EnCom Corporation The Analysis of Earnings Quality.

32

EnCom Corporation The Analysis of Earnings Quality

-

Upload

stephen-griffith -

Category

Documents

-

view

258 -

download

2

Transcript of EnCom Corporation The Analysis of Earnings Quality.

EnCom CorporationThe Analysis of Earnings Quality

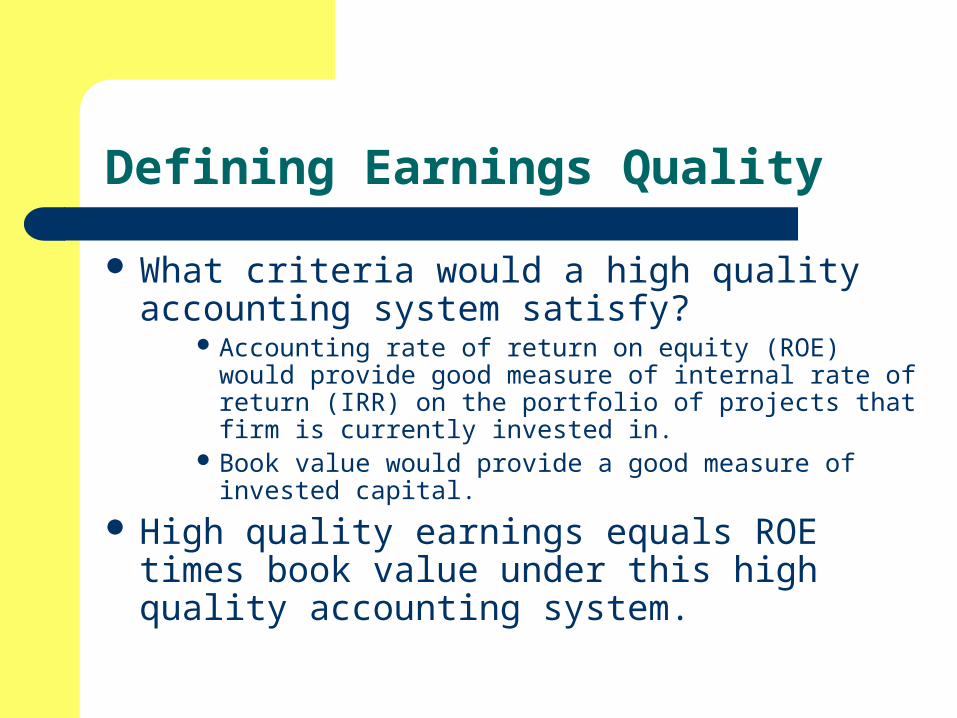

Defining Earnings Quality

What criteria would a high quality accounting system satisfy?

Accounting rate of return on equity (ROE) would provide good measure of internal rate of return (IRR) on the portfolio of projects that firm is currently invested in.

Book value would provide a good measure of invested capital.

High quality earnings equals ROE times book value under this high quality accounting system.

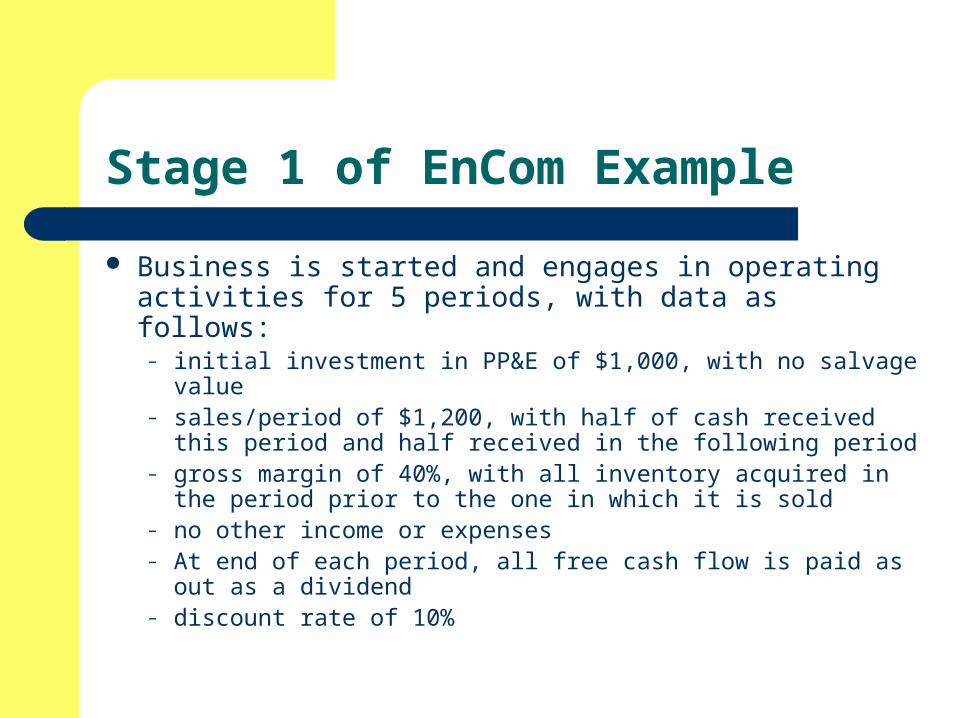

Stage 1 of EnCom Example

Business is started and engages in operating activities for 5 periods, with data as follows:

– initial investment in PP&E of $1,000, with no salvage value– sales/period of $1,200, with half of cash received this period

and half received in the following period– gross margin of 40%, with all inventory acquired in the period

prior to the one in which it is sold– no other income or expenses– At end of each period, all free cash flow is paid as out as a

dividend– discount rate of 10%

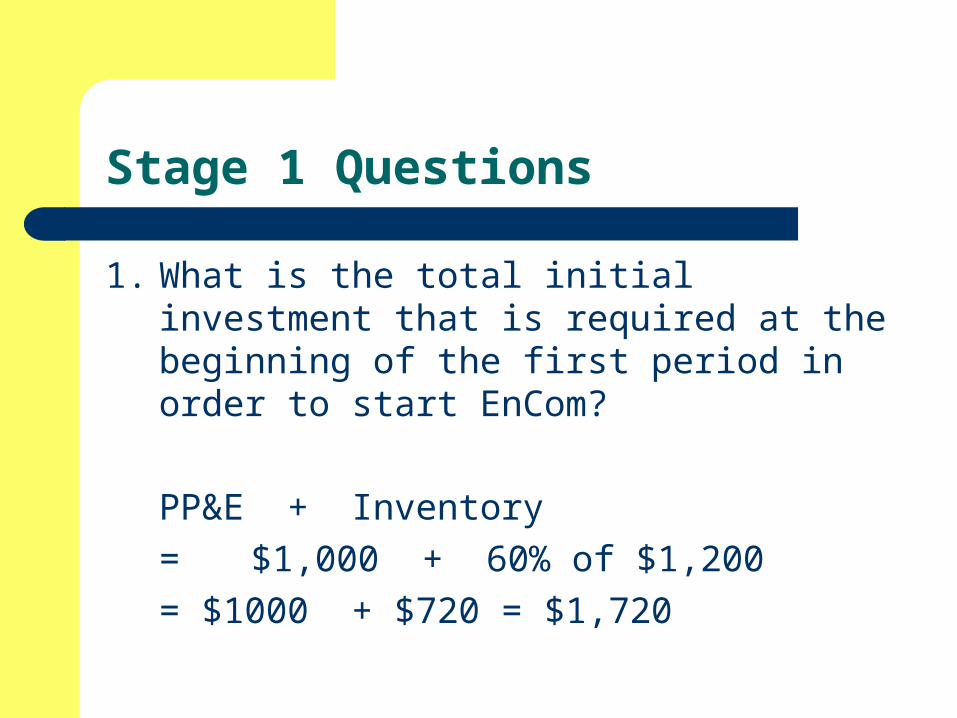

Stage 1 Questions

1. What is the total initial investment that is required at the beginning of the first period in order to start EnCom?

PP&E + Inventory

= $1,000 + 60% of $1,200

= $1000 + $720 = $1,720

Stage 1 Questions

2. Compute the value of EnCom immediately after the initial investment at the beginning of period 1 using the discounted free cash flow method.

3. Compute EnCom’s internal rate of return.

Solution (double click to see computations)

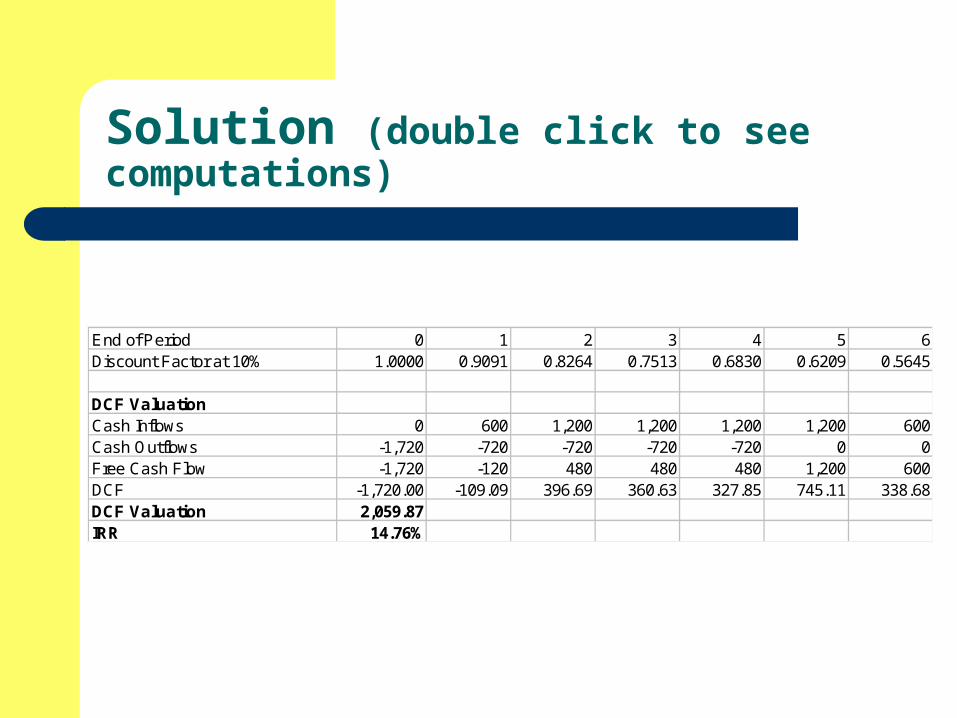

End of Period 0 1 2 3 4 5 6Discount Factor at 10% 1.0000 0.9091 0.8264 0.7513 0.6830 0.6209 0.5645

DCF ValuationCash Inflows 0 600 1,200 1,200 1,200 1,200 600Cash Outflows -1,720 -720 -720 -720 -720 0 0Free Cash Flow -1,720 -120 480 480 480 1,200 600DCF -1,720.00 -109.09 396.69 360.63 327.85 745.11 338.68DCF Valuation 2,059.87IRR 14.76%

Stage 1 Questions

4. Prepare financial statements (income statements and balance sheets) for EnCom for each of the five periods that it is in business.

Solution (double click to see formulas)

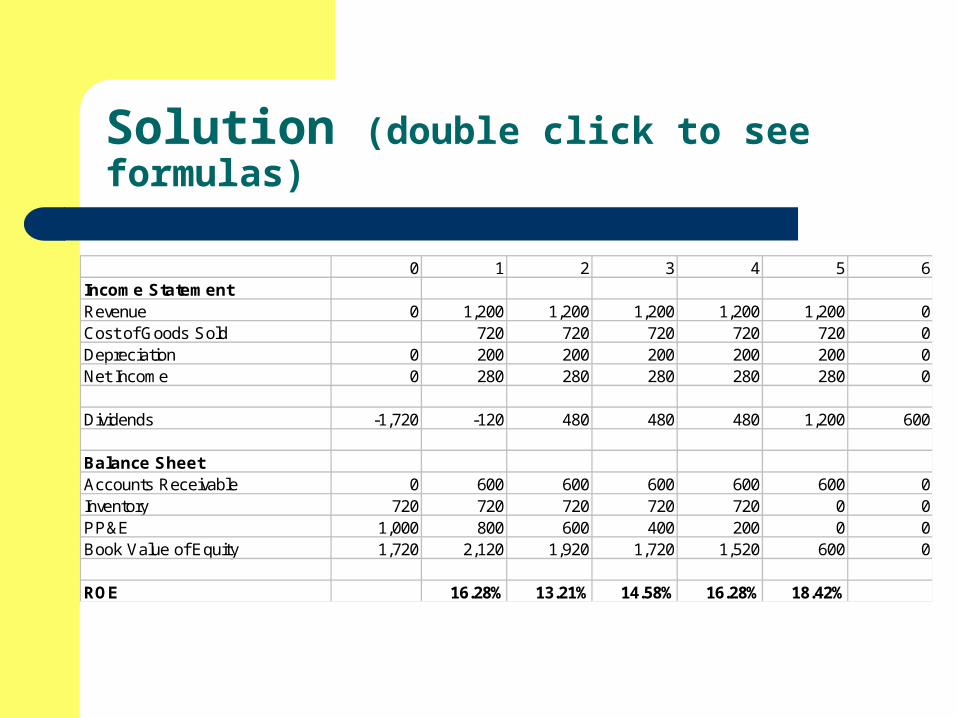

0 1 2 3 4 5 6Income StatementRevenue 0 1,200 1,200 1,200 1,200 1,200 0Cost of Goods Sold 720 720 720 720 720 0Depreciation 0 200 200 200 200 200 0Net Income 0 280 280 280 280 280 0

Dividends -1,720 -120 480 480 480 1,200 600

Balance SheetAccounts Receivable 0 600 600 600 600 600 0Inventory 720 720 720 720 720 0 0PP&E 1,000 800 600 400 200 0 0Book Value of Equity 1,720 2,120 1,920 1,720 1,520 600 0

ROE 16.28% 13.21% 14.58% 16.28% 18.42%

Stage 1 Questions

5. Compare EnCom’s free cash flows and earnings for each of the five periods. Overall, which of the two measures do you think provides the best measure of EnCom’s periodic performance? Why?

Earnings, because they provide a more timely and a less noisy measure of periodic performance.

Stage 1 Questions

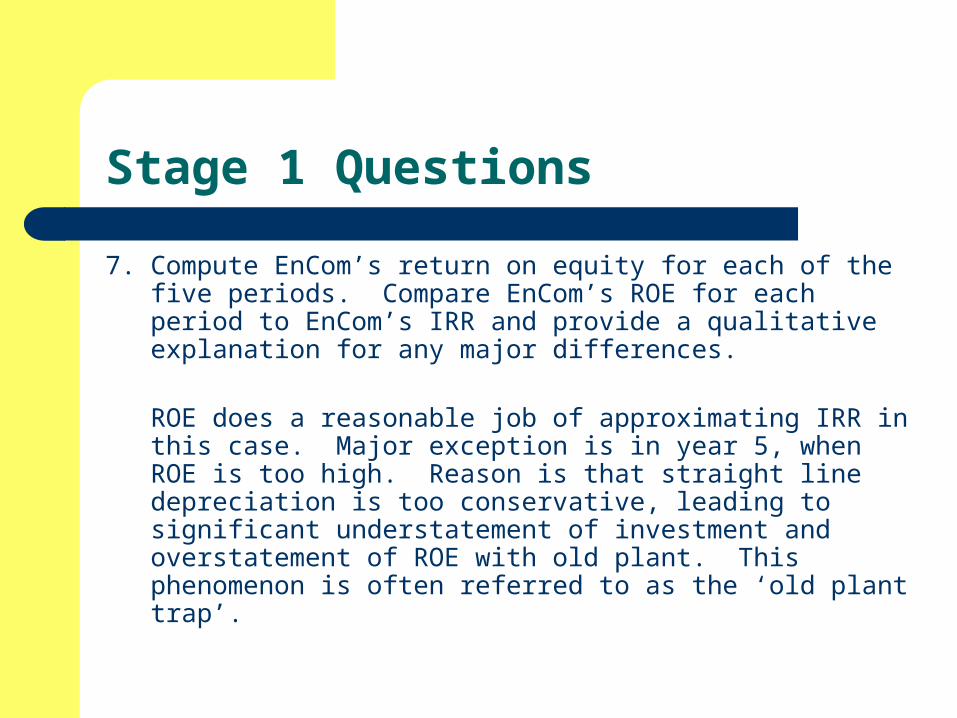

7. Compute EnCom’s return on equity for each of the five periods. Compare EnCom’s ROE for each period to EnCom’s IRR and provide a qualitative explanation for any major differences.

ROE does a reasonable job of approximating IRR in this case. Major exception is in year 5, when ROE is too high. Reason is that straight line depreciation is too conservative, leading to significant understatement of investment and overstatement of ROE with old plant. This phenomenon is often referred to as the ‘old plant trap’.

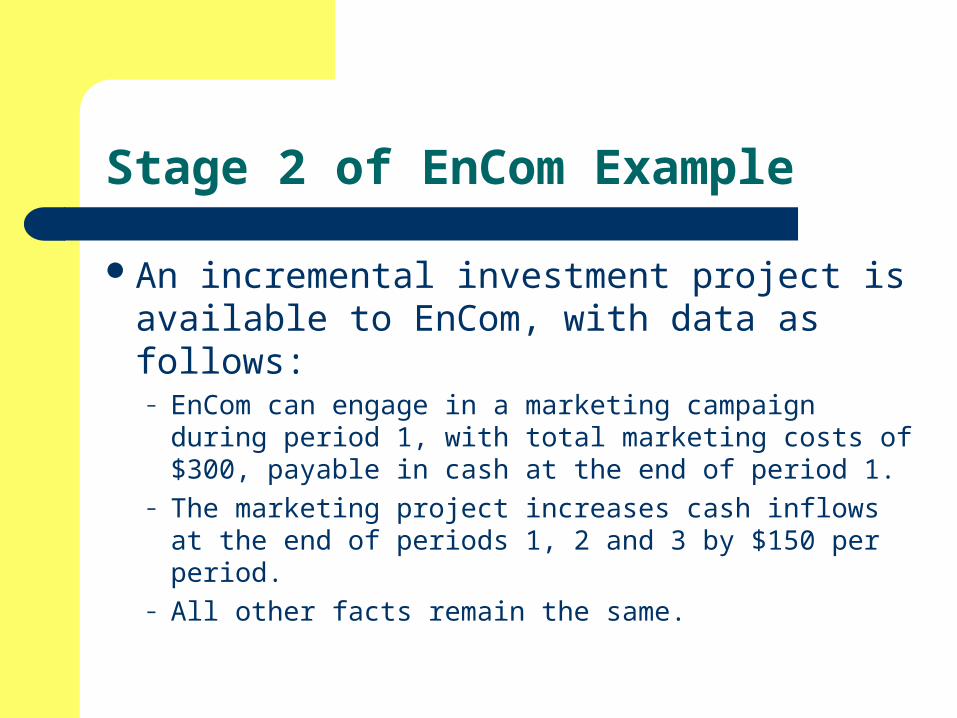

Stage 2 of EnCom Example

An incremental investment project is available to EnCom, with data as follows:– EnCom can engage in a marketing campaign during

period 1, with total marketing costs of $300, payable in cash at the end of period 1.

– The marketing project increases cash inflows at the end of periods 1, 2 and 3 by $150 per period.

– All other facts remain the same.

Stage 2 Questions

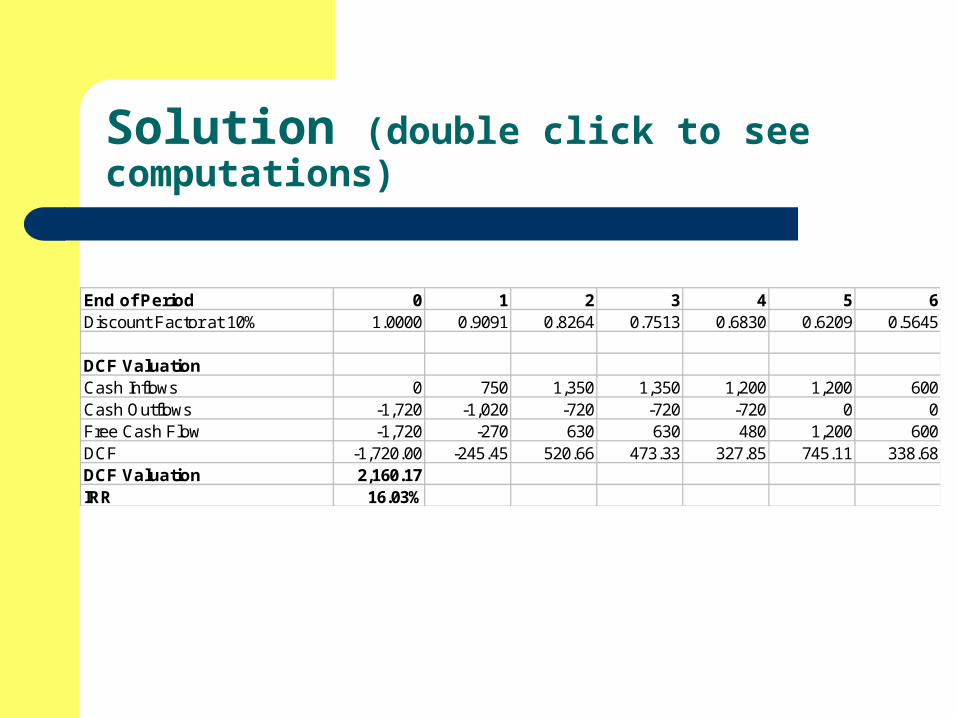

1. Compute the value of EnCom with the incremental project immediately after the initial investment at the beginning of period 1 using the discounted free cash flow method. Should EnCom invest in the incremental project?

2. Compute EnCom’s IRR with the incremental investment project.

Solution (double click to see computations)

End of Period 0 1 2 3 4 5 6Discount Factor at 10% 1.0000 0.9091 0.8264 0.7513 0.6830 0.6209 0.5645

DCF ValuationCash Inflows 0 750 1,350 1,350 1,200 1,200 600Cash Outflows -1,720 -1,020 -720 -720 -720 0 0Free Cash Flow -1,720 -270 630 630 480 1,200 600DCF -1,720.00 -245.45 520.66 473.33 327.85 745.11 338.68DCF Valuation 2,160.17IRR 16.03%

Stage 2 Questions

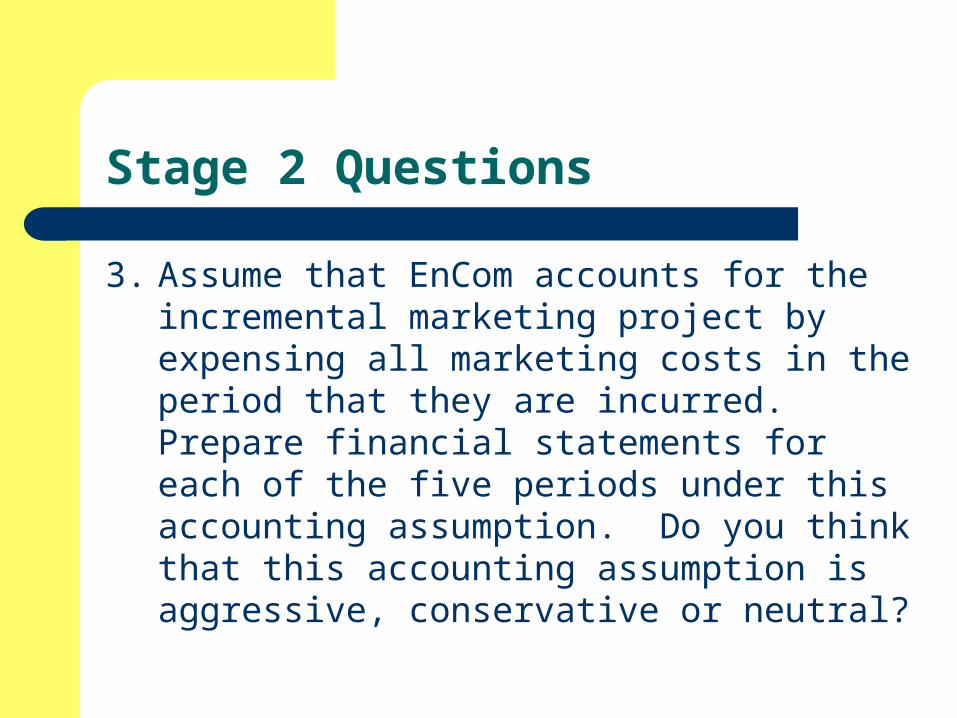

3. Assume that EnCom accounts for the incremental marketing project by expensing all marketing costs in the period that they are incurred. Prepare financial statements for each of the five periods under this accounting assumption. Do you think that this accounting assumption is aggressive, conservative or neutral?

Solution (double click to see formulas)

0 1 2 3 4 5 6Income StatementRevenue 0 1,350 1,350 1,350 1,200 1,200 0Cost of Goods Sold 720 720 720 720 720 0Depreciation 0 200 200 200 200 200 0Marketing Costs 300 0 0 0 0 0Net Income 0 130 430 430 280 280 0

Dividends -1,720 -270 630 630 480 1,200 600

Balance SheetAccounts Receivable 0 600 600 600 600 600 0Inventory 720 720 720 720 720 0 0PP&E 1,000 800 600 400 200 0 0Book Value of Equity 1,720 2,120 1,920 1,720 1,520 600 0

ROE 7.56% 20.28% 22.40% 16.28% 18.42%

Stage 2 Questions

4. Assume that EnCom accounts for the incremental marketing project by capitalizing marketing costs and then amortizing them in proportion to the benefits received. Prepare financial statements for each of the five periods under this accounting assumption. Do you think that this accounting assumption is aggressive, conservative or neutral?

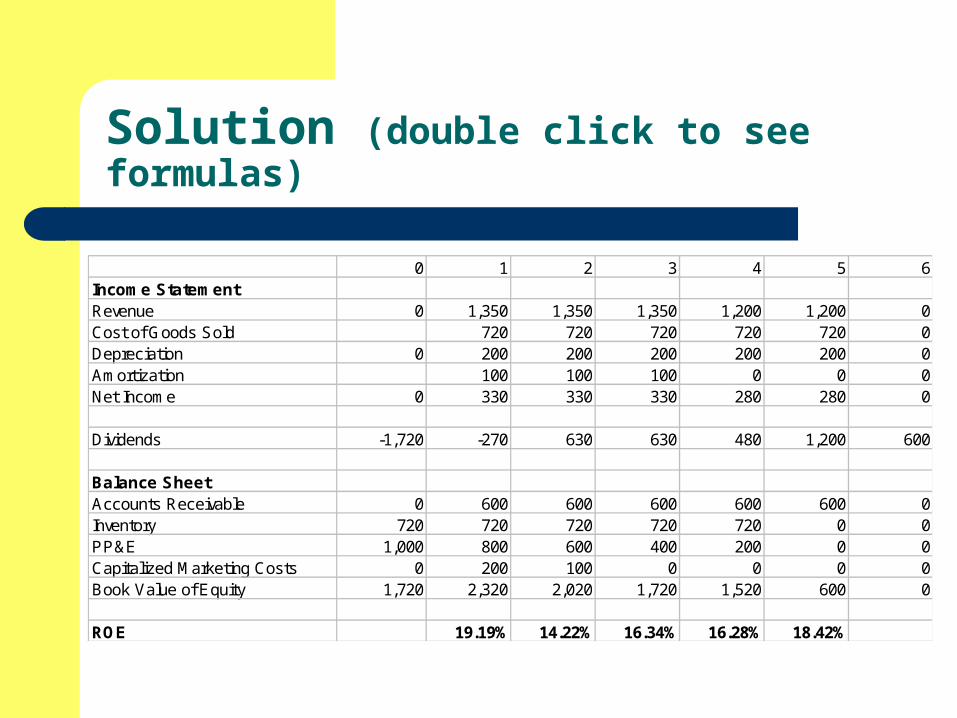

Solution (double click to see formulas)

0 1 2 3 4 5 6Income StatementRevenue 0 1,350 1,350 1,350 1,200 1,200 0Cost of Goods Sold 720 720 720 720 720 0Depreciation 0 200 200 200 200 200 0Amortization 100 100 100 0 0 0Net Income 0 330 330 330 280 280 0

Dividends -1,720 -270 630 630 480 1,200 600

Balance SheetAccounts Receivable 0 600 600 600 600 600 0Inventory 720 720 720 720 720 0 0PP&E 1,000 800 600 400 200 0 0Capitalized Marketing Costs 0 200 100 0 0 0 0Book Value of Equity 1,720 2,320 2,020 1,720 1,520 600 0

ROE 19.19% 14.22% 16.34% 16.28% 18.42%

Stage 2 Questions

5. Assume that EnCom accounts for the incremental marketing project by capitalizing marketing costs and then expensing all of these costs in the first period in which no benefits are received from the project. Prepare financial statements for each of the five periods under this accounting assumption. Do you think that this accounting assumption is aggressive, conservative or neutral?

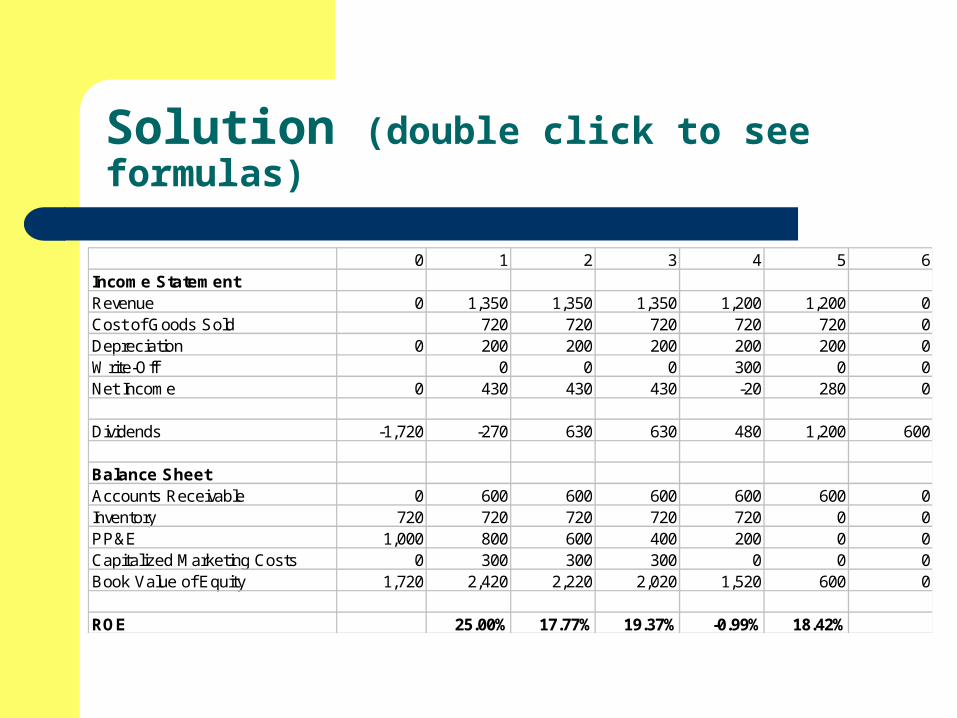

Solution (double click to see formulas)

0 1 2 3 4 5 6Income StatementRevenue 0 1,350 1,350 1,350 1,200 1,200 0Cost of Goods Sold 720 720 720 720 720 0Depreciation 0 200 200 200 200 200 0Write-Off 0 0 0 300 0 0Net Income 0 430 430 430 -20 280 0

Dividends -1,720 -270 630 630 480 1,200 600

Balance SheetAccounts Receivable 0 600 600 600 600 600 0Inventory 720 720 720 720 720 0 0PP&E 1,000 800 600 400 200 0 0Capitalized Marketing Costs 0 300 300 300 0 0 0Book Value of Equity 1,720 2,420 2,220 2,020 1,520 600 0

ROE 25.00% 17.77% 19.37% -0.99% 18.42%

Stage 2 Questions

6. Which of the above three accounting methods do you think provides the best measure of EnCom’s periodic performance? Why?

Amortizing over 3 years, because it matches the costs of the marketing project with the benefits that it generates.

Stage 2 Questions

7. Compute EnCom’s ROE for each of the five periods using each of the above three accounting methods. Explain how each of the different accounting methods impacts EnCom’s ROE.

• Immediately expensing the costs temporarily depresses ROE, but leads to inflated ROE in the future. This is conservative accounting.

• Write-off of the costs after they no longer yield any benefits temporarily inflates ROE, but leads to depressed ROE in the future. This is aggressive accounting.

Stage 2 Questions

8. Using the insights from the EnCom example, provide a qualitative explanation of the impact of aggressive and conservative accounting on a firm’s ROE relative to its IRR.

• Aggressive accounting involves the overstatement of investment. In periods of growth in investment, it leads to inflated ROE, but when growth slows, ROE is depressed.

• Conservative accounting involves the understatement of investment. In periods of growth in investment, it leads to depressed ROE, but when growth slows, ROE is inflated.

Stage 3 Questions

1. Provide a separate residual income valuation for EnCom immediately after the start of business using each of the three accounting methods from Stage 2.

Solution (double click to see computations)

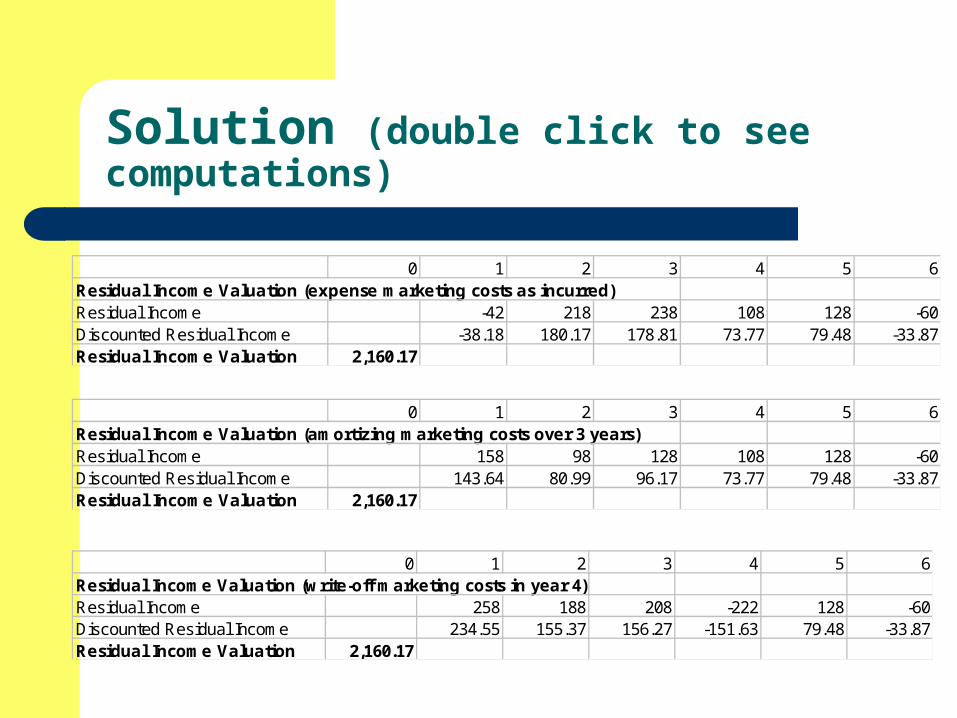

0 1 2 3 4 5 6Residual Income Valuation (expense marketing costs as incurred)Residual Income -42 218 238 108 128 -60Discounted Residual Income -38.18 180.17 178.81 73.77 79.48 -33.87Residual Income Valuation 2,160.17

0 1 2 3 4 5 6Residual Income Valuation (amortizing marketing costs over 3 years)Residual Income 158 98 128 108 128 -60Discounted Residual Income 143.64 80.99 96.17 73.77 79.48 -33.87Residual Income Valuation 2,160.17

0 1 2 3 4 5 6Residual Income Valuation (write-off marketing costs in year 4)Residual Income 258 188 208 -222 128 -60Discounted Residual Income 234.55 155.37 156.27 -151.63 79.48 -33.87Residual Income Valuation 2,160.17

Stage 3 Questions

2. In question 1 above, you should have arrived at the same valuation regardless of the accounting method employed. Provide a qualitative explanation as to why the different accounting methods have no impact on the valuation.The accounting technique selected has no effect on cash flows or dividends, and hence has no impact on the valuation. Note that conservative accounting leads to low residual income in earlier years and high residual income in later years. Conversely, aggressive accounting leads to high residual income in earlier years and low residual income in later years.

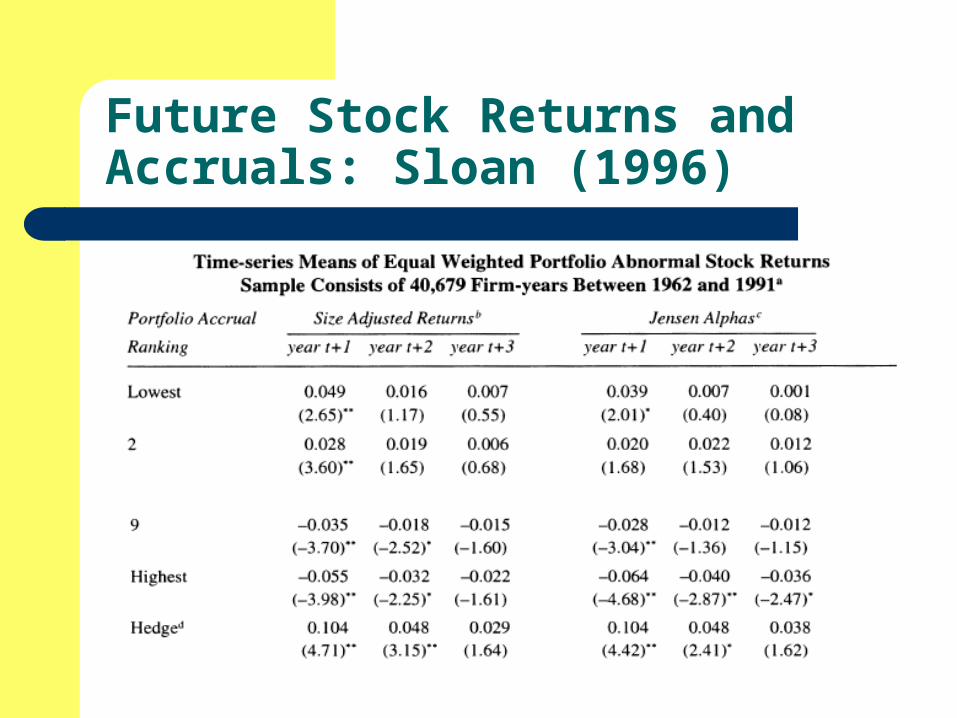

Exploiting Information in Accruals: Sloan (1996)

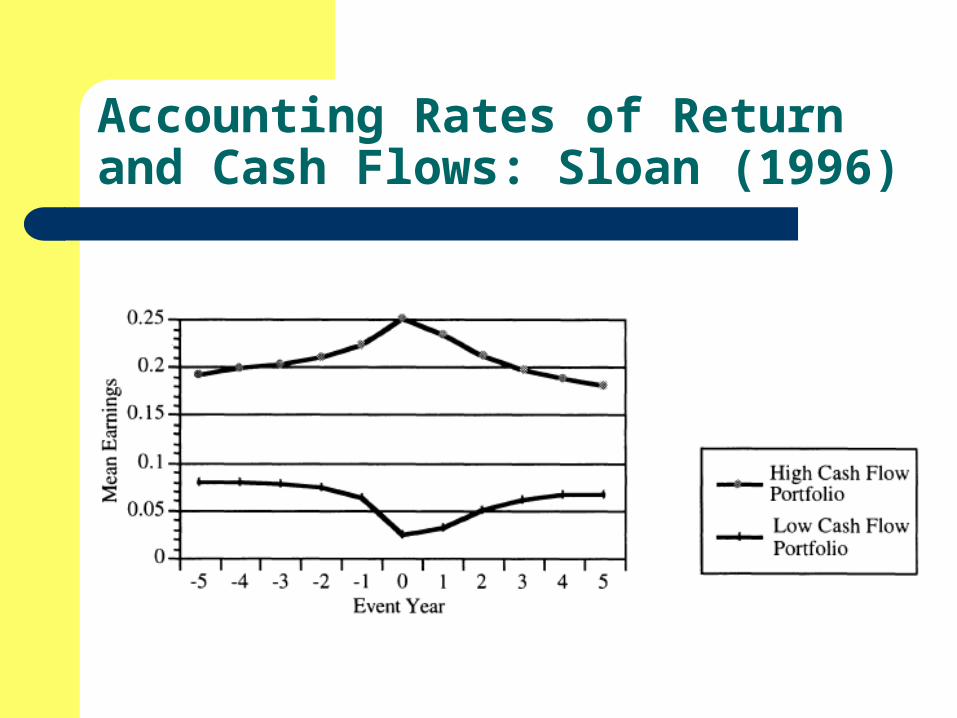

Accruals represent the difference between earnings and cash flows, so earnings consists of an ‘accrual component’ and a ‘cash flow component’.

In long run, earnings = cash flows and accruals=0. Accruals are the less reliable component of earnings,

and represent the component that is typically used to manage/manipulate earnings:

– Artificially high accruals temporarily inflate earnings and accounting rates of return

– Artificially low accruals temporarily depress earnings and accounting rates of return

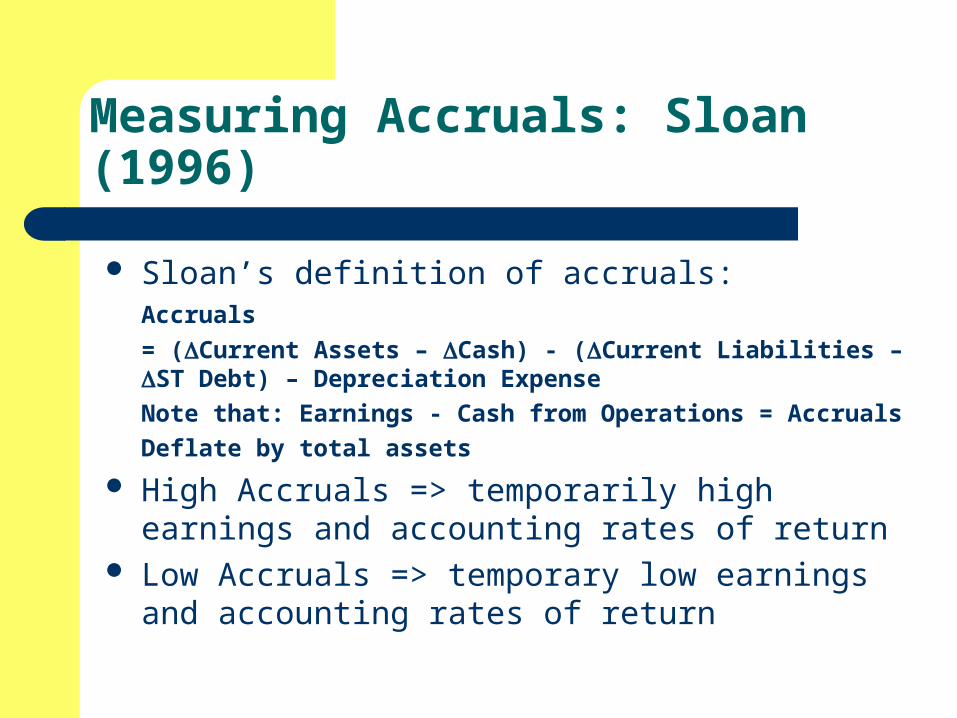

Measuring Accruals: Sloan (1996)

Sloan’s definition of accruals:Accruals

= (Current Assets – Cash) - (Current Liabilities – ST Debt) – Depreciation Expense

Note that: Earnings - Cash from Operations = Accruals

Deflate by total assets

High Accruals => temporarily high earnings and accounting rates of return

Low Accruals => temporary low earnings and accounting rates of return

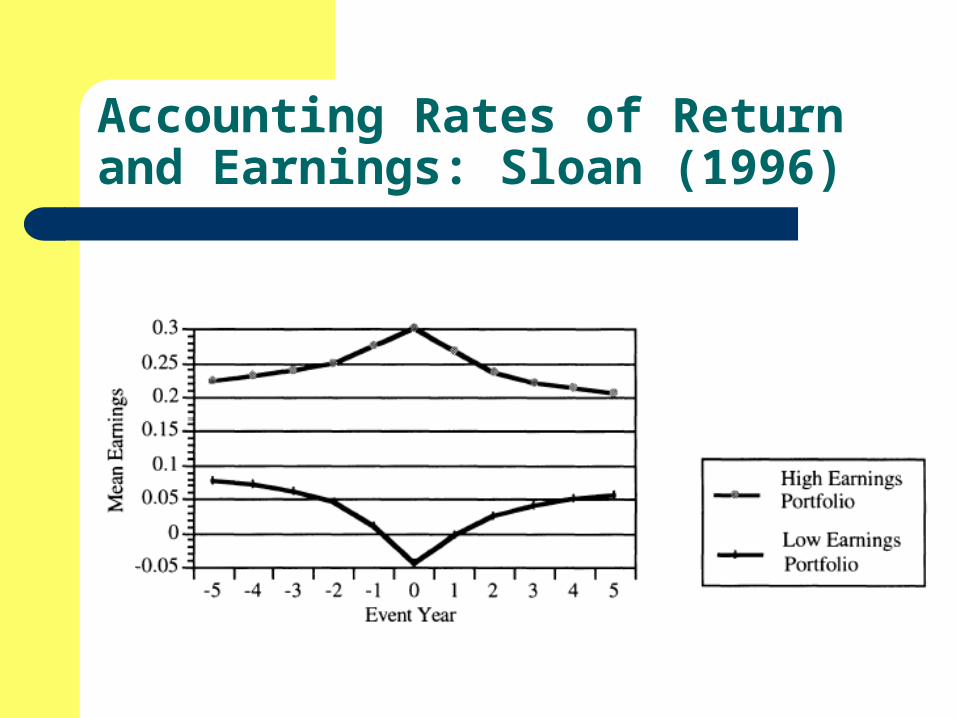

Accounting Rates of Return and Earnings: Sloan (1996)

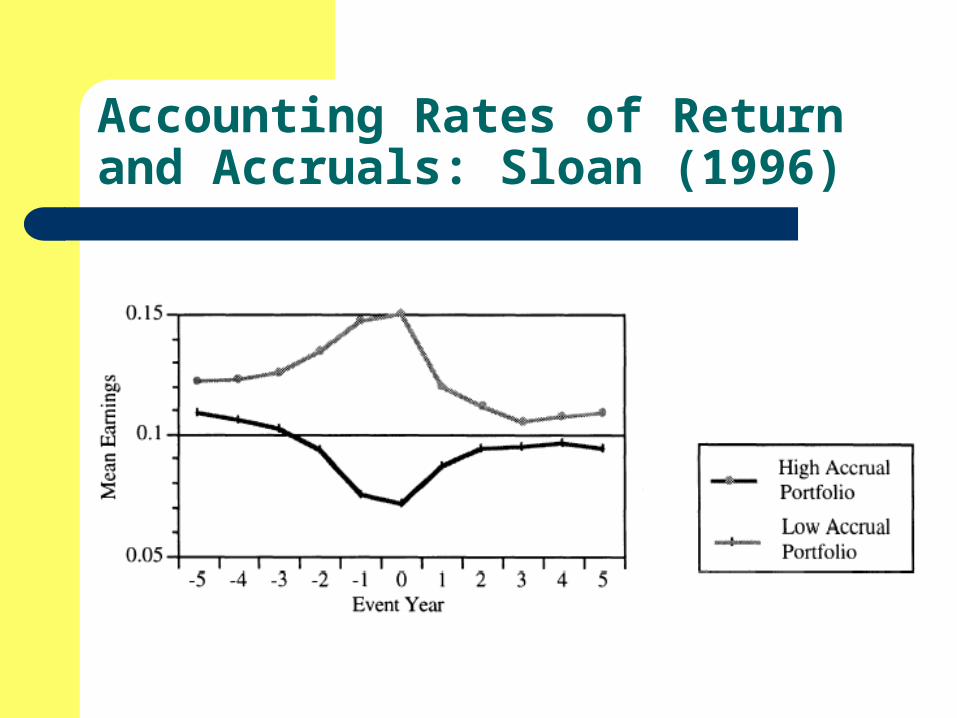

Accounting Rates of Return and Accruals: Sloan (1996)

Accounting Rates of Return and Cash Flows: Sloan (1996)

Future Stock Returns and Accruals: Sloan (1996)

Concluding Comments

Quality of earnings analysis yields significant insights into the sustainability of earnings, and these insights do not appear to be incorporated into stock prices on a timely basis.

Quantitative methods, like those just covered, work well. Detailed fundamental analysis should yield further rewards.