Environmental Tax Reform: Examples from China, Vietnam...

41

Environmental Tax Reform: Examples from China, Vietnam and other developing countries Research Seminar in the Development Research Group, Environment and Energy Team Washington D.C., World Bank, MC 2-850, February 15, 1.00-2.30 p.m. Kai Schlegelmilch Economist Vice President of Green Budget Germany/Europe (GBG/GBE) www.foes.de [email protected]

-

Upload

truongthien -

Category

Documents

-

view

216 -

download

0

Transcript of Environmental Tax Reform: Examples from China, Vietnam...

Environmental Tax Reform:

Examples from China, Vietnam and other

developing countries

Research Seminar in the Development Research Group,

Environment and Energy Team

Washington D.C., World Bank, MC 2-850, February 15, 1.00-2.30

p.m.

Kai SchlegelmilchEconomist

Vice President of Green Budget Germany/Europe (GBG/GBE)

www.foes.de

2

Structure of presentation

1) Introduction of Green Budget Germany (GBG)

2) Need for an Environmental Fiscal Reform (EFR)

3) Recent Developments in Europe

4) EFR Reform Elements in Germany

5) ETR-approaches in China, Barbados, Burkina Faso,

South Africa, Uganda and Vanuatu

6) Conclusions

3

1. Green Budget Germany (GBG)–

Forum Ökologisch-Soziale Marktwirtschaft (FÖS)

• Non-Profit Non-Governmental Organization

– founded in 1994

– Target groups: economy, science and politics

• Fields of expertise

Commitment to Market-Based Instruments in environmental policy such as:

– Environmental Fiscal/Tax Reform: Taxes on energy and resources

– Cutting of environmentally harmful subsidies

– Emissions Trading

– Financial Transaction Tax and Property Tax

• Main activities

Studies and Newsletters

Conferences and Trainings

Examples:

European platform on these topics: Green Budget Europe (GBE) since 2008

Organisation of the Global Conference on Environmental Taxation in 2007

Several studies on environmentally harmful subsidies

4

2. Need for EFR – Changing the tax structure

• Tax structure: diminishing part of environmental

taxes

44,0% 45,8% 47,7% 49,4% 47,0% 46,6% 44,4%

21,1% 20,0% 16,5%17,7% 15,9% 16,3%15,5%

12,6% 11,8% 11,3% 9,3%10,6% 11,7%

11,2%

18,0% 18,3% 18,1% 18,2% 21,0% 20,2%19,3%

4,3% 4,2% 5,1% 6,5% 5,6% 5,1% 9,6%

1980 1990 1998 2003 2010 2013 2015

Environment

Neutral

Capital

Labor

Social

insurances

Tax shift with

additional ETR of

52 Bn. €

ETR

1999-2003

Expectations from 2010

based on official tax

assessment, May 2010

5

2. Why energy prices matter

6

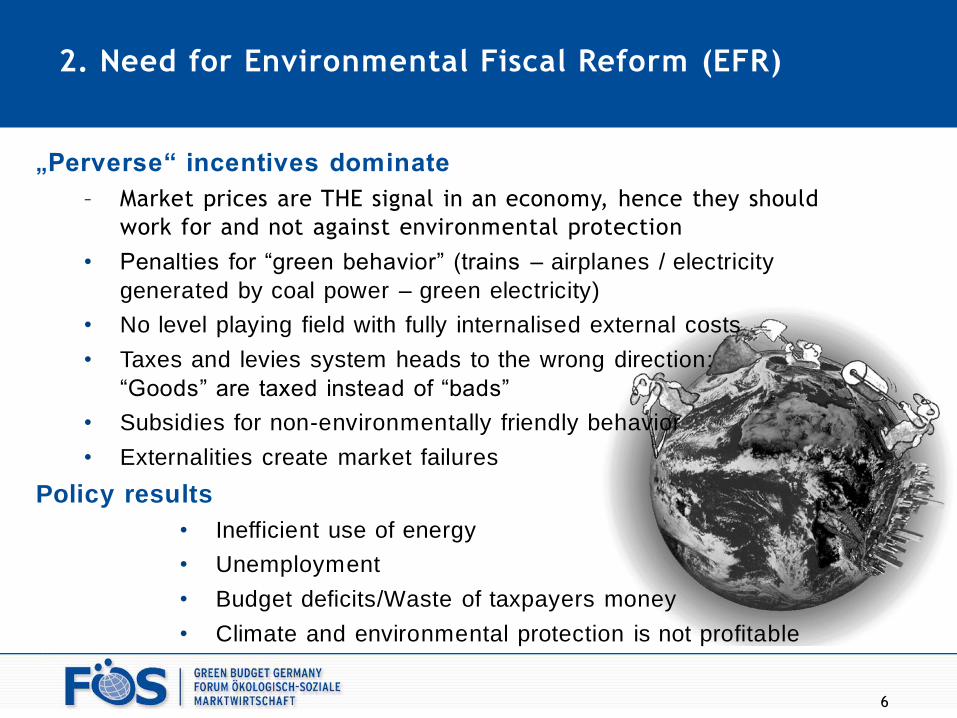

2. Need for Environmental Fiscal Reform (EFR)

„Perverse“ incentives dominate

– Market prices are THE signal in an economy, hence they should

work for and not against environmental protection

• Penalties for “green behavior” (trains – airplanes / electricity

generated by coal power – green electricity)

• No level playing field with fully internalised external costs

• Taxes and levies system heads to the wrong direction:

“Goods” are taxed instead of “bads”

• Subsidies for non-environmentally friendly behavior

• Externalities create market failures

Policy results

• Inefficient use of energy

• Unemployment

• Budget deficits/Waste of taxpayers money

• Climate and environmental protection is not profitable

7

3. History of EFR Reform elements:

Implemented in Europe and intentions beyond

• Debate started more than 20 years ago in the late

1980ies

• In Europe several countries started with first tax

shifts in 1990ies, still ongoing until today.

• On European level, unanimity is required, hence

progress is slow, but in 2004 a minimum energy tax

rates on energy products was established

• 2009 Ireland introduced a carbon tax, 2011 Finland

and Sweden increased their CO2-/energy tax rates

• (Australia plans carbon tax from 2012 – news from

14.2.2011)

8

EU-Average 14,9 149,445

Portugal 21,4 213,830

Netherlands 25,4 254,200

Romania 29,1 291,475

Bulgaria 30,7 306,780

Denmark 33,2 332,426

Hungary 35,8 358,450

Italy 40,3 403,210

Sweden 41,3 412,559

EU-Durchschnitt 149,44493

1,0 1,8 2,1 2,7 2,9

5,6 5,7

5,7 6,1 8

,1 8,6 9,6 1

0,9

10,9

11,1 12,3

13,2

13,5

14,2

14,9

21,4

25,4

29,1 30,7 3

3,2 3

5,8

40,3

41,3

0

5

10

15

20

25

30

35

40

45

Luxem

bourg

Belg

ium

Lit

huania

Slo

vakia

Gre

ece

Latv

ia

Fra

nce

Pola

nd

Germ

any

Fin

land

Spain

Czech R

epublic

Irela

nd

Aust

ria

Est

onia

Slo

venia

Unit

ed K

ingdom

Cypru

s

Malt

a

EU

-Avera

ge

Port

ugal

Neth

erl

ands

Rom

ania

Bulg

ari

a

Denm

ark

Hungary

Italy

Sw

eden

3. Taxes on light heating fuel in Europe (€-

Cent/liter)

Germany still has to catch up in this area

9

4. EFR Reform elements – Implemented in

Germany

• Germany was a late-comer: Left-wing government

introduced the first tax shift in 1999-2003

• Labour taxes were reduced and transport/heating fuel

taxes were increased and an electricity tax was

introduced between 1999-2003

Impacts: - 2-3% CO2-emissions, first time ever lasting

reduction of fuel sales, up to 250,000 additional jobs

created

• Tax subsidies for car transport were reduced several

times

10

4. EFR Reform elements – Implemented in Germany

• Conservative government continued with elements in 2011

• In Germany, there is a cross-party consensus that fiscal elements

help the environment and the fiscal needs

Steps and Elements:

• Hard coal subsidies were reduced and will be phased out by 2018

• 2011 the following elements were introduced:

– Ticket fees in air traffic

– Heavy goods vehicle toll

– Reduction of exemptions from the energy tax

– Accelerated reduction of hard coal subsidies

– Nuclear fuel

• GBG proposed all these elements and more and most was

implemented

11

4. EFR Reform elements – Recently implemented in

Germany

1. Example:

Transport sector: Air traffic

• fastest-growing traffic sector

• numerous financial privileges

• Inclusion of air traffic in European emissions trading

as of 2012 has been decided

– taxation and steering effects of that inclusion will be

comparatively weak, in addition to taking time to

manifest

• difficult to implement EU-wide kerosene tax due to

veto right of each of the 27 EU member states in

matters concerning taxation

12

4. EFR Reform elements – Recently implemented in

Germany

Transport sector: Air traffic

• GBG claimed

– Introduction of a per-flight fee or an airplane tax

France and Kingdom, the main competitors, already had a ticket tax in place. Mainly Germany still served as a tax heaven

• Introduction of a per-flight fee by January 1st 2011

– < 2500 km: 8 Euro, < 6000 km: 25 Euro, > 6000 km: 45 Euro

Additional revenue of 1 bn. Euro p.a.

• GBG recommends

- Differentiating of the fees (Economy and Business Class)

- Including freight transport

13

13

4. EFR Reform elements – Recently implemented in

Germany

2. Example:

Non-internalised costs of nuclear fuels

• Health and environmental (incl. CO2) impacts during

extraction of uranium

• Environmental risks during transportation

• No final deposit of nuclear waste available or in sight

• Danger of severe accidents (Tchernobyl)

• Possible military use

• Possible abuse by terrorists

External costs in Germany alone for the period 1950-

2008 amount to 4.2 and 11,413.4 billion €

14

4. EFR Reform elements – Recently implemented in

Germany

Energy sector: nuclear energy

• GBG claimed

– Internalising external costs for nuclear fuels

• Introduction of a tax on nuclear fuel:

145 Euro/ g Plutonium and Uranium

= 1.0 – 1.5 €-Cent/kWh

• GBG recommends

– Further internalisation of environmental damage costs

– Compensation of all profits resulting from the exclusion

from emissions trading and thus wind fall profits

– 350 Euro/ g Plutonium and Uranium

= 2,5 €-Cent/ kWh, from 2013 on: 3,5 €-Cent/ kWh

15

5. EFR in developing countries

EFR: 3 potential benefits of relevance to developing countries:

• mobilise own revenues for governments, thus getting less dependent on ODA

• improve environmental management and conserve resources

• reduce poverty

16

5. EFR in developing countries

Examples of countries working on EFR:

• Vietnam: Sina is going to present this success story

• China: China Council on International Cooperation on Environment and Development (CCICED) set up task-force in 2008 to examine potential for environmental taxes

• South Africa: front-runner in Africa, EFR in budget…

• Recent Study for the European Commission:Barbados, Burkina Faso, South Africa, Uganda, Vanuatu – more findings are following

• China Council for International Development on Environment and Development proposes to introduce a long-term oriented carbon/energy tax in predictable and small steps and a comprehensive environmentally-related tax reform – in the Annual General Meeting in November 2009.

• A carbon tax (instead of an energy tax) is thus now under intensive discussion to be included in the next 5-Year-Plan (2011-2015). The State Council may likely suggest it, but in March 2011 the China People„s Party Congress has to approve it.

• Hence, the earliest date of its introduction could be mid 2011 or early 2012.

• It may be rather a carbon than an energy tax not least given the „threats“ of a border tax adjustment from the USA, the EU and France.

• The German development agency GTZ supported this process

• Entire studies on China are available at: http://www.foes.de/publikationen/studien/?lang=en/#franz3

5. ETR in China

18

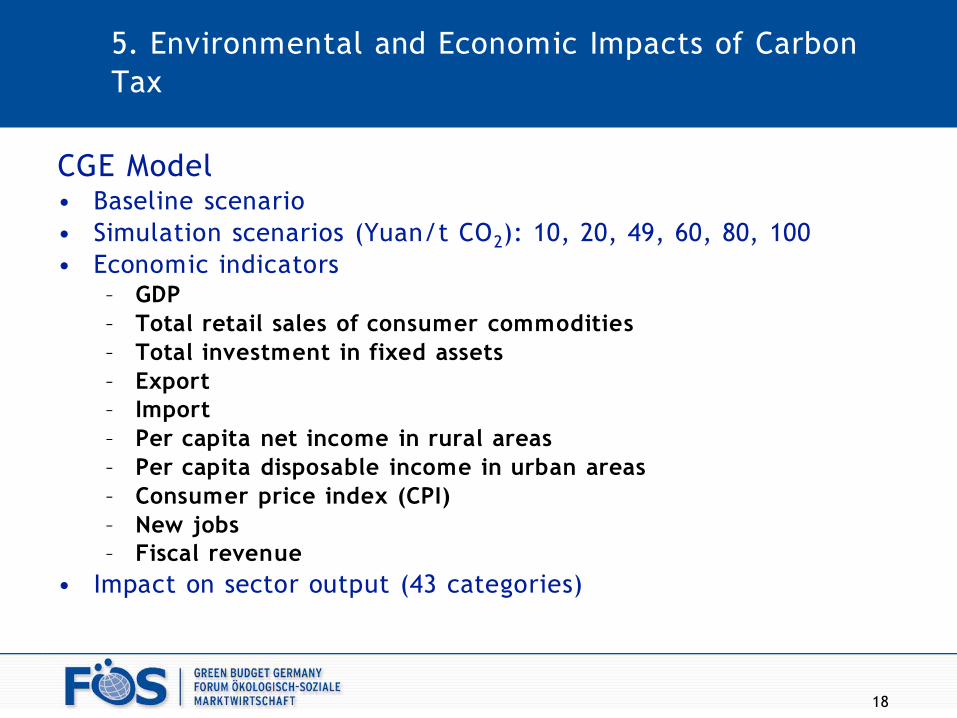

5. Environmental and Economic Impacts of Carbon

Tax

CGE Model• Baseline scenario

• Simulation scenarios (Yuan/t CO2): 10, 20, 49, 60, 80, 100

• Economic indicators– GDP

– Total retail sales of consumer commodities

– Total investment in fixed assets

– Export

– Import

– Per capita net income in rural areas

– Per capita disposable income in urban areas

– Consumer price index (CPI)

– New jobs

– Fiscal revenue

• Impact on sector output (43 categories)

19

• Significant effect on energy-saving and emission-

reduction

• The adverse impact on economic development will

decrease gradually and eventually economic growth

will be accelerated

• Slight decrease of increase rate of fiscal revenues

• Short-term negative effect on enterprises‟

investment, consumer prices, export and

employment, but the effect will soon gradually

diminish

5. Environmental and Economic Impacts of

Carbon Tax

20

5. Impact on GDP Growth Rate [%]

21

5. Change of Growth Rate of CO2 Emission [%]

22

5. Change of Growth Rate of SO2 Emission

23

A –coal mining and processing

B-petroleum and natural gas extraction,

C-petroleum refining, coking and nuclear fuel processing

D-chemical industry,

E-metal smelting and processing

F-ordinary machinery and special purposes equipment

G-transportation equipment

H-electric equipment and machinery,

I-electronic telecommunications and computer

5. Impact of Carbon Tax on Sector Output 2010 [%]

24

5. Impact of Carbon Tax on Sector Output

• Output of energy-intensive industries substantially

effected and obvious effect of structural adjustment

– Energy intensive industries:

coal mining and processing, petroleum and natural gas

extraction, petroleum refining, coking and nuclear fuel

processing, chemical industry, metal smelting and

processing

– Hi-tec industries:

electronic telecommunications and computer, ordinary

machinery and special purposes equipment,

transportation equipment, electric equipment and

machinery

25

5. EFR Activities in the 5 ACP countries

Barbados Burkina Faso South Africa Uganda Vanuatu

Environmental

taxes

Energy

productsYes Yes Yes Yes Yes

Transport /

vehiclesMainly

related to

energy/vehi

cle fuels

Mainly

related to

energy/vehi

cle fuels

Yes Yes Yes

Other environ.

taxesYes Yes Yes Yes

User charges

water

sanitation

waste

Yes Yes Yes

Feed-in-tariff

(renewable

electricity

Yes Yes

26

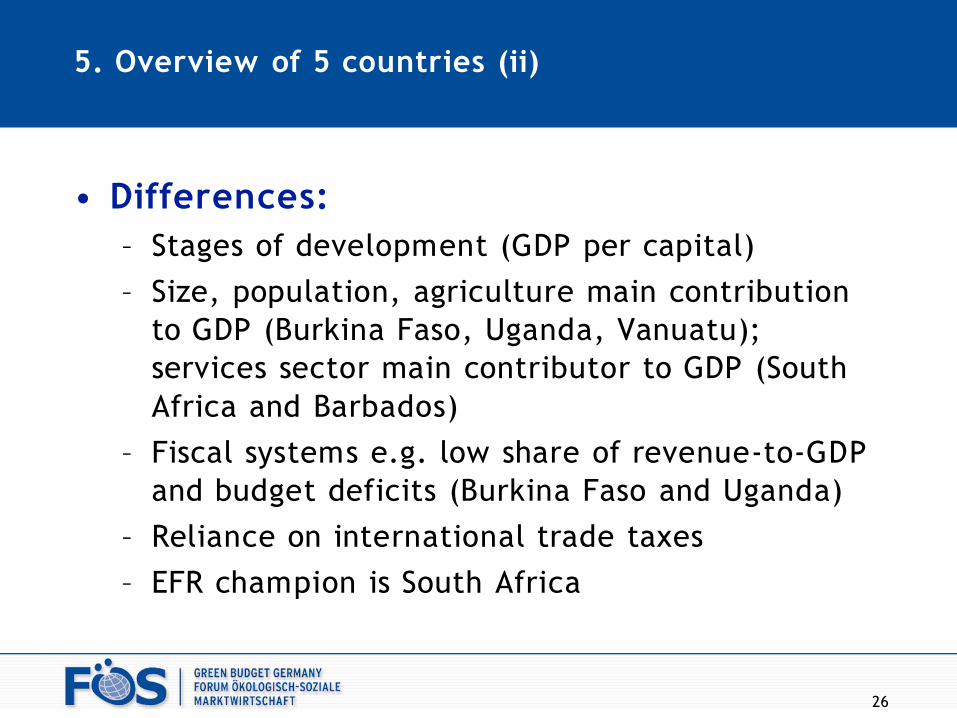

5. Overview of 5 countries (ii)

• Differences:

– Stages of development (GDP per capital)

– Size, population, agriculture main contribution

to GDP (Burkina Faso, Uganda, Vanuatu);

services sector main contributor to GDP (South

Africa and Barbados)

– Fiscal systems e.g. low share of revenue-to-GDP

and budget deficits (Burkina Faso and Uganda)

– Reliance on international trade taxes

– EFR champion is South Africa

27

5. Barbados

• Taxes on vehicles are already progressive.Possible improvement: using CO2-emissions as tax bases

• Heavy fuel oil should also be taxed as large sulphur dioxide emissions are caused by this.

• The so-called environmental levy requires more environmental focus. So far, it is only a waste-oriented levy. Main link seems to be that revenues shall be gathered for covering the costs of scrapping particularly of cars.

• The property tax should be based on environmentally relevant factors and not just varied according to the development of housing prices. Not at least since space is very limited on Barbados, it should take over the function of guiding towards optimal allocation of the space, (e.g. number of persons living per square meter or using categories).

• A similar function could be taken by the land tax.

• Streamlining the tax system and reducing administration by merging both tax forms.

• The current reform of the electricity prices and tariffs is a huge window of opportunity to make price incentives consistent with sustainable development.

28

5. Burkina Faso

• Several environmental, social and economic challenges

• Heavy reliance on donor funding and low domestic revenues

• Several policy/institutional initiatives, under sustainable development

– Strategy for accelerated growth and sustainable development (La SCADD); Ministerial efforts to integrate environment into other policies in Ministries and enterprises; MDG target on poverty alleviation

– Budget reforms 2010 – to increase domestic revenues

• identified potential sectors, further discussion on EFR: energy (solar, biomass, biofules); transport; rural development; carbon credits; water and sanitation; mining

• Good time to start conversation about possible entry points for EFR, focus on identified sectors and proposals; institutional/policy initiatives and objectives - crucial to include local stakeholders and experts at all levels

• EFR-Training has been successfully applied in 2010 by GIZ

29

5. South Africa

• Wide application of environmental taxes and concept of EFR is

well-known as promoted by OECD DAC and World Bank

• National Treasury – decisive player; published the Draft Policy

Paper A Framework For Considering Market-Based Instruments To

Support Environmental Fiscal Reform In South Africa in 2006

• Free basic service delivery (water, electricity) - huge inequalities

of income and wealth in South Africa: but the socially motivated

free basic service delivery could lead to increased consumption

• Proposals for the introduction of new environmental taxes are

underway – they are analysed quantitatively and qualitatively –

often by stakeholders (university): EFR design (in particular how

revenues are recycled) is decisive for achieving economic,

environmental and social benefits (poverty eradication is key for

all policy proposals)

30

5. Uganda

• Budget deficit and reliance of donor assistance there is a need for mobilising domestic resources

• Transport fuel taxes are important revenue source ratio of environmental tax-to-total tax revenues is high and reveals the significance of the fiscal aspect of them

• Huge investment needs in environmental infrastructure (electricity, water and sanitation)

• Proposals of revising of existing or introducing new EFR instruments must be closely linked to the Poverty Eradication Action Plan (PEAP)

• The PEAP limited the introduction of new instruments as it anticipates that setting of water tariffs based on the full cost recovery principle is considered not being practicable and implying that the financing of water and sanitation investments is under the responsibility of the Government of Uganda (funds have to be allocated from national budget)

31

5. Vanuatu (I)

• No established system of environmental fees and charges, foregoing revenues

• Large potential for developing proposals for EFR-elements as it has large potentials for renewable energies, but they require significant incentive schemes e.g. via tax differentiation.

• Electricity: Cost of electricity is relatively high; the quality of supply is superior to neighbouring countries. Tariffs are set on the basis of diesel generation costs, and the savings are deposited into a Special Reserve Fund financing rural electrification.

• Utilities Regulatory Authority currently does a full review of the tariffs.

• Transport: Duty on diesel + gasoline is at 25 VUV/l (0.17 EUR/l) plus VAT at 12.5% = 35 VUV/litre (0.24 EUR/l = 40% of the price due to taxes).However Vanuatu aims at reducing costs for transportation and utilities as one of the priorities.

• The fee for motor cars varies from VUV 11.200 to VUV 38.000 (80-260 EUR) according to their tonnage and cylinder capacity number.

32

5. Vanuatu (II)

• Water: Good basis for managing Vanuatu’s water resources, but not much is activated.

• Tariffs for urban water supplies are high, caused by high costs of delivery and operation. The tariff structure (2007) is based on

– a fixed connection fee for < 25m3 per quarter and

– graded tariffs (<50m3 = 55.13 VUV/m3 – >200m3 = 82.70 VUV/m3).

• The Priorities and Action Agenda (PAA) 2006-2015 recommends following the principle that tariffs for service delivery should fully recover capital and operating costs, or if there are social obligations, they should be determined + funded through government subsidies – a reasonable approach

• Wastewater is uncontrolled and unregulated with no tariffs. This could be easily introduced as there are a variety of NGOs and donors funding community-based sanitation and wastewater management.

• Rural water supplies are donor-funded

• Urban water supplies are funded by fees and tariffs.

• Waste: Charges for waste collection/disposal are low compared with other Pacific Islands. Full cost recovery in capital Port Vila is the ultimate aim though limited by the ability to pay. Hence, the costs of waste collection and disposal should be accounted for on an annual basis and should be set based on the ability to pay with increases towards full cost recovery over the medium term.

33

5. Vanuatu (III)

Tourism should be prepared to pay for the services of providing a clean environment:

Hydropower stations (via water user fees) to cover the cost of watershed management and to compensate upstream landholders from undertaking logging or other land uses that cause problems for the power station (Payment for ecosystem services – PES);

Payment of a volumetrically determined fee for bottled mineral water that would be used to compensate landowners and cover the cost of watershed management and mandatory water quality monitoring;

Payment of an environmental “bed tax” for tourists (typically €2-4 per night) used for keeping the environment clean;

An environmental “docking fee” for all yachtsmen and cruise boat tourists

An air ticket tax to be added to all airline tickets

Increase the taxation of fossil fuels in small predictable steps to increase energy productivity and to stimulate the use of the domestic sources, particularly copra, which should be taxed at a lower rate

34

5. Vanuatu (IV)

• Proposals for further EFR-elements:– Impose environmental fee for cruise ship tourists visiting Vanuatu (funds for

management of coastal waters).

– Levying a water charge to encourage rational use of water.

– Consider effective ways to minimize the powers of Ministers to enter into agreements with foreign investors to avoid or even abolish existing environmentally harmful subsidies.

– Introduce an incentive scheme for substitution of imported diesel fuel by domestic coconut oil.

– Consider environmental performance bonds for land developers and forest concessionaires,

– Consider lodgement fees for environmental impact assessments (EIA),

– Consider charges for annual inspections of manufacturing facilities ,

– Consider discharge fees for discharge of treated water to watercourses,

– Consider fees/deposit refund-scheme for accepting used batteries or e-waste for recycling,

– Consider higher business licensing fees for registration or certification of environmental industries

– Consider licences for mini-buses and taxis; parking fees for private transport services, including buses and taxis

– A registration fee should be introduced and graded according to emission levels of classical pollutants (guided by the Euro-norms) and CO2-emissions and the price of the car.

– Construction is on the sharp increase using environmentally sensitive resources such as coral aggregate, gravel and sand, contributing to aggravate coastal erosion, hence an aggregates levy like e.g. in the UK or partially in DK is recommended.

35

5. EC-project conclusions (I)

– principle and concept of environmental fiscal reform (EFR) is not too widely known in ACP countries. However, South Africa, less so Burkina Faso and Uganda are exceptions in the five countries

– however, the use of EFR instruments is widespread in ACP countries but there are differences in design, quality and quantity

– mobilising revenues by strengthening domestic revenue bases is important;

– the reform of user charges for water, sanitation and waste (cost recovery charges) is a necessity in all ACP countries, also in poorer ones. Social considerations (i.e. affordability issue) must be taken into account when designing these pricing tools. Experiences of cleverly designed user charges are manifold and can also be combined with funding instruments, such as output-based aid (OBA) schemes.

36

5. EC-project conclusions (II)

– fiscal instruments in environmental policy, such as energy and CO2 taxes, emission trading schemes, etc., are attracting more attention and popularity in the last two decades. An IMF Working Paper noted this as „the most important recent development that could be suggestive of the direction of future tax policy trends (Norregaard and Khan, 2007, p.7)‟

– A possible entry point for making the EFR concept known could be the African initiative on taxation / fiscal reform: „Africa Tax Administration Forum‟ (ATAF) which was launched in Kampala/Uganda in November 2009. This initiative seeks to increase African countries‟ financial independence and contribute to economic development and good governance on the African continent‟;

– There is no „one size fits all‟ EFR approach. Individual EFR instruments and a „comprehensive EFR‟ must be designed by taking into account country specific conditions, i.e. economical, fiscal, social, institutional, legal aspects must be considered;

6. Overall Conclusions (II)

• Instead of binding caps, many countries might rather go for environmental fiscal instruments (or do both).

• Inflation problem:Fuel taxes — like other environmental taxes — are quantity-based which means: Their revenue is automatically devalued by inflation: In Germany since 2003 alone, by 0.07 Euro/liter (0.10 U$/liter).Recommendation: Adjustment for inflation, if not income

•EC Budget support is an important financial tool to support tax/fiscal reforms and can be used to promote integration of environmental objectives and use of MBIs/EFR for sustainable development objectives, while contributing to domestic revenue generation.

• Possible linking World Bank Activities to the requirement of introducing EFR-elements?

38

Most promising:

• Vietnam will introduce an ETR in 2012

• China is seriously considering it for 2012-15

Increasingly more, also transition economies and developing countries see environmental fiscal reforms (EFR) as crucial policy to

• make the market work for environmental protection

• get a society on a low-carbon trajectory;

• help develop new industries that will provide sustainable jobs

• provide competitive advantages for the industry;

• contribute to restoring fiscal stability after the recession, the current

window of opportunity as it pays off for environment and fiscal policy

However:

• It needs a long-term effort to change the tax and fiscal structure

• It needs intensive trainings for policy makers and staff

• It needs comprehensive communications and marketing

6. Overall Conclusions (I)

39

6. Why is EFR not yet mainstream?

• poor integration of environment into other policies such as economic policy, national budget plans, development policy, poverty-reduction and sustainable development

• weak, fragmented environment policy and Ministries

• inadequate human capital to carry-out policy enforcements

• inadequate knowledge of the economic value of environmental resources or services and social costs of environmental damages

• poor coordination of national initiatives

• sub-national governance issues and existing legal and institutional constraints, etc

• Proper functioning legal and institutional frameworks; strong environmental agencies and enforcement, local ownership and acceptability – contribute to effective EFR

40

6. Environmental Fiscal Reform – GIZ-Training

Capacity Development for Environmental Fiscal

Reform GBG has designed an interactive training seminar that focuses on the

different conceptual and thematic dimensions of EFR. The training is

based on the OECD Development Assistance Committee (DAC)

Guidelines on “EFR for Poverty Reduction”.

It has already been applied in Burkina Faso, Mexico, Indonesia,

Vietnam and Thailand, UNEP/UNDP are considering its application

Objectives of the EFR Training: Understanding of EFR basic

In-depth knowledge of EFR approaches in sectors and countries

Detailed knowledge of the potential benefits and limits of EFR

Increased capacity to discuss and design appropriate EFR strategies

Details: http://www.foes.de/pdf/GTZ_EFR_Training_Description2.pdf

41

Vielen Dank für Ihre Aufmerksamkeit!

Thank you for your attention!

Kai Schlegelmilch

Vice President of

Green Budget Germany

Schwedenstraße 15a, 13357 Berlin, Germany

Tel: +49-30-76 23 991-30

www.foes.de

European Commission Study Project Website:

http://www.foes.de/internationales/oefr-in-entwicklungslaendern/