), and town-and industry of the employing establishment. There is no information on education in the data, and the Census data used by AKM to get information on educational attainments are pretty useless in our case because the last available Census dates back to 1990 and many of the workers active during the 1990's were still at school in 1990.

To reduce the sample size, we use data for the region Ile-de-France (greater Paris) only.20 Moreover, we restrict the panel to the period 1996-1998, our last available survey. We have deliberately selected a much shorter period than is available because we want to find out whether it is possible to estimate our structural model over a homogeneous period of the business cycle. It would have been very hard indeed to defend the assumption of time-invariant parameters (the job offer arrival rate parameters in particular) had we been using a longer panel.

Moreover, to enhance the precision of the empirical moments (means, vari- ances) of the within-firm earnings distribution that will be needed in the estima- tion, we select only those workers employed at firms of size no smaller than five employees. We shall comment on this selection later in the paper.

Ideally, one would want to follow all the trajectories of all individuals employed by firms of size greater than 5 and operating in Ile-de-France in 1996 over the three-year period 1996-1998. However, for confidentiality reasons, INSEE pro- vides individual identifiers only for the subsample of individuals who were born in October of even-numbered years. The 1996-1998 panel that we shall use is therefore an exogenous selection of all available individual trajectories (about 1/20th). Note, however, that the exhaustive individual declarations are available, only without the individual identifiers. This is still useful to compute the exact distribution of wages within each establishment. Note that, because of attrition (workers retiring, or starting their own business, or becoming unemployed, or going to the public sector), only the initial cross-section forms a representative sample.

We construct seven datasets corresponding to seven different occupational categories: (i) executives, managers and engineers, (ii) administrative and sales supervisors, (iii) technical supervisors and technicians, (iv) administrative staff, (v) skilled manual workers, (vi) sales and service employees, and (vii) unskilled manual workers. Each observation specifies the following information col- lected from the employers' yearly records: (i) the individual's identifier, (ii) the employer's identifier, (iii) the year, (iv) yearly earnings, (v) the number (between

20 The region is Ile-de-France, and it comprises 8 departements (Paris, Seine et Marne, Yvelines, Essonne, Hauts de Seine, Seine-Saint-Denis, Val de Marne, Val d'Oise).

2312 F. POSTEL-VINAY AND J.-M. ROBIN

1 and 360) of the day when the record starts, (vi) the number of the day when it ends, and (vii) the number of hours worked in year (iii) by (i) in (ii) between day (v) and day (vi). By sorting the data by columns (i), (ii), (v), and (vi), one can thus construct a panel of individual trajectories. Note that there can exist several records for one single worker in one given year if the individual has changed employer several times in that year. Lastly, the wage variable that we shall use in the empirical analysis is the hourly wage rate.

Compared to a standard panel (NLSY, PSID, ...) the DADS panel keeps track of the employing establishment. This peculiarity allowed AKM to estimate an error component model with a double index (individual x establishment), and made possible a decomposition of log wages into three components: an individual component, a component for each establishment, and a residual term.

4.2. Descriptive Analysis of the Data

We start the descriptive analysis with a look at worker mobility patterns. The panel sample indicates for example that worker i was employed at establishment j during d days in 1996 within a time interval beginning this day of 1996 and ending that day of 1996. A trajectory featuring an employer change may be such that the end of one employment spell does not coincide with the beginning of the next one, and a worker may also leave the panel before the end of the recording period. There is no way of knowing the status of the worker during such periods not covered by a wage statement. He/she may have permanently or temporarily quit participating, or be unemployed, or have found a job in the public sector, or have started up his/her own business. In the estimation, we shall interpret temporary attrition as resulting from layoffs and permanent attrition as resulting from either layoffs or retirements. Moreover, we arbitrarily define a job-to-job mobility as an employer change with an intervening unemployment spell of less than 15 days.

Table I reports some statistics about worker mobility. It shows that, depend- ing on the occupational category, 42 to 55 per cent of the workers stayed in the same job over the entire recording period of 3 years, while only 5 to 23 per cent changed jobs without passing through a period of unemployment. Job-to-job mobility therefore appears to be rather limited in this period, which corresponds to the end of a recession, in spite of the fact that job-to-job mobility (and worker mobility in general) is usually found much more substantial around Paris than in the rest of France. Concerning the mobility between employment and nonem- ployment, the sample mean employment duration (which is censored at 3 years) is close to 2 years for all worker categories, while the median of that same dura- tion (not reported here) is above 3 years for all categories. The sample mean

21 The least-squares estimation of AKM requires many years of observations as the individual and firm fixed effects are identified only from mobility. Over the 1976-1987 period of their observation sample, 90% of individuals change employers 3 times or less. A three-year panel would therefore yield very imprecise estimates.

EQUILIBRIUM WAGE DISPERSION 2313

TABLE I

DESCRIPTIVE ANALYSIS OF WORKER MOBILITY

Percentage whose first

Number Percentage with recorded mobility is from job... Sample mean Sample mean of indiv. no recorded ... to-out unemployment employment

Occupation trajectories mobility (%) ... to-job (%) of sample (%) spell duration spell duration

Executives, managers, 22,757 46.2 23.4 30.4 0.96 yrs 2.09 yrs and engineers

Supervisors, administrative, 14,977 48.1 19.3 32.5 1.16 yrs 2.11 yrs and sales

Technical supervisors 7,448 55.5 16.0 28.6 1.07 yrs 2.28 yrs and technicians

Administrative support 14,903 54.3 8.2 37.5 1.30 yrs 2.23 yrs Skilled manual workers 12,557 55.9 5.2 38.9 1.16 yrs 2.28 yrs Sales and service workers 5,926 45.1 5.5 49.4 1.28 yrs 2.06 yrs Unskilled manual workers 4,416 42.5 7.0 50.5 1.29 yrs 1.98 yrs

duration of nonemployment lies between 12 and 14 months, while its median (not reported here) is close to one year for all categories.

To reassure ourselves that it is legitimate to consider the sole region Ile-de- France as a self-contained labor market, we can look at cross-regional worker mobility. Looking at the sequence of employer locations for all workers in the panel, we find that only 4.7 percent of them leave Ile-de-France during the record- ing period. Cross-regional mobility is therefore extremely limited over the period considered, and we can safely ignore it.

Finally, we may want to look at the stability of our occupational categorization of workers. We use the loosest available classification (next to pooling all work- ers together in a single class), which contains 7 categories (see above). It turns out that in total 81.3 per cent of the workers do not change category over the recording period, and close to 4 per cent change twice or more. A more detailed look at those mobility patterns shows that the mobility is notably due to skilled white collars becoming executives, and unskilled blue collars becoming skilled blue collars.

We now turn to a description of wage mobility. Table II displays some infor- mation about the wage changes experienced by workers after their first recorded job-to-job mobility. The nominal wages available in the data were deflated using the Consumer Price Index (+1.23% in 1996 and +0.7% in 1997). The reported statistics include medians and 5 selected quantiles of the distribution of wage changes in the relevant population of workers. We see on that table that, even though the median wage variation after a job-to-job mobility is practically always positive, between 36 and 55 per cent of workers changing jobs do it at the price of a wage decrease. This observation confirms our initial feeling that it was impor- tant to model a wage setting mechanism allowing for such wage cuts due to job changes.

Table III reports similar information about the wage changes experienced between January 1, 1996 and December 31, 1997 for workers who held the same

2314 F. POSTEL-VINAY AND J.-M. ROBIN

TABLE II

VARIATION IN REAL WAGE AFTER FIRST RECORDED JOB-TO-JOB MOBILITY (I.E. WITH LESS THAN 15 DAYS WORK INTERRUPTION) IN 96-98

Median % obs. such that A log wage <

Occupation Nb. obs. Alog wage (%) -0.10 -0.05 0 0.05 0.10

Executives, managers, and engineers 5,335 3.1 23.6 28.5 38.1 55.1 65.4 Supervisors, administrative, and sales 2,893 3.7 21.6 27.1 36.6 54.3 65.2 Technical supervisors and technicians 1,190 3.8 14.0 20.2 32.2 55.5 67.3 Administrative support 1,222 2.2 21.5 28.7 40.7 60.5 69.2 Skilled manual workers 657 0.5 33.2 37.7 49.2 62.3 72.0 Sales and service workers 326 1.4 31.3 37.7 45.1 58.0 67.5 Unskilled manual workers 310 -1.3 33.5 42.9 54.5 63.4 72.3

job over this period. Indeed, we have several wages recorded for the same indi- vidual in the same firm-establishment if the worker stays employed by one firm for more than one year. Unfortunately, there is no way to know exactly at which moment he/she experienced a wage increase if the daily wage reported one year is greater than the one reported the year before. As the table shows, it frequently happens (around 30 per cent of the times, depending on worker categories) that real wages decrease from one year to the next even when the worker has not changed employers. Obviously, our model cannot deliver such downward wage changes. They may reflect fluctuations of bonuses with the firm's activity since there is no way of separating contractual wages from bonuses, which in some cases may be a nonnegligible share of remunerations. Wage changes may also reflect occupation changes within the same establishment and compensating dif- ferentials. These wage fluctuations could be captured in the model in an ad hoc way by a pure idiosyncratic shock. Nevertheless, we prefer to estimate the struc- tural model as it was laid out in the preceding sections at the price of a lack of fit because our main goal here is precisely to evaluate the ability of the struc- tural model to reproduce the main features of the dynamics of wages. Incorpo- rating productivity fluctuations into the model is certainly not a straightforward

TABLE III

VARIATION IN REAL WAGE BETWEEN 01/01/96 AND 31/12/97 WHEN HOLDING THE SAME JOB OVER THIS PERIOD

Median % obs. such that A log wage <

Occupation Nb. obs. Alog wage (%) -0.10 -0.05 0 0.05 0.10

Executives, managers, and engineers 16,102 2.7 6.6 11.3 28.5 64.4 80.0 Supervisors, administrative, and sales 15,592 2.6 7.9 12.9 28.6 65.2 81.1 Technical supervisors and technicians 5,644 2.5 6.6 11.9 29.6 68.1 85.0 Administrative support 11,105 2.2 7.9 12.4 30.0 69.8 84.2 Skilled manual workers 9,747 1.9 7.9 15.0 34.9 69.5 85.1 Sales and service workers 4,192 2.5 7.4 12.8 31.4 64.5 79.1 Unskilled manual workers 2,847 2.2 7.7 14.6 32.9 66.4 81.9

EQUILIBRIUM WAGE DISPERSION 2315

extension, as we know that it generates endogenous job destruction (see e.g. Mortensen and Pissarides (1994)).

5. ESTIMATION METHOD

The aim of this section is to show how the data we have just described can be used with a given specification of the utility function U(.) to provide non- parametric estimates of the distributions of individual abilities and firm marginal labor productivities, together with the other one-dimensional parameters of the model, namely the transition rates 8, ,u, AO, A1, and the discount rate p.

We shall restrict our attention to utility functions of the CRRA form (4) and normalize EU(E) to 0.22 As we saw in the theory part, this specification allows for a multiplicative separation of individual and firm effects within the wage function: 4O(, q, p) = E4(1, q, p).

The discrete nature of the data, the fact that all individual wage records are aggregated within each calendar year, implies a complicated censoring of the continuous-time trajectories generated by the theoretical model. Maximum like- lihood therefore fails as a potential candidate for an estimation method. We develop an alternative multi-step estimation procedure in the spirit of that pro- posed by Bontemps, Robin, and Van den Berg (2000) to estimate the BM model. The estimation procedure separates the parameters that can be estimated from a cross-section of wages (the heterogeneity distributions) from the parameters requiring transition data for identification (the transition rates AO, A1, 8, and ,u).

We prefer the multi-step estimation method to a more efficient, one-step, full- information estimation method even in a parametric context, because it allows better control of which data are used to identify and estimate which parameter. We know indeed that full-information estimation guarantees efficiency only if the model is correctly specified, but can be a source of considerable bias otherwise.23

5.1. Notation

The previously described 96-98 DADS panel is a set {(wit, fi, D?, Di`), i = 1, ... , N, t = 1, . . . , Ti}, where i indexes workers and t indexes administrative records, i.e. wit is the real wage rate paid by employer ftt E {1,. . . , M} to worker iE {1,. . , N} during the time interval [DO, D' ] (with Do, DXE{1,..., 3 x 360} in daily time units) covered by the tth administrative record. Note that there may exist more than one record in the same year of observation. The number of

22 That is: EU(s) = f U(s)h(s) d? = 0, implying that E,1-a = 1. -,min 23 For example, the transition parameter A1 contributes to the distributions of both durations and

cross-sectional wages. Suppose that the theoretical restrictions on the form of the earnings distribu- tion fails to fit the data well. Then a full-information estimation method could use the parameter A1 to improve the fit of the model's earnings distribution with the data at the cost of a reduced fit with the duration data. This is why we prefer to identify A1 from duration data and impose it afterwards in the estimation of the parameters that are specific to the wage distribution.

2316 F. POSTEL-VINAY AND J.-M. ROBIN

observations per worker, Ti, may thus vary across workers depending on attrition (interrupted records such that D? 1 > Dt + 15 for some t) or mobility (more than one employment spell in the same year: D' t?1-D?< 360 for some t). There are as many datasets as we distinguish occupational categories (seven). For the sake of notational simplicity we do not index observations by the corresponding occupation.

The subsample {(wil, f1l, Do, Dil), i = 1, . . . , N} is exhaustive of all employed workers in the Paris region working at firms of size at least equal to five, but the variables (Wit, ftt, DO, D 1 ) for t > 1 are missing for about 19 out of 20 randomly selected workers.

To circumvent the difficulty of describing the time aggregation process implied by the raw data, we limit our estimation sample to the set {(wi, , d1i, vi, d2i); i- 1,. . , N}, where:

(i) wi =wi1, f_ fil are the wage and firm identifier characterizing the first record for individual i (at least one exists),

(ii) dli is the length of the uninterrupted time span over which worker i is observed working at firm fi, which we compute as

Ti

dli = D' - Do + E I{ft = fi, Dot < Dil t_1 + 15} x (D' -DO?) t=2

(1{ } is the indicator function), (iii) vi is 1 or 0 depending on whether or not the declared wages are equal

in all records covered by the first employment spell of length d1l (it thus indi- cates whether the worker has received zero or at least one wage raise during his employment period at firm fi), and

(iv) d2i is the time spent out of the sample before a possible re-entry. The wage observations that are not used for the estimation will be used subse-

quently to assess the ability of the estimated model to reproduce individual wage dynamics.

Finally, let Ij denote the set of identifiers of the workers employed at any firm j, j = 1, . . . , M. We denote by yj the mean earnings utility of employees of firm j: yj = (1/#Ij) Ei,j JU(wi), where #Ij is the cardinal of set Ij (i.e. the size of firm j), and as pj the unobserved mpl of firm j. We also denote as si the unobserved ability of worker i.

5.2. Identifying Assumptions

In addition to all the assumptions already explicitly or implicitly stated in the theory, the estimation procedure rests on the following identifying assumptions:

IDENTIFYING ASSUMPTION 1: The set {wi, i = 1, . . . , N} is a set of N inde- pendent draws from the steady-state equilibrium wage distribution.

This first assumption is relatively innocuous. It amounts to assuming that a cross-section of yearly earnings is a good approximation of a cross-section of

EQUILIBRIUM WAGE DISPERSION 2317

instantaneous earnings rates. It neglects all wage changes within one year that are not recorded in the administrative data.

IDENTIFYING ASSUMPTION 2: At the theoretical steady-state, the conditional mean earnings utility y(p) _ E[U(w) Ip] is a strictly increasing function of the firm's mpl p.

The second assumption is restrictive but likely to be true. In order to identify the unobserved mpl pj for each firm j, without a long enough panel of wages to estimate firm effects from mobile workers,24 we need to rely on the assump- tion that there exists a moment of the within-firm wage distribution that is in a one-to-one relationship with p. What is more arbitrary is the choice of which moment to use. There are two obvious choices: firm size and firm mean earn- ings utility (mean wage or mean log wage). We discard the first choice because the theoretical value of the steady-state size of a firm with productivity p is a function of the sampling weight f (p)/ly(p) which, in the absence of any convinc- ing theory of matching, need not be a monotonic function of productivity (see below Section 6.7). Mean earnings utilities per firm appears as a better choice, if only because the average wage per firm would be the OLS estimate of the firm effect in a wage equation with firm unobserved heterogeneity. It thus seems nat- ural to use this estimator to retrieve the structural firm heterogeneity variable. For this empirical strategy to work, within-firm mean earnings utility must be a monotonic function of the firm mpl p.

In Appendix A.3 we derive the steady-state equilibrium conditional expectation of any function T(w) of the wage paid by a firm of type p to any of its employees taken at random. Clearly, the simplest formula is obtained for T(w) = U(w), in which case one has:25

(13) E[U(w)lp] = U(p) - [1 + K1F(p)]2 l (1-K)K1F(q) U'(q) dq,

where o- = p/(p +8 + /i). The function y(p) = E[U(w) Ip] is locally increasing at p if and only if

y'(p) = -(1 -o-)KjF(p)U'(p) + 2K4f(p)[1? + KF(p)]

fP 1 + (1- u)K,F(q) U'(q)d 0 'b

[1 +K,F(q)]2

24 We are definitely not yet capable of estimating our structural model using a long panel like AKM or Abowd and Kramarz (2000). Remember that they assume a simple static, linear error component model and they already face huge numerical difficulties. Adding nonlinearities and dynamics, as in our model, is beyond reach for the time being.

25 In the sequel, all mathematical expectation signs refer to the steady-state equilibrium distribution derived in the theoretical section.

2318 F. POSTEL-VINAY AND J.-M. ROBIN

If there is a nonmonotonicity problem, it can thus only occur at the left end of the support of p (the negative contribution to the positivity of the derivative is proportional to a decreasing function of p: F(p)U'(p)). In particular, for Pmin,

Y (Pmin) > ? E<~ f (Pmin) > 21 (1 --)K1 U'(Pmin) > 0 ~~~ 2 1 + (1 - O-)K1 U(Pmin) - U(b)'

which implies that the left tail of the sampling distribution of p must not be too thin. It will hold true if workers are sufficiently myopic (o- large), or if U(Pmin) - U(b) is large enough, or if on-the-job turnover is limited (K1 small). Note that in particular, under this identifying assumption, Pmin is strictly greater than b.

IDENTIFYING ASSUMPTION 3: There are no sampling errors in the computation of within-firm mean earnings utilities y1.

The third identifying assumption, together with Identifying Assumption 1, means that the empirical measure y, is exactly equal to the theoretical condi- tional expectation of individual earnings utilities within firm j: yj = y(pj). Firms with greater observed values of mean earnings utilities must also have greater productivity values, and firms with close values of mean earnings utility must also have close productivity values. Identifying Assumption 2 then allows identifica- tion of pj from yj by inverting function y(.). We denote p(.) = y-1 )

How acceptable is Identifying Assumption 3? Sampling errors are related to firm sizes #Ij and within-firm wage dispersions. The greater the size, the smaller the error. But the distribution of firm sizes is highly concentrated in the region of small sizes (but still displays very long tails). Therefore, the existence of sampling errors is something that should be taken care of. Unfortunately, our nonparamet- ric estimation method cannot cope with an additional measurement or sampling error to be added to the three theoretical stochastic components of wages (per- son, firm, and friction effects). To limit the sampling errors, we only retain the firms of size greater than five in our sample.26 A more severe trimming (more than ten, twenty.... ) does not change the results very much, as opposed to any less severe selection (more than two for example). Firm size greater than five thus seems a good compromise.27

26 Dropping wage observations for employees of establishments employing strictly less than five workers of the same occupation trimmed 18% of individual wage observations for higher managers and engineers, 26% for lower managers, 24% for technicians, 25% for administrative employees, 40% for sales and service workers, 29% for skilled blue collars, and 32% for unskilled blue collars. The selection on establishments is quite considerable since about 83%-88% of all establishments, depending on the occupation, are thus withdrawn from the estimation sample. As usual, the fact that most establishments employ a very small number of workers is hard to cope with using our models where firms are continuous sets of workers.

27 In comparison, notice that AKM also estimate the fixed effects by least-square methods that are only asymptotically consistent. Moreover, the fixed effects are only estimated for mobile workers, which therefore implies an endogenous selection similar to the one to which we proceed. Lastly, in the ten-year panel that they use, only 8% of the workers have changed employers strictly more than three times and 19% strictly more than twice (see Table 1 in AKM, p, 267). The individual fixed effects are therefore very imprecisely estimated.

EQUILIBRIUM WAGE DISPERSION 2319

5.3. Outline of the Estimation Method

To preserve the paper's readability, we confine the full description of the some- what complex estimation procedure to Appendix B. Here we only describe its main logic, which goes through the following stages:

(i) We first estimate the transition parameters 8, ,u, AO. and A1 by maximizing the likelihood of individual observations (d1i, 6, d2i), i = 1, .. ., N, conditional on the mean earnings utilities Yf, within firms fi. In writing this conditional likeli- hood function, we use equation (7) to replace anywhere it is needed the sampling cdf F(pf.) by

F(p(yf.)) = (1 + Kj) L(p(yf.)) 1 + K,L(p(yf.)

where L(p(yf.)) Z(yf.) is the cdf of the distribution of firms' yj's across work- ers, which can be nonparametrically and consistently estimated using the cross section of matched employer-employee data {(wi, f ), i = 1, . . . , N}.

(ii) Next, we use the identifying restriction on mean earnings utilities and pro- ductivities: yj = y(pj), to obtain a semiparametric estimate of pj given yj by inverting the theoretical function p - y(p) = E[U(w)lp]. Note that the com- putation of y(p) requires a value of the workers' discount rate p. Now, remem- ber that the discount rate conditions the option value component of the wage function O(E, q, p), and is, as such, a determinant of within-firm wage disper- sion. It is thus also estimated at this stage, together with the cross-sectional vari- ance of individual abilities transformed by U, VU(si), by fitting within-firm mean squared earnings utilities, ( j/#Ij) EiE,j U(Wi)2, with their theoretical counter- parts, E[U(w)21p = pj]' for all firms j.