Epic research special report of 03 aug 2015

8

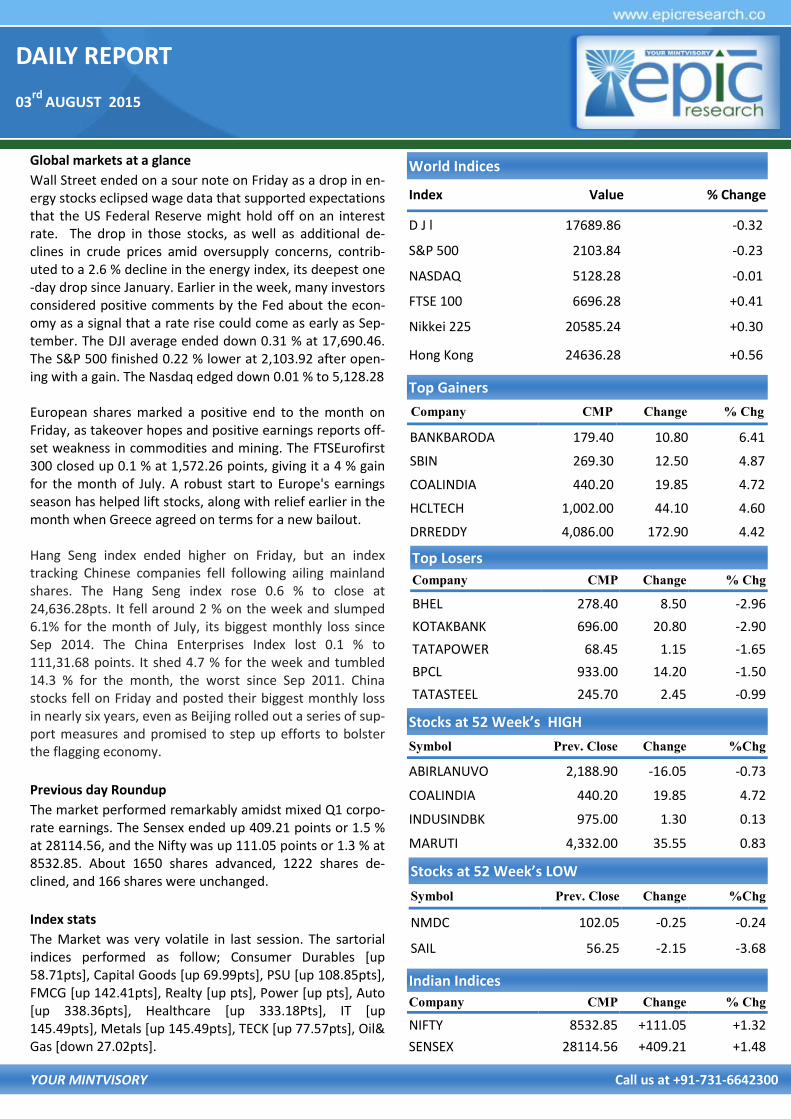

DAILY REPORT 03 rd AUGUST 2015 YOUR MINTVISORY Call us at +91-731-6642300 Global markets at a glance Wall Street ended on a sour note on Friday as a drop in en- ergy stocks eclipsed wage data that supported expectations that the US Federal Reserve might hold off on an interest rate. The drop in those stocks, as well as additional de- clines in crude prices amid oversupply concerns, contrib- uted to a 2.6 % decline in the energy index, its deepest one -day drop since January. Earlier in the week, many investors considered positive comments by the Fed about the econ- omy as a signal that a rate rise could come as early as Sep- tember. The DJI average ended down 0.31 % at 17,690.46. The S&P 500 finished 0.22 % lower at 2,103.92 after open- ing with a gain. The Nasdaq edged down 0.01 % to 5,128.28 European shares marked a positive end to the month on Friday, as takeover hopes and positive earnings reports off- set weakness in commodities and mining. The FTSEurofirst 300 closed up 0.1 % at 1,572.26 points, giving it a 4 % gain for the month of July. A robust start to Europe's earnings season has helped lift stocks, along with relief earlier in the month when Greece agreed on terms for a new bailout. Hang Seng index ended higher on Friday, but an index tracking Chinese companies fell following ailing mainland shares. The Hang Seng index rose 0.6 % to close at 24,636.28pts. It fell around 2 % on the week and slumped 6.1% for the month of July, its biggest monthly loss since Sep 2014. The China Enterprises Index lost 0.1 % to 111,31.68 points. It shed 4.7 % for the week and tumbled 14.3 % for the month, the worst since Sep 2011. China stocks fell on Friday and posted their biggest monthly loss in nearly six years, even as Beijing rolled out a series of sup- port measures and promised to step up efforts to bolster the flagging economy. Previous day Roundup The market performed remarkably amidst mixed Q1 corpo- rate earnings. The Sensex ended up 409.21 points or 1.5 % at 28114.56, and the Nifty was up 111.05 points or 1.3 % at 8532.85. About 1650 shares advanced, 1222 shares de- clined, and 166 shares were unchanged. Index stats The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [up 58.71pts], Capital Goods [up 69.99pts], PSU [up 108.85pts], FMCG [up 142.41pts], Realty [up pts], Power [up pts], Auto [up 338.36pts], Healthcare [up 333.18Pts], IT [up 145.49pts], Metals [up 145.49pts], TECK [up 77.57pts], Oil& Gas [down 27.02pts]. World Indices Index Value % Change D J l 17689.86 -0.32 S&P 500 2103.84 -0.23 NASDAQ 5128.28 -0.01 FTSE 100 6696.28 +0.41 Nikkei 225 20585.24 +0.30 Hong Kong 24636.28 +0.56 Top Gainers Company CMP Change % Chg BANKBARODA 179.40 10.80 6.41 SBIN 269.30 12.50 4.87 COALINDIA 440.20 19.85 4.72 HCLTECH 1,002.00 44.10 4.60 DRREDDY 4,086.00 172.90 4.42 Top Losers Company CMP Change % Chg BHEL 278.40 8.50 -2.96 KOTAKBANK 696.00 20.80 -2.90 TATAPOWER 68.45 1.15 -1.65 BPCL 933.00 14.20 -1.50 TATASTEEL 245.70 2.45 -0.99 Stocks at 52 Week’s HIGH Symbol Prev. Close Change %Chg ABIRLANUVO 2,188.90 -16.05 -0.73 COALINDIA 440.20 19.85 4.72 INDUSINDBK 975.00 1.30 0.13 MARUTI 4,332.00 35.55 0.83 Indian Indices Company CMP Change % Chg NIFTY 8532.85 +111.05 +1.32 SENSEX 28114.56 +409.21 +1.48 Stocks at 52 Week’s LOW Symbol Prev. Close Change %Chg NMDC 102.05 -0.25 -0.24 SAIL 56.25 -2.15 -3.68

-

Upload

epic-research-private-limited -

Category

Business

-

view

156 -

download

2

Transcript of Epic research special report of 03 aug 2015

DAILY REPORT

03rd

AUGUST 2015

YOUR MINTVISORY Call us at +91-731-6642300

Global markets at a glance

Wall Street ended on a sour note on Friday as a drop in en-ergy stocks eclipsed wage data that supported expectations that the US Federal Reserve might hold off on an interest rate. The drop in those stocks, as well as additional de-clines in crude prices amid oversupply concerns, contrib-uted to a 2.6 % decline in the energy index, its deepest one-day drop since January. Earlier in the week, many investors considered positive comments by the Fed about the econ-omy as a signal that a rate rise could come as early as Sep-tember. The DJI average ended down 0.31 % at 17,690.46. The S&P 500 finished 0.22 % lower at 2,103.92 after open-ing with a gain. The Nasdaq edged down 0.01 % to 5,128.28 European shares marked a positive end to the month on Friday, as takeover hopes and positive earnings reports off-set weakness in commodities and mining. The FTSEurofirst 300 closed up 0.1 % at 1,572.26 points, giving it a 4 % gain for the month of July. A robust start to Europe's earnings season has helped lift stocks, along with relief earlier in the month when Greece agreed on terms for a new bailout. Hang Seng index ended higher on Friday, but an index tracking Chinese companies fell following ailing mainland shares. The Hang Seng index rose 0.6 % to close at 24,636.28pts. It fell around 2 % on the week and slumped 6.1% for the month of July, its biggest monthly loss since Sep 2014. The China Enterprises Index lost 0.1 % to 111,31.68 points. It shed 4.7 % for the week and tumbled 14.3 % for the month, the worst since Sep 2011. China stocks fell on Friday and posted their biggest monthly loss in nearly six years, even as Beijing rolled out a series of sup-port measures and promised to step up efforts to bolster the flagging economy.

Previous day Roundup

The market performed remarkably amidst mixed Q1 corpo-rate earnings. The Sensex ended up 409.21 points or 1.5 % at 28114.56, and the Nifty was up 111.05 points or 1.3 % at 8532.85. About 1650 shares advanced, 1222 shares de-clined, and 166 shares were unchanged.

Index stats

The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [up 58.71pts], Capital Goods [up 69.99pts], PSU [up 108.85pts], FMCG [up 142.41pts], Realty [up pts], Power [up pts], Auto [up 338.36pts], Healthcare [up 333.18Pts], IT [up 145.49pts], Metals [up 145.49pts], TECK [up 77.57pts], Oil& Gas [down 27.02pts].

World Indices

Index Value % Change

D J l 17689.86 -0.32

S&P 500 2103.84 -0.23

NASDAQ 5128.28 -0.01

FTSE 100 6696.28 +0.41

Nikkei 225 20585.24 +0.30

Hong Kong 24636.28 +0.56

Top Gainers

Company CMP Change % Chg

BANKBARODA 179.40 10.80 6.41

SBIN 269.30 12.50 4.87

COALINDIA 440.20 19.85 4.72

HCLTECH 1,002.00 44.10 4.60

DRREDDY 4,086.00 172.90 4.42

Top Losers

Company CMP Change % Chg

BHEL 278.40 8.50 -2.96

KOTAKBANK 696.00 20.80 -2.90

TATAPOWER 68.45 1.15 -1.65

BPCL 933.00 14.20 -1.50

TATASTEEL 245.70 2.45 -0.99

Stocks at 52 Week’s HIGH

Symbol Prev. Close Change %Chg

ABIRLANUVO 2,188.90 -16.05 -0.73

COALINDIA 440.20 19.85 4.72

INDUSINDBK 975.00 1.30 0.13

MARUTI 4,332.00 35.55 0.83

Indian Indices

Company CMP Change % Chg

NIFTY 8532.85 +111.05 +1.32

SENSEX 28114.56 +409.21 +1.48

Stocks at 52 Week’s LOW

Symbol Prev. Close Change %Chg

NMDC 102.05 -0.25 -0.24

SAIL 56.25 -2.15 -3.68

DAILY REPORT

03rd

AUGUST 2015

YOUR MINTVISORY Call us at +91-731-6642300

STOCK RECOMMENDATION [CASH]

1. RAJESH EXPROT (CASH)

After correcting in last three session RAJESHEXPORT bounced from 454 and finished with 13.31% on EOD chart while it made life time high of 556.70 so if it cross 530 level then we can see new high in upcoming session so we ad-vise to buy in intraday above 530 use strict stop loss of 520 for target of 537-545-555.

MACRO NEWS

L&T Q1 profit misses forecast, tanks 37%. Revenue in-line, up 6.7%. Order inflows decline 21%

Titan Q1 net dips 15% to Rs 151cr; jewellery sales sink 11%

Sun TV Q1 net up 19% to Rs 197.28cr, ad revenue grows 16%

ICICI Bank Q1 profit rises 12%, retail loan surges 25%, asset quality improves

Strides Arcolab gets USFDA nod for Benzonatate cap-sules

Bombay HC tells FSSAI, Nestle to retest Maggie samples

Core sector growth slows to 3% in June from 4.4% in May

Govt planning to deduct part of subsidies to boost de-mand

USFDA denies approval for SPARC's anti-glaucoma eye-drop

PSBs get new treasury of Rs 70,000 crore to address the issue of bad loans

India closer to nod for 100 per cent biofuel; draft re-leased for emission standards

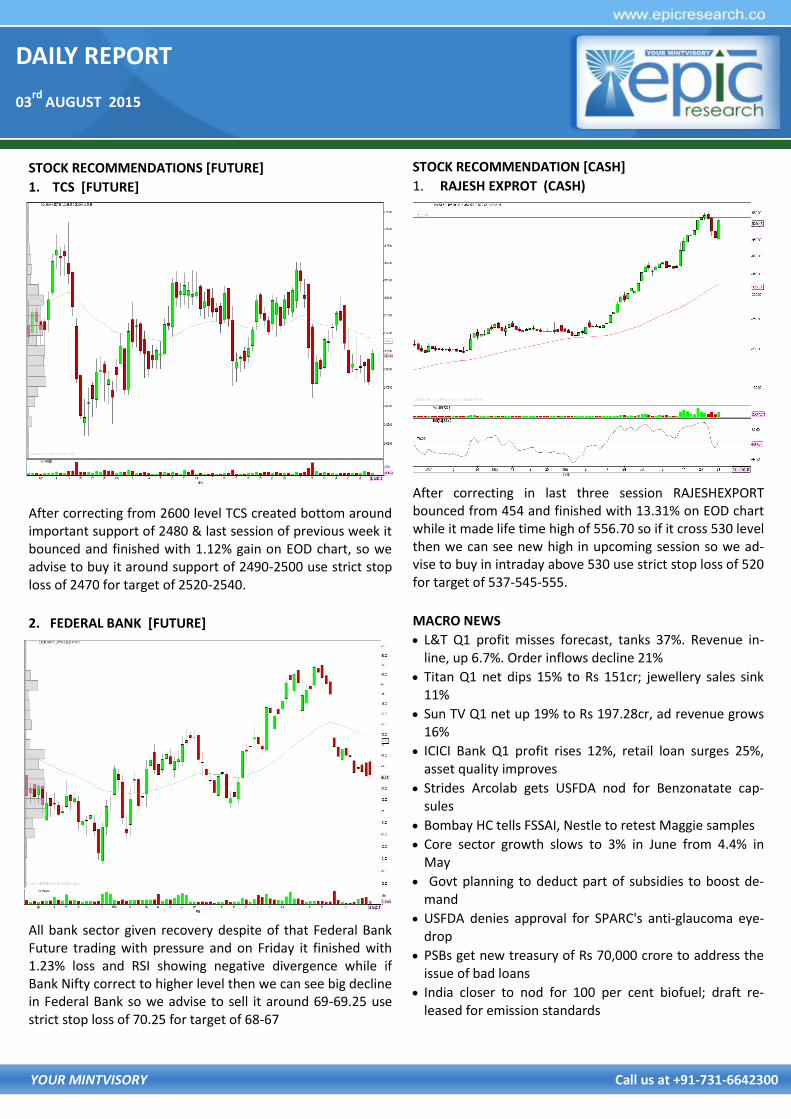

STOCK RECOMMENDATIONS [FUTURE]

1. TCS [FUTURE]

After correcting from 2600 level TCS created bottom around important support of 2480 & last session of previous week it bounced and finished with 1.12% gain on EOD chart, so we advise to buy it around support of 2490-2500 use strict stop loss of 2470 for target of 2520-2540.

2. FEDERAL BANK [FUTURE]

All bank sector given recovery despite of that Federal Bank Future trading with pressure and on Friday it finished with 1.23% loss and RSI showing negative divergence while if Bank Nifty correct to higher level then we can see big decline in Federal Bank so we advise to sell it around 69-69.25 use strict stop loss of 70.25 for target of 68-67

DAILY REPORT

03rd

AUGUST 2015

YOUR MINTVISORY Call us at +91-731-6642300

FUTURE & OPTION

MOST ACTIVE PUT OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY PE 8,400 64.25 4,09,302 31,18,600

NIFTY PE 8,500 94.50 3,11,588 20,03,825

BANKNIFTY PE 18,000 129.55 27,398 2,49,725

ICICIBANK PE 290 4.90 5,373 11,40,000

LT PE 1,700 25.50 5,224 2,20,750

ICICIBANK PE 300 8.65 4,705 12,50,000

RELIANCE PE 1,000 21.50 2,892 3,85,250

SBIN PE 250 2.80 2,380 13,46,000

MOST ACTIVE CALL OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY CE 8,700 66.20 4,38,331 32,42,625

NIFTY CE 8,800 37.60 3,37,621 34,92,900

BANKNIFTY CE 19,000 323.00 45,220 3,56,350

ICICIBANK CE 310 7.40 11,286 37,91,000

ICICIBANK CE 300 11.80 9,167 19,90,000

LT CE 1,900 23.65 5,677 2,17,125

SBIN CE 300 2.10 4,680 15,93,000

RELIANCE CE 1,020 19.00 4,447 4,74,750

FII DERIVATIVES STATISTICS

BUY OPEN INTEREST AT THE END OF THE DAY SELL

No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores NET AMOUNT

INDEX FUTURES 105490 2508.03 59484 1353.41 624228 14762.83 1154.62

INDEX OPTIONS 474316 11930.71 427213 10590.67 2288804 61237.57 1340.04

STOCK FUTURES 118212 3380.31 108130 3038.98 1757951 48654.68 341.33

STOCK OPTIONS 72755 1967.87 67024 1809.62 49538 1352.82 158.25

TOTAL 2994.23

STOCKS IN NEWS Tata Power to launch app for consumers in six months

Maruti Suzuki July sales spike 20.1%, passenger cars lead

NTPC signs JV with Jharkhand for Patratu Power Plant

CESC lines up Rs 3,000 crore for renewables, acquisi-tions on radar

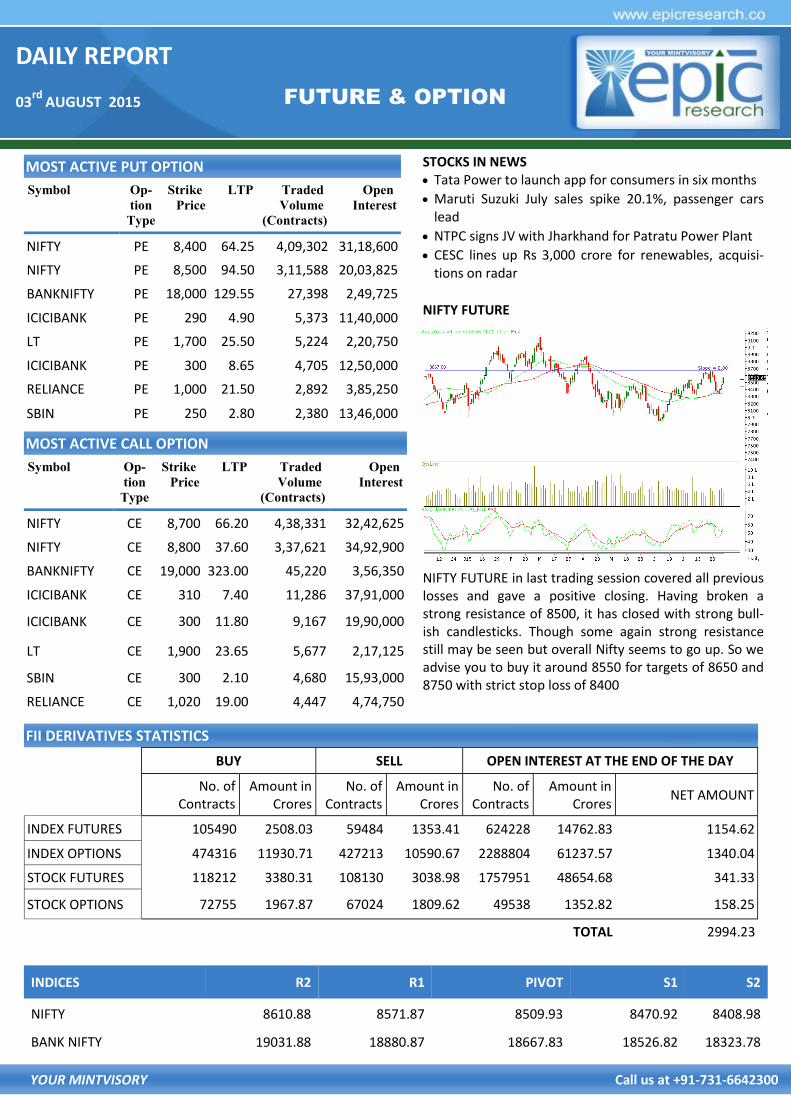

NIFTY FUTURE

NIFTY FUTURE in last trading session covered all previous losses and gave a positive closing. Having broken a strong resistance of 8500, it has closed with strong bull-ish candlesticks. Though some again strong resistance still may be seen but overall Nifty seems to go up. So we advise you to buy it around 8550 for targets of 8650 and 8750 with strict stop loss of 8400

INDICES R2 R1 PIVOT S1 S2

NIFTY 8610.88 8571.87 8509.93 8470.92 8408.98

BANK NIFTY 19031.88 18880.87 18667.83 18526.82 18323.78

DAILY REPORT

03rd

AUGUST 2015

YOUR MINTVISORY Call us at +91-731-6642300

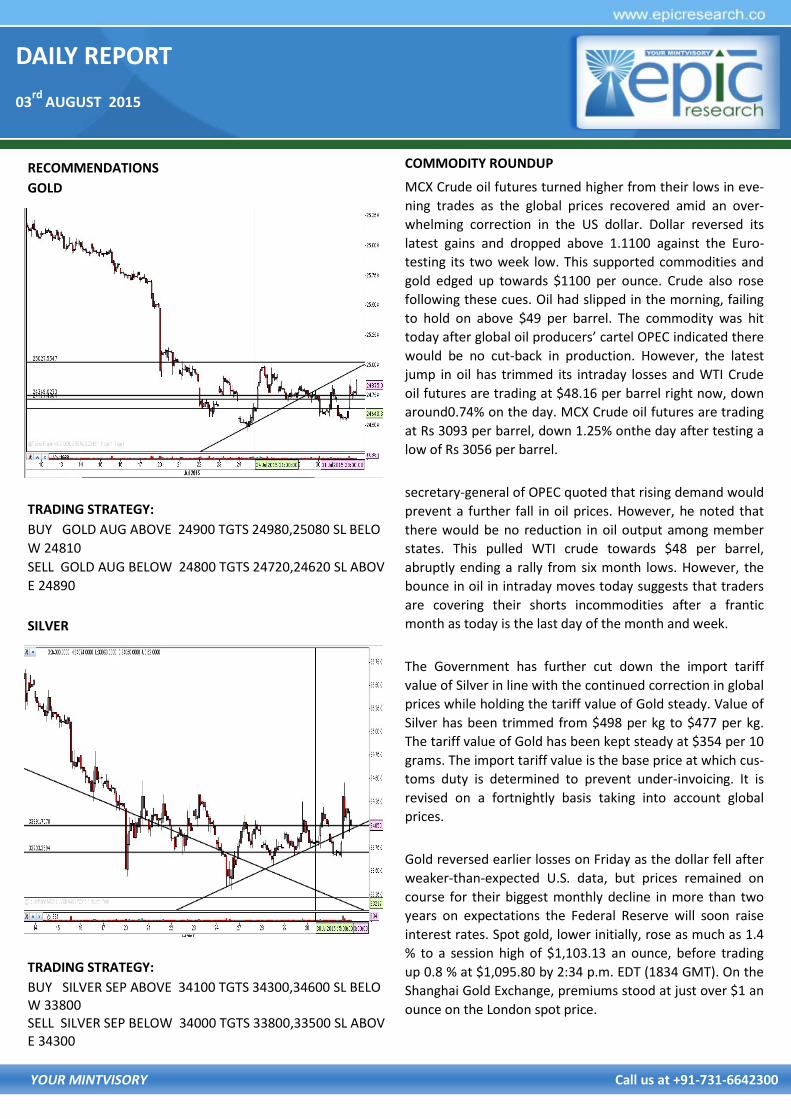

RECOMMENDATIONS

GOLD

TRADING STRATEGY:

BUY GOLD AUG ABOVE 24900 TGTS 24980,25080 SL BELO

W 24810

SELL GOLD AUG BELOW 24800 TGTS 24720,24620 SL ABOV

E 24890

SILVER

TRADING STRATEGY:

BUY SILVER SEP ABOVE 34100 TGTS 34300,34600 SL BELOW 33800 SELL SILVER SEP BELOW 34000 TGTS 33800,33500 SL ABOVE 34300

COMMODITY ROUNDUP

MCX Crude oil futures turned higher from their lows in eve-

ning trades as the global prices recovered amid an over-

whelming correction in the US dollar. Dollar reversed its

latest gains and dropped above 1.1100 against the Euro-

testing its two week low. This supported commodities and

gold edged up towards $1100 per ounce. Crude also rose

following these cues. Oil had slipped in the morning, failing

to hold on above $49 per barrel. The commodity was hit

today after global oil producers’ cartel OPEC indicated there

would be no cut-back in production. However, the latest

jump in oil has trimmed its intraday losses and WTI Crude

oil futures are trading at $48.16 per barrel right now, down

around0.74% on the day. MCX Crude oil futures are trading

at Rs 3093 per barrel, down 1.25% onthe day after testing a

low of Rs 3056 per barrel.

secretary-general of OPEC quoted that rising demand would

prevent a further fall in oil prices. However, he noted that

there would be no reduction in oil output among member

states. This pulled WTI crude towards $48 per barrel,

abruptly ending a rally from six month lows. However, the

bounce in oil in intraday moves today suggests that traders

are covering their shorts incommodities after a frantic

month as today is the last day of the month and week.

The Government has further cut down the import tariff

value of Silver in line with the continued correction in global

prices while holding the tariff value of Gold steady. Value of

Silver has been trimmed from $498 per kg to $477 per kg.

The tariff value of Gold has been kept steady at $354 per 10

grams. The import tariff value is the base price at which cus-

toms duty is determined to prevent under-invoicing. It is

revised on a fortnightly basis taking into account global

prices.

Gold reversed earlier losses on Friday as the dollar fell after

weaker-than-expected U.S. data, but prices remained on

course for their biggest monthly decline in more than two

years on expectations the Federal Reserve will soon raise

interest rates. Spot gold, lower initially, rose as much as 1.4

% to a session high of $1,103.13 an ounce, before trading

up 0.8 % at $1,095.80 by 2:34 p.m. EDT (1834 GMT). On the

Shanghai Gold Exchange, premiums stood at just over $1 an

ounce on the London spot price.

DAILY REPORT

03rd

AUGUST 2015

YOUR MINTVISORY Call us at +91-731-6642300

NCDEX

RECOMMENDATIONS

DHANIYA

BUY CORIANDER AUG ABOVE 11410 TARGET 11435 11475 S

L BELOW 11380

SELL CORIANDER AUG BELOW 11225 TARGET 11200 11160

SL ABOVE 11255

GUARSGUM

BUY GUARGUM OCT ABOVE 8170 TARGET 8220 8290 SL BE

LOW 8110

SELL GUARGUM OCT BELOW 7980 TARGET 7930 7860 SL

ABOVE 8040

NCDEX ROUNDUP

NCDEX Chana futures have lost heavy ground after sliding from highs above Rs 5000 per quintal at the start of June 2015. The counter currently trades at Rs 4646 per quintal, down 0.34% on the day amid continued short selling. The open interest in the counter surged nearly 10% today, indi-cating continued short selling by traders amid hopes of a strong Kharif pulses harvest.

Turmeric futures also dropped following the monsoon cues and less upcountry demand. The NCDEX Turmeric futures for August are trading at Rs 7104 per quintal, down 0.84% on the day. Supplies are steady in Nizamabad mandi and traders are not interested in buying in futures market after the counter tested a contract low near Rs 6600 per quintal earlier this week. A slide under Rs 7K could trigger a fresh wave of selling.

NCDEX Soybeans futures are trading at Rs 3269 per quintal, down 0.70% for the August delivery. The next deliveries are down around Rs 100 from the August futures, indicating that traders are expecting a further drop in the commodity in coming days as harvest draws near. Much of the sowing in Madhya Pradesh, the soybean bowl of India have been completed by the end of last month, triggering hopes of a sharp increase in the yields.

sharp increase in the yields.

NCDEX INDICES

Index Value % Change

CAETOR SEED 3990 +0.10

CHANA 4590 -0.30

CORIANDER 11226 -1.04

COTTON SEED 1950 -0.86

GUAR SEED 3570 -4.01

JEERA 15050 -2.02

MUSTARDSEED 4197 +0.55

REF. SOY OIL 578.1 +0.40

SUGAR M GRADE 060 -1.45

TURMERIC 1516 -0.39

DAILY REPORT

03rd

AUGUST 2015

YOUR MINTVISORY Call us at +91-731-6642300

RBI Reference Rate

Currency Rate Currency Rate

Rupee- $ 64.0054 Yen-100 51.5500

Euro 70.1627 GBP 99.8356

CURRENCY

USD/INR

BUY USD/INR AUG ABOVE 64.55 TARGET 64.68 64.83 SL BE-LOW 64.35

SELL USD/INR AUG BELOW 64.4 TARGET 64.27 64.12 SL ABOVE 64.6

EUR/INR

BUY EUR/INR AUG ABOVE 70.9 TARGET 71.05 71.25 SL BE-LOW 70.7

SELL EUR/INR AUG BELOW 70.68 TARGET 70.53 70.33 SL ABOVE 70.88

CURRENCY MARKET UPDATES:

TThe rupee slipped further by 9 paise to end at 64.13

against the US dollar on sustained demand for the Ameri-

can currency from banks and importers despite weak over-

seas sentiment. Notwithstanding strong rally in domestic

equity markets, month-end demand for the dollar from

importers predominantly weighed on the rupee, forex

dealers said. Besides, sustained capital outflows pressur-

ized the local currency. The rupee resumed substantially

lower at 64.10 against Thursday closing level of 64.04 at

the Interbank Forex on increased dollar demand from im-

porters. However, it witnessed a sharp rebound to touch

an intra-day high of 63.9850 before sliding back to hit a

fresh low of 64.17 and closed at 64.13, revealing a loss of 9

paise, or 0.14%.

The dollar eased against other major currencies ahead of

key macro data, including upcoming US consumer senti-

ment. The US dollar index, which measures the green-

back's strength against a trade-weighted basket of six ma-

jor currencies, was down by 0.19 per cent at 97.42. Mean-

while, FPIs remained net sellers and sold shares worth a

net Rs 170.68 crore yesterday.

The US dollar eased in European trades and helped Gold

launch an amazing turn around from its five and half year

lows near $1080 per ounce today. The metal stayed under

stress yesterday after the US real gross domestic product

increased at an annual rate of 2.3% in the second quarter

compared to expectations for an increase of about 2.6%.

Markets remained focused on a rate hike from the US Fed

in September after the data as the US Commerce Depart-

ment also revealed a notable upward revision to the data

for the first quarter. The first quarter GDP rose by an up-

wardly revised 0.6% compared to the 0.2%contraction that

had been reported. However, bulk of these losses have

been covered now and the metal currently quotes at

$1094 per ounce, up half a % on the day. The Dollar has

eased from one week high against the Euro and currently

trades at 1.1140 mark.

DAILY REPORT

03rd

AUGUST 2015

YOUR MINTVISORY Call us at +91-731-6642300

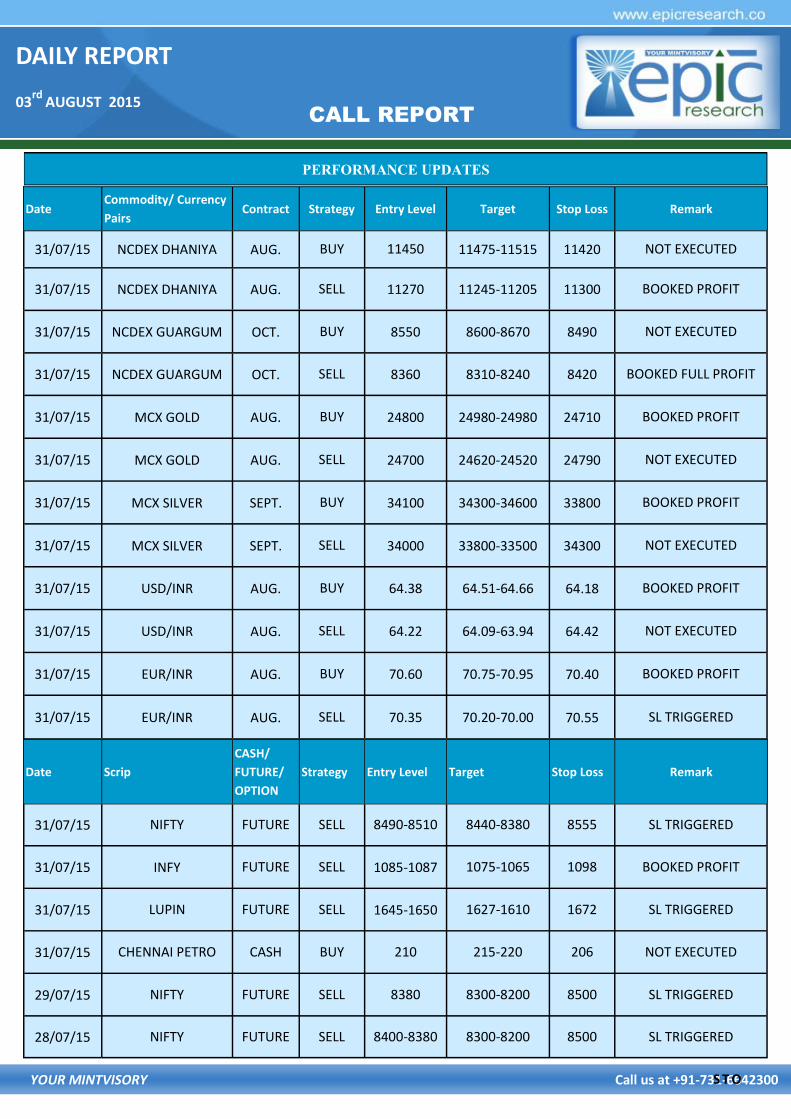

CALL REPORT

S T O

PERFORMANCE UPDATES

Date Commodity/ Currency

Pairs Contract Strategy Entry Level Target Stop Loss Remark

31/07/15 NCDEX DHANIYA AUG. BUY 11450 11475-11515 11420 NOT EXECUTED

31/07/15 NCDEX DHANIYA AUG. SELL 11270 11245-11205 11300 BOOKED PROFIT

31/07/15 NCDEX GUARGUM OCT. BUY 8550 8600-8670 8490 NOT EXECUTED

31/07/15 NCDEX GUARGUM OCT. SELL 8360 8310-8240 8420 BOOKED FULL PROFIT

31/07/15 MCX GOLD AUG. BUY 24800 24980-24980 24710 BOOKED PROFIT

31/07/15 MCX GOLD AUG. SELL 24700 24620-24520 24790 NOT EXECUTED

31/07/15 MCX SILVER SEPT. BUY 34100 34300-34600 33800 BOOKED PROFIT

31/07/15 MCX SILVER SEPT. SELL 34000 33800-33500 34300 NOT EXECUTED

31/07/15 USD/INR AUG. BUY 64.38 64.51-64.66 64.18 BOOKED PROFIT

31/07/15 USD/INR AUG. SELL 64.22 64.09-63.94 64.42 NOT EXECUTED

31/07/15 EUR/INR AUG. BUY 70.60 70.75-70.95 70.40 BOOKED PROFIT

31/07/15 EUR/INR AUG. SELL 70.35 70.20-70.00 70.55 SL TRIGGERED

Date Scrip

CASH/

FUTURE/

OPTION

Strategy Entry Level Target Stop Loss Remark

31/07/15 NIFTY FUTURE SELL 8490-8510 8440-8380 8555 SL TRIGGERED

31/07/15 INFY FUTURE SELL 1085-1087 1075-1065 1098 BOOKED PROFIT

31/07/15 LUPIN FUTURE SELL 1645-1650 1627-1610 1672 SL TRIGGERED

31/07/15 CHENNAI PETRO CASH BUY 210 215-220 206 NOT EXECUTED

29/07/15 NIFTY FUTURE SELL 8380 8300-8200 8500 SL TRIGGERED

28/07/15 NIFTY FUTURE SELL 8400-8380 8300-8200 8500 SL TRIGGERED

DAILY REPORT

03rd

AUGUST 2015

YOUR MINTVISORY Call us at +91-731-6642300

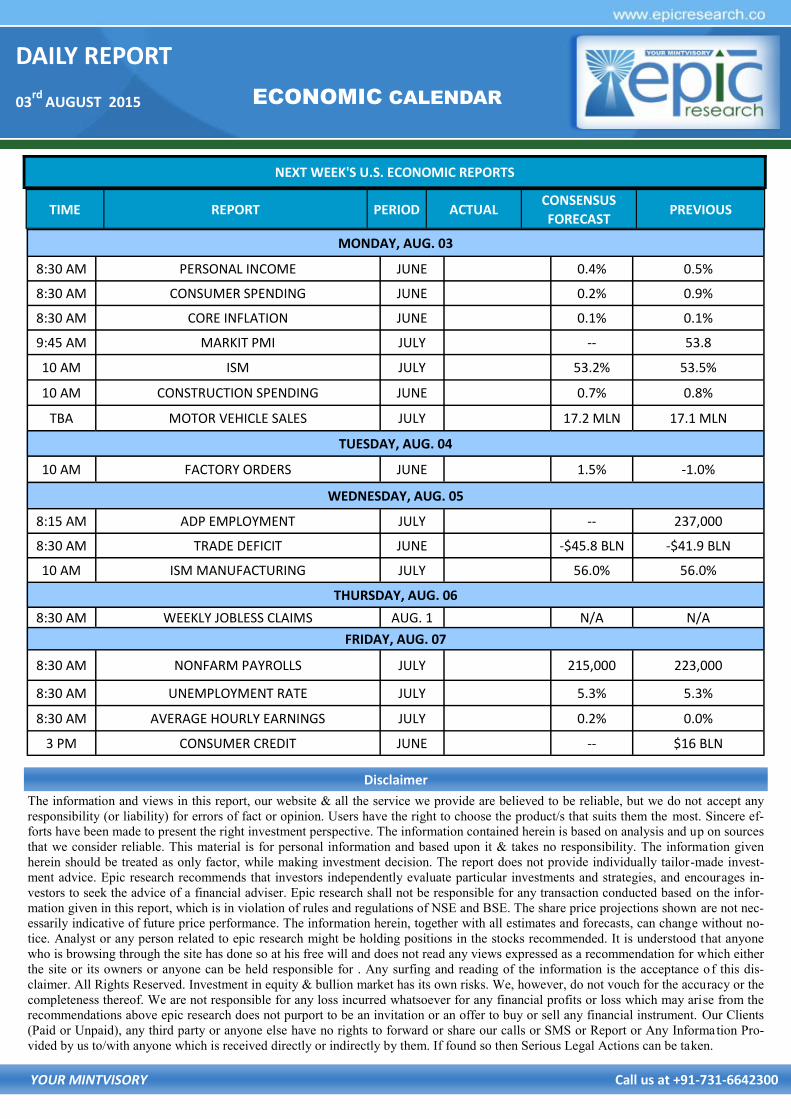

NEXT WEEK'S U.S. ECONOMIC REPORTS

ECONOMIC CALENDAR

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any

responsibility (or liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most. Sincere ef-

forts have been made to present the right investment perspective. The information contained herein is based on analysis and up on sources

that we consider reliable. This material is for personal information and based upon it & takes no responsibility. The information given

herein should be treated as only factor, while making investment decision. The report does not provide individually tailor-made invest-

ment advice. Epic research recommends that investors independently evaluate particular investments and strategies, and encourages in-

vestors to seek the advice of a financial adviser. Epic research shall not be responsible for any transaction conducted based on the infor-

mation given in this report, which is in violation of rules and regulations of NSE and BSE. The share price projections shown are not nec-

essarily indicative of future price performance. The information herein, together with all estimates and forecasts, can change without no-

tice. Analyst or any person related to epic research might be holding positions in the stocks recommended. It is understood that anyone

who is browsing through the site has done so at his free will and does not read any views expressed as a recommendation for which either

the site or its owners or anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this dis-

claimer. All Rights Reserved. Investment in equity & bullion market has its own risks. We, however, do not vouch for the accuracy or the

completeness thereof. We are not responsible for any loss incurred whatsoever for any financial profits or loss which may arise from the

recommendations above epic research does not purport to be an invitation or an offer to buy or sell any financial instrument. Our Clients

(Paid or Unpaid), any third party or anyone else have no rights to forward or share our calls or SMS or Report or Any Information Pro-

vided by us to/with anyone which is received directly or indirectly by them. If found so then Serious Legal Actions can be taken.

Disclaimer

TIME REPORT PERIOD ACTUAL CONSENSUS

FORECAST PREVIOUS

MONDAY, AUG. 03

8:30 AM PERSONAL INCOME JUNE 0.4% 0.5%

8:30 AM CONSUMER SPENDING JUNE 0.2% 0.9%

8:30 AM CORE INFLATION JUNE 0.1% 0.1%

9:45 AM MARKIT PMI JULY -- 53.8

10 AM ISM JULY 53.2% 53.5%

10 AM CONSTRUCTION SPENDING JUNE 0.7% 0.8%

TBA MOTOR VEHICLE SALES JULY 17.2 MLN 17.1 MLN

TUESDAY, AUG. 04

10 AM FACTORY ORDERS JUNE 1.5% -1.0%

WEDNESDAY, AUG. 05

8:15 AM ADP EMPLOYMENT JULY -- 237,000

8:30 AM TRADE DEFICIT JUNE -$45.8 BLN -$41.9 BLN

10 AM ISM MANUFACTURING JULY 56.0% 56.0%

THURSDAY, AUG. 06

8:30 AM WEEKLY JOBLESS CLAIMS AUG. 1 N/A N/A

FRIDAY, AUG. 07

8:30 AM NONFARM PAYROLLS JULY 215,000 223,000

8:30 AM UNEMPLOYMENT RATE JULY 5.3% 5.3%

8:30 AM AVERAGE HOURLY EARNINGS JULY 0.2% 0.0%

3 PM CONSUMER CREDIT JUNE -- $16 BLN