Energy Outlook- Medicine Hat

27

Janet Annesley – Vice President, CAPP Outlook for Canadian Oil & Gas Industry Medicine Hat September 15, 2011

-

Upload

economic-development-alliance-of-southeast-alberta -

Category

Documents

-

view

220 -

download

1

description

On September 15, 2011 the Economic Development Alliance of Southeast Alberta invited Janet Annelsy, VP of Communications for the Canadian Association of Petroleum Producers (CAPP) to talk about the energy outlook in Canada and more specifically in Alberta and the southeast region.

Transcript of Energy Outlook- Medicine Hat

Janet Annesley – Vice President, CAPP

Outlook for Canadian Oil & Gas Industry

Medicine Hat

September 15, 2011

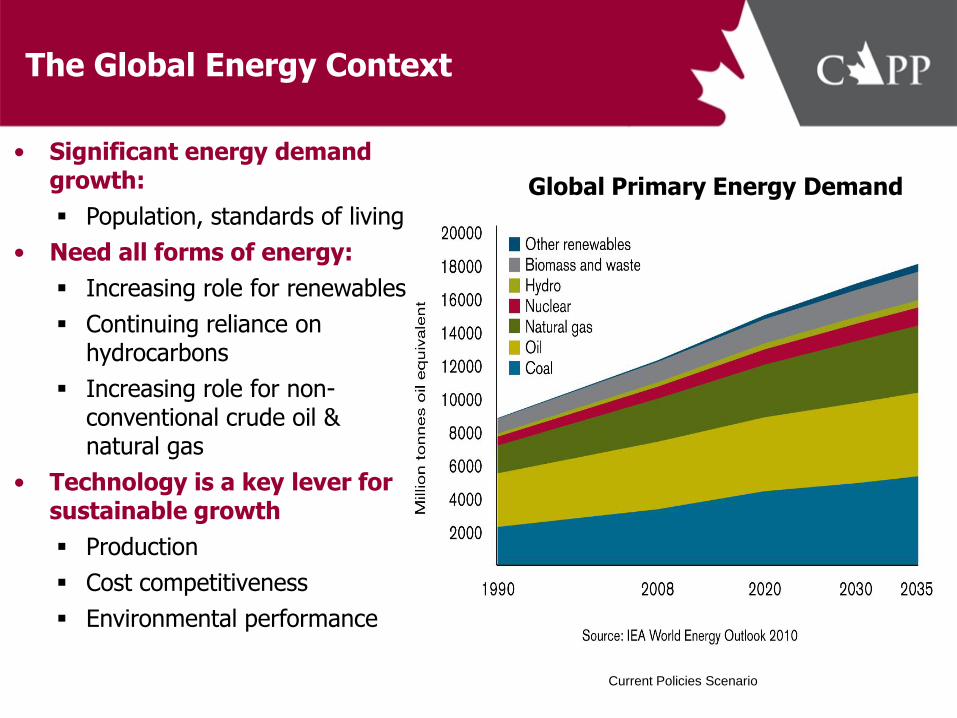

The Global Energy Context

• Significant energy demand growth:

Population, standards of living

• Need all forms of energy:

Increasing role for renewables

Continuing reliance on hydrocarbons

Increasing role for non- conventional crude oil & natural gas

• Technology is a key lever for sustainable growth

Production

Cost competitiveness

Environmental performance

Current Policies Scenario

Global Primary Energy Demand

Canada is a Global Energy Player

#3 Canada is third in the

world in natural gas production.

#1 Canada has the

world’s largest uranium reserves.

#2 Canada is second in

the world in hydro-electricity generation.

#3 Canada is 3rd to Saudi

Arabia & Venezuela in crude oil reserves

4

A Comparison of Annual Revenues Major Canadian Product-Selling Industries

Upstream Oil & Gas

Autos Manufacturing

Forestry & Logging Wheat & Barley

Uranium0

20

40

60

80

100

120

Reven

ues (

$C

Bil

lio

ns)

Source: Statistics Canada, CAPP, Canadian Wheat Board, Natural Resources Canada, Canadian Nuclear Association, ARC

Financial Corp.

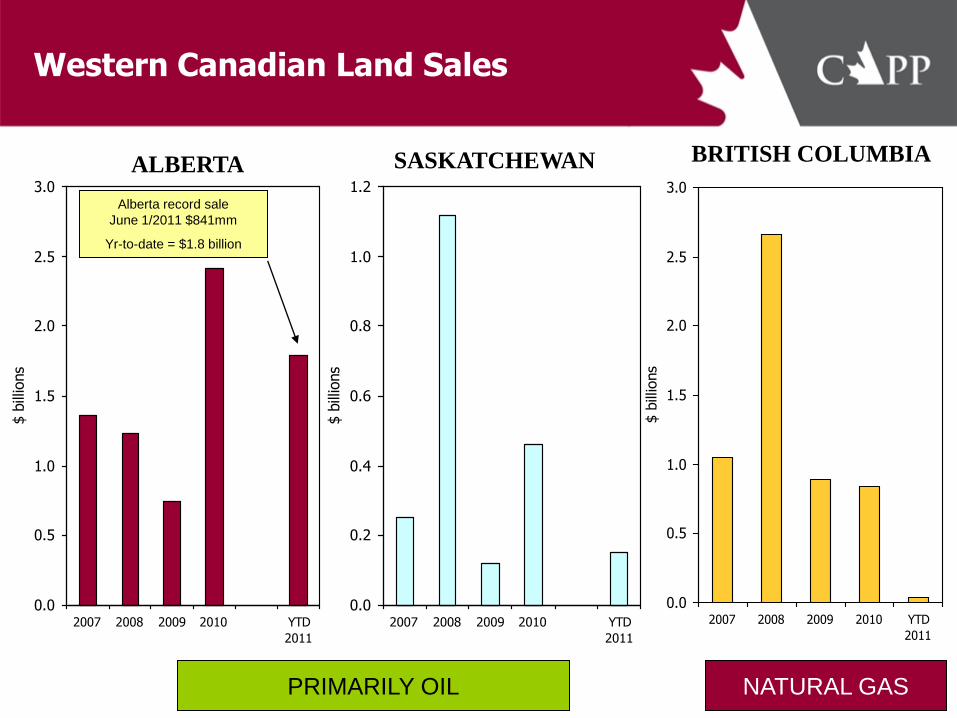

Western Canadian Land Sales

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2007 2008 2009 2010 YTD

2011

$ b

illio

ns

ALBERTA

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2007 2008 2009 2010 YTD

2011

$ b

illio

ns

BRITISH COLUMBIA

0.0

0.2

0.4

0.6

0.8

1.0

1.2

2007 2008 2009 2010 YTD

2011

$ b

illio

ns

SASKATCHEWAN

PRIMARILY OIL NATURAL GAS

Alberta record sale

June 1/2011 $841mm

Yr-to-date = $1.8 billion

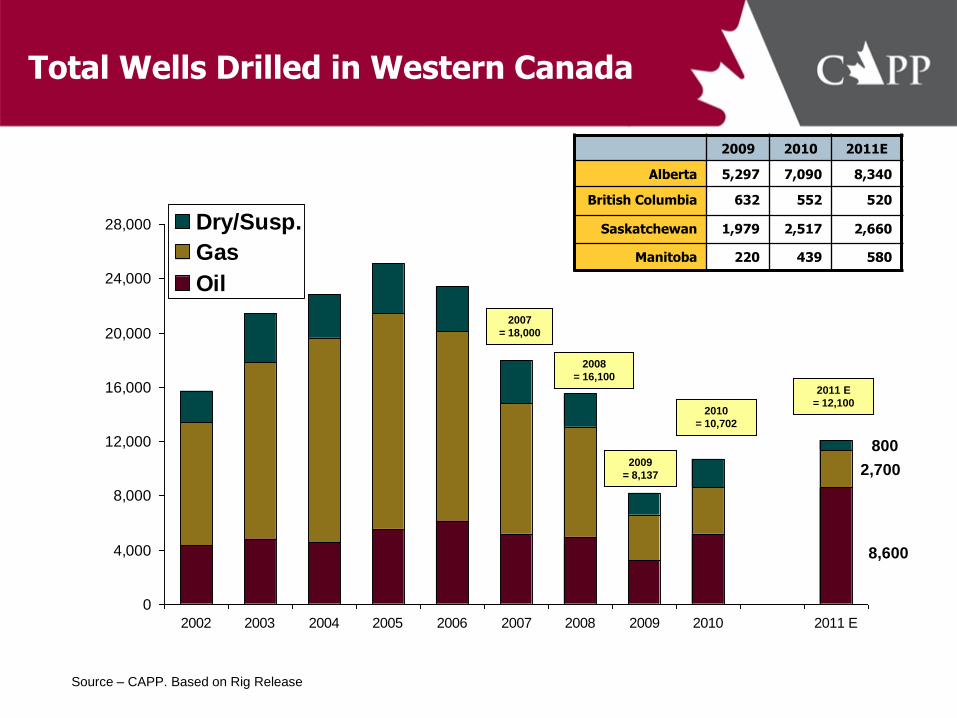

Total Wells Drilled in Western Canada

Source – CAPP. Based on Rig Release

0

4,000

8,000

12,000

16,000

20,000

24,000

28,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 E

Dry/Susp.

Gas

Oil

2007

= 18,000

2008

= 16,100

2009

= 8,137

2010

= 10,702

2011 E

= 12,100

8,600

2,700

800

2009 2010 2011E

Alberta 5,297 7,090 8,340

British Columbia 632 552 520

Saskatchewan 1,979 2,517 2,660

Manitoba 220 439 580

Oil-Directed Well Licences Issued in W. Canada (Cumulative)

Source: Nickle’s DOB

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2009

2006 - 2008

2010

Emerging “Tight Oil” Opportunities

2011

Gas-Directed Well Licences Issued in W. Canada (Cumulative)

Source: Nickle’s DOB

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 & 2008

2011

2006

2009 & 2010

Slowdown in gas / CBM drilling

Industry Capital Spending

Cdn $billions

Northern Canada

2009 2010E 2011F

$0.2 $0.5 $0.3

Oil Sands

2009 2010E 2011F

$11 $13 $16

Western Canada

2009 2010E 2011F

$20 $26 $27

East Coast Offshore

2009 2010E 2011F

$1.7 $2.5 $3.0

Note: Excludes spending mergers & acquisitions

Oil & Gas Investment Spending: 2009: $34 billion 2010: $42 billion (estimate) 2011: $46 billion (forecast)

AB $12 $15 $17

BC $5 $7 $5

SK $3 $4 $5

`09 `10E `11F

10

Contribution to Upstream Revenue (% of Total Revenue by Commodity)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1990 1995 2000 2005 2010 2015

As

a P

erc

en

t o

f T

ota

l R

eve

nu

es

Natural Gas

Oil Sands

Crude Oil and Liquids

Source: CAPP, ARC Financial Corp.

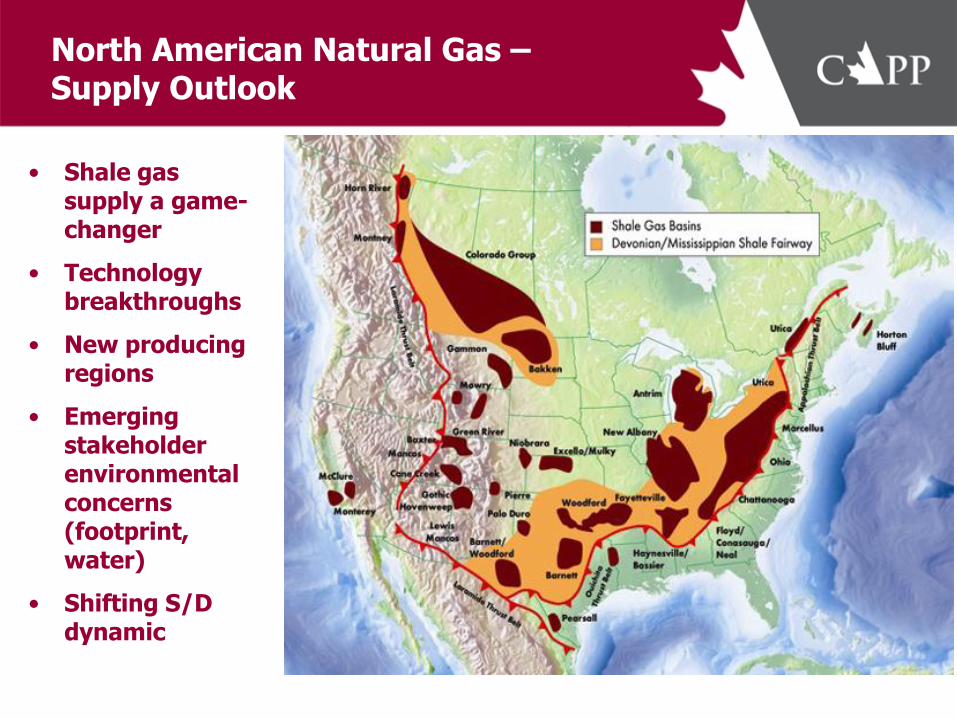

North American Natural Gas – Supply Outlook

• Shale gas supply a game-changer

• Technology breakthroughs

• New producing regions

• Emerging stakeholder environmental concerns (footprint, water)

• Shifting S/D dynamic

W. Canada Natural Gas Production

13

14

15

16

17

18

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

bill

ion c

ubic

feet

per

day

Source: FirstEnergy Capital

2007

WCSB Field Receipts:

2008 – 15.7 bcf/d

2009 – 14.7 bcf/d

2010 – 14.3 bcf/d

2008

2009

2010

2011

0

2

4

6

8

10

12

14

16

18

20

2005 2008 2011 2014 2017 2020

Bcfd

0

2

4

6

8

10

12

14

16

18

20

2005 2008 2011 2014 2017 2020

Bcf

d

Mackenzie Delta

Eastern Canada

Horn & Cordova

Montney

CBM

Conventional

Cdn. Natural Gas Production Forecasts (Recovery and Continued Low Price Cases)

Price Recovery Case

Continued Low Price Case

Note: Prices do not exceed $4/GJ over the forecast period

Note: Prices recover to at least a level of $5.50/GJ

N.A. Natural Gas Pipelines & 2010 Cdn. Exports to U.S. (bcf/d)

TransCanada Transmission Mainline

TQ&M

Westcoast

Kern River

Northwest Northern Border

TransCanada Alberta (NGTL)

NGPL

ANR

ANR El Paso

SoCal

PGT

Texas Eastern

Panhandle

Algonquin

Transcontinental

NGPL

Northwest

Foothills

El Paso

Transwestern

Trailblazer

M&NE

CNG

Iroquois PNGTS Lakes Great

Pacific NW

1.5 bcf/d

California

1.4 bcf/d

Central

4.1 bcf/d

Northeast

2.0 bcf/d

Alliance

ANG/ Foothills

PG&E

Mackenzie Valley Pipeline

Alaska Natural Gas Pipeline

Proposed

Kitimat LNG

Project

Global Crude Oil Reserves by Country

Source: Oil & Gas Journal Dec. 2010

25 20 19

3037

46

60

92102

115

137

175

211

260

0

50

100

150

200

250

300

Saud

i Ara

bia

Vene

zuela

Cana

daIran

Iraq

Kuwait

Abu Dha

bi

Russ

ia

Liby

a

Niger

ia

Kazh

akhs

tan

Qatar

China

Unite

d St

ates

bill

ion b

arr

els

Restricted

(79%)

Open to

Private

Sector

Oil Sands

56%

Other

44%

World Oil Reserves Open to

Private Sector

Canadian Oil Sands and Conventional Oil Production Forecast (2011-2025)

Atlantic Canada

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2005 2007 2009 2011 2013 2015 2017 2019 2021 2023 2025

thousand b

pd

Actual Forecast

In Situ

Mining

Conventional Heavy

Conventional Light Pentanes/Condensate

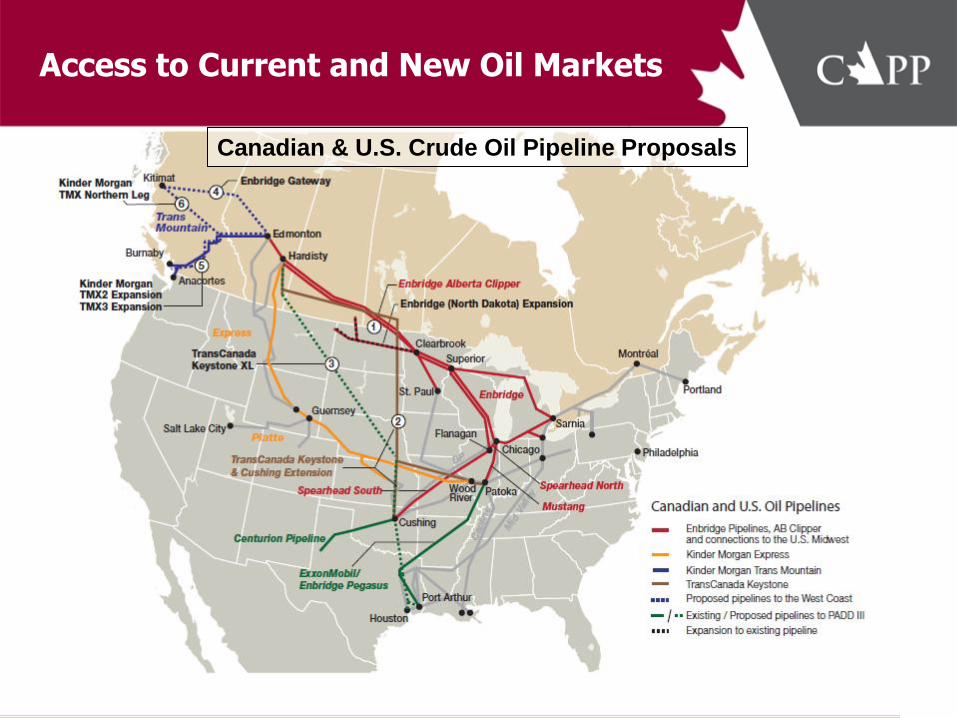

Access to Current and New Oil Markets

Canadian & U.S. Crude Oil Pipeline Proposals

Environmental & Social Performance

• Focus on both crude oil / oil sands & natural gas

• Reputation = Performance + Communication

Continuous performance improvement

More effective messaging (breadth, channels, transparency)

Improved industry collaboration

• Key concerns expressed regarding oil & gas development:

Local / regional environmental & social impacts (air, land, water, biodiversity)

Global climate change

Role of fossil fuels in future energy system

Royal Society of Canada Report Environmental & Health Impacts of Canada’s Oil Sands Industry

• Science-based, independent analysis of the environmental aspects of Canada’s oil sands

• Addresses many of the issues and perceptions of oil sands development: Reclamation is not keeping pace, but

sustainable reclamation is achievable

Water use does not threaten viability of the Athabasca River

No impact on Athabasca water quality/ecosystem and no evidence of impact on human health in downstream communities

Tailings technologies are emerging, but tailings inventory is growing

GHG emissions per barrel are reducing but growing production creates a challenge in meeting international commitments

Minimal impacts on regional air quality December 2010

North American GHG Emissions (2009): Coal-Fired Power and Oil Sands

15 megatonnes

50 megatonnes

100 megatonnes

FL

GA

TX

NC

MI

AL

MO KY

IN OH

NE

NM

ND

CO

SC

KS

IA

TN

WV

WY

VA

MN

UT

OK

WI

AZ

AR

AK

LA

IL

NV

OR

MT

SD

NJ

NY

NH

MS

Legend

U.S. Coal fired power

generating plants

Canadian coal-fired power

generating plants

Canadian oil sands

Sources: U.S. DOE/EIA & Environment Canada

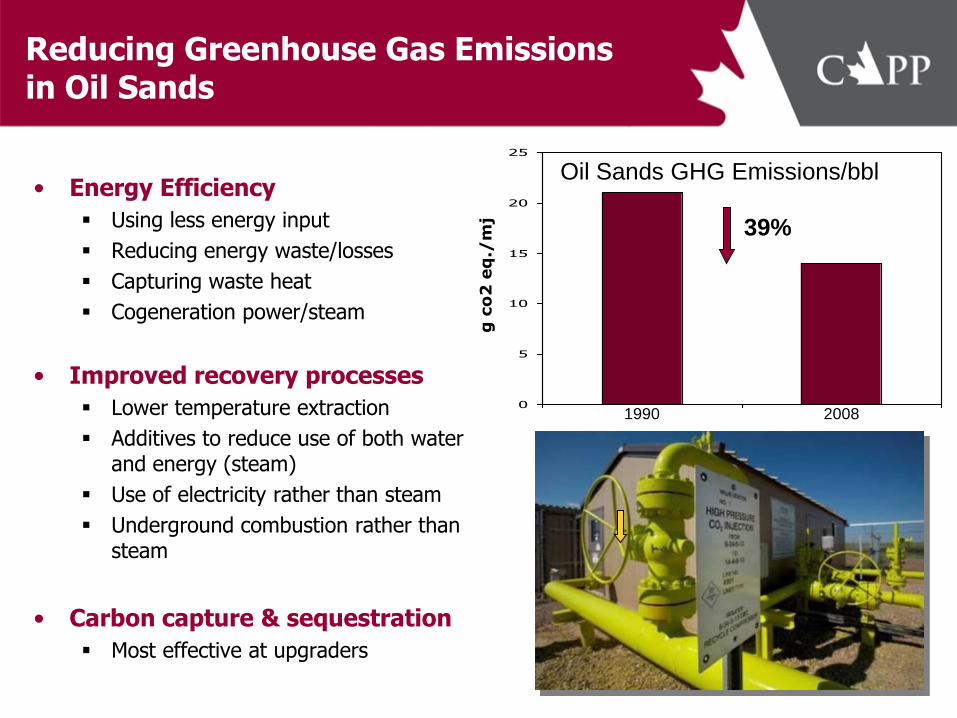

Reducing Greenhouse Gas Emissions in Oil Sands

• Energy Efficiency

Using less energy input

Reducing energy waste/losses

Capturing waste heat

Cogeneration power/steam

• Improved recovery processes

Lower temperature extraction

Additives to reduce use of both water and energy (steam)

Use of electricity rather than steam

Underground combustion rather than steam

• Carbon capture & sequestration

Most effective at upgraders

0

5

10

15

20

25

Oil Sands GHG Emissions/bbl

39%

g c

o2

eq

./m

j

1990 2008

Industry Communications & Engagement - A Portfolio of Activity

• Communications & outreach:

Advertising

Media – mainstream, social

Speeches & presentations

National Oil Sands Dialogues

Meetings & tours

Responsible Canadian Energy Report

Employees

Educational materials (fact books, etc.)

• Directly by industry and via 3rd parties

• Canada, U.S., Europe, Asia

Oil Sands Advertising - Communicating with the Public

To demonstrate that industry takes these issues seriously and what is being done by “real people” to address them.

CAPP TV – Success Stories

A Canadian Energy Strategy

• CAPP supports a Canadian Energy Strategy – clarify and communicate objectives, align resources, implement enabling policy.

• Proposed strategy: Growth in increasingly sustainable hydrocarbon production Growth in renewable energy Shifts in energy demand arising largely from energy efficiency and conservation.

• Market forces are key determinant in decisions on energy supply, transportation and use

• Governments have an important role to play in developing and implementing enabling public policy: Fiscal competitiveness

Regulatory reform

Diversification of markets

Policy to encourage continuous improvement in environmental and social performance

Lower carbon domestic energy supply and use

Technology & innovation

Energy efficiency and conservation

Energy education

Workforce of future

• Recent CEMM at Kananaskis established positive momentum.

Summary

• “3Es”

Environmental performance

Energy security & reliability

Economic growth

• Competitiveness & social license are “must haves”

• Reputation = Performance + Communication

Technology is key performance lever

We all have a role in communication / outreach

• We need to work together & we all need to step up!

A great opportunity for Canada……needs innovative, creative, committed, determined people to make it happen!