Epic research special report of 10 aug 2015

8

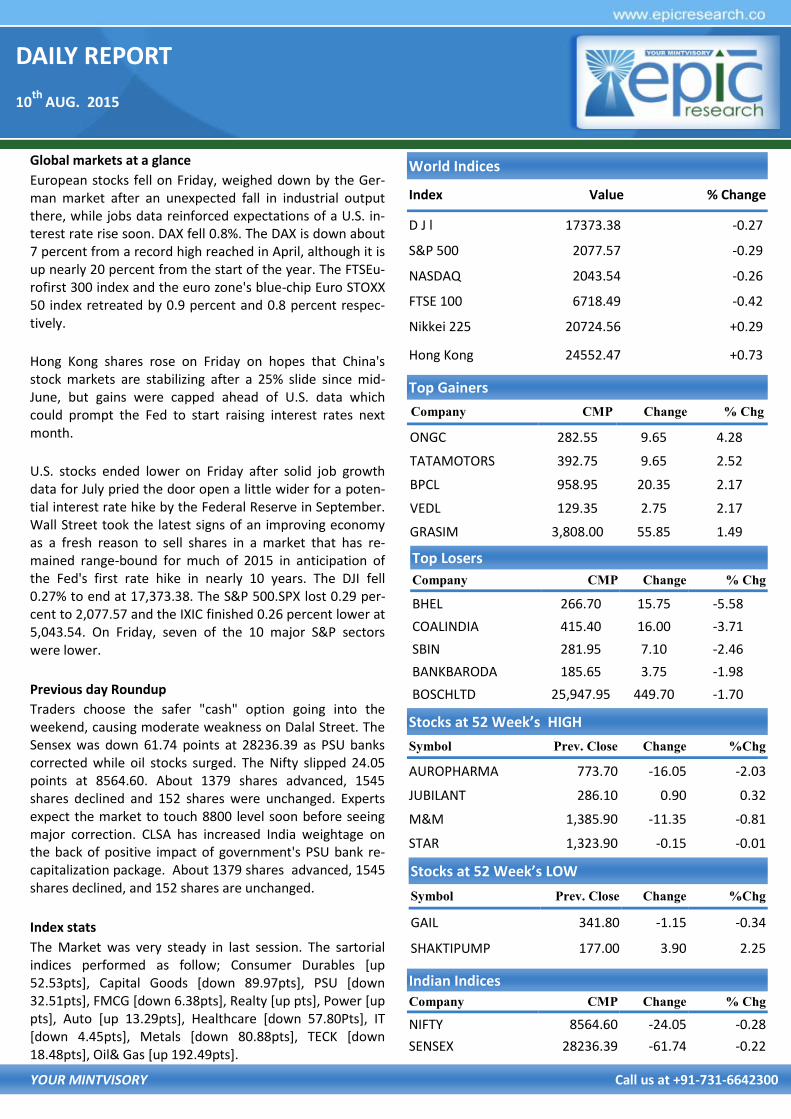

DAILY REPORT 10 th AUG. 2015 YOUR MINTVISORY Call us at +91-731-6642300 Global markets at a glance European stocks fell on Friday, weighed down by the Ger- man market after an unexpected fall in industrial output there, while jobs data reinforced expectations of a U.S. in- terest rate rise soon. DAX fell 0.8%. The DAX is down about 7 percent from a record high reached in April, although it is up nearly 20 percent from the start of the year. The FTSEu- rofirst 300 index and the euro zone's blue-chip Euro STOXX 50 index retreated by 0.9 percent and 0.8 percent respec- tively. Hong Kong shares rose on Friday on hopes that China's stock markets are stabilizing after a 25% slide since mid- June, but gains were capped ahead of U.S. data which could prompt the Fed to start raising interest rates next month. U.S. stocks ended lower on Friday after solid job growth data for July pried the door open a little wider for a poten- tial interest rate hike by the Federal Reserve in September. Wall Street took the latest signs of an improving economy as a fresh reason to sell shares in a market that has re- mained range-bound for much of 2015 in anticipation of the Fed's first rate hike in nearly 10 years. The DJI fell 0.27% to end at 17,373.38. The S&P 500.SPX lost 0.29 per- cent to 2,077.57 and the IXIC finished 0.26 percent lower at 5,043.54. On Friday, seven of the 10 major S&P sectors were lower. Previous day Roundup Traders choose the safer "cash" option going into the weekend, causing moderate weakness on Dalal Street. The Sensex was down 61.74 points at 28236.39 as PSU banks corrected while oil stocks surged. The Nifty slipped 24.05 points at 8564.60. About 1379 shares advanced, 1545 shares declined and 152 shares were unchanged. Experts expect the market to touch 8800 level soon before seeing major correction. CLSA has increased India weightage on the back of positive impact of government's PSU bank re- capitalization package. About 1379 shares advanced, 1545 shares declined, and 152 shares are unchanged. Index stats The Market was very steady in last session. The sartorial indices performed as follow; Consumer Durables [up 52.53pts], Capital Goods [down 89.97pts], PSU [down 32.51pts], FMCG [down 6.38pts], Realty [up pts], Power [up pts], Auto [up 13.29pts], Healthcare [down 57.80Pts], IT [down 4.45pts], Metals [down 80.88pts], TECK [down 18.48pts], Oil& Gas [up 192.49pts]. World Indices Index Value % Change D J l 17373.38 -0.27 S&P 500 2077.57 -0.29 NASDAQ 2043.54 -0.26 FTSE 100 6718.49 -0.42 Nikkei 225 20724.56 +0.29 Hong Kong 24552.47 +0.73 Top Gainers Company CMP Change % Chg ONGC 282.55 9.65 4.28 TATAMOTORS 392.75 9.65 2.52 BPCL 958.95 20.35 2.17 VEDL 129.35 2.75 2.17 GRASIM 3,808.00 55.85 1.49 Top Losers Company CMP Change % Chg BHEL 266.70 15.75 -5.58 COALINDIA 415.40 16.00 -3.71 SBIN 281.95 7.10 -2.46 BANKBARODA 185.65 3.75 -1.98 BOSCHLTD 25,947.95 449.70 -1.70 Stocks at 52 Week’s HIGH Symbol Prev. Close Change %Chg AUROPHARMA 773.70 -16.05 -2.03 JUBILANT 286.10 0.90 0.32 M&M 1,385.90 -11.35 -0.81 STAR 1,323.90 -0.15 -0.01 Indian Indices Company CMP Change % Chg NIFTY 8564.60 -24.05 -0.28 SENSEX 28236.39 -61.74 -0.22 Stocks at 52 Week’s LOW Symbol Prev. Close Change %Chg GAIL 341.80 -1.15 -0.34 SHAKTIPUMP 177.00 3.90 2.25

-

Upload

epic-research-private-limited -

Category

Business

-

view

23 -

download

1

Transcript of Epic research special report of 10 aug 2015

DAILY REPORT

10th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

Global markets at a glance

European stocks fell on Friday, weighed down by the Ger-man market after an unexpected fall in industrial output there, while jobs data reinforced expectations of a U.S. in-terest rate rise soon. DAX fell 0.8%. The DAX is down about 7 percent from a record high reached in April, although it is up nearly 20 percent from the start of the year. The FTSEu-rofirst 300 index and the euro zone's blue-chip Euro STOXX 50 index retreated by 0.9 percent and 0.8 percent respec-tively.

Hong Kong shares rose on Friday on hopes that China's stock markets are stabilizing after a 25% slide since mid-June, but gains were capped ahead of U.S. data which could prompt the Fed to start raising interest rates next month.

U.S. stocks ended lower on Friday after solid job growth data for July pried the door open a little wider for a poten-tial interest rate hike by the Federal Reserve in September. Wall Street took the latest signs of an improving economy as a fresh reason to sell shares in a market that has re-mained range-bound for much of 2015 in anticipation of the Fed's first rate hike in nearly 10 years. The DJI fell 0.27% to end at 17,373.38. The S&P 500.SPX lost 0.29 per-cent to 2,077.57 and the IXIC finished 0.26 percent lower at 5,043.54. On Friday, seven of the 10 major S&P sectors were lower.

Previous day Roundup

Traders choose the safer "cash" option going into the weekend, causing moderate weakness on Dalal Street. The Sensex was down 61.74 points at 28236.39 as PSU banks corrected while oil stocks surged. The Nifty slipped 24.05 points at 8564.60. About 1379 shares advanced, 1545 shares declined and 152 shares were unchanged. Experts expect the market to touch 8800 level soon before seeing major correction. CLSA has increased India weightage on the back of positive impact of government's PSU bank re-capitalization package. About 1379 shares advanced, 1545 shares declined, and 152 shares are unchanged.

Index stats

The Market was very steady in last session. The sartorial indices performed as follow; Consumer Durables [up 52.53pts], Capital Goods [down 89.97pts], PSU [down 32.51pts], FMCG [down 6.38pts], Realty [up pts], Power [up pts], Auto [up 13.29pts], Healthcare [down 57.80Pts], IT [down 4.45pts], Metals [down 80.88pts], TECK [down 18.48pts], Oil& Gas [up 192.49pts].

World Indices

Index Value % Change

D J l 17373.38 -0.27

S&P 500 2077.57 -0.29

NASDAQ 2043.54 -0.26

FTSE 100 6718.49 -0.42

Nikkei 225 20724.56 +0.29

Hong Kong 24552.47 +0.73

Top Gainers

Company CMP Change % Chg

ONGC 282.55 9.65 4.28

TATAMOTORS 392.75 9.65 2.52

BPCL 958.95 20.35 2.17

VEDL 129.35 2.75 2.17

GRASIM 3,808.00 55.85 1.49

Top Losers

Company CMP Change % Chg

BHEL 266.70 15.75 -5.58

COALINDIA 415.40 16.00 -3.71

SBIN 281.95 7.10 -2.46

BANKBARODA 185.65 3.75 -1.98

BOSCHLTD 25,947.95 449.70 -1.70

Stocks at 52 Week’s HIGH

Symbol Prev. Close Change %Chg

AUROPHARMA 773.70 -16.05 -2.03

JUBILANT 286.10 0.90 0.32

M&M 1,385.90 -11.35 -0.81

STAR 1,323.90 -0.15 -0.01

Indian Indices

Company CMP Change % Chg

NIFTY 8564.60 -24.05 -0.28

SENSEX 28236.39 -61.74 -0.22

Stocks at 52 Week’s LOW

Symbol Prev. Close Change %Chg

GAIL 341.80 -1.15 -0.34

SHAKTIPUMP 177.00 3.90 2.25

DAILY REPORT

10th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

STOCK RECOMMENDATION [CASH]

1. INTELLECT (CASH)

INTELLECT made new life time high of 193.50 and today it finished with 12.30% gain at 183.80 still indicator showing more up side so we advise to buy it above 187.50 use strict stop loss of 183 for targets of 190-193-196

MACRO NEWS

Sebi has initiated an internal study of suggestions made

by the SC-appointed SIT on black money and the matter

will be discussed by regulator's board later this month.

BHEL Q1 shocks; profit tanks 83%, EBITDA loss Rs 209 cr

M&M Q1 net profit down 7%, cost saving supports EBITDA

Grasim Q1 net flat at Rs 485 cr, VSF revenue up 15%

FRL Q1 net profit at Rs 6 cr, revenue rises 22.4%

Canara Bank seeks to recover Rs 500cr via e-auctions

Tata Motors Q1 net dips 48% to Rs 2,769 cr as JLR dents

earnings

6 bidders for 51% stake in Reliance Infratel; deal could value the co at Rs 25,000 cr

Govt expands Digital India cover, allows Aadhaar enrol-ments of NRIs, PIOs, OICs

Greenpeace cautions bidders on 39 coal blocks ahead of auction

Pharma industry backs government's decision to defer

trade talks with European Union

FTIL, NSEL merger delayed for 3 months till Oct 31

Maruti aims to sell upto 5K units of S-Cross every month

US jobs post solid gains; unemployment flat

STOCK RECOMMENDATIONS [FUTURE]

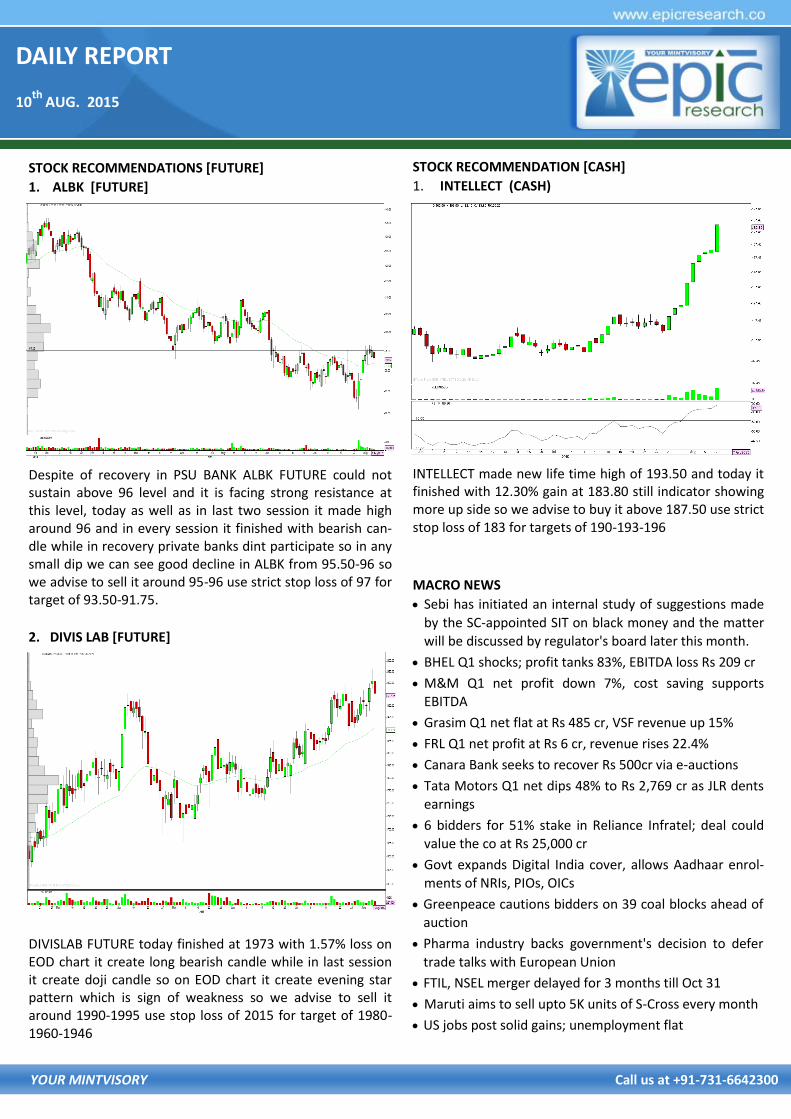

1. ALBK [FUTURE]

Despite of recovery in PSU BANK ALBK FUTURE could not sustain above 96 level and it is facing strong resistance at this level, today as well as in last two session it made high around 96 and in every session it finished with bearish can-dle while in recovery private banks dint participate so in any small dip we can see good decline in ALBK from 95.50-96 so we advise to sell it around 95-96 use strict stop loss of 97 for target of 93.50-91.75.

2. DIVIS LAB [FUTURE]

DIVISLAB FUTURE today finished at 1973 with 1.57% loss on EOD chart it create long bearish candle while in last session it create doji candle so on EOD chart it create evening star pattern which is sign of weakness so we advise to sell it around 1990-1995 use stop loss of 2015 for target of 1980-1960-1946

DAILY REPORT

10th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

FUTURE & OPTION

MOST ACTIVE PUT OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY PE 8,300 9.00 12,62,696 55,89,025

NIFTY PE 8,400 36.70 8,79,465 38,57,525

BANKNIFTY PE 18,000 16.00 89,315 7,89,000

YESBANK PE 800 2.80 11,424 6,93,750

RELIANCE PE 1,000 6.90 6,247 6,57,750

MARUTI PE 4,200 3.95 5,987 1,80,375

YESBANK PE 780 0.75 5,401 2,93,000

SBIN PE 250 0.85 3,723 11,90,000

MOST ACTIVE CALL OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY CE 8,400 24.50 17,37,962 60,13,125

NIFTY CE 8,300 91.50 5,79,894 17,08,950

BANKNIFTY CE 18,500 21.95 1,35,175 6,20,750

YESBANK CE 820 5.65 11,603 5,56,250

MARUTI CE 4,300 10.50 9,536 1,24,375

INFY CE 1,100 3.25 8,533 8,88,250

RELAINCE CE 1,020 1.35 7,895 10,03,250

SBIN CE 260 0.40 7,409 24,09,000

FII DERIVATIVES STATISTICS

BUY OPEN INTEREST AT THE END OF THE DAY SELL

No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores NET AMOUNT

INDEX FUTURES 21658 489.07 13089 404.21 658456 15692.28 84.86

INDEX OPTIONS 242843 6012.95 234462 5770.31 2632223 70398.27 242.64

STOCK FUTURES 75779 2095.54 92012 2597.71 1818342 50999.52 -502.18

STOCK OPTIONS 62430 1649.32 62161 1633.04 108611 3038.31 16.28

TOTAL 158.39

STOCKS IN NEWS Tata Power looking at acquiring stressed assets BHEL commissions 500 MW thermal unit at Vindhya-

chal STPS Essar Oil ropes in ex-HPCL chief Subir Roy Choudhury

for retail push; eyes 5,000 outlets over 2 years Tata Steel seeks legal solution to Noamundi mine issue

with Jharkhand government Dr Reddy’s Laboratories eyes in-licensing pacts with

European, Japanese firms to spur domestic revenue ICICI Bank at higher risk of bad loans

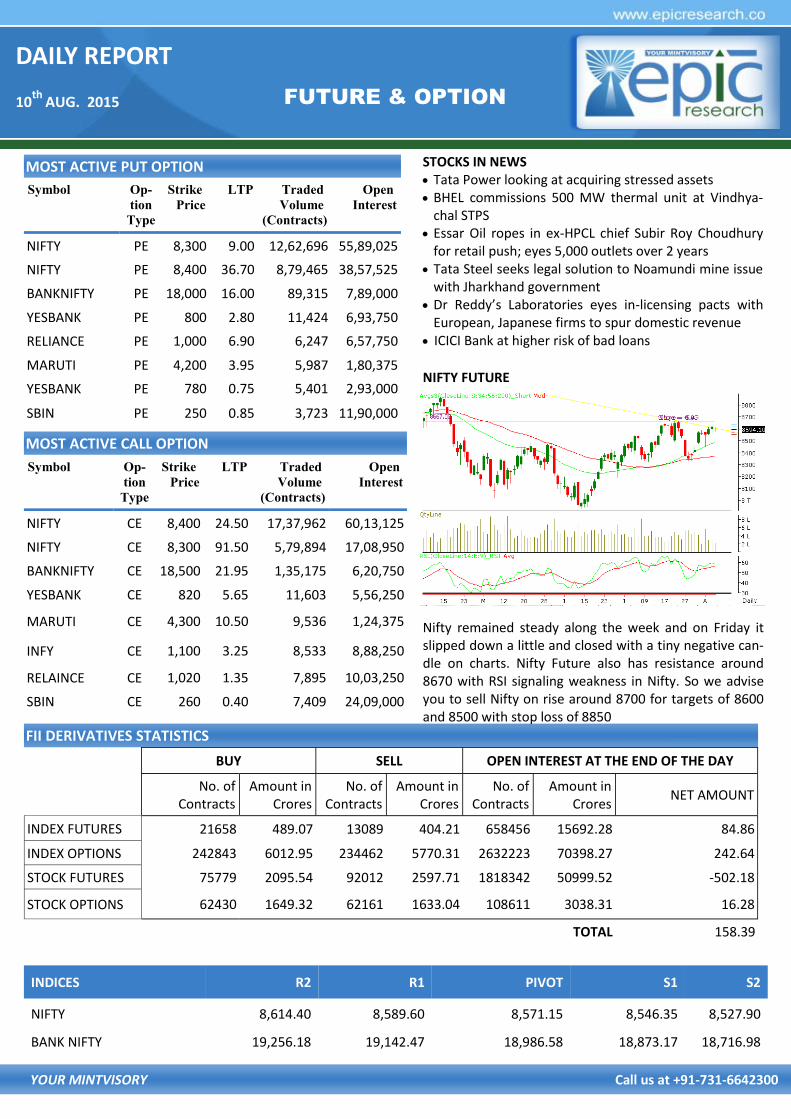

NIFTY FUTURE

Nifty remained steady along the week and on Friday it slipped down a little and closed with a tiny negative can-dle on charts. Nifty Future also has resistance around 8670 with RSI signaling weakness in Nifty. So we advise you to sell Nifty on rise around 8700 for targets of 8600 and 8500 with stop loss of 8850

INDICES R2 R1 PIVOT S1 S2

NIFTY 8,614.40 8,589.60 8,571.15 8,546.35 8,527.90

BANK NIFTY 19,256.18 19,142.47 18,986.58 18,873.17 18,716.98

DAILY REPORT

10th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RECOMMENDATIONS

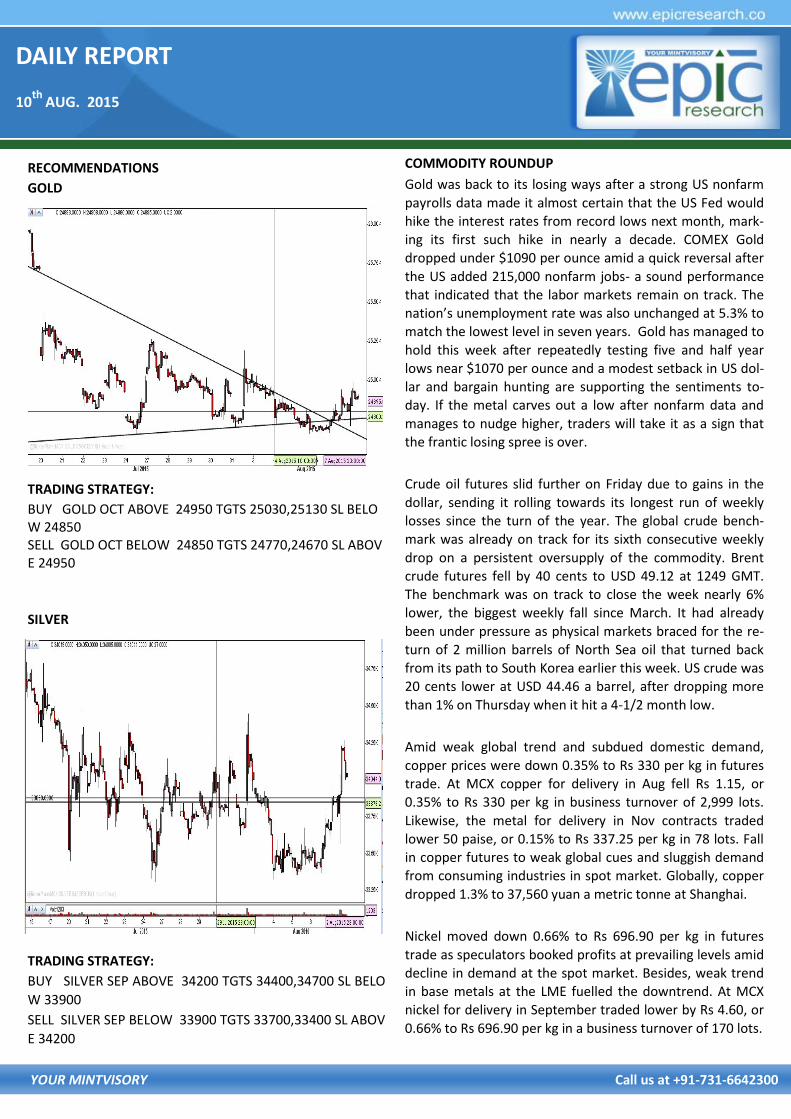

GOLD

TRADING STRATEGY:

BUY GOLD OCT ABOVE 24950 TGTS 25030,25130 SL BELOW 24850 SELL GOLD OCT BELOW 24850 TGTS 24770,24670 SL ABOVE 24950

SILVER

TRADING STRATEGY:

BUY SILVER SEP ABOVE 34200 TGTS 34400,34700 SL BELO

W 33900

SELL SILVER SEP BELOW 33900 TGTS 33700,33400 SL ABOV

E 34200

COMMODITY ROUNDUP

Gold was back to its losing ways after a strong US nonfarm

payrolls data made it almost certain that the US Fed would hike the interest rates from record lows next month, mark-ing its first such hike in nearly a decade. COMEX Gold dropped under $1090 per ounce amid a quick reversal after

the US added 215,000 nonfarm jobs- a sound performance that indicated that the labor markets remain on track. The

nation’s unemployment rate was also unchanged at 5.3% to match the lowest level in seven years. Gold has managed to

hold this week after repeatedly testing five and half year lows near $1070 per ounce and a modest setback in US dol-lar and bargain hunting are supporting the sentiments to-

day. If the metal carves out a low after nonfarm data and

manages to nudge higher, traders will take it as a sign that the frantic losing spree is over.

Crude oil futures slid further on Friday due to gains in the

dollar, sending it rolling towards its longest run of weekly

losses since the turn of the year. The global crude bench-mark was already on track for its sixth consecutive weekly

drop on a persistent oversupply of the commodity. Brent crude futures fell by 40 cents to USD 49.12 at 1249 GMT. The benchmark was on track to close the week nearly 6%

lower, the biggest weekly fall since March. It had already

been under pressure as physical markets braced for the re-

turn of 2 million barrels of North Sea oil that turned back from its path to South Korea earlier this week. US crude was

20 cents lower at USD 44.46 a barrel, after dropping more

than 1% on Thursday when it hit a 4-1/2 month low.

Amid weak global trend and subdued domestic demand,

copper prices were down 0.35% to Rs 330 per kg in futures

trade. At MCX copper for delivery in Aug fell Rs 1.15, or 0.35% to Rs 330 per kg in business turnover of 2,999 lots.

Likewise, the metal for delivery in Nov contracts traded lower 50 paise, or 0.15% to Rs 337.25 per kg in 78 lots. Fall in copper futures to weak global cues and sluggish demand from consuming industries in spot market. Globally, copper

dropped 1.3% to 37,560 yuan a metric tonne at Shanghai.

Nickel moved down 0.66% to Rs 696.90 per kg in futures

trade as speculators booked profits at prevailing levels amid decline in demand at the spot market. Besides, weak trend in base metals at the LME fuelled the downtrend. At MCX

nickel for delivery in September traded lower by Rs 4.60, or

0.66% to Rs 696.90 per kg in a business turnover of 170 lots.

DAILY REPORT

10th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NCDEX

RECOMMENDATIONS

DHANIYA

BUY CORIANDER SEP ABOVE 10690 TARGET 10720 10760 SL

BELOW 10660

SELL CORIANDER SEP BELOW 10524 TARGET 10494 10454

SL ABOVE 10554

GUARSGUM

BUY GUARGUM OCT ABOVE 8300 TARGET 8350 8420 SL

BELOW 8240

SELL GUARGUM OCT BELOW 8000 TARGET 7950 7880 SL

ABOVE 8060

NCDEX ROUNDUP

Sharp bounce back was seen in wheat futures in today's trading as government has imposed import duty on wheat. The NCDEX futures swelled by almost 1 percent from the last trading. As per the official sources, The government will impose an import duty of 10 per cent on wheat effective until March 31 next year, reinstating tariffs after a gap of eight years following big purchases in recent months. This was mainly due to cheap import of wheat by some private players in the last month. Some of the private firms signed deals to import 500,000 tonnes of high-protein Australian wheat in last June. The NCDEX futures added 0.74 percent today to currently trade at Rs 1502 per quintal after hitting the intraday high of Rs 1519 per quintal.

Global dairy giant Fonterra is expecting a recovery in dairy prices, terming their unsustainably low, even as it slashed its forecast for payouts to farmers this season to the lowest in 13 years, and slashed its investment budget. The New Zealand-based co-operative, the world's top milk exporter, reduced to NZ$3.85 per kg of milk solids, from NZ$5.25 per kg of milk solids, its estimate for its payment to farmers for milk in 2015-16. The downgraded estimate matched the payout in 2005-06, the smallest since 2002-03, when Fon-terra paid producers NZ$3.34 per kg of milk solids.

The total sown area as on 7th August, as per reports re-ceived from States, stands at847.40 lakh hectare as com-pared to 808.40 lakh hectare at this time last year, re-cording arise of nearly 5%.

NCDEX INDICES

Index Value % Change

CAETOR SEED 3963 -0.63

CHANA 4356 +1.11

CORIANDER 10495 +3.99

COTTON SEED 1930 +0.78

GUAR SEED 3674 -0.14

JEERA 14660 +0.96

MUSTARDSEED 4052 -1.24

REF. SOY OIL 568.3 +0.31

SUGAR M GRADE 7362 +3.98

TURMERIC 1501 +0.67

DAILY REPORT

10th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RBI Reference Rate

Currency Rate Currency Rate

Rupee- $ 63.8061 Yen-100 51.1300

Euro 69.6571 GBP 98.9250

CURRENCY

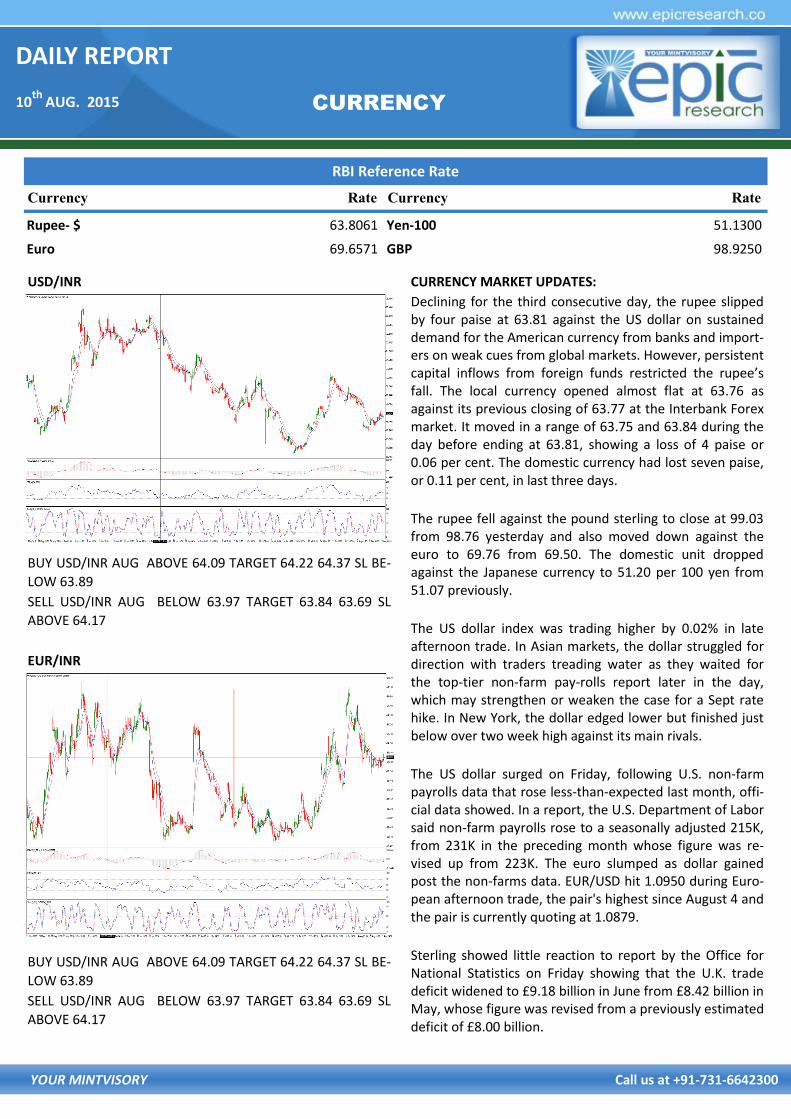

USD/INR

BUY USD/INR AUG ABOVE 64.09 TARGET 64.22 64.37 SL BE-

LOW 63.89

SELL USD/INR AUG BELOW 63.97 TARGET 63.84 63.69 SL

ABOVE 64.17

EUR/INR

BUY USD/INR AUG ABOVE 64.09 TARGET 64.22 64.37 SL BE-

LOW 63.89

SELL USD/INR AUG BELOW 63.97 TARGET 63.84 63.69 SL

ABOVE 64.17

CURRENCY MARKET UPDATES:

Declining for the third consecutive day, the rupee slipped by four paise at 63.81 against the US dollar on sustained demand for the American currency from banks and import-ers on weak cues from global markets. However, persistent capital inflows from foreign funds restricted the rupee’s fall. The local currency opened almost flat at 63.76 as against its previous closing of 63.77 at the Interbank Forex market. It moved in a range of 63.75 and 63.84 during the day before ending at 63.81, showing a loss of 4 paise or 0.06 per cent. The domestic currency had lost seven paise, or 0.11 per cent, in last three days.

The rupee fell against the pound sterling to close at 99.03 from 98.76 yesterday and also moved down against the euro to 69.76 from 69.50. The domestic unit dropped against the Japanese currency to 51.20 per 100 yen from 51.07 previously.

The US dollar index was trading higher by 0.02% in late afternoon trade. In Asian markets, the dollar struggled for direction with traders treading water as they waited for the top-tier non-farm pay-rolls report later in the day, which may strengthen or weaken the case for a Sept rate hike. In New York, the dollar edged lower but finished just below over two week high against its main rivals.

The US dollar surged on Friday, following U.S. non-farm payrolls data that rose less-than-expected last month, offi-cial data showed. In a report, the U.S. Department of Labor said non-farm payrolls rose to a seasonally adjusted 215K, from 231K in the preceding month whose figure was re-vised up from 223K. The euro slumped as dollar gained post the non-farms data. EUR/USD hit 1.0950 during Euro-pean afternoon trade, the pair's highest since August 4 and the pair is currently quoting at 1.0879.

Sterling showed little reaction to report by the Office for National Statistics on Friday showing that the U.K. trade deficit widened to £9.18 billion in June from £8.42 billion in May, whose figure was revised from a previously estimated deficit of £8.00 billion.

DAILY REPORT

10th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

CALL REPORT

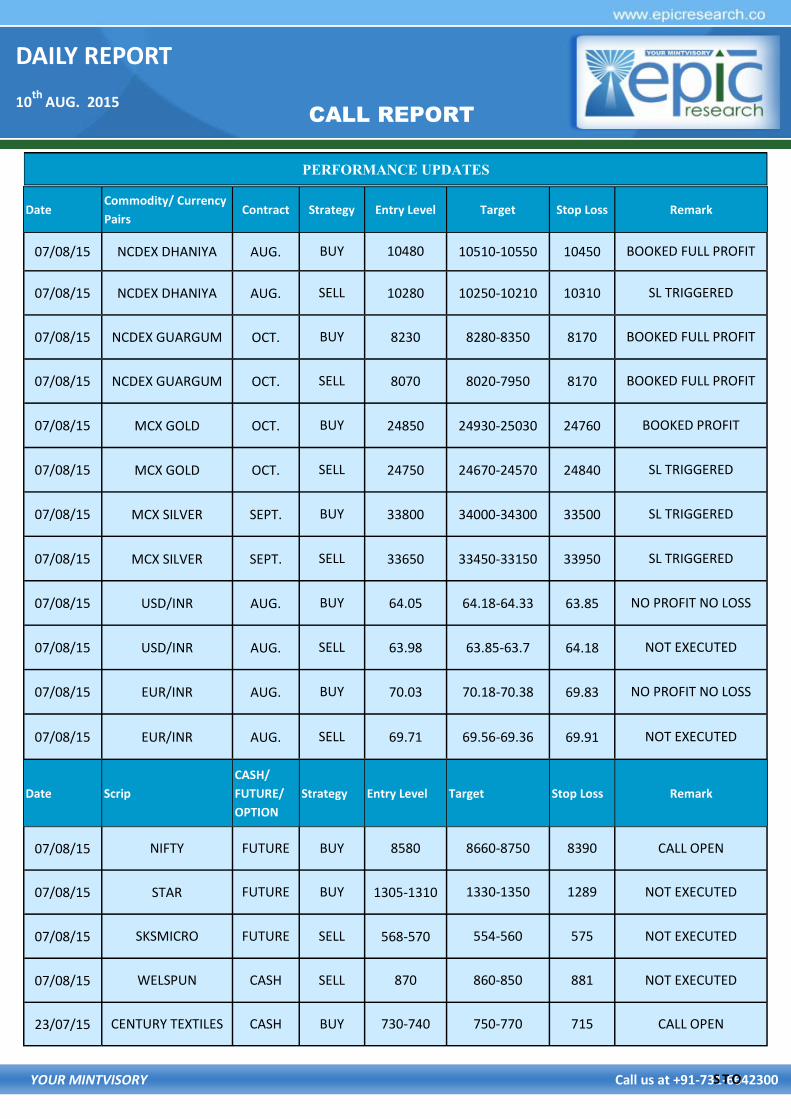

S T O

PERFORMANCE UPDATES

Date Commodity/ Currency

Pairs Contract Strategy Entry Level Target Stop Loss Remark

07/08/15 NCDEX DHANIYA AUG. BUY 10480 10510-10550 10450 BOOKED FULL PROFIT

07/08/15 NCDEX DHANIYA AUG. SELL 10280 10250-10210 10310 SL TRIGGERED

07/08/15 NCDEX GUARGUM OCT. BUY 8230 8280-8350 8170 BOOKED FULL PROFIT

07/08/15 NCDEX GUARGUM OCT. SELL 8070 8020-7950 8170 BOOKED FULL PROFIT

07/08/15 MCX GOLD OCT. BUY 24850 24930-25030 24760 BOOKED PROFIT

07/08/15 MCX GOLD OCT. SELL 24750 24670-24570 24840 SL TRIGGERED

07/08/15 MCX SILVER SEPT. BUY 33800 34000-34300 33500 SL TRIGGERED

07/08/15 MCX SILVER SEPT. SELL 33650 33450-33150 33950 SL TRIGGERED

07/08/15 USD/INR AUG. BUY 64.05 64.18-64.33 63.85 NO PROFIT NO LOSS

07/08/15 USD/INR AUG. SELL 63.98 63.85-63.7 64.18 NOT EXECUTED

07/08/15 EUR/INR AUG. BUY 70.03 70.18-70.38 69.83 NO PROFIT NO LOSS

07/08/15 EUR/INR AUG. SELL 69.71 69.56-69.36 69.91 NOT EXECUTED

Date Scrip

CASH/

FUTURE/

OPTION

Strategy Entry Level Target Stop Loss Remark

07/08/15 NIFTY FUTURE BUY 8580 8660-8750 8390 CALL OPEN

07/08/15 STAR FUTURE BUY 1305-1310 1330-1350 1289 NOT EXECUTED

07/08/15 SKSMICRO FUTURE SELL 568-570 554-560 575 NOT EXECUTED

07/08/15 WELSPUN CASH SELL 870 860-850 881 NOT EXECUTED

23/07/15 CENTURY TEXTILES CASH BUY 730-740 750-770 715 CALL OPEN

DAILY REPORT

10th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NEXT WEEK'S U.S. ECONOMIC REPORTS

ECONOMIC CALENDAR

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any

responsibility (or liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most. Sincere ef-

forts have been made to present the right investment perspective. The information contained herein is based on analysis and up on sources

that we consider reliable. This material is for personal information and based upon it & takes no responsibility. The information given

herein should be treated as only factor, while making investment decision. The report does not provide individually tailor-made invest-

ment advice. Epic research recommends that investors independently evaluate particular investments and strategies, and encourages in-

vestors to seek the advice of a financial adviser. Epic research shall not be responsible for any transaction conducted based on the infor-

mation given in this report, which is in violation of rules and regulations of NSE and BSE. The share price projections shown are not nec-

essarily indicative of future price performance. The information herein, together with all estimates and forecasts, can change without no-

tice. Analyst or any person related to epic research might be holding positions in the stocks recommended. It is understood that anyone

who is browsing through the site has done so at his free will and does not read any views expressed as a recommendation for which either

the site or its owners or anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this dis-

claimer. All Rights Reserved. Investment in equity & bullion market has its own risks. We, however, do not vouch for the accuracy or the

completeness thereof. We are not responsible for any loss incurred whatsoever for any financial profits or loss which may arise from the

recommendations above epic research does not purport to be an invitation or an offer to buy or sell any financial instrument. Our Clients

(Paid or Unpaid), any third party or anyone else have no rights to forward or share our calls or SMS or Report or Any Information Pro-

vided by us to/with anyone which is received directly or indirectly by them. If found so then Serious Legal Actions can be taken.

Disclaimer

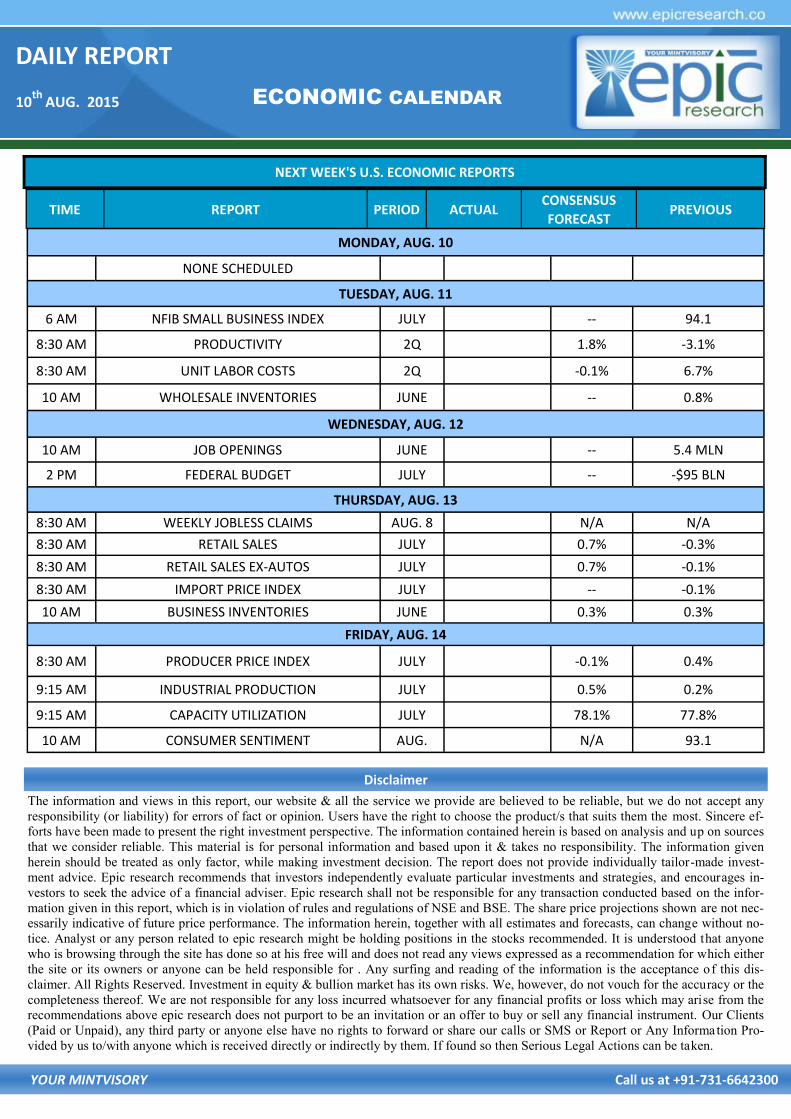

TIME REPORT PERIOD ACTUAL CONSENSUS

FORECAST PREVIOUS

MONDAY, AUG. 10

NONE SCHEDULED

TUESDAY, AUG. 11

6 AM NFIB SMALL BUSINESS INDEX JULY -- 94.1

8:30 AM PRODUCTIVITY 2Q 1.8% -3.1%

8:30 AM UNIT LABOR COSTS 2Q -0.1% 6.7%

10 AM WHOLESALE INVENTORIES JUNE -- 0.8%

WEDNESDAY, AUG. 12

10 AM JOB OPENINGS JUNE -- 5.4 MLN

2 PM FEDERAL BUDGET JULY -- -$95 BLN

THURSDAY, AUG. 13

8:30 AM WEEKLY JOBLESS CLAIMS AUG. 8 N/A N/A

8:30 AM RETAIL SALES JULY 0.7% -0.3%

8:30 AM RETAIL SALES EX-AUTOS JULY 0.7% -0.1%

8:30 AM IMPORT PRICE INDEX JULY -- -0.1%

10 AM BUSINESS INVENTORIES JUNE 0.3% 0.3%

FRIDAY, AUG. 14

8:30 AM PRODUCER PRICE INDEX JULY -0.1% 0.4%

9:15 AM INDUSTRIAL PRODUCTION JULY 0.5% 0.2%

9:15 AM CAPACITY UTILIZATION JULY 78.1% 77.8%

10 AM CONSUMER SENTIMENT AUG. N/A 93.1