ENVIRONMENTAL, SOCIAL AND GOVERNANCE QUARTERLY … · 4/11/2016 · media, following a second ......

16

COLUMBIATHREADNEEDLE.COM ENVIRONMENTAL, SOCIAL AND GOVERNANCE QUARTERLY REPORT QUARTERLY REPORT JULY TO SEPTEMBER 2016 INFORMATION FOR INVESTMENT PROFESSIONALS

Transcript of ENVIRONMENTAL, SOCIAL AND GOVERNANCE QUARTERLY … · 4/11/2016 · media, following a second ......

COLUMBIATHREADNEEDLE.COM

ENVIRONMENTAL, SOCIAL AND GOVERNANCE QUARTERLY REPORT

QUARTERLY REPORTJULY TO SEPTEMBER 2016INFORMATION FOR INVESTMENT PROFESSIONALS

Columbia Threadneedle Investments is the global brand name of the Columbia and Threadneedle group of companies.

1

Environmental, Social and Governance Quarterly Report

SUMMARYA substantial body of our research this quarter, and related voting and engagement activities, was directed at Asian and emerging market companies. Overall, we were encouraged by the proactive approach to engagement displayed at some of these companies.

More generally, we cast at least one dissenting vote at 146 meetings, which represented 47% of the total. In our Proxy Voting section, we outline the issues voted on, ranging from human rights to bribery and corruption, as well as the mechanisms for voicing concerns and encouraging improvements. These mechanisms include votes against directors, reports and accounts, or votes for shareholders’ resolutions.

By the start of October, ratifications of the Paris Agreement accelerated; the EU and other countries ratified and 4 November has been confirmed as the date on which the agreement will come into force. In tandem, we have seen continued growth of the green bond market. Work with investment teams across the firm has been undertaken, for example around opportunities and risks inherent in automated and electric vehicles, clearly benefiting from the global interest in green solutions.

Finally the developments around stewardship and fiduciary duties of investors have continued, and we see wider stakeholder support for responsible investment continue to grow.

2

Environmental, Social and Governance Quarterly Report

PROXY VOTINGColumbia Threadneedle Investments views proxy voting at meetings as one of the most effective ways of signalling our approval (or otherwise) of a company’s governance, management, board and strategy, including a significant ESG element in all of the above. We take a collaborative approach to making voting decisions as well as a range of different research sources, and we make our final voting decision in collaboration with the firm’s portfolio managers and analysts. You can view all voting decisions made 14 days after the company meeting on our website.1

We voted at 313 meetings across 34 global markets in the third quarter, fewer than the previous quarter, where voting action is generally higher. Over half (177) were held in the United Kingdom, where March year-ends lead to a flurry of activity in July. A significant number of meetings were also held in India, another market with a later voting season. The majority of meetings were annual (72%) with 27% extraordinary and the remaining 1% combined (both annual and extraordinary).

Meetings Voted by Region

0%

10%

20%

30%

60%

50%

40%

UK Far East &Emerging Markets

North AmericaEurope JapanLatin America

57%

27%

7% 6%2% 2%

0

1

2

3

4

5

6

Directors Reports& Accounts

ESGResolution

Action notpossible

Action nottaken

Num

ber o

f mee

tings

5%

2% 2%

3%

1%

Bribery &Corruption

Human &Labour Rights

Environmental

Lobbying

Health, Safety& Quality

ESG issues in voting analysisBreakdown of ESG voting action

20%13%

20%

20%

27%

During the quarter, we did not support 355 resolutions – at least one dissenting vote was cast at 146 meetings, which accounted for 47% of the total. We continued to register dissenting votes on proposals which we believed were not the interests of our clients. As with the same period last year, director and remuneration-related concerns made up the bulk of voting action. Just under half of our dissenting votes came from the focus on directors.

The UK remains our largest voting market, based on both meeting volume and the percentage of assets under management. Executive remuneration continues to be a focus for investors and the media, following a second quarter in which a number of high-profile remuneration reports were defeated; this ‘proxy season’ registered the most dissenting votes since 2012’s ‘shareholder spring’. In the third quarter, 12 remuneration proposals which we did not support received less than 90% support from the shareholder base. In total, we did not support 32 remuneration-related proposals during the period, and did not support the elections of a number of directors on remuneration committees. We may choose to target individual directors who bear responsibility in cases where we see ongoing pay practices as problematic.

Of the 52 meetings held in India, we did not support at least one voting item at 39. It is common in India to bundle executives’ elections and remuneration into one voting item. We believe shareholders should have a say on each of these items, separately; this drove a number of our dissenting votes.

1Our voting decisions may be accessed at: http://vds.issproxy.com/SearchPage.php?CustomerID=2775

3

Environmental, Social and Governance Quarterly Report

Breakdown of dissenting votes

Remuneration

Director Related

Reorganisations and Mergers

Capitalisation

Other Business

Supporting Shareholder Proposals

Audit Related46%

25%

11%

9%

4%

3% 2%

VOTING ON COMPANIES WITH CONTROVERSIAL ENVIRONMENTAL AND SOCIAL PRACTICESWe were eligible to vote at meetings of ten companies where significant concerns exist given worst-in-class management of ESG issues, or evidence of severe controversies amounting to a breach of UN Global Compact standards. In seven meetings, we voted against directors due to ESG issues, and in several cases, we voted against the annual report and accounts. In three cases, all special meetings, we were unable to take appropriate ESG-related voting action, as the meetings were related to capitalisation, amalgamation, and by-law amendments.

SHAREHOLDERS’ RESOLUTIONSIn terms of shareholder resolutions, there were only three meetings with ESG-related resolutions. We supported two, which were related to lobbying and disclosure. The other did not warrant our support.

0%

10%

20%

30%

60%

50%

40%

UK Far East &Emerging Markets

North AmericaEurope JapanLatin America

57%

27%

7% 6%2% 2%

0

1

2

3

4

5

6

Directors Reports& Accounts

ESGResolution

Action notpossible

Action nottaken

Num

ber o

f mee

tings

5%

2% 2%

3%

1%

Bribery &Corruption

Human &Labour Rights

Environmental

Lobbying

Health, Safety& Quality

ESG issues in voting analysisBreakdown of ESG voting action

20%13%

20%

20%

27%

4

Environmental, Social and Governance Quarterly Report

ESG ENGAGEMENTThe Responsible Investment team continued engaging with numerous companies throughout the quarter. In prioritising our work, we seek to focus proactive engagement efforts on the more material or contentious issues and the companies in which we have large holdings, based on either monetary value or on the percentage of issued shares. There are a number of companies with which we have ongoing engagements, as well as those we speak to on a more ad-hoc basis when potential issues arise.

We continue to actively participate in a number of investor networks, which complements our approach to engagement and understanding of the issues and wider sentiment. Along with other investors, we raise market and company-specific ESG issues, share insights and best practice. This quarter, we engaged with the 29 companies listed below, some multiple times.

Environmental, social and governance discussionsBHP Billiton, Burberry, Chr Hansen, G4S, KEPCO, Marks & Spencer, Novartis, Reckitt Benckiser, Richemont, Rio Tinto, Shanks Group

Specific governance focusAstraZeneca, Cobham, Compass Group, De La Rue, DS Smith, Genus, GKN, Intermediate Capital Group, Johnson Matthey, Kansai Nerolac Paints, Macquarie, Rolls-Royce, Ryanair, Sepura, Sika, Spirent, Wincanton

Specific social focusNCC Group

VOTING-RELATED ENGAGEMENT HIGHLIGHTSRemuneration – misalignment of pay practices, performance and company strategy Burberry and DS Smith

While deciding how to vote on remuneration items at companies, we consider compensation practices on whether they sufficiently align management and shareholder interests by supporting long-term strategy and avoiding pay for failure.Before Burberry’s annual general meeting (AGM), we met with the company a number of times to discuss our ongoing concerns, including those relating to the company’s remuneration practices. In 2014, when Christopher Bailey was promoted internally to the post of CEO while retaining his role as Chief Creative Officer, he was awarded a £30 million pay packet. This led shareholders to vote down the company’s remuneration report, amid concerns about quantum, and the scope of the roles. Total returns between the time of his promotion and the 2016 AGM were negative.The company has been responsive to shareholder concerns and, in light of performance, awarded no bonuses, among other measures. Given the changing dynamic, we chose to abstain on the remuneration report, rather than oppose it. Reflecting perceived changes, only13% of shareholders dissented by abstaining or casting opposing votes. Since the 2016 AGM there has been further progress; the company has announced the appointment of a new CEO and a new COO, while Chris Bailey refocuses on his creative role.We have long been concerned with the remuneration practices at DS Smith, particularly with regard to the rates of pay and levels of disclosure. We continue to believe the company’s pay levels are running ahead of (good) performance, with each individual aspect of pay structured to be ahead of the market on a stand-alone basis. The company cites opaque, custom benchmarking as the reason for the positioning of its pay arrangements. In spite of continuing engagement with the company, its lack of progress meant that we maintained our position and did not support either the remuneration report or the re-election of the remuneration committee chair. However, in spite of continuing concerns, an increasing number of shareholders have acquiesced on the issue over time. In 2014, 23% of shareholders did not support the remuneration report; which dropped to 18% in 2015 and 12% in 2016.

5

Environmental, Social and Governance Quarterly Report

Board composition – maintaining independent oversight Ryanair and Richemont

The role of the board is to provide independent oversight to management. Where we believe this key role is being compromised, we will take voting action.

Between its 2015 and 2016 AGMs, Ryanair’s total returns became negative. Engagement with the company has sought to address issues related to the board and its practices. The company has a relatively small number of independent directors on the board; issues include the tenure of some directors, two of whom are former executives, while another comes from the company’s long-time broker. Concerns also exist around the awarding of share options to individuals who are otherwise independent. The practice of awarding share-based incentives to non-executive directors (NEDs) concerns us, as evidence suggests that this practice can weaken independent oversight.

Levels of experience and contribution made by individual directors have to be assessed against the operation of the board as a whole, while also considering the company’s performance. Due to these concerns and notwithstanding the company’s performance, we abstained on the election of a number of directors. These included the chairman, who bears ultimate responsibility for the company’s corporate governance practices. He did not receive the support of 12% of shareholders. We did not support the remuneration report, reflecting concerns about the use of share options for non-executives. We were joined in this vote 17% of shareholders.

Richemont is another company where a long-term history of engagement is linked to voting action. This company’s total returns were also negative between the 2015 and 2016 AGMs. At Richmont, minority shareholder votes are muted as the company is controlled by the Rupert family’s investment vehicle. Other issues that have been the subject of engagement are the board and its limited independent representation, given issues around tenure, business connections, related-party transactions and connections to the family.

The founder is heavily involved in the company, as the chairman of the board and of the nomination committee. In such cases, we look for assurances that the board will be able to operate effectively and in the interests of all shareholders. As founder-controlled companies are particularly susceptible to key man risk, we have focused on succession planning and board diversity. Ultimately, we chose not to support a number of directors due to our concerns about board balance, but the voting outcomes are unknown given the company does not release its voting results.

On one positive note there have been developments on gender diversity. Prior to the AGM, the board had one woman (non-executive) out of 19 directors, but has promoted a second (executive) director to the board in Cyrille Vigneron.

6

Environmental, Social and Governance Quarterly Report

ESG RESEARCHESG RESEARCH IN ASIA AND EMERGING MARKETSThis quarter, a significant proportion of our research pertained to companies in Asia and emerging markets. Three case studies are outlined below, which show the broad range of issues, markets and sectors considered in the course of our research.

ULTRATECH CEMENTIndian cement company Ultratech was identified during our quarterly monitoring process as worst-in-class by an ESG research provider. This triggered a review and reassessment of the firm, which led to our investment team posing related questions to the company, and gathering the latest information on its sustainability performance. While noting the potential for improvement in emissions management, the exercise confirmed significant progress in health and safety and water management.

For instance, Ultratech improved its health and safety performance, reducing injury rates for 2016 We also found evidence of a proactive water conservation strategy, which is appropriate to the company’s operation in a region of high water stress. Equally, we noted that UltraTech Concrete was India’s first eco-friendly concrete, as recognised by the Indian Green Building Council, enabling the company to benefit from sustainability growth opportunities.

We were pleased that within a month of our review, the external ESG research provider also upgraded its outlook on the firm.

KOREA ELECTRIC POWER COMPANYKorea Electric Power Company (KEPCO) is South Korea’s largest electric utility company; over 50% of the company is government owned. Following a review of the company during our voting analysis of the AGM, we identified that KEPCO has been involved in a number of controversies in recent years. These include a corruption investigation regarding alleged receipt of kickback payments in the US, community opposition and environmental concerns in pipeline construction, and questions over health and safety performance and oversight, particularly in a subsidiary operating nuclear power plants.

This led to a wider ESG review and engagement on a broader range of material issues. The company’s proactive approach to dialogue has been encouraging and we were able to assess progress on some of the issues.

nn The company has produced a detailed code of ethics and guidelines tailored to different groups (such as suppliers, those overseeing contracts, employees and executives). It publically discloses the training it provides on this issue.

nn On health and safety, we were given only a high-level indication of fatality and injury rates; this indicates a further need for improvement on performance and transparency. The company was open about the failure of oversight in a nuclear subsidiary; this related to a supplier’s forgery of nuclear-related safety documents and the changes this has prompted, including the cessation of the relationship with the supplier and significant alterations to management.

nn In line with South Korea’s increased focus on sustainability and climate change issues, we also noted KEPCO’s strategic goal to become a ‘smart energy creator’. On government recommendations, KEPCO is devoting resources towards new energy businesses, including energy storage systems, renewable energy, smart grids, electric vehicles and advanced metering infrastructure. Although the 2016 target investment was KRW 6.4 trillion, the company expects the actual spending rate to be half this sum by the end of the year, due to the time needed to review the viability and profitability of these projects. However, the company’s management assured us they would continue with the analysis and update investors on their progress.

7

Environmental, Social and Governance Quarterly Report

PT TELEKOMUNIKASI INDONESIAAs part of a long-term stock review, the ESG elements of this Indonesian telecommunications company were analysed. In terms of its own processes, the company is influenced by its majority state-ownership and has embedded the sustainable development of the Indonesian economy into its strategy. It is set to benefit from access to digitalisation opportunities – as it pursues growth in areas with limited digital penetration – and also supports Indonesian start-ups and digital innovation.

The company’s attention to customer satisfaction aligns with the enhanced regulatory focus on this issue. Human capital issues are also well managed, which is important given the high degree of unionisation (c. 90%) and the need for sector-specific skills. There are also clear processes for managing enterprise risk, as well as supply-chain risks including human rights issues.

As part of this review, we also assessed macro ESG issues in Indonesia, and assessed the ESG performance of other companies in the market. The team’s analysis fed in to, amongst other things, the firm’s thematic research on telecoms, and risks and opportunities inherent in the sector.

GREEN BONDS – DEVELOPMENTS AND MARKET UPDATEGreen financing has become a political focus, following the G20 announcement in September that green bonds would be a key tool to support the global goals for mitigation of and adaption to climate change. Issuance in 2016 so far has come from global issuers such as the Asian Development Bank, Mexico City Airport and Bank of China, as well as local Swedish authorities. As these types of issues find a place in portfolios, ongoing developments and new tools are helping to improve analytical capabilities. Moody’s and S&P have both proposed green bond frameworks to assist investors in evaluating the extent and scope of the green characteristics. Indeed, some bonds have come under scrutiny for not being sufficiently compliant with the green bond principles.

The Green Bond Principles identify use of proceeds as the following core outcome areas:

nn Renewable energy

nn Energy efficiency

nn Pollution prevention and control

nn Sustainable management of living natural resources

nn Terrestrial and aquatic biodiversity conservation

nn Clean transportation

nn Sustainable water management

nn Climate change adaptation

nn Eco-efficient products, production technologies and processes

The key discussion point from green bond evaluation methodologies includes the potential for this use of proceeds to be prioritised in terms of ‘shades of green’. Each framework will take a slightly different view. One approach is to split the activities between mitigation of and adaptation to climate change, where renewable energy and energy efficiency rank highest in terms of ‘shades of green’. Clearly, the definitions and interpretations are up to individual investors and, as can be seen with the range of approaches to general ESG research, several frameworks are likely to be developed over time.

8

Environmental, Social and Governance Quarterly Report

INVESTMENT THEMES: ESG IMPLICATIONS RELATED TO ADAS, AUTOMATED AND ELECTRIC VEHICLES This quarter, we analysed ESG-related themes that could be considered important to the development of automated driver assistance systems (ADAS) and electric vehicles. These ESG factors can impact consumer trust and demand for such vehicles. At the same time, significant opportunities are presented by these themes. This is particularly relevant in a world of political support for lower carbon emissions which potentially creates longer-term headwinds for oil demand. At the same time, society globally is more conscious of safety risks related to transportation. The main ESG issues highlighted include:

nn Cybersecurity and hacking – in the event of an incident there may be lower consumer trust in products. The need for solution providers is greater than ever as a result.

nn Insurance premiums – electric vehicles currently see an approximately 20% premium to normal vehicles and in the short term insurers may see increased opportunities for revenue growth with ADAS and AV.

nn Safety and regulation – regulation is developing but ADAS is generally seen as a safer option in terms of parking assistance, for example.

nn Environmental regulation and efficiency – growth in electric vehicles is seen as more important than hybrid vehicles but, in all jurisdictions including the EU, the US, China and India, regulation related to emissions is tightening. Furthermore, ADAS can enable vehicles to become more fuel efficient.

nn Infrastructure developments – we see a need for greater social acceptance and investment in the network.

nn Operational sound practices – issues such as human rights and sourcing, conflict minerals, battery disposal and human rights need to be addressed from a regulatory as well as a consumer trust perspective.

The sector implications from these themes are wide ranging and the Threadneedle Ethical UK Equity fund, for example, specifically targets companies deriving revenue or growth from many of these areas.

9

Environmental, Social and Governance Quarterly Report

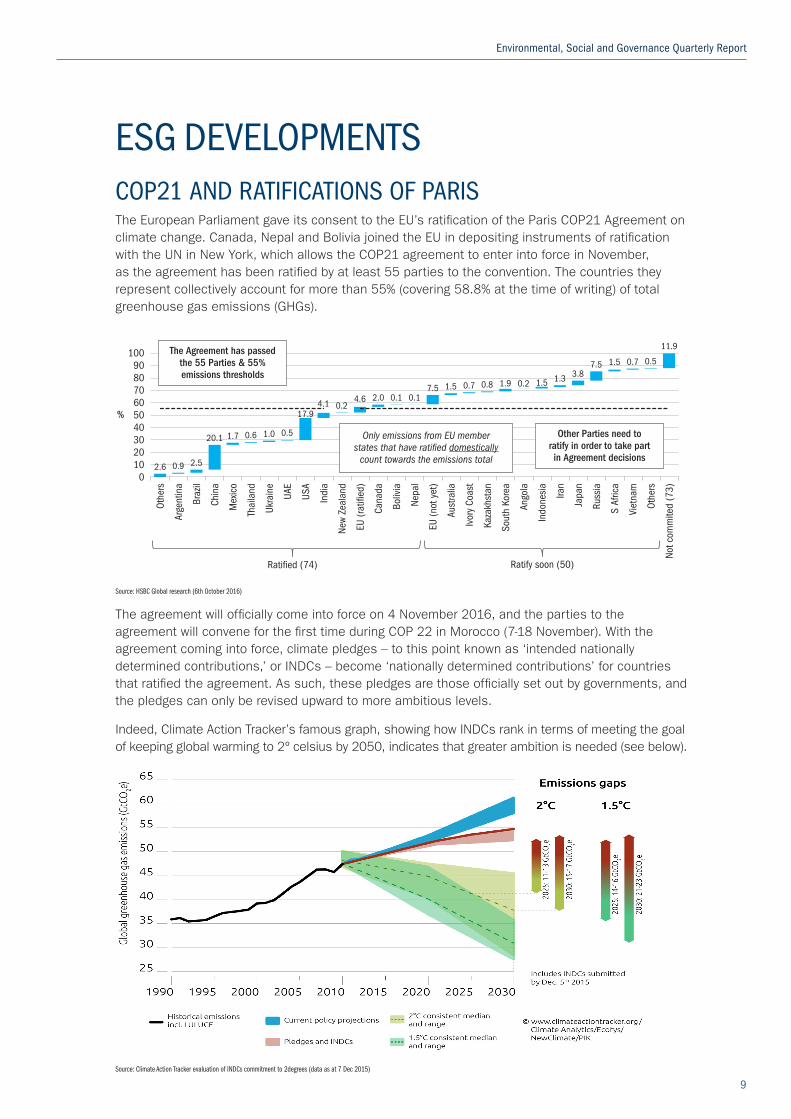

ESG DEVELOPMENTSCOP21 AND RATIFICATIONS OF PARISThe European Parliament gave its consent to the EU’s ratification of the Paris COP21 Agreement on climate change. Canada, Nepal and Bolivia joined the EU in depositing instruments of ratification with the UN in New York, which allows the COP21 agreement to enter into force in November, as the agreement has been ratified by at least 55 parties to the convention. The countries they represent collectively account for more than 55% (covering 58.8% at the time of writing) of total greenhouse gas emissions (GHGs).

0102030405060708090

100

Othe

rs

Arge

ntin

a

Braz

il

Chin

a

Mex

ico

Thai

land

Ukra

ine

UAE

USA

Indi

a

New

Zeal

and

EU (r

atifi

ed)

Cana

da

Boliv

ia

Nepa

l

EU (n

ot y

et)

Aust

ralia

Ivor

y Co

ast

Kaza

khst

an

Sout

h Ko

rea

Ango

la

Indo

nesi

a

Iran

Japa

n

Russ

ia

S Af

rica

Viet

nam

Othe

rs

Not c

omm

ited

(73)

%

Ratify soon (50)Ratified (74)

The Agreement has passedthe 55 Parties & 55%emissions thresholds

Only emissions from EU memberstates that have ratified domestically

count towards the emissions total

Other Parties need toratify in order to take partin Agreement decisions

80

90

100

110

120

130

140

2013 2014 2015

15% 25% 33% 50% All companies

2.6 0.9 2.5

20.1 1.7 0.6 1.0 0.5

17.94.1 0.2

4.6 2.0 0.1 0.17.5 1.5 0.7 0.8 1.9 0.2 1.5 1.3 3.8

7.5 1.5 0.7 0.5

11.9

Source: HSBC Global research (6th October 2016)

The agreement will officially come into force on 4 November 2016, and the parties to the agreement will convene for the first time during COP 22 in Morocco (7-18 November). With the agreement coming into force, climate pledges – to this point known as ‘intended nationally determined contributions,’ or INDCs – become ‘nationally determined contributions’ for countries that ratified the agreement. As such, these pledges are those officially set out by governments, and the pledges can only be revised upward to more ambitious levels.

Indeed, Climate Action Tracker’s famous graph, showing how INDCs rank in terms of meeting the goal of keeping global warming to 2º celsius by 2050, indicates that greater ambition is needed (see below).

Home About INDCs Countries Global Data (beta) Methodology Publications What's new?

18Home › Global › Emissions Gap

CAT Emissions Gaps

7th December 2015

Data underlying the above graph can be downloaded here.

Emissions gaps between current pledges and 2°C consistent pathways

In addition to the global temperature outcomes of policies and pledges, the CAT also assess theexpected absolute emissions in 2020, 2025, and 2030 and compares these with benchmarkemissions consistent with limiting warming below 2°C with likely (≥66%) probability and with limitingwarming below 1.5°C by 2100 (with ≥50% probability) for these years.

As of 7 December 2015, a substantial gap remains between the levels of emissions in 2025 and 2030projected in the INDCs submitted to the UNFCCC and the lower levels that would be consistent withlimiting warming below 2°C (or 1.5°C).

With the INDCs submitted by 7 December 2015, the CAT projects that total global emissions wouldbe 52-54 GtCO2e in 2025 and 53-55 GtCO2e in 2030 (the red shaded area in the above graph),signicantly above present global emissions of about 48 GtCO2e. We therefore estimate theemissions gap at 11-13 GtCO2e in 2025, growing to about 15-17 GtCO2e in 2030.

The emissions gap for the 1.5°C pathway is about 3 GtCO2e larger than the 2°C gap in 2025, and 6GtCO2e larger in 2030.

The gaps between current policy projections and the 1.5°C and 2°C benchmarks are higher than thepledge gaps. This means that currently implemented government policies are not strong enough toachieve the pledges governments have made. Current policies are estimated to result in emissions of55-57 GtCO2e in 2025 and 58-61 GtCO2e in 2030 (the blue shaded area). The policy gap to 2°Cincreases from 12-18 GtCO2e in 2025 to 21-28 GtCO2e in 2030.

Temperatures

Emissions Gap

Further Information

Source: Climate Action Tracker evaluation of INDCs commitment to 2degrees (data as at 7 Dec 2015)

10

Environmental, Social and Governance Quarterly Report

In Canada we have already seen signs of increased ambition. During the parliamentary debate, which approved the ratification, Prime Minister Justin Trudeau announced nationwide carbon pricing from 2018, raising the coverage from 85% to 100% of the economy.

We follow the theme of climate change closely and these developments present both risks and opportunities to our investments. For example, our Ethical UK Equity fund owns securities that directly benefit from greater focus on climate change in the form of both mitigation and adaptation solutions.

CONTINUING FOCUS ON GENDER DIVERSITYEarlier this year, within EMEA, we became the first asset manager to sign the UK Treasury’s Women in Finance Charter, a pledge for gender balance across financial services. The charter is a commitment to work together to build a more balanced and fair industry. The firms that signed the charter collectively employ over 375,000 people within the UK. As a signatory, we are pledging to support gender diversity; Mark Burgess, our Chief Investment Officer EMEA and Global Head of Equities, will take the lead on commitment.

We have also published a range of gender diversity targets for the firm and we disclose ongoing and historic performance towards those targets. We believe targets are important statements of intent and provide a tangible goal to work towards while also recognising our current position. We remain keenly interested in the wider reporting on progress and continuing evidence of its significance.

BROAD-BASED STUDY OF THE IMPACTS OF GENDER DIVERSITYFirstly, Morgan Stanley2 sought to build a quantitative framework assessing companies on five themes related to gender diversity: Representation (at different levels); Empowerment (key C-suite and board roles); Equality in Pay (also referred to as the gender pay gap); Diversity Policies and Work/Life Balance Programmes. The analysis found that companies with high gender diversity have delivered slightly higher and less volatile returns on equity and have lower accruals compared with their low-diversity or sector peers. Highly gender diverse companies have also moderately outperformed their low-diversity and sector peers in the past five years, on average.

STUDY OF THE IMPACTS OF C-SUITE REPRESENTATIONWith debate increasingly focusing on diversity at the executive level, work by Credit Suisse3 found evidence of outperformance by firms with a high proportion of female senior management, particularly evident in those companies where this level reached 50%, over a period in which the MSCI ACWI index declined by 1% on an annual basis. The effects related to share price performance are illustrated below. We also found associations in respect to sales growth, return on assets and earnings per share.

Share price performance for baskets with different tiers of female participation in senior management (since 2013)

0102030405060708090

100

Othe

rs

Arge

ntin

a

Braz

il

Chin

a

Mex

ico

Thai

land

Ukra

ine

UAE

USA

Indi

a

New

Zeal

and

EU (r

atifi

ed)

Cana

da

Boliv

ia

Nepa

l

EU (n

ot y

et)

Aust

ralia

Ivor

y Co

ast

Kaza

khst

an

Sout

h Ko

rea

Ango

la

Indo

nesi

a

Iran

Japa

n

Russ

ia

S Af

rica

Viet

nam

Othe

rs

Not c

omm

ited

(73)

%

Ratify soon (50)Ratified (74)

The Agreement has passedthe 55 Parties & 55%emissions thresholds

Only emissions from EU memberstates that have ratified domestically

count towards the emissions total

Other Parties need toratify in order to take partin Agreement decisions

80

90

100

110

120

130

140

2013 2014 2015

15% 25% 33% 50% All companies

2.6 0.9 2.5

20.1 1.7 0.6 1.0 0.5

17.94.1 0.2

4.6 2.0 0.1 0.17.5 1.5 0.7 0.8 1.9 0.2 1.5 1.3 3.8

7.5 1.5 0.7 0.5

11.9

Source: Bloomberg, CS Gender 3000

2Morgan Stanley, Global Quantitative Research: Putting Gender Diversity to Work: Better Fundamentals, Less Volatility, May 2016 3Credit Suisse, CS Gender 3000: The Reward for Change, September 2016

11

Environmental, Social and Governance Quarterly Report

WHAT THE TREND DATA IS SHOWINGWe have highlighted the following examples of available resources to offer some headline numbers on current progress. In addition, they also signpost key sources of information for those interested in looking further into the trends and current progress.

nn In the UK, we have seen the proportion of female non-executive directors in the FTSE 100 (FTSE 250) board reach 31.4% (25.7%), according to Cranfield’s “The Female FTSE Board Report 2016”, although at executive director level, the figure falls to 9.7% (5.6%). nn In a European context, EWB’s report “Gender Diversity on European Boards – Realising Europe’s Potential: Progress and Challenges” (2016) provided an in-depth review of the progress that has been seen across Europe since 2011, although it also highlights continuing issues and weak progress in areas other than board representation. nnMore broadly, SpencerStuart’s 2016 “Global Board of Directors Survey” highlighted not just the overall state of diversity across public and private company boards but also explored the dramatic differences of perspective seen between men and women across a range of issues including diversity.

RESPONSIBLE INVESTMENT IN EUROPE AND THE LAWThe pace of the extent of ESG-related reforms is impressive, whether in relation to reviews of corporate governance codes, the proliferation of stewardship codes, or the extent of new guidance or thought leadership reports. Among these, one extremely important area of focus relates to the nature and scope of fiduciary duty in terms of investment and, more specifically, responsible investment.

There have been more developments in this area, following an in-depth, detailed review of fiduciary duty by the UK Law Commission, “Fiduciary Duties of Investment Intermediaries” (June 2014), which provided clarity on the ability of pension fund trustees to incorporate sustainability and ESG factors into investment. The UK Law Commission provided a very clear assessment of why and how trustees could account for ESG factors given their duties of balancing returns against risk. This year, further UK regulatory guidance for pension schemes has been issued, following up on the Law Commission’s work.

Similarly, at the end of 2015, the US Department of Labor affirmed that incorporating environmental, social and governance factors into investments was compatible with the fiduciary duty of plan sponsors (normally the employer or employee organisation administering the pension plan) covered under the Employee Retirement Income Securities Act (ERISA) and that “collateral benefits” include environmental protection, social equity and financial stability.

In the first few months of this year, before concluding that the integration of environmental factors in investment policies and the decision-making process of institutional investors is compatible with existing legal frameworks across the EU, the European Commission further discussed the state of the ESG market and obstacles to long-term, sustainable investment.

As the quarter came to an end, the European Fund and Asset Management Association (EFAMA) published its own report on the state of responsible investment and issues surrounding it. The first part of the report reviewed the European asset management industry’s role and involvement in responsible investment.

From the importance of reliable and accurate reporting by companies to the debate about performance and responsible investment, the report sets out EFAMA’s outlook and recommendations on the key questions about responsible investment. These involve the role of legislation, the different selection methods in the responsible investment process and the emergence of new areas such as green bonds and impact investing.

Asset managers’ fiduciary duty towards clients is a key component of EFAMA’s views on responsible investment. The report highlights the importance placed on asset owners to first understand and define their own values and specific objectives, and to have a clear idea on how these should be incorporated, if at all, into their investment mandates. It further details country-by-country descriptions of the legal frameworks, and various private sector initiatives, on responsible investment in 14 key European markets.

12

Environmental, Social and Governance Quarterly Report

APPENDIXCOLUMBIA THREADNEEDLE INVESTMENTS, EMEA PRI RATINGFor the second consecutive year, we achieved a best-in-class, A+ rating from the Principles for Responsible Investment (PRI), for our approach to responsible investment. An outline of the PRI’s assessment, mapped onto different asset classes and themes, is shown below.

Threadneedle Asset Management Ltd

Summary Scorecard

AUM Module name Yourscore

01. Strategy &Governance

0 02. Listed Equity Not applicable

0 03. Fixed Income – SSA Not applicable

004. Fixed Income –Corporate Financial Not applicable

0 05. Fixed Income –Corporate Non-Financial

Not applicable

006. Fixed IncomeSecuritised Not applicable

0 07. Private Equity Not applicable

0 08. Property Not applicable

0 09. Infrastructure Not applicableIndi

rect

– M

anag

er S

elec

tion,

App

oint

men

t & M

onito

ring

A+B

Yourscore

Medianscore

AUM Module name Yourscore

10. Listed Equity – Incorporation

>50%

>50%

<10%

11. Listed Equity – Active Ownership

<10%

12. Fixed Income – SSA

10-50%

13. Fixed Income – Corporate Financial

0

14. Fixed Income – Corporate Non-Financial

Not applicable

0

15. Fixed Income – Securitised

Not applicable

<10% 17. Property

16. Private Equity

0 18. Infrastructure Not applicable

Dire

ct &

Act

ive

Owne

rshi

p M

odul

esA

A

A

A

A

A

Yourscore

Medianscore

A

B

C

C

C

C

13

Environmental, Social and Governance Quarterly Report

Notes

To find out more visit COLUMBIATHREADNEEDLE.COM

Important information: Past performance is not a guide to future performance. The value of investments and any income is not guaranteed and can go down as well as up and may be affected by exchange rate fluctuations. This means that an investor may not get back the amount invested. Threadneedle Specialist Investment Funds ICVC (“TSIF”) is an open-ended investment company structured as an umbrella company, incorporated in England and Wales, authorised and regulated in the UK by the Financial Conduct Authority (FCA) as a UCITS scheme. This material is for information only and does not constitute an offer or solicitation of an order to buy or sell any securities or other financial instruments, or to provide investment advice or services. This document is a marketing communication. The research and analysis included in this document have not been prepared in accordance with the legal requirements designed to promote its independence and have been produced by Columbia Threadneedle Investments for its own investment management activities, may have been acted upon prior to publication and is made available here incidentally. Any opinions expressed are made as at the date of publication but are subject to change without notice and should not be seen as investment advice. Information obtained from external sources is believed to be reliable but its accuracy or completeness cannot be guaranteed. Issued by Threadneedle Investment Services Limited. Registered in England and Wales, Registered No. 3701768, Cannon Place, 78 Cannon Street, London, EC4N 6AG, United Kingdom. Authorised and regulated in the UK by the Financial Conduct Authority. Columbia Threadneedle Investments is the global brand name of the Columbia and Threadneedle group of companies. columbiathreadneedle.com Issued 10.16 | Valid to 04.17 | J25831

KEY RISKSThe following risk factors should be considered in reference to the Threadneedle Ethical UK Equity Fund. Investment Risk: The value of investments can fall as well as rise and investors might not get back the sum originally invested. Issuer Risk: The Fund invests in securities whose value would be significantly affected if the issuer refused, was unable to or was perceived to be unable to pay. Liquidity Risk: The fund holds assets which could prove difficult to sell. The fund may have to lower the selling price, sell other investments or forego more appealing investment opportunities. Inflation Risk: Most bond and cash funds offer limited capital growth potential and an income that is not linked to inflation. Inflation is likely to affect the value of capital and income over time. Interest Rate Risk: Changes in interest rates are likely to affect the fund’s value. In general, as interest rates rise, the price of a fixed rate bond will fall, and vice versa. Derivatives for EPM/Hedging: The investment policy of the fund allows it to invest in derivatives for the purposes of reducing risk or minimising the cost of transactions.