Epic research special report of 19 aug 2015

8

DAILY REPORT 19 th AUG. 2015 YOUR MINTVISORY Call us at +91-731-6642300 Global markets at a glance A 6.0 percent tumble in Chinese shares on Tuesday, and weak earnings from Wal-Mart pressured US stocks and copper prices saw six year lows. Chinese stocks earlier plunged on concerns that companies may pull more money out of China as economic growth slows, lowering earnings for U.S. and European companies dependent on revenue from China. The Shanghai Composite Index closed down 6.1% at 3,749.12 points in its biggest daily decline since July 27, after recovering for 3 days. The CSI300 index .CSI300 of the largest listed companies in Shanghai and Shenzhen fell 6.2% at 3,825.41. Wal-Mart Stores Inc, the world's largest retailer by reve- nue, saw its stock fall 3.4 percent to USD 69.48, and was the biggest drag on both the Dow Jones Industrial Average and S&P 500 stock index, after reporting weaker-than- expected quarterly earnings and lowering its full-year fore- cast. The DJI average fell 33.84 points, or 0.19%, to 17,511.34, the S&P 500 dropped 5.52 points, or 0.26%, to 2,096.92 and the Nasdaq declined 32.35 points, or 0.64%, to 5,059.35. MSCI's broadest index of Asia-Pacific shares outside Japan .MIAPJ0000PUS was down 1.2% after hitting its lowest since July 2013. Japan's Nikkei .N225 dipped 0.3%. MSCI's all-country world stock index eased 0.31%. Britain's FTSE 100 closed down 0.4% Previous day Roundup It was another day of consolidation on Dalal Street as eq- uity benchmarks started the session on a positive note but wiped out those gains in afternoon trade to close margin- ally lower, weighed down by crash in Chinese shares. Sen- sex fell 46.73 pts to 27831.54. The 50-share NSE Nifty de- clined 10.75 pts to 8466.55 after hitting an intraday high of 8525.75 and low of 8433.60. However, the broader mar- kets outperformed benchmarks, supported by retail and HNIs. The BSE Midcap gained 0.5% and Smallcap rose 0.9%. The market breadth remained positive throughout the ses- sion as about 1633 shares advanced against 1234 shares declined on the BSE. Index stats The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [up 131.25pts], Capital Goods [up 157.05pts], PSU [down 35.03pts], FMCG [down 4.19pts], Realty [down 4.45pts], Power [down 3.38 pts], Auto [up 116.58Pts], Healthcare [down 102.37Pts], IT [up 186.89pts], Metals [down 151.90pts], TECK [up 60.92pts], Oil& Gas [down 0.79pts]. World Indices Index Value % Change D J l 17511.34 -0.19 S&P 500 2096.92 -0.26 NASDAQ 5059.35 -0.64 FTSE 100 6526.29 -0.37 Nikkei 225 20448.50 -0.52 Hong Kong 23427.51 -0.20 Top Gainers Company CMP Change % Chg BPCL 898.50 33.35 3.85 TATASTEEL 252.40 5.65 2.29 TCS 2,745.95 61.20 2.28 MARUTI 4,647.90 98.10 2.16 TECHM 563.45 11.55 2.09 Top Losers Company CMP Change % Chg GAIL 329.30 15.75 -4.56 COALINDIA 363.60 16.25 -4.28 NMDC 95.35 3.70 -3.74 CAIRN 150.00 4.25 -2.76 CIPLA 685.00 18.15 -2.58 Stocks at 52 Week’s HIGH Symbol Prev. Close Change %Chg ADANIPORTS 362.90 4.60 1.28 AUROPHARMA 785.05 1.65 0.21 CEATLTD 1,118.25 49.05 4.59 INFY 1,162.50 20.35 1.78 MARUTI 4,647.90 98.10 2.16 Indian Indices Company CMP Change % Chg NIFTY 8466.55 -10.75 -0.13 SENSEX 27831.54 -46.73 -0.17 Stocks at 52 Week’s LOW Symbol Prev. Close Change %Chg AMTEKAUTO 128.40 -4.85 -3.64 HINDALCO 88.60 -2.05 -2.26 ONGC 260.70 -3.30 -1.25

-

Upload

epic-research-private-limited -

Category

Business

-

view

28 -

download

1

Transcript of Epic research special report of 19 aug 2015

DAILY REPORT

19th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

Global markets at a glance A 6.0 percent tumble in Chinese shares on Tuesday, and weak earnings from Wal-Mart pressured US stocks and copper prices saw six year lows. Chinese stocks earlier plunged on concerns that companies may pull more money out of China as economic growth slows, lowering earnings for U.S. and European companies dependent on revenue from China. The Shanghai Composite Index closed down 6.1% at 3,749.12 points in its biggest daily decline since July 27, after recovering for 3 days. The CSI300 index .CSI300 of the largest listed companies in Shanghai and Shenzhen fell 6.2% at 3,825.41. Wal-Mart Stores Inc, the world's largest retailer by reve-nue, saw its stock fall 3.4 percent to USD 69.48, and was the biggest drag on both the Dow Jones Industrial Average and S&P 500 stock index, after reporting weaker-than-expected quarterly earnings and lowering its full-year fore-cast. The DJI average fell 33.84 points, or 0.19%, to 17,511.34, the S&P 500 dropped 5.52 points, or 0.26%, to 2,096.92 and the Nasdaq declined 32.35 points, or 0.64%, to 5,059.35. MSCI's broadest index of Asia-Pacific shares outside Japan .MIAPJ0000PUS was down 1.2% after hitting its lowest since July 2013. Japan's Nikkei .N225 dipped 0.3%. MSCI's all-country world stock index eased 0.31%. Britain's FTSE 100 closed down 0.4% Previous day Roundup It was another day of consolidation on Dalal Street as eq-uity benchmarks started the session on a positive note but wiped out those gains in afternoon trade to close margin-ally lower, weighed down by crash in Chinese shares. Sen-sex fell 46.73 pts to 27831.54. The 50-share NSE Nifty de-clined 10.75 pts to 8466.55 after hitting an intraday high of 8525.75 and low of 8433.60. However, the broader mar-kets outperformed benchmarks, supported by retail and HNIs. The BSE Midcap gained 0.5% and Smallcap rose 0.9%. The market breadth remained positive throughout the ses-sion as about 1633 shares advanced against 1234 shares declined on the BSE. Index stats The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [up 131.25pts], Capital Goods [up 157.05pts], PSU [down 35.03pts], FMCG [down 4.19pts], Realty [down 4.45pts], Power [down 3.38 pts], Auto [up 116.58Pts], Healthcare [down 102.37Pts], IT [up 186.89pts], Metals [down 151.90pts], TECK [up 60.92pts], Oil& Gas [down 0.79pts].

World Indices

Index Value % Change

D J l 17511.34 -0.19

S&P 500 2096.92 -0.26

NASDAQ 5059.35 -0.64

FTSE 100 6526.29 -0.37

Nikkei 225 20448.50 -0.52

Hong Kong 23427.51 -0.20

Top Gainers

Company CMP Change % Chg

BPCL 898.50 33.35 3.85

TATASTEEL 252.40 5.65 2.29

TCS 2,745.95 61.20 2.28

MARUTI 4,647.90 98.10 2.16

TECHM 563.45 11.55 2.09

Top Losers

Company CMP Change % Chg

GAIL 329.30 15.75 -4.56

COALINDIA 363.60 16.25 -4.28

NMDC 95.35 3.70 -3.74

CAIRN 150.00 4.25 -2.76

CIPLA 685.00 18.15 -2.58

Stocks at 52 Week’s HIGH

Symbol Prev. Close Change %Chg

ADANIPORTS 362.90 4.60 1.28

AUROPHARMA 785.05 1.65 0.21

CEATLTD 1,118.25 49.05 4.59

INFY 1,162.50 20.35 1.78

MARUTI 4,647.90 98.10 2.16

Indian Indices

Company CMP Change % Chg

NIFTY 8466.55 -10.75 -0.13

SENSEX 27831.54 -46.73 -0.17

Stocks at 52 Week’s LOW

Symbol Prev. Close Change %Chg

AMTEKAUTO 128.40 -4.85 -3.64

HINDALCO 88.60 -2.05 -2.26

ONGC 260.70 -3.30 -1.25

DAILY REPORT

19th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

STOCK RECOMMENDATION [CASH]

1. RAJESH EXPORTS (CASH)

After consolidating in last three session today RAJESHEXPO made new life time high of 615 and finished at 605.95 with 5.76% gain since RSI at 72 so we can see more upside for that long it above 616 for target of 621-630-640 use strict stop loss of 605

MACRO NEWS

Coal prices fall to 12-year lows as China, India join de-mand slowdown

India to see 2,500 MW addl solar power capacity: Report

PM pledges Rs 1.65L cr pkg at Bihar rally, takes on Nitish

Govt feels onion heat, asks MMTC to import 10K tonnes

Govt to ease FDI norms in e-commerce

MMTC Floats Tender To Import 60,000 Tonnes Of Aus-tralian Coking Coal For Oct/Nov Delivery Govt Asks MMTC To Import 10,000 Tonnes Of Onion; Directs NAFED To Cancel Its Tender:

Hero MotoCorp R&D spends rise six-fold in fiscal 2015

Aam Admi Party demands action against power distribu-tion companies on leaked CAG report

Aluminium producers to meet PMO to press for import duty hike

TRF Bags Rs 73.90 crore order from BHEL

CIL to seek shareholders' nod to extend CMD's tenure till 2017

Vedanta's Goa mine may restart iron ore export to China

Birlas oppose Lodha-led acquisition of 2 cement units

Coal India to tweak e-auctions to check falling prices

Commerce Ministry may set up think-tank for pharma-ceutical sector

STOCK RECOMMENDATIONS [FUTURE] 1. VEDL [FUTURE]

Today Metal sector share finished with mixed side in that VEDL future finished with 2% loss in last three session it is consolidating around 101 while it made low of while in de-rivative it made life time low of 99.25 Since Nifty it also near to Resistance so at this time if it break this level then we can see vertical fall so we advise to sell it below 101.40 with strict stop loss 103.10 for target of 100.10-99-97.

2. ABIRLANUVO [FUTURE]

ABIRLANUVO Future finished with bearish candle on EOD chart it create double top formation and in last two trading session it correct from 2340. RSI has given crossover so we advise to create short position around 2290-2300 with strict stop loss of 2340 for target of 2260-2230 if it hit second tar-get then it can be positional short for target of 2100.

DAILY REPORT

19th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

FUTURE & OPTION

MOST ACTIVE PUT OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY CE 8,400 49.70 8,32,051 42,12,050

NIFTY CE 8,500 90.00 7,47,108 25,34,025

BANKNIFTY CE 18,500 123.00 72,375 5,36,725

SBIN CE 270 1.90 7,067 32,88,000

SBIN CE 280 4.95 5,553 30,67,000

ASHOKLEY CE 90 0.50 4,630 38,72,000

TATASTEEL CE 250 5.50 3,204 11,89,000

TATASTEEL CE 240 2.25 3,047 13,79,000

MOST ACTIVE CALL OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY PE 8,500 69.85 9,87,106 38,73,150

NIFTY PE 8,700 12.00 7,79,758 44,62,150

BANKNIFTY PE 19,000 159.50 78,766 6,57,000

SBIN PE 300 2.15 10,939 59,05,000

ASHOKLEY PE 100 1.80 10,726 39,44,000

INFY PE 1,200 7.95 5,537 5,97,500

TATASTEEL PE 260 3.60 5,253 25,24,000

FII DERIVATIVES STATISTICS

BUY OPEN INTEREST AT THE END OF THE DAY SELL

No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores NET AMOUNT

INDEX FUTURES 54674 1299.43 52571 1280.47 592820 14171.63 18.96

INDEX OPTIONS 512308 12720.33 490694 12042.05 2961998 77686.75 678.28

STOCK FUTURES 115519 3381.23 103636 2973.47 1929618 53115.38 407.75

STOCK OPTIONS 88732 2551.87 91229 2608.75 149777 4055.89 -56.88

TOTAL 1048.10

STOCKS IN NEWS SBI says merger with its associate on hold Rajesh Exports bags Rs 1,170 crore order from UAE for

gold, diamond-studded jewellery Power Grid to commission Rs 12,000-crore Assam-Agra

line by month-end DLF sells land parcel in Kochi for Rs 111 cr Jindal Saw To Seek Shareholder Nod To Raise Up To

`1,000 Cr Via NCDs On Sep 18 IOC set to exceed its capex target of `56200 cr by end

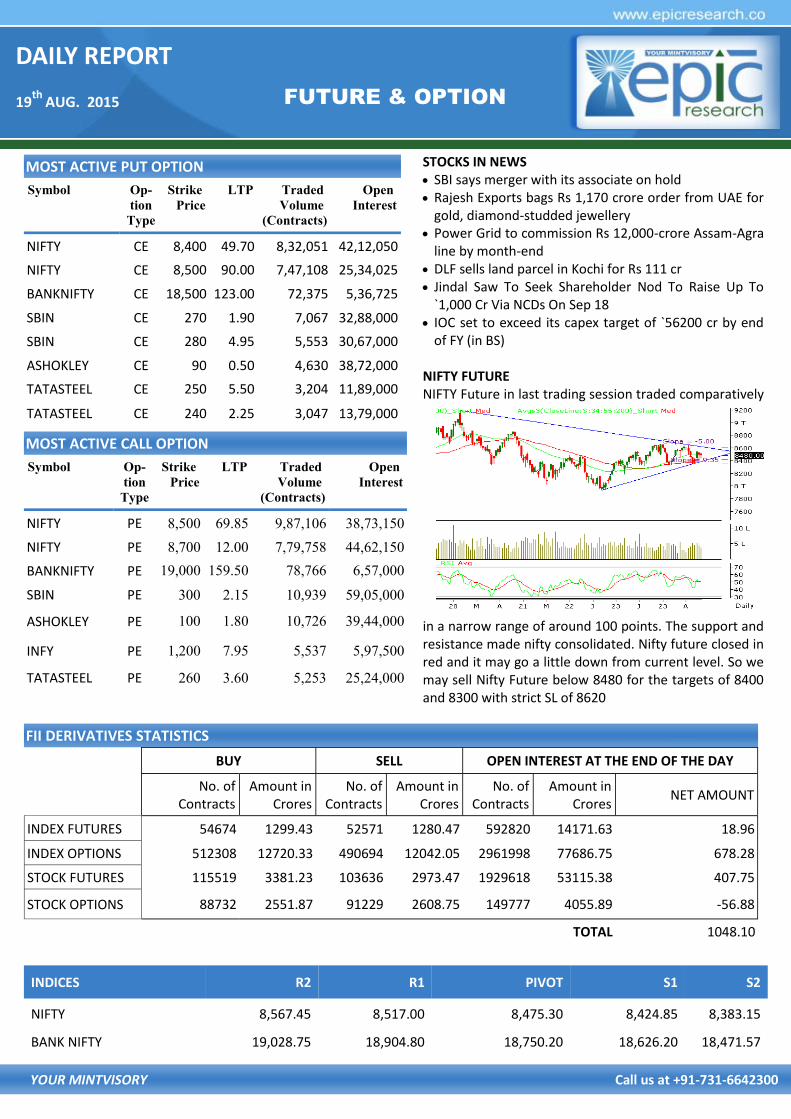

of FY (in BS) NIFTY FUTURE NIFTY Future in last trading session traded comparatively

in a narrow range of around 100 points. The support and resistance made nifty consolidated. Nifty future closed in red and it may go a little down from current level. So we may sell Nifty Future below 8480 for the targets of 8400 and 8300 with strict SL of 8620

INDICES R2 R1 PIVOT S1 S2

NIFTY 8,567.45 8,517.00 8,475.30 8,424.85 8,383.15

BANK NIFTY 19,028.75 18,904.80 18,750.20 18,626.20 18,471.57

DAILY REPORT

19th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RECOMMENDATIONS

GOLD

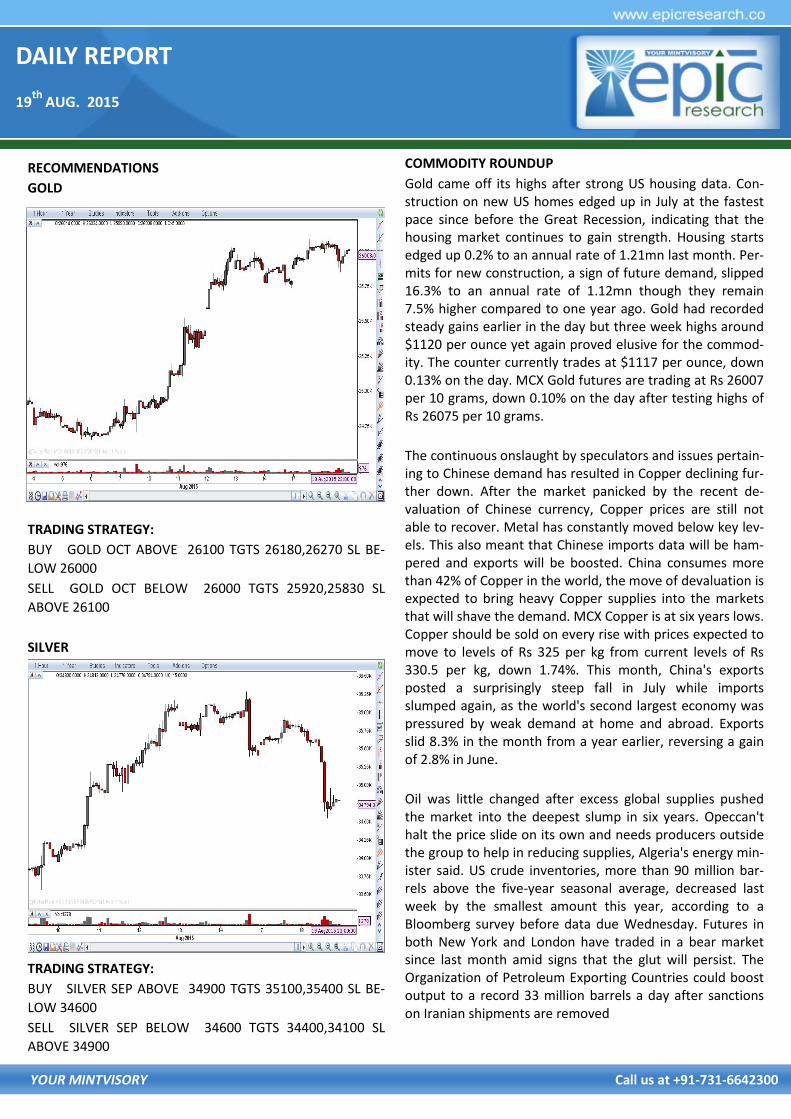

TRADING STRATEGY:

BUY GOLD OCT ABOVE 26100 TGTS 26180,26270 SL BE-

LOW 26000

SELL GOLD OCT BELOW 26000 TGTS 25920,25830 SL

ABOVE 26100

SILVER

TRADING STRATEGY:

BUY SILVER SEP ABOVE 34900 TGTS 35100,35400 SL BE-

LOW 34600

SELL SILVER SEP BELOW 34600 TGTS 34400,34100 SL

ABOVE 34900

COMMODITY ROUNDUP

Gold came off its highs after strong US housing data. Con-struction on new US homes edged up in July at the fastest pace since before the Great Recession, indicating that the housing market continues to gain strength. Housing starts edged up 0.2% to an annual rate of 1.21mn last month. Per-mits for new construction, a sign of future demand, slipped 16.3% to an annual rate of 1.12mn though they remain 7.5% higher compared to one year ago. Gold had recorded steady gains earlier in the day but three week highs around $1120 per ounce yet again proved elusive for the commod-ity. The counter currently trades at $1117 per ounce, down 0.13% on the day. MCX Gold futures are trading at Rs 26007 per 10 grams, down 0.10% on the day after testing highs of Rs 26075 per 10 grams.

The continuous onslaught by speculators and issues pertain-ing to Chinese demand has resulted in Copper declining fur-ther down. After the market panicked by the recent de-valuation of Chinese currency, Copper prices are still not able to recover. Metal has constantly moved below key lev-els. This also meant that Chinese imports data will be ham-pered and exports will be boosted. China consumes more than 42% of Copper in the world, the move of devaluation is expected to bring heavy Copper supplies into the markets that will shave the demand. MCX Copper is at six years lows. Copper should be sold on every rise with prices expected to move to levels of Rs 325 per kg from current levels of Rs 330.5 per kg, down 1.74%. This month, China's exports posted a surprisingly steep fall in July while imports slumped again, as the world's second largest economy was pressured by weak demand at home and abroad. Exports slid 8.3% in the month from a year earlier, reversing a gain of 2.8% in June.

Oil was little changed after excess global supplies pushed the market into the deepest slump in six years. Opeccan't halt the price slide on its own and needs producers outside the group to help in reducing supplies, Algeria's energy min-ister said. US crude inventories, more than 90 million bar-rels above the five-year seasonal average, decreased last week by the smallest amount this year, according to a Bloomberg survey before data due Wednesday. Futures in both New York and London have traded in a bear market since last month amid signs that the glut will persist. The Organization of Petroleum Exporting Countries could boost output to a record 33 million barrels a day after sanctions on Iranian shipments are removed

DAILY REPORT

19th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NCDEX

RECOMMENDATIONS

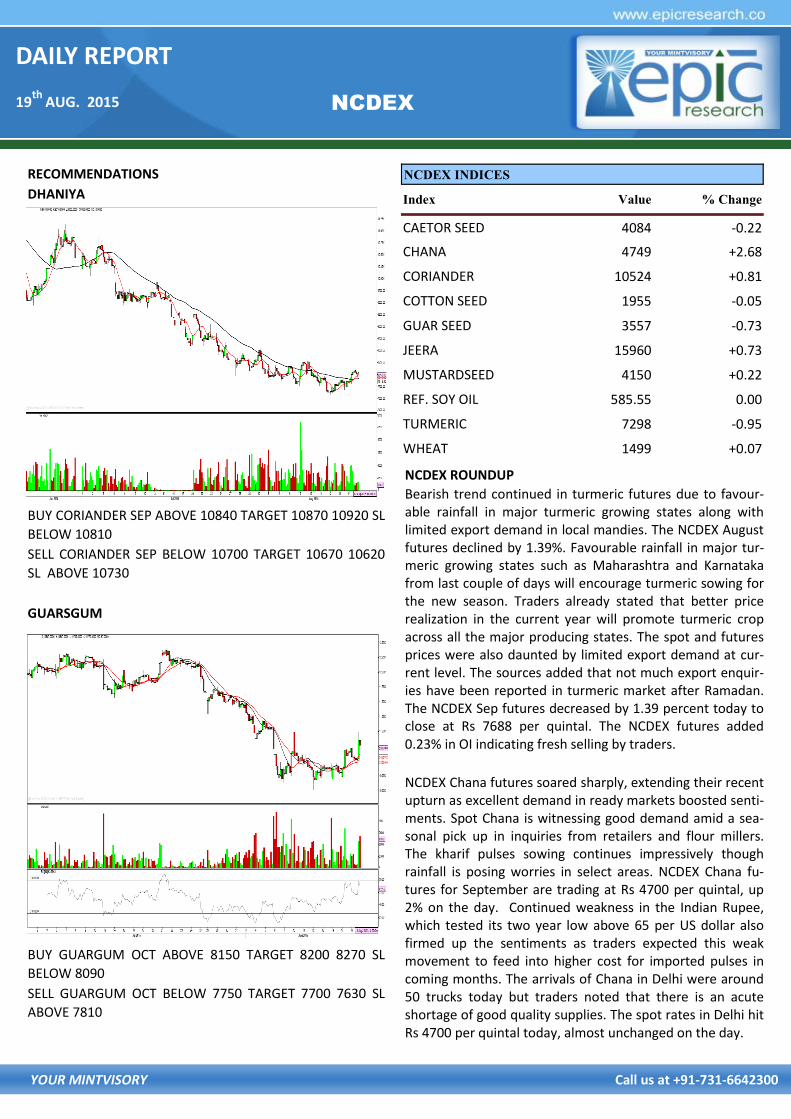

DHANIYA

BUY CORIANDER SEP ABOVE 10840 TARGET 10870 10920 SL

BELOW 10810

SELL CORIANDER SEP BELOW 10700 TARGET 10670 10620

SL ABOVE 10730

GUARSGUM

BUY GUARGUM OCT ABOVE 8150 TARGET 8200 8270 SL

BELOW 8090

SELL GUARGUM OCT BELOW 7750 TARGET 7700 7630 SL

ABOVE 7810

NCDEX ROUNDUP

Bearish trend continued in turmeric futures due to favour-able rainfall in major turmeric growing states along with limited export demand in local mandies. The NCDEX August futures declined by 1.39%. Favourable rainfall in major tur-meric growing states such as Maharashtra and Karnataka from last couple of days will encourage turmeric sowing for the new season. Traders already stated that better price realization in the current year will promote turmeric crop across all the major producing states. The spot and futures prices were also daunted by limited export demand at cur-rent level. The sources added that not much export enquir-ies have been reported in turmeric market after Ramadan. The NCDEX Sep futures decreased by 1.39 percent today to close at Rs 7688 per quintal. The NCDEX futures added 0.23% in OI indicating fresh selling by traders.

NCDEX Chana futures soared sharply, extending their recent upturn as excellent demand in ready markets boosted senti-ments. Spot Chana is witnessing good demand amid a sea-sonal pick up in inquiries from retailers and flour millers. The kharif pulses sowing continues impressively though rainfall is posing worries in select areas. NCDEX Chana fu-tures for September are trading at Rs 4700 per quintal, up 2% on the day. Continued weakness in the Indian Rupee, which tested its two year low above 65 per US dollar also firmed up the sentiments as traders expected this weak movement to feed into higher cost for imported pulses in coming months. The arrivals of Chana in Delhi were around 50 trucks today but traders noted that there is an acute shortage of good quality supplies. The spot rates in Delhi hit Rs 4700 per quintal today, almost unchanged on the day.

NCDEX INDICES

Index Value % Change

CAETOR SEED 4084 -0.22

CHANA 4749 +2.68

CORIANDER 10524 +0.81

COTTON SEED 1955 -0.05

GUAR SEED 3557 -0.73

JEERA 15960 +0.73

MUSTARDSEED 4150 +0.22

REF. SOY OIL 585.55 0.00

TURMERIC 7298 -0.95

WHEAT 1499 +0.07

DAILY REPORT

19th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

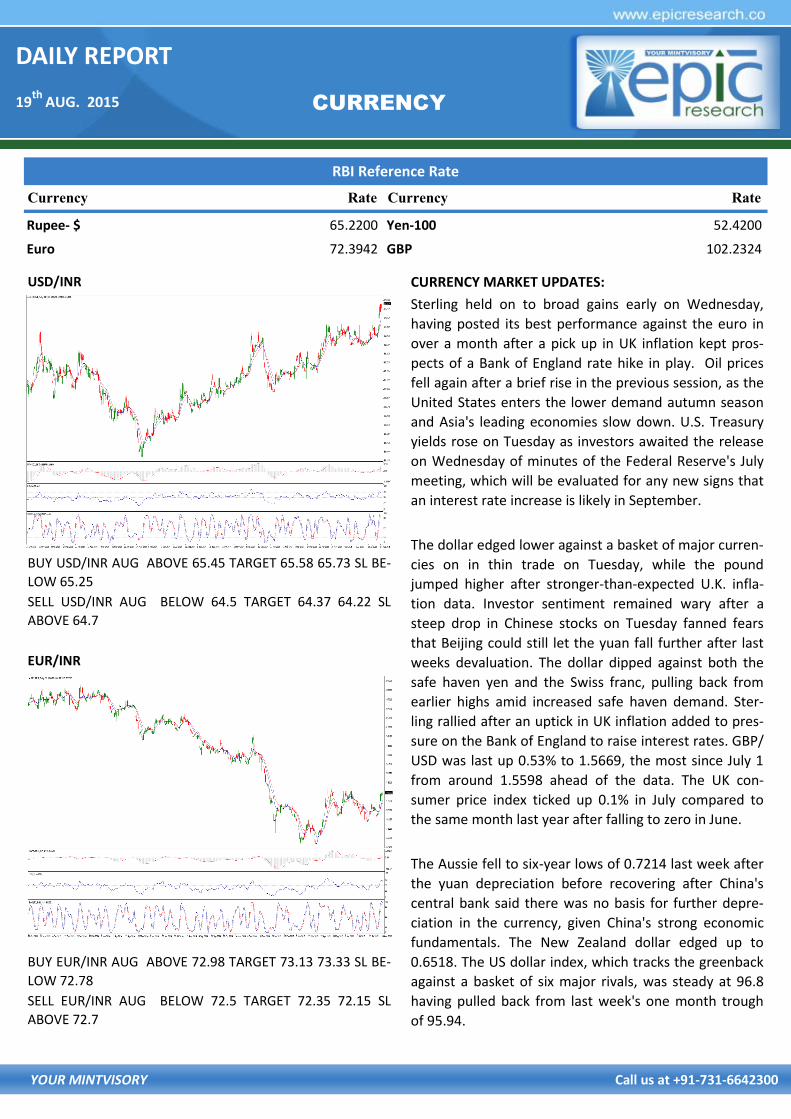

RBI Reference Rate

Currency Rate Currency Rate

Rupee- $ 65.2200 Yen-100 52.4200

Euro 72.3942 GBP 102.2324

CURRENCY

USD/INR

BUY USD/INR AUG ABOVE 65.45 TARGET 65.58 65.73 SL BE-

LOW 65.25

SELL USD/INR AUG BELOW 64.5 TARGET 64.37 64.22 SL

ABOVE 64.7

EUR/INR

BUY EUR/INR AUG ABOVE 72.98 TARGET 73.13 73.33 SL BE-

LOW 72.78

SELL EUR/INR AUG BELOW 72.5 TARGET 72.35 72.15 SL

ABOVE 72.7

CURRENCY MARKET UPDATES:

Sterling held on to broad gains early on Wednesday,

having posted its best performance against the euro in

over a month after a pick up in UK inflation kept pros-

pects of a Bank of England rate hike in play. Oil prices

fell again after a brief rise in the previous session, as the

United States enters the lower demand autumn season

and Asia's leading economies slow down. U.S. Treasury

yields rose on Tuesday as investors awaited the release

on Wednesday of minutes of the Federal Reserve's July

meeting, which will be evaluated for any new signs that

an interest rate increase is likely in September.

The dollar edged lower against a basket of major curren-

cies on in thin trade on Tuesday, while the pound

jumped higher after stronger-than-expected U.K. infla-

tion data. Investor sentiment remained wary after a

steep drop in Chinese stocks on Tuesday fanned fears

that Beijing could still let the yuan fall further after last

weeks devaluation. The dollar dipped against both the

safe haven yen and the Swiss franc, pulling back from

earlier highs amid increased safe haven demand. Ster-

ling rallied after an uptick in UK inflation added to pres-

sure on the Bank of England to raise interest rates. GBP/

USD was last up 0.53% to 1.5669, the most since July 1

from around 1.5598 ahead of the data. The UK con-

sumer price index ticked up 0.1% in July compared to

the same month last year after falling to zero in June.

The Aussie fell to six-year lows of 0.7214 last week after

the yuan depreciation before recovering after China's

central bank said there was no basis for further depre-

ciation in the currency, given China's strong economic

fundamentals. The New Zealand dollar edged up to

0.6518. The US dollar index, which tracks the greenback

against a basket of six major rivals, was steady at 96.8

having pulled back from last week's one month trough

of 95.94.

DAILY REPORT

19th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

CALL REPORT

S T O

PERFORMANCE UPDATES

Date Commodity/ Currency

Pairs Contract Strategy Entry Level Target Stop Loss Remark

18/08/15 NCDEX DHANIYA SEPT. BUY 10840 10865-1095 10810 BOOKED FULL PROFIT

18/08/15 NCDEX DHANIYA SEPT. SELL 10600 10575-10525 10630 BOOKED FULL PROFIT

18/08/15 NCDEX GUARGUM OCT. BUY 8120 8170-8240 8060 SL TRIGGERED

18/08/15 NCDEX GUARGUM OCT. SELL 7960 7910-7840 8020 BOOKED FULL PROFIT

18/08/15 MCX GOLD OCT. BUY 26100 26180-26270 26000 NO PROFIT NO LOSS

18/08/15 MCX GOLD OCT. SELL 25900 25820-25730 26000 SL TRIGGERED

18/08/15 MCX SILVER SEPT. BUY 36150 36350-36650 35850 NOT EXECUTED

18/08/15 MCX SILVER SEPT. SELL 35800 35600-35300 36100 BOOKED FULL PROFIT

18/08/15 USD/INR AUG. BUY 65.50 65.63-65.78 65.30 NO PROFIT NO LOSS

18/08/15 USD/INR AUG. SELL 65.33 65.20-65.05 65.53 NO PROFIT NO LOSS

18/08/15 EUR/INR AUG. BUY 72.69 72.84-73.04 72.49 NO PROFIT NO LOSS

18/08/15 EUR/INR AUG. SELL 72.43 72.28-72.08 72.63 NO PROFIT NO LOSS

Date Scrip

CASH/

FUTURE/

OPTION

Strategy Entry Level Target Stop Loss Remark

18/08/15 NIFTY FUTURE BUY 8500 8580-8700 8350 CALL OPEN

18/08/15 KSCL FUTURE SELL 483 476-470 490 NOT EXECUTED

18/08/15 AMTEK AUTO FUTURE SELL 129 128-127 131 BOOKED PROFIT

18/08/15 AMARAJBAT CASH BUY 1067 1075-1085 1049 NOT EXECUTED

14/08/15 NIFTY FUTURE SELL 8460-8480 8380-8250 8600 CALL OPEN

17/08/15 NIFTY FUTURE BUY 8500 8580-8700 8350 NO PROFIT NO LOSS

DAILY REPORT

19th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

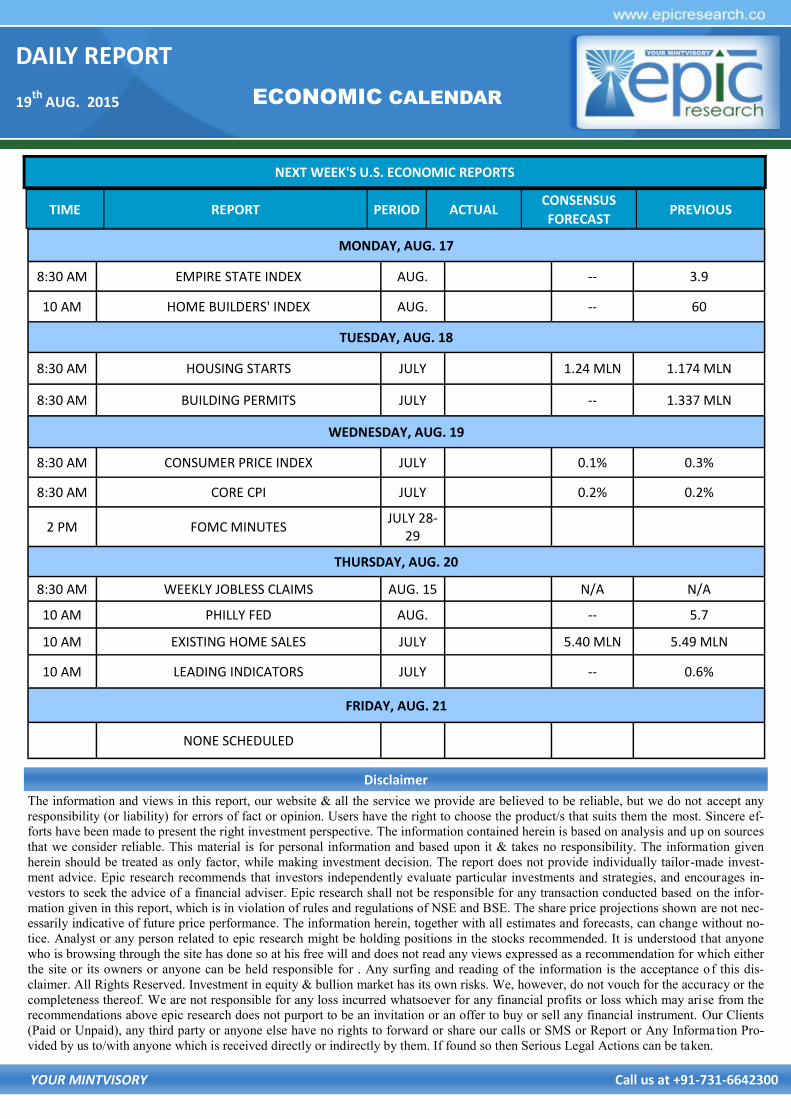

NEXT WEEK'S U.S. ECONOMIC REPORTS

ECONOMIC CALENDAR

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any

responsibility (or liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most. Sincere ef-

forts have been made to present the right investment perspective. The information contained herein is based on analysis and up on sources

that we consider reliable. This material is for personal information and based upon it & takes no responsibility. The information given

herein should be treated as only factor, while making investment decision. The report does not provide individually tailor-made invest-

ment advice. Epic research recommends that investors independently evaluate particular investments and strategies, and encourages in-

vestors to seek the advice of a financial adviser. Epic research shall not be responsible for any transaction conducted based on the infor-

mation given in this report, which is in violation of rules and regulations of NSE and BSE. The share price projections shown are not nec-

essarily indicative of future price performance. The information herein, together with all estimates and forecasts, can change without no-

tice. Analyst or any person related to epic research might be holding positions in the stocks recommended. It is understood that anyone

who is browsing through the site has done so at his free will and does not read any views expressed as a recommendation for which either

the site or its owners or anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this dis-

claimer. All Rights Reserved. Investment in equity & bullion market has its own risks. We, however, do not vouch for the accuracy or the

completeness thereof. We are not responsible for any loss incurred whatsoever for any financial profits or loss which may arise from the

recommendations above epic research does not purport to be an invitation or an offer to buy or sell any financial instrument. Our Clients

(Paid or Unpaid), any third party or anyone else have no rights to forward or share our calls or SMS or Report or Any Information Pro-

vided by us to/with anyone which is received directly or indirectly by them. If found so then Serious Legal Actions can be taken.

Disclaimer

TIME REPORT PERIOD ACTUAL CONSENSUS

FORECAST PREVIOUS

MONDAY, AUG. 17

8:30 AM EMPIRE STATE INDEX AUG. -- 3.9

10 AM HOME BUILDERS' INDEX AUG. -- 60

TUESDAY, AUG. 18

8:30 AM HOUSING STARTS JULY 1.24 MLN 1.174 MLN

8:30 AM BUILDING PERMITS JULY -- 1.337 MLN

WEDNESDAY, AUG. 19

8:30 AM CONSUMER PRICE INDEX JULY 0.1% 0.3%

8:30 AM CORE CPI JULY 0.2% 0.2%

2 PM FOMC MINUTES JULY 28-

29

THURSDAY, AUG. 20

8:30 AM WEEKLY JOBLESS CLAIMS AUG. 15 N/A N/A

10 AM PHILLY FED AUG. -- 5.7

10 AM EXISTING HOME SALES JULY 5.40 MLN 5.49 MLN

10 AM LEADING INDICATORS JULY -- 0.6%

FRIDAY, AUG. 21

NONE SCHEDULED