Energy Environmental Application S - lignite.gr · 1 2 Waste Management Waste to Energy...

29

Biogas Projects Development in Greece Georgios Panousis Mechanical Engineer, MSc Energy Production & Management, M.Sc HELECTOR S.A Department of energy projects Development Energy & Environmental Application S.A

Transcript of Energy Environmental Application S - lignite.gr · 1 2 Waste Management Waste to Energy...

Biogas Projects Development in Greece

Georgios PanousisMechanical Engineer, MSc

Energy Production & Management, M.ScHELECTOR S.A

Department of energy projects Development

Energy & Environmental Application S.A

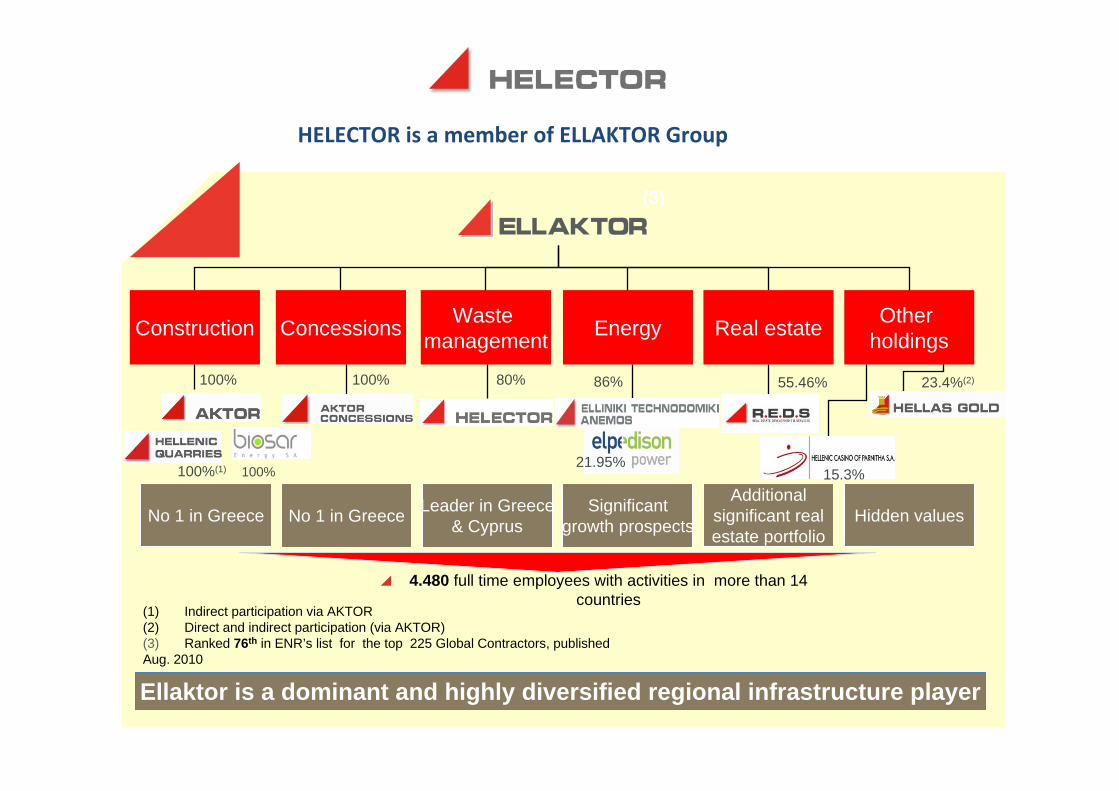

Other holdingsConcessionsConstruction Real estateWaste

management Energy

100% 100% 80% 86% 55.46% 23.4%(2)

100%(1)

No 1 in Greece Leader in Greece& Cyprus

Significantgrowth prospects

Additionalsignificant realestate portfolio

No 1 in Greece Hidden values

4.480 full time employees with activities in more than 14 countries

(1) Indirect participation via AKTOR(2) Direct and indirect participation (via AKTOR)(3) Ranked 76th in ENR’s list for the top 225 Global Contractors, published Aug. 2010

Ellaktor is a dominant and highly diversified regional infrastructure player

100%21.95%

(3)

15.3%

HELECTOR is a member of ELLAKTOR Group

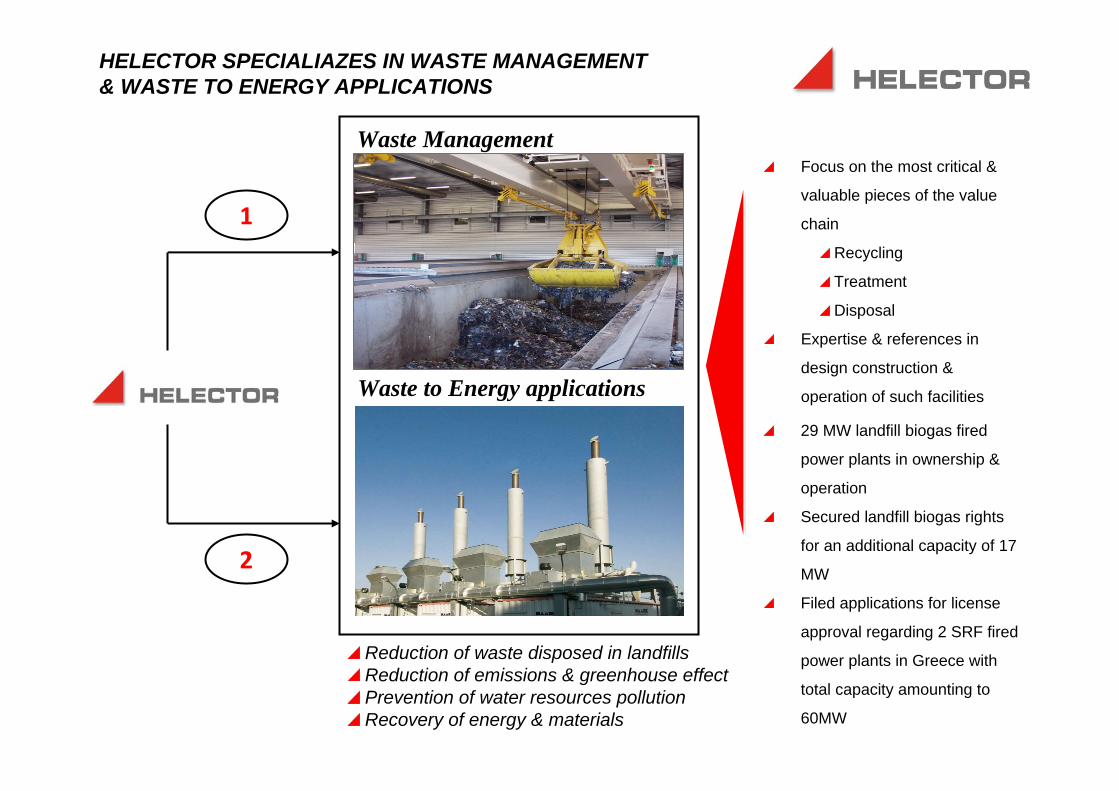

1

2

Waste Management

Waste to Energy applications

Focus on the most critical &

valuable pieces of the value

chain

Recycling

Treatment

Disposal

Expertise & references in

design construction &

operation of such facilities

29 MW landfill biogas fired

power plants in ownership &

operation

Secured landfill biogas rights

for an additional capacity of 17

MW

Filed applications for license

approval regarding 2 SRF fired

power plants in Greece with

total capacity amounting to

60MW

HELECTOR SPECIALIAZES IN WASTE MANAGEMENT & WASTE TO ENERGY APPLICATIONS

Reduction of waste disposed in landfills Reduction of emissions & greenhouse effectPrevention of water resources pollution Recovery of energy & materials

Primary Sources for Biogas Production in Greece

Livestock FarmsLivestock Farms

Agricultural crops, residuesAgricultural crops, residues

Industrial activities (vegetables, fruits, meat, milk industry)

Industrial activities (vegetables, fruits, meat, milk industry)

MSW treatment, sanitary landfill sites, sewage treatment

plants

MSW treatment, sanitary landfill sites, sewage treatment

plants

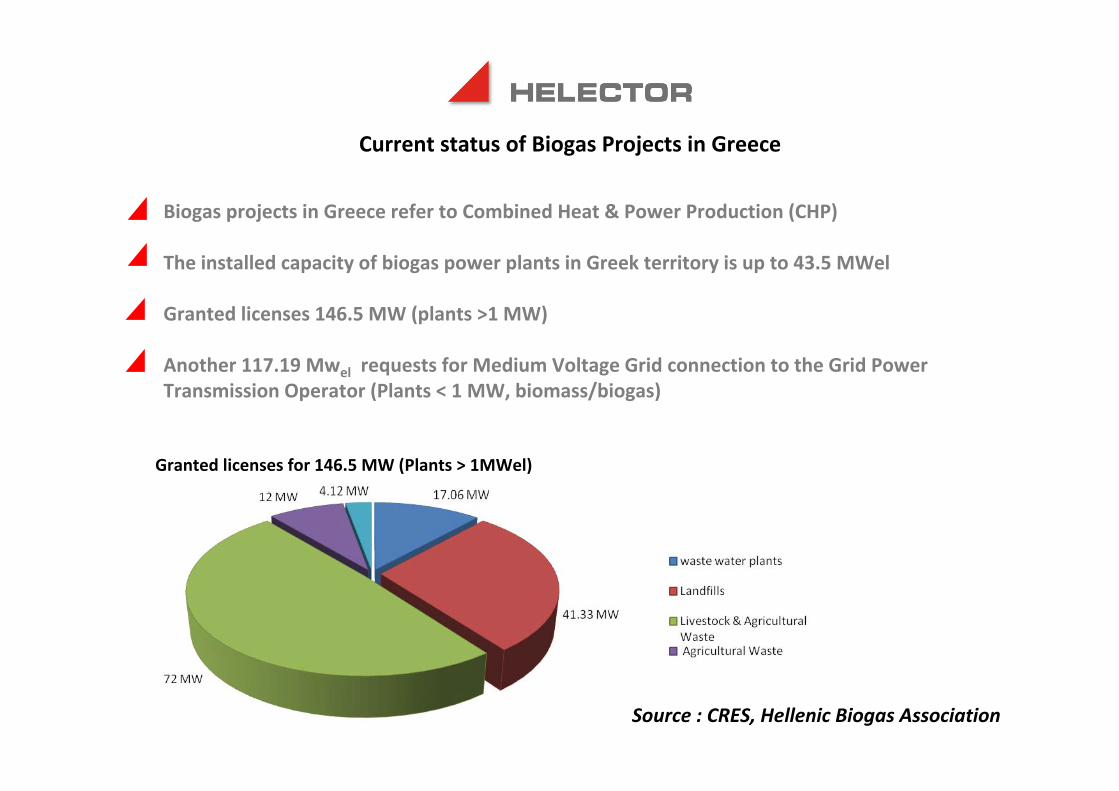

Current status of Biogas Projects in Greece

Biogas projects in Greece refer to Combined Heat & Power Production (CHP)

The installed capacity of biogas power plants in Greek territory is up to 43.5 MWel

Granted licenses 146.5 MW (plants >1 MW)

Another 117.19 Mwel requests for Medium Voltage Grid connection to the Grid Power Transmission Operator (Plants < 1 MW, biomass/biogas)

Granted licenses for 146.5 MW (Plants > 1MWel)

Source : CRES, Hellenic Biogas Association

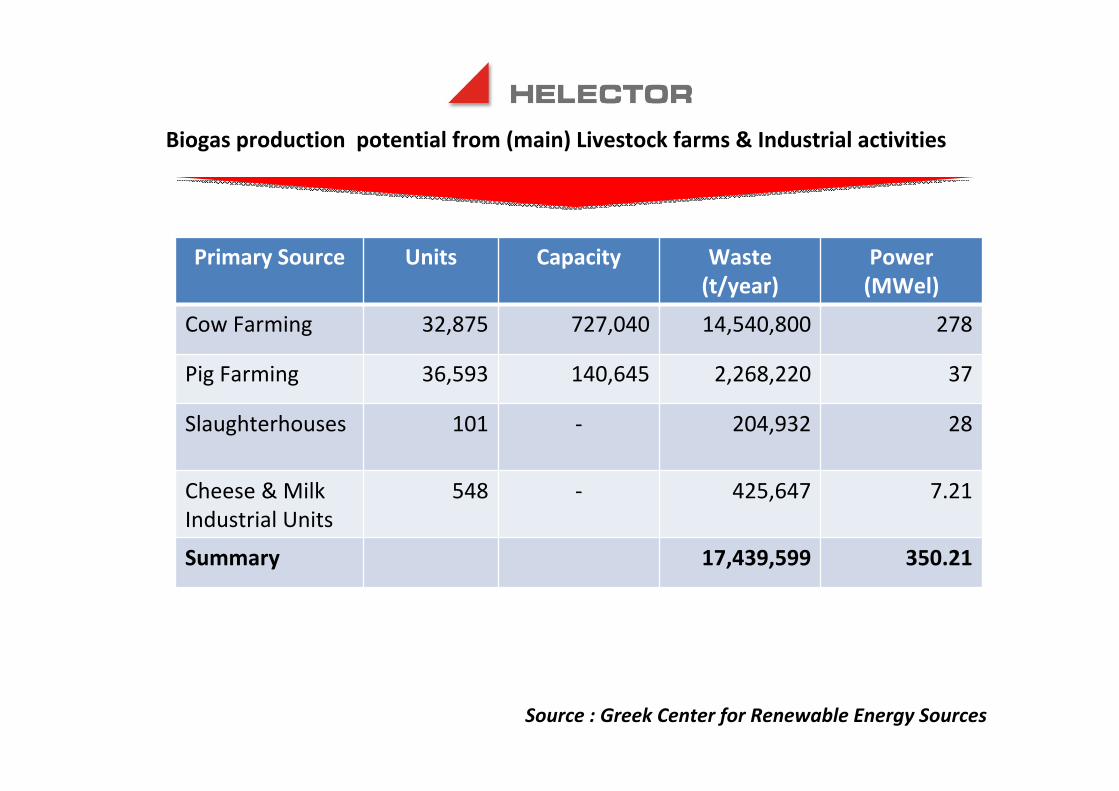

Primary Source Units Capacity Waste (t/year)

Power (MWel)

Cow Farming 32,875 727,040 14,540,800 278

Pig Farming 36,593 140,645 2,268,220 37

Slaughterhouses 101 ‐ 204,932 28

Cheese & Milk Industrial Units

548 ‐ 425,647 7.21

Summary 17,439,599 350.21

Biogas production potential from (main) Livestock farms & Industrial activities

Source : Greek Center for Renewable Energy Sources

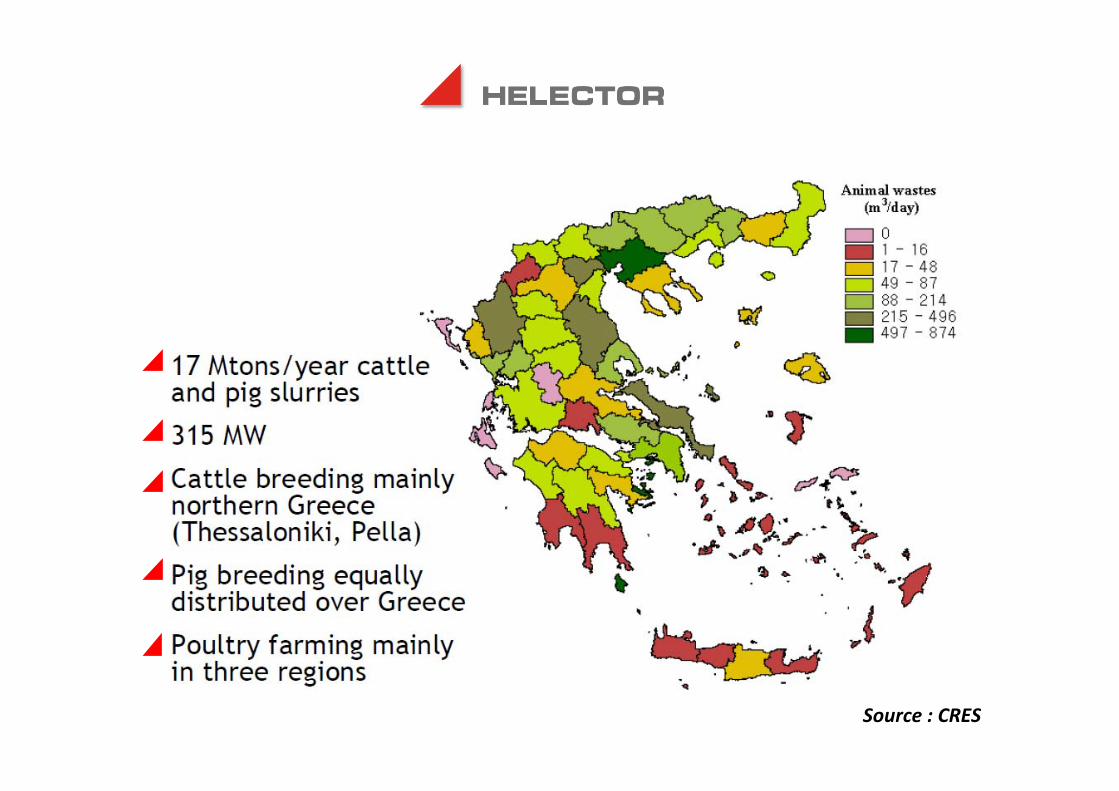

Source : CRES

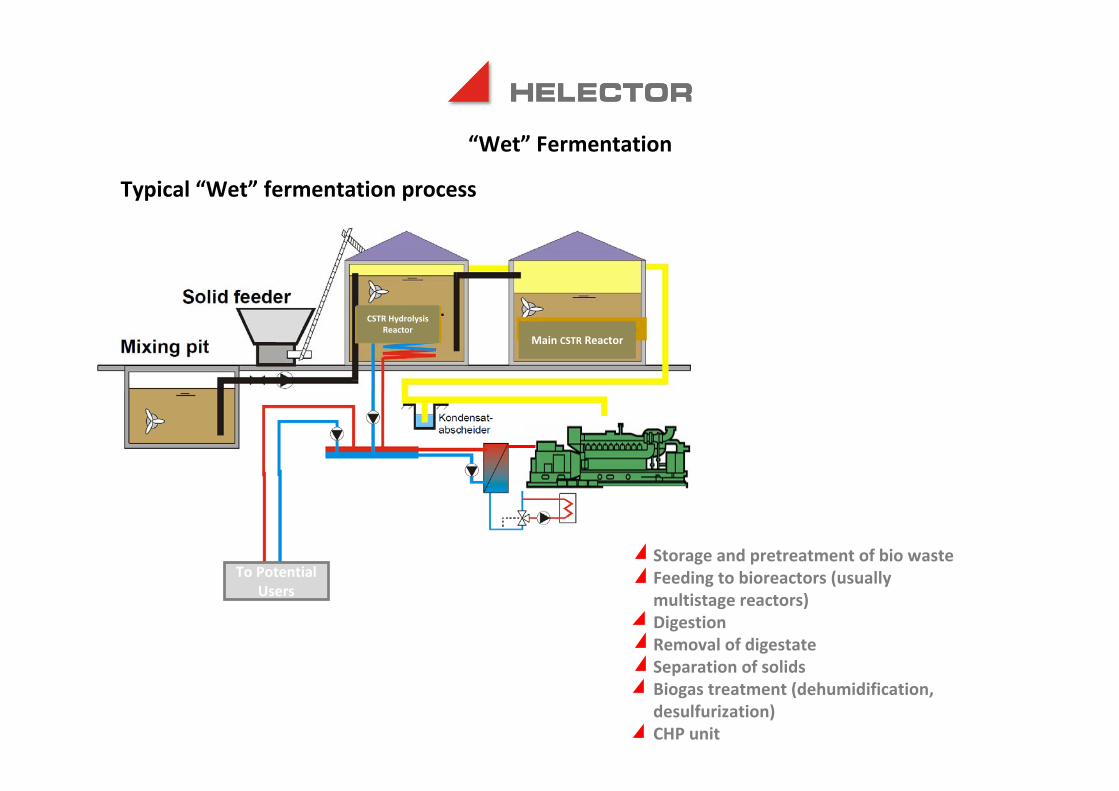

Fermentation Technologies

“Wet” Fermentation “Dry” Fermentation

Applied on substrates of :Liquefied animal wasteSewage sludgeGeneral wet substrates with up to 15 % TS

Applied on substrates of :Solid manureEnergy cropsAgriculture products (e.g. corn silage)Biodegradable fraction of MSWStackable Biomass

To Potential Users

“Wet” Fermentation

Typical “Wet” fermentation process

Storage and pretreatment of bio wasteFeeding to bioreactors (usually multistage reactors)DigestionRemoval of digestate Separation of solidsBiogas treatment (dehumidification, desulfurization)CHP unit

CSTR Hydrolysis Reactor

Main CSTR Reactor

BiofilterPercolate

tank

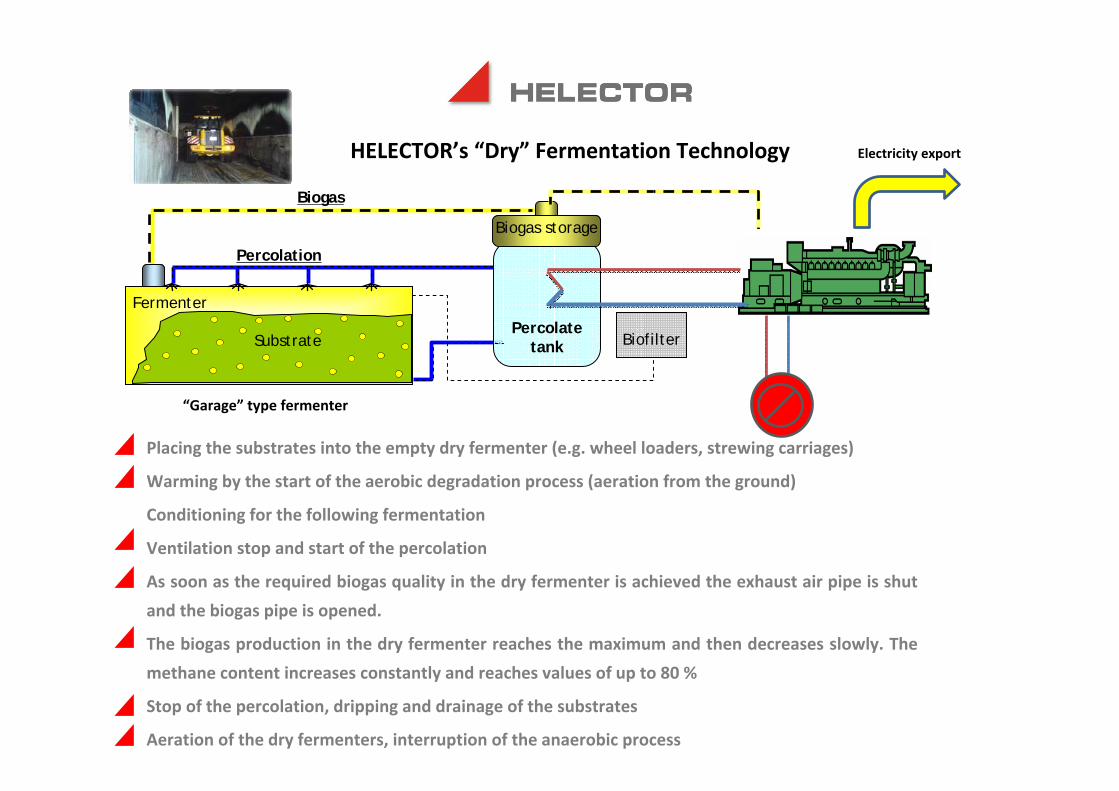

Biogas storage

Fermenter

Substrate

Percolation

Biogas

HELECTOR’s “Dry” Fermentation Technology

Placing the substrates into the empty dry fermenter (e.g. wheel loaders, strewing carriages)

Warming by the start of the aerobic degradation process (aeration from the ground)

Conditioning for the following fermentation

Ventilation stop and start of the percolation

As soon as the required biogas quality in the dry fermenter is achieved the exhaust air pipe is shut

and the biogas pipe is opened.

The biogas production in the dry fermenter reaches the maximum and then decreases slowly. The

methane content increases constantly and reaches values of up to 80 %

Stop of the percolation, dripping and drainage of the substrates

Aeration of the dry fermenters, interruption of the anaerobic process

“Garage” type fermenter

Electricity export

“Dry” vs. “Wet” Fermentation

Significantly lower water requirement No mashing requiredEffluent free operation possible

Lower process energy requirementno mixing mechanism requiredMinimal electric and thermal energy requirement

Less movable machine partsless material wear

Modularly extendable plants

Synergie in the use of agricultural equipment (e.g. wheel loaders, tractors, mixing carriages, manure spreaders etc.)

Simpler (stackable) storage and treatment of digestate

No heating of the dry fermenters

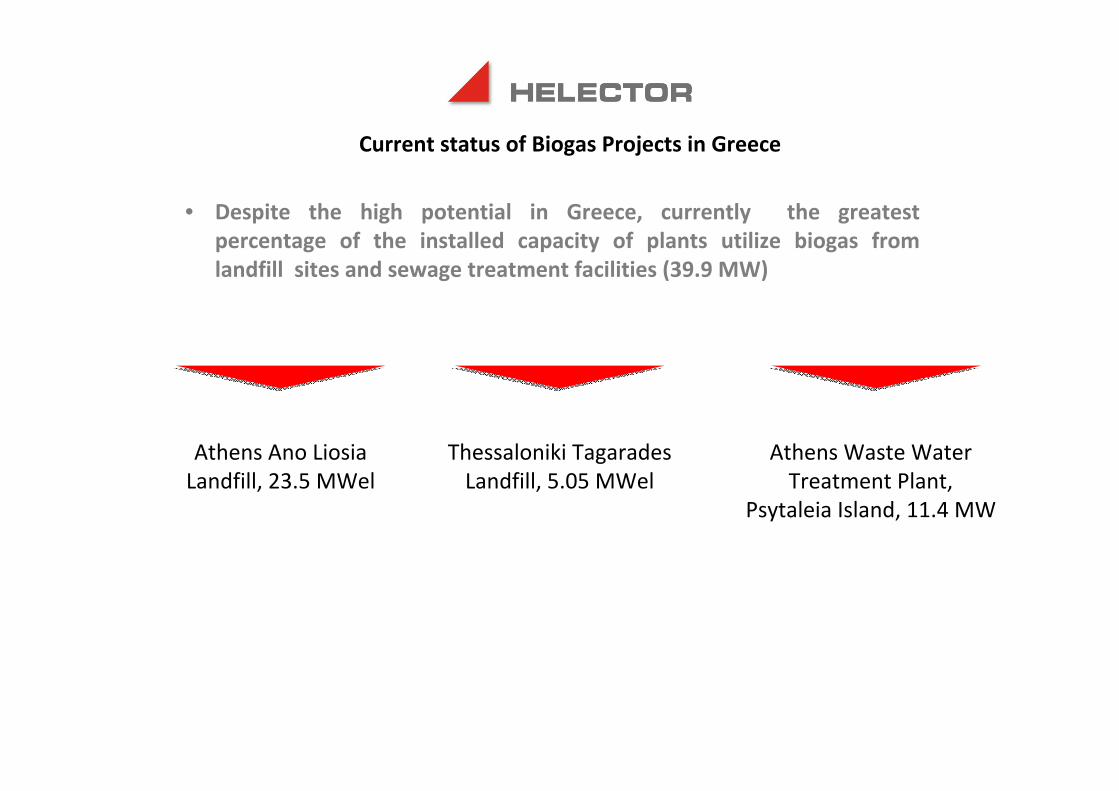

Current status of Biogas Projects in Greece

• Despite the high potential in Greece, currently the greatest percentage of the installed capacity of plants utilize biogas from landfill sites and sewage treatment facilities (39.9 MW)

Athens Ano Liosia Landfill, 23.5 MWel

Thessaloniki Tagarades Landfill, 5.05 MWel

Athens Waste Water Treatment Plant,

Psytaleia Island, 11.4 MW

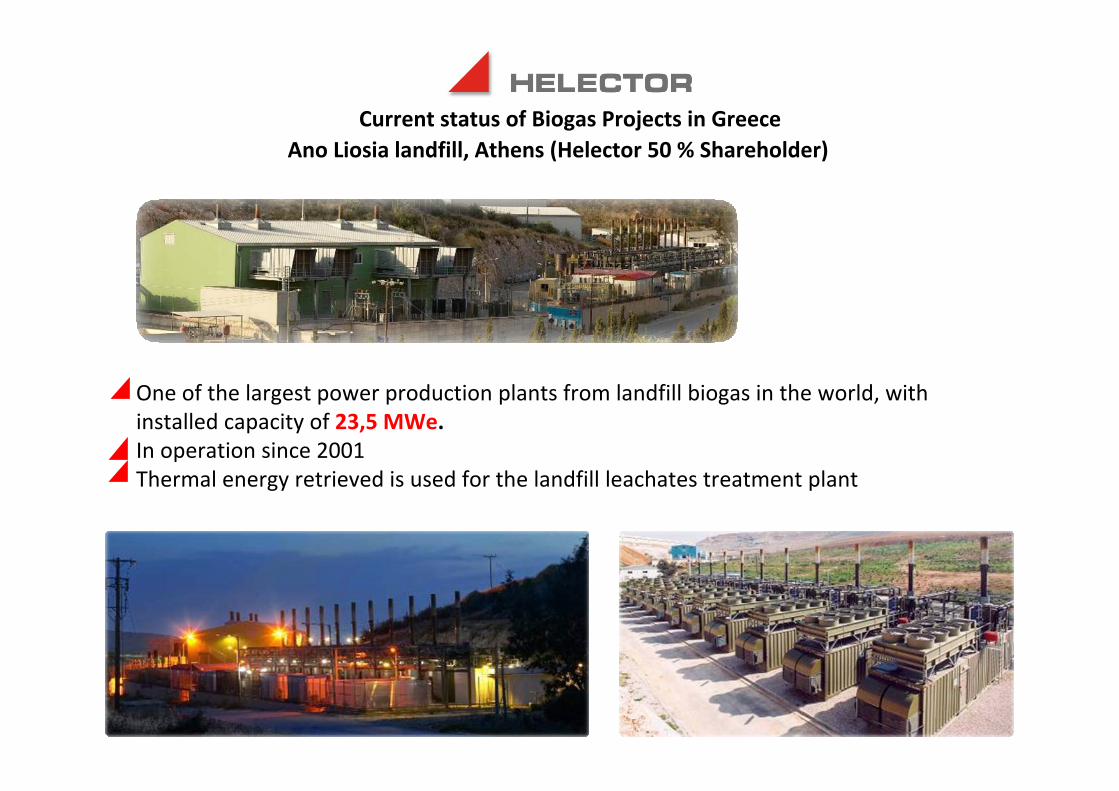

Ano Liosia landfill, Athens (Helector 50 % Shareholder)

One of the largest power production plants from landfill biogas in the world, with installed capacity of 23,5 MWe. In operation since 2001Thermal energy retrieved is used for the landfill leachates treatment plant

Current status of Biogas Projects in Greece

• One of the largest power plants from biogas globally of installed capacity 23.5 MWe. operation since 2001.

• 11 x Deutz TBG 620 v16 • 4 x Jenbacher JMS 620 B.L• Produced power sold to the DESMIE S.A. (

Power Administrator of Greece).• Thermal recovery of energy used for biological

treatment of leachate from Fyli Landfill • Granted rights for 10 MW expansion in Fyli

Landfill site• Construction and operation by BEAL S.A

(Helector 50 % Shareholder)

Current status of Biogas Projects in Greece

• 5,0 MWe in Tagarades, Thessaloniki. In operation since 2007

• 4 x Deutz TBG 620 v16

• Produced power sold to the DESMIE S.A. ( Power Administrator of Greece).

• Expansion perspective by 2,5MW

Tagarades landfill, Thessaloniki (Helector100 % Shareholder)

Biogas from Sewage Sludge Anaerobic Digestion in Waste Water Treatment facility

Installed capacity 11.4 Mwel

Operation by EYDAP S.A (Athens Water Supply and Sewerage Company )

Source : EYDAP S.A

Current status of Biogas Projects in Greece

Other Small Biogas Plants Installations in Greece

KREKA S.ABiogas 675 m/day

Farma Chitas S.A 1 MW CHP

TYRAS S.A

Gkasnakis S.A, 250 kWel

BIOENERGEIAKI MANTINEIAS S.A , 480 kW under construction

Contribution of Biogas projects

Use of a renewable & sustainable source for Heat & Power production

Independence from fossil fuels & electricity imports

Creation of working places during the construction & operation process

Profitable activity for local farmers associations

Reduction of animal farming & food industry environmental impact (odors, uncontrolled byproducts disposal, greenhouse effect impact)

Integrated solution for Energy recovery & Management of Waste and Industrial activities byproducts

Constraints in Biogas Projects Development in Greece

Feedstock supply chain issues•Ensuring continuous supply over plant’s lifetime•Great dispersion of primary sources•Need of a well structured logistics mechanism•Dependence on “others” activities (Farmers, Industries, etc.)

Obstacles in Environmental licensing

Insufficient Projects’ financing •Lack of experience in business risks from biogas projects operation•Banks are reluctant for financing due to the current economic situation in Greece

Lack of synergies. Investments in Biogas Plants would be more attractive in case of plant integration with other activities:‐District Heating of local residences or industries‐Green houses heating

Thoughtless Renewable Energy Plants installation requests from anyone ‐Application’s accumulation in authorities‐Commitment of power grid lines ‐Delays in “serious” investments

Financing Issues –Problems Identification & solutions

No risk assessment & management in main issues such as supply chain, licensing obstacles, technology use. Business plans should be very analytical and accurate on these issues

Greek Banks do not have the required experience in relevant projects – And in the current situation nor the necessary liquidity.

Great delays in the absorption of subsidies resources

Sense of insecurity for “feed in tariffs” levels in long term basis – Extra taxation in renewable projects as in 2012. Need of clear warrantees in pricing policies by the state.

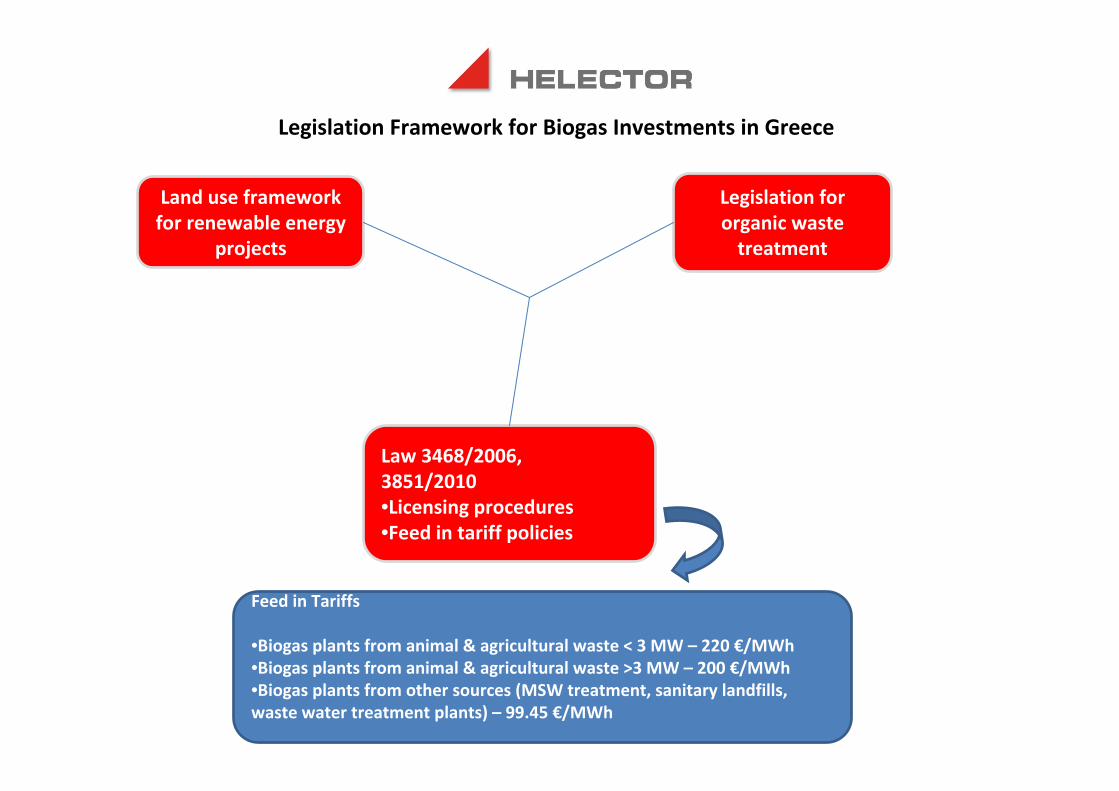

Legislation Framework for Biogas Investments in Greece

Land use framework for renewable energy

projects

Law 3468/2006,3851/2010•Licensing procedures•Feed in tariff policies

Legislation for organic waste treatment

Feed in Tariffs

•Biogas plants from animal & agricultural waste < 3 MW – 220 €/MWh•Biogas plants from animal & agricultural waste >3 MW – 200 €/MWh•Biogas plants from other sources (MSW treatment, sanitary landfills, waste water treatment plants) – 99.45 €/MWh

HELECTOR’s position in the developing Biogas Market

Technology provider in “Dry” Fermentation Power Plants through Helector GmbH (6.7 MW Reference Plants)

Close cooperation with technology providers for “wet” Fermentation Power Plants

Experienced Contractor in waste management & waste to energy projects

Experienced Operator of Biogas CHP power plants

Helector S.A acts as:

Energy from Landfill biogas

Construction of landfill gas grid

Process Diagram

Installation of biogas engines

Helector S.A constructs and operates landfill gas power stations

Reference plants•23.0 MW landfill gas power plant in Athens (Shareholder 50 %)•5.0 MW landfill gas in Thessaloniki Greece (shareholder 100 %)•20 MW , Jordan, under Development

Experience in all fields (gas field collection, pretreatment, internal combustion engines, maintenance, overhauls, plant operation)

Landfill Biogas Plants

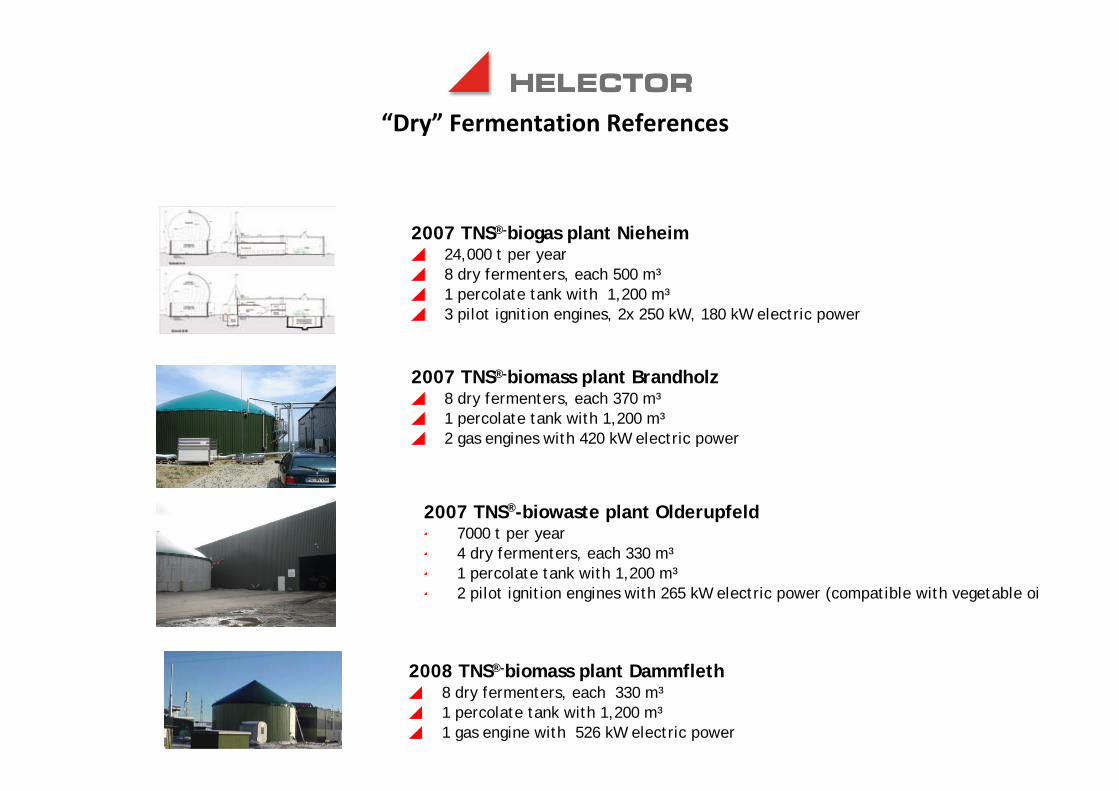

“Dry” Fermentation References

2003 TNS®‐biomass plant Pirow4 dry fermenters, each 150 m³1 percolate tank with 1,600 m³1 wet fermenter / 1 second digester with 1,500 m³1 final storage with 2,500 m³2 gas engines, each 250 kW electric power

2006 TNS®-biomass plant Friedersdorf8 dry fermenters, each 330 m³1 percolate tank with 1,000 m³2 pilot ignition engines each 250 kW electric power

2007 TNS®-biomass plant Barnstedt4 dry fermenters, each 330 m³1 percolate tank with 700 m³2 pilot ignition engines, each 210 kW electric power (compatible with vegetable oil)

2005 TNS®-biowaste plant Halle-Lochau50,000 t per year, therefrom 20,000 t biowaste8 dry fermenters, each 240m³1 percolate tank with 1,200 m³1 wet fermenter with 2,600m³ / 1 second digester with 3,100 m³1 final storage with 3,100m³2 gas engines with 526 kW electric power

2007 TNS®-biogas plant Nieheim24,000 t per year8 dry fermenters, each 500 m³1 percolate tank with 1,200 m³3 pilot ignition engines, 2x 250 kW, 180 kW electric power

2008 TNS®-biomass plant Dammfleth8 dry fermenters, each 330 m³1 percolate tank with 1,200 m³1 gas engine with 526 kW electric power

2007 TNS®-biowaste plant Olderupfeld7000 t per year4 dry fermenters, each 330 m³1 percolate tank with 1,200 m³2 pilot ignition engines with 265 kW electric power (compatible with vegetable oi

2007 TNS®-biomass plant Brandholz8 dry fermenters, each 370 m³1 percolate tank with 1,200 m³2 gas engines with 420 kW electric power

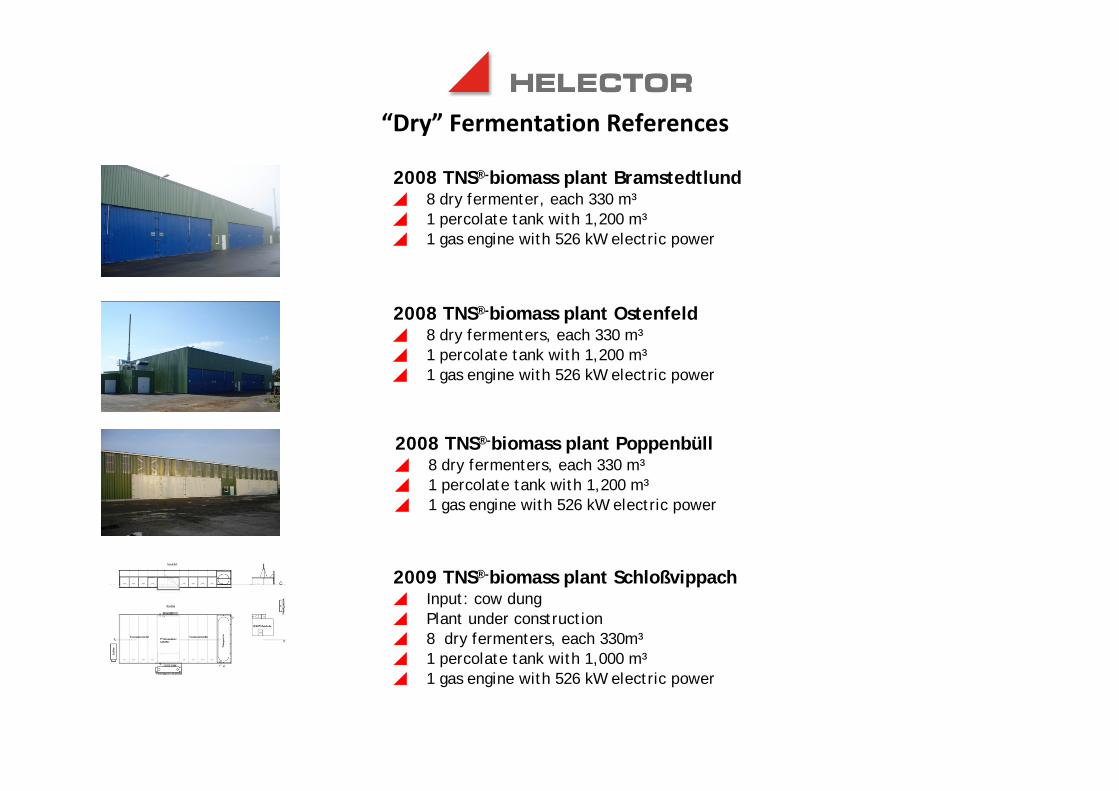

“Dry” Fermentation References

2008 TNS®-biomass plant Ostenfeld8 dry fermenters, each 330 m³1 percolate tank with 1,200 m³1 gas engine with 526 kW electric power

2008 TNS®-biomass plant Poppenbüll8 dry fermenters, each 330 m³1 percolate tank with 1,200 m³1 gas engine with 526 kW electric power

2009 TNS®-biomass plant SchloßvippachInput: cow dungPlant under construction8 dry fermenters, each 330m³1 percolate tank with 1,000 m³1 gas engine with 526 kW electric power

2008 TNS®-biomass plant Bramstedtlund8 dry fermenter, each 330 m³1 percolate tank with 1,200 m³1 gas engine with 526 kW electric power

“Dry” Fermentation References

Ensuring the continuous supply of primary feedstock (supply contracts with local farmers)

Use of “state of the art” technologies with high conversion efficiency

Simplify of licensing procedure

Information of all the involved parties (Investors, local authorities)

Education of residents & local organizations

Development of synergies between Energy and Agriculture Sectors

Improvement of financing mechanisms

Ensuring a stable framework of pricing policy & operation issues (digestate use)

Stricter framework in order to promote the “mature” business plans

Suggestions for further biogas projects development