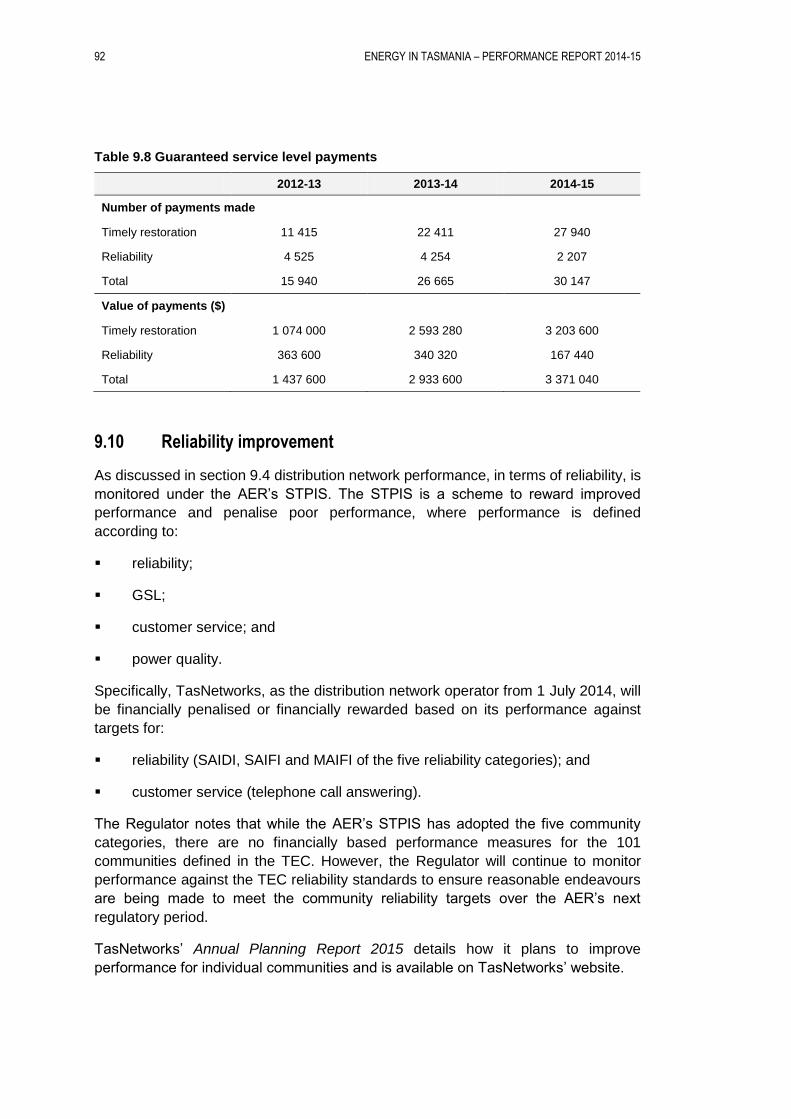

ENERGY IN TASMANIA PERFORMANCE REPORT 2014 15 in Tasmania 2014... · GBE Government Business...

178

ENERGY IN TASMANIA – PERFORMANCE REPORT 2014–15 Office of the Tasmanian Economic Regulator

Transcript of ENERGY IN TASMANIA PERFORMANCE REPORT 2014 15 in Tasmania 2014... · GBE Government Business...

ENERGY IN TASMANIA – PERFORMANCE REPORT

2014–15

Office of the Tasmanian Economic Regulator

Printed January 2016

Office of the Tasmanian Economic Regulator

ISBN 978-0-7246-5388-1

Copyright

© Office of the Tasmanian Economic Regulator

CONTACT DETAILS

Office of the Tasmanian Economic Regulator

Office hours: 8.45am to 5.00pm, Monday to Friday

(except public holidays)

Postal address: GPO Box 770, Hobart, Tasmania 7001

Telephone: (03) 6166 4422 or international +61 3 6166 4422

Email: [email protected]

Website: www.economicregulator.tas.gov.au

ENERGY IN TASMANIA - PERFORMANCE REPORT 2014-15

TABLE OF CONTENTS

TABLE OF CONTENTS .................................................................................... 1

ACRONYMS ............................................................................................................... I

EXECUTIVE SUMMARY ........................................................................................... V

1 OVERVIEW OF THE TASMANIAN ENERGY INDUSTRY ............................. 1

2 ENERGY CONSUMPTION IN TASMANIA ..................................................... 5

2.1 Introduction ................................................................................. 5

2.2 Residential energy consumption ................................................. 6

2.3 Commercial energy consumption ............................................... 7

2.4 Industry energy consumption ...................................................... 8

2.5 Electricity demand ....................................................................... 8

3 OVERVIEW OF THE TASMANIAN ELECTRICITY SUPPLY INDUSTRY ... 13

3.1 Introduction ............................................................................... 13

3.2 Industry structure and participants ............................................ 13

4 ELECTRICITY REGULATION ...................................................................... 15

4.1 Introduction ............................................................................... 15

4.2 Legislative and regulatory framework ....................................... 15

5 REGULATORY BODIES .............................................................................. 19

5.1 Introduction ............................................................................... 19

5.2 Australian Energy Market Commission ..................................... 19

5.3 Australian Energy Regulator ..................................................... 20

5.4 Australian Energy Market Operator .......................................... 21

5.5 Tasmanian Economic Regulator ............................................... 22

5.5.1 Overview ................................................................................. 22

5.5.2 Pricing and pricing related functions ....................................... 23

5.5.3 Regulatory reporting ............................................................... 28

5.5.4 Performance reporting ............................................................ 29

ENERGY IN TASMANIA - PERFORMANCE REPORT 2014-15

5.5.5 Customer Consultative Committee ......................................... 29

6 OTHER GOVERNMENT BODIES ................................................................ 31

6.1 Introduction ............................................................................... 31

6.2 Department of Treasury and Finance ....................................... 31

6.3 Energy Policy Branch, Department of State Growth ................. 31

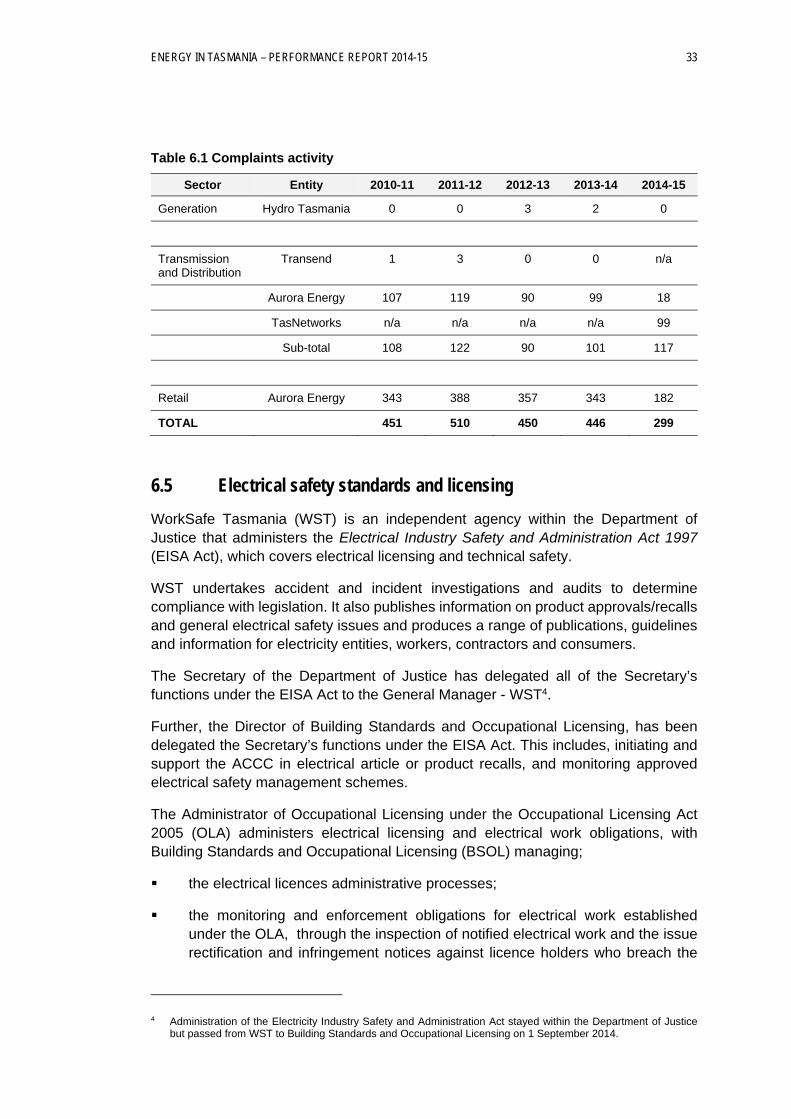

6.4 Energy Ombudsman ................................................................. 32

6.5 Electrical safety standards and licensing .................................. 33

6.6 Climate change policies and regulators .................................... 34

6.6.1 Carbon pricing mechanism ..................................................... 34

6.6.2 Direct Action Policy ................................................................. 35

6.6.3 Renewable Energy Target ...................................................... 35

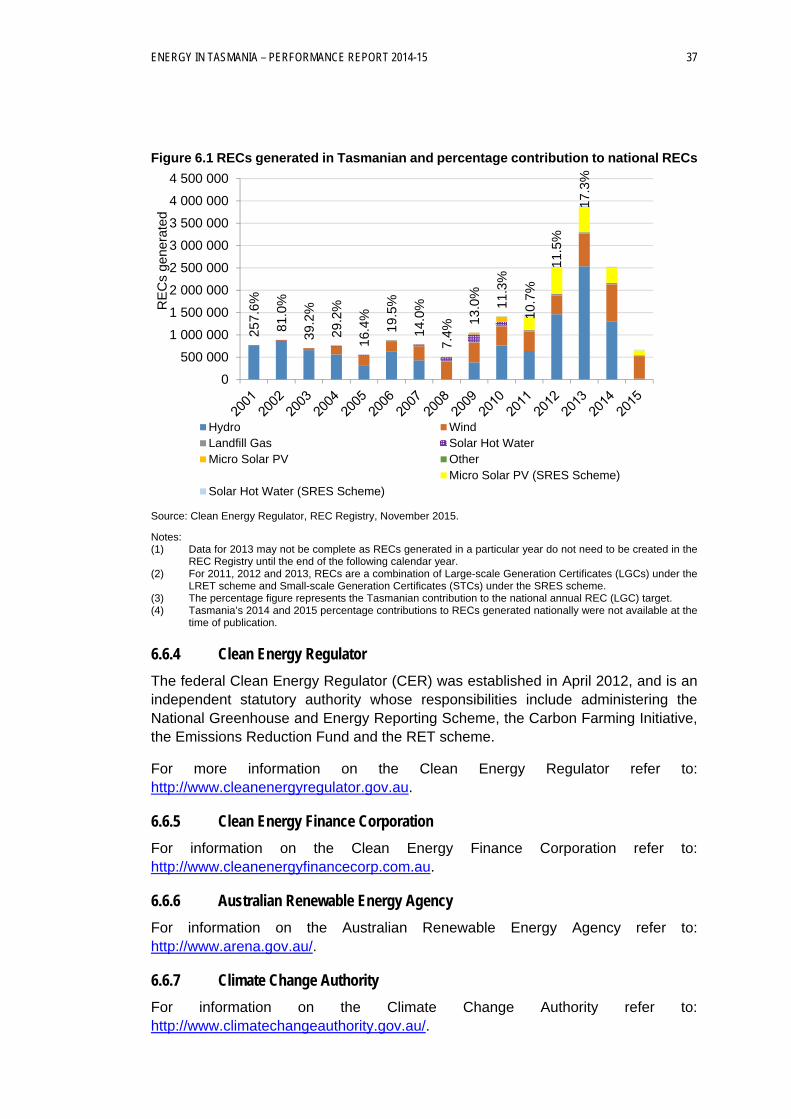

6.6.4 Clean Energy Regulator ......................................................... 37

6.6.5 Clean Energy Finance Corporation ........................................ 37

6.6.6 Australian Renewable Energy Agency ................................... 37

6.6.7 Climate Change Authority ....................................................... 37

7 GENERATION .............................................................................................. 39

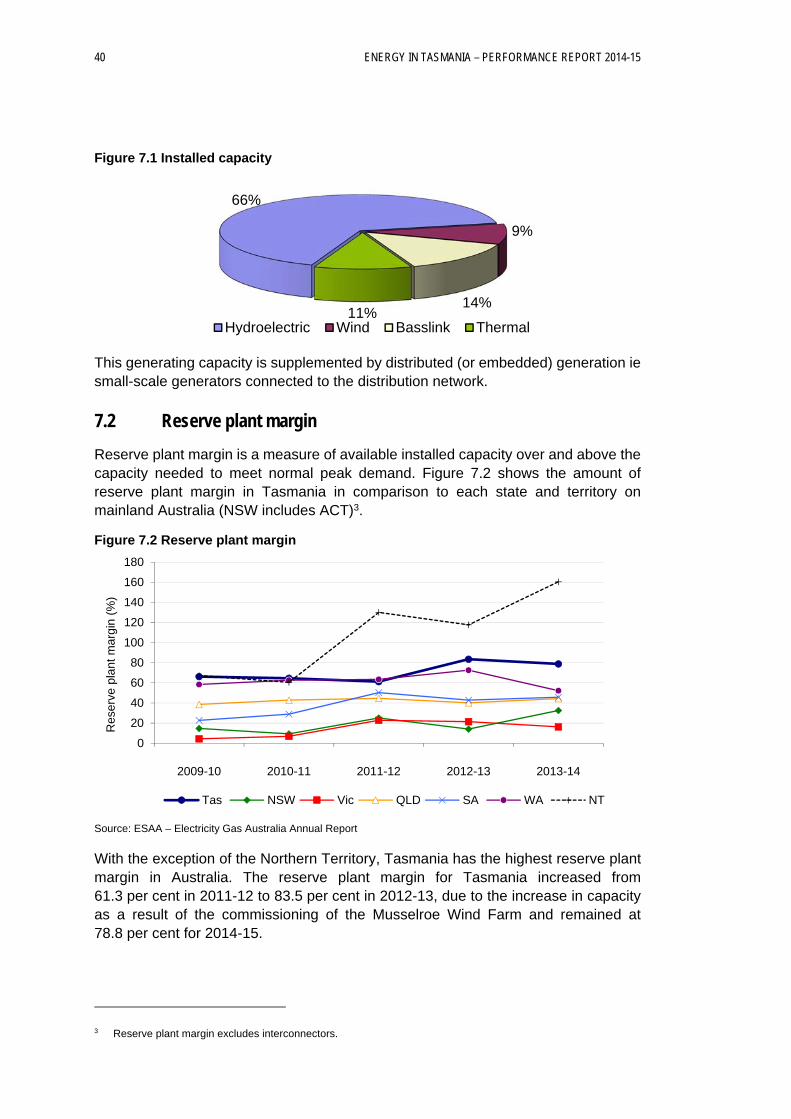

7.1 Installed capacity ...................................................................... 39

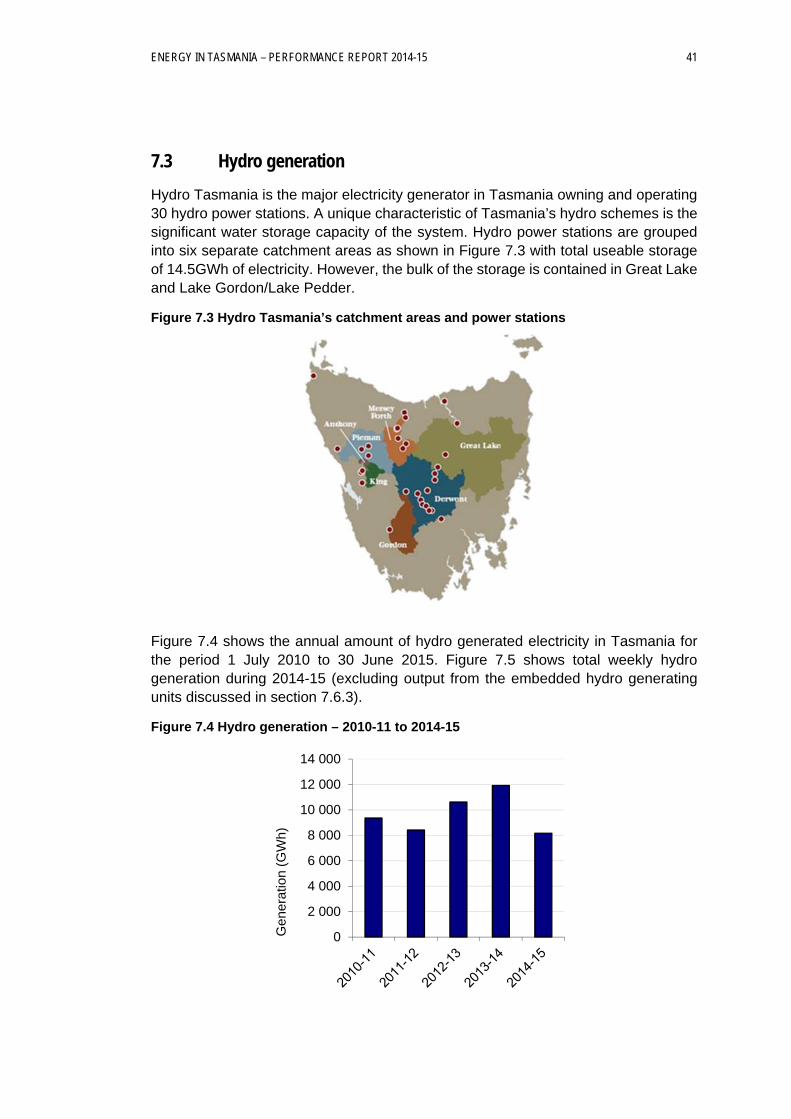

7.2 Reserve plant margin ................................................................ 40

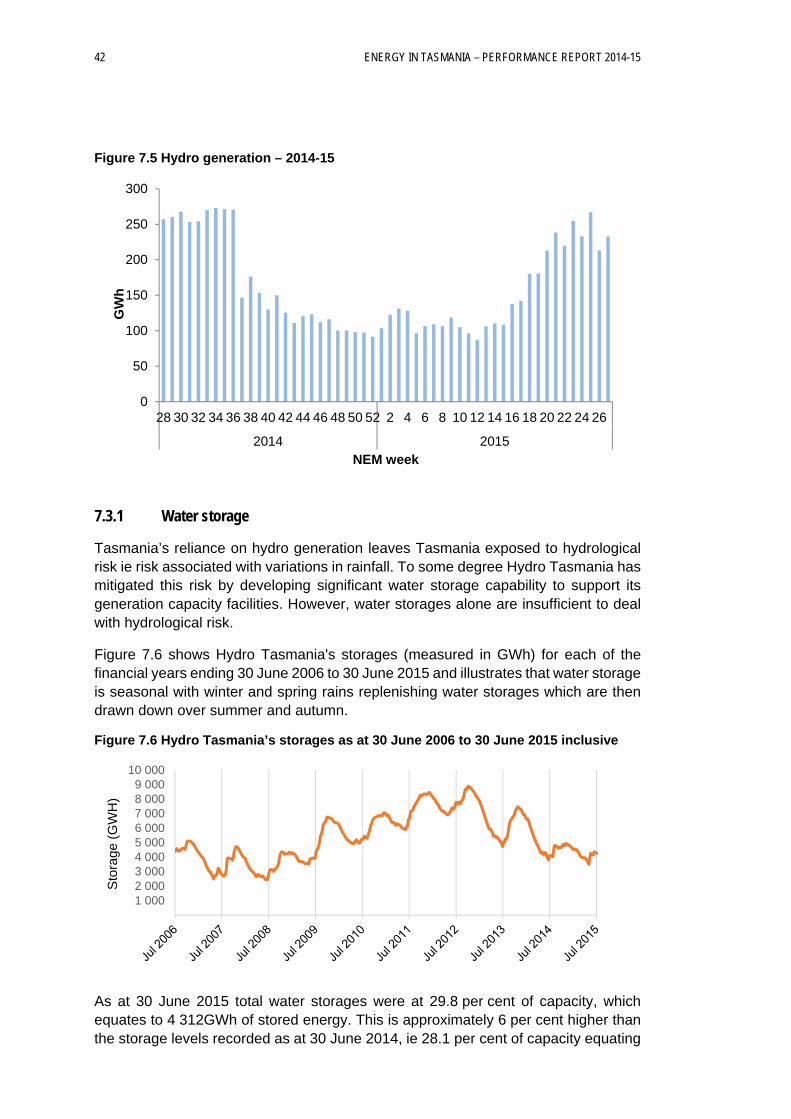

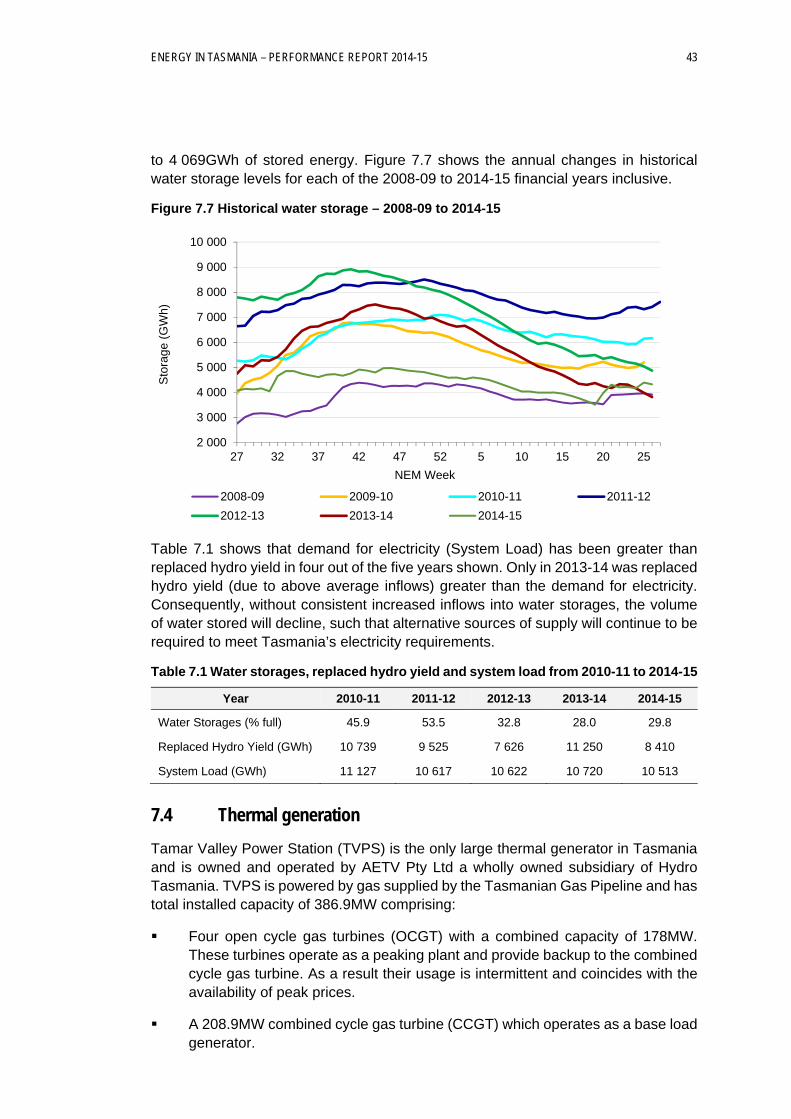

7.3 Hydro generation ...................................................................... 41

7.3.1 Water storage ......................................................................... 42

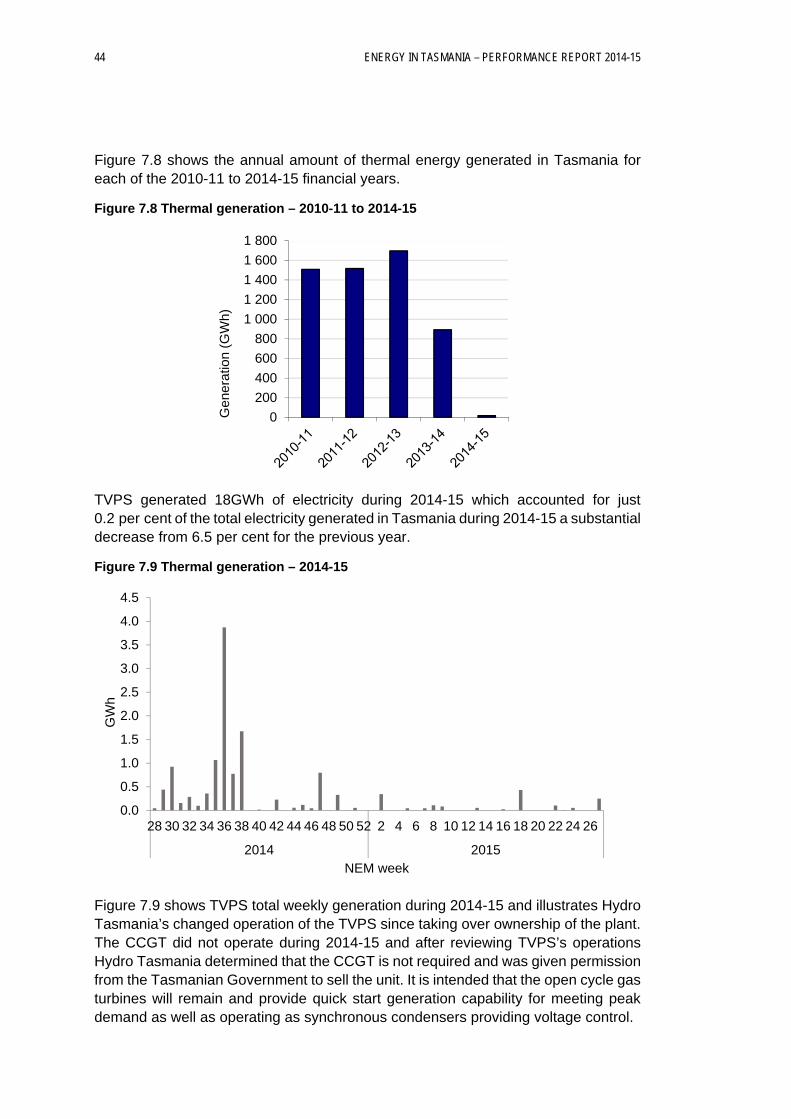

7.4 Thermal generation ................................................................... 43

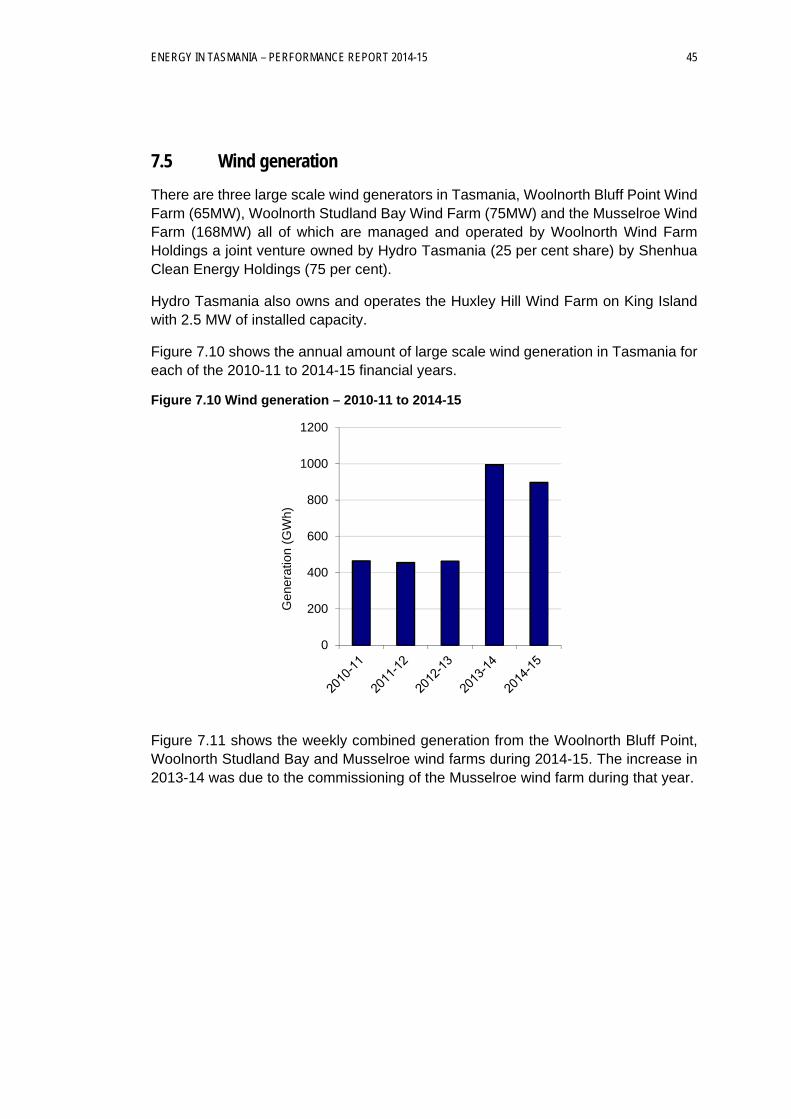

7.5 Wind generation ........................................................................ 45

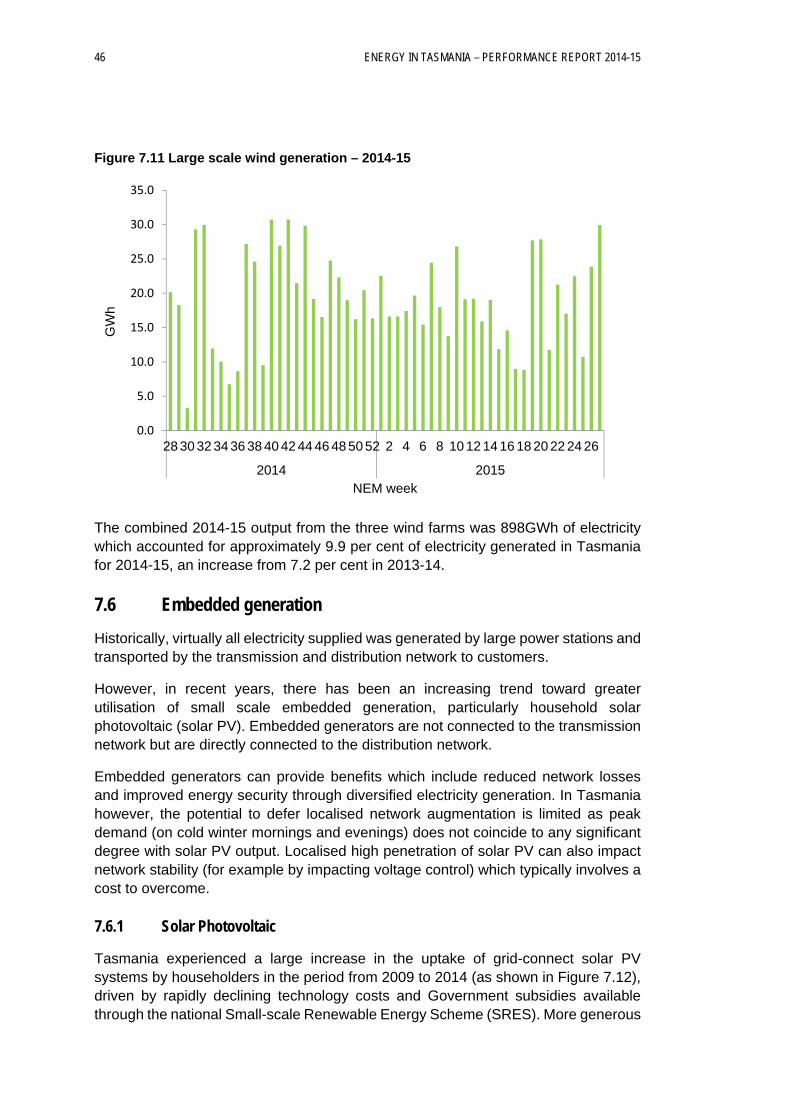

7.6 Embedded generation ............................................................... 46

7.6.1 Solar Photovoltaic ................................................................... 46

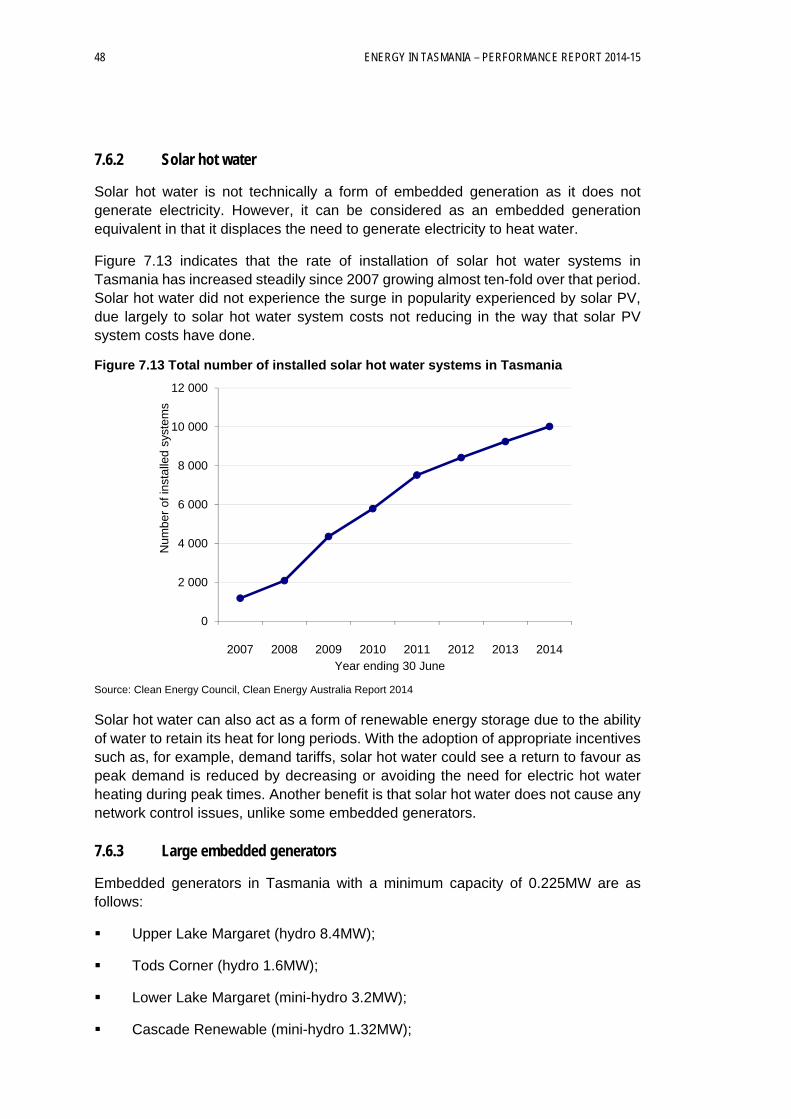

7.6.2 Solar hot water ........................................................................ 48

7.6.3 Large embedded generators .................................................. 48

7.7 Generation performance ........................................................... 49

7.7.1 Availability ............................................................................... 49

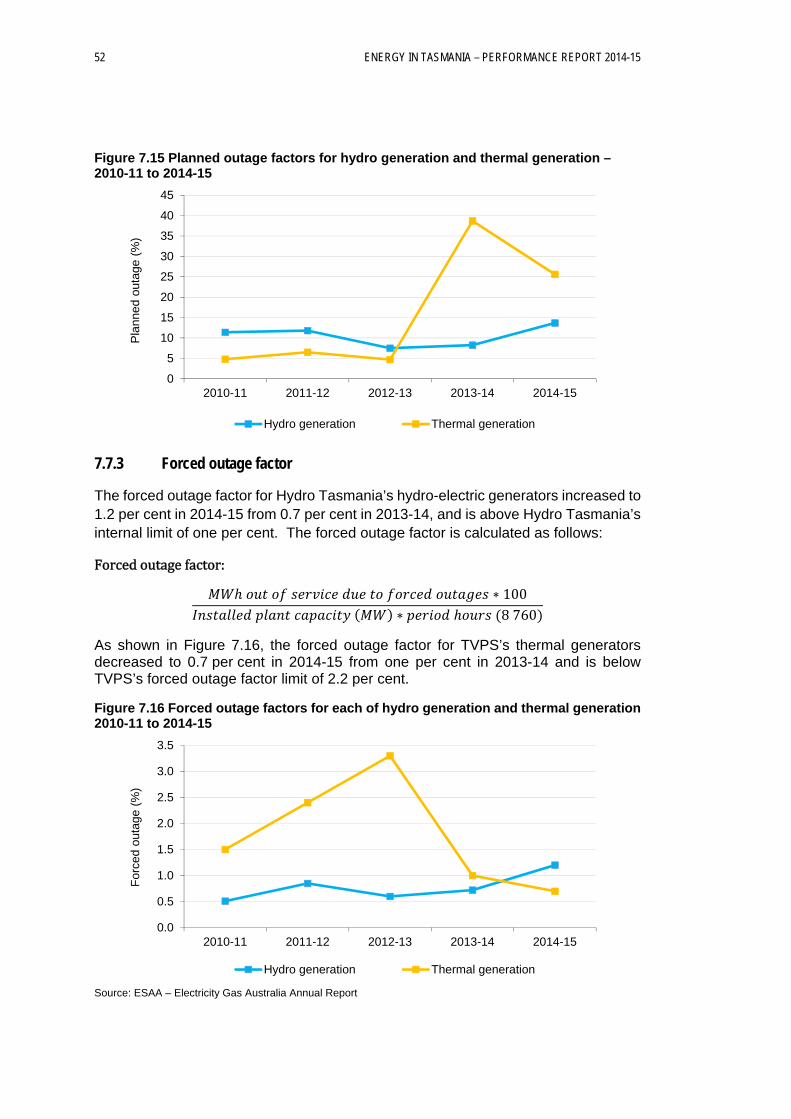

7.7.2 Planned outage factor............................................................. 51

7.7.3 Forced outage factor............................................................... 52

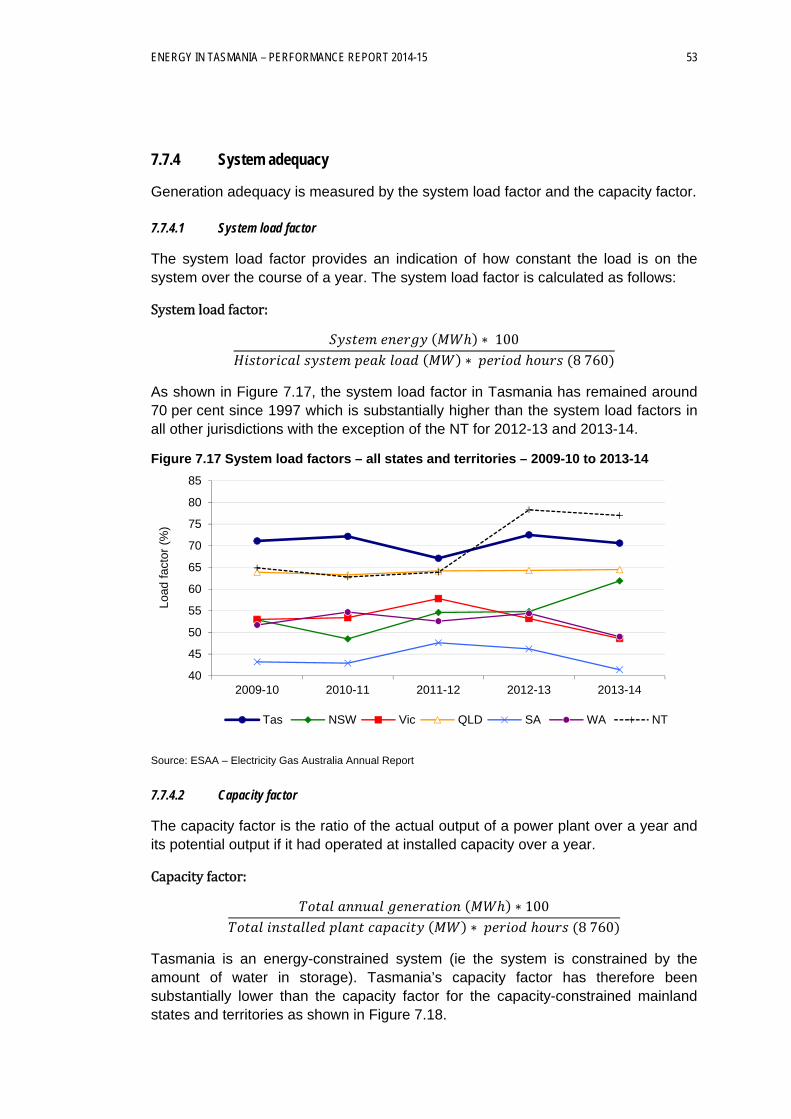

7.7.4 System adequacy ................................................................... 53

7.7.5 Basslink imports ...................................................................... 54

8 TRANSMISSION ........................................................................................... 57

8.1 Introduction ............................................................................... 57

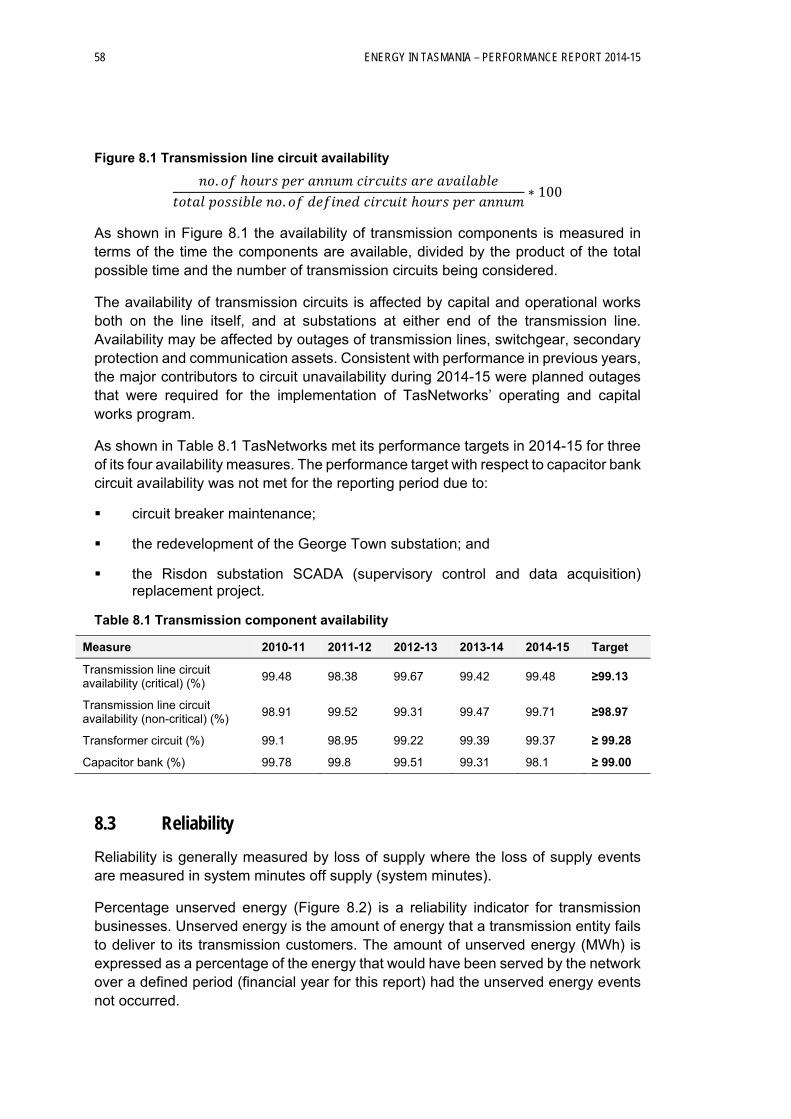

8.2 Availability ................................................................................. 57

ENERGY IN TASMANIA - PERFORMANCE REPORT 2014-15

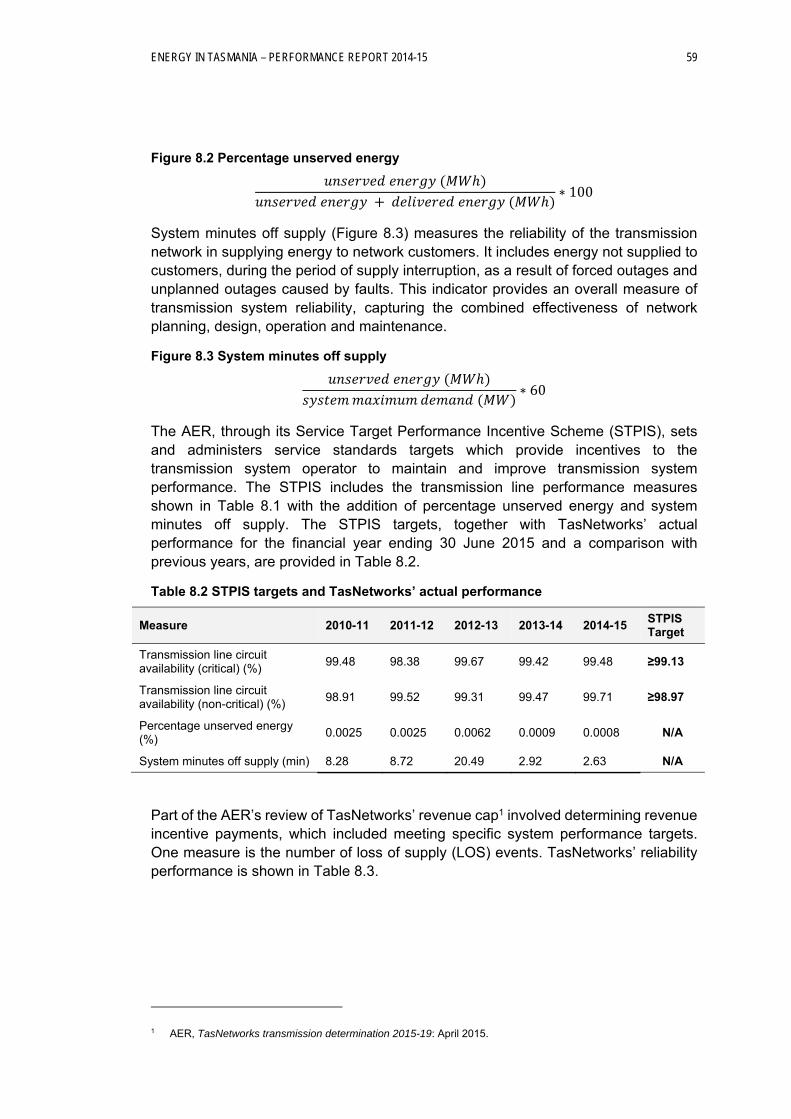

8.3 Reliability ................................................................................... 58

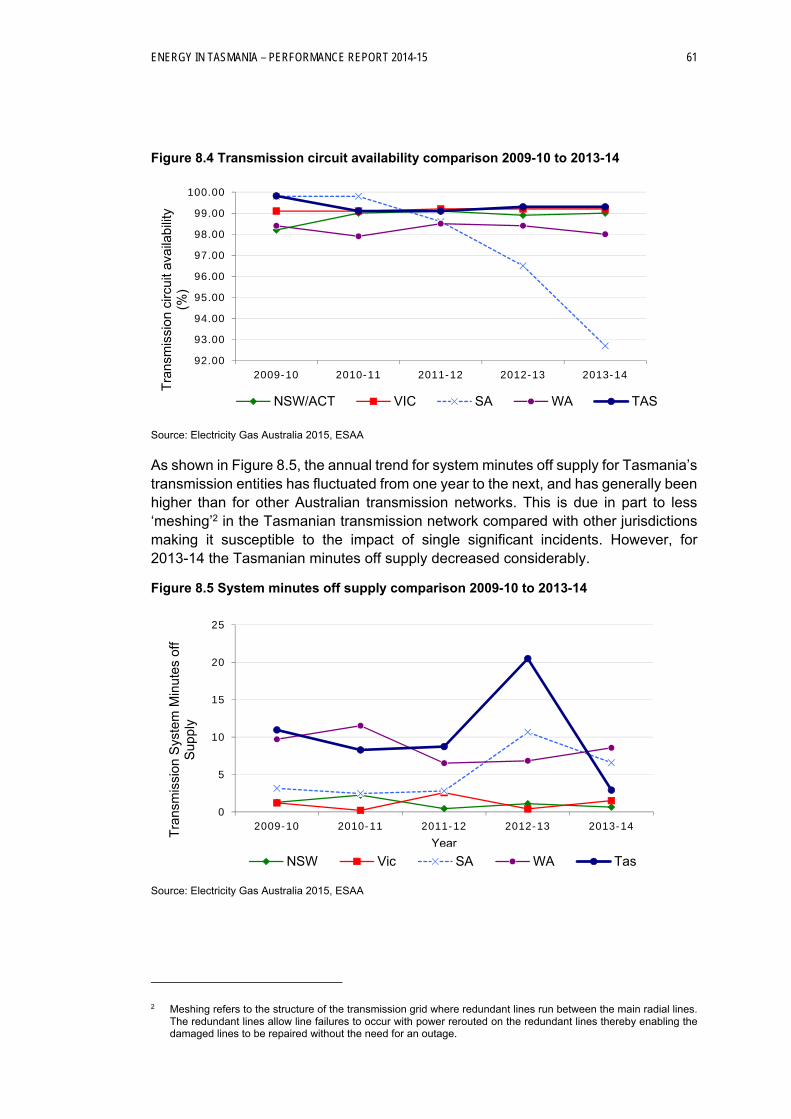

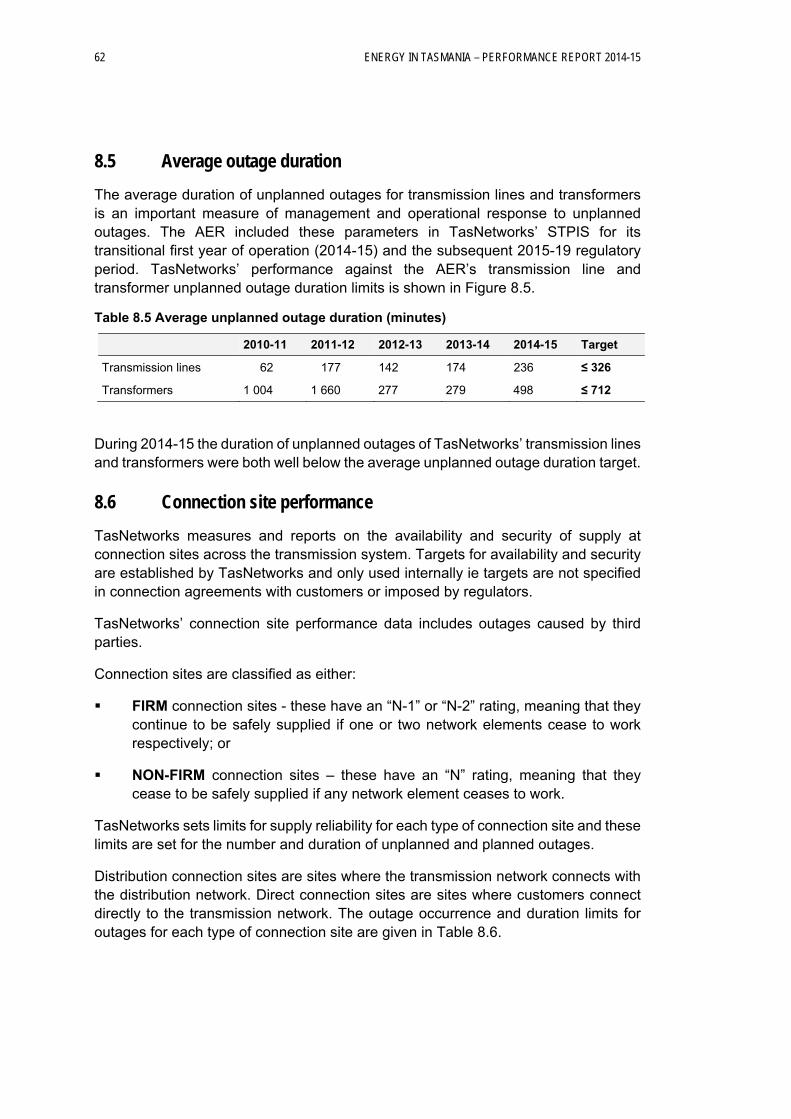

8.4 Comparison with other jurisdictions .......................................... 60

8.5 Average outage duration ........................................................... 62

8.6 Connection site performance .................................................... 62

8.6.1 Unplanned outages ................................................................. 63

8.6.2 Planned outages ..................................................................... 63

8.7 Connection site security for firm connection points ................... 63

8.8 Constraints ................................................................................ 64

8.8.1 Transmission system constraints ........................................... 64

8.8.2 Transmission network capacity constraints ............................ 65

8.8.3 Terminal substation capacity constraints................................ 65

8.9 System losses ........................................................................... 65

8.9.1 Energy losses in the NEM ...................................................... 65

8.10 Transmission security and planning criteria .............................. 66

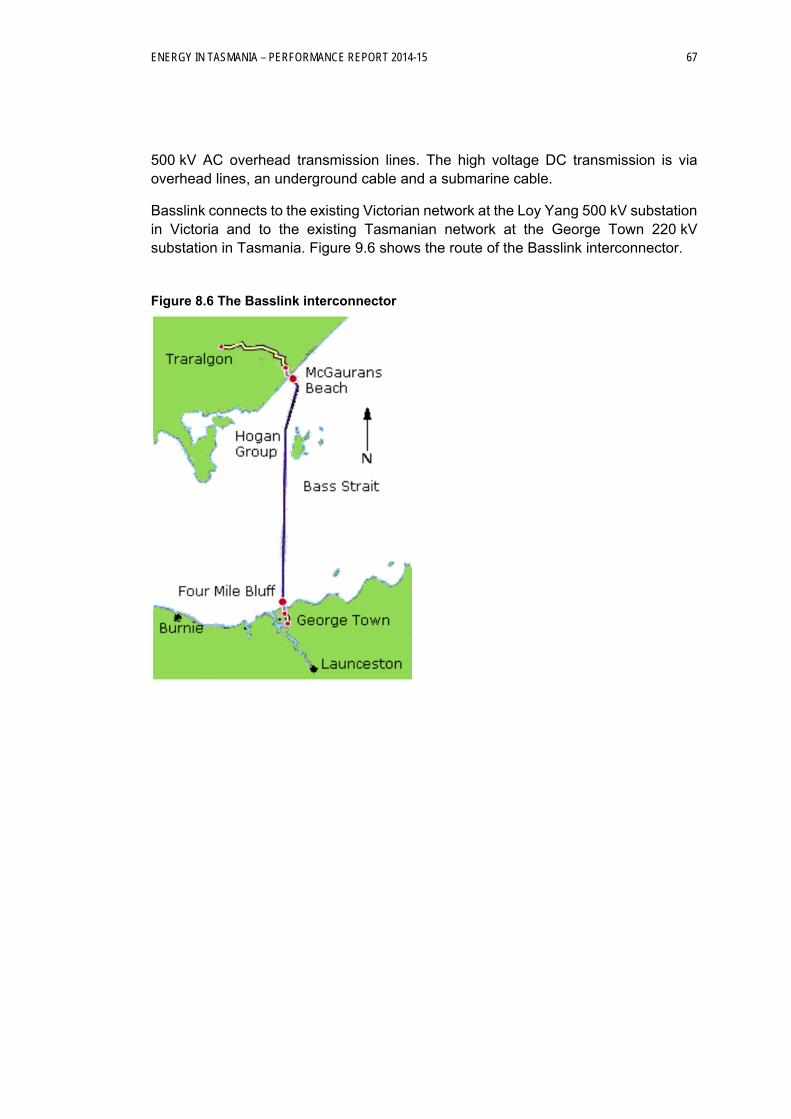

8.11 Basslink Interconnector ............................................................. 66

8.11.1 Basslink operation .................................................................. 68

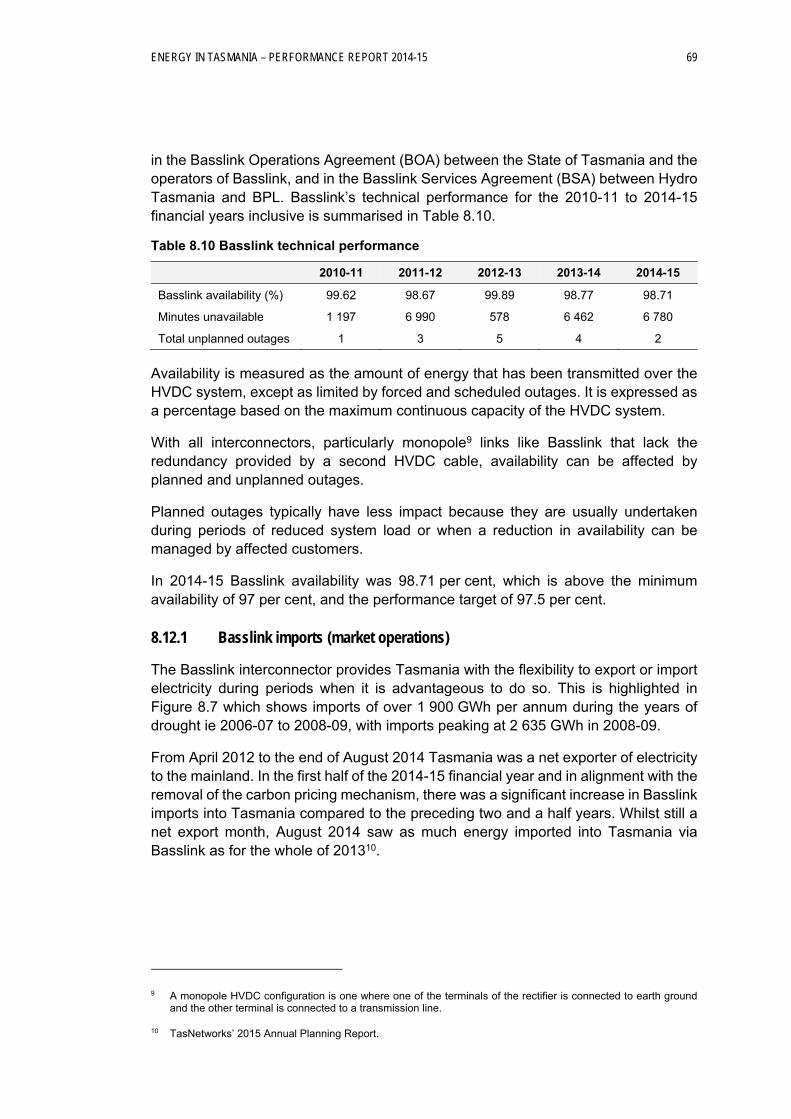

8.12 Basslink technical performance ................................................ 68

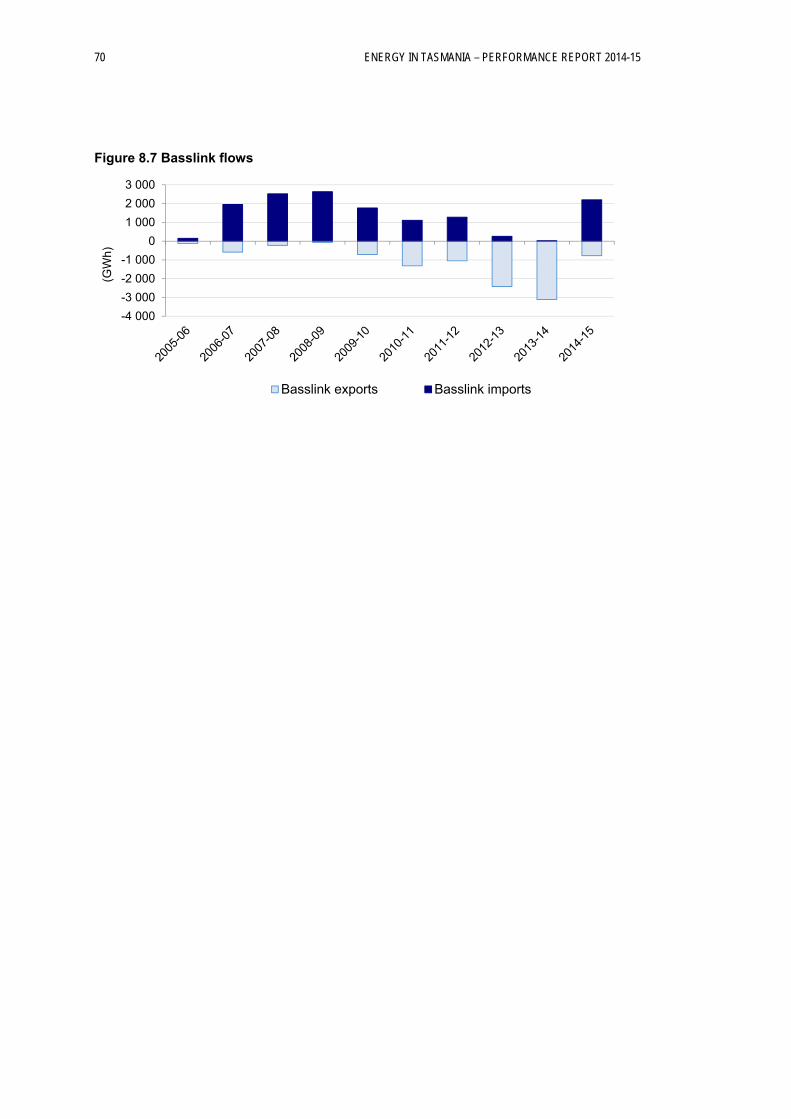

8.12.1 Basslink imports (market operations) ..................................... 69

9 ELECTRICITY DISTRIBUTION .................................................................... 71

9.1 Introduction ............................................................................... 71

9.2 The distribution network ............................................................ 71

9.3 Performance measures ............................................................. 72

9.3.1 SAIDI ...................................................................................... 72

9.3.2 SAIFI ....................................................................................... 72

9.3.3 CAIDI ...................................................................................... 73

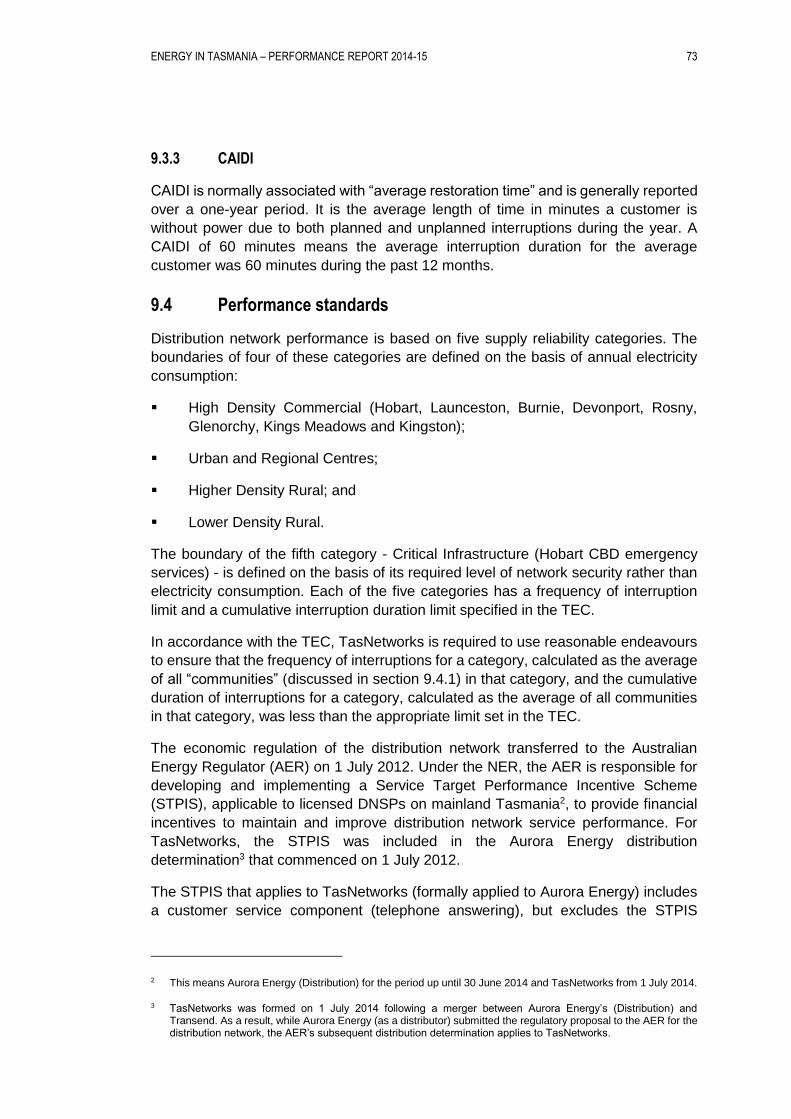

9.4 Performance standards ............................................................. 73

9.4.1 Communities ........................................................................... 74

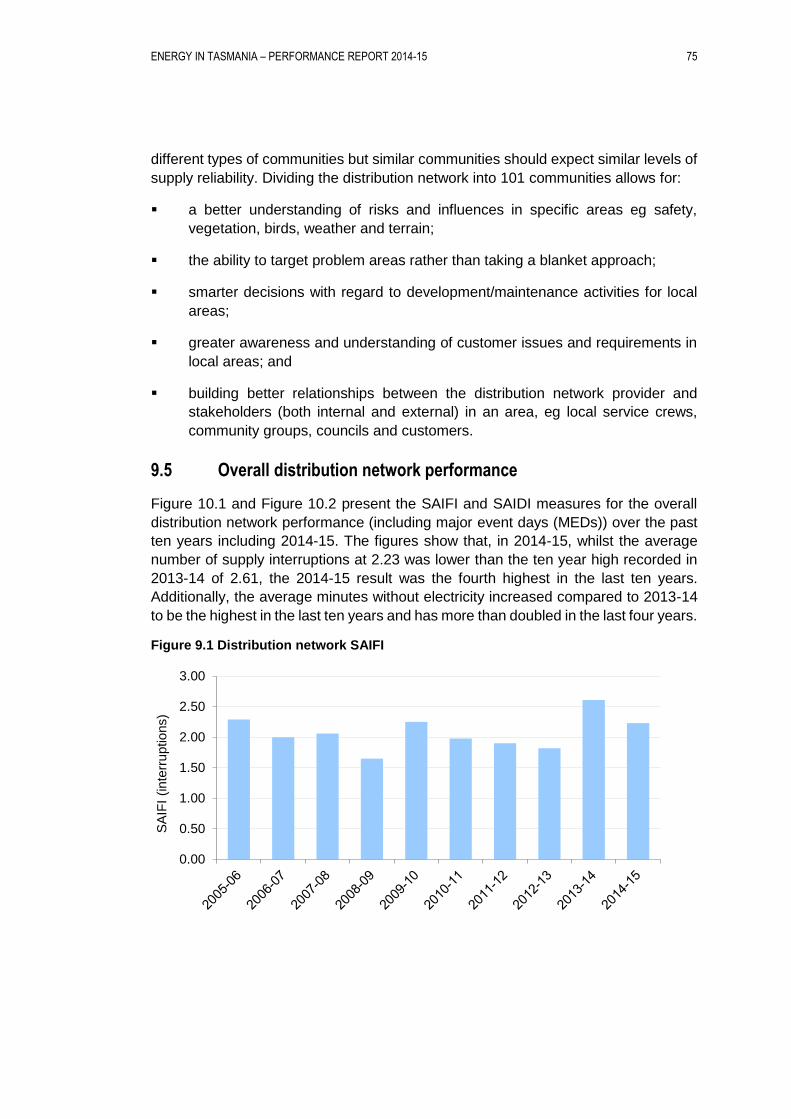

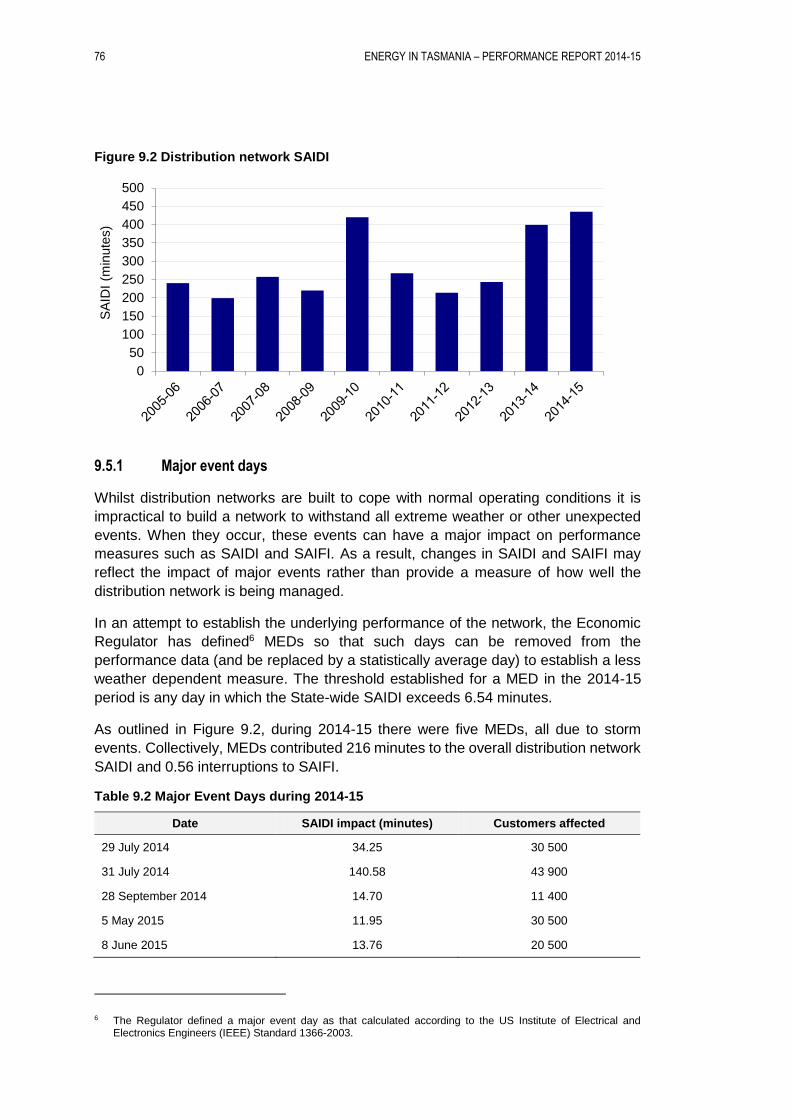

9.5 Overall distribution network performance ................................. 75

9.5.1 Major event days .................................................................... 76

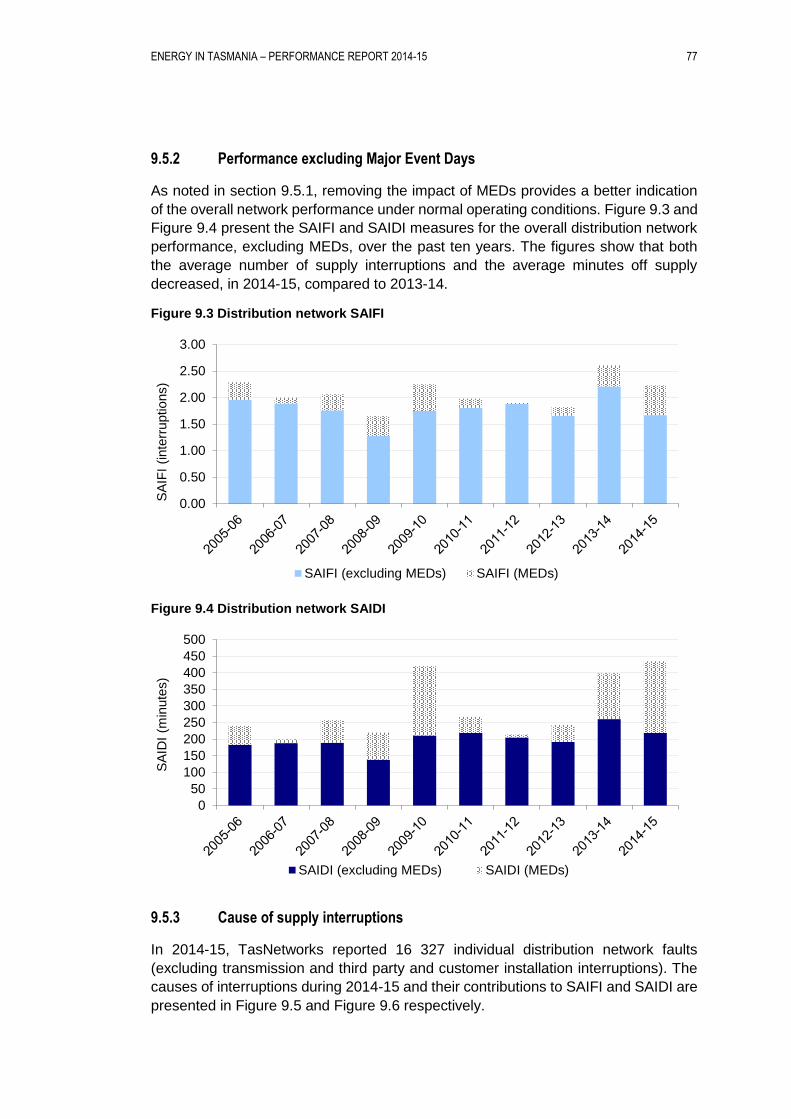

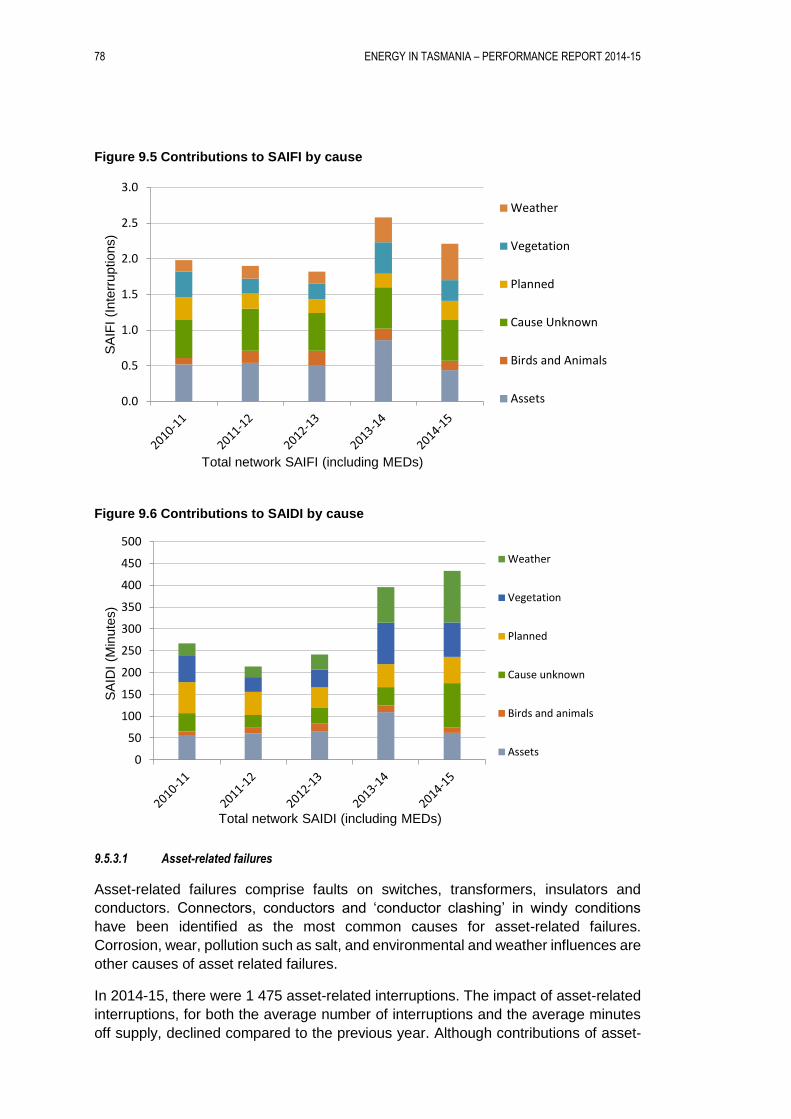

9.5.2 Performance excluding Major Event Days ............................. 77

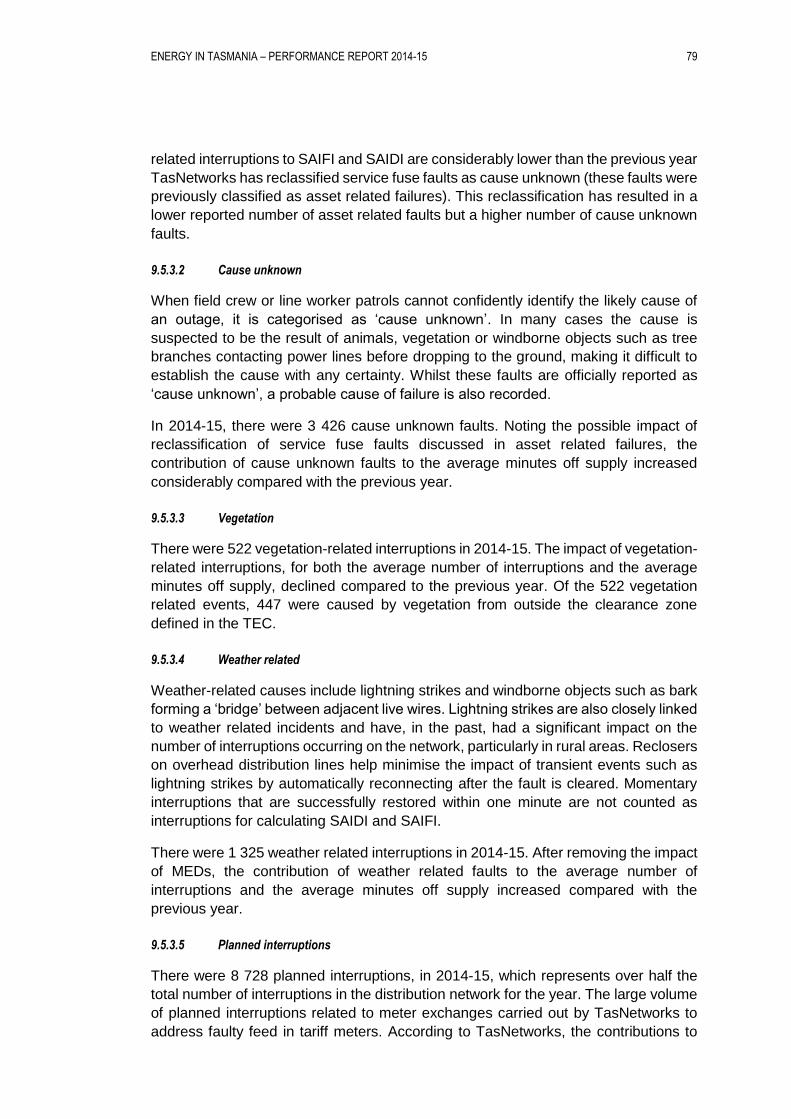

9.5.3 Cause of supply interruptions ................................................. 77

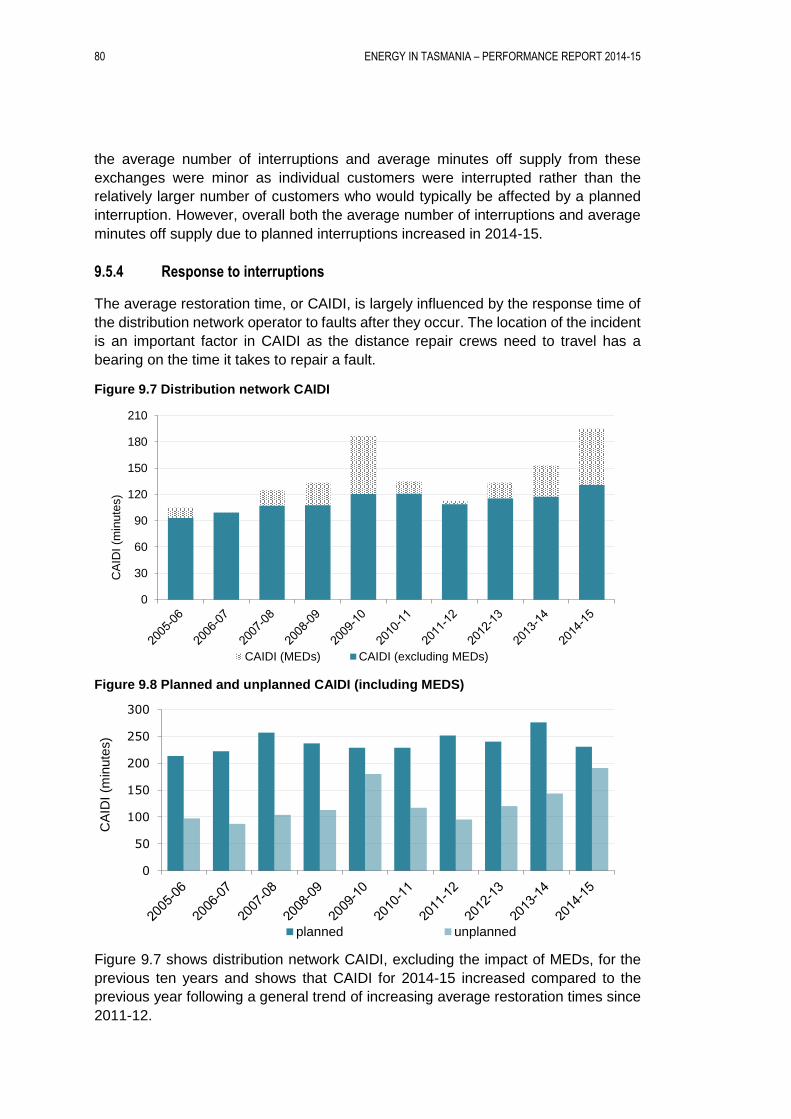

9.5.4 Response to interruptions ....................................................... 80

9.6 Distribution network performance for TEC community categories ................................................................................. 81

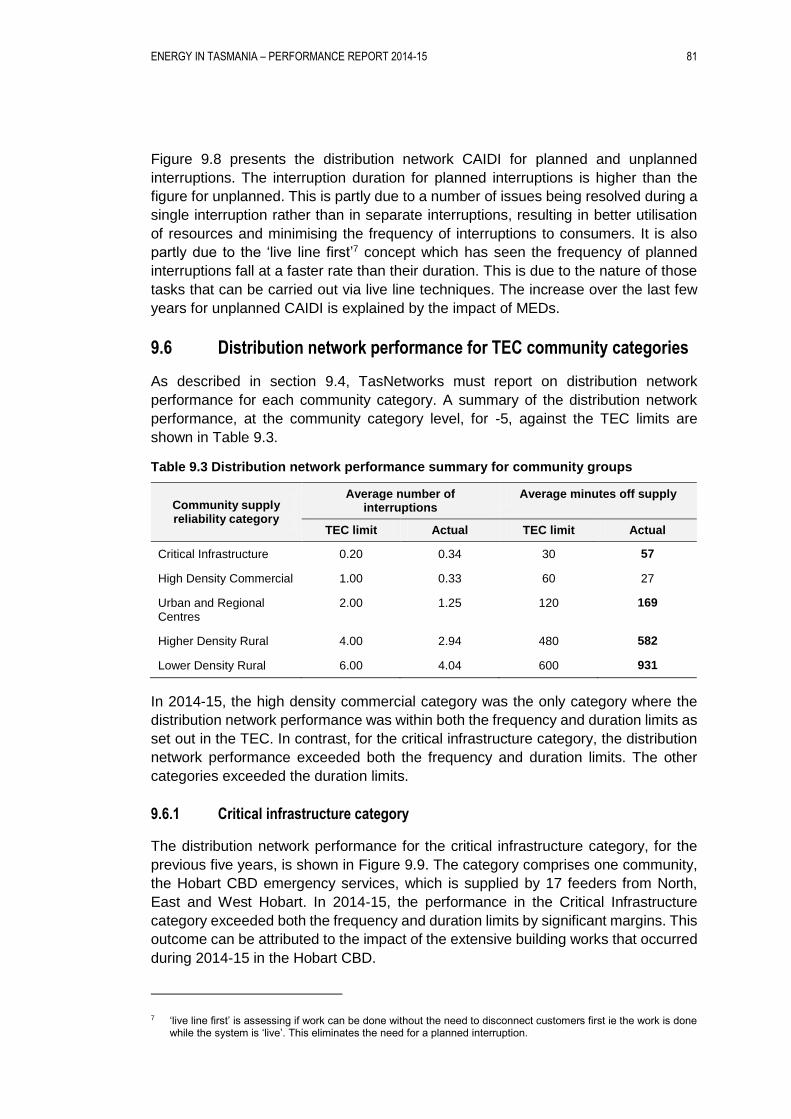

9.6.1 Critical infrastructure category ................................................ 81

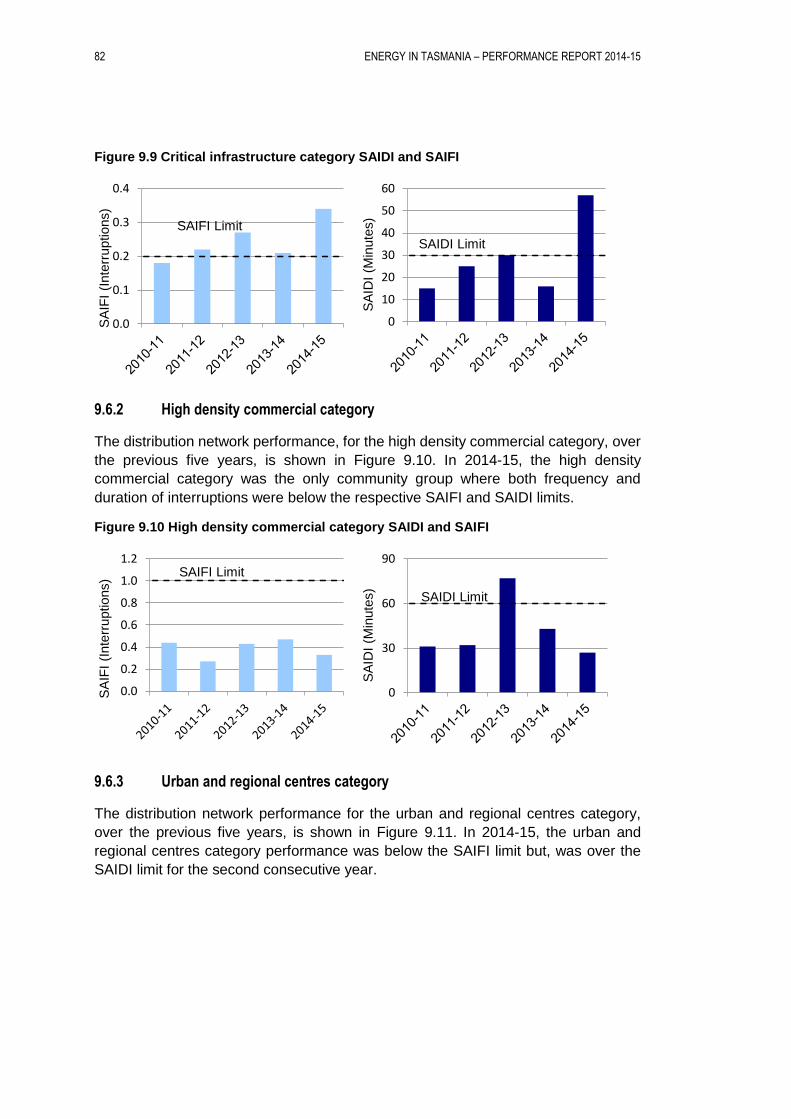

9.6.2 High density commercial category .......................................... 82

9.6.3 Urban and regional centres category ..................................... 82

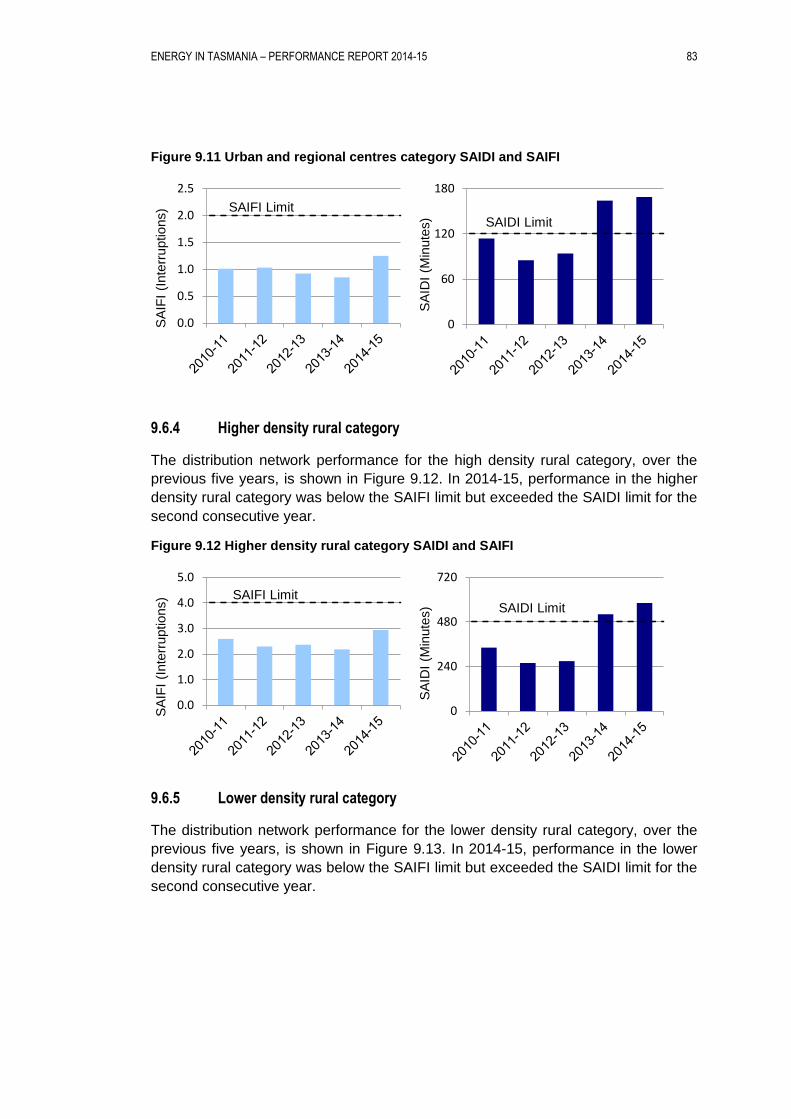

9.6.4 Higher density rural category .................................................. 83

ENERGY IN TASMANIA - PERFORMANCE REPORT 2014-15

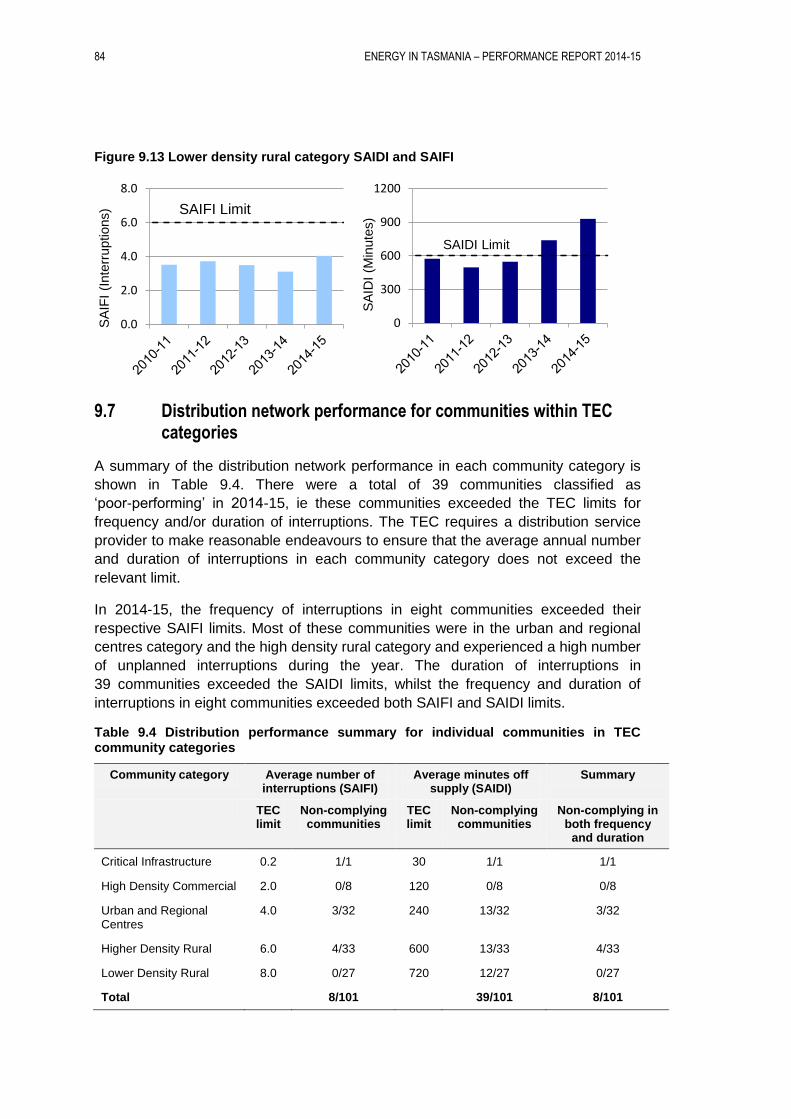

9.6.5 Lower density rural category .................................................. 83

9.7 Distribution network performance for communities within TEC categories ................................................................................. 84

9.7.1 Critical infrastructure community SAIDI and SAIFI ................. 85

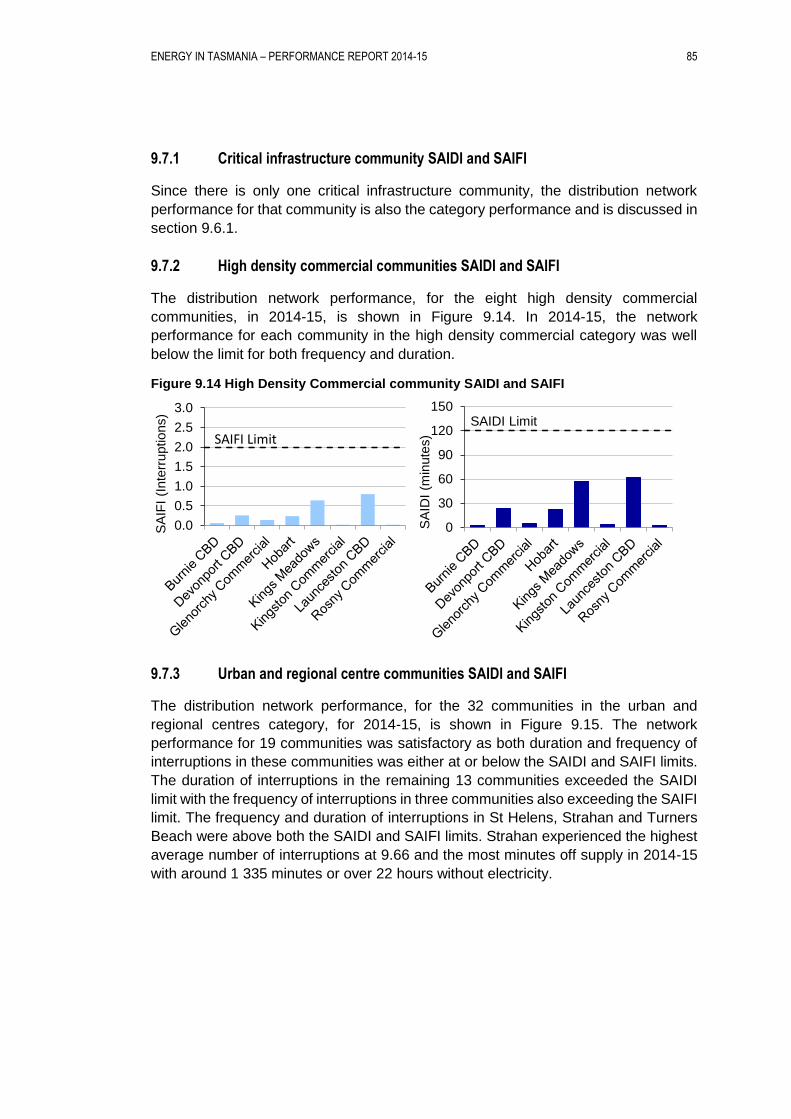

9.7.2 High density commercial communities SAIDI and SAIFI ........ 85

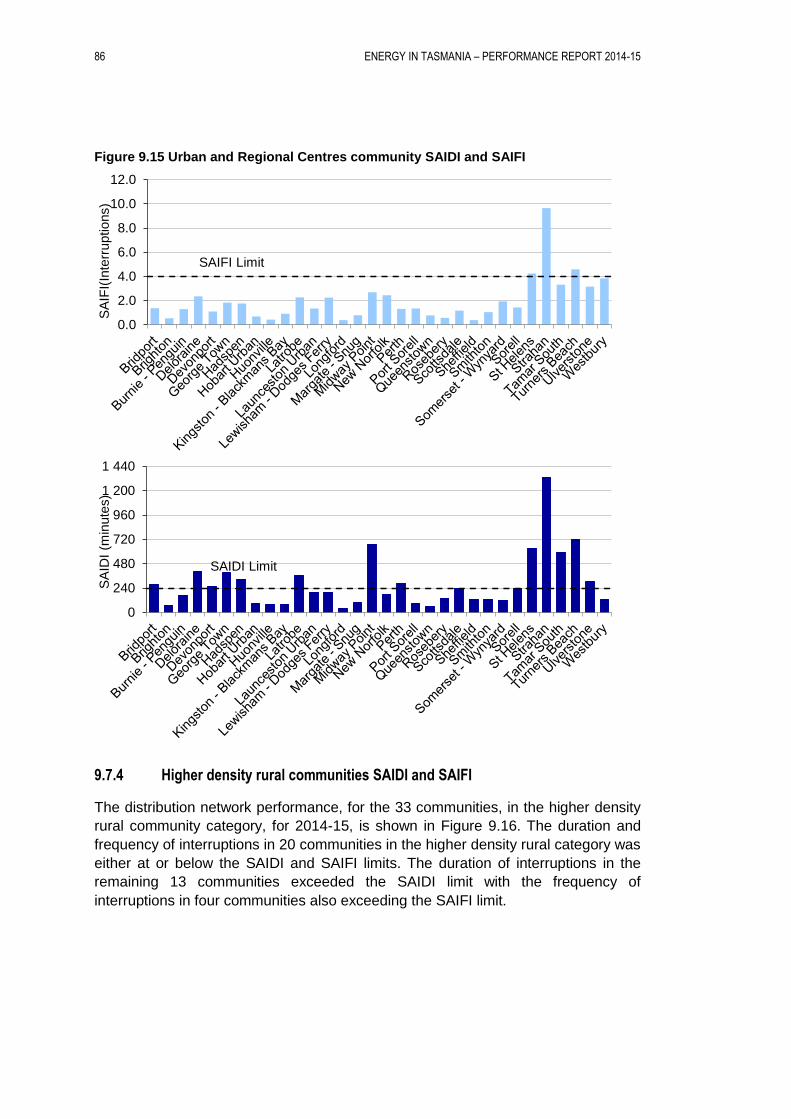

9.7.3 Urban and regional centre communities SAIDI and SAIFI ..... 85

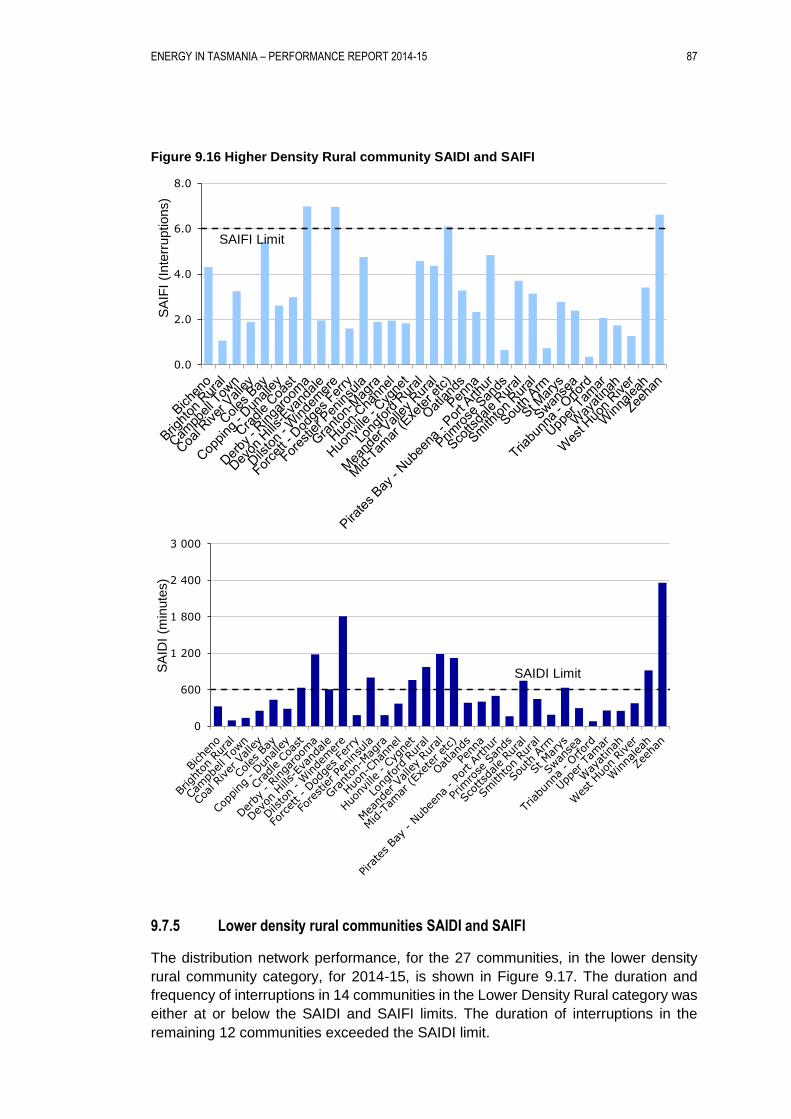

9.7.4 Higher density rural communities SAIDI and SAIFI ................ 86

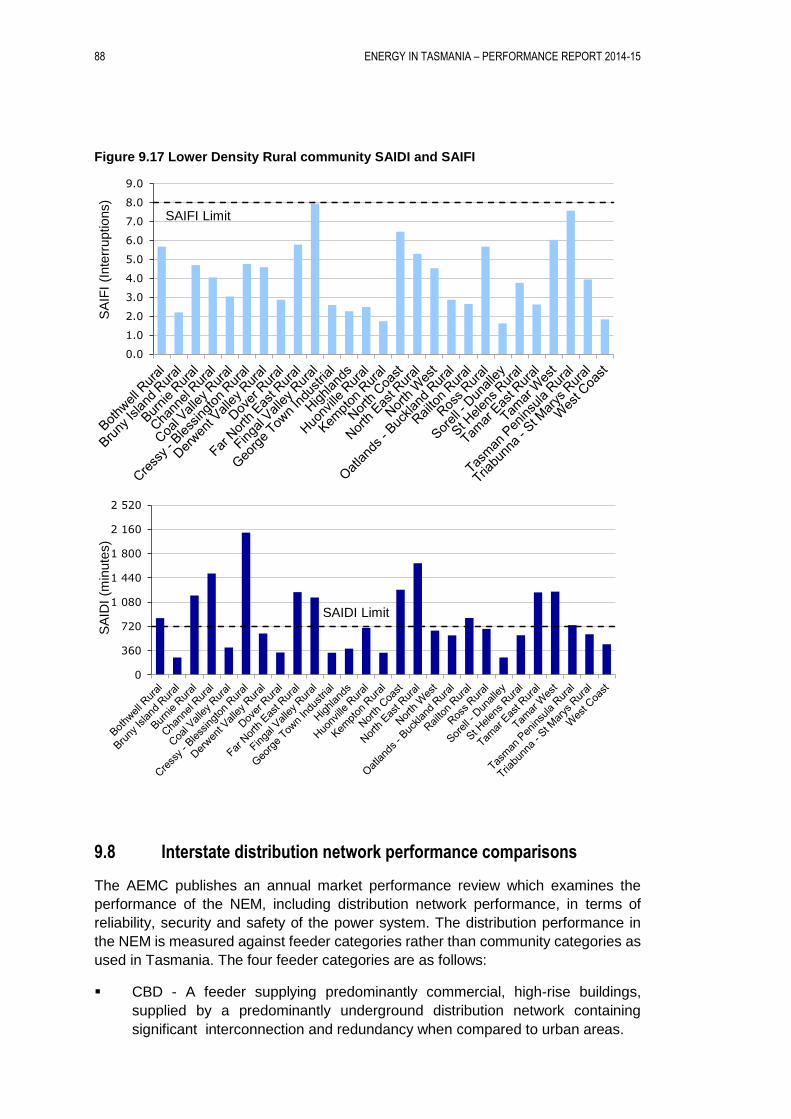

9.7.5 Lower density rural communities SAIDI and SAIFI ................ 87

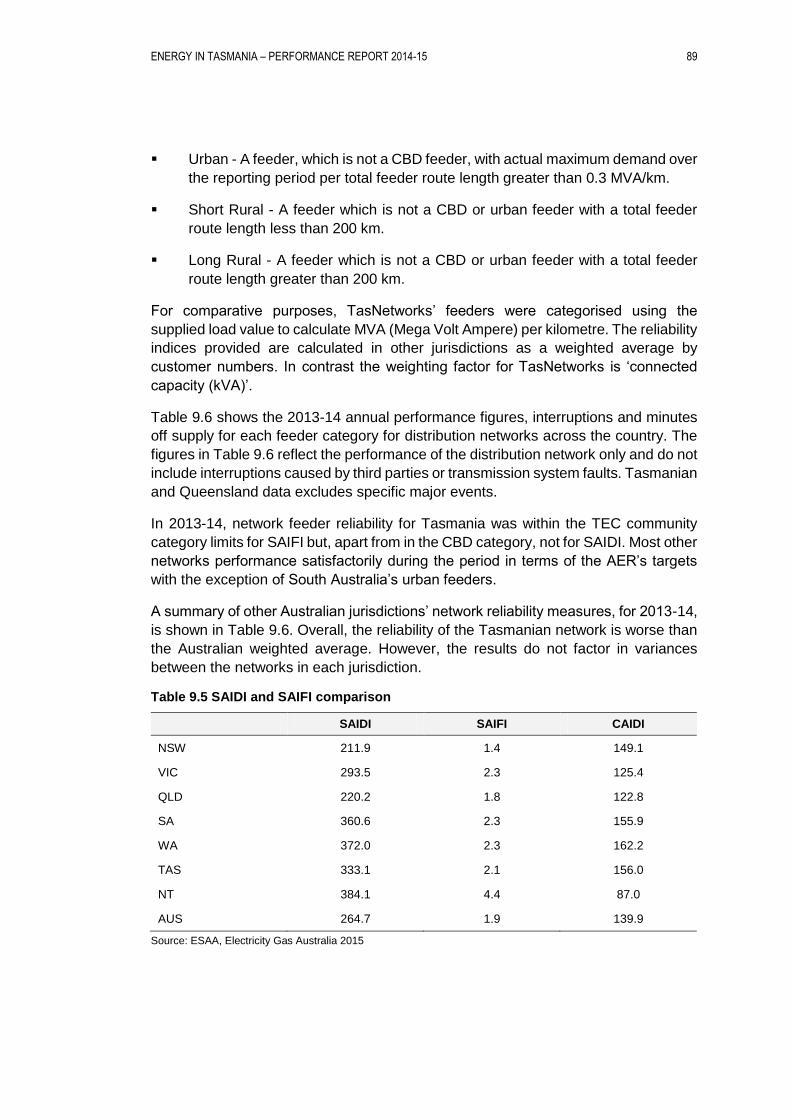

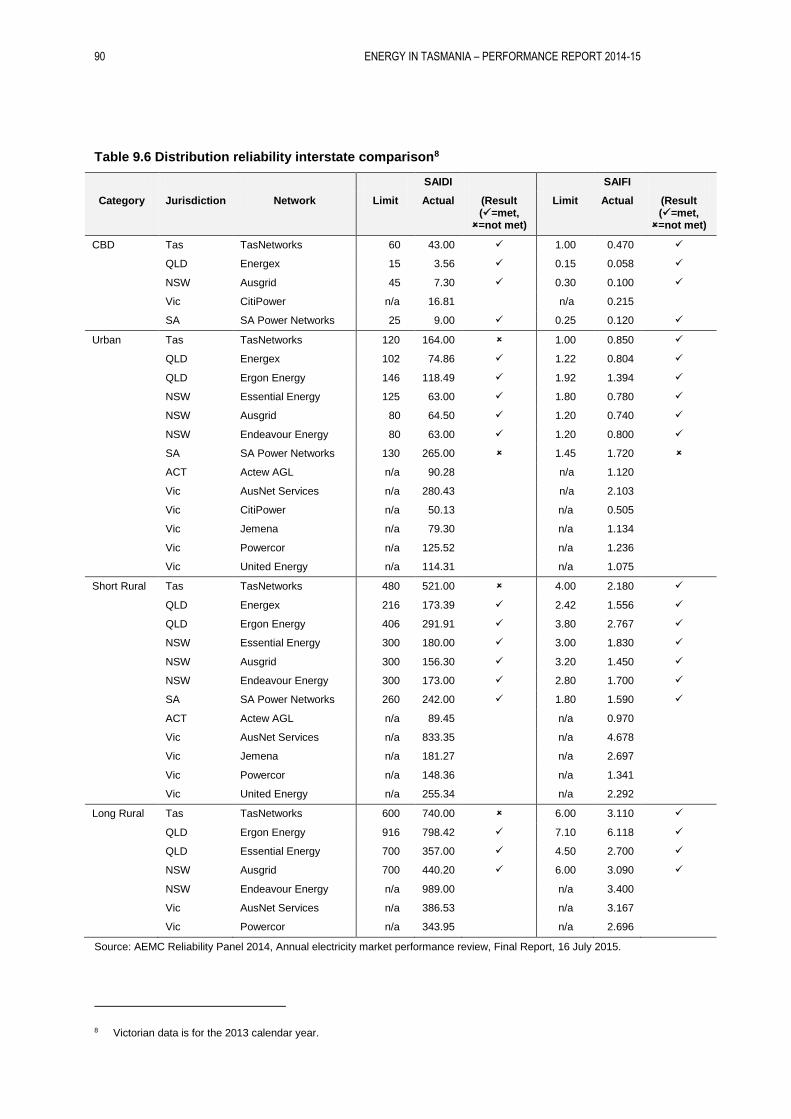

9.8 Interstate distribution network performance comparisons ........ 88

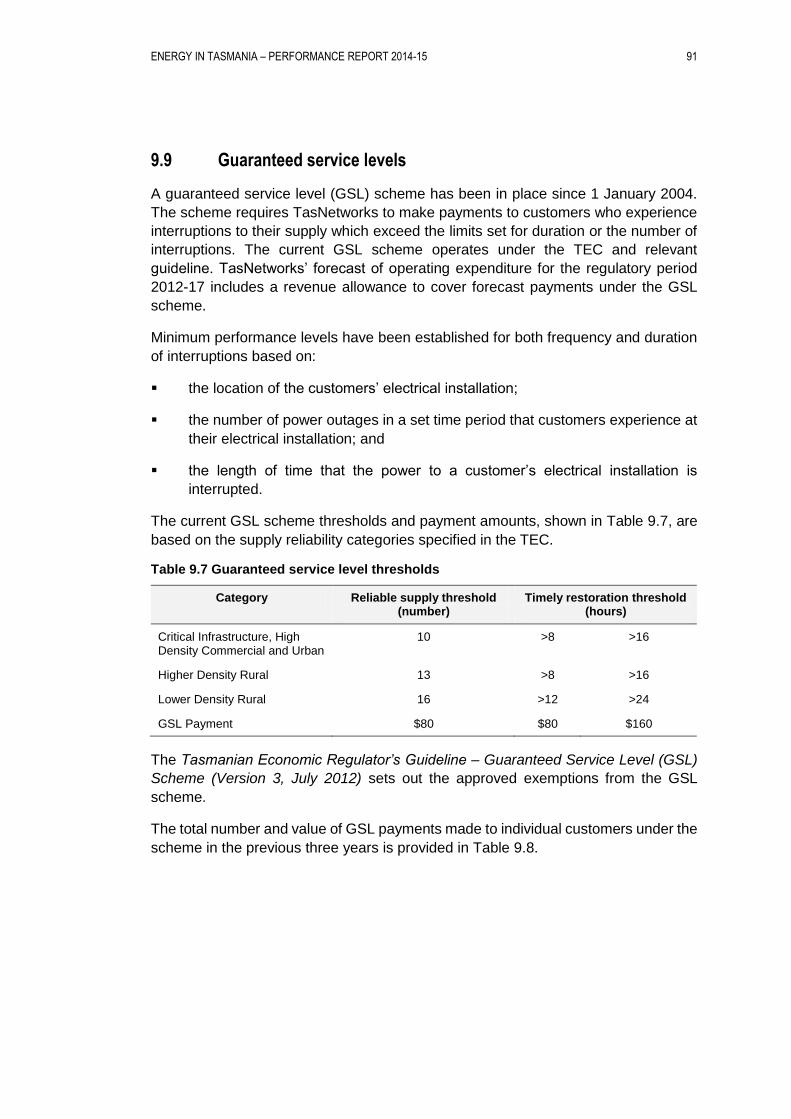

9.9 Guaranteed service levels ........................................................ 91

9.10 Reliability improvement ............................................................. 92

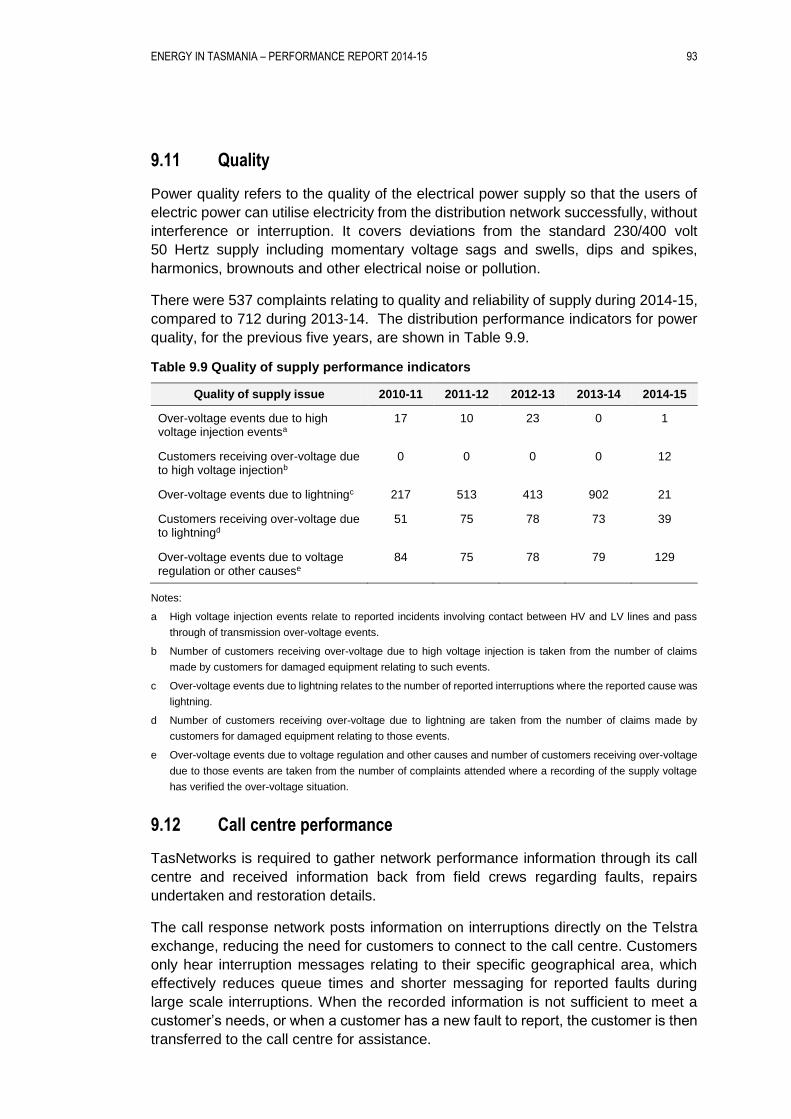

9.11 Quality ....................................................................................... 93

9.12 Call centre performance ............................................................ 93

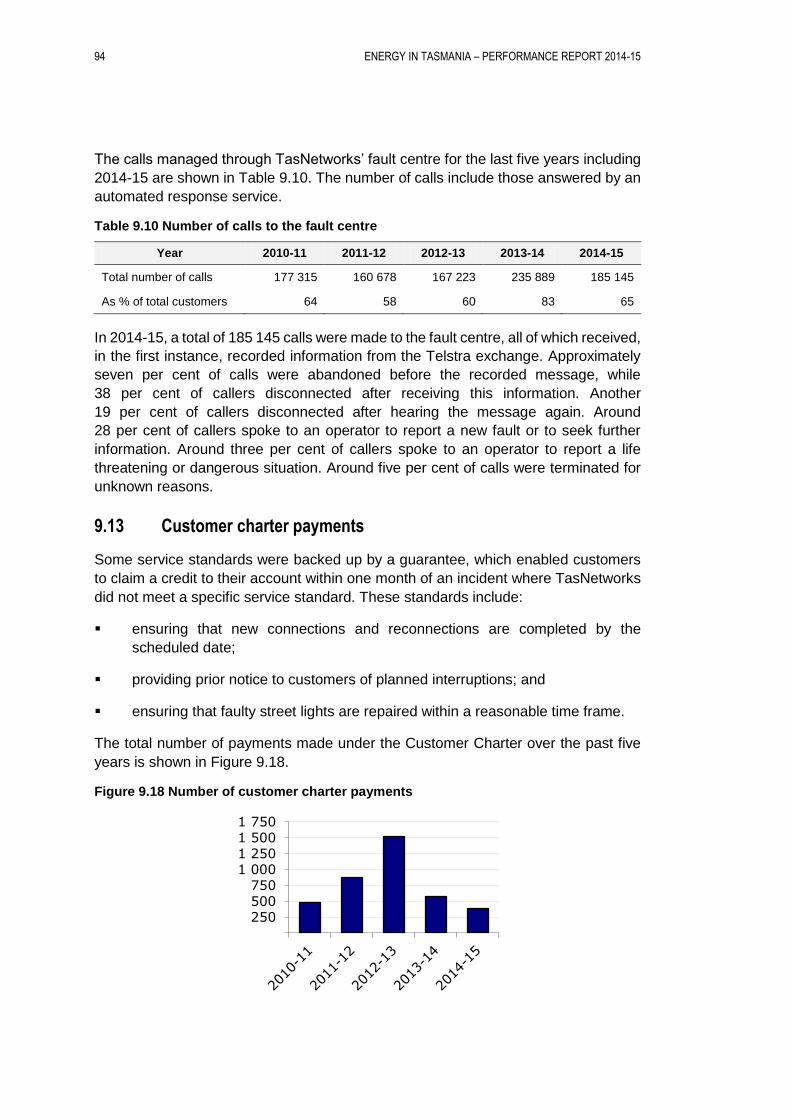

9.13 Customer charter payments ...................................................... 94

10 TASMANIAN ELECTRICITY MARKET ........................................................ 97

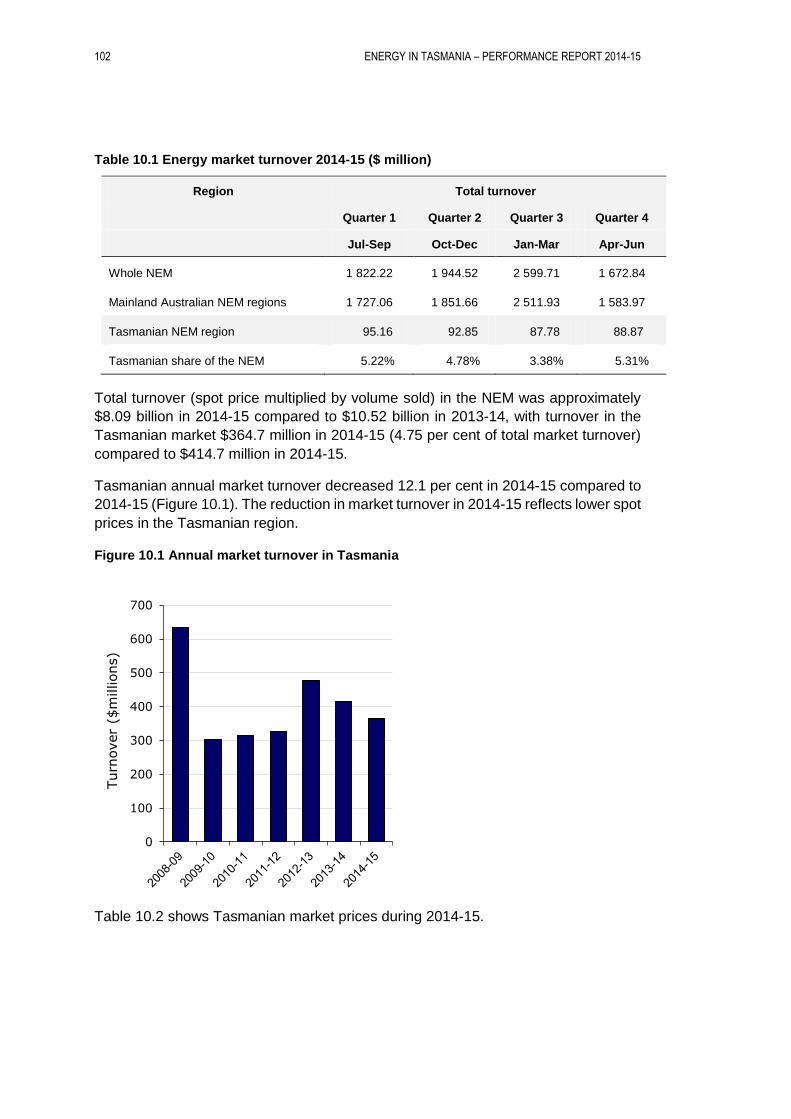

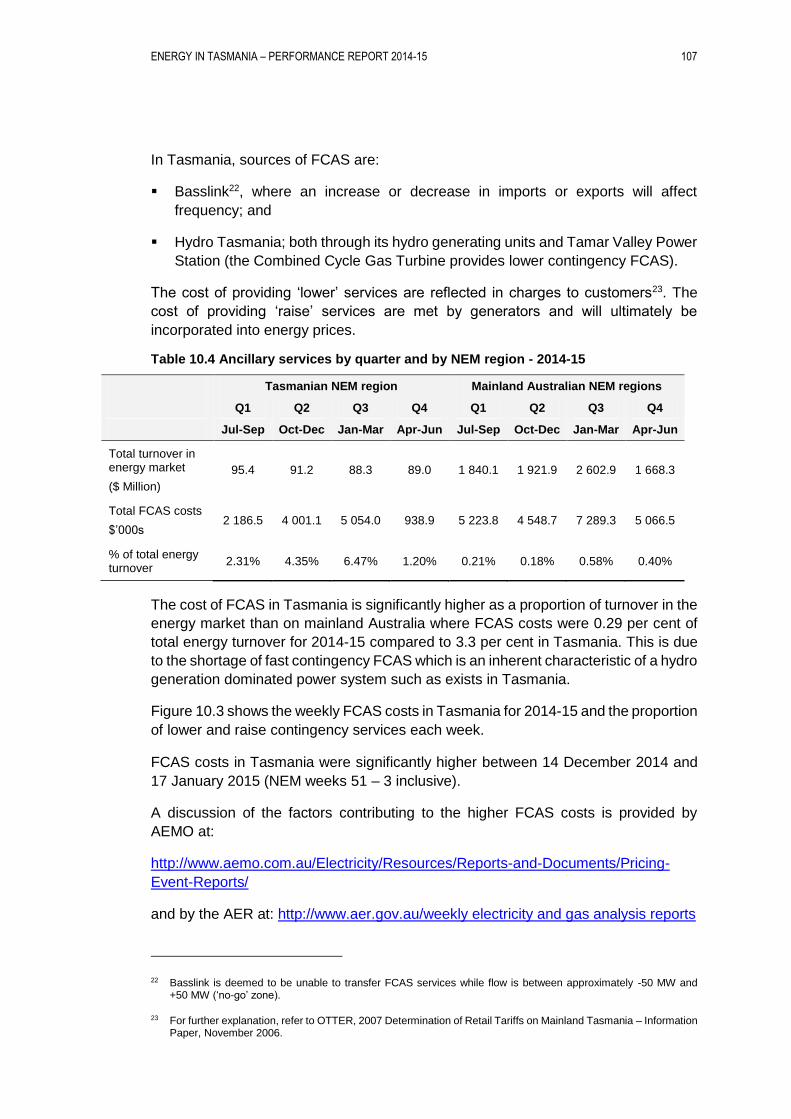

10.1 Wholesale market ................................................................... 97

10.1.1 The National Electricity Market ............................................... 97

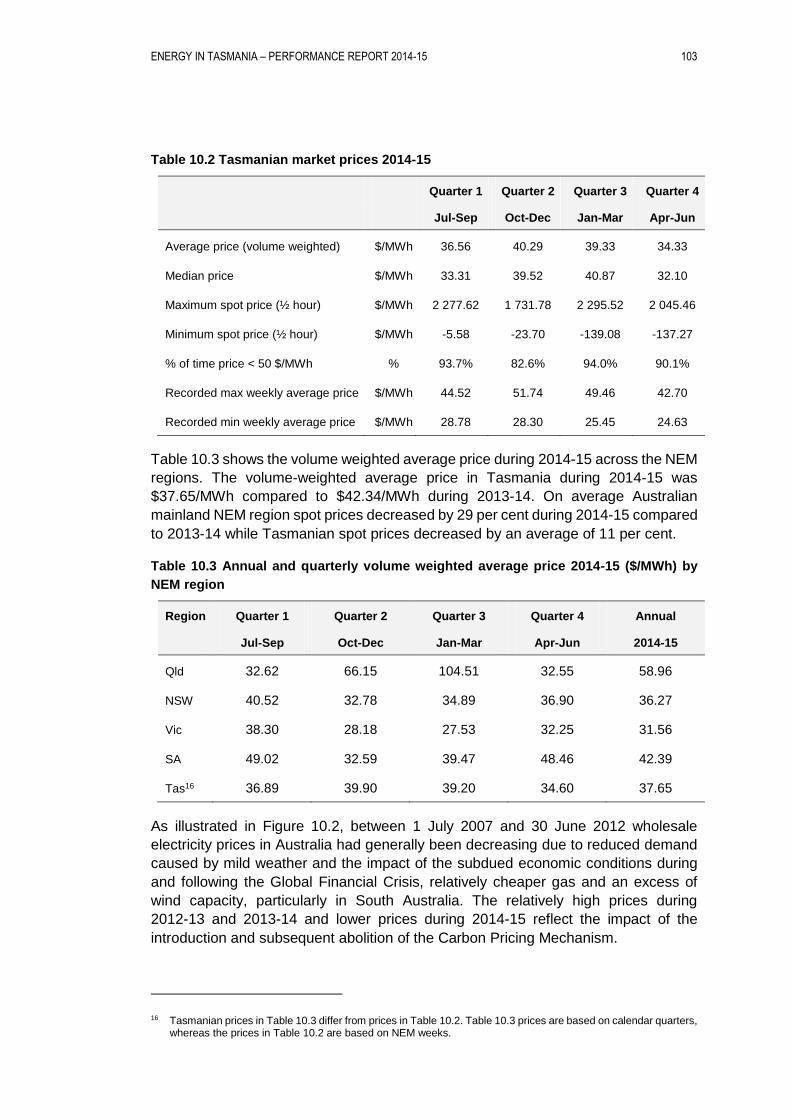

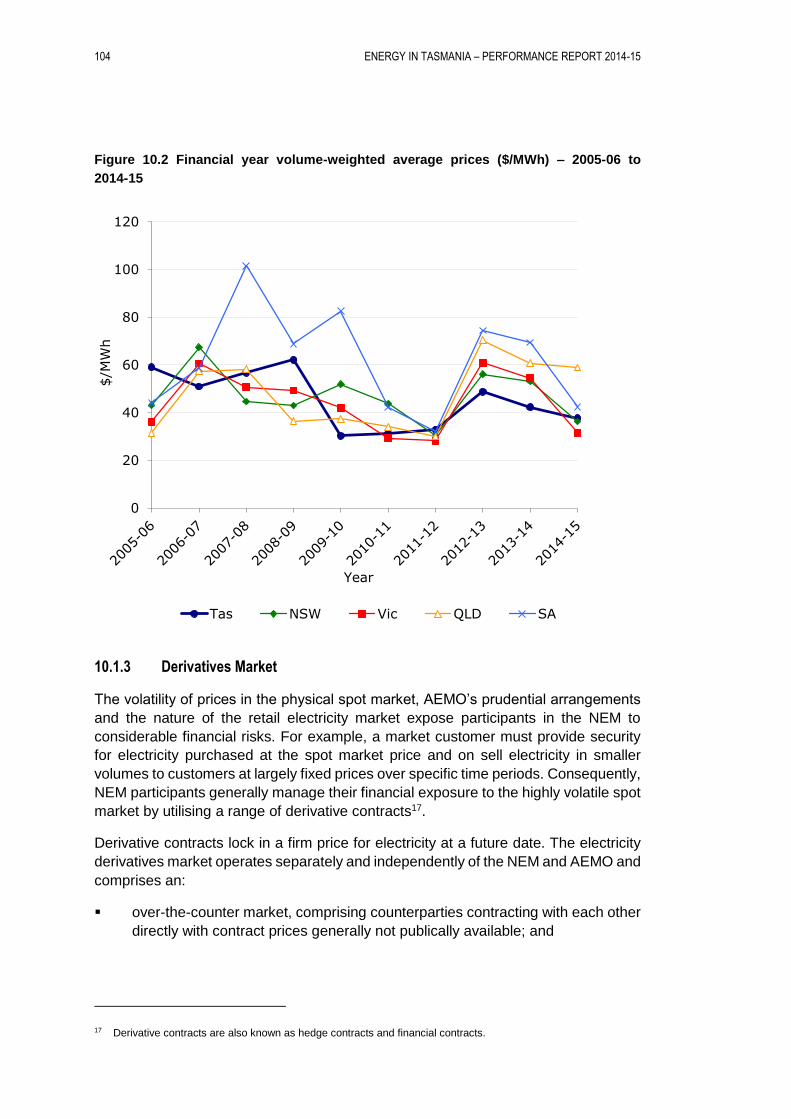

10.1.2 Spot market overview ........................................................... 101

10.1.3 Derivatives Market ................................................................ 104

10.1.4 Frequency control ancillary services .................................... 106

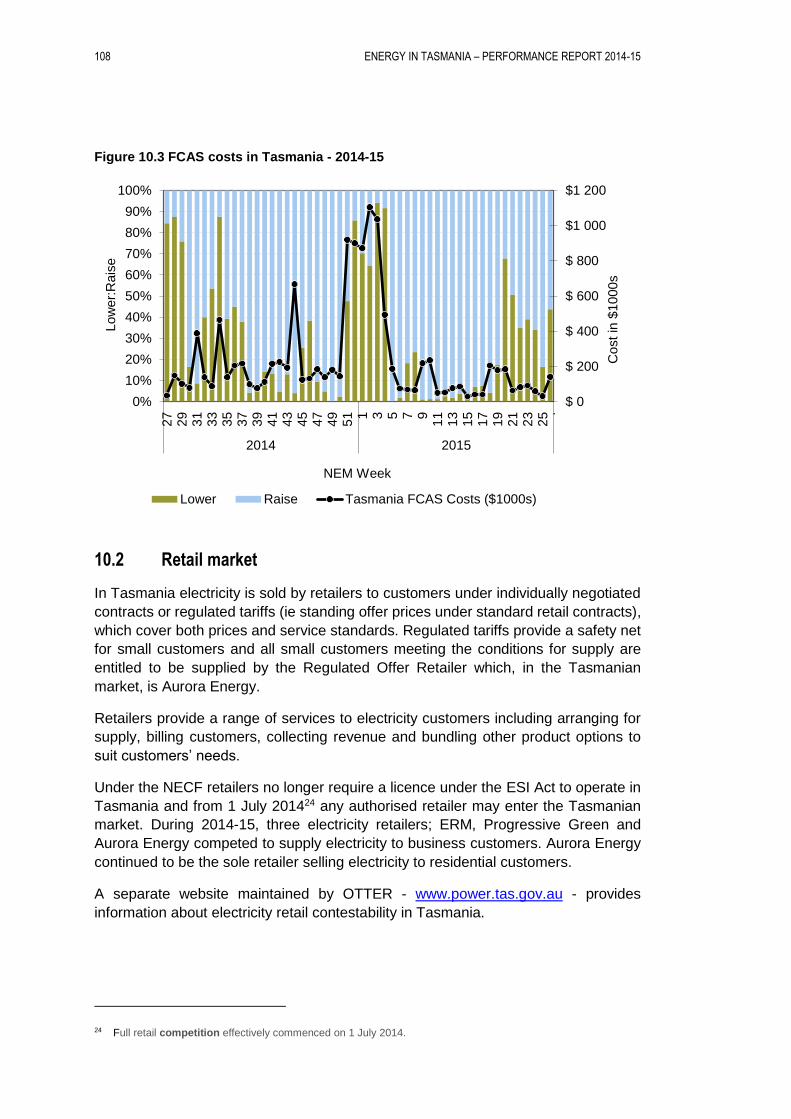

10.2 Retail market ........................................................................... 108

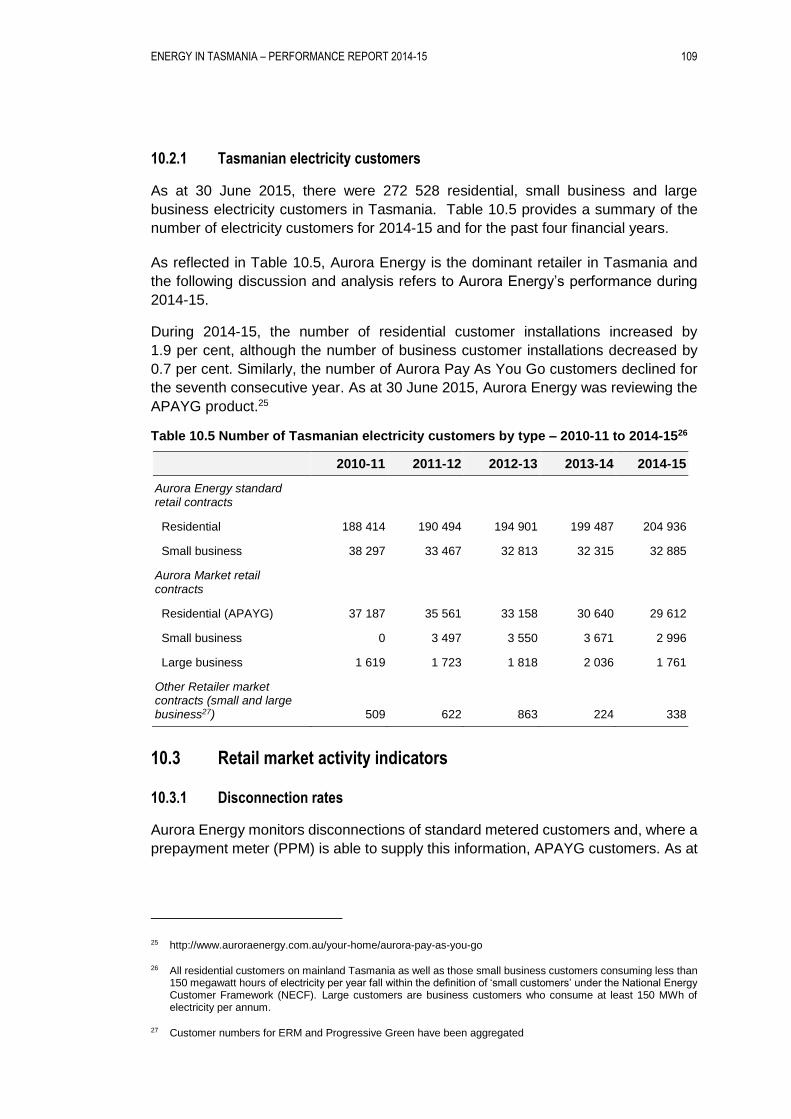

10.2.1 Tasmanian electricity customers .......................................... 109

10.3 Retail market activity indicators .............................................. 109

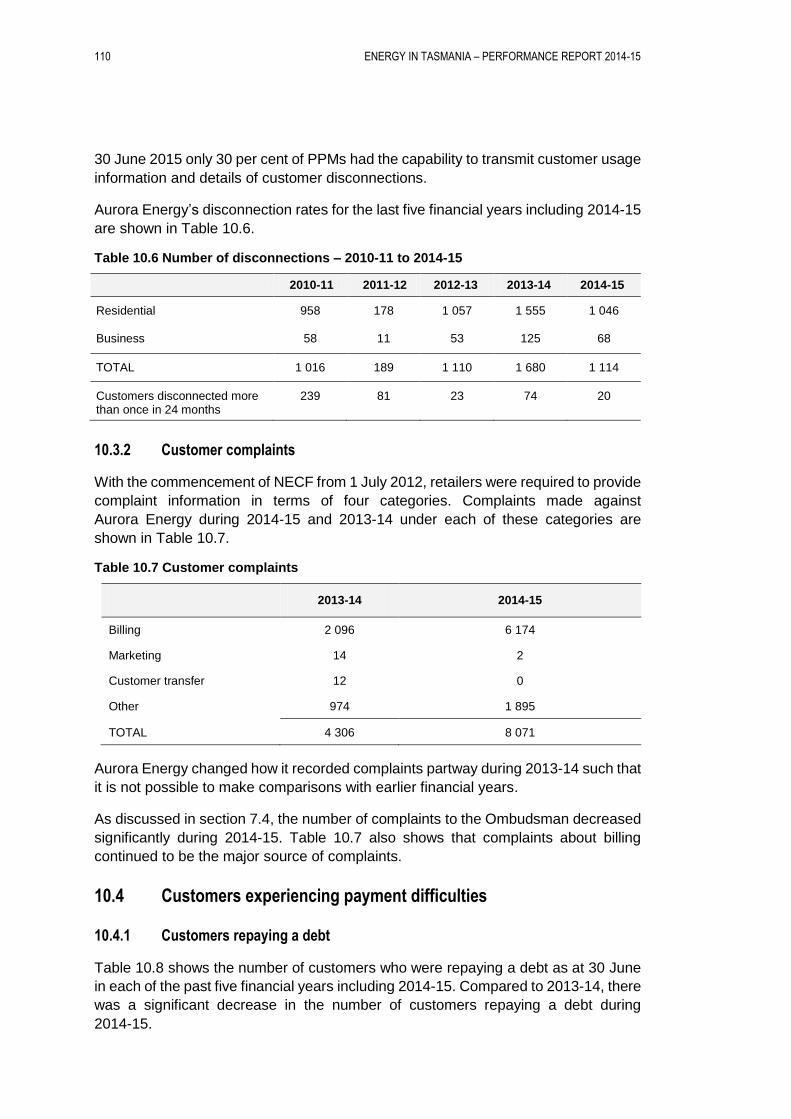

10.3.1 Disconnection rates .............................................................. 109

10.3.2 Customer complaints ............................................................ 110

10.4 Customers experiencing payment difficulties .......................... 110

10.4.1 Customers repaying a debt .................................................. 110

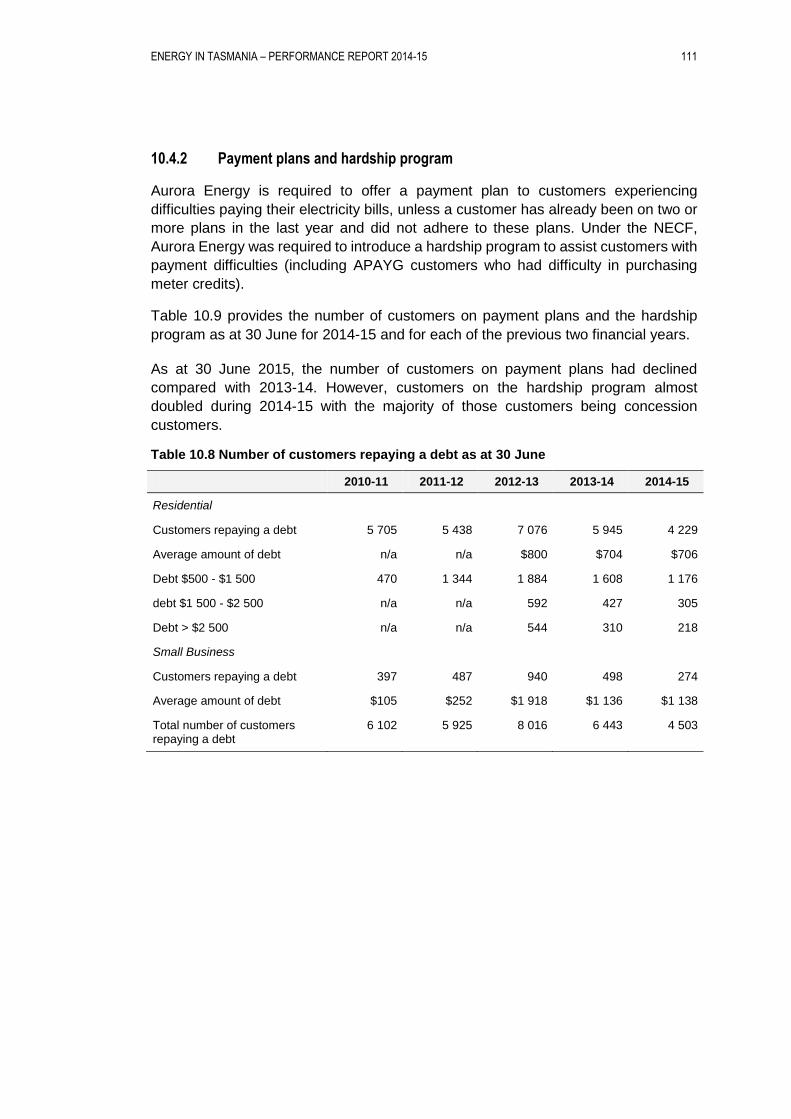

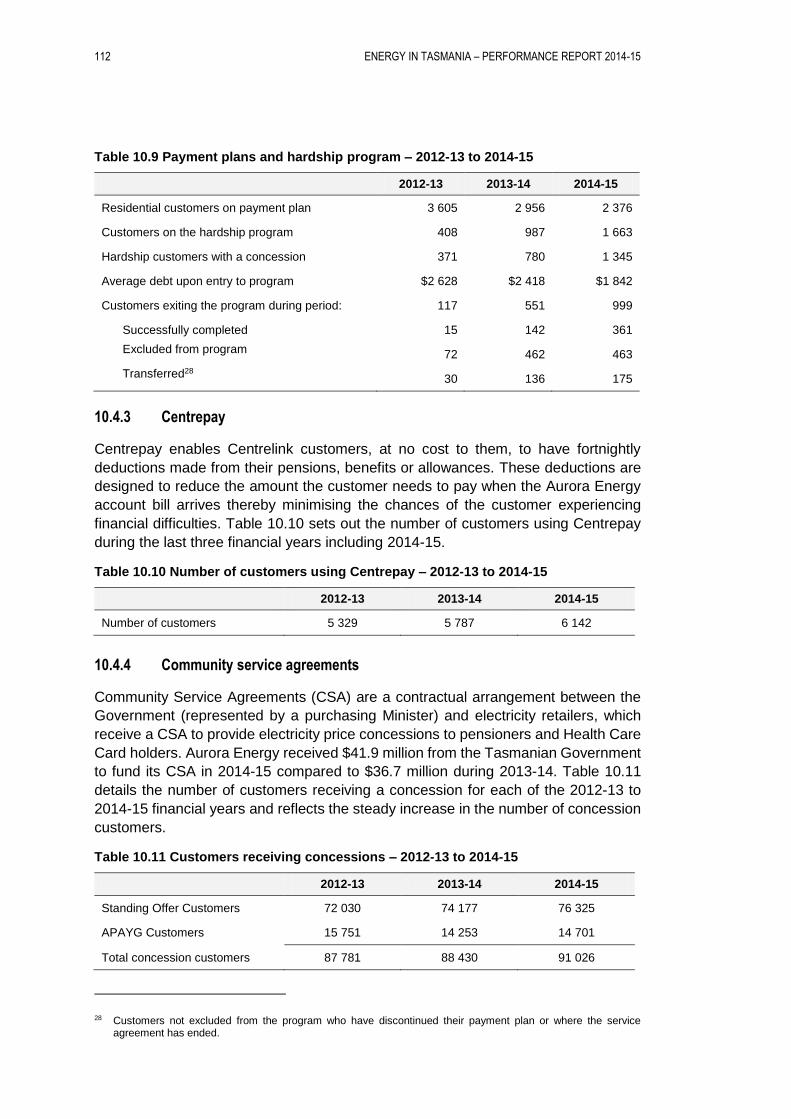

10.4.2 Payment plans and hardship program.................................. 111

10.4.3 Centrepay ............................................................................. 112

10.4.4 Community service agreements ........................................... 112

10.4.5 Tasmanian Government assistance for vulnerable households ........................................................................... 113

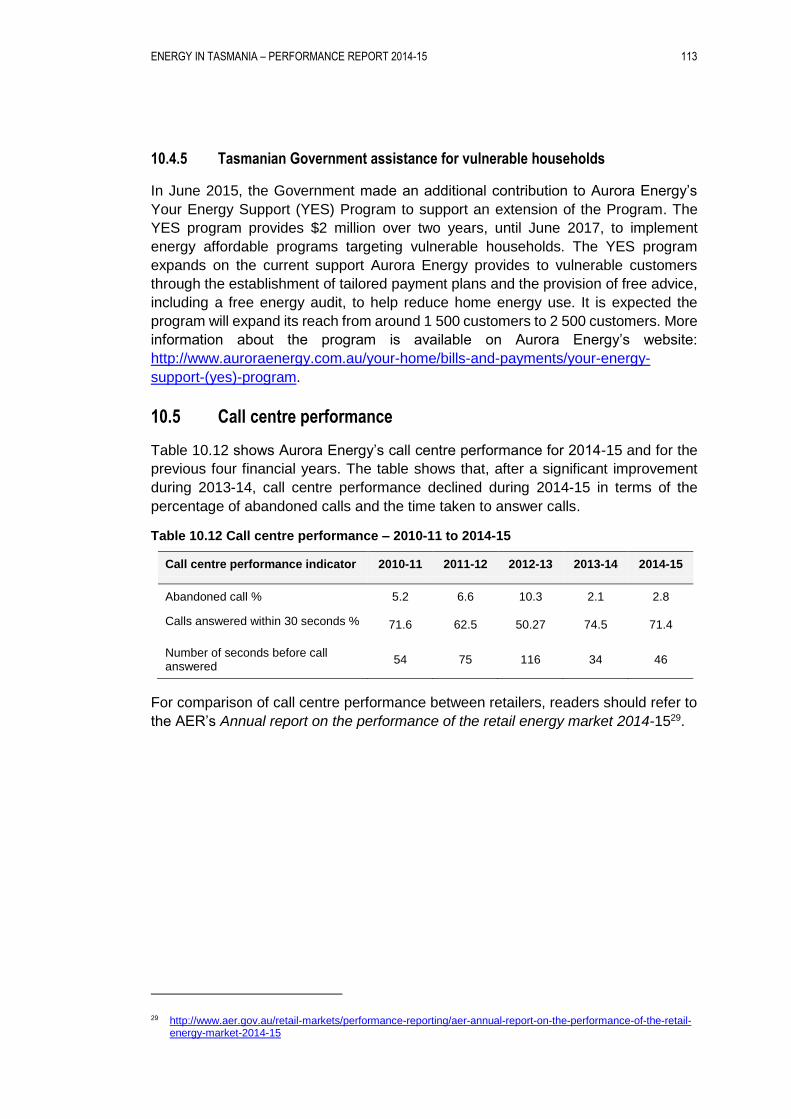

10.5 Call centre performance .......................................................... 113

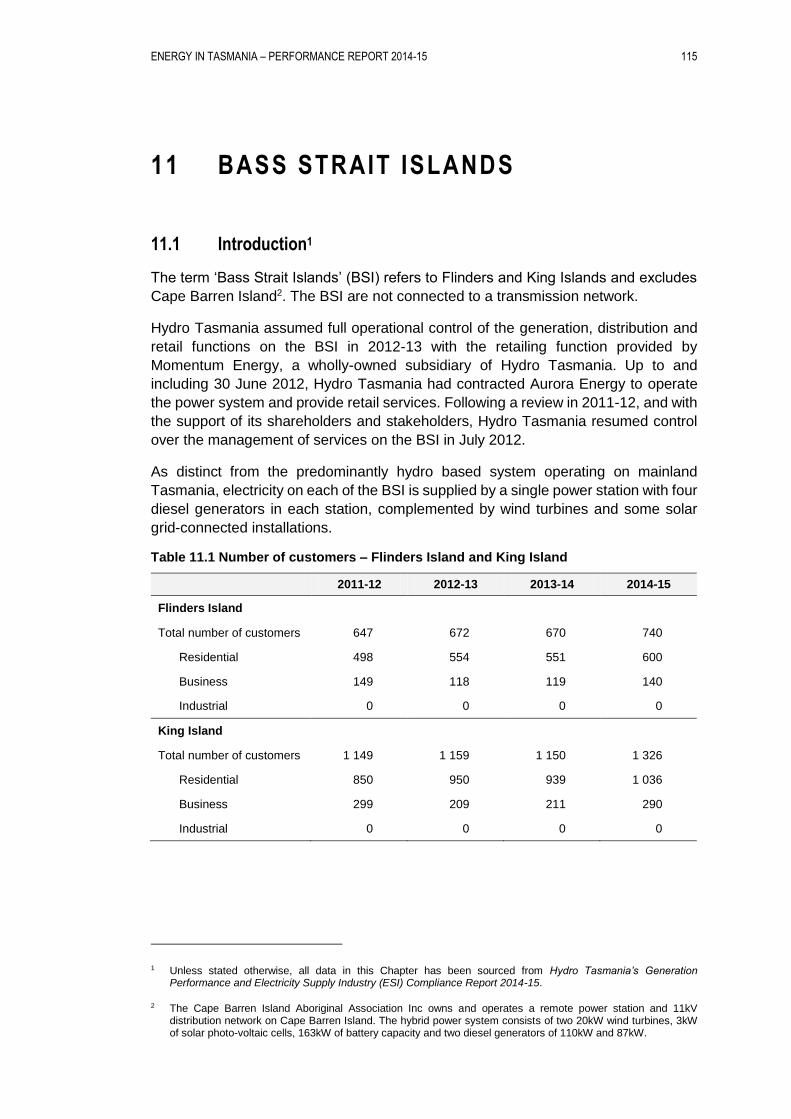

11 BASS STRAIT ISLANDS ............................................................................ 115

11.1 Introduction ............................................................................. 115

11.2 Regulatory arrangements ....................................................... 116

11.3 Generation .............................................................................. 116

ENERGY IN TASMANIA - PERFORMANCE REPORT 2014-15

11.3.1 Flinders Island ...................................................................... 116

11.3.2 King Island ............................................................................ 116

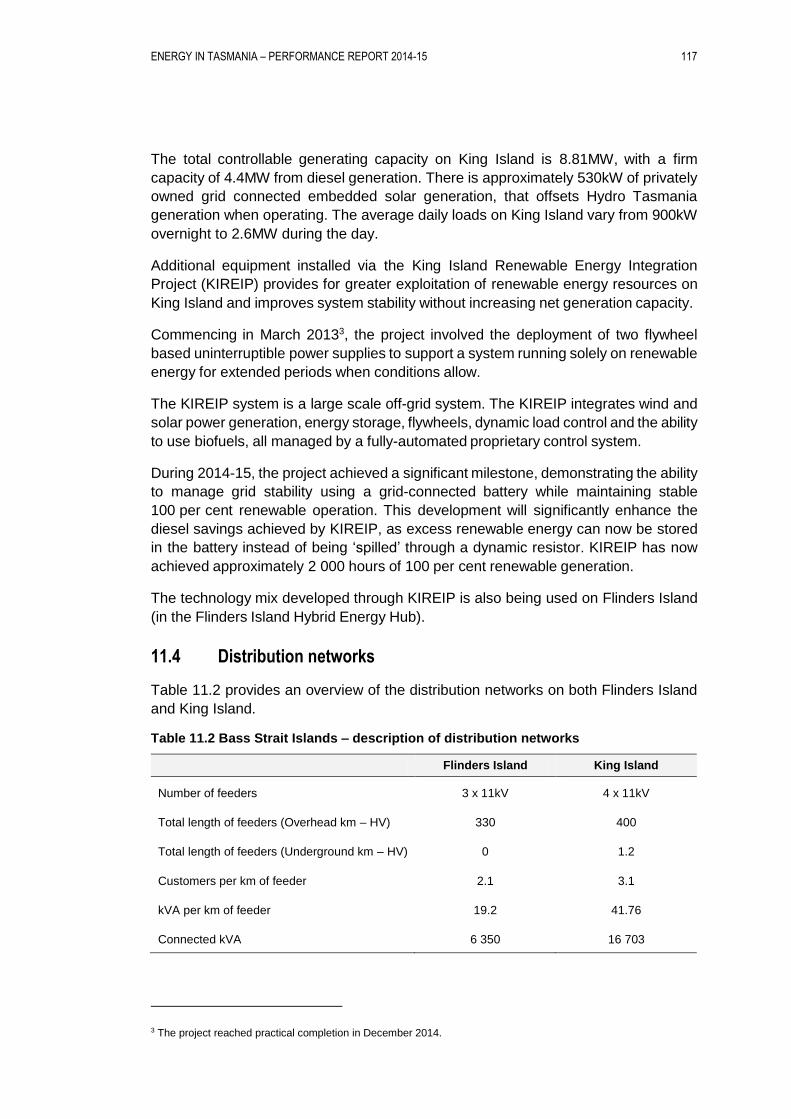

11.4 Distribution networks ............................................................... 117

11.5 Performance ........................................................................... 117

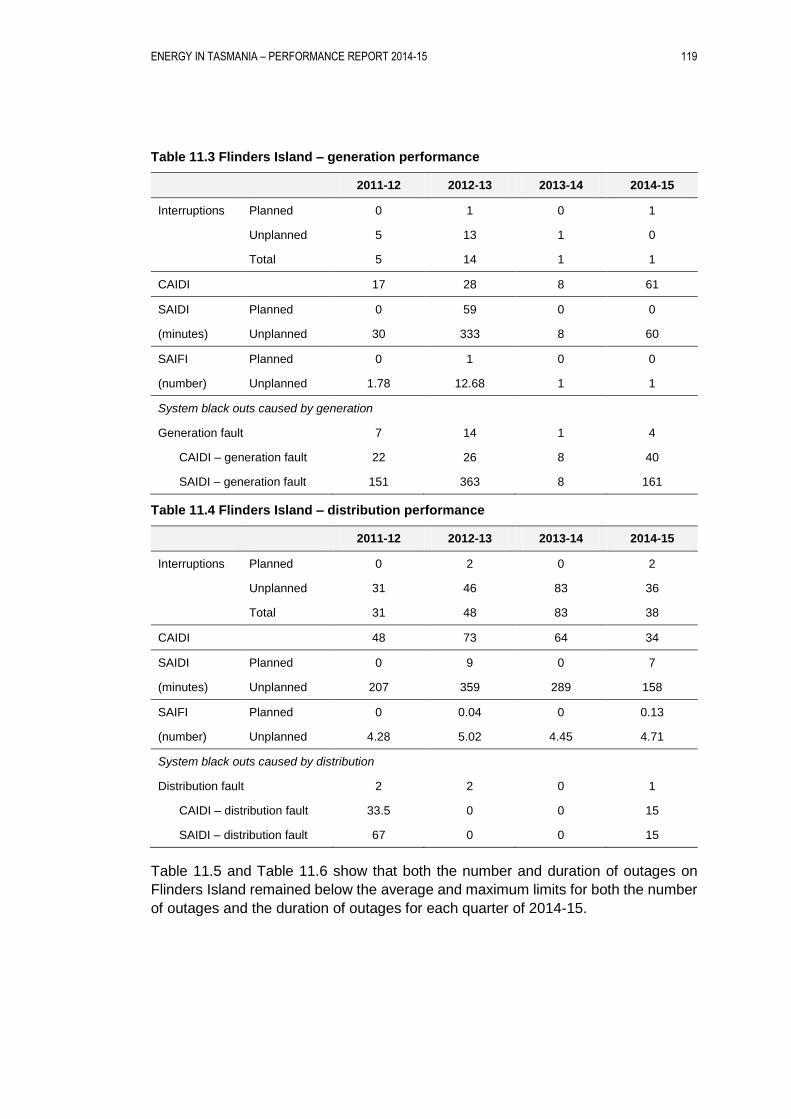

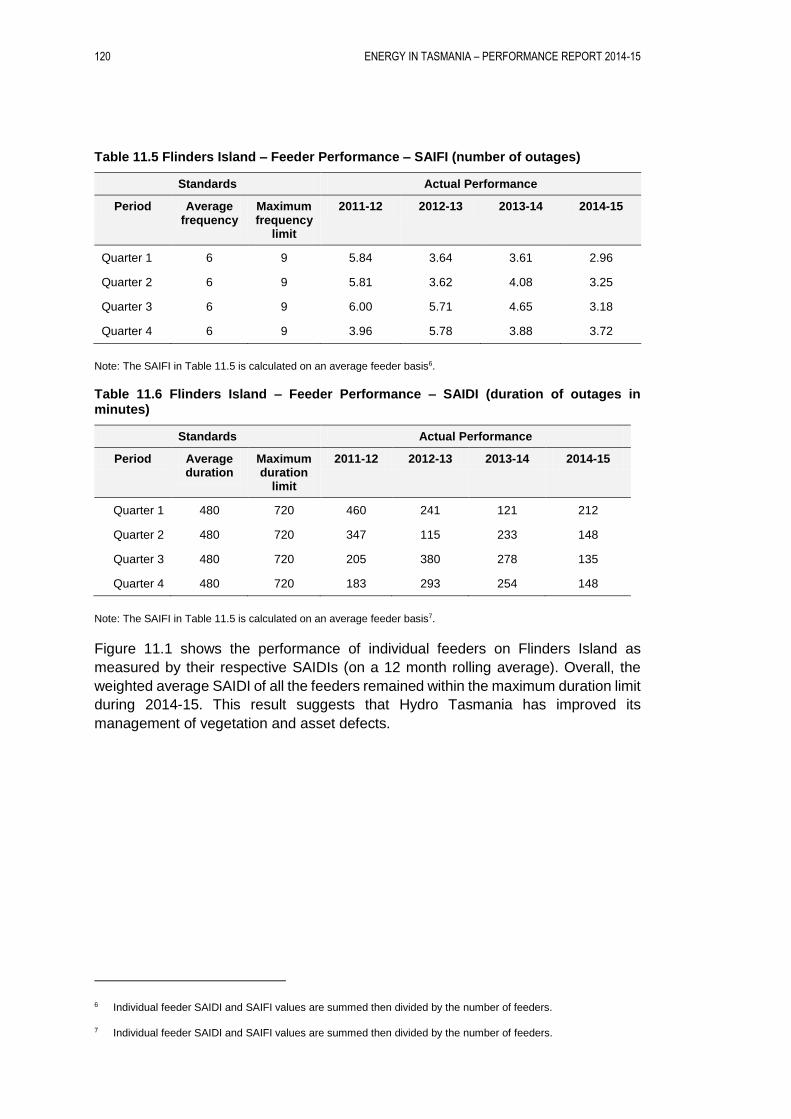

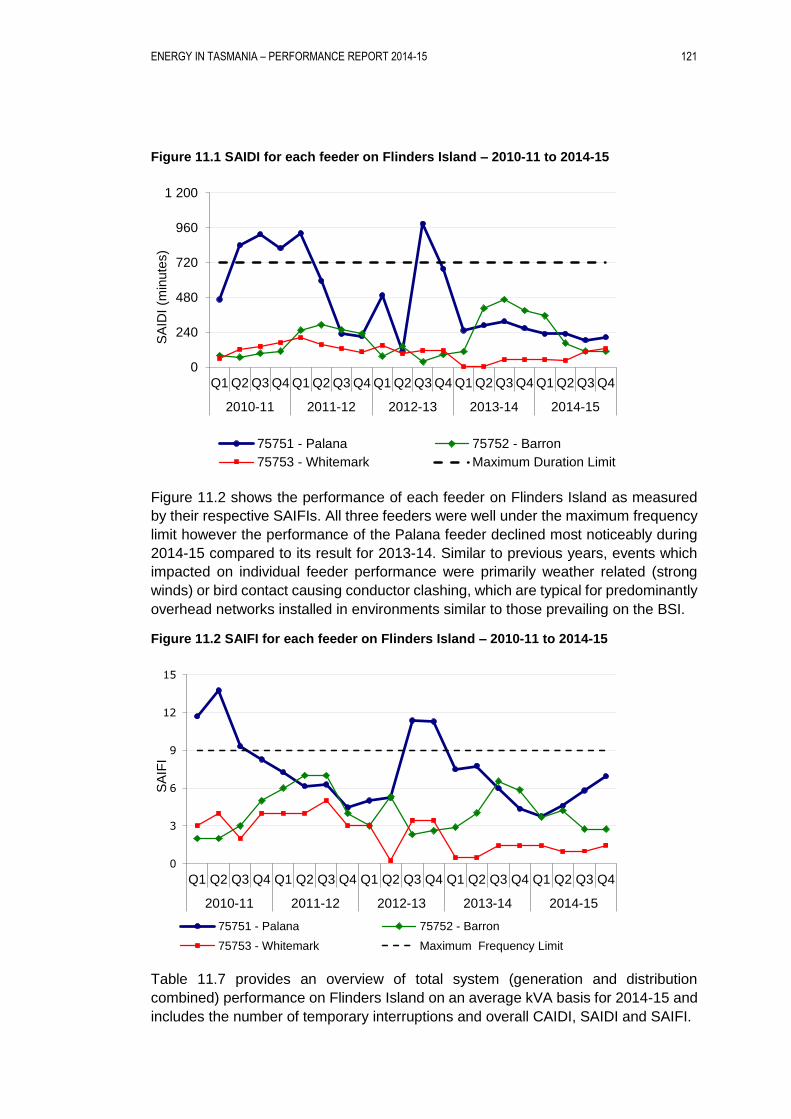

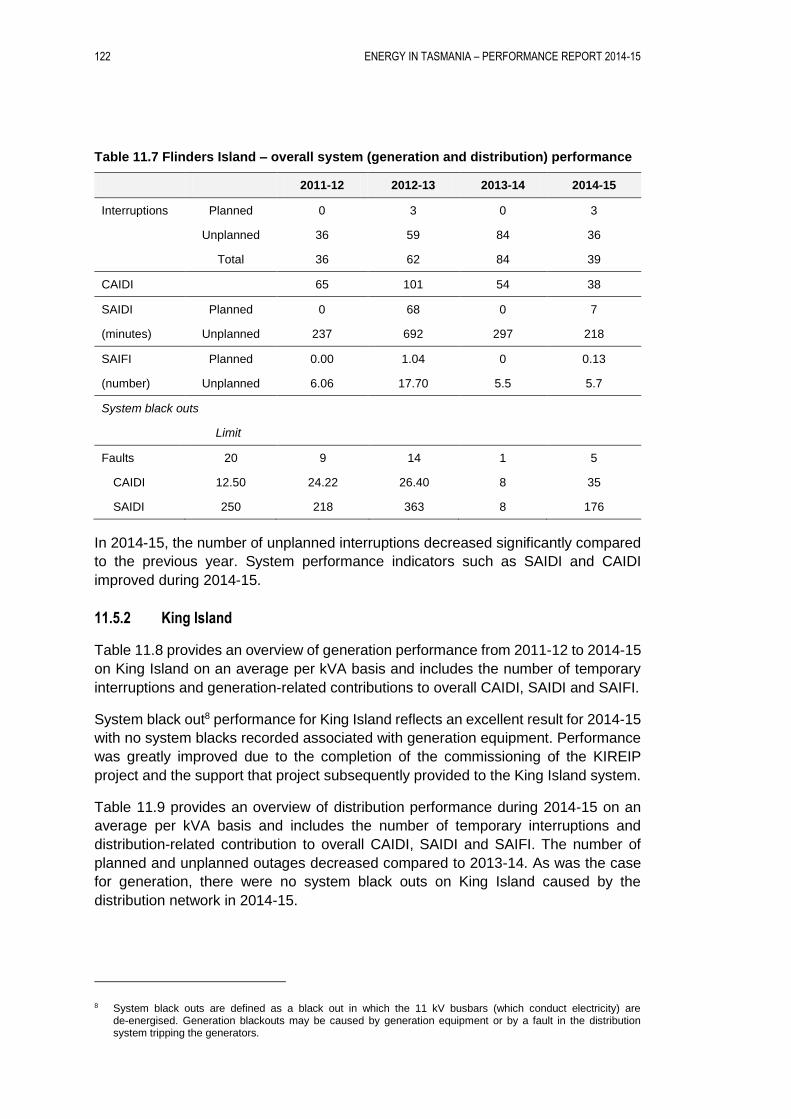

11.5.1 Flinders Island ...................................................................... 118

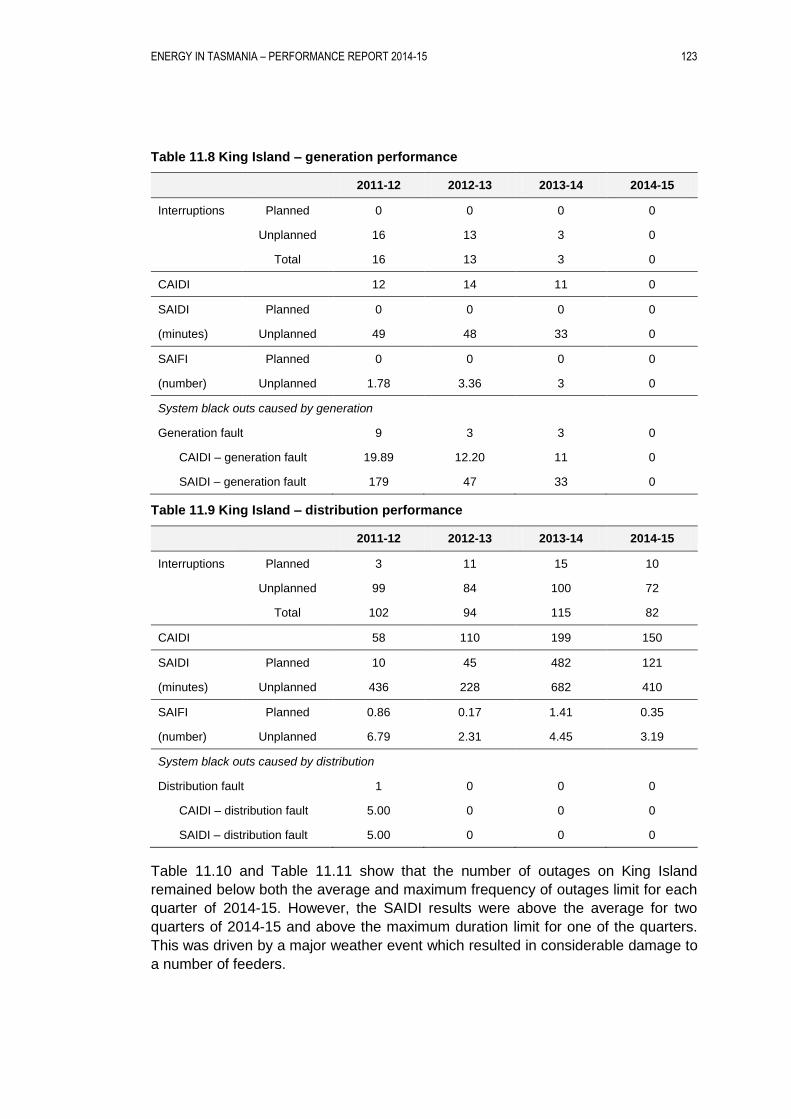

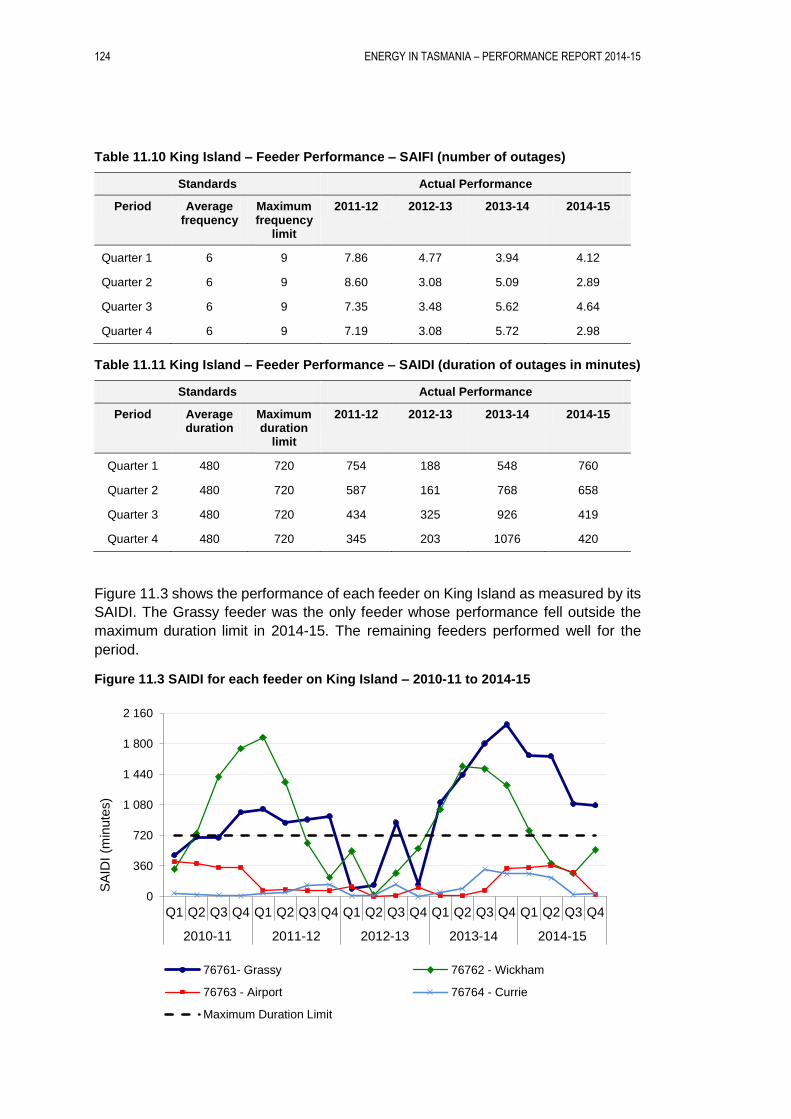

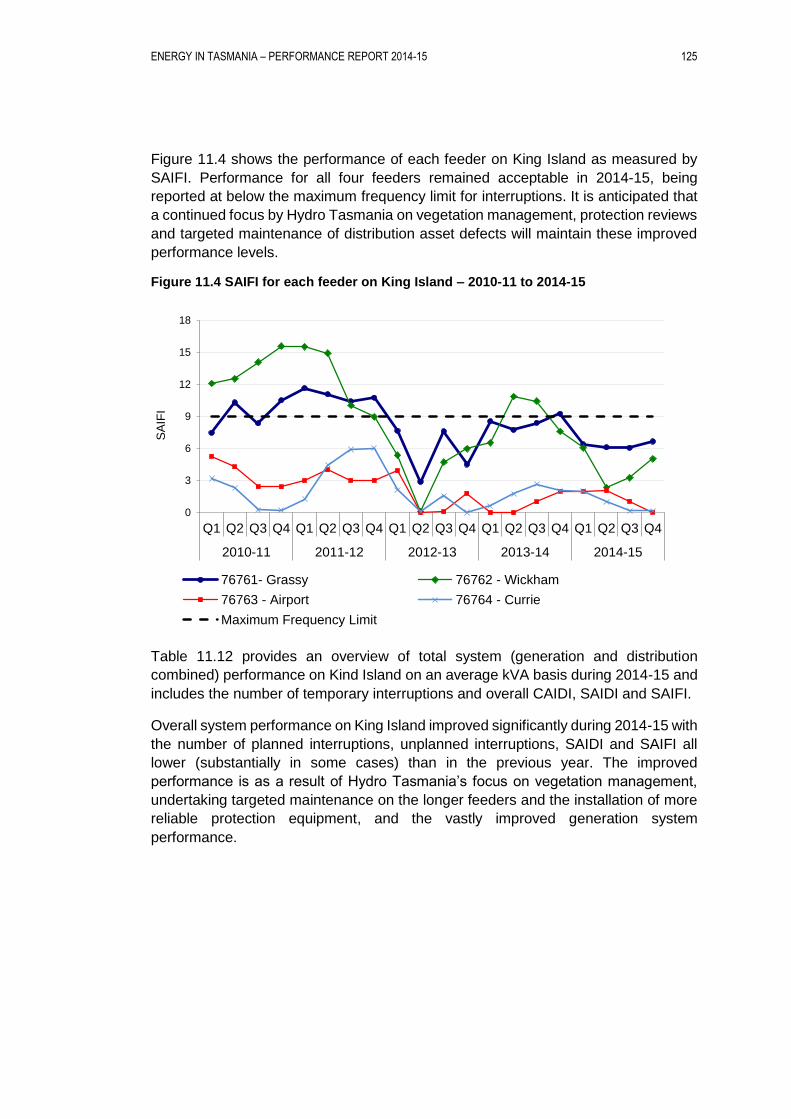

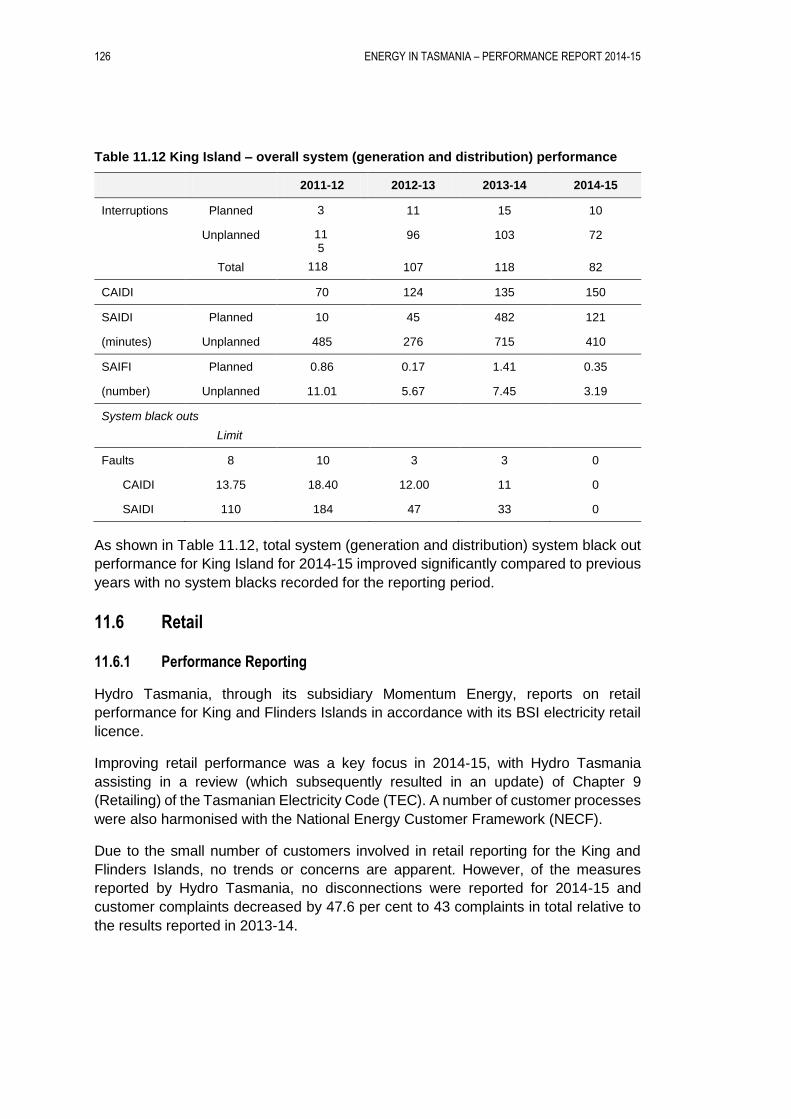

11.5.2 King Island ............................................................................ 122

11.6 Retail ....................................................................................... 126

11.6.1 Performance Reporting ........................................................ 126

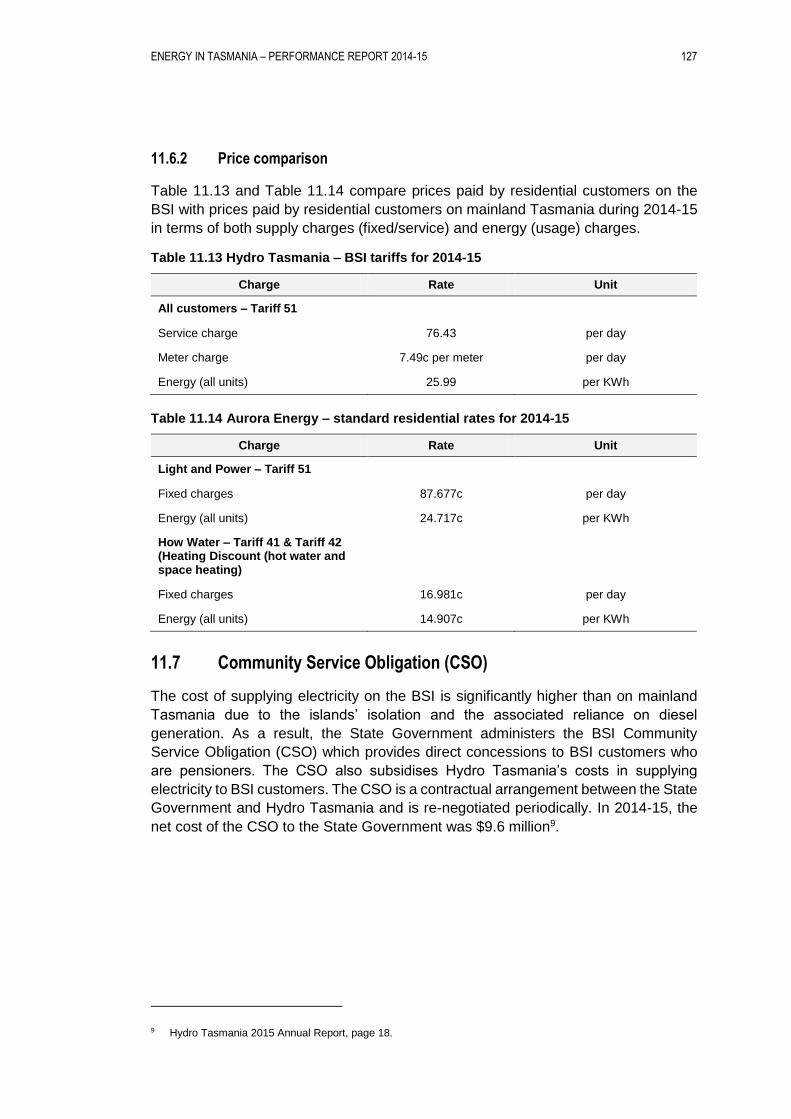

11.6.2 Price comparison .................................................................. 126

11.7 Community Service Obligation (CSO) .................................... 127

12 FUTURE DIRECTIONS............................................................................... 129

12.1 Introduction ............................................................................. 129

12.2 Issues ...................................................................................... 129

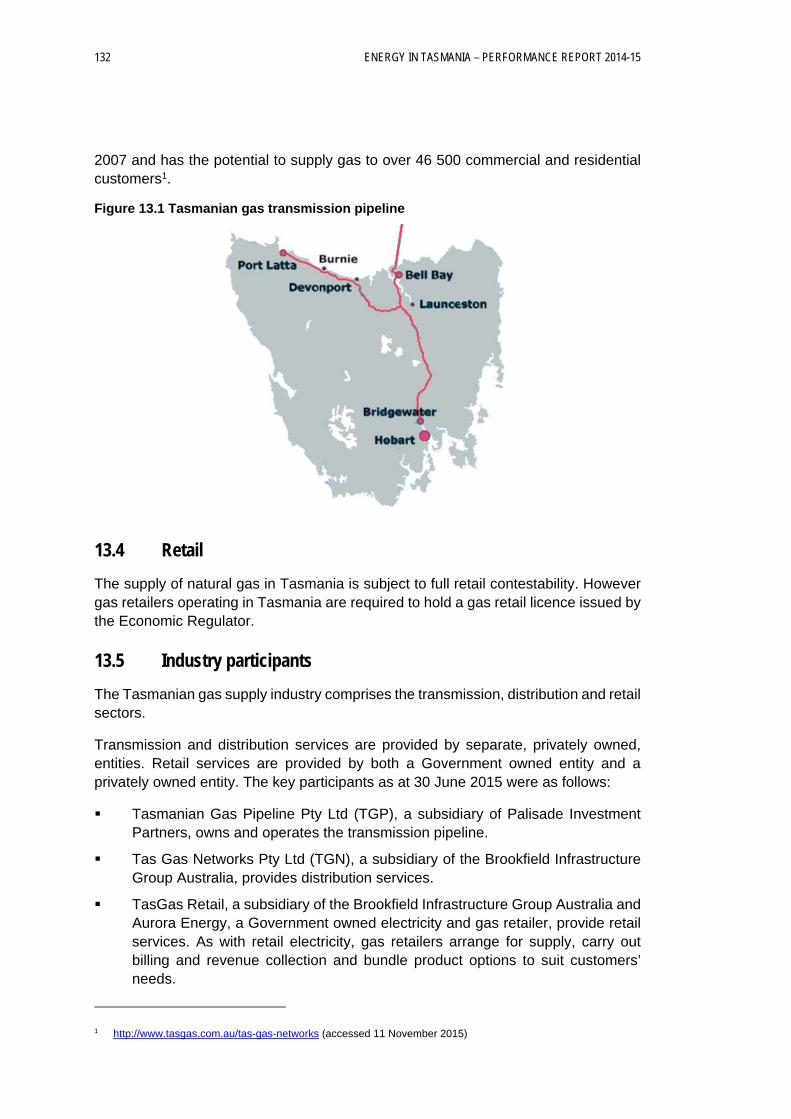

13 OVERVIEW OF THE NATURAL GAS INDUSTRY ..................................... 131

13.1 Introduction ............................................................................. 131

13.2 Transmission ........................................................................... 131

13.3 Distribution .............................................................................. 131

13.4 Retail ....................................................................................... 132

13.5 Industry participants ................................................................ 132

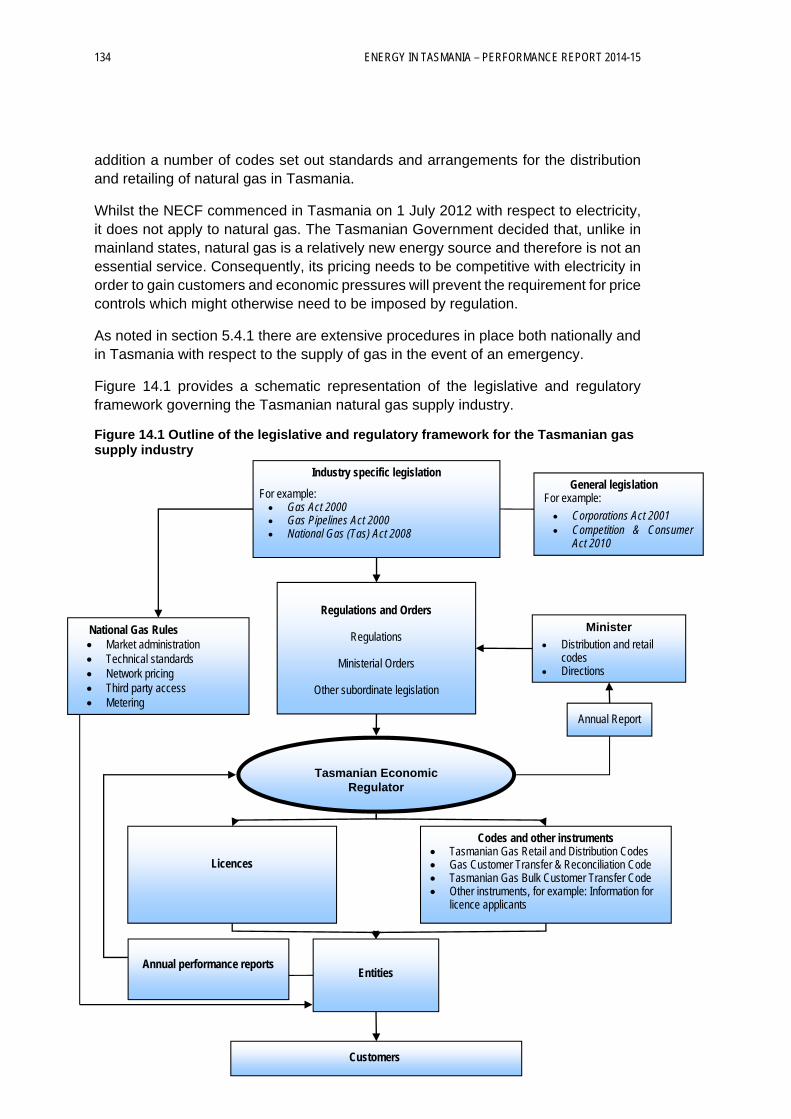

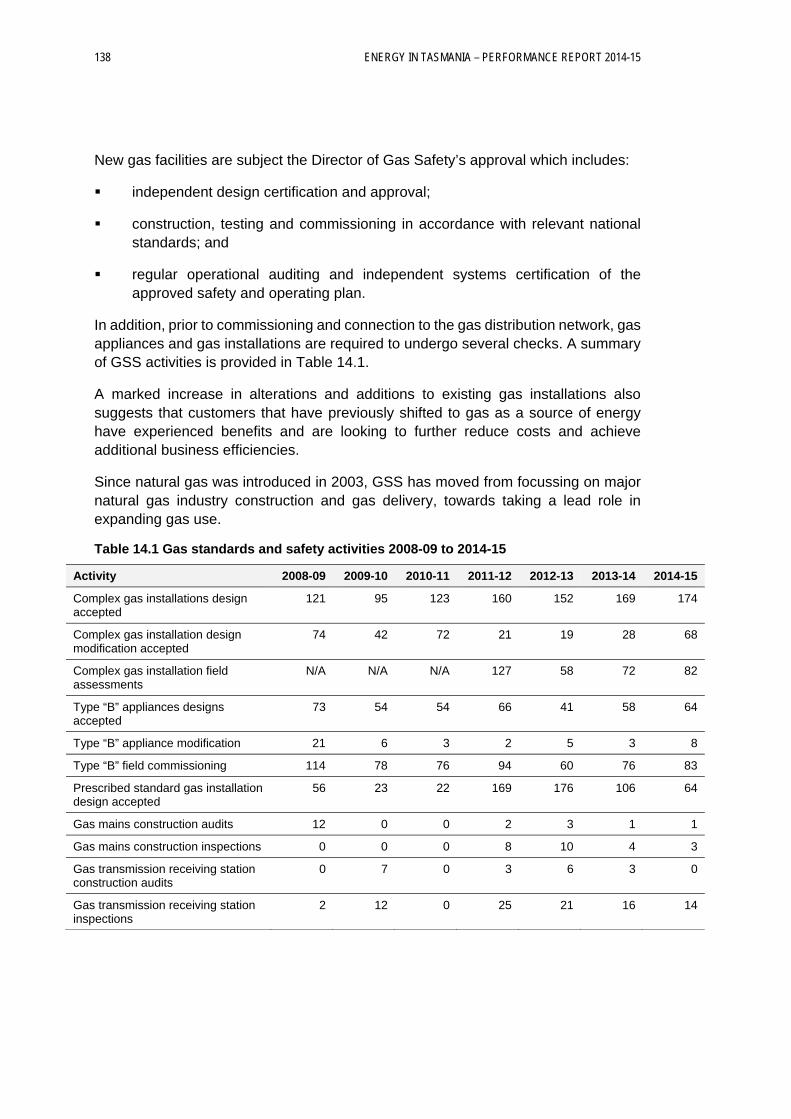

14 GAS REGULATION .................................................................................... 133

14.1 Introduction ............................................................................. 133

14.2 Legislative and regulatory framework ..................................... 133

14.3 Regulators ............................................................................... 135

14.3.1 Tasmanian Economic Regulator .......................................... 135

14.3.2 Tasmanian Energy Ombudsman .......................................... 137

14.3.3 Director of Gas Safety .......................................................... 137

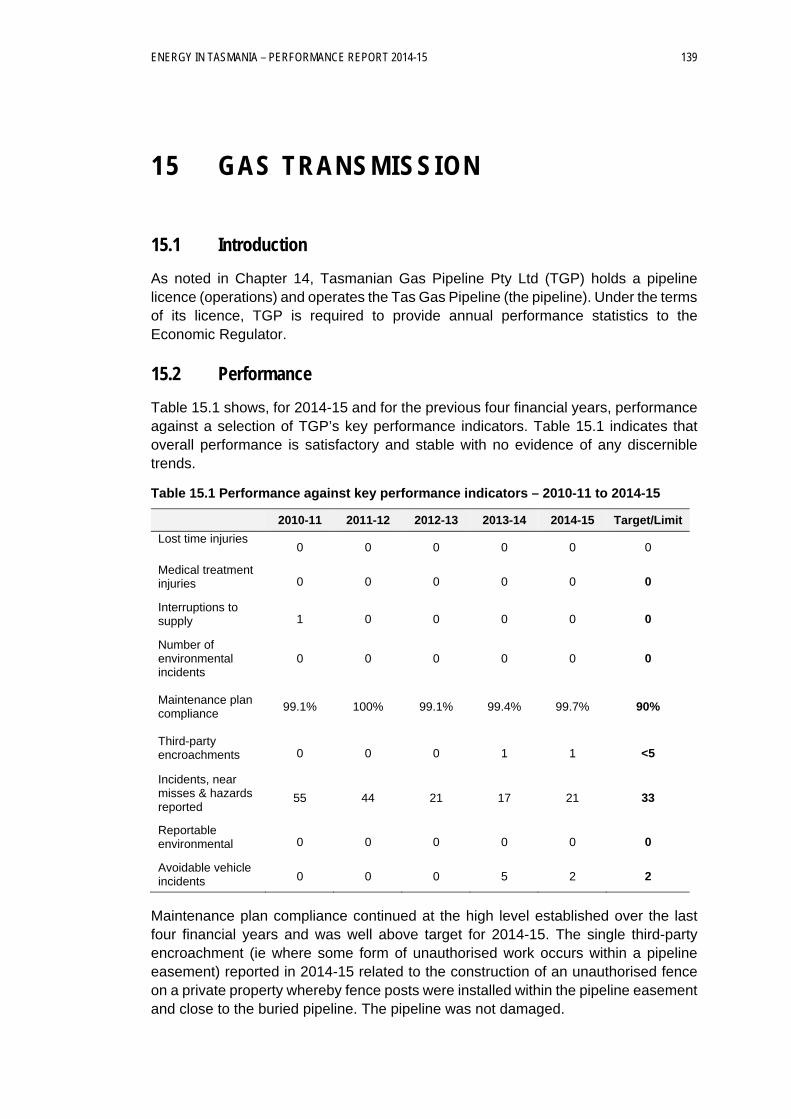

15 GAS TRANSMISSION ................................................................................ 139

15.1 Introduction ............................................................................. 139

15.2 Performance ........................................................................... 139

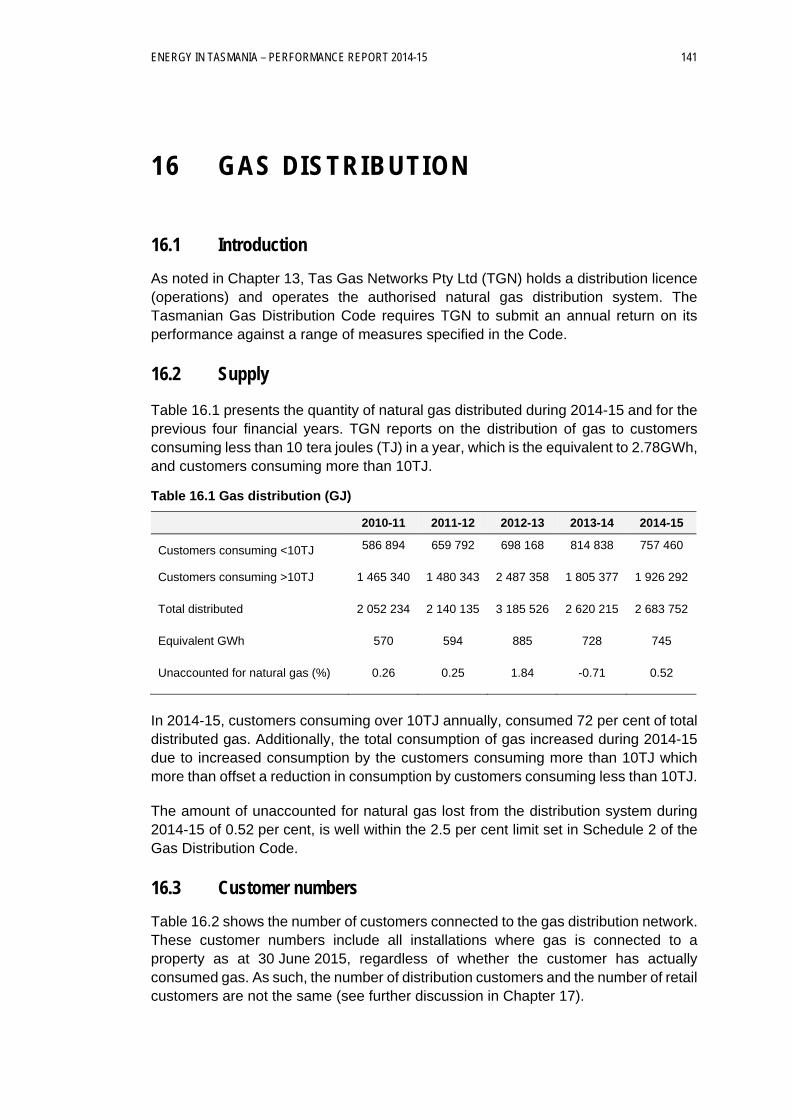

16 GAS DISTRIBUTION .................................................................................. 141

16.1 Introduction ............................................................................. 141

ENERGY IN TASMANIA - PERFORMANCE REPORT 2014-15

16.2 Supply ..................................................................................... 141

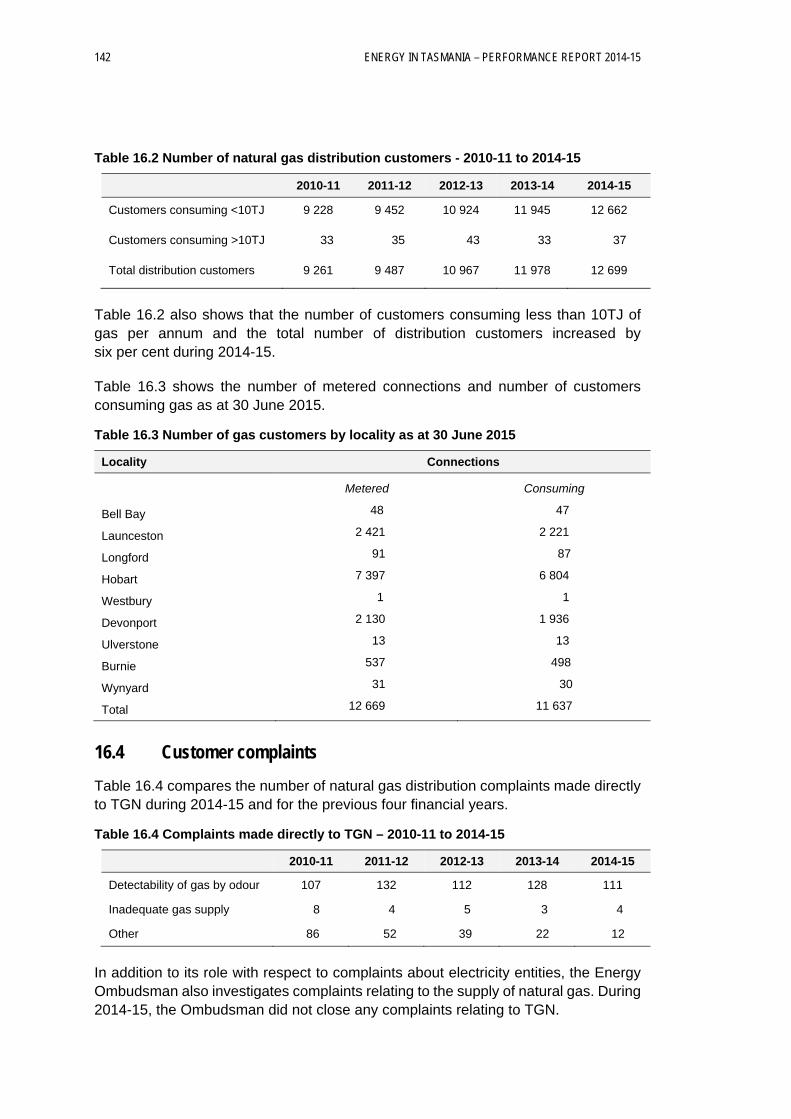

16.3 Customer numbers ................................................................. 141

16.4 Customer complaints .............................................................. 142

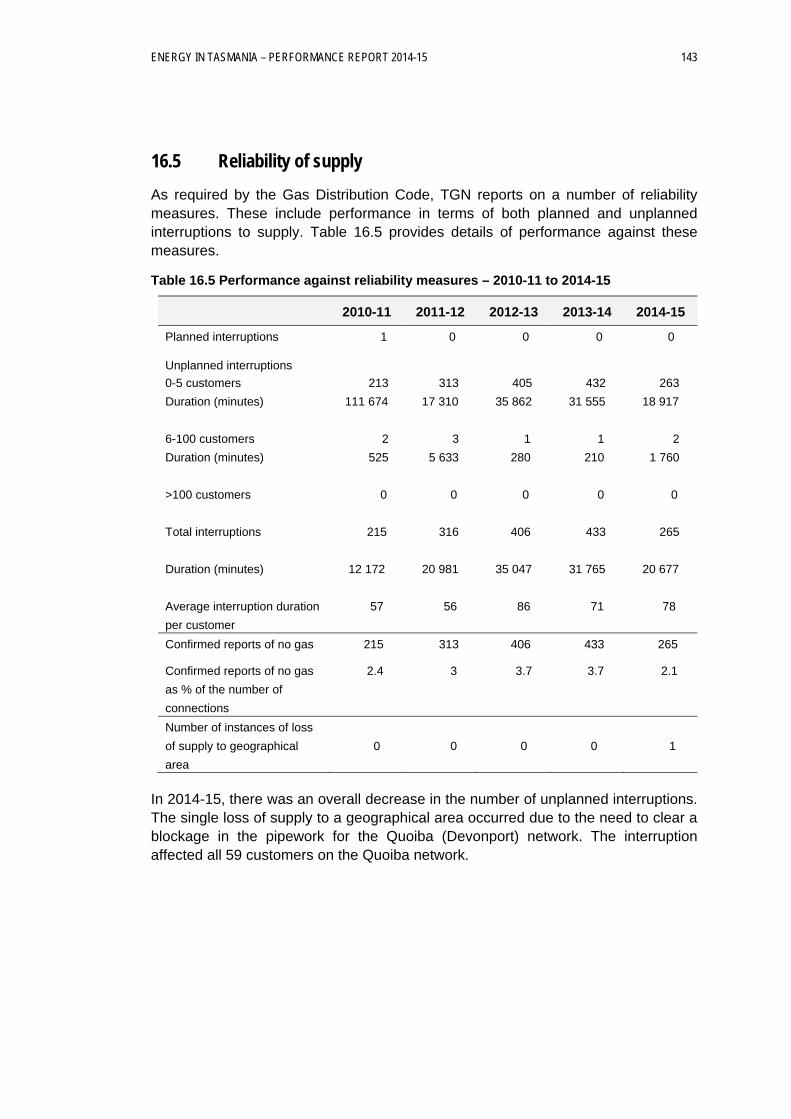

16.5 Reliability of supply ................................................................. 143

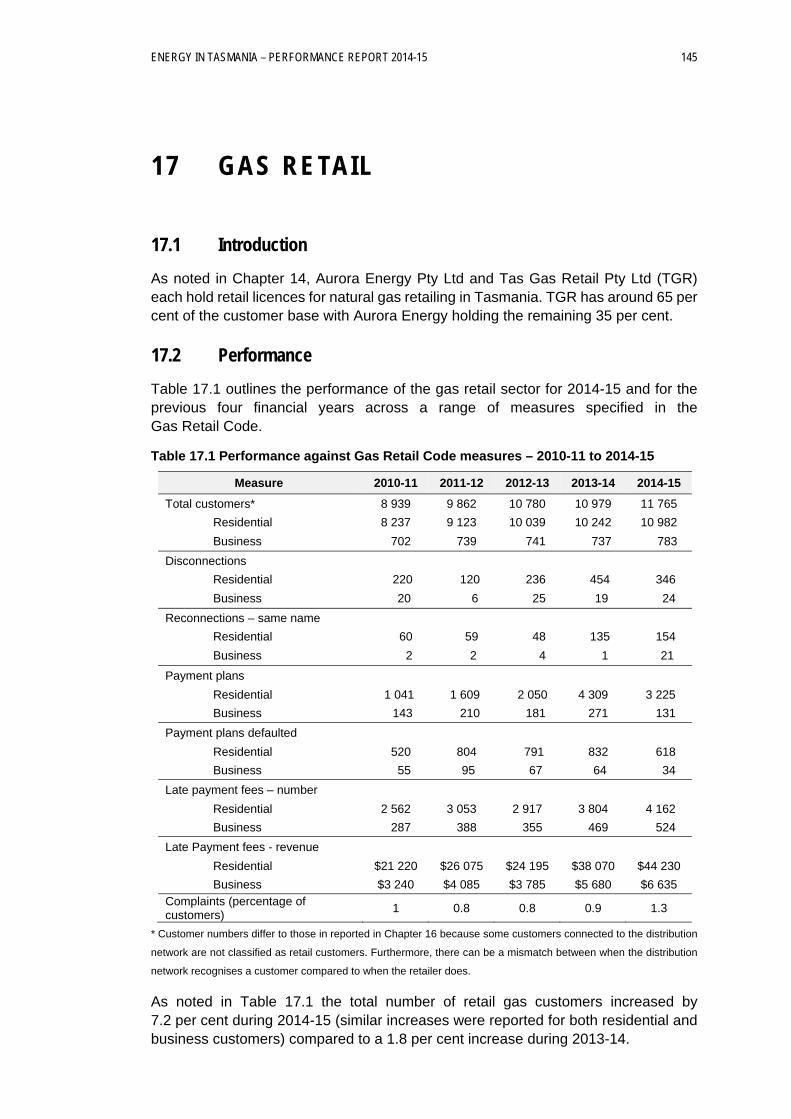

17 GAS RETAIL .............................................................................................. 145

17.1 Introduction ............................................................................. 145

17.2 Performance ........................................................................... 145

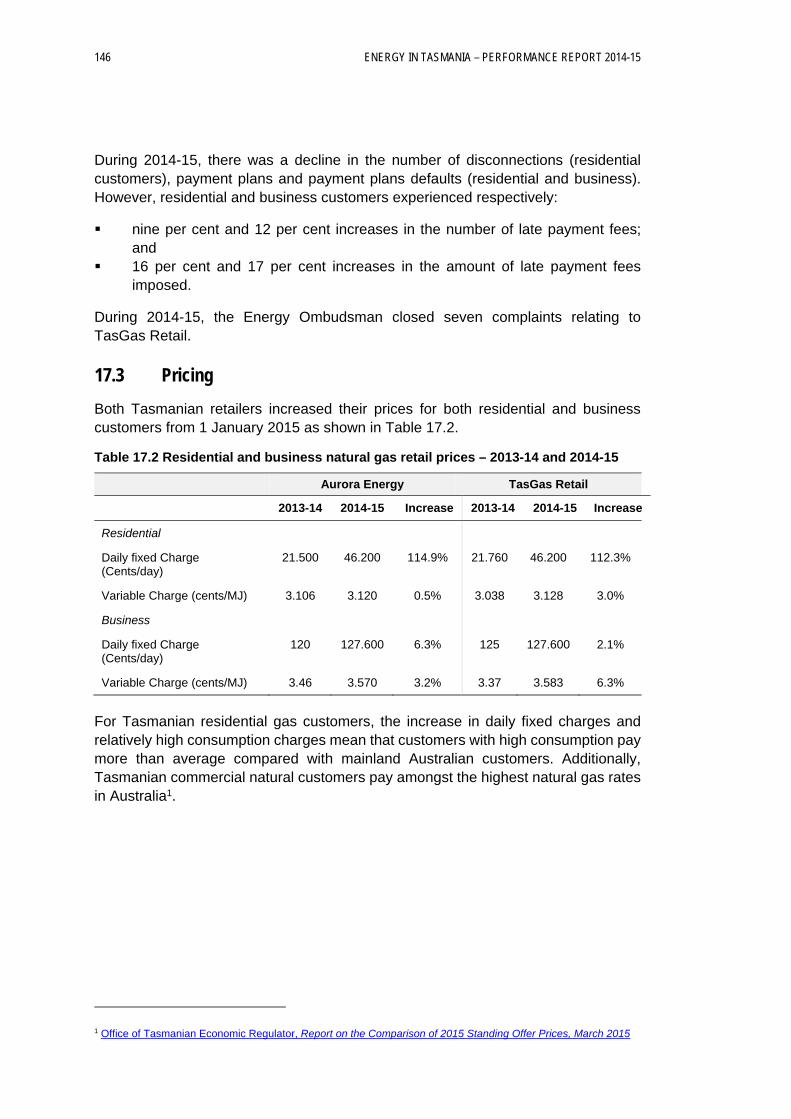

17.3 Pricing ..................................................................................... 146

18 FUTURE DIRECTIONS............................................................................... 147

18.1 Introduction ............................................................................. 147

18.2 Issues ...................................................................................... 147

19 OVERVIEW OF OTHER FUEL SOURCES ................................................ 149

20 PETROLEUM .............................................................................................. 151

20.1 Introduction ............................................................................. 151

20.2 Regulation ............................................................................... 151

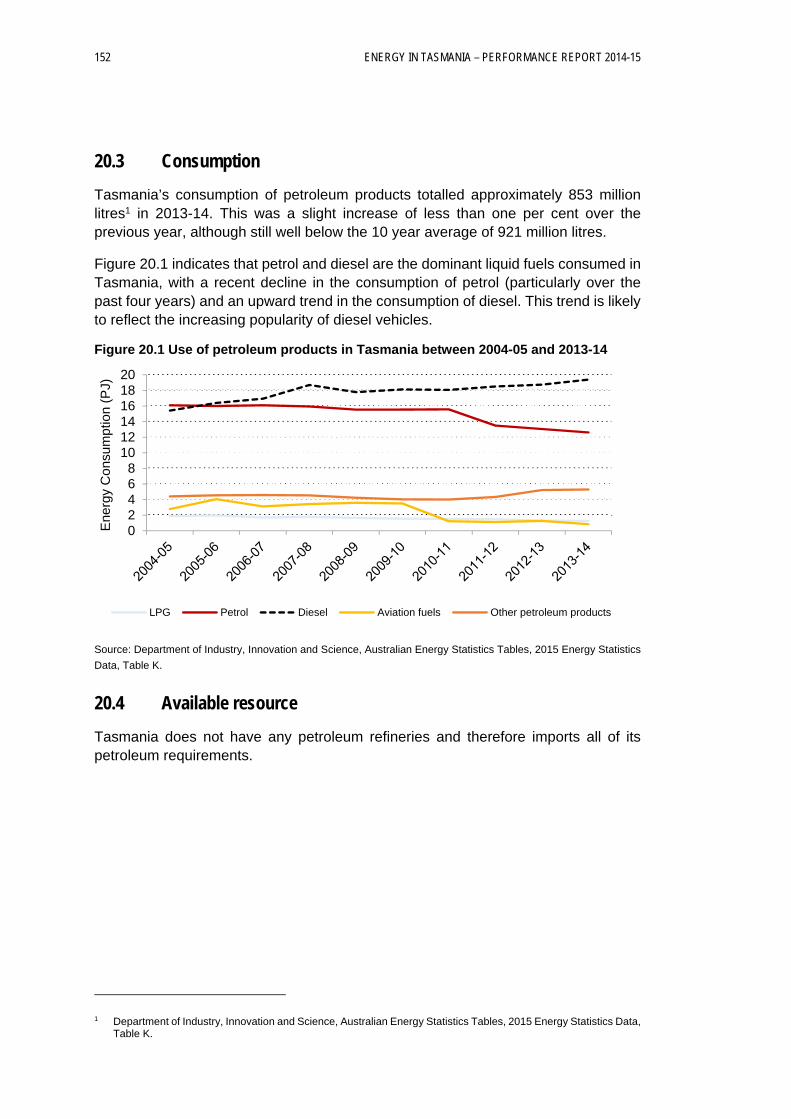

20.3 Consumption ........................................................................... 152

20.4 Available resource .................................................................. 152

21 COAL .......................................................................................................... 153

21.1 Introduction ............................................................................. 153

21.2 Regulation ............................................................................... 153

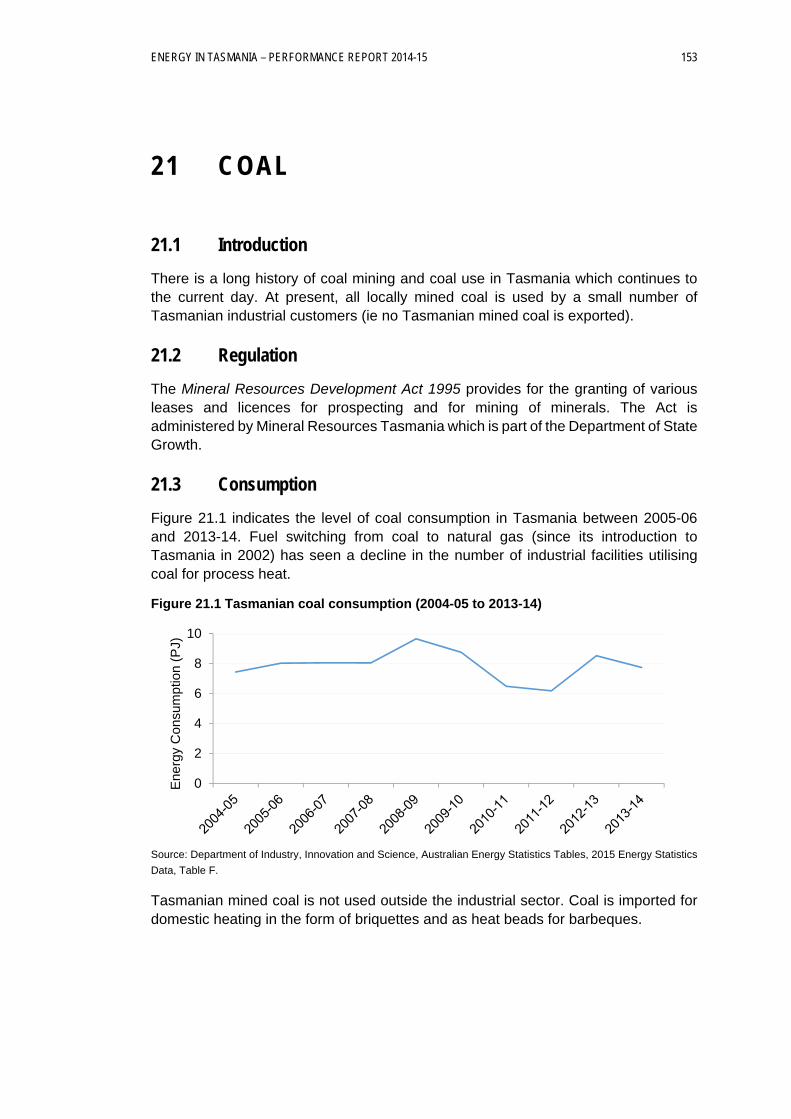

21.3 Consumption ........................................................................... 153

21.4 Available resource .................................................................. 154

21.5 Future directions ..................................................................... 154

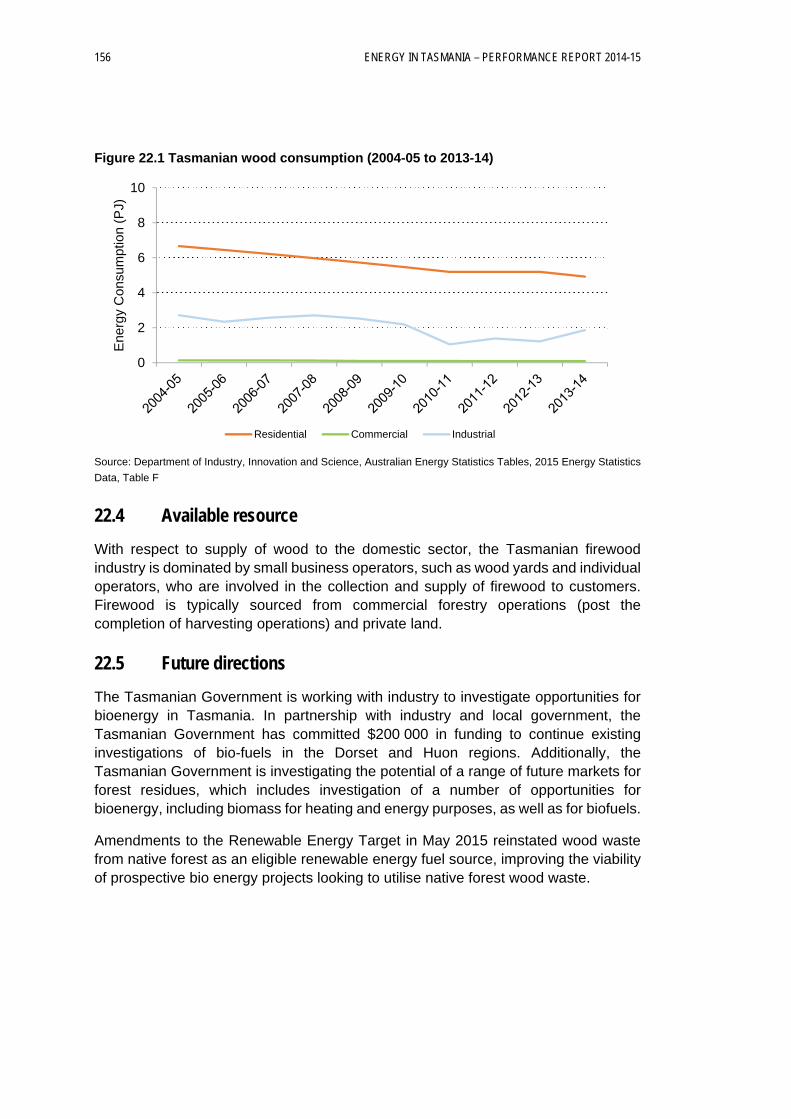

22 WOOD ........................................................................................................ 155

22.1 Introduction ............................................................................. 155

22.2 Regulation ............................................................................... 155

22.3 Consumption ........................................................................... 155

22.4 Available resource .................................................................. 156

ENERGY IN TASMANIA - PERFORMANCE REPORT 2014-15

22.5 Future directions ..................................................................... 156

APPENDIX 1 – CONTRIBUTIONS TO THE ECONOMY ....................................... A-1

Electricity .......................................................................................... A-1

Gas ................................................................................................ A-3

Other fuel sources ............................................................................ A-3

ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15 I

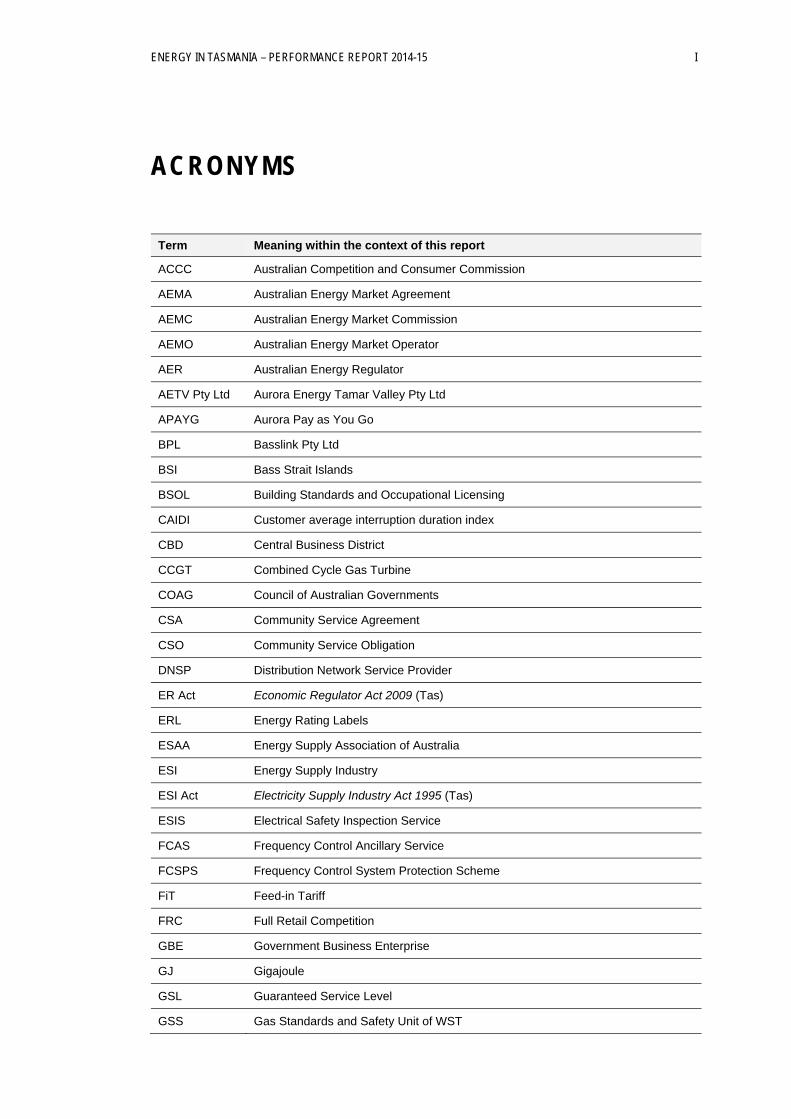

ACRONYMS

Term Meaning within the context of this report

ACCC Australian Competition and Consumer Commission

AEMA Australian Energy Market Agreement

AEMC Australian Energy Market Commission

AEMO Australian Energy Market Operator

AER Australian Energy Regulator

AETV Pty Ltd Aurora Energy Tamar Valley Pty Ltd

APAYG Aurora Pay as You Go

BPL Basslink Pty Ltd

BSI Bass Strait Islands

BSOL Building Standards and Occupational Licensing

CAIDI Customer average interruption duration index

CBD Central Business District

CCGT Combined Cycle Gas Turbine

COAG Council of Australian Governments

CSA Community Service Agreement

CSO Community Service Obligation

DNSP Distribution Network Service Provider

ER Act Economic Regulator Act 2009 (Tas)

ERL Energy Rating Labels

ESAA Energy Supply Association of Australia

ESI Energy Supply Industry

ESI Act Electricity Supply Industry Act 1995 (Tas)

ESIS Electrical Safety Inspection Service

FCAS Frequency Control Ancillary Service

FCSPS Frequency Control System Protection Scheme

FiT Feed-in Tariff

FRC Full Retail Competition

GBE Government Business Enterprise

GJ Gigajoule

GSL Guaranteed Service Level

GSS Gas Standards and Safety Unit of WST

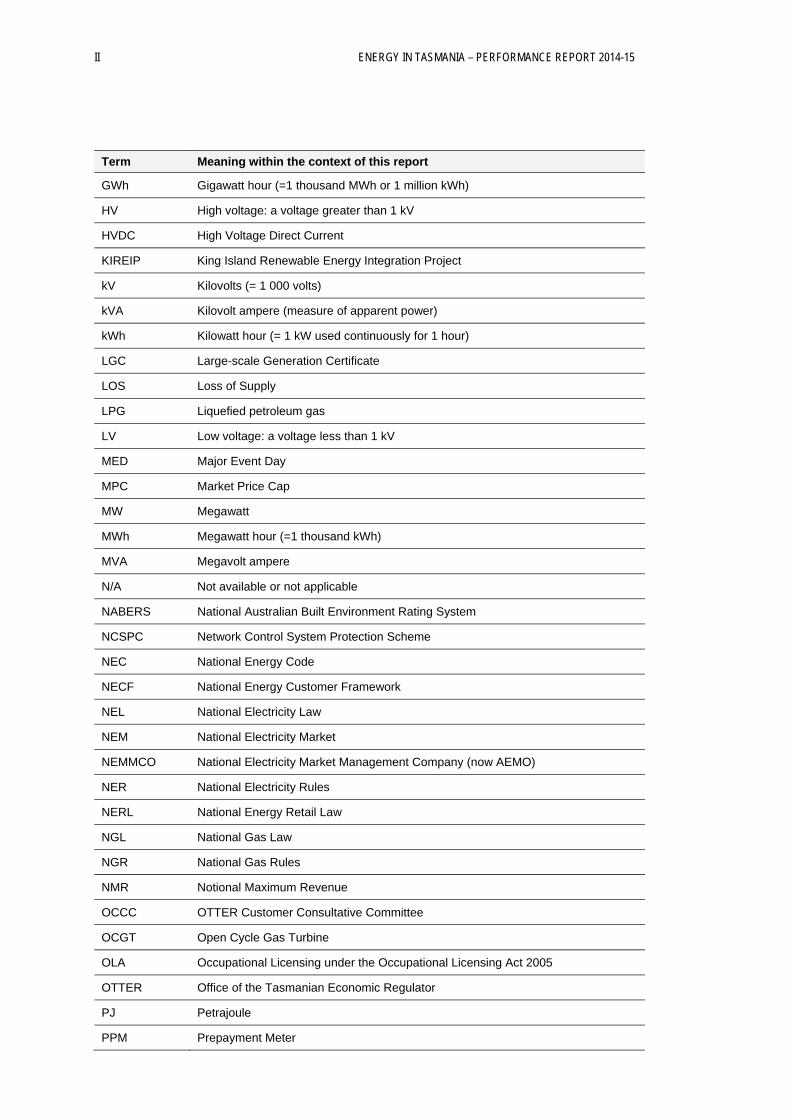

II ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15

Term Meaning within the context of this report

GWh Gigawatt hour (=1 thousand MWh or 1 million kWh)

HV High voltage: a voltage greater than 1 kV

HVDC High Voltage Direct Current

KIREIP King Island Renewable Energy Integration Project

kV Kilovolts (= 1 000 volts)

kVA Kilovolt ampere (measure of apparent power)

kWh Kilowatt hour (= 1 kW used continuously for 1 hour)

LGC Large-scale Generation Certificate

LOS Loss of Supply

LPG Liquefied petroleum gas

LV Low voltage: a voltage less than 1 kV

MED Major Event Day

MPC Market Price Cap

MW Megawatt

MWh Megawatt hour (=1 thousand kWh)

MVA Megavolt ampere

N/A Not available or not applicable

NABERS National Australian Built Environment Rating System

NCSPC Network Control System Protection Scheme

NEC National Energy Code

NECF National Energy Customer Framework

NEL National Electricity Law

NEM National Electricity Market

NEMMCO National Electricity Market Management Company (now AEMO)

NER National Electricity Rules

NERL National Energy Retail Law

NGL National Gas Law

NGR National Gas Rules

NMR Notional Maximum Revenue

OCCC OTTER Customer Consultative Committee

OCGT Open Cycle Gas Turbine

OLA Occupational Licensing under the Occupational Licensing Act 2005

OTTER Office of the Tasmanian Economic Regulator

PJ Petrajoule

PPM Prepayment Meter

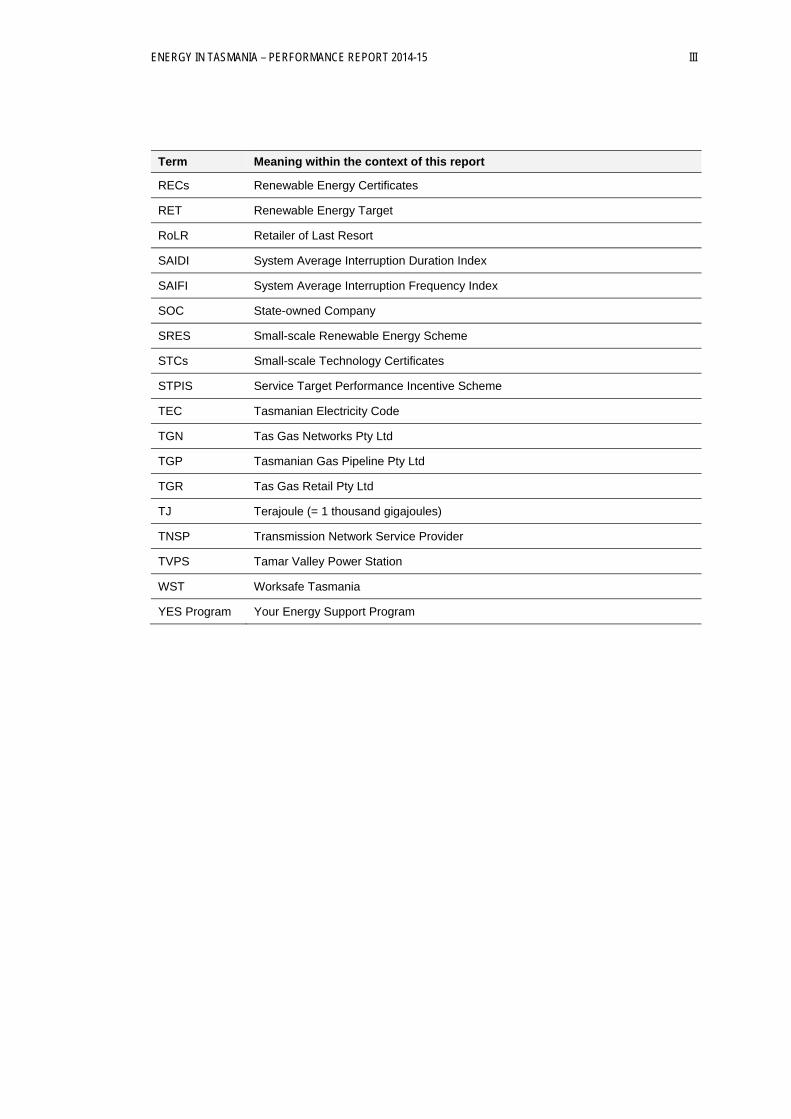

ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15 III

Term Meaning within the context of this report

RECs Renewable Energy Certificates

RET Renewable Energy Target

RoLR Retailer of Last Resort

SAIDI System Average Interruption Duration Index

SAIFI System Average Interruption Frequency Index

SOC State-owned Company

SRES Small-scale Renewable Energy Scheme

STCs Small-scale Technology Certificates

STPIS Service Target Performance Incentive Scheme

TEC Tasmanian Electricity Code

TGN Tas Gas Networks Pty Ltd

TGP Tasmanian Gas Pipeline Pty Ltd

TGR Tas Gas Retail Pty Ltd

TJ Terajoule (= 1 thousand gigajoules)

TNSP Transmission Network Service Provider

TVPS Tamar Valley Power Station

WST Worksafe Tasmania

YES Program Your Energy Support Program

ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15 V

EXECUTIVE SUMMARY

The Tasmanian Economic Regulator is required, by the Electricity Supply Industry Act 1995, the Gas Act 2000 and the Gas Pipelines Act 2000 to, amongst other things:

establish and monitor proper standards of safety, reliability and quality in the supply of electricity and natural gas; and

protect the interests of electricity and natural gas consumers.

The Economic Regulator may also, of its own initiative, or under direction from the Minister for Energy and the Treasurer, prepare a state of the industry report, in respect to the performance of the electricity and gas supply industries.

In Tasmania, energy is sourced not only from electricity and gas, but also from petroleum products, coal and wood. This Report examines the state of the electricity and gas industries, provides an overview of other fuel sources and summarises the performance of the various electricity and gas supply entities operating in Tasmania during the 2014-15 financial year. The Report aims to make the entities publicly accountable for their performance and for the standard of the services they provide.

Following the trend since 2008-09, Tasmanian electricity demand declined during 2014-15. Similarly, during 2014-15, the amount of electricity generated in Tasmania declined, with a significant increase in Basslink imports and a decline in exports.

The change in Basslink flows was due partly to the removal of the carbon pricing mechanism, from 1 July 2014, but it also reflects reduced inflows and relatively low storage levels for hydro generation. During 2014-15, hydro generation declined by around one-third, compared with 2013-14. There was also less wind generation, due to weather conditions, while there was minimal thermal generation at the Tamar Valley Power Station (TVPS).

Aurora Energy continued to be the sole retailer for residential electricity customers. The number of customers using Aurora’s Pay As You Go continued to decline during 2014-15. For the period, there were less customers repaying a debt. However, more customers were on Aurora’s hardship program than in previous years, with most being concession customers.

Due to reduced TVPS generation during 2014-15, the gas transmission pipeline operated at less than 20 per cent of capacity. Despite this, the volume of gas distributed to other consumers increased in the period. The increased demand was from larger customers, offset slightly by less demand from smaller gas customers. Overall, the number of residential and business gas customers increased, continuing the steady growth in the gas retail market of recent years.

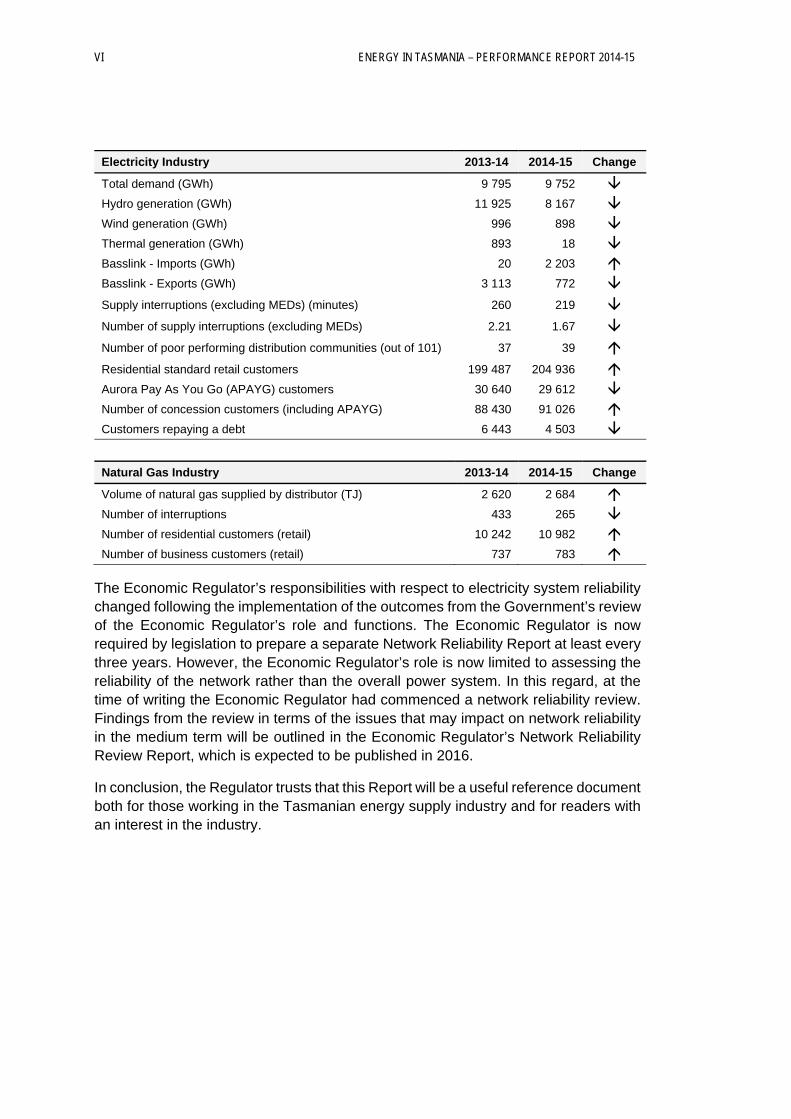

Overall, the Tasmanian electricity and natural gas sectors met most of the relevant performance standards during 2014-15. Key performance highlights for 2014-15 compared to performance during 2013-14 are summarised in the following table.

VI ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15

Electricity Industry 2013-14 2014-15 Change

Total demand (GWh) 9 795 9 752 Hydro generation (GWh) 11 925 8 167 Wind generation (GWh) 996 898 Thermal generation (GWh) 893 18 Basslink - Imports (GWh) 20 2 203 Basslink - Exports (GWh) 3 113 772 Supply interruptions (excluding MEDs) (minutes) 260 219 Number of supply interruptions (excluding MEDs) 2.21 1.67 Number of poor performing distribution communities (out of 101) 37 39 Residential standard retail customers 199 487 204 936 Aurora Pay As You Go (APAYG) customers 30 640 29 612 Number of concession customers (including APAYG) 88 430 91 026 Customers repaying a debt 6 443 4 503

Natural Gas Industry 2013-14 2014-15 Change

Volume of natural gas supplied by distributor (TJ) 2 620 2 684 Number of interruptions 433 265 Number of residential customers (retail) 10 242 10 982 Number of business customers (retail) 737 783

The Economic Regulator’s responsibilities with respect to electricity system reliability changed following the implementation of the outcomes from the Government’s review of the Economic Regulator’s role and functions. The Economic Regulator is now required by legislation to prepare a separate Network Reliability Report at least every three years. However, the Economic Regulator’s role is now limited to assessing the reliability of the network rather than the overall power system. In this regard, at the time of writing the Economic Regulator had commenced a network reliability review. Findings from the review in terms of the issues that may impact on network reliability in the medium term will be outlined in the Economic Regulator’s Network Reliability Review Report, which is expected to be published in 2016.

In conclusion, the Regulator trusts that this Report will be a useful reference document both for those working in the Tasmanian energy supply industry and for readers with an interest in the industry.

ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15 1

1 OVERVIEW OF THE TASMANIAN ENERGY INDUSTRY

Public reporting of performance is an important tool to protect consumers and promote efficiency and competition. This is particularly the case in markets dominated by a limited number of players as is the case with the Tasmanian energy supply industry.

In this regard, the Electricity Supply Industry Act 1995 (ESI Act) gives the Tasmanian Economic Regulator (the Regulator) certain functions to protect the interests of electricity consumers through, among other things, establishing and enforcing appropriate standards of safety, security, reliability and quality. The Regulator is also responsible for gas regulation under the Gas Act 2000 (Gas Act), Gas Pipelines Act 2000 (Gas Pipelines Act) and the Gas Pipelines Access (Tasmania) Act 2000.

Under the ESI Act, the Gas Act and the Gas Pipelines Act, the Economic Regulator may prepare state of the industry performance reports with respect to the performance of the electricity supply and gas supply industries.

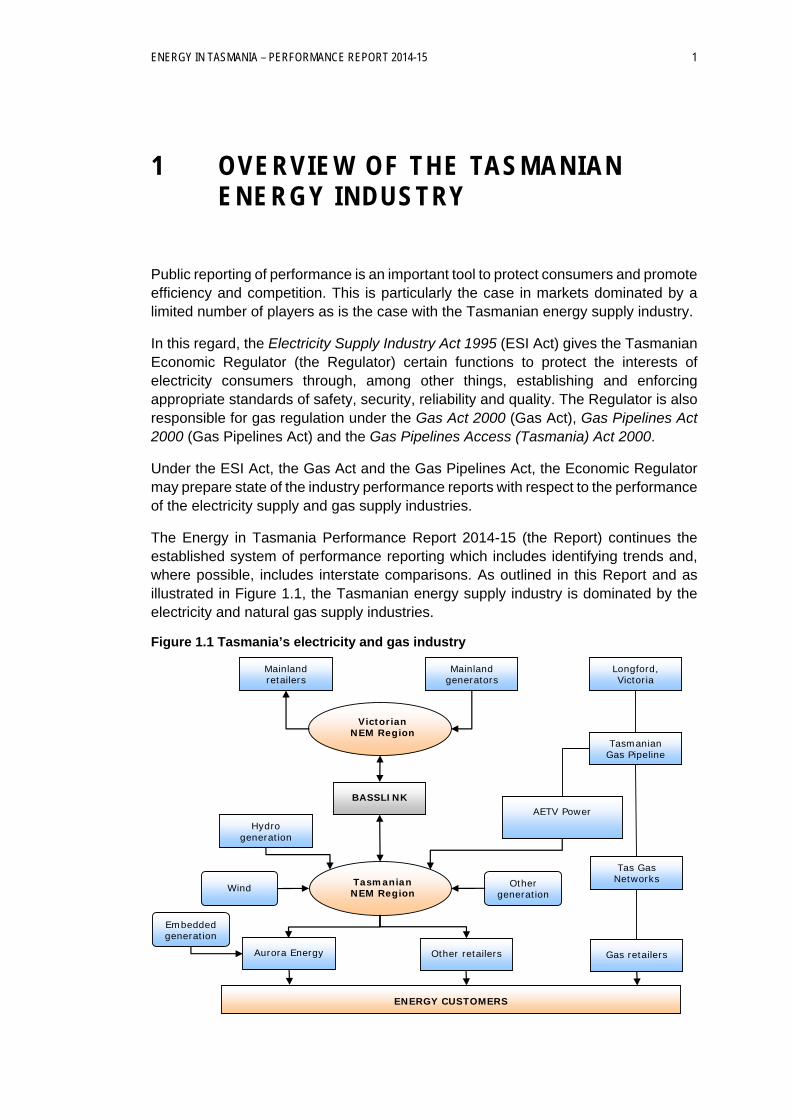

The Energy in Tasmania Performance Report 2014-15 (the Report) continues the established system of performance reporting which includes identifying trends and, where possible, includes interstate comparisons. As outlined in this Report and as illustrated in Figure 1.1, the Tasmanian energy supply industry is dominated by the electricity and natural gas supply industries.

Figure 1.1 Tasmania’s electricity and gas industry

Mainland retailers

Mainland generators

Longford, Victoria

Victorian NEM Region

Tasmanian Gas Pipeline

BASSLINK

Hydro generation

AETV Power

Tas Gas Networks

Gas retailers Other retailers Aurora Energy

Tasmanian NEM Region

ENERGY CUSTOMERS

Wind Other generation

Embedded generation

2 ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15

The Report also includes sections, prepared by the Department of State Growth, in relation to other fuel sources namely petroleum, coal and wood. The Economic Regulator does not have any regulatory role in relation to these additional fuel sources.

The Report, therefore, aims to provide consumers with a comprehensive review of the performance of the Tasmanian energy industry, covering all major energy sources used in Tasmania.

The energy supply industry is of fundamental importance to the Tasmanian economy. The price and reliability of energy supplied impacts significantly on the economic performance of other sectors of the Tasmanian economy. In addition, it provides employment, generates investment, and contributes to the State Budget by way of taxes and returns to owners (ie income tax equivalent payments, guarantee fees and dividends). More details about the respective contributions made by the electricity, gas and other fuel source industries to the Tasmanian economy are outlined in Appendix 1.

The energy supply industry in Tasmania is also exposed to national and international economic developments. With the Basslink electricity interconnector, the gas transmission pipeline, and greater sea and air access, Tasmania's economy has become more closely integrated with the Australian mainland economy. State economic performance and, to a lesser degree, growth in population and household expenditure, also have an impact on aggregate energy usage and on the economic performance of the energy supply industry.

In this regard, Chapter 2 of this Report outlines Tasmanian energy consumption during 2014-15 and presents an overview of Tasmanian energy demand and the contributions made by the various energy sources to the amount of energy consumed during 2014-15.

The balance of the Report (with the exception of the chapters on other fuels) presents the Economic Regulator’s assessment of the performance during 2014-15 of the various entities involved in the electricity supply and gas supply industries.

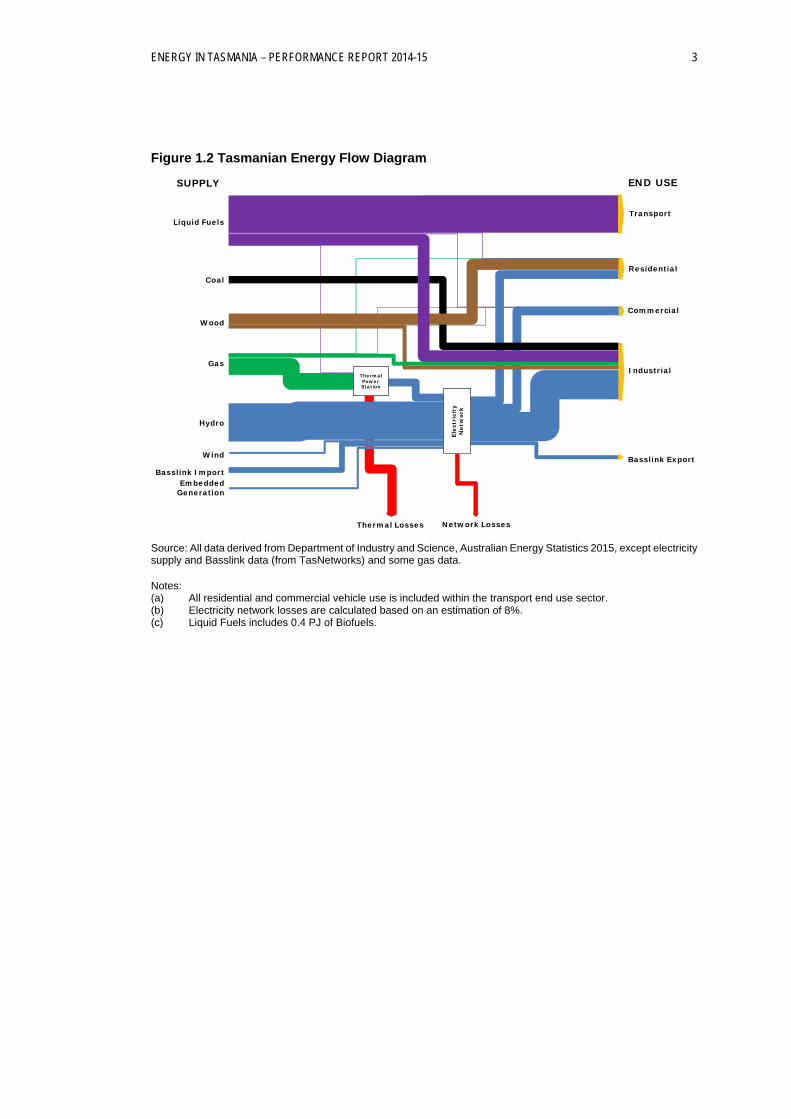

To provide further context for the remainder of this Report, Figure 1.2 reflects the various Tasmanian energy flows from supply sectors to end use sectors. The relative contribution of each flow in terms of both supply and end use is indicated by the thickness of the respective lines.

ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15 3

Figure 1.2 Tasmanian Energy Flow Diagram

Source: All data derived from Department of Industry and Science, Australian Energy Statistics 2015, except electricity supply and Basslink data (from TasNetworks) and some gas data.

Notes: (a) All residential and commercial vehicle use is included within the transport end use sector. (b) Electricity network losses are calculated based on an estimation of 8%. (c) Liquid Fuels includes 0.4 PJ of Biofuels.

ThermalPower Station

Elec

tric

ity

Net

wor

k

Transport

Residential

Commercial

Industrial

Basslink Export

Network LossesThermal Losses

Liquid Fuels

Coal

Wood

Gas

Hydro

Wind

Basslink ImportEmbedded

Generation

SUPPLY END USE

ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15 5

2 ENERGY CONSUMPTION IN TASMANIA

2.1 Introduction

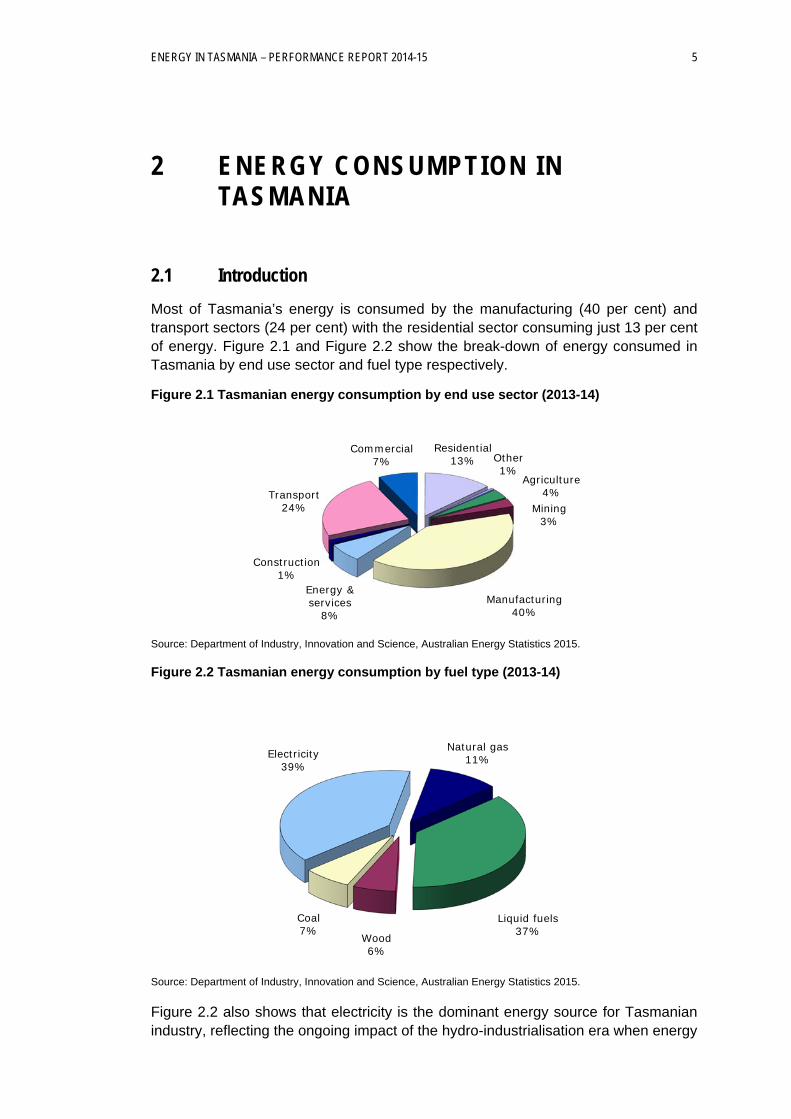

Most of Tasmania’s energy is consumed by the manufacturing (40 per cent) and transport sectors (24 per cent) with the residential sector consuming just 13 per cent of energy. Figure 2.1 and Figure 2.2 show the break-down of energy consumed in Tasmania by end use sector and fuel type respectively.

Figure 2.1 Tasmanian energy consumption by end use sector (2013-14)

Source: Department of Industry, Innovation and Science, Australian Energy Statistics 2015.

Figure 2.2 Tasmanian energy consumption by fuel type (2013-14)

Source: Department of Industry, Innovation and Science, Australian Energy Statistics 2015.

Figure 2.2 also shows that electricity is the dominant energy source for Tasmanian industry, reflecting the ongoing impact of the hydro-industrialisation era when energy

Agriculture4%

Mining3%

Manufacturing40%

Energy & services

8%

Construction1%

Transport24%

Commercial7%

Residential13% Other

1%

Liquid fuels37%Wood

6%

Coal7%

Electricity39%

Natural gas11%

6 ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15

intensive industries such as aluminium, manganese and zinc smelting and paper and cement manufacturing were established in Tasmania.

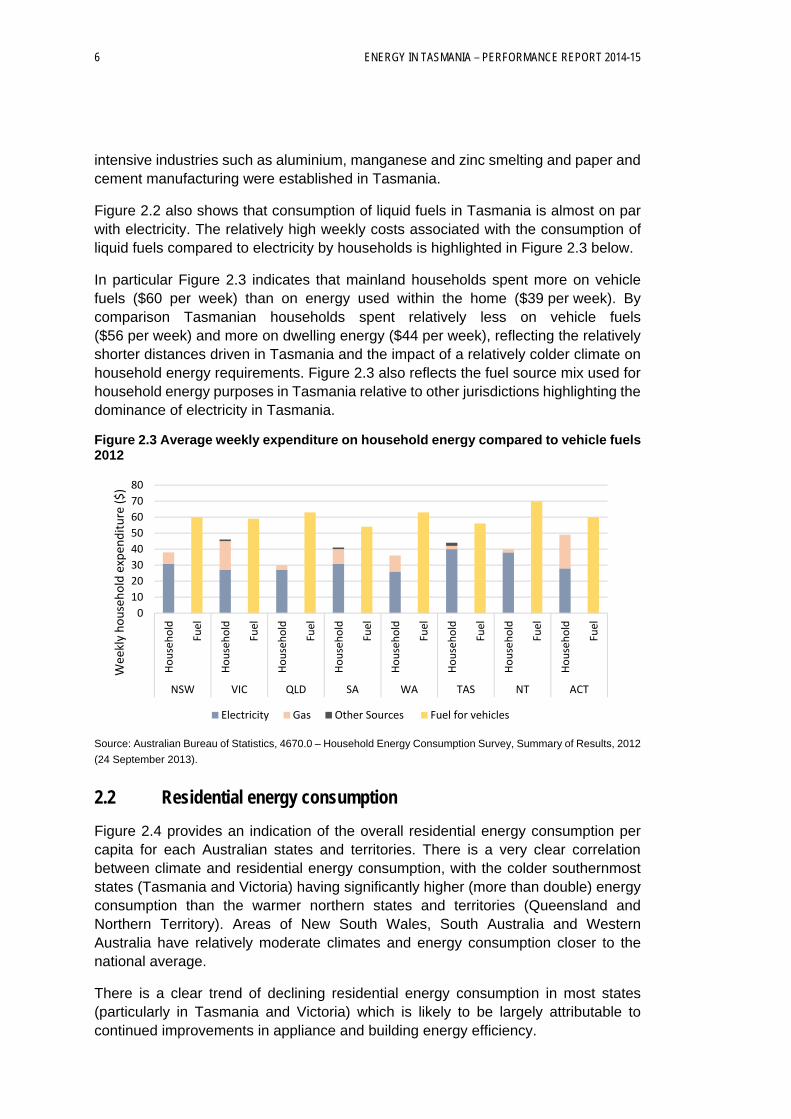

Figure 2.2 also shows that consumption of liquid fuels in Tasmania is almost on par with electricity. The relatively high weekly costs associated with the consumption of liquid fuels compared to electricity by households is highlighted in Figure 2.3 below.

In particular Figure 2.3 indicates that mainland households spent more on vehicle fuels ($60 per week) than on energy used within the home ($39 per week). By comparison Tasmanian households spent relatively less on vehicle fuels ($56 per week) and more on dwelling energy ($44 per week), reflecting the relatively shorter distances driven in Tasmania and the impact of a relatively colder climate on household energy requirements. Figure 2.3 also reflects the fuel source mix used for household energy purposes in Tasmania relative to other jurisdictions highlighting the dominance of electricity in Tasmania.

Figure 2.3 Average weekly expenditure on household energy compared to vehicle fuels 2012

Source: Australian Bureau of Statistics, 4670.0 – Household Energy Consumption Survey, Summary of Results, 2012

(24 September 2013).

2.2 Residential energy consumption

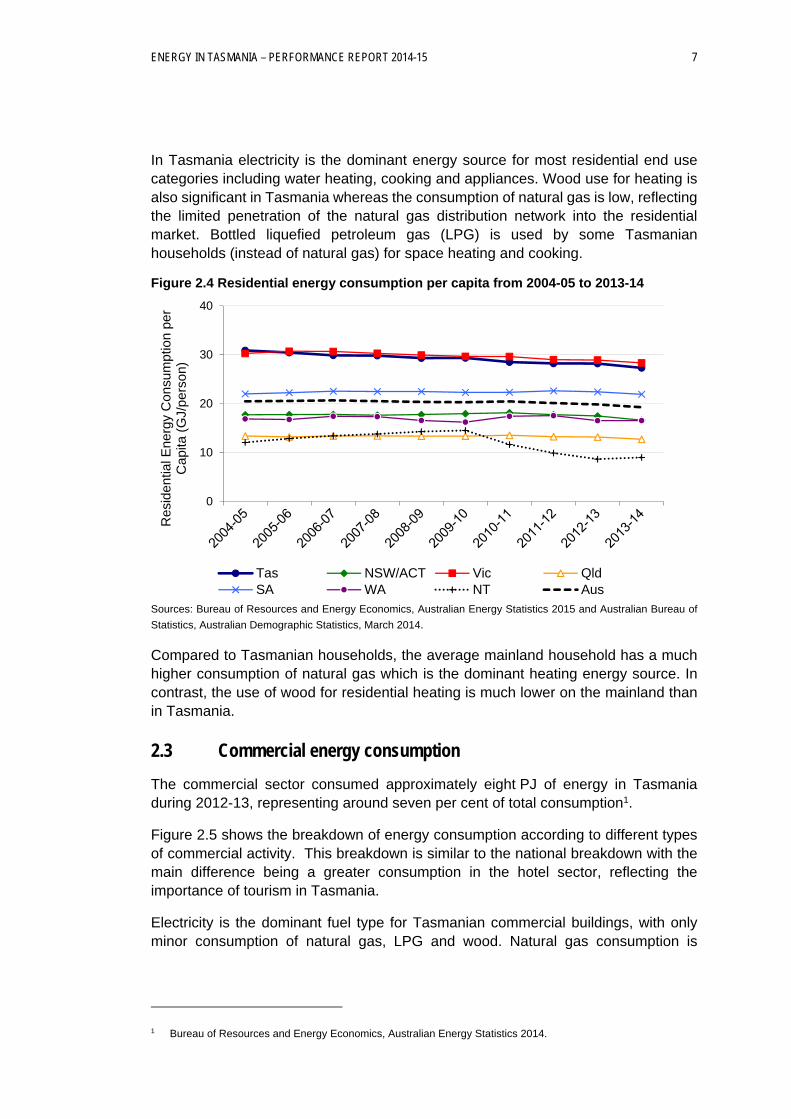

Figure 2.4 provides an indication of the overall residential energy consumption per capita for each Australian states and territories. There is a very clear correlation between climate and residential energy consumption, with the colder southernmost states (Tasmania and Victoria) having significantly higher (more than double) energy consumption than the warmer northern states and territories (Queensland and Northern Territory). Areas of New South Wales, South Australia and Western Australia have relatively moderate climates and energy consumption closer to the national average.

There is a clear trend of declining residential energy consumption in most states (particularly in Tasmania and Victoria) which is likely to be largely attributable to continued improvements in appliance and building energy efficiency.

0

10

20

30

40

50

60

70

80

Household

Fuel

Household

Fuel

Household

Fuel

Household

Fuel

Household

Fuel

Household

Fuel

Household

Fuel

Household

Fuel

NSW VIC QLD SA WA TAS NT ACT

Weekly household expen

diture ($)

Electricity Gas Other Sources Fuel for vehicles

ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15 7

In Tasmania electricity is the dominant energy source for most residential end use categories including water heating, cooking and appliances. Wood use for heating is also significant in Tasmania whereas the consumption of natural gas is low, reflecting the limited penetration of the natural gas distribution network into the residential market. Bottled liquefied petroleum gas (LPG) is used by some Tasmanian households (instead of natural gas) for space heating and cooking.

Figure 2.4 Residential energy consumption per capita from 2004-05 to 2013-14

Sources: Bureau of Resources and Energy Economics, Australian Energy Statistics 2015 and Australian Bureau of

Statistics, Australian Demographic Statistics, March 2014.

Compared to Tasmanian households, the average mainland household has a much higher consumption of natural gas which is the dominant heating energy source. In contrast, the use of wood for residential heating is much lower on the mainland than in Tasmania.

2.3 Commercial energy consumption

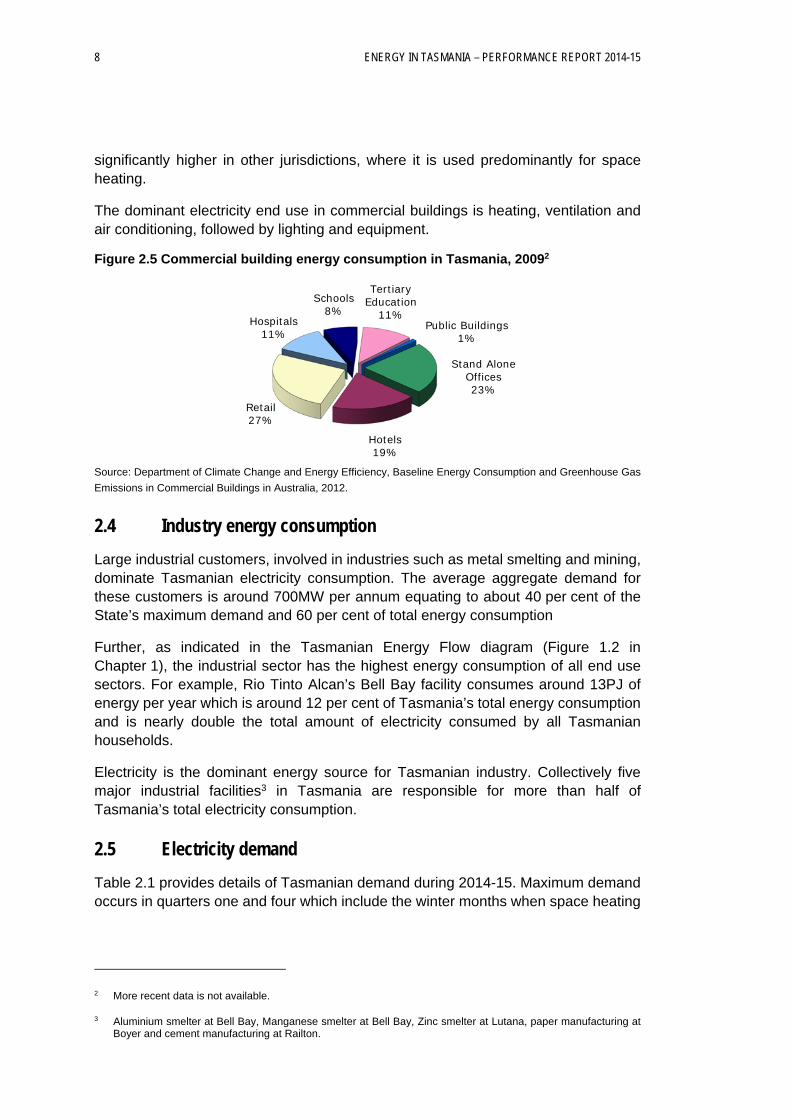

The commercial sector consumed approximately eight PJ of energy in Tasmania during 2012-13, representing around seven per cent of total consumption1.

Figure 2.5 shows the breakdown of energy consumption according to different types of commercial activity. This breakdown is similar to the national breakdown with the main difference being a greater consumption in the hotel sector, reflecting the importance of tourism in Tasmania.

Electricity is the dominant fuel type for Tasmanian commercial buildings, with only minor consumption of natural gas, LPG and wood. Natural gas consumption is

1 Bureau of Resources and Energy Economics, Australian Energy Statistics 2014.

0

10

20

30

40

Res

iden

tial E

nerg

y C

onsu

mpt

ion

per

Cap

ita (

GJ/

pers

on)

Tas NSW/ACT Vic QldSA WA NT Aus

8 ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15

significantly higher in other jurisdictions, where it is used predominantly for space heating.

The dominant electricity end use in commercial buildings is heating, ventilation and air conditioning, followed by lighting and equipment.

Figure 2.5 Commercial building energy consumption in Tasmania, 20092

Source: Department of Climate Change and Energy Efficiency, Baseline Energy Consumption and Greenhouse Gas

Emissions in Commercial Buildings in Australia, 2012.

2.4 Industry energy consumption

Large industrial customers, involved in industries such as metal smelting and mining, dominate Tasmanian electricity consumption. The average aggregate demand for these customers is around 700MW per annum equating to about 40 per cent of the State’s maximum demand and 60 per cent of total energy consumption

Further, as indicated in the Tasmanian Energy Flow diagram (Figure 1.2 in Chapter 1), the industrial sector has the highest energy consumption of all end use sectors. For example, Rio Tinto Alcan’s Bell Bay facility consumes around 13PJ of energy per year which is around 12 per cent of Tasmania’s total energy consumption and is nearly double the total amount of electricity consumed by all Tasmanian households.

Electricity is the dominant energy source for Tasmanian industry. Collectively five major industrial facilities3 in Tasmania are responsible for more than half of Tasmania’s total electricity consumption.

2.5 Electricity demand

Table 2.1 provides details of Tasmanian demand during 2014-15. Maximum demand occurs in quarters one and four which include the winter months when space heating

2 More recent data is not available.

3 Aluminium smelter at Bell Bay, Manganese smelter at Bell Bay, Zinc smelter at Lutana, paper manufacturing at Boyer and cement manufacturing at Railton.

Stand Alone Offices23%

Hotels19%

Retail27%

Hospitals11%

Schools8%

Tertiary Education

11%Public Buildings

1%

ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15 9

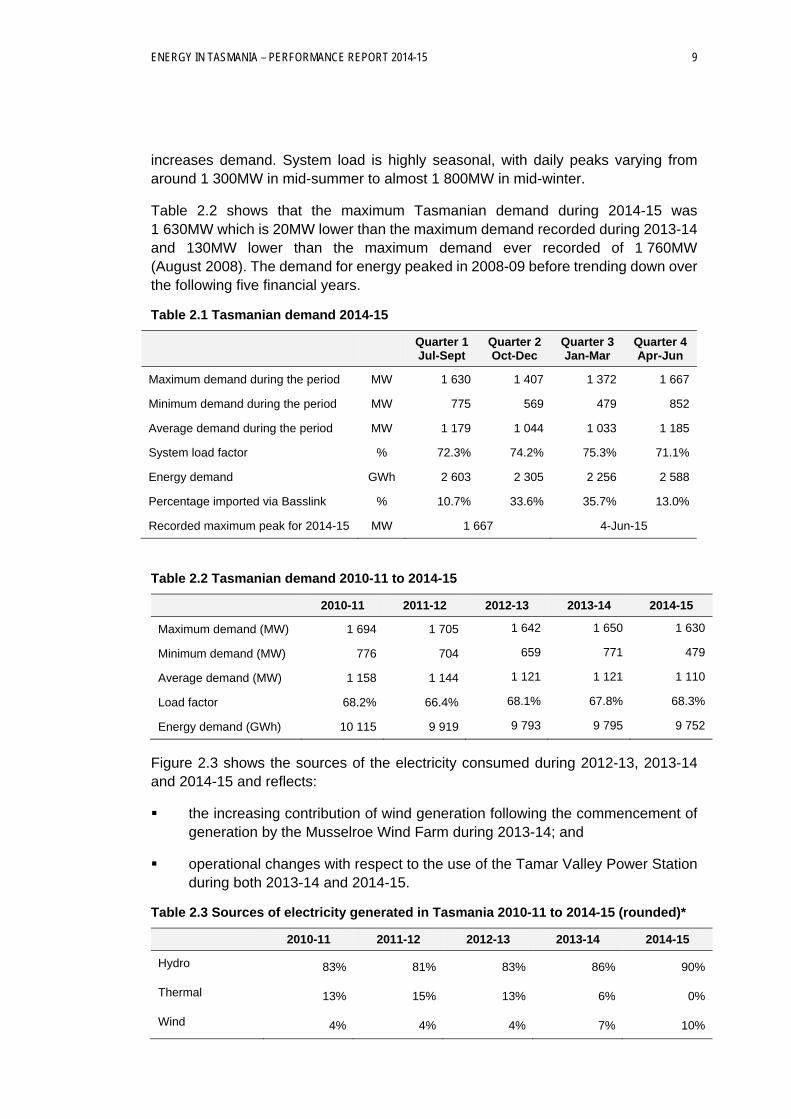

increases demand. System load is highly seasonal, with daily peaks varying from around 1 300MW in mid-summer to almost 1 800MW in mid-winter.

Table 2.2 shows that the maximum Tasmanian demand during 2014-15 was 1 630MW which is 20MW lower than the maximum demand recorded during 2013-14 and 130MW lower than the maximum demand ever recorded of 1 760MW (August 2008). The demand for energy peaked in 2008-09 before trending down over the following five financial years.

Table 2.1 Tasmanian demand 2014-15

Quarter 1 Jul-Sept

Quarter 2 Oct-Dec

Quarter 3 Jan-Mar

Quarter 4 Apr-Jun

Maximum demand during the period MW 1 630 1 407 1 372 1 667

Minimum demand during the period MW 775 569 479 852

Average demand during the period MW 1 179 1 044 1 033 1 185

System load factor % 72.3% 74.2% 75.3% 71.1%

Energy demand GWh 2 603 2 305 2 256 2 588

Percentage imported via Basslink % 10.7% 33.6% 35.7% 13.0%

Recorded maximum peak for 2014-15 MW 1 667 4-Jun-15

Table 2.2 Tasmanian demand 2010-11 to 2014-15

2010-11 2011-12 2012-13 2013-14 2014-15

Maximum demand (MW) 1 694 1 705 1 642 1 650 1 630

Minimum demand (MW) 776 704 659 771 479

Average demand (MW) 1 158 1 144 1 121 1 121 1 110

Load factor 68.2% 66.4% 68.1% 67.8% 68.3%

Energy demand (GWh) 10 115 9 919 9 793 9 795 9 752

Figure 2.3 shows the sources of the electricity consumed during 2012-13, 2013-14 and 2014-15 and reflects:

the increasing contribution of wind generation following the commencement of generation by the Musselroe Wind Farm during 2013-14; and

operational changes with respect to the use of the Tamar Valley Power Station during both 2013-14 and 2014-15.

Table 2.3 Sources of electricity generated in Tasmania 2010-11 to 2014-15 (rounded)*

2010-11 2011-12 2012-13 2013-14 2014-15

Hydro 83% 81% 83% 86% 90%

Thermal 13% 15% 13% 6% 0%

Wind 4% 4% 4% 7% 10%

10 ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15

*excludes Basslink imports and solar PV

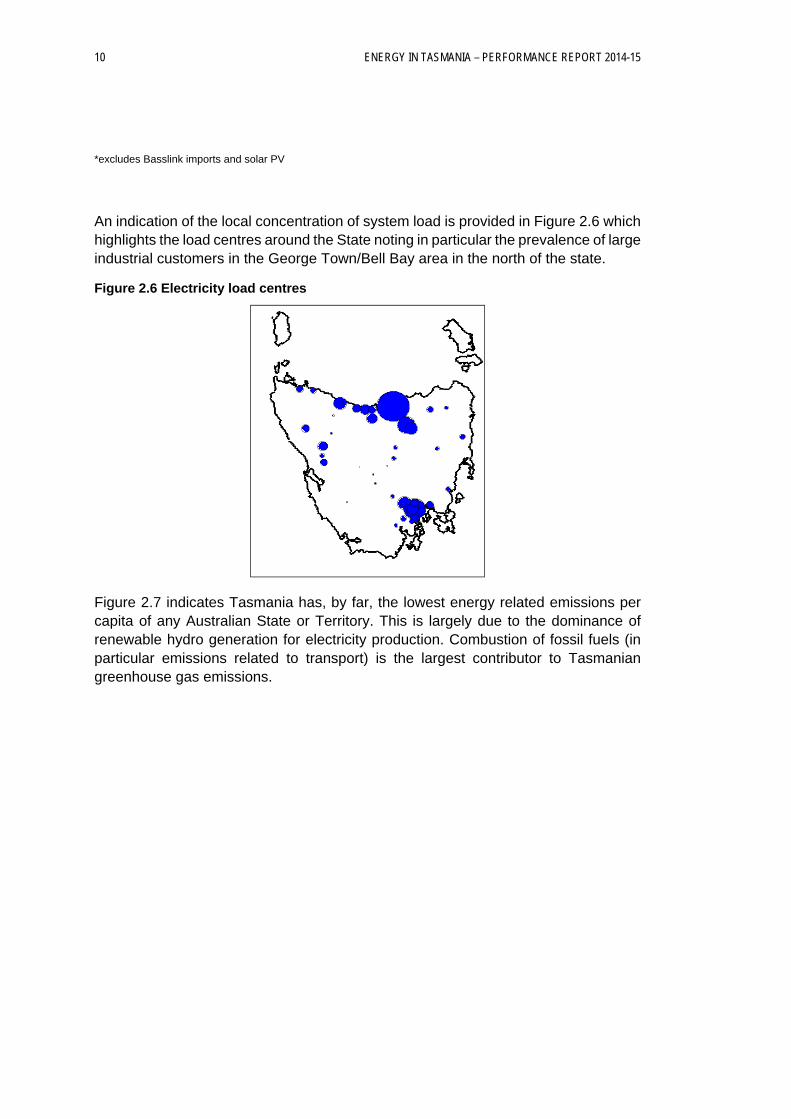

An indication of the local concentration of system load is provided in Figure 2.6 which highlights the load centres around the State noting in particular the prevalence of large industrial customers in the George Town/Bell Bay area in the north of the state.

Figure 2.6 Electricity load centres

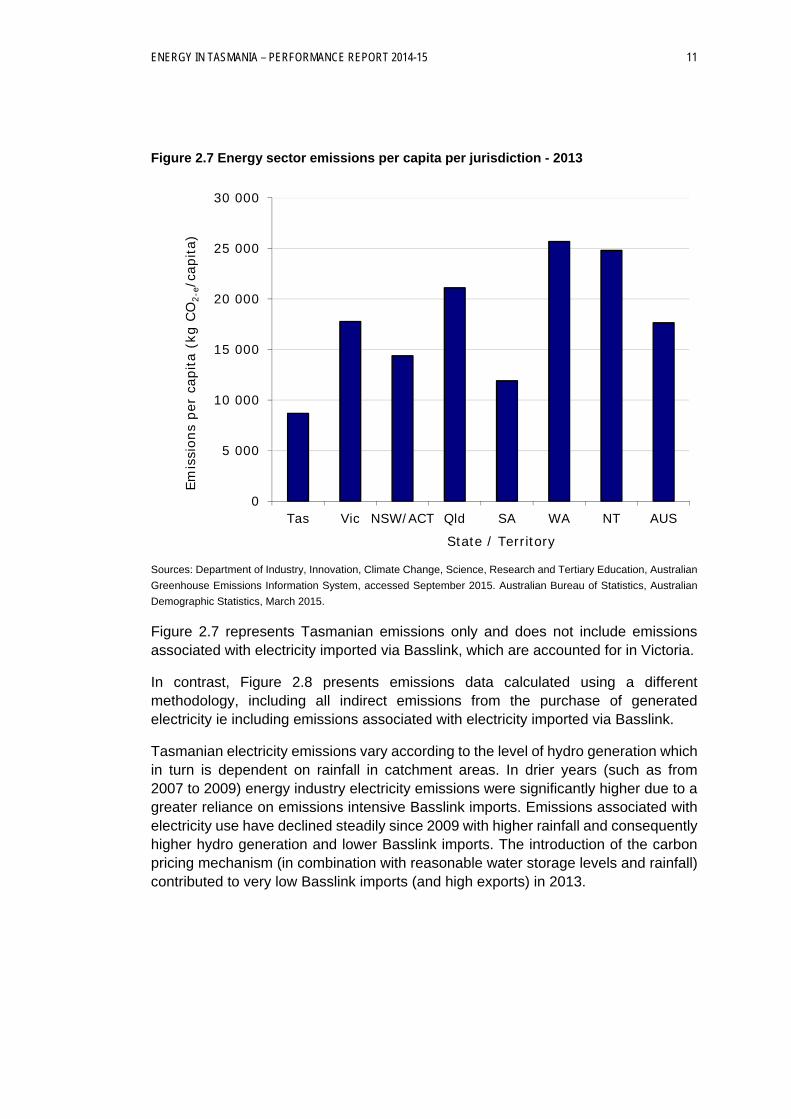

Figure 2.7 indicates Tasmania has, by far, the lowest energy related emissions per capita of any Australian State or Territory. This is largely due to the dominance of renewable hydro generation for electricity production. Combustion of fossil fuels (in particular emissions related to transport) is the largest contributor to Tasmanian greenhouse gas emissions.

273

ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15 11

Figure 2.7 Energy sector emissions per capita per jurisdiction - 2013

Sources: Department of Industry, Innovation, Climate Change, Science, Research and Tertiary Education, Australian

Greenhouse Emissions Information System, accessed September 2015. Australian Bureau of Statistics, Australian

Demographic Statistics, March 2015.

Figure 2.7 represents Tasmanian emissions only and does not include emissions associated with electricity imported via Basslink, which are accounted for in Victoria.

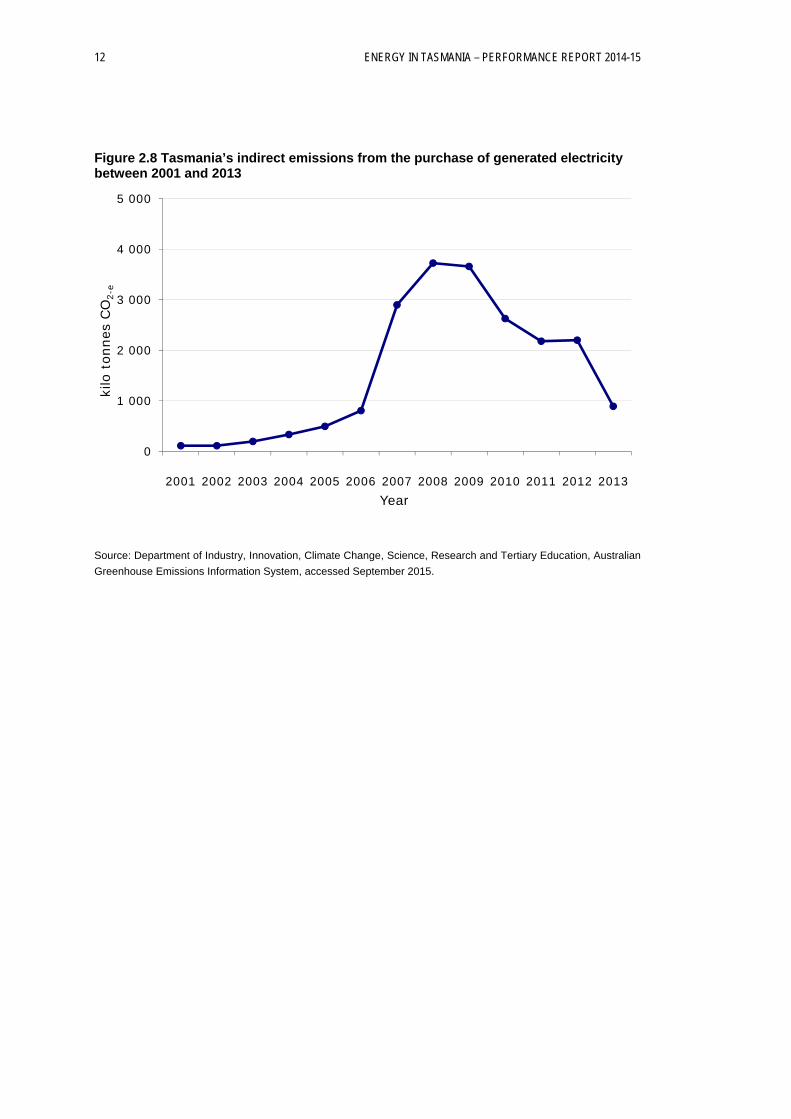

In contrast, Figure 2.8 presents emissions data calculated using a different methodology, including all indirect emissions from the purchase of generated electricity ie including emissions associated with electricity imported via Basslink.

Tasmanian electricity emissions vary according to the level of hydro generation which in turn is dependent on rainfall in catchment areas. In drier years (such as from 2007 to 2009) energy industry electricity emissions were significantly higher due to a greater reliance on emissions intensive Basslink imports. Emissions associated with electricity use have declined steadily since 2009 with higher rainfall and consequently higher hydro generation and lower Basslink imports. The introduction of the carbon pricing mechanism (in combination with reasonable water storage levels and rainfall) contributed to very low Basslink imports (and high exports) in 2013.

0

5 000

10 000

15 000

20 000

25 000

30 000

Tas Vic NSW/ACT Qld SA WA NT AUS

Emis

sion

s pe

r ca

pita

(kg

CO

2-e/

capi

ta)

State / Territory

12 ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15

Figure 2.8 Tasmania’s indirect emissions from the purchase of generated electricity between 2001 and 2013

Source: Department of Industry, Innovation, Climate Change, Science, Research and Tertiary Education, Australian

Greenhouse Emissions Information System, accessed September 2015.

0

1 000

2 000

3 000

4 000

5 000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

kilo

ton

nes

CO

2-e

Year

ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15 13

3 OVERVIEW OF THE TASMANIAN ELECTRICITY SUPPLY INDUSTRY

3.1 Introduction

This Chapter provides an overview of the electricity supply industry in Tasmanian together with details of the current industry participants.

3.2 Industry structure and participants

The Tasmanian electricity supply industry comprises the generation, transmission, distribution and retail sectors. The Tasmanian generation and retail sectors are open to competition whilst transmission and distribution services are provided by a privately owned entity and a Government owned utility. The key participants as at 30 June 2015 were as follows:

The major electricity generator in Tasmania is Hydro Tasmania, a Government Business Enterprise that holds a licence for electricity generation in Tasmania as well as responsibility for generation, distribution and retailing on King and Flinders Islands – the ‘Bass Strait Islands’ (BSI).

Hydro Tasmania also owns and operates the gas-fired Tamar Valley Power Station (TVPS).

Hydro Tasmania also partly owns and operates the wind farms at Studland Bay and Bluff Point (collectively known as Woolnorth) and the Musselroe wind farm.

Hydro Tasmania sells the electricity it generates from its Tasmanian mainland operations in the National Electricity Market.

Hydro Tasmania's Ministerial Charter is intended to ensure that the reliability and security of the State's hydro system is maintained.

TasNetworks, a State-owned Company (SOC) operating under Corporations Law, provides transmission and distribution services on mainland Tasmania. TasNetworks distribution and transmission services are subject to economic regulation by the Australian Energy Regulator (AER).

Basslink Pty Ltd, a wholly owned subsidiary of the Keppel Infrastructure Trust, owns and operates the Bass Strait interconnector. Basslink Pty Ltd is classified as a transmission network service provider (TNSP) under the National Electricity Market (NEM).

Aurora Energy Pty Ltd (Aurora Energy), a SOC operating under Corporations Law, holds a retail authorisation for mainland Tasmania and is also the

14 ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15

regulated offer retailer for Tasmania and the “retailer of last resort” (RoLR)1. As the regulated offer retailer for the Tasmania jurisdiction Aurora Energy is required to supply electricity at Standing Offer prices to small customers (ie those consuming less than 150 MWh per annum) on mainland Tasmania.

ERM Power Retail Pty Ltd and by Progressive Green Pty Ltd are also authorised retailers and provide retail services to Tasmanian customers.

1 Under the National Electricity Customer Framework (NECF) scheme, the RoLR is required to ensure ongoing supply to consumers in cases where a retailer unexpectedly exits the industry.

ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15 15

4 ELECTRICITY REGULATION

4.1 Introduction

This chapter provides an overview of the regulatory framework for the Tasmanian electricity supply industry. The framework is a combination of national and jurisdictional arrangements.

All states and territories signed the Australian Energy Market Agreement (AEMA) in 2004, which outlined the intended functions and powers of the Australian Energy Regulator (AER) and the Australian Energy Market Commission (AEMC), as well as those functions that would remain with state and territory regulators.

In 2007, the Council of Australian Governments (COAG) agreed to establish a single, industry-funded national energy market operator for both electricity and gas - the Australian Energy Market Operator (AEMO)1, to provide energy market governance on a national basis. With respect to electricity, AEMO took over former NEMMCO functions.

COAG also established the Standing Council on Energy and Resources2 (SCER) which was replaced by the COAG Energy Council in December 2013. The COAG Energy Council’s focus is on developing an integrated and coherent national energy policy.

4.2 Legislative and regulatory framework

The National Electricity Law (NEL) and National Electricity Rules (NER) provide the overarching national regulatory framework for the electricity industry. However, many complementary state-based regulatory instruments remain.

The Economic Regulator Act 2009 (ER Act) created an independent Tasmanian Economic Regulator with responsibility under the Electricity Supply Industry Act 1995 (ESI Act) for regulating the Tasmanian electricity supply industry3.

The ESI Act also requires the Regulator to issue the Tasmanian Electricity Code (TEC). The TEC was based largely on the then National Electricity Code (NEC) but has been amended significantly following subsequent state and national reforms to the electricity supply industry.

1 For information on the history of AEMO, please see www.aemo.com.au

2 SCER replaced the Ministerial Council on Energy.

3 From 1 July 2015, the three person Tasmanian Economic Regulator Board was replaced and a single Tasmanian Economic Regulator appointed in accordance with legislative amendments introduced following the Government’s review of the Regulator’s role and functions. See section 5.5of this Report for further details.

16 ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15

On 1 July 2012 the National Energy Customer Framework (NECF) commenced in Tasmania with the AER assuming responsibility for authorising retailers operating in Tasmania4.

The NECF is a legislative package, comprising the National Energy Retail Law (NERL) and the National Energy Retail Rules (NERR) that implements the remainder of the national energy reforms agreed to between jurisdictions. The NECF also facilitates the transition to the national regulation of energy markets. Specifically, the NECF transfers consumer protection functions such as minimum contract terms and conditions and customer protection from state jurisdictions to the AER. However, the Regulator continues to be responsible for price regulation of standing offer prices (see Chapter 5).

The NECF introduced a new set of national laws, rules, and regulations governing the retail sale of energy to consumers. Due to changed reporting requirements for retailers under the NECF the Regulator no longer reports on retail electricity consumption.

Although under the NECF the AER is responsible for regulating energy retailers, retailers authorised to sell electricity under the NERL who operate in Tasmania also have obligations under the following Tasmanian legislation in addition to those under the National Energy Retail Law (Tasmania) Act:

Electricity Supply Industry Regulations 2008;

Electricity Supply Industry (Customer) Regulations 2012; and

Electricity Supply Industry (Pricing and Related Matters) Regulations 2013.

Full retail contestability for residential and business customers was introduced on 1 July 2014. Further information on the NECF and retail market reforms can be found on the AER’s website at www.aer.gov.au and the AEMC’s website at www.aemc.gov.au.

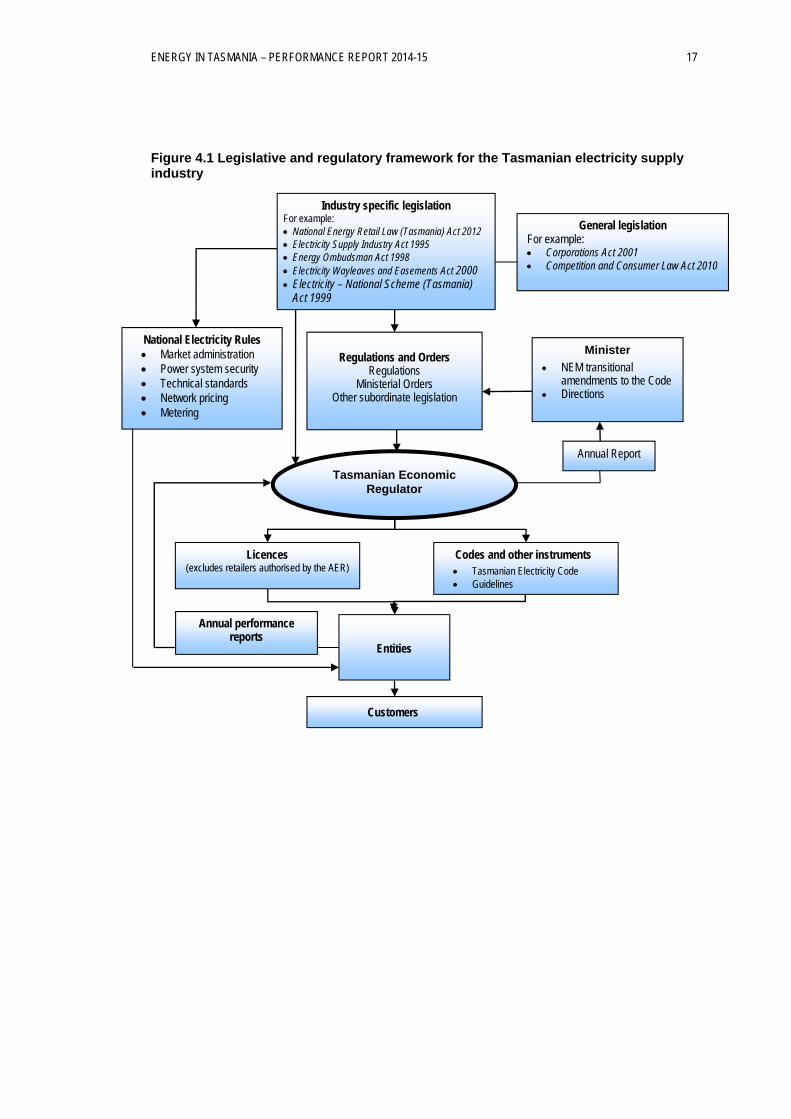

Figure 4.1 provides a schematic representation of the legislative and regulatory framework governing the Tasmanian electricity supply industry.

4 The AER had been responsible for the regulation of transmission services since 2009.

ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15 17

Figure 4.1 Legislative and regulatory framework for the Tasmanian electricity supply industry

Regulations and Orders Regulations

Ministerial Orders Other subordinate legislation

Minister

NEM transitional amendments to the Code

Directions

Tasmanian Economic Regulator

National Electricity Rules Market administration Power system security Technical standards Network pricing Metering

Licences (excludes retailers authorised by the AER)

Entities

Annual performance reports

Customers

Codes and other instruments Tasmanian Electricity Code Guidelines

General legislation For example: Corporations Act 2001 Competition and Consumer Law Act 2010

Industry specific legislation For example: National Energy Retail Law (Tasmania) Act 2012 Electricity Supply Industry Act 1995 Energy Ombudsman Act 1998 Electricity Wayleaves and Easements Act 2000 Electricity – National Scheme (Tasmania)

Act 1999

Annual Report

ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15 19

5 REGULATORY BODIES

5.1 Introduction

This Chapter provides a description of the National and Tasmanian regulatory bodies involved in regulating the Tasmanian energy supply industry and outlines their respective roles and functions.

5.2 Australian Energy Market Commission

The AEMC was established as a national independent body in 2005, in accordance with the Australian Energy Market Agreement (AEMA).

The AEMC is responsible for market development and providing advice to relevant organisations in relation to the NEM.

The AEMC also makes rules under the National Electricity Law, the National Gas Law and the National Energy Retail Law. These rules cover areas such as participation in the wholesale spot market for electricity and similar markets for gas, economic regulation of network services and energy-specific consumer protections. The AEMC does not have any regulatory enforcement responsibilities and is unable to initiate rule changes itself other than those of a minor administrative nature1.

The AEMC’s Reliability Panel (established by the AEMC under the National Electricity Law):

monitors, reviews and reports on the safety, security and reliability of the national electricity system, in accordance with the NER;

at the request of the AEMC, provides advice in relation to the safety, security and reliability of the national electricity system; and

manages and executes any other functions or powers conferred on it under the Law and the Rules.

The Reliability Panel sets the frequency standards for Tasmanian. Although Tasmania is a participating jurisdiction in the NEM, the Tasmanian power system is not synchronised with the mainland’s power system due to the Basslink interconnector being an asynchronous direct current (DC) connection. As a result, the frequency operating standards adopted in Tasmania allow for wider variations than their NEM mainland equivalents. The significantly wider standards recognise that a large number of installed hydroelectric generators are unable to change their output rapidly therefore relatively large fluctuations in power can occur in Tasmania

1 For further information on the AEMC, please see www.aemc.gov.au

20 ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15

(compared to the mainland) from the operations of large industrial users, generator trips, transmission line trips and power transfers over Basslink.

The Reliability Panel has set Tasmanian frequency standards that specify the normal operating frequency band (49.85 to 50.15 Hz) for the power system and the duration and circumstances in which the frequency is allowed to deviate from that frequency band (eg if a contingency or load event occurs).

A system protection scheme (SPS) was constructed in conjunction with Basslink to manage network contingencies or an outage on Basslink. The SPS encompasses two parts; the Frequency Control System Protection Scheme (FCSPS) and the Network Control System Protection Scheme (NCSPS).

The FCSPS is designed to ensure that, following the loss of Basslink, the Tasmanian frequency remains within the standards by initiating load shedding by contracted customers or increased or decreased output from contracted generators.

The NCSPS facilitates higher power transfers from Tasmania to Victoria via Basslink by allowing selected transmission lines in Tasmania to transfer power up to 95 per cent of their continuous ratings under normal system conditions, prior to the occurrence of a transmission contingency. For more information on the NCSPS refer to pages 137-8 of the 2011-12 Energy in Tasmania report.

The Tasmanian Economic Regulator has a Memorandum of Understanding with the AEMC to facilitate the sharing of relevant information, cooperation and coordination between the organisations.

5.3 Australian Energy Regulator

The AER is a statutory body established in 2005 and funded by the Australian Government. Although the AER is part of the ACCC it operates as a separate legal entity. The AER is accountable to governments and market participants through consultation, reporting, transparent obligations and accessible avenues of appeal against regulatory decisions.

The AER exercises powers under a national energy legislative framework which, for electricity, includes the NEL, the NECF and associated rules and sector specific regulatory functions. It is responsible for the regulation of the electricity wholesale market and economic regulation of electricity and gas transmission and distribution networks. As such, the AER is responsible for the economic regulation of TasNetworks’ distribution and transmission services. The AER's determination specifies the revenues, prices and levels of service in respect of those services2.

2 TasNetworks was formed on 1 July 2014 following a merger between Aurora Energy’s distribution network and Transend’s transmission network. As a result, while Aurora Energy (as a distributor) submitted the regulatory proposal to the AER for the distribution network, the AER’s subsequent determination applies to TasNetworks.

ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15 21

5.4 Australian Energy Market Operator

The AEMO was created in 2009 by COAG to manage the NEM and gas markets. It is an independent, member-based organisation with membership split 60/40 between government and industry. Government members of AEMO include the state governments of Queensland, New South Wales, Victoria, South Australia and Tasmania, the Australian Capital Territory and the Commonwealth. Private members include Australia’s major energy generators, wholesalers and retailers.

In relation to electricity, AEMO is responsible for:

power system operation and market operation;

national transmission planning;

monitoring transmission services; and

facilitating energy market development.

AEMO’s functions are set out in the NEL while the NER prescribes all procedures and processes for market operations, power system security, network connection and access, pricing for network services in the NEM and national transmission planning.

In its power system security role, AEMO is responsible for:

ensuring that the power system is operated in a safe, secure and reliable manner; and

emergency management in respect to the power system.

To ensure that key technical characteristics of the power system such as frequency, network loading and voltage are maintained within prescribed limits AEMO operates an ancillary services market. More details about ancillary services are set out in Chapter 7 (Generation).

AEMO exercises its emergency management responsibilities under an agreed framework in all NEM jurisdictions (Tasmania, Victoria, South Australia, Australian Capital Territory, New South Wales and Queensland) known as the Power System Emergency Management Plan (PSEMP).

There are also a number of other national plans in relation to emergency management:

the National Gas Emergency Response Protocol; and

the National Liquid Fuel Emergency Response Plan.

Tasmania has committed to aligning its emergency management procedures with these national plans through memoranda of understanding with the mainland jurisdictions.

There are currently a number of committees in Tasmania that deal with emergency management issues in relation to the energy supply industry. At the time of writing,

22 ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15

the Department of State Growth was reviewing the roles and functions of these committees.

5.5 Tasmanian Economic Regulator

5.5.1 Overview

With the exception of specific legislative provisions, the Economic Regulator is not subject to Ministerial direction and therefore operates independently from the Tasmanian Government.

The Electricity Supply Industry Act 1995 (ESI Act) gives the Economic Regulator certain functions to protect the interests of electricity consumers by, among other things, establishing and enforcing appropriate standards of safety, security, reliability and quality.

During 2014-15, the structure of the Economic Regulator and its role and functions changed as a result of the introduction of changes in the Economic Regulator Amendment Act 2015 (the Amendment Act). The Amendment Act was based on the outcomes from the Government’s review of the Economic Regulator’s role and functions and made a number of consequential amendments to the industry specific acts that govern the Economic Regulator’s operations.

In terms of the Economic Regulator Act 2009 (ER Act) and the Economic Regulator itself, the Amendment Act:

reduced the membership of the Economic Regulator from a three person panel to a single person with the capacity to appoint an Assistant Economic Regulator for specific functions if required;

provided for the capacity to appoint an Acting Economic Regulator in instances where the Regulator is indisposed;

required that all appointments are to be made by the Minister responsible for the ER Act; and

allowed for the appointment of the Economic Regulator to be external to the State Service.

With respect to electricity, the Amendment Act required the Economic Regulator to:

prepare an energy industry performance report on its own initiative, or if directed to by the Energy Minister with the agreement of the Minister responsible for the ER Act (ie the Treasurer);

prepare interstate electricity price comparisons on its own initiative or if directed to by the Minister responsible for the pricing-related provisions in the ESI Act, with agreement from the Minister responsible for the ER Act;

produce annual comparisons of Aurora Pay as You Go (APAYG) and standard tariff prices for electricity customers in Tasmania; and

ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15 23

prepare a report on Tasmania’s electricity network reliability every three years or more frequently at the Regulator’s own initiative or if directed to by the Energy Minister, with the agreement of the Minister responsible for the ER Act.

The Amendment Act received Royal Assent on 19 May 2015 with the consequential changes becoming effective from 1 July 2015.

In relation to this Report, on 7 September 2015, the Minister for Energy and the Treasurer jointly directed the Regulator to prepare a performance report for 2014-15.

During 2014-15 the Economic Regulator had the following responsibilities in relation to electricity:

administering the licensing system for electricity entities (with the exception of retailer authorisations which are the AER’s responsibility);

monitoring and regulating technical standards;

monitoring and enforcing compliance;

issuing, maintaining, administering and enforcing electricity codes and guidelines;

reviewing and reporting on the power system reliability3;

regulating prices for declared electrical services (eg raise contingency FCAS);

determining regulated Feed-in Tariff (FiT) rates;

determining Aurora Energy’s standing offer retail electricity prices;

monitoring wholesale electricity financial contract prices; and

other functions under the electricity legislative and regulatory frameworks.

5.5.2 Pricing and pricing related functions

The Economic Regulator is responsible for determining standing offer prices and making regulated feed-in tariff (FiT) rate determinations for standard FiT customers. The Economic Regulator also monitors certain wholesale electricity financial contract prices.

5.5.2.1 Standing offer prices

The framework under which the Economic Regulator sets standing offer prices includes the:

ESI Act;

3 Changed to network reliability from 1 July 2015.

24 ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15

Electricity Supply Industry (Pricing and Related Matters) Regulations 2013; and

Electricity Guideline for the Approval of Standing Offer Prices in accordance with the 2013 Standing Offer Determination (April 2014).

The prices paid by small customers for the supply of electricity are determined by the Economic Regulator after undertaking a price investigation which considers the costs a retailer incurs in supplying electricity to small customers4. The resulting determination sets out a formula which calculates a notional maximum revenue (NMR) which is then used to determine the maximum standing offer prices5.

The NMR is composed of the following costs:

purchasing electricity for resale (wholesale electricity costs);

transporting electricity over the network (network costs);

complying with mandatory renewable energy schemes (RET costs);

AEMO market charges;

providing services to customers including billing, collection and responding to enquiries (cost to serve); and

a margin to compensate the retailer for its investment in the business and the risks it assumes in providing those retail services.

Subject to the Economic Regulator’s approval, standing offer prices are adjusted each year in accordance with the relevant determination and the Economic Regulator’s price reset guideline.

The Economic Regulator approved Aurora Energy’s pricing proposal for 2014-15 on 19 June 2014 which saw a price reduction of 7.8 per cent for 2014-15. On 19 June 2015 the Regulator approved a 1.95 per cent price increase for 2015-16.

5.5.2.2 Regulated FiT rates

The Economic Regulator is also responsible for determining the annual Regulated FiT rate that applies to Standard FiT customers.

Standard FiT customers are customers who installed a qualifying micro distributed generation system on or after 31 August 2013. The regulated FiT rate determination does not apply to Transitional FiT customers who:

had a qualifying micro distributed generation system installed as at 31 August 2013; or

4 Customers who consume up to 150 MWh per annum.

5 A determination is the legal document that specifies how the prices are calculated during each year of the regulatory period.

ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15 25

entered into a contract to install a qualifying new micro distributed generation system or extend an existing micro distributed generation system before 31 August 2013 and the new system or extension was installed and connected before 31 August 2014.

In December 2012 the COAG agreed on revised National Principles for FiT Arrangements. These revised principles outline, among other things, that all premium FiT arrangements were to be closed to new participants by 2014.

Consistent with the COAG reforms, and as part of the 2013 Tasmanian electricity reforms, the FiT rate applying in Tasmania was reviewed.

The Tasmanian Government announced on 18 August 2013 that:

the then current 1:1 FiT arrangement would be closed at midnight on 30 August 2013 and would be grandfathered for existing (or contracted) installations until 1 January 2019;

customers applying to install eligible micro distributed generation systems on or after 31 August 2013 were entitled to a ‘transitional FiT’ of 8 c/kWh from 31 August 2013 until 31 December 2013;

the Economic Regulator would determine the FiT rate to apply from 1 January 2014 for all new installations occurring on or after 31 August 2013; and

the Economic Regulator would review the FiT rate on an annual basis.

The Economic Regulator was required by the Minister of Finance to prepare a report recommending a minimum FiT rate to apply from 1 January 2014, for net exported electricity. The report was completed in October 2013 and in November 2013 legislation was passed which, among other things, provided legal power for the first FiT determination to be made incorporating the recommended FiT as specified in the Economic Regulator’s report.

In December 2013, the Economic Regulator made a Regulated FiT Determination for Standard FiT Customers6, following an amendment to the ESI Act and Electricity Supply Industry (Pricing and Related Matters) Regulations 2013. For the period 1 July 2014 to 30 June 2015, the Economic Regulator determined a regulated FiT rate of 5.500 c/kWh.

Transitional FiT customers continue to receive the benefit of the transitional FiT rates in respect of billing periods, and those parts of billing periods, that expire before 1 January 2019 (ie 28.283 cents per kWh for residential customers and, for small business customers, 38.577 cents per kWh for the first 500 kWh supplied during each billing period and 28.319 cents per kWh for each kWh supplied above 500 kWh during each billing period).

6 See Regulated Feed-in Tariff Determination for Standard Feed-in Tariff Customers (6 December 2014).

26 ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15

5.5.2.3 Wholesale contract prices

To facilitate the introduction of Full Retail Contestability (FRC)7 on mainland Tasmania from 1 July 2014 and to provide certainty for retailers entering the Tasmanian electricity market, the Economic Regulator became responsible, from 1 January 2014, for regulating certain financial contracts offered by Hydro Tasmania8.

The framework includes a legislated instrument (known as the Wholesale Contract Regulatory Instrument) which specifies the terms and conditions for the financial derivative contracts and how prices for the contracts are derived.

Under the framework, Hydro Tasmania is required to offer four regulated derivative contracts to authorised retailers operating in Tasmania.

The aim of providing regulated derivative contracts is to reduce the risk faced by retailers entering the Tasmanian market to a level comparable to the risk facing retailers in other regions of the NEM and consequently increasing the likelihood of retailers entering the Tasmanian market.

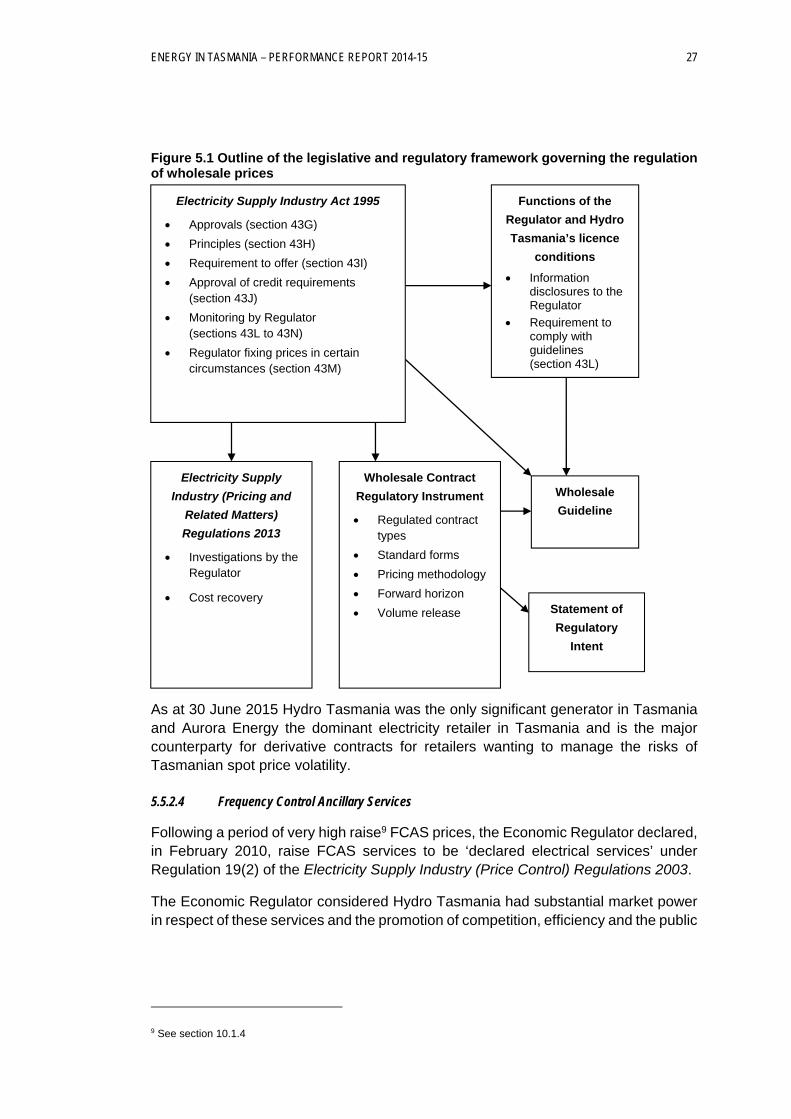

As depicted in Figure 5.1 the framework governing the regulation of Hydro Tasmania’s wholesale contract prices includes the:

ESI Act;

Electricity Supply Industry (Pricing and Related Matters) Regulations 2013;

Wholesale Contract Regulatory Instrument;

Statement of Regulatory Intent - Wholesale Contract Regulation (April 2014); and

Electricity Wholesale Contract Guideline (Version 1, December 2013).

7 All electricity customers are able to choose their retailer. Also referred to as Full Retail Competition (FRC).

8 Additional information on the regulation of Hydro Tasmania’s derivative contacts can be found at: http://www.economicregulator.tas.gov.au/domino/otter.nsf/elect-v/06R

ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15 27

Figure 5.1 Outline of the legislative and regulatory framework governing the regulation of wholesale prices

As at 30 June 2015 Hydro Tasmania was the only significant generator in Tasmania and Aurora Energy the dominant electricity retailer in Tasmania and is the major counterparty for derivative contracts for retailers wanting to manage the risks of Tasmanian spot price volatility.

5.5.2.4 Frequency Control Ancillary Services

Following a period of very high raise9 FCAS prices, the Economic Regulator declared, in February 2010, raise FCAS services to be ‘declared electrical services’ under Regulation 19(2) of the Electricity Supply Industry (Price Control) Regulations 2003.

The Economic Regulator considered Hydro Tasmania had substantial market power in respect of these services and the promotion of competition, efficiency and the public

9 See section 10.1.4

Electricity Supply

Industry (Pricing and

Related Matters)

Regulations 2013

Investigations by the Regulator

Cost recovery

Wholesale Contract

Regulatory Instrument

Regulated contract types

Standard forms

Pricing methodology

Forward horizon

Volume release

Wholesale

Guideline

Electricity Supply Industry Act 1995

Approvals (section 43G)

Principles (section 43H)

Requirement to offer (section 43I)

Approval of credit requirements (section 43J)

Monitoring by Regulator (sections 43L to 43N)

Regulator fixing prices in certain circumstances (section 43M)

Functions of the

Regulator and Hydro

Tasmania’s licence

conditions

Information disclosures to the Regulator

Requirement to comply with guidelines (section 43L)

Statement of

Regulatory

Intent

28 ENERGY IN TASMANIA – PERFORMANCE REPORT 2014-15

interest required the making of the declaration. For more information refer to the Regulator’s FCAS Final Report10.

The Economic Regulator also determined that the price of the FCAS ‘safety net’ contract would be calculated on 15 January and 15 July of each year of the Determination. The Determination commenced on 28 January 2011 and expires on 31 January 2016.

In accordance with Regulation 35 of the Electricity Supply Industry (Pricing and Related Matters) Regulations 2013 the Economic Regulator is required, to invite submissions on whether the declaration of FCAS as a declared electrical service should be retained or revoked.

On 27 April 2015, the Economic Regulator published its Retention or revocation of the declaration of raise contingency Frequency Control Ancillary Services (FCAS) as a declared electrical service – Consultation Paper which outlined the circumstances that, in the Regulator’s view, warranted the revocation of the declaration.

After considering submissions on this consultation paper the Economic Regulator decided to revoke the determination11. In making this decision the Regulator noted that it will continue to monitor FCAS pricing to ensure that regulatory action can be taken if evidence is found of inappropriate pricing behaviour.

5.5.3 Regulatory reporting

Under their respective licences, electricity entities are required to develop a series of management plans in accordance with the TEC. Management plans include asset management, vegetation management and emergency management plans. Certain licensees are also required to produce a compliance plan which outlines the procedures, practices and strategies for managing and auditing the licensee’s compliance with the applicable legislation, regulations and codes.

In accordance with the Regulator’s Regulatory Reporting Guideline Version 3, July 2014, licensees’ compliance and management plans are periodically reviewed by an independent appraiser who then prepares a report for the Economic Regulator.

The timing and scope of these appraisals is determined by the Economic Regulator based on the outcomes of a risk assessment which considers the outcomes from previous appraisals and the likely impact of any changed circumstances on the entity’s operations and, therefore, compliance with obligations.