Enhanced 17

43

Multinational Cost of Capital & Capital Structure Multinational Cost of Capital & Capital Structure 17 17 Chapter Chapter South-Western/Thomson Learning © 2003

Transcript of Enhanced 17

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 1/43

Multinational Cost of Capital& Capital Structure

Multinational Cost of Capital& Capital Structure

1717 Chapter Chapter

South-Western/Thomson Learning © 2003

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 2/43

C17 - 2

Chapter Objectives

• To explain how corporate and

country characteristics influence an

MNC’s cost of capital;• To explain why there are differences in the

costs of capital across countries; and

• To explain how corporate and countrycharacteristics are considered by an MNC

when it establishes its capital structure.

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 3/43

C17 - 3

Cost of Capital

• A firm’s capital consists of equity (retained

earnings and funds obtained by issuing

stock) and debt (borrowed funds).• The cost of equity reflects an opportunity

cost, while the cost of debt is reflected in

interest expenses.

• Firms want a capital structure that will

minimize their cost of capital, and hence the

required rate of return on projects.

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 4/43

C17 - 4

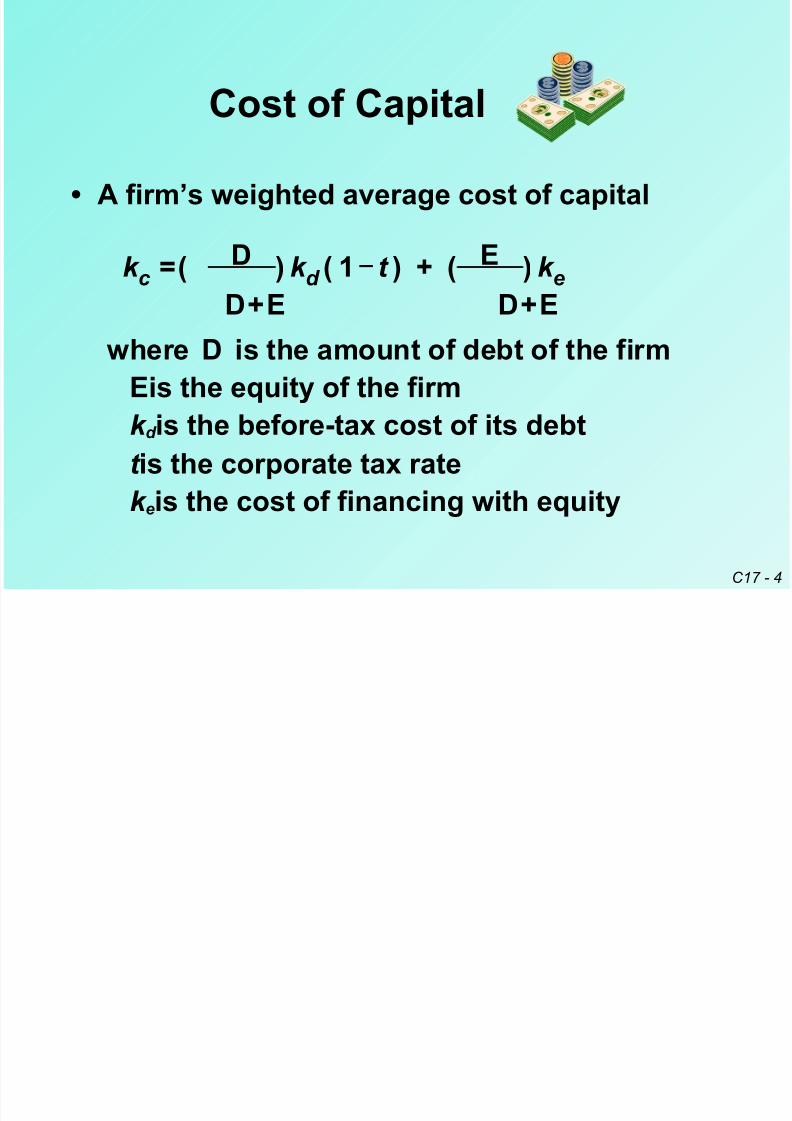

• A firm’s weighted average cost of capital

k c = (D

) k d (

1 _

t

) + (E

) k eD + E D + E

where D is the amount of debt of the firm

Eis the equity of the firm

k d is the before-tax cost of its debt

t is the corporate tax rate

k eis the cost of financing with equity

Cost of Capital

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 5/43

C17 - 5

• The interest payments on debt are tax

deductible. However, as interest expenses

increase, the probability of bankruptcy willincrease too.

• It is favorable to increase the use of debt

financing until the point at which the

bankruptcy probability becomes large

enough to offset the tax advantage of using

debt.

Cost of Capital

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 6/43

C17 - 6

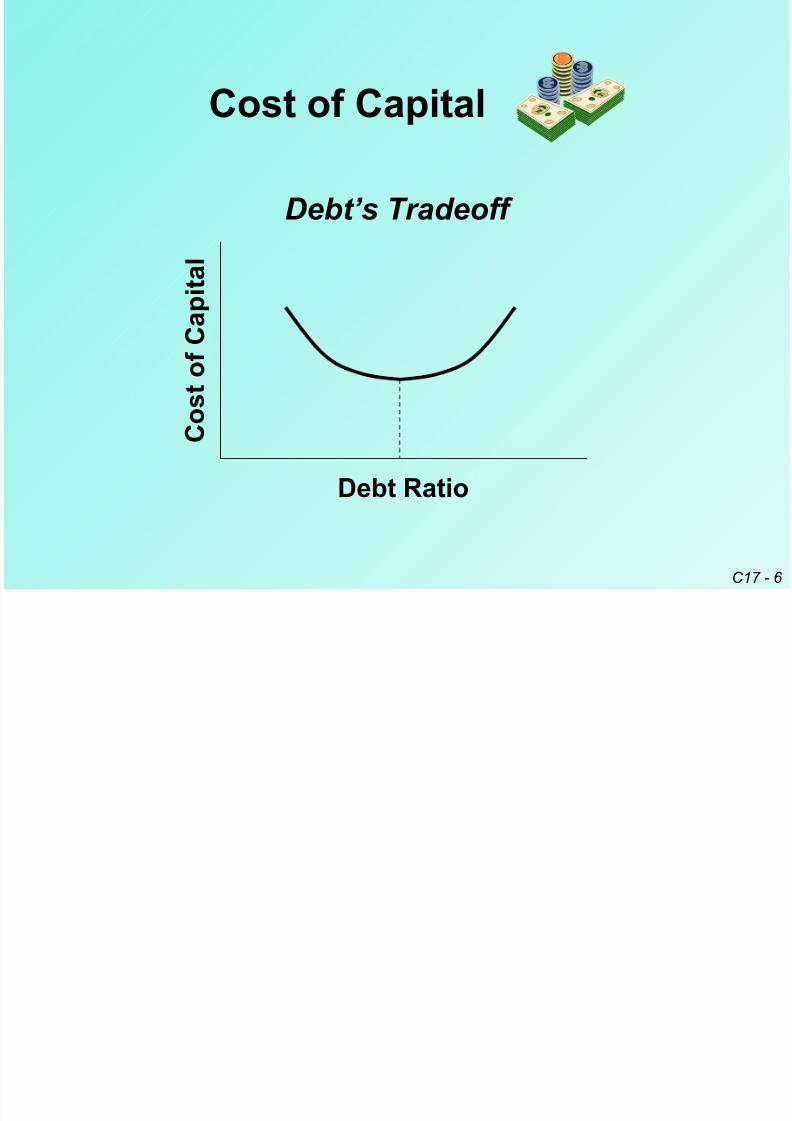

Debt’s Tradeoff

Cost of Capital

Co

st

ofCapita

l

Debt Ratio

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 7/43C17 - 7

Cost of Capital for MNCs

• The cost of capital for MNCs may differ

from that for domestic firms because of

the following differences.Size of Firm. Because of their size, MNCs

are often given preferential treatment by

creditors. They can usually achievesmaller per unit flotation costs too.

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 8/43C17 - 8

Acess to International Capital Markets.

MNCs are normally able to obtain funds

through international capital markets, wherethe cost of funds may be lower.

International Diversification. M NCs may

have more stable cash inflows due to

international diversification, such that their

probability of bankruptcy may be lower.

Cost of Capital for MNCs

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 9/43C17 - 9

Exposure to Exchange Rate Risk. MNCs

may be more exposed to exchange rate

fluctuations, such that their cash flows maybe more uncertain and their probability of

bankruptcy higher.

Exposure to Country Risk. M NCs that have

a higher percentage of assets invested in

foreign countries are more exposed to

country risk.

Cost of Capital for MNCs

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 10/43C17 - 10

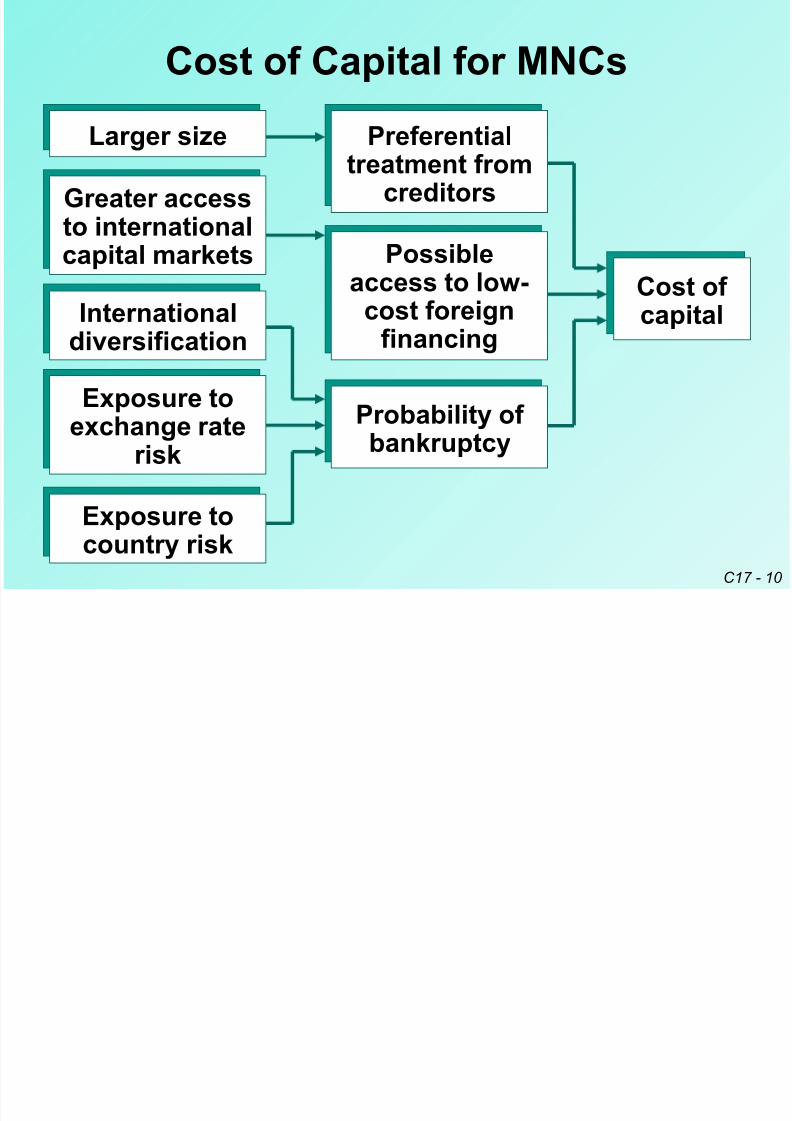

Cost of Capital for MNCs

Possible

access to low-cost foreign

financing

Preferentialtreatment from

creditorsGreater accessto internationalcapital markets

Larger size

Internationaldiversification

Exposure toexchange rate

risk

Exposure to

country risk

Cost of capital

Probability of bankruptcy

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 11/43C17 - 11

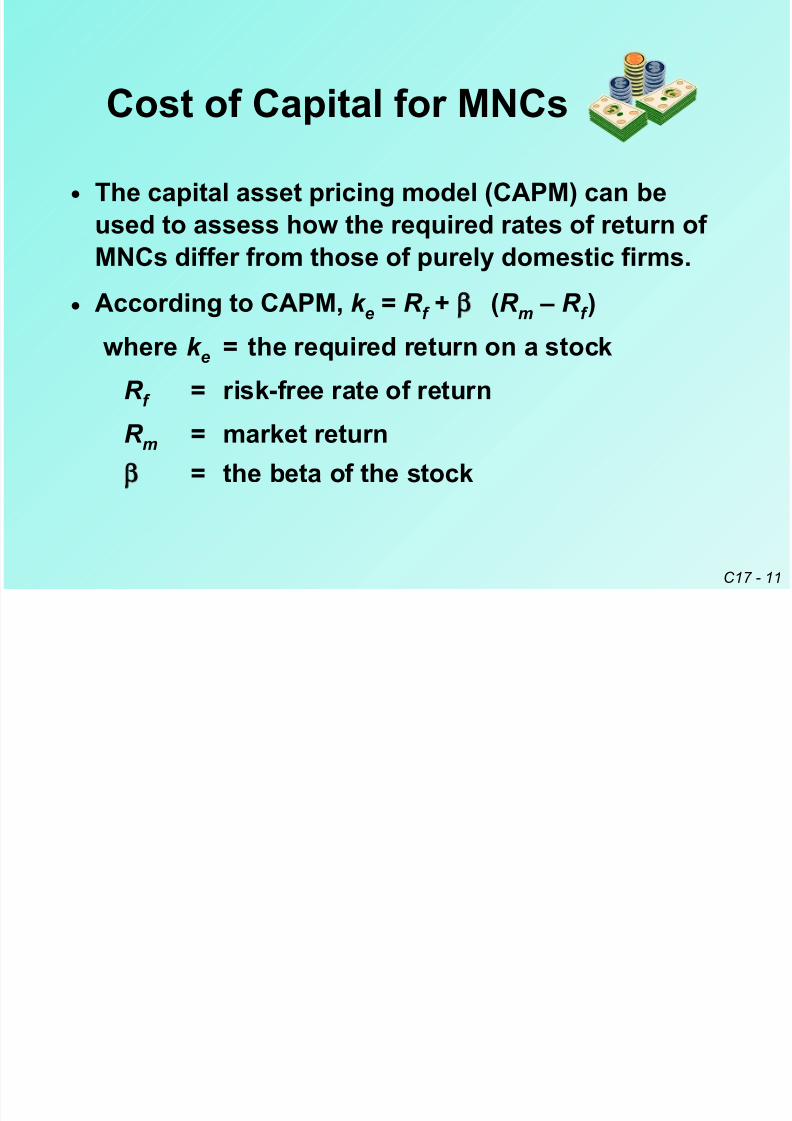

• The capital asset pricing model (CAPM) can be

used to assess how the required rates of return of

MNCs differ from those of purely domestic firms.

• According to CAPM, k e = R f + β (R m – R f )

where k e = the required return on a stock

R f = risk-free rate of return

R m = market return

β = the beta of the stock

Cost of Capital for MNCs

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 12/43C17 - 12

• A stock’s beta represents the sensitivity of

the stock’s returns to market returns, just as

a project’s beta represents the sensitivity of the project’s cash flows to market

conditions.

• The lower a project’s beta, the lower its

systematic risk, and the lower its required

rate of return, if its unsystematic risk can be

diversified away.

Cost of Capital for MNCs

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 13/43C17 - 13

• An MNC that increases its foreign sales may

be able to reduce its stock’s beta, and hence

the return required by investors. Thistranslates into a lower overall cost of

capital.

• However, MNCs may consider unsystematic

risk as an important factor when

determining a foreign project’s required rate

of return.

Cost of Capital for MNCs

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 14/43C17 - 14

• Hence, we cannot be certain if an MNC will

have a lower cost of capital than a purely

domestic firm in the same industry.

Cost of Capital for MNCs

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 15/43C17 - 15

Costs of Capital Across Countries

• The cost of capital may vary across

countries, such that:

MNCs based in some countries may have acompetitive advantage over others;

MNCs may be able to adjust their

international operations and sources of

funds to capitalize on the differences; and MNCs based in some countries may have a

more debt-intensive capital structure.

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 16/43C17 - 16

Costs of Capital Across Countries

• The cost of debt to a firm is primarily

determined by the prevailing risk-free

interest rate of the borrowed currency and the risk premium required by creditors.

• The risk-free rate is determined by the

interaction of the supply and demand for

funds. It may vary due to different tax laws,

demographics, monetary policies, and

economic conditions.

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 17/43C17 - 17

Costs of Capital Across Countries

• The risk premium compensates creditors

for the risk that the borrower may be

unable to meet its payment obligations.• The risk premium may vary due to

different economic conditions,

relationships between corporations andcreditors, government intervention, and

degrees of financial leverage.

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 18/43C17 - 18

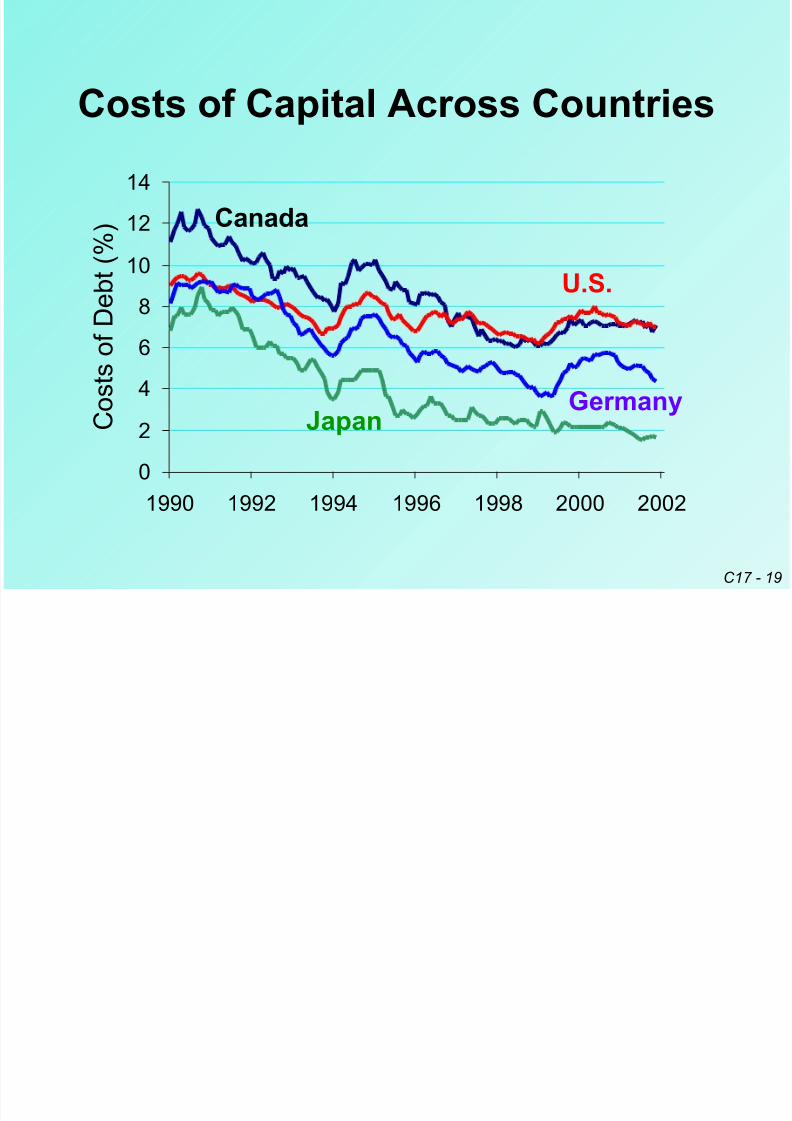

Costs of Capital Across Countries

• Although the cost of debt may vary across

countries, there is some positive

correlation among country cost-of-debtlevels over time.

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 19/43C17 - 19

Costs of Capital Across Countries

0

2

4

6

8

10

12

14

1990 1992 1994 1996 1998 2000 2002

Canada

U.S.

GermanyJapanC

osts

ofDebt

(%)

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 20/43C17 - 20

Costs of Capital Across Countries

• A country’s cost of equity represents an

opportunity cost – what the shareholders

could have earned on investments withsimilar risk if the equity funds had been

distributed to them.

•The return on equity can be measured by

the risk-free interest rate plus a premium

that reflects the risk of the firm.

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 21/43C17 - 21

Costs of Capital Across Countries

• A country’s cost of equity can also be

estimated by applying the price/earnings

multiple to a given stream of earnings.• A high price/earnings multiple implies that

the firm receives a high price when selling

new stock for a given level of earnings.

So, the cost of equity financing is low.

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 22/43C17 - 22

Costs of Capital Across Countries

• The costs of debt and equity can be

combined, using the relative proportions

of debt and equity as weights, to derive anoverall cost of capital.

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 23/43

C17 - 23

• For country-specific information, visit:

¤ http://www.bloomberg.com/

¤ http://www.pwcglobal.com

¤ http://www.morganstanley.com/gef/

¤ http://www.worldbank.org/data/

¤ http://biz.yahoo.com/ifc/

Online Application

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 24/43

C17 - 24

Using the Cost of Capital

for Assessing Foreign Projects• Foreign projects may have risk levels

different from that of the MNC, such that

the MNC’s weighted average cost of capital (WACC) may not be the appropriate

required rate of return.

•There are various ways to account for this

risk differential in the capital budgeting

process.

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 25/43

C17 - 25

Using the Cost of Capital

for Assessing Foreign ProjectsDerive NPVs based on the WACC.

¤ The probability distribution of NPVs can be

computed to determine the probability that theforeign project will generate a return that is at

least equal to the firm’s WACC.

Adjust the WACC for the risk differential.

¤ The MNC may estimate the cost of equity and

the after-tax cost of debt of the funds needed

to finance the project.

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 26/43

C17 - 26

The MNC’s

Capital Structure Decision• The overall capital structure of an MNC is

essentially a combination of the capital

structures of the parent body and itssubsidiaries.

• The capital structure decision involves the

choice of debt versus equity financing,

and is influenced by both corporate and

country characteristics.

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 27/43

C17 - 27

The MNC’s

Capital Structure DecisionCorporate Characteristics

• Stability of cash flows. MNCs with more stable

cash flows can handle more debt.• Credit risk. MNCs that have lower credit risk

have more access to credit.

• Access to retained earnings. Profitable MNCs

and MNCs with less growth may be able to

finance most of their investment with retained

earnings.

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 28/43

C17 - 28

The MNC’s

Capital Structure Decision

• Agency problems. Host country

shareholders may monitor a subsidiary,though not from the parent’s perspective.

• Guarantees on debt. If the parent backs the

subsidiary’s debt, the subsidiary may be ableto borrow more.

Corporate Characteristics

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 29/43

C17 - 29

Country Characteristics

• Stock restrictions. MNCs in countries

where investors have less investmentopportunities may be able to raise equity

at a lower cost.

• Interest rates. MNCs may be able to obtainloanable funds (debt) at a lower cost in

some countries.

The MNC’s

Capital Structure Decision

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 30/43

C17 - 30

• Country risk. If the host government islikely to block funds or confiscate assets,

the subsidiary may prefer debt financing.

The MNC’s

Capital Structure Decision

• Strength of currencies. MNCs tend to borrow the host

country currency if they expect it to weaken, so as toreduce their exposure to exchange rate risk.

Country Characteristics

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 31/43

C17 - 31

• Tax laws. MNCs may use more local debt

financing if the local tax rates (corporatetax rate, withholding tax rate, etc.) are

higher.

The MNC’s

Capital Structure DecisionCountry Characteristics

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 32/43

C17 - 32

Interaction Between Subsidiary

and Parent Financing DecisionsIncreased debt financing by the subsidiary

⇒A larger amount of internal funds may be

available to the parent.⇒The need for debt financing by the parent may

be reduced.

• The revised composition of debt financing may

affect the interest charged on debt as well as

the MNC’s overall exposure to exchange rate

risk.

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 33/43

C17 - 33

Interaction Between Subsidiary

and Parent Financing DecisionsReduced debt financing by the subsidiary

⇒A smaller amount of internal funds may be

available to the parent.⇒The need for debt financing by the parent may

be increased.

• The revised composition of debt financing may

affect the interest charged on debt as well as

the MNC’s overall exposure to exchange rate

risk.

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 34/43

C17 - 34

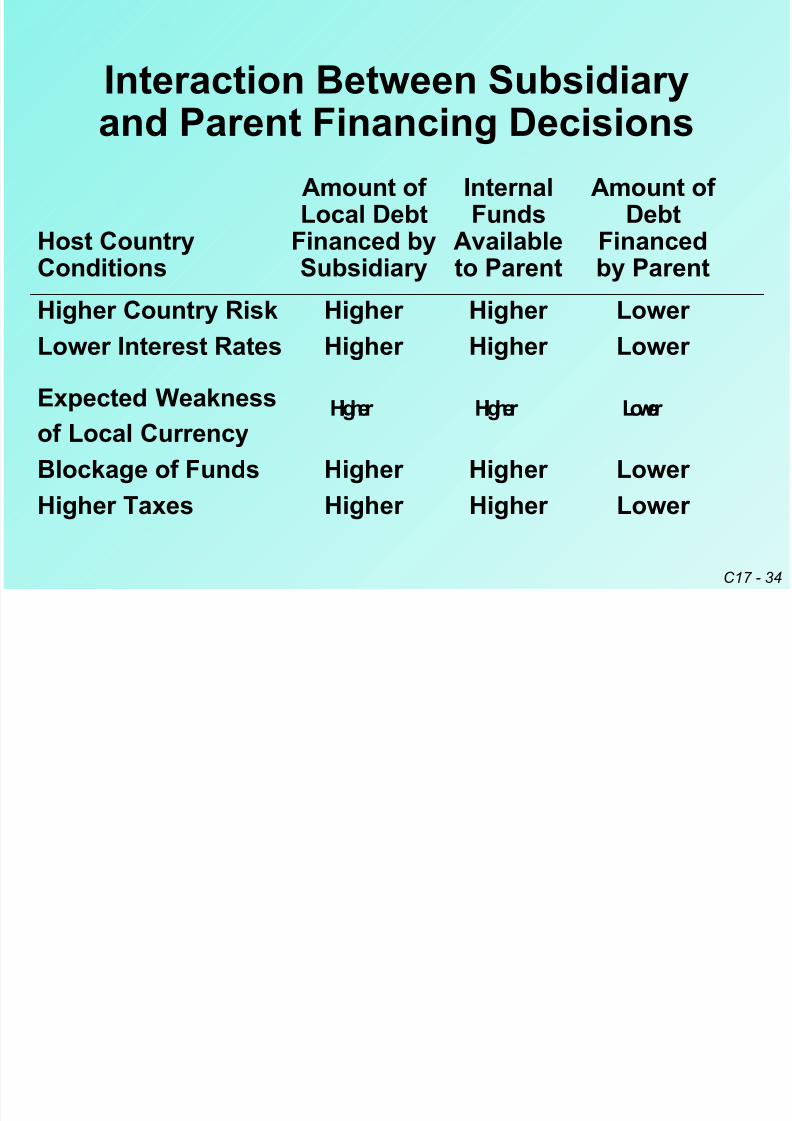

Amount of Internal Amount of Local Debt Funds Debt

Host Country Financed by Available Financed

Conditions Subsidiary to Parent by ParentHigher Country Risk Higher Higher Lower

Lower Interest Rates Higher Higher Lower

Expected WeaknessHigher Higher Lower of Local Currency

Blockage of Funds Higher Higher Lower

Higher Taxes Higher Higher Lower

Interaction Between Subsidiary

and Parent Financing Decisions

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 35/43

C17 - 35

Using a Target Capital Structure

on a Local versus Global Basis• An MNC may deviate from its “local” target

capital structure as necessitated by local

conditions.• However, the proportions of debt and equity

financing in one subsidiary may be adjusted

to offset an abnormal degree of financial

leverage in another subsidiary.

• Hence, the MNC may still achieve its “global”

target capital structure.

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 36/43

C17 - 36

Using a Target Capital Structure

on a Local versus Global Basis• Note that a capital structure revision may

result in a higher cost of capital.

• Hence, an unusually high or low degree of financial leverage should only be adopted

if the benefits outweigh the overall costs.

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 37/43

C17 - 37

• The volumes of debt and equity issued in

financial markets vary across countries,

indicating that firms in some countries(such as Japan) have a higher degree of

financial leverage on average.

• However, conditions may change over time.

In Germany for example, firms are shiftingfrom local bank loans to the use of debt

security and equity markets.

Using a Target Capital Structure

on a Local versus Global Basis

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 38/43

C17 - 38

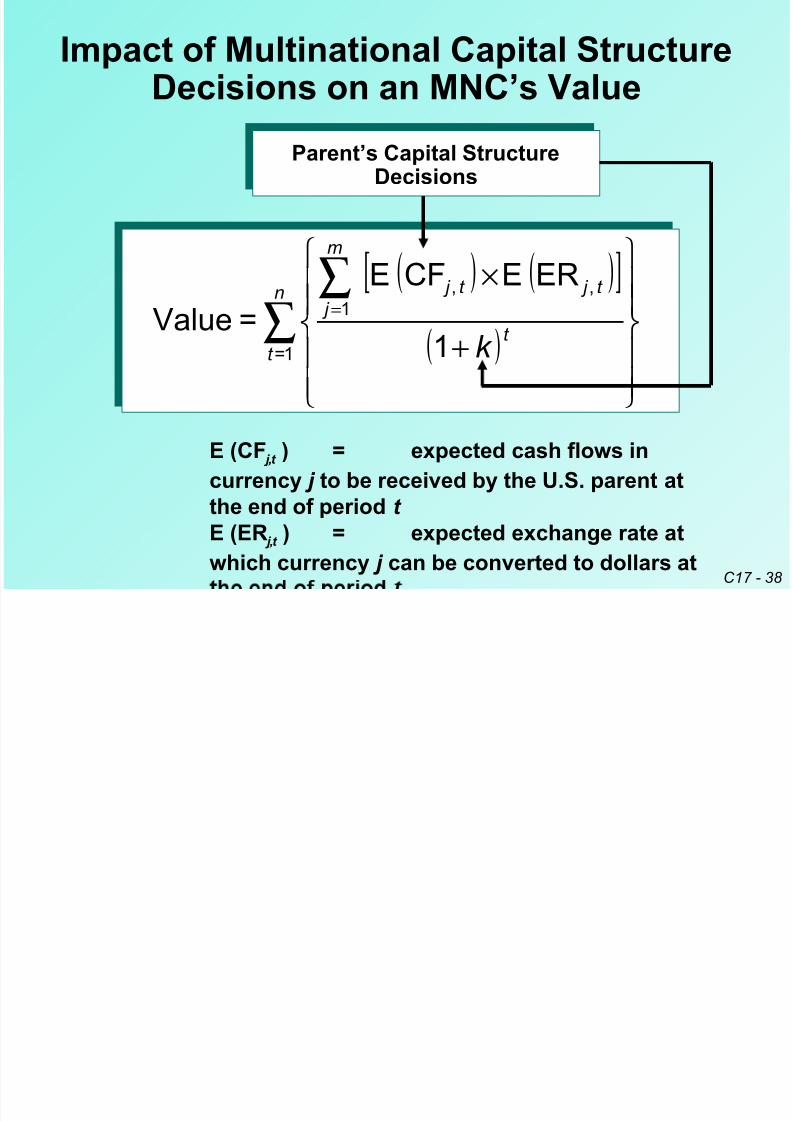

Impact of Multinational Capital StructureDecisions on an MNC’s Value

( ) ( )[ ]( )

∑ ∑

+

×=

n

t t

m

j t j t j

k 1=

1

,,

1

ERECFE =Value

E (CF j,t ) = expected cash flows in

currency j to be received by the U.S. parent at

the end of period t

E (ER j,t ) = expected exchange rate at

which currency j can be converted to dollars at

Parent’s Capital StructureDecisions

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 39/43

C17 - 39

• Introduction to the Cost of Capital

¤ Comparing the Costs of Equity and Debt

• Cost of Capital for MNCs- Size of Firm

- Access to International Capital Markets

- International Diversification- Exposure to Exchange Rate Risk

- Exposure to Country Risk

Chapter Review

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 40/43

C17 - 40

Chapter Review

• Cost of Capital for MNCs … continued

¤ Cost of Capital Comparison Using the

CAPM¤ Implications of the CAPM for an MNC’s

Risk

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 41/43

C17 - 41

Chapter Review

• Costs of Capital Across Countries

¤ Country Differences in the Cost of Debt

¤ Country Differences in the Cost of Equity¤ Combining the Costs of Debt and Equity

• Using the Cost of Capital for Assessing

Foreign Projects¤ Derive NPVs Based on the WACC

¤ Adjust the WACC for the Risk Differential

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 42/43

C17 - 42

Chapter Review

• The MNC’s Capital Structure Decision

¤ Influence of Corporate Characteristics

¤Influence of Country Characteristics

• Interaction Between Subsidiary and Parent

Financing Decisions

¤ Impact of Increased Debt Financing by the

Subsidiary¤ Impact of Reduced Debt Financing by the

Subsidiary

8/6/2019 Enhanced 17

http://slidepdf.com/reader/full/enhanced-17 43/43

Chapter Review

• Using a Target Capital Structure on a Local

versus Global Basis

¤

Offsetting a Subsidiary’s Abnormal Degree of Financial Leverage

¤ Limitations of Offsets

¤ Differences in Financing Tendencies Among

Countries

• Impact of Capital Structure Decisions on an

MNC’s Value

![Structure Total 2013 rolls [Salt Okunur] [Uyumluluk Modu] · 2015-03-17 · Hot Strip Mill Work Rolls ICDP (including enhanced carbide) HiCr iron (including enhanced carbide) HiCr](https://static.fdocuments.us/doc/165x107/5e76d05cb0fe166d1527c7ec/structure-total-2013-rolls-salt-okunur-uyumluluk-modu-2015-03-17-hot-strip.jpg)