Entrepreneurship and Small Business Management Chapter 13 Using Financial Statements to Guide a...

28

Entrepreneurship and Small Business Management Chapter 13 Using Financial Statements to Guide a Business

-

Upload

gerald-manning -

Category

Documents

-

view

216 -

download

1

Transcript of Entrepreneurship and Small Business Management Chapter 13 Using Financial Statements to Guide a...

Entrepreneurship and Small Business Management

Chapter 13 Using Financial Statements to

Guide a Business

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.2

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Ch. 13 Performance Objectives Understand an income statement.

Examine a balance sheet to determine a business’s financing strategy.

Use the balance sheet equation for analysis.

Perform a financial ratio analysis of an income statement.

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.3

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Ch. 13 Performance Objectives(continued)

Calculate return on investment.

Perform same-size (common-size) analysis of an income statement.

Use quick, current, and debt ratios to analyze a balance sheet.

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.4

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Financial Statements Entrepreneurs use three basic

financial statements: Income statement Balance sheet Cash flow statement

Together, these financial reports show the health of a business at a glance.

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.5

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Income Statement Shows profit or loss over a particular

time period Revenues > Expenses = Positive Balance Expenses > Revenues = Negative

Balance

Prepared monthly

Serves as a scorecard; helps reveal problems

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.6

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

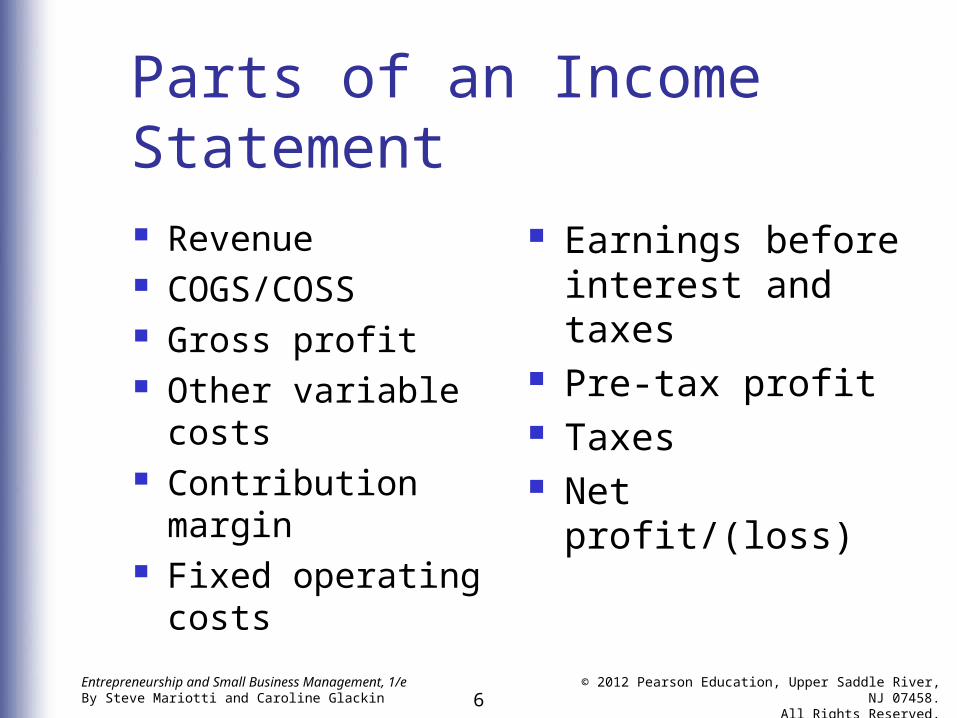

Parts of an Income Statement Revenue COGS/COSS Gross profit Other variable

costs Contribution

margin Fixed operating

costs

Earnings before interest and taxes

Pre-tax profit Taxes Net profit/(loss)

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.7

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Income Statement: Basic Format

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.8

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Income Statement Calculations

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.9

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

A Simple Income Statement

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.10

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

An Income Statement for a More Complex Business

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.11

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Balance Sheet Called a “point-in-time” financial

statement because it shows the state of a business at a given moment

Typically prepared quarterly and at the end of the fiscal year (12-month accounting period chosen by the firm)

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.12

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Parts of a Balance Sheet Assets—things the company owns

that are worth money Liabilities—the company’s debts

that must be paid (including unpaid bills)

Owner’s Equity (OE)— Assets – Liabilities = OE Also called “net worth” The amount of capital in the company

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.13

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Balance Sheet (Horizontal Format)

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.14

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Types/Examples of Assets Current assets—cash, items easily turned

into cash, and items used within one year Accounts receivable Inventory Supplies

Long-term assets—items that would take the business more than one year to use Equipment Furniture Machinery Real estate

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.15

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Types/Examples of Liabilities Current liabilities—debts scheduled for

payment within one year (includes portion of long-term debt due within the year)

Long-term liabilities—debts to be paid over a time period longer than one year

Examples of liabilities: Accounts payable (bills) Loans from banks, family, or friends Mortgages Lines of credit

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.16

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

The Balance Sheet Equation

Assets – Liabilities = Owner’s Equity (OE)or

Assets = Liabilities + Owner’s Equityor

Liabilities = Assets – Owner’s Equity

(Net worth and capital are other names for OE.)

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.17

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Total Assets Must Equal (“Balance”) Total Liabilities + Owner’s Equity

If an item was financed with debt, the loan is a liability.

If an item was purchased with the owner’s (or shareholders’) money, it was financed with equity.

Liabilities and owner’s equity pay for all assets.

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.18

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Analyzing Balance Sheet Data

Compare balance sheets from two different points in time to see progress.

Calculate the percentage of change between the reports for each line item.

An increase in owner’s equity is one way to measure success.

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.19

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Income Statement RatiosExpress each line item as a percentage of sales to see the relationship between items.

Amount (M)

Calculation % of Sales

Sales $10 ($10 ÷ $10) x 100

100%

Less total COGS $ 4 ($4 ÷ $10) X 100

40%

Less other var. costs

$ 0

Contribution margin

$ 6 ($6 ÷ $10) X 100

60%

Less fixed op. costs

$ 3 ($3 ÷ $10) x 100

30%

Profit $ 3 ($3 ÷ $10) x 100

30%

Taxes $ 1 ($1 ÷ $10) x 100

10%

Net profit/(loss) $ 2 ($2 ÷ $10) x 100

20%

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.20

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Return on Investment (ROI)

Entrepreneurs “invest” time, energy, and money because they expect a “return” of money or satisfaction.

Return on investment (ROI) measures return as a percentage of the original investment.

(Net Profit ÷ Investment) X 100 = ROI%

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.21

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Things Needed to Calculate ROI

Net profit—amount the firm has earned beyond what it has spent to cover costs

Total investment—start-up investment plus any additional money invested later

Period of time for which you are calculating ROI—typically one month or one year

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.22

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Return on Sales (ROS) ROS is also called the “profit

margin” because it is an important measure of business profitability.

Net income ÷ sales = ROS

To express this ratio as a percentage, multiply it by 100.

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.23

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Volume and Price Impact ROS

ROS Margin Range

Typical Product

Very low 2-5% Very high volume OR very high price

Low 6-10% High volume OR high price

Moderate 11-20% Moderate volume AND moderate price

High 20-30% Low volume OR low price

Very high 30% and up Very low volume OR very low price

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.24

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Common-Sized (“Same-Size”) Analysis Lets you compare income statements,

even if sales amounts vary.

Compare your expenses with those incurred by other businesses in your industry, or for your own company at different points in time.

Operating ratio—expresses what percentage of sales dollars a particular expense item is using up

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.25

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Quick and Current RatiosQuick Ratio: (Cash + Marketable Securities) ÷ Current

Liabilities Marketable securities—investments such as

certificates of deposit or Treasury bills If the quick ratio is greater than one, there is

enough cash to cover all bills (but not loans) within 24 hours.

Current Ratio: Current Assets ÷ Current Liabilities If the current ratio is greater than one, the

business could sell some assets to pay off its debts.

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.26

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Debt Ratios

Debt-to-Equity Ratio: Total Debt ÷ Equity Indicates how many dollars in the business

were provided by owners/investors Example: A ratio of 1-to-1 means for every

$1 of debt, the company owns $1 of assets.

Debt Ratio: Total Debt ÷ Total Assets Indicates how many dollars in the business

were provided by creditors Example: A ratio of 0.5 means the

company is in debt for 50% of its assets.

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.27

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Operating Efficiency Ratios Collection-period ratio—measures

the average number of days that sales are going uncollected

Receivable turnover ratio—measures the efficiency of your company’s efforts to collect receivables

Inventory turnover ratio—measures how quickly inventory is being sold

© 2012 Pearson Education, Upper Saddle River, NJ 07458.

All Rights Reserved.28

Entrepreneurship and Small Business Management, 1/eBy Steve Mariotti and Caroline Glackin

Formulas for Calculating Operating Efficiency Ratios Collection-Period Ratio:

Average Accounts Receivable (Balance Sheet) Average Daily Sales (Income Statement)

Receivable Turnover Ratio:

Total Sales (Income Statement) Average Accounts Receivable (Balance Sheet)

Inventory Turnover Ratio:

Cost of Goods Sold (Income Statement) Average Inventory (Balance Sheet)

= # of days

= # of times

= # of times