Engineering Economics -...

28

Engineering Economics Chapter 3 Interest and Equivalence

Transcript of Engineering Economics -...

Engineering Economics

Chapter 3

Interest and Equivalence

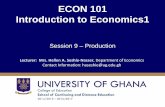

Cash Flow Diagrams (CFD)

• Costs & benefits of engineering products occur over time

– Use Cash Flow Diagram to represent them.

• CFD illustrates the size, sign, and timing of individual cash

flows.

• Use one perspective: One person’s cash outflow is another

person’s inflow

• 0 1 2 3 4 5

2

$100

Time 0

(Today)

$100 $100(+)

$150(-) $150

$50

Cash Flow Diagrams (CFD)

• Used to model the positive and negative cash flows.

• At each time at which cash flow will occur, a vertical

arrow is added, point down for costs and up for

revenues.

• Cash flow are drawn to relative scale

• Rent and insurance are beginning-of-period cash

flows; i.e. just put an arrow in where it occurs.

• O&M, salvages, and revenues are assumed to be end-

of-period cash flows.

3

4

Example 3-1

Purchase a new $30,000 mixing machine. The machine

may be paid for in one of two ways

– A. Pay the full price now minus a 3% discount

– B. Pay $5000 now, $8000 at the end of 1st yr, and $6000 at

end of next four year

List the alternatives in the form of a table of cash flows

5

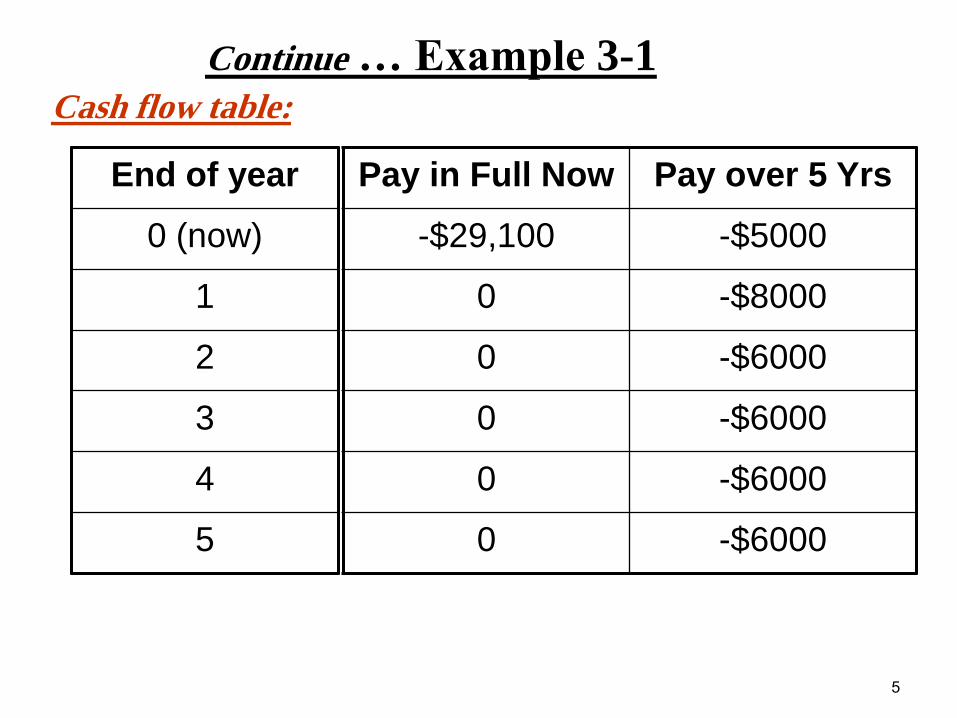

Continue … Example 3-1

End of year

0 (now)

1

2

3

4

5

Pay in Full Now Pay over 5 Yrs

-$29,100 -$5000

0 -$8000

0 -$6000

0 -$6000

0 -$6000

0 -$6000

Cash flow table:

6

Example 3-2

A man borrowed $1000 from a bank at 8% interest.

– At the end of 1st yr: Pay half of the $1000 principal amount

plus the interest.

– At the end of 2nd yr: Pay the remaining half of the principal

amount plus the interest for the second year.

Compute the borrower’s cash flow

End of Year Cash Flows

0 (Now) +$1000

1 -580

2 -540

7

Time Value of Money

• If monetary consequences occur in a short period of

time → Simply add the various sums of money

• What if time span is greater?

• $100 cash today vs. $100 cash a year from now?

• Money is rented. The rent is called the interest

• If you put $100 in the bank today, and interest rate

is 9% → $109 a year from now

8

Interest

• Simple Interest

• Compound interest

9

Simple Interest

• Interest that is computed only on the original sum

and not on accrued interest.

– e.g. if you loaned someone the amount of P at a simple

interest rate of i for a period of n years:

• Total interest earned = P × i × n = P i n

• The amount of money due after n years:

F = P + P i n

Or F = P(1+ i n)

10

Example 3-3

You loaned a friend $5000 for 5 years at a simple

interest rate of 8% per year.

How much interest you receive from the loan?

How much will your friend pay you at the end of 5 yrs.

Total interest earned = P i n = (5000)(0.08)(5) = $2000

Amount due at the end of loan = P + P i n = 5000 + 2000

= $7000

11

Compound Interest

• This is the interest normally used in real life

• Interest on top of interest

• Next year’s interest is calculated based on the unpaid

balance due, which includes the unpaid interest from

the preceding period.

12

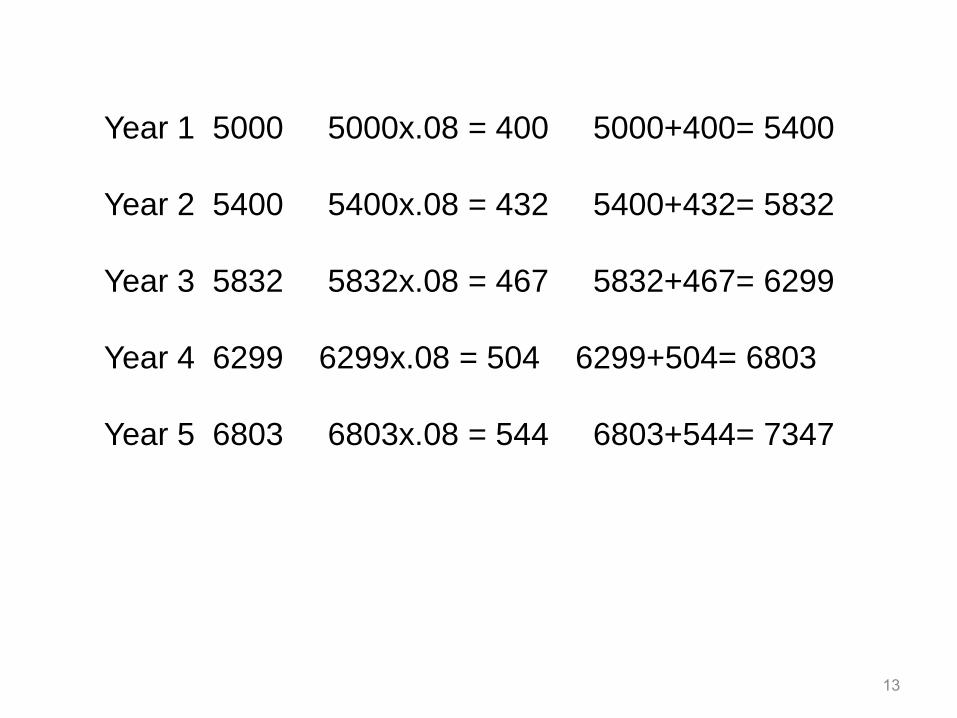

Example 3-4

• To highlight the difference between simple and compound interest, rework Example 3-3 using an interest rate of 8%per year compound interest. How will this change affect the amount that your friend pays you at the end of 5 years?

• Original loan amount (original principal) = $5000

• Loan term = 5 years

• Interest rate charged = 8%per year compound interest

13

Year 1 5000 5000x.08 = 400 5000+400= 5400

Year 2 5400 5400x.08 = 432 5400+432= 5832

Year 3 5832 5832x.08 = 467 5832+467= 6299

Year 4 6299 6299x.08 = 504 6299+504= 6803

Year 5 6803 6803x.08 = 544 6803+544= 7347

… Compound Interest Compound interest is interest that is charged on the original sum

and un-paid interest. You put $500 in a bank for 3 years at 6% compound interest per

year. At the end of year 1 you have (1.06) 500 = $530. At the end of year 2 you have (1.06) 530 = $561.80. At the end of year 3 you have (1.06) $561.80 = $595.51. Note: $595.51 = (1.06) 561.80 = (1.06) (1.06) 530 = (1.06) (1.06) (1.06) 500 = 500 (1.06)3

14

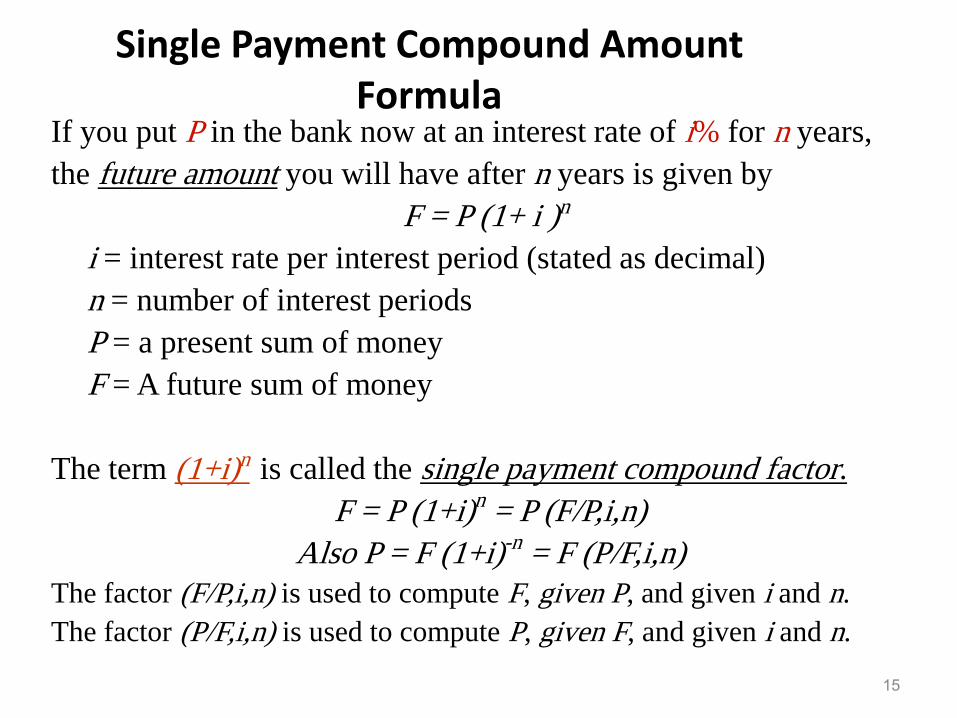

Single Payment Compound Amount Formula

If you put P in the bank now at an interest rate of i% for n years,

the future amount you will have after n years is given by

F = P (1+ i )n

i = interest rate per interest period (stated as decimal)

n = number of interest periods

P = a present sum of money

F = A future sum of money

The term (1+i)n is called the single payment compound factor.

F = P (1+i)n = P (F/P,i,n)

Also P = F (1+i)-n = F (P/F,i,n)

The factor (F/P,i,n) is used to compute F, given P, and given i and n.

The factor (P/F,i,n) is used to compute P, given F, and given i and n.

15

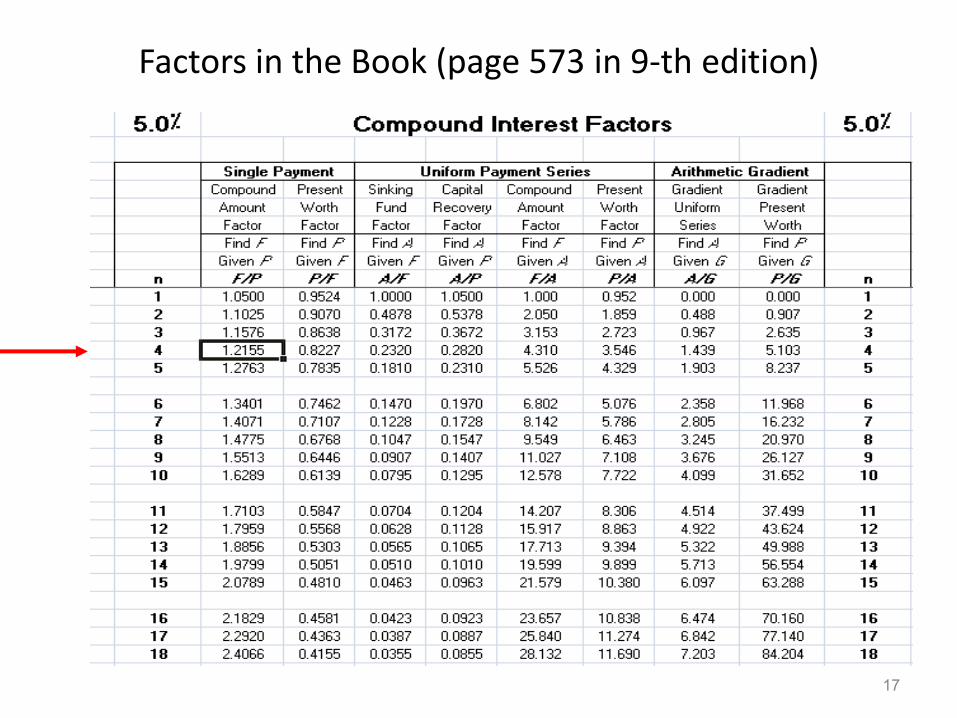

Present Value Example 3-6 If you want to have $800 in savings at the end of four years, and 5% interest is paid annually, how much do you need to put into the savings account today? We solve F = P (1+i)n for P with i = 0.05, n = 4, F = $800.

P = F/(1+i)n = F(1+i)-n

P = 800/(1.05)4 = 800 (1.05)-4 = 800 (0.8227) = $658.16.

Alternate Solution

Single Payment Present Worth Formula

P = F/(1+i)n = F(1+i)-n

P = F (P/F,i,n) , i = 5% and n = 4 periods

From tables in Appendix B, (P/F,i,n) = 0.8227 P = 800 x 0.8227 = $658.16

16

F = 800

P = ?

Factors in the Book (page 573 in 9-th edition)

17

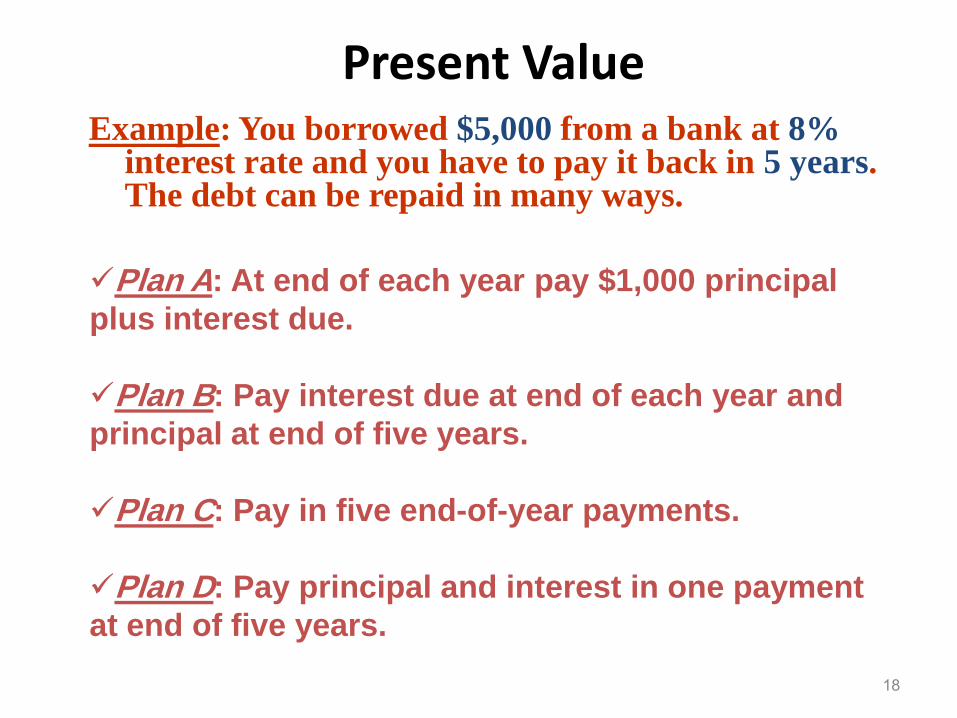

Present Value Example: You borrowed $5,000 from a bank at 8%

interest rate and you have to pay it back in 5 years. The debt can be repaid in many ways.

18

Plan A: At end of each year pay $1,000 principal

plus interest due.

Plan B: Pay interest due at end of each year and

principal at end of five years.

Plan C: Pay in five end-of-year payments.

Plan D: Pay principal and interest in one payment

at end of five years.

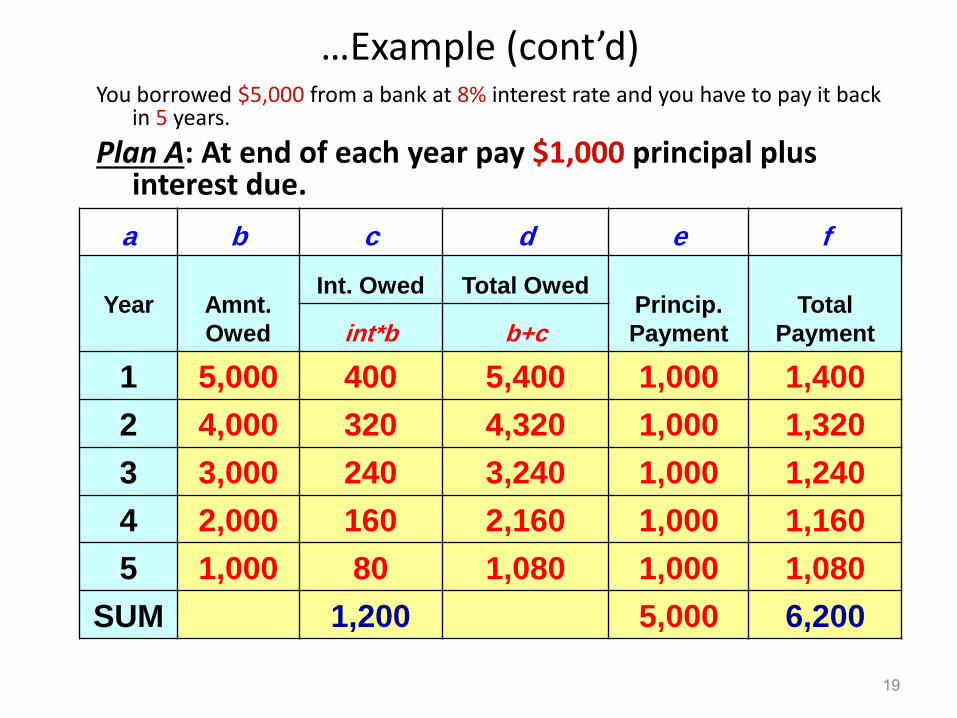

…Example (cont’d) You borrowed $5,000 from a bank at 8% interest rate and you have to pay it back

in 5 years.

Plan A: At end of each year pay $1,000 principal plus interest due.

a b c d e f

Year

Amnt.

Owed

Int. Owed Total Owed Princip.

Payment

Total

Payment int*b b+c

1 5,000 400 5,400 1,000 1,400

2 4,000 320 4,320 1,000 1,320

3 3,000 240 3,240 1,000 1,240

4 2,000 160 2,160 1,000 1,160

5 1,000 80 1,080 1,000 1,080

SUM 1,200 5,000 6,200

19

…Example (cont'd) You borrowed $5,000 from a bank at 8% interest rate and you have to pay it back

in 5 years.

Plan B: Pay interest due at end of each year and principal at end of five years.

a b c d e f

Year

Amnt.

Owed

Int. Owed Total Owed Princip.

Payment

Total

Payment int*b b+c

1 5,000 400 5,400 0 400

2 5,000 400 5,400 0 400

3 5,000 400 5,400 0 400

4 5,000 400 5,400 0 400

5 5,000 400 5,400 5,000 5,400

SUM 2,000 5,000 7,000

20

… Example (cont'd) You borrowed $5,000 from a bank at 8% interest rate and you have to pay it back

in 5 years.

Plan C: Pay in five end-of-year payments.

a b c d e f

Year

Amnt.

Owed

Int. Owed Total Owed Princip.

Payment

Total

Payment int*b b+c

1 5,000 400 5,400 852 1,252

2 4,148 332 4,480 920 1,252

3 3,227 258 3,485 994 1,252

4 2,233 179 2,412 1,074 1,252

5 1,160 93 1,252 1,160 1,252

SUM 1,261 5,000 6,261

21

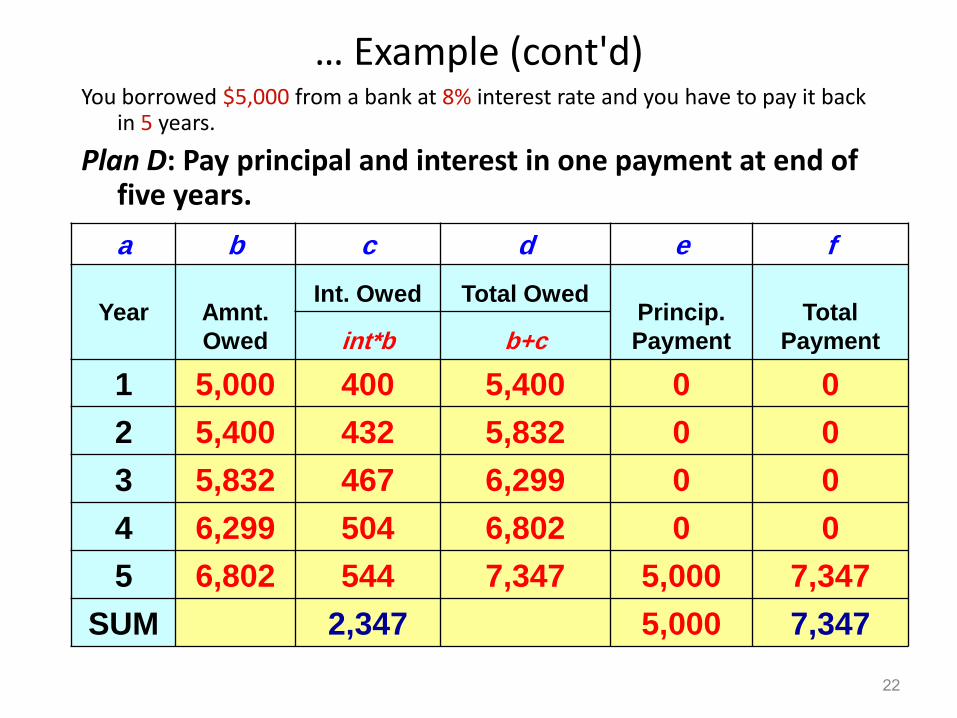

… Example (cont'd) You borrowed $5,000 from a bank at 8% interest rate and you have to pay it back

in 5 years.

Plan D: Pay principal and interest in one payment at end of five years.

a b c d e f

Year

Amnt.

Owed

Int. Owed Total Owed Princip.

Payment

Total

Payment int*b b+c

1 5,000 400 5,400 0 0

2 5,400 432 5,832 0 0

3 5,832 467 6,299 0 0

4 6,299 504 6,802 0 0

5 6,802 544 7,347 5,000 7,347

SUM 2,347 5,000 7,347

22

23

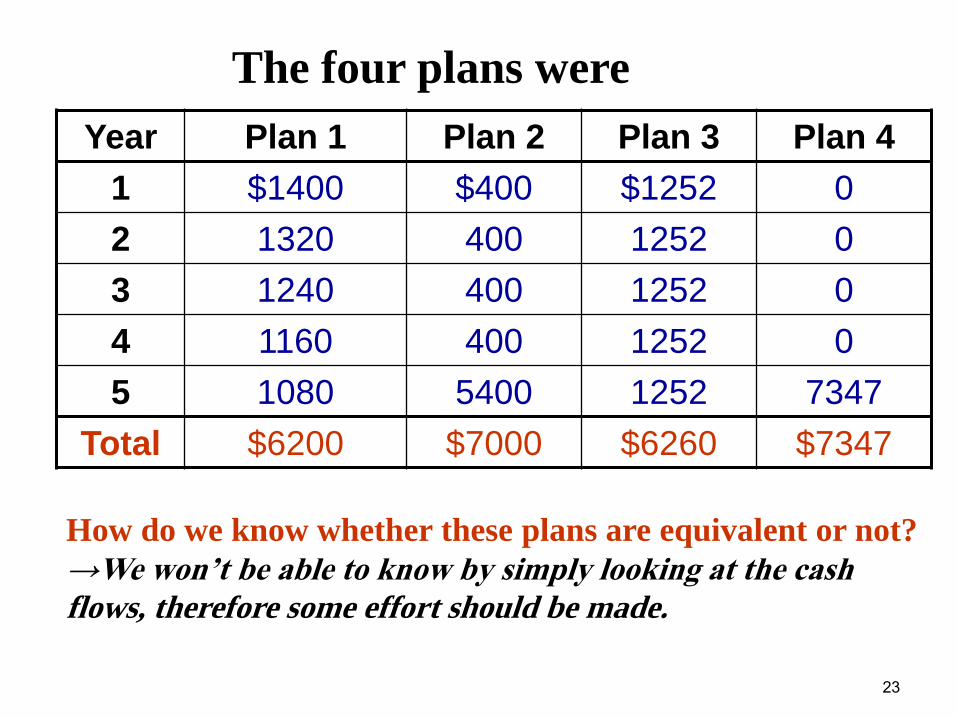

The four plans were

Year Plan 1 Plan 2 Plan 3 Plan 4

1 $1400 $400 $1252 0

2 1320 400 1252 0

3 1240 400 1252 0

4 1160 400 1252 0

5 1080 5400 1252 7347

Total $6200 $7000 $6260 $7347

How do we know whether these plans are equivalent or not?

→We won’t be able to know by simply looking at the cash

flows, therefore some effort should be made.

24

Equivalence

• In the previous example, four payment plans were

described.

• The four plans were used to accomplish the task of

repaying a debt of $5000 with interest at 8%.

• All four plans are equivalent to $5000 now.

• i.e. all four plans are said to be equivalent to each

other and to $5000 now.

25

In 3 years, you need $400 to pay a debt. In two more years, you need $600 more to pay a second debt. How much should you put in the bank today to meet these two needs if the bank pays 12% per year?

Interest is compounded yearly P = 400(P/F,12%,3) + 600(P/F,12%,5) = 400 (0.7118) + 600 (0.5674) = 284.72 + 340.44 = $625.16

Example 3-8

$400

0 1 2 3 4 5

$600

Alternate Solution

P = F(1+i)-n

P = 400(1+0.12)-3

+ 600(1+0.12)-5

P = $625.17

P

26

In 3 years, you need $400 to pay a debt. In two more years, you need $600 more to pay a second debt. How much should you put in the bank today to meet these two needs if the bank pays 12% compounded monthly?

Interest is compounded yearly

P = 400(P/F,12%,3) + 600(P/F,12%,5)

= 400 (0.7118) + 600 (0.5674)

= 284.72 + 340.44 = $625.16

Example 3-8 (Interest Compounded monthly)

$400

0 1 2 3 4 5

$600

Interest is compounded monthly

P = 400(P/F,12%/12,3*12) + 600(P/F,12%/12,5*12)

= 400(P/F,1%,36) + 600(P/F,1%,60)

= 400 (0.6989) + 600 (0.5504)

= 279.56 + 330.24 = $609.80

P

27

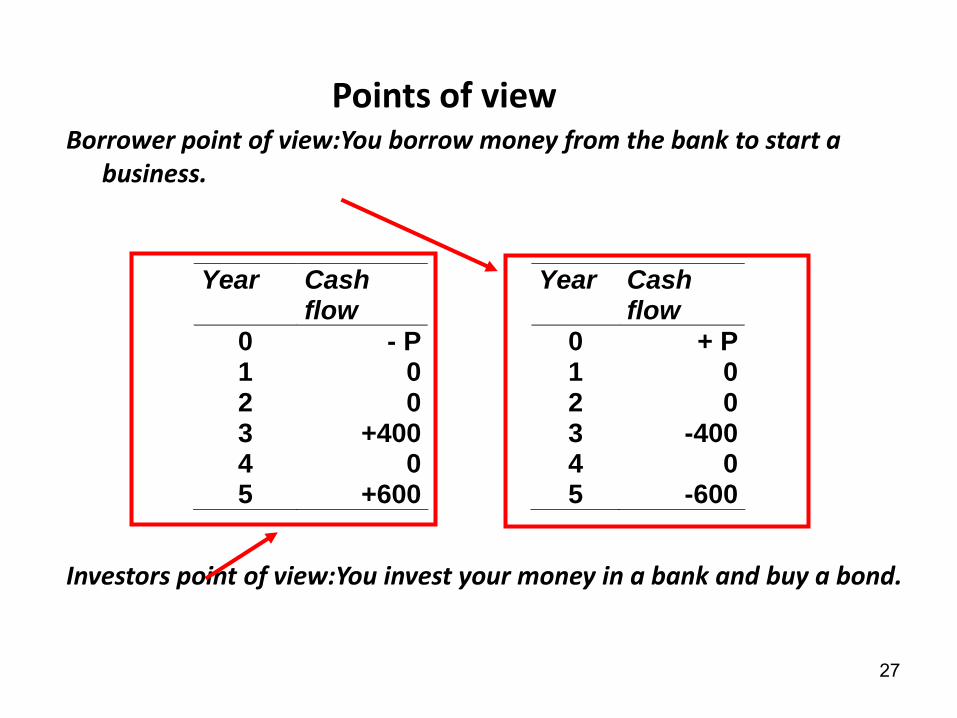

Borrower point of view:You borrow money from the bank to start a business.

Investors point of view:You invest your money in a bank and buy a bond.

Points of view

Year Cash flow

0 - P 1 0 2 0 3 +400 4 0 5 +600

Year Cash flow

0 + P 1 0 2 0 3 -400 4 0 5 -600

28

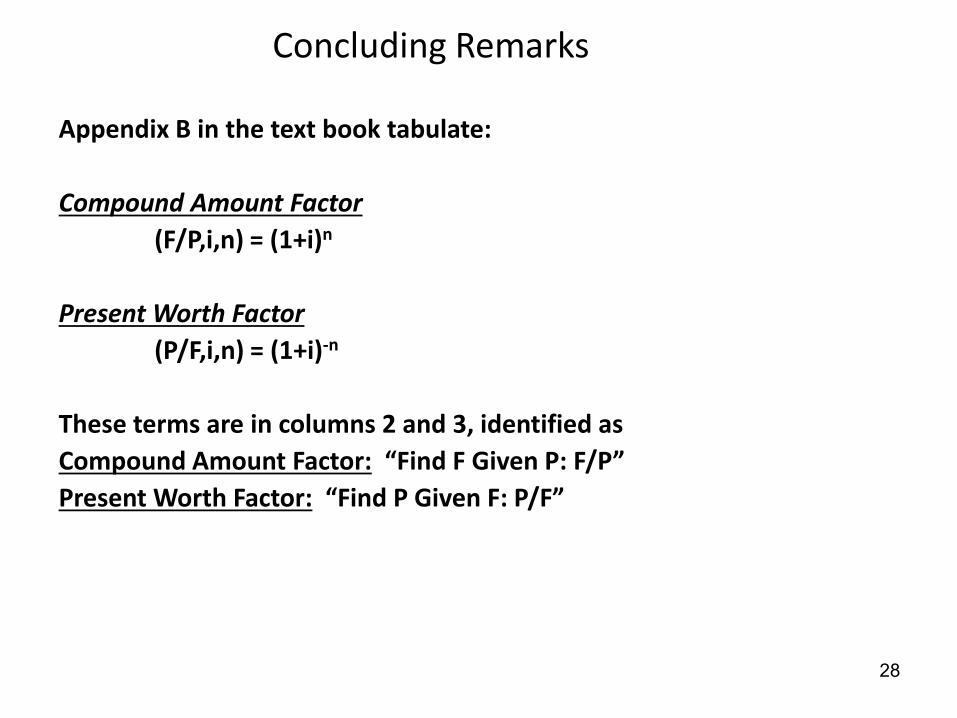

Appendix B in the text book tabulate:

Compound Amount Factor

(F/P,i,n) = (1+i)n

Present Worth Factor

(P/F,i,n) = (1+i)-n

These terms are in columns 2 and 3, identified as

Compound Amount Factor: “Find F Given P: F/P”

Present Worth Factor: “Find P Given F: P/F”

Concluding Remarks