Enablers of TMT support fr integrated management control systems innovations

25

Enablers of top management team support for integrated management control systems innovations Jessica Lee a , Mohamed Z. Elbashir b , Habib Mahama a,d, ⁎, Steve G. Sutton c,1 a Research School of Accounting and BIS, Australian National University, Canberra ACT 0200, Australia b College of Business and Economics, Qatar University, Doha, P.O. Box 2713, Qatar c College of Business Administration, University of Central Florida, P.O. Box 161400, Orlando, FL 32816, United States d College of Business and Economics, United Arab Emirates University, P.O. Box 15556, Al-Ain, UAE article info abstract Article history: Received 7 January 2013 Received in revised form 22 July 2013 Accepted 28 July 2013 Top management team (TMT) support has been identified as one of the most important critical factors to the success of management control systems (MCS) innovations. However, prior studies have taken TMT support for MCS innovations as a given rather than considering the factors that determine whether that support will actually exist and the extent thereof. Prior studies also follow a monolithic approach and treat TMT support for MCS innovations as a black box rather than a combination of processes and stages that develop sequentially over time. We conceptualise TMT support for MCS innovations as consisting of two stages (TMT belief and participation in MCS innovations). We draw on Upper Echelon and knowledge creation theories to motivate and test four enablers of TMT support for an integrated MCS innovation. We theorize the four enablers as TMT's strategic IT knowledge, TMT knowledge creation processes, CIO's strategic business and IT knowledge, and the interaction between TMT and the CIO. We test the research model using survey data that was collected from 347 Australian organisations. The results from the data analyses confirm the hypothesised relationships, supporting the theorized synergies among the four antecedents to TMT support. There are several implications for theory and practice that should be considered in future studies examining the role of TMT in supporting new MCS innovations. © 2013 Elsevier Inc. All rights reserved. Keywords: Top management team support Integrated management control systems TMT belief TMT participation TMT's strategic IT knowledge TMT knowledge creation processes CIO's strategic business knowledge TMT/CIO interaction International Journal of Accounting Information Systems 15 (2014) 1–25 ⁎ Corresponding author. Tel.: +61 2 6125 4857. E-mail addresses: [email protected] (J. Lee), [email protected] (M.Z. Elbashir), [email protected] (H. Mahama), [email protected] (S.G. Sutton). 1 Tel.: +1 407 823 5857. 1467-0895/$ – see front matter © 2013 Elsevier Inc. All rights reserved. http://dx.doi.org/10.1016/j.accinf.2013.07.001 Contents lists available at ScienceDirect International Journal of Accounting Information Systems

-

Upload

jessica-lee -

Category

Documents

-

view

258 -

download

0

Transcript of Enablers of TMT support fr integrated management control systems innovations

International Journal of Accounting Information Systems 15 (2014) 1–25

Contents lists available at ScienceDirect

International Journal of AccountingInformation Systems

Enablers of top management team support

for integrated management controlsystems innovationsJessica Lee a, Mohamed Z. Elbashir b, Habib Mahama a,d,⁎, Steve G. Sutton c,1

a Research School of Accounting and BIS, Australian National University, Canberra ACT 0200, Australiab College of Business and Economics, Qatar University, Doha, P.O. Box 2713, Qatarc College of Business Administration, University of Central Florida, P.O. Box 161400, Orlando, FL 32816, United Statesd College of Business and Economics, United Arab Emirates University, P.O. Box 15556, Al-Ain, UAE

a r t i c l e i n f o

⁎ Corresponding author. Tel.: +61 2 6125 4857.E-mail addresses: [email protected] (J. Lee),

(H. Mahama), [email protected] (S.G. Sutton).1 Tel.: +1 407 823 5857.

1467-0895/$ – see front matter © 2013 Elsevier Inc.http://dx.doi.org/10.1016/j.accinf.2013.07.001

a b s t r a c t

Article history:Received 7 January 2013Received in revised form 22 July 2013Accepted 28 July 2013

Topmanagement team (TMT) support has been identified as one of themost important critical factors to the success of management controlsystems (MCS) innovations. However, prior studies have taken TMTsupport for MCS innovations as a given rather than considering thefactors that determine whether that support will actually exist andthe extent thereof. Prior studies also follow a monolithic approach andtreat TMT support for MCS innovations as a black box rather than acombination of processes and stages that develop sequentially overtime. We conceptualise TMT support for MCS innovations as consistingof two stages (TMT belief and participation in MCS innovations). Wedraw on Upper Echelon and knowledge creation theories to motivateand test four enablers of TMT support for an integratedMCS innovation.We theorize the four enablers as TMT's strategic IT knowledge,TMT knowledge creation processes, CIO's strategic business and ITknowledge, and the interaction between TMT and the CIO. We testthe research model using survey data that was collected from 347Australian organisations. The results from the data analyses confirm thehypothesised relationships, supporting the theorized synergies amongthe four antecedents to TMT support. There are several implications fortheory and practice that should be considered in future studiesexamining the role of TMT in supporting new MCS innovations.

© 2013 Elsevier Inc. All rights reserved.

Keywords:Top management team supportIntegrated management control systemsTMT beliefTMT participationTMT's strategic IT knowledgeTMT knowledge creation processesCIO's strategic business knowledgeTMT/CIO interaction

[email protected] (M.Z. Elbashir), [email protected]

All rights reserved.

2 J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

1. Introduction

The purpose of this study is to examine the enablers of top management team (TMT) members' supportfor integrated management control systems (MSC) innovations. Since Johnson and Kaplan's (1987)publication of “Relevance Lost: the Rise and Fall of Management Accounting”, there has been significantattempts at innovatingmanagement accounting techniques and controls with the view to regaining practicalrelevance. More recently, management control innovations have focused on leveraging existing controls bytaking advantage of the generative, analytical, and integrative capacity of information technology (IT) todevelop integrated management control systems (Rom and Rohde, 2006; Williams and Williams, 2007;Grabski et al., 2011). The focus on “integrated”MCS rather than isolatedMCS stems from thewell-establishedview in management accounting literature that the management control systems of organisations do notoperate in isolation; rather they are interrelated and work as a package (Otley, 1980; Dent, 1990; Chenhall,2003; Malmi and Brown, 2008). The central issue in packaging controls through IT-based innovations is theirability to provide useful information through combining complementary management controls as a package.While in principle these innovations offer significant transformative capacities in the management control oforganisations, research indicates that there is lower than expected adoption and implementation of theseinnovations (Granlund, 2011). The existing literature suggests that the lower uptake of these innovations isdue to lack of top management team (TMT) support. Consequently, this paper focuses on examining thefactors that drive TMT support for integrated MCS innovations.

Prior studies indicate that the role of TMT support is crucial for the successful adoption, implementationand use of MCS innovations. For instance, in contingency-based research, TMT leadership and support is oneof the important organisational contingencies that determine the design and use of various MCS innovations(see for example, Cotton et al., 2003; Cavalluzzo and Ittner, 2004; Chenhall, 2004). Similarly, the strategicmanagement literature highlights the important role that TMT plays in the design and use of MCS (Carpenteret al., 2004; Wilkin and Chenhall, 2010).2 This line of research attributes the positive relationship betweenTMT support and the deployment of MCS to the authority and power inherent in TMT (Hambrick andMason,1984; Abernethy et al., 2010). Support by TMT is crucial as that determines the sufficiency of resources (suchas finances, time, information and human resources) committed to MCS innovations (Anderson and Young,1999; Chenhall, 2004; Naranjo-Gil andHartmann, 2007) and also signals to organisationalmemberswhat topmanagers consider strategically important to delivering outcomes.

Given the importance of TMT support for MCS innovation, most prior studies assume that such supportwill flow naturally and almost certainly for MCS innovation in all cases. Contrary to this, some existingresearch suggests that the nature and form of TMT support for MCS innovations are built over time anddepend on several cognitive, psychological, and contextual factors (Hambrick et al., 1993; Lewis et al., 2003).Recent studies also show that the level of TMT support for MCS innovations varies across organisations(Anderson and Young, 1999; Liang et al., 2007). This evidence implies that rather than taking TMT support forMCS innovations as a given, it is essential to investigate and understand the enablers of the support. In doingso, this will enhance the theoretical and empirical links between their assumed reasons of existence and theirimpact on MCS innovations (Shields and Shields, 1998; Chenhall, 2003; Luft and Shields, 2003). Identifyingthe enablers of TMT support forMCS innovationwill also help future research to build and test richer researchmodels that link the antecedents of TMT support for MCS to organisational choices and outcomes.

This study makes several contributions to the current MCS literature. The study opens the black box ofTMT support forMCS innovations by building and testing a richermodel of the drivers of TMT support forMCSinnovations. From a pragmatic standpoint, this study informs practitioners and consultants on how togenerate TMT support for MCS innovations. By knowing these factors, organisations will be able to enhancethem and achieve higher TMT support for integrated MCS innovation.

The structure of the remainder of the paper is as follows. The following section presents the theoreticaldevelopment of the research model and hypotheses. An overview of the methodology, operationalization ofconstructs, data analysis, and discussion of results follow. We conclude with a discussion of limitations andimplications of the findings for practice and future research.

2 Upper echelon literature argues that organisations do not make choices but they are the reflection of its top managers who makethose choices and decisions (Hambrick and Mason, 1984).

3J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

2. Literature review and hypotheses development

2.1. The concept of TMT support

MCS have evolved over time since Johnson and Kaplan's (1987) book entitled “Relevance Lost: the Riseand Fall of Management Accounting”. Johnson and Kaplan (1987) recognised that traditional managementaccounting procedures used at that time had lost their relevance to manager's planning, control, and decisionmaking asmanagement accounting had failed to keep pacewith changes in the organisational landscape, andwere often “too late, too aggregated and too distorted to be relevant for planning, decision making andcontrol” (Johnson and Kaplan, 1987, p. 1). For management accounting to be relevant and applicable formanagement control in organisations, management accounting processes need to keep pace with thechanging and evolving information and control needs of organisations (Johnson and Kaplan, 1987). Johnsonand Kaplan (1987) argued that the relevance of management accounting and control systems should beregained by capitalising on significant developments in information technology, which can enable anexpansion of organisational information gathering and processing capabilities. These technologicaldevelopments have grantedmanagement accounting researchers and practitioners the foundation to explorepossibilities for improving the relevance of management control systems.

The combination of Johnson and Kaplan's (1987) call for relevance and advances in informationtechnology has led to the development of a number of MCS innovations; including activity-based costmanagement (ABC/M), performance measurement systems (PMS), activity-based budgeting (ABB) andbeyond budgeting (Kaplan and Norton, 1992; Anderson and Young, 1999). A more recent innovation is theintegrated MCS which employs information technology (IT) paradigms to combine several standalone MCSinnovations to generate reports for cybernetic controls (Elbashir et al., 2011). By facilitating such integrationand allowing organisations to use themas amultifarious package, integratedMCS innovations further amplifythe capabilities of these MCS innovations (Williams, 2004, 2008). Once integrated MCS innovations areconnected to the organisational central databases, they can draw on broad-scale data to deliver an expandedset of relevant, accurate and timely management accounting information (Howard, 2003; Brignall andBallantine, 2004;Williams, 2004, 2008). For instance, information generated byABC/Mcan be fed into ABB, andbeused as an input for BSC simultaneously. As such, integratedMCS innovations are able to deliver an extensiveset of business analytics, key performance indicators, and pre-built managementmetrics and reports (Howard,2003; Williams, 2004, 2008).3 Thus, integrated MCS innovations are increasingly valued for their provision ofmanagement control reports and information, which improves management decisionmaking across the valuechain and enhances the performance of a range of business processes (Elbashir et al., 2008).

While in principle the benefits of various MCS innovations are obvious, studies over the past ten years havefound that in practice the adoption rates of various MCS innovations are relatively low (Chenhall, 2004; Nixonand Burns, 2012). For instance, Hendricks et al. (2012) show that only 23.5% of Canadian firms across a range ofindustries adopted the balanced scorecard (BSC). These findings are inconsistent with the value-enhancingevidence cited in the MCS innovation literature. Consequently, this line of research has prompted researchersto examine the drivers of successful adoption, implementation and use of MCS innovations. In doing so,TMT support is often identified as one of the, if not the most, important success factors for MCS innovations(e.g., Shields, 1995; Anderson and Young, 1999; McGowan and Klammer, 1997; Krumwiede, 1998).

Top management team (TMT) is defined in prior literature as a group of the most influential seniorexecutives, such as the Chief Executive Officer (CEO), Chief Operating Officer (COO), and Chief FinancialOfficer (CFO), with an overall responsibility for the organisation (Hambrick andMason, 1984; Armstrong andSambamurthy, 1999; Henri, 2006). TMT are heavily involved in the strategic decisionmaking of organisations(Simons et al., 1999; Collins and Clark, 2003), and plays a significant role in influencing the organisationalstrategies, choices and outcomes (Hambrick and Mason, 1984; Carpenter et al., 2004). It is partly theinfluential role of TMT that leads researchers to argue that the support TMT offers is crucial to adoption,implementation and use of MCS innovations. Despite the overwhelming evidence on the role of TMT in MCSinnovation success, their level of support varies across organisations. It is unclear why TMT in someorganisations fail to provide the support required for MCS innovations. Existing research suggests that the

3 Davila and Foster (2007) identified 46 specific categories of MCS, all of which are supported by the extensive set of pre-builtreports and metrics included in most BI-enabled MCS innovations (Howard, 2003).

4 J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

nature and form of TMT support is built over time and depends on several contextual factors (Lewis et al.,2003). Building on the knowledge management and innovation literature, the current study develops andtests a model of TMT support for integrated MCS innovation and the enablers of such support.

While TMT support is said to be crucial, there is inconsistency in the way researchers conceptualise it(Anderson, 1995; Shields, 1995; Anderson and Young, 1999). For instance, one group of studies refer to TMTsupport as TMT participation, including their contribution in physical activities related to MCS innovations(Norris, 2002). This includes providing adequate resources, such as time, money and personnel by TMT tosupport MCS innovations (e.g., Shields, 1995; Foster and Swenson, 1997; Krumwiede, 1998; Brown et al.,2004; Chenhall, 2004). Another group of studies refer to TMT support as TMT beliefs, that is, the psychologicalstate of TMT towards MCS innovations (e.g., Powell, 1995; Liu and Pan, 2007; Sartorius, 2007). For instance,Liu and Pan (2007) refer to TMT support as TMT's enthusiasm for encouraging innovative ideas. The viewfollowed in this study is consistent with the innovation literature that TMT support is not either/or but is bothparticipation (physical activities) and belief (psychological state) and that theoretical models of TMT supportshould encompass both TMT participation and TMT beliefs (Chatterjee et al., 2002).

Our research focuses on examining these two dimensions of TMT support for integrated MCS innovation.Specifically, we propose that TMT support is built in two stages (belief and participation) and show the pathdependence between these two stages. We build and test a research model that depicts the factors that drivethese two stages of TMT support. In particular, the research model suggests that TMT's strategic IT knowledge,TMT knowledge creation modes, CIO business and IT knowledge, and the level of interaction between CIO andTMTmembers will drive TMT support for integratedMCS innovation. Fig. 1 depicts the conceptual model testedin this study.

2.2. TMT beliefs and TMT participation in integrated MCS innovation

TMT participation in integrated MCS innovations refers to a set of physical activities performed by seniorexecutives in the management of MCS innovations (Chatterjee et al., 2002). TMT participates by playingactive roles in planning activities related toMCS innovations (Chatterjee et al., 2002). This can range from thearticulation of a vision for the organisational use of MCS innovations, to the formulation of plans andstrategies to translate such visions into reality. TMT are also responsible for establishing appropriate goals andstandards to monitor MCS innovations (Chatterjee et al., 2002). It may also involve either shaping theorganisational context tomake itmore adaptive to theMCS or facilitating the adoption of theMCS innovationto the characteristics of the organisation (Sharma and Yetton, 2003). Engaging in these activities requiresubstantial commitment of costly human and material resources. As the resources available to TMT arelimited, they can and will only direct resources to these activities if they are convinced about the value of theMCS innovation to the organisation (Chenhall, 2004).

Fig. 1. Research model and hypotheses.

5J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

We argue that TMT belief in MCS innovation is an important factor that explains TMT participation. TMTbeliefs in MCS innovations refer to the subjective psychological state and probability estimates of TMT,reflecting the degree of importance and significance TMT accord to MCS innovations in organisations(Chatterjee et al., 2002). As stated by Chatterjee et al. (2002), TMT beliefs encompass the extent to whichsenior executives believe that MCS innovations have the potential of providing significant business benefitsand competitive advantages, as well as the extent to which TMT believe that MCS innovations are able tosupport the business activities and strategies of the organisation. We expect such beliefs to be positivelyassociated with the level of TMT participation in integratedMCS innovation. This expectation is supported bythe Theory of Reasoned Action (TRA) (Fishbein and Ajzen, 1975; Ajzen and Fishbein, 1980) and the relatedTechnology AcceptanceModel (TAM) (Davis, 1989; Davis et al., 1989). According to TRA, TMTwill participatein MCS innovations-related activities if they believe that MCS innovations are valuable and relevant to theorganisation. Likewise, according to the TAM literature TMTwill increase their participation in activities thatwill enhance theMCS innovations if they believe the innovations to be useful in enhancing their performanceas decision makers. The above discussion leads to the following hypothesis:

H1. TMT's belief in an integrated MCS innovation has a positive effect on TMT's participation in theinnovation.

2.3. Enablers of TMT belief in integrated MCS innovation

TMT beliefs are subjective probability estimates about the consequences of an action (Lewis et al., 2003).Lewis et al. (2003) suggest that TMT develop beliefs about innovation after incorporating their assessments ofvarious outcomes associated with the organisational use of such innovation. Such assessments are results ofthe process through which TMT gather, synthesise and assess information about innovations (Lewis et al.,2003). Similarly, Agarwal (2000) suggests that TMT's beliefs are formed as a result of their cognitiveevaluations of information relating to the consequences of accepting or using innovation. As such, knowledgeand information serve as the basis for TMT beliefs about innovation.

2.4. TMT's strategic IT knowledge and TMT beliefs in integrated MCS innovations

TMT's strategic IT knowledge refers to TMT's understanding of themerits, opportunities and advantages ofIT in supporting the organisation business strategy (Anderson et al., 2002; Elbashir et al., 2011). It alsoencompasses TMT's awareness of the organisational needs of IT and TMT's attentiveness to the organisationalimpacts of IT (Argyris and Kaplan, 1994).

As integrated MCS innovations draw heavily on IT, TMT's strategic IT knowledge is expected to form thebasis upon which TMT come to identify the benefits, relevance and value of this innovation (Walsh, 1988;Thomas andMcDaniel, 1990). Strategic IT knowledge will enable TMT to form their opinion about and assessthe value of integrated MCS innovations for the organisation (Walsh, 1988).

The absorptive capacity literature also suggests that TMT's prior related knowledge influences their abilityto recognise the benefits of MCS innovations. That is, in order to engage in the process of collecting,synthesising and assessing information related to integratedMCS innovation, TMTmust have prior related ITknowledge (Thomas and McDaniel, 1990). Strategic IT knowledge will enable TMT to form beliefs aboutintegrated MCS innovation. This leads to the following hypothesis:

H2. TMT's strategic IT knowledge has a positive effect on TMT belief in integrated MCS innovations.

2.5. TMT knowledge creation process and TMT beliefs in integrated MCS innovations

TMT's knowledge creation process captures the action and interactionmodes that enable TMT to generatenew knowledge and renew existing knowledge (Nonaka, 1994; Nonaka and Takeuchi, 1995; Nonaka et al.,2000). According to the knowledge creation framework, TMT are exposed to new information about MCSinnovations through knowledge creation activities including socialising with other individuals andexperimenting with new innovative ideas and managerial techniques. IT people are a key source throughwhich TMT gathers information about MCS innovations (Lewis et al., 2003). Such information may come in

6 J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

different forms of modality, such as oral, written or observation. Through processing of information receivedfrom internal and external sources, TMT will be able to create new knowledge (Nonaka, 1994; Nonaka andTakeuchi, 1995; Nonaka et al., 2000). This new knowledge will enable TMT to draw on it as a reference informing their estimates of the organisational benefits of MCS innovations (Wyer and Radvansky, 1999).Therefore, the process of knowledge creation enlarges the cognitive resources available for TMT to drawon asreference knowledge, thereby solidifying TMT's belief in an integrated MCS innovation. This leads to thefollowing hypothesis:

H3. TMT's knowledge creation process has a positive effect on TMT's belief in integratedMCS innovations.

2.6. CIO's strategic business and IT knowledge and TMT belief in integrated MCS innovations

CIO's strategic business and IT knowledge encompasses the CIO's understanding of the organisation'soverall business domain, competitive forces, core capabilities, strategic goals, products and services, andrelated IT innovations (Armstrong and Sambamurthy, 1999; Bassellier and Benbasat, 2004). It also reflectsCIO's awareness of TMT's strategic and tactical thinking, and the ability to perceive organisational needs for ITinnovations (Watson, 1990). CIOs with strategic business and IT knowledge are expected to positivelyinfluence TMT's estimates of the organisational benefits of integrated MCS innovations (Agarwal, 2000).

As integrated MCS innovations are based on IT, TMT rely heavily on CIOs who possess greater relevantexpertise (Enns et al., 2003a,b, 2007). CIOs with strategic business and IT knowledge are able to “organise keyarguments, assemble supporting data, (and) carefully think through the context of the delivery” to influenceTMT's estimates of likelihood that MCS innovations are able to provide organisational benefits (Enns et al.,2007, p. 34). They are able to argue a compelling and rational case for howMCS innovations are important andrelevant to the organisation (Enns et al., 2003a,b, 2007).

Strategic business and IT knowledge enables CIOs to recognise and communicate the organisational needsfor MCS innovations. These CIOs are also able to capture the kernel of success stories of integrated MCSinnovations from elsewhere, and conceptualise the potential relevance of these opportunities and benefits tothe organisation (Smalts et al., 2006). In addition, CIOswith strategic business and IT knowledge are able to usenon-technical business language to communicate and interact with other TMT members (Bassellier andBenbasat, 2004; Enns et al., 2007) and are able to translate the language of IT into the language of business (andvice versa). They are also able to develop MCS innovations measures based on business effectiveness criteria,such as cost reduction, inventory reduction and business process productivity (Applegate and Elam, 1992).

Moreover, with strategic business and IT knowledge, CIOs are able to align MCS innovations with theoverall strategic direction of the organisation. Such knowledge enables CIOs to recognise and identifyinnovative ways of blending the capabilities of MCS innovations with the organisational needs, priorities andopportunities (Smalts et al., 2006). By havingMCS innovationswhich are consistentwith the overall strategicdirection of the organisation, CIOs are able to positively influence TMT's estimates of the organisationalbenefits of MCS innovations (Enns et al., 2003a,b; Bassellier and Benbasat, 2004). In addition, with strategicbusiness and IT knowledge, CIOs are perceived to be an executive, rather than a mere functional manager(Enns et al., 2001, 2007). This is important as TMT's information processing capacity may be saturated attimes. In such cases, the ability of TMT to make subjective estimates of the benefits of integrated MCSinnovation is impaired. This may cause TMT to rely and endorse CIO's recommendation that integrated MCSinnovations are important and relevant to the organisation (Agarwal, 2000; Lewis et al., 2003). Therefore,CIOs with strategic business and IT knowledge are able to positively influence TMT's subjective estimates ofthe benefits of integratedMCS innovations to the organisation, increasing their beliefs in theMCS innovations.This leads to the following hypothesis:

H4. CIO's strategic business and IT knowledge have a positive effect on TMT's belief in integrated MCSinnovations.

2.7. TMT/CIO interactions and TMT belief in integrated MCS innovations

As indicated earlier, TMT belief in integrated MCS innovations is a function of the subjective probabilityestimates about the organisational value of the innovations. An important factor in these probability

7J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

estimates is the extent of strategic alignment of the innovation. That is, the alignment between businessstrategy and the various dimensions of integrated MCS innovation and the shared cognition of CIOs andTMT about the business value of this innovation (Preston and Karahanna, 2009). Preston and Karahanna(2009) argue that the nature of interaction between CIOs and TMT is vital to facilitating strategicalignment and shared cognition of the business value of MCS innovation.

TMT/CIO interactions create a platform or a mechanism for TMT to infuse strategic thinking into MCSinnovation processes by communicating the information processing and control requirements to CIOs. Thisprovides the CIOs the opportunity to improve their knowledge about organisational needs for MCS innovationand to tailor MCS innovation activities towards meeting those needs (Doll, 1985). TMT/CIO interaction alsoallows CIOs to articulate the strategic relevance of MCS innovation by highlighting both the tangible andintangible values ofMCS innovation directlywith TMT. The question and answer approach that generally guidessuch interactive settings also creates opportunities for TMT to seek clarification on the nature of MCSinnovations; the strategic, operational and resource implications of such innovation; and theway the innovationprocess is to be managed. Seeking such clarification allows CIOs to better explain how MCS innovations arealigned to organisational strategy and the value that will emanate from such strategic alignment.

In addition, the Upper Echelons theory suggests that TMT beliefs and strategic choices reflect the cognitivebasis of TMTmembers (Preston andKarahanna, 2009), hence shared cognition between TMT and CIOs has thepropensity to influence TMT belief in MCS innovation. Shared cognition is an important basis for effectivelyintegrating strategic business knowledge with integrated MCS innovation and thus allows for bettercommunication of the meaning and relevance of such innovations to value creation within the organisation.We argue that the exchange of knowledge and information that takes place when TMT and CIOs interactfacilitates the development of shared cognition among them about how MCS innovation can be used toenhance organisational capabilities and leverage organisational value (Armstrong and Sambamurthy, 1999;Preston and Karahanna, 2009). As such, it is theorized that the interaction between TMT and the CIO willinfluence TMT belief about integrated MCS innovations. This leads to the following hypothesis:

H5. The level of interaction between TMT and the CIO has a positive effect on TMT's belief in integratedMCS innovations.

3. Research method

Datawas collected through a large field survey of customers froman international BI software vendor. TheBI vendor distributes BI software that combinesmultiple cybernetic control tools (such as activity-costing andmanagement, balanced scorecard, KPIs, etc.) as a package of integrated MCS. This integrated MCS providesaccess to over 200 different pre-built reports based on more than 500 KPIs and analytics designed to answerover 2900 business critical questions.

The use of clients from a single vendor controls for potential variations in capabilities of BI softwareprovided by different BI vendors. The vendor provided a contact list of their clients under a writtennon-disclosure agreement. Where possible, multiple respondents from each organisation were selected fromthe vendor's contact list. For organisationswhichhad one contact person on the list, the organisationwas onlyselected if the contact personwas a seniormanager such as a CEO, CFO, or CIO. Amultiple respondent strategywas preferred as it enables collection of rich data, mitigates potential bias, and enhances accuracy (Huber andPower, 1985; Sethi and King, 1994).

The survey was conducted in accordance with the guidance of Dillman et al. (2009). Survey packetscontaining a printed copy of the survey, along with a cover letter and reply-paid envelope were posted toparticipants. After four weeks, a reminder was emailed to all participants. A second survey package wasmailed to the non-respondents four weeks after the first reminder. Two weeks later, a third and finalreminder alongwith a link to the online version of the surveywas emailed to thosewho had not responded tothe second survey package. On average, three respondents from each targeted organisation received thesurvey. The survey was sent to 1873 managers in 612 organisations. A total of 419 usable responses werereceived from 220 organisations. This resulted in response rate of 22% for individual responses.4 Respondents

4 An ANOVA test was performed to compare the paper-based responses with the on-line responses. No significant differences arefound on any of the main variables of the study, which indicates that the different data collection modes that have been used in thestudy did not create a response bias.

8 J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

were given the option to respond for the organisation as a whole or for the strategic business unit (SBU) inwhich they worked. This option allowed for the possibility that in the case of very large organisations it couldbe difficult for an individual to assess the entire company. Using the responses for SBUs as uniqueorganisational responses, the responses represent 347 organisations.

The consistency of responses from multiple respondents of the same organisation is examined usingtwo tests: (1) computing the correlation between multiple responses (Armstrong and Sambamurthy,1999), and (2) the co-efficient of the inter-class correlation (ICC) (Shrout and Fleiss, 1979). All correlationsbetween multiple respondents of the same organisation were found to be highly significant. The ICCcoefficients for all the raters (between 2 and 5 responses per organisation) range from 0.76 to 0.94. Theresults of the two tests provide strong evidence of consistency between multiple responses from a singleorganisation. In such cases, the average score from multiple respondents was used as the response of theTMT as a whole. On the other hand, for firms with a single respondent, the individual response was used torepresent TMT.

To test for non-response bias, early and late responses on the main variables of the study were comparedin paired samples of 150, 100, 50, and 40 responses using an ANOVA test. Responses that we receivedfollowing the second reminder were also compared with those received before the reminder. The resultsreveal no significant differences on the responses across these paired samples indicating an absence ofresponse bias. Out of the respondents indicating theywere unable to complete the survey, 70 noted companypolicy precluded their completion of the survey. Moreover, 37 respondents indicated other members fromtheir company had responded on their behalf, 11 had left their company, and 8 indicated that the survey wasnot relevant to them.

Exploratory Factor Analysis (EFA) was used to perform Harman's one-factor test that examineswhether a common method variance problem exists (Podsakoff and Organ, 1986). The results of theanalysis show that there are at least seven “unrotated” factors that account for 70% of the variance in themeasurement items used. We also performed additional tests for commonmethod variance as suggestedin prior literature (Podsakoff and Organ, 1986; Podsakoff et al., 2003). We added amarker variable that isnot relevant to the TMT support construct tested in the study and we examined the research model bothwith and without the marker variables. The results show that the results do not change and the markervariable is not significant. We also added the highest factor from the unrotated explanatory factoranalysis to the PLS model as a control variable. The findings also show that the results of the originalmodel are not affected by the control “general factor” variable. The results from all these tests indicatethat there is no significant common method variance that threatens the quality of the data (Zhuang andLederer, 2003).

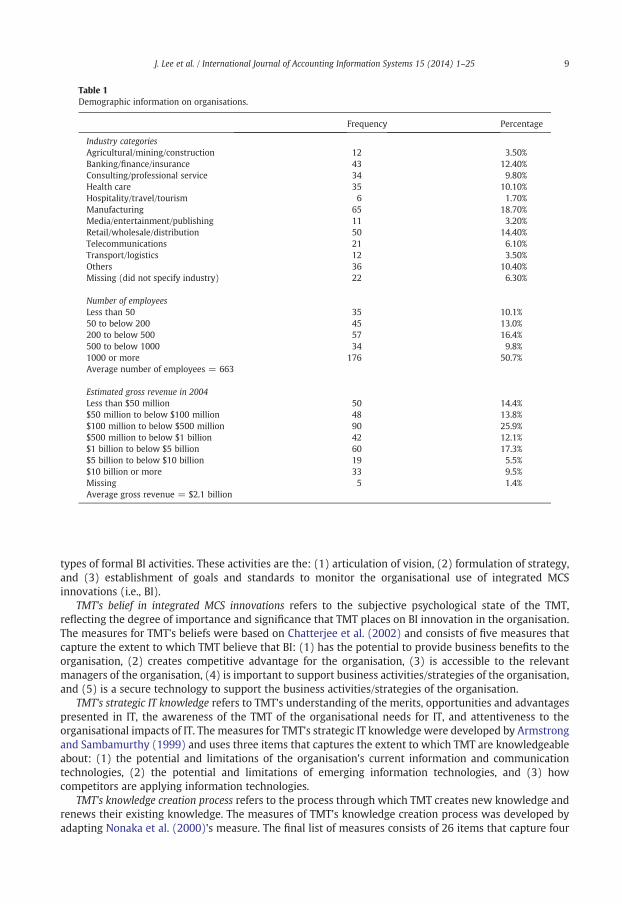

3.2. Demographics

Information was collected from the respondents on their organisations (see Table 1). Responses arepredominantly from large organisations with an average of 663 employees and gross revenue of over A$2 billion per year. About half (50.7%) of the organisations in the survey sample had at least 1000employees; about a quarter (25.9%) had gross revenue ranging from $100 million to below $500 million.The largest industry grouping was manufacturing, accounting for 18.7% of all survey respondents. This wasfollowed by retail, wholesale, and distribution (14.4%), and then banking, finance, and insurance (12.4%).Hospitality, travel and tourism received the least representation in the sample (1.7%).

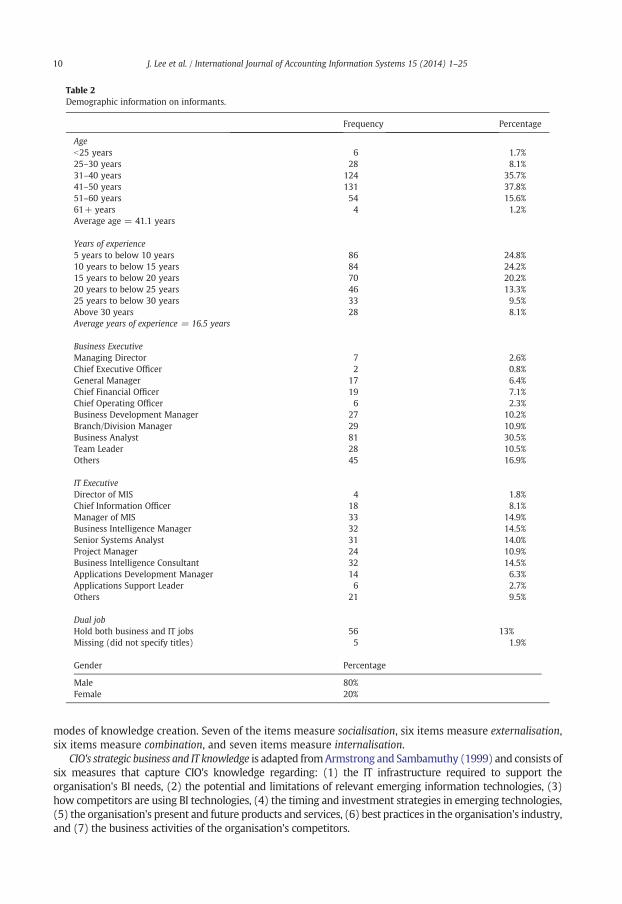

The respondents also provided personal demographic data (see Table 2). The average age of respondentswas 41.1 years with 16.5 years of work experience, and 80% of respondents being male. 54% of respondentsclassified themselves as executives/managers, 46% as IT executives/managers, and 13% held both businessand IT jobs.

3.3. Operationalization of constructs

TMT's participation in integrated MCS innovations refers to a set of physical activities performed by thesenior executives in the management of MCS innovations as they pertain to BI in this study. TMT'sparticipation in integrated MCS innovations is measured in this study by using a three-item scale adaptedfrom Chatterjee et al. (2002). The items measure the extent to which TMT actively participates in three

Table 1Demographic information on organisations.

Frequency Percentage

Industry categoriesAgricultural/mining/construction 12 3.50%Banking/finance/insurance 43 12.40%Consulting/professional service 34 9.80%Health care 35 10.10%Hospitality/travel/tourism 6 1.70%Manufacturing 65 18.70%Media/entertainment/publishing 11 3.20%Retail/wholesale/distribution 50 14.40%Telecommunications 21 6.10%Transport/logistics 12 3.50%Others 36 10.40%Missing (did not specify industry) 22 6.30%

Number of employeesLess than 50 35 10.1%50 to below 200 45 13.0%200 to below 500 57 16.4%500 to below 1000 34 9.8%1000 or more 176 50.7%Average number of employees = 663

Estimated gross revenue in 2004Less than $50 million 50 14.4%$50 million to below $100 million 48 13.8%$100 million to below $500 million 90 25.9%$500 million to below $1 billion 42 12.1%$1 billion to below $5 billion 60 17.3%$5 billion to below $10 billion 19 5.5%$10 billion or more 33 9.5%Missing 5 1.4%Average gross revenue = $2.1 billion

9J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

types of formal BI activities. These activities are the: (1) articulation of vision, (2) formulation of strategy,and (3) establishment of goals and standards to monitor the organisational use of integrated MCSinnovations (i.e., BI).

TMT's belief in integrated MCS innovations refers to the subjective psychological state of the TMT,reflecting the degree of importance and significance that TMT places on BI innovation in the organisation.The measures for TMT's beliefs were based on Chatterjee et al. (2002) and consists of five measures thatcapture the extent to which TMT believe that BI: (1) has the potential to provide business benefits to theorganisation, (2) creates competitive advantage for the organisation, (3) is accessible to the relevantmanagers of the organisation, (4) is important to support business activities/strategies of the organisation,and (5) is a secure technology to support the business activities/strategies of the organisation.

TMT's strategic IT knowledge refers to TMT's understanding of the merits, opportunities and advantagespresented in IT, the awareness of the TMT of the organisational needs for IT, and attentiveness to theorganisational impacts of IT. The measures for TMT's strategic IT knowledge were developed by Armstrongand Sambamurthy (1999) and uses three items that captures the extent to which TMT are knowledgeableabout: (1) the potential and limitations of the organisation's current information and communicationtechnologies, (2) the potential and limitations of emerging information technologies, and (3) howcompetitors are applying information technologies.

TMT's knowledge creation process refers to the process through which TMT creates new knowledge andrenews their existing knowledge. The measures of TMT's knowledge creation process was developed byadapting Nonaka et al. (2000)'s measure. The final list of measures consists of 26 items that capture four

Table 2Demographic information on informants.

Frequency Percentage

Ageb25 years 6 1.7%25–30 years 28 8.1%31–40 years 124 35.7%41–50 years 131 37.8%51–60 years 54 15.6%61+ years 4 1.2%Average age = 41.1 years

Years of experience5 years to below 10 years 86 24.8%10 years to below 15 years 84 24.2%15 years to below 20 years 70 20.2%20 years to below 25 years 46 13.3%25 years to below 30 years 33 9.5%Above 30 years 28 8.1%Average years of experience = 16.5 years

Business ExecutiveManaging Director 7 2.6%Chief Executive Officer 2 0.8%General Manager 17 6.4%Chief Financial Officer 19 7.1%Chief Operating Officer 6 2.3%Business Development Manager 27 10.2%Branch/Division Manager 29 10.9%Business Analyst 81 30.5%Team Leader 28 10.5%Others 45 16.9%

IT ExecutiveDirector of MIS 4 1.8%Chief Information Officer 18 8.1%Manager of MIS 33 14.9%Business Intelligence Manager 32 14.5%Senior Systems Analyst 31 14.0%Project Manager 24 10.9%Business Intelligence Consultant 32 14.5%Applications Development Manager 14 6.3%Applications Support Leader 6 2.7%Others 21 9.5%

Dual jobHold both business and IT jobs 56 13%Missing (did not specify titles) 5 1.9%

Gender Percentage

Male 80%Female 20%

10 J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

modes of knowledge creation. Seven of the items measure socialisation, six items measure externalisation,six items measure combination, and seven items measure internalisation.

CIO's strategic business and IT knowledge is adapted fromArmstrong and Sambamuthy (1999) and consists ofsix measures that capture CIO's knowledge regarding: (1) the IT infrastructure required to support theorganisation's BI needs, (2) the potential and limitations of relevant emerging information technologies, (3)how competitors are using BI technologies, (4) the timing and investment strategies in emerging technologies,(5) the organisation's present and future products and services, (6) best practices in the organisation's industry,and (7) the business activities of the organisation's competitors.

11J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

The level of TMT/CIO interaction consists of two measures adapted from Armstrong and Sambamurthy(1999) and uses two items capturing: (1) extent to which the CIO is involved with TMT members, and(2) number of hierarchical levels between CIO and TMT.

3.4. Control variables

Time since adoption is included in the model to control for whether TMT support is built overtime whileTMT becomes familiar with the integrated MCS innovation and experiences the advantages to theorganisation. The longer the organisation uses an integrated MCS innovation, the greater TMT support islikely to be (Purvis et al., 2000). The measure of time since adoption is the number of years since theintegrated MCS innovations were adopted by the organisation.

Organisational size is included in the research model to control for the organisational support that isdriven by the size of resources that the organisation possesses (Zhu and Kraemer, 2002; Subramani, 2004).Prior studies suggest that larger organisations have greater ability to provide support for MCS innovations.

CIO as member of TMT controls for the possibility that TMT support for MCS innovations is influenced by aTMT design which includes the CIO as a member of the TMT. Existing literature suggests that CIOs are able toprovidemore support for IT projects when they form part of TMT (Applegate and Elam, 1992; Armstrong andSambamurthy, 1999).

4. Data analysis

We use Smart PLS (Ringle et al., 2005), a component-based structural equation modelling technique totest both the measurement and structural models.5 The bootstrapping resampling approach was used togenerate 1000 random samples of observations from the original data set. The paths' coefficients werere-estimated using each of these random sample observations. This approach computes the t-statistics andprovides a valid estimate of the significance of the path coefficients (Chin, 1998b).

4.1. Discussion of the measurement model

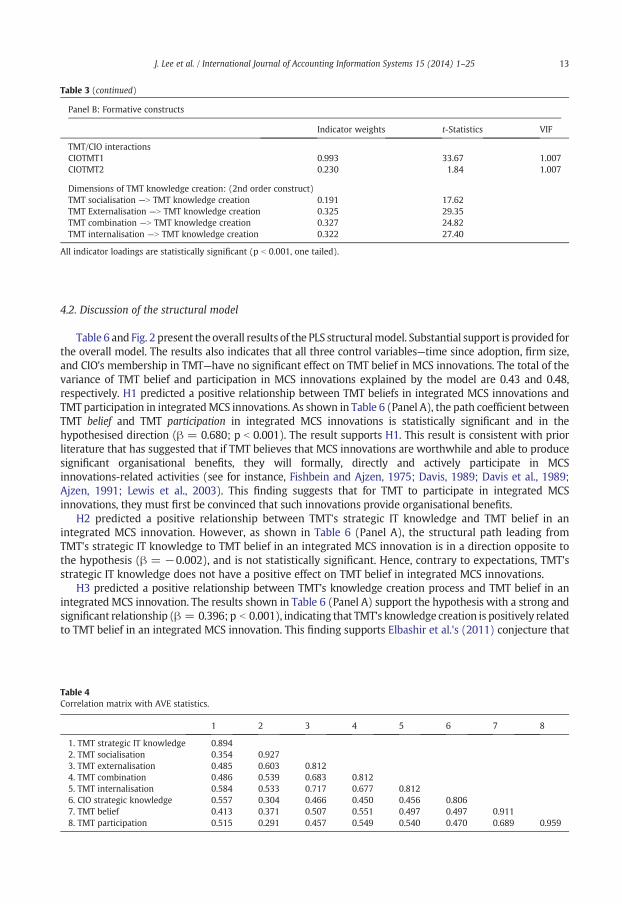

The test of the measurement model includes examining the internal consistency and convergent anddiscriminant validity of the instrument items. All composite reliability scores of the latent constructs(reported in Table 3) are well above the recommended level of .70, thus indicating adequate reliability ofthe reflective item measures for each such construct (Nunnally and Bernstein, 1978). Item loadingstogether with the average variance extracted (AVE) were used to examine the convergent validity of eachconstruct's measure (Van den Bosch et al., 1999). Table 3 shows that all the reflective constructs haveitems loading of above 0.70 which indicates their significant contribution to the measured construct.Moreover, the average variance extracted (AVE) for all constructs was above 0.50, demonstrating theconvergent validity of the measurement items (Fornell and Larcker, 1981). This also indicates that eachmeasured construct explains more than 0.50 of the variation in the observed variables.

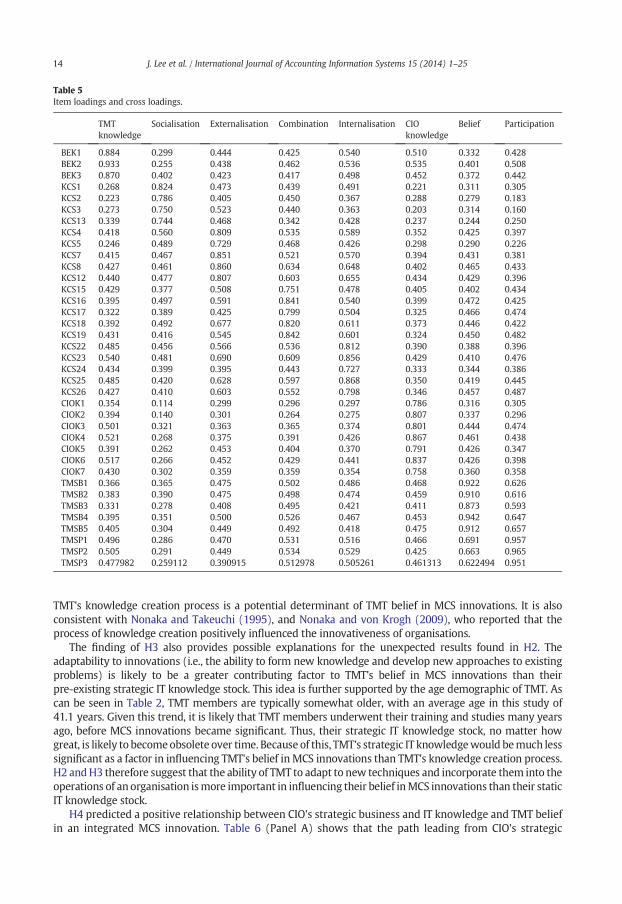

Table 4 shows that the values of the square root of the AVE (on the diagonal) are all greater than theinter-construct correlations (off the diagonal). This demonstrates that the measures exhibit satisfactorydiscriminant validity.6 An additional test of discriminant validity was conducted where each measurementitem is assessed to ensure that it has a higher loading on its assigned factor than on any other factors (Chin,1998b; Gefen et al., 2000); and the results are shown in Table 5. Each of the measurement items loadedhigher on the appropriate construct than on any other construct providing further support for thediscriminant validity of the measures used in the study.

5 PLS is more appropriate than other SEM techniques such as covariance-based SEM because (1) the data used lacks themultivariate distribution, and (2) one of the constructs tested in the research model utilizes measurement models that are formative(interaction between CIO and TMT members). The use of covariance-based SEM to model the construct as formative can result in anunidentified model (Kline, 2006).

6 For satisfactory discriminant validity, the square root of AVE of the construct should be greater than the variance shared betweenthe construct and other constructs in the research model (Chin, 1998a).

Table 3Measurement model statistics.

Panel A: Reflective constructs

Individual item loadings, t-statistics, composite reliability, and average variance extracted (AVE)

Latent variable Loadings t-Statistics

TMT strategic IT knowledge (composite reliability = 0.92; AVE = 0.80)BEK1: The potential and limitations of the organisation's current information and communicationtechnologies

0.884 44.37

BEK2: The potential and limitations of emerging information technologies 0.933 107.86BEK3: How competitors are applying information technologies 0.870 40.51

TMT knowledge creation process (socialisation) (composite reliability = 0.86; AVE = 0.60)KCS1: Share ideas/experiences with clients and suppliers 0.824 37.24KCS2: Share ideas/experiences with external experts 0.786 23.65KCS3: Gather information/ideas from competitors 0.750 23.86KCS13: Engage in dialogue with subordinates to exchange various ideas and knowledge 0.744 24.88

TMT knowledge creation process (externalisation) (composite reliability = 0.91; AVE = 0.66)KCS6 Develop new strategies/business opportunities by… 0.809 38.05KCS7 Make regular contacts with each other through… 0.729 24.50KCS8 Share information/ideas/experiences with… 0.851 46.65KCS9 Demonstrate and model their expertise to other… 0.860 44.55KCS10 Engage in dialogue with subordinates to exchange… 0.807 41.01

TMT knowledge creation process (combination) (composite reliability = 0.91; AVE = 0.66)KCS15 Plan strategies by using computer simulation and… 0.751 26.61KCS16 Gather and summarize information from different… 0.841 44.42KCS17 Build databases on products/services by gathering… 0.799 31.42KCS18 Convene meetings where new concepts and… 0.820 41.64KCS19 Use information technologies to collect/transmit… 0.842 46.05

TMT knowledge creation process (internalisation) (composite reliability = 0.91; AVE = 0.66)KCS22 Experiment with new management practices to… 0.812 38.13KCS23 Are keen to understand different groups' visions… 0.856 54.13KCS24 Read business/IT publications 0.727 19.23KCS25 Use “learning by involvement” in different projects… 0.868 53.84KCS26 Foster a work environment that is supportive of… 0.798 31.47

CIO strategic business and IT knowledge (composite reliability = 0.93; AVE = 0.65)CIOK1: The IT infrastructure required to support the organisation's business intelligence needs 0.786 28.69CIOK2: The potential and limitations of relevant emerging information technologies 0.807 31.40CIOK3: How competitors are using business intelligence technologies 0.801 36.89CIOK4: Timing and investment strategies in emerging technologies 0.867 65.04CIOK5: The organisation's present and future products and service 0.791 30.12CIOK6: What is considered best practice in the organisation's industry 0.837 40.94CIOK7: The business activities of the organisation's competitors 0.758 26.23

TMT's beliefs in MCS innovations (composite reliability = 0.96; AVE = 0.83)TMSB1: Business Intelligence Systems have the potential to provide business benefits tothe organisation.

0.922 93.06

TMSB2: Business Intelligence Systems create competitive advantages for the organisation. 0.910 87.04TMSB3: Business Intelligence Systems are accessible to the relevant managers of the organisation. 0.873 55.52TMSB4: Business Intelligence Systems are important to support business activities/strategies ofthe organisation.

0.942 141.76

TMSB5: Business Intelligence Systems are secure technologies to support business activities/strategiesof the organisation.

0.912 83.99

TMT's participation in MCS innovations (composite reliability = 0.97; AVE = 0.92)TMSP1: Articulating the vision for organisational use of Business Intelligence Systems 0.957 167.62TMSP2: Formulating the strategy for the organisational use of Business Intelligence Systems 0.965 186.59TMSP3: Establishing goals and standards to monitor Business Intelligence Systems projects 0.951 151.28

12 J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

Table 3 (continued)

Panel B: Formative constructs

Indicator weights t-Statistics VIF

TMT/CIO interactionsCIOTMT1 0.993 33.67 1.007CIOTMT2 0.230 1.84 1.007

Dimensions of TMT knowledge creation: (2nd order construct)TMT socialisation —N TMT knowledge creation 0.191 17.62TMT Externalisation —N TMT knowledge creation 0.325 29.35TMT combination —N TMT knowledge creation 0.327 24.82TMT internalisation —N TMT knowledge creation 0.322 27.40

All indicator loadings are statistically significant (p b 0.001, one tailed).

13J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

4.2. Discussion of the structural model

Table 6 and Fig. 2 present the overall results of the PLS structuralmodel. Substantial support is provided forthe overall model. The results also indicates that all three control variables—time since adoption, firm size,and CIO's membership in TMT—have no significant effect on TMT belief in MCS innovations. The total of thevariance of TMT belief and participation in MCS innovations explained by the model are 0.43 and 0.48,respectively. H1 predicted a positive relationship between TMT beliefs in integrated MCS innovations andTMT participation in integratedMCS innovations. As shown in Table 6 (Panel A), the path coefficient betweenTMT belief and TMT participation in integrated MCS innovations is statistically significant and in thehypothesised direction (β = 0.680; p b 0.001). The result supports H1. This result is consistent with priorliterature that has suggested that if TMT believes that MCS innovations are worthwhile and able to producesignificant organisational benefits, they will formally, directly and actively participate in MCSinnovations-related activities (see for instance, Fishbein and Ajzen, 1975; Davis, 1989; Davis et al., 1989;Ajzen, 1991; Lewis et al., 2003). This finding suggests that for TMT to participate in integrated MCSinnovations, they must first be convinced that such innovations provide organisational benefits.

H2 predicted a positive relationship between TMT's strategic IT knowledge and TMT belief in anintegrated MCS innovation. However, as shown in Table 6 (Panel A), the structural path leading fromTMT's strategic IT knowledge to TMT belief in an integrated MCS innovation is in a direction opposite tothe hypothesis (β = −0.002), and is not statistically significant. Hence, contrary to expectations, TMT'sstrategic IT knowledge does not have a positive effect on TMT belief in integrated MCS innovations.

H3 predicted a positive relationship between TMT's knowledge creation process and TMT belief in anintegrated MCS innovation. The results shown in Table 6 (Panel A) support the hypothesis with a strong andsignificant relationship (β = 0.396; p b 0.001), indicating that TMT's knowledge creation is positively relatedto TMT belief in an integrated MCS innovation. This finding supports Elbashir et al.'s (2011) conjecture that

Table 4Correlation matrix with AVE statistics.

1 2 3 4 5 6 7 8

1. TMT strategic IT knowledge 0.8942. TMT socialisation 0.354 0.9273. TMT externalisation 0.485 0.603 0.8124. TMT combination 0.486 0.539 0.683 0.8125. TMT internalisation 0.584 0.533 0.717 0.677 0.8126. CIO strategic knowledge 0.557 0.304 0.466 0.450 0.456 0.8067. TMT belief 0.413 0.371 0.507 0.551 0.497 0.497 0.9118. TMT participation 0.515 0.291 0.457 0.549 0.540 0.470 0.689 0.959

Table 5Item loadings and cross loadings.

TMTknowledge

Socialisation Externalisation Combination Internalisation CIOknowledge

Belief Participation

BEK1 0.884 0.299 0.444 0.425 0.540 0.510 0.332 0.428BEK2 0.933 0.255 0.438 0.462 0.536 0.535 0.401 0.508BEK3 0.870 0.402 0.423 0.417 0.498 0.452 0.372 0.442KCS1 0.268 0.824 0.473 0.439 0.491 0.221 0.311 0.305KCS2 0.223 0.786 0.405 0.450 0.367 0.288 0.279 0.183KCS3 0.273 0.750 0.523 0.440 0.363 0.203 0.314 0.160KCS13 0.339 0.744 0.468 0.342 0.428 0.237 0.244 0.250KCS4 0.418 0.560 0.809 0.535 0.589 0.352 0.425 0.397KCS5 0.246 0.489 0.729 0.468 0.426 0.298 0.290 0.226KCS7 0.415 0.467 0.851 0.521 0.570 0.394 0.431 0.381KCS8 0.427 0.461 0.860 0.634 0.648 0.402 0.465 0.433KCS12 0.440 0.477 0.807 0.603 0.655 0.434 0.429 0.396KCS15 0.429 0.377 0.508 0.751 0.478 0.405 0.402 0.434KCS16 0.395 0.497 0.591 0.841 0.540 0.399 0.472 0.425KCS17 0.322 0.389 0.425 0.799 0.504 0.325 0.466 0.474KCS18 0.392 0.492 0.677 0.820 0.611 0.373 0.446 0.422KCS19 0.431 0.416 0.545 0.842 0.601 0.324 0.450 0.482KCS22 0.485 0.456 0.566 0.536 0.812 0.390 0.388 0.396KCS23 0.540 0.481 0.690 0.609 0.856 0.429 0.410 0.476KCS24 0.434 0.399 0.395 0.443 0.727 0.333 0.344 0.386KCS25 0.485 0.420 0.628 0.597 0.868 0.350 0.419 0.445KCS26 0.427 0.410 0.603 0.552 0.798 0.346 0.457 0.487CIOK1 0.354 0.114 0.299 0.296 0.297 0.786 0.316 0.305CIOK2 0.394 0.140 0.301 0.264 0.275 0.807 0.337 0.296CIOK3 0.501 0.321 0.363 0.365 0.374 0.801 0.444 0.474CIOK4 0.521 0.268 0.375 0.391 0.426 0.867 0.461 0.438CIOK5 0.391 0.262 0.453 0.404 0.370 0.791 0.426 0.347CIOK6 0.517 0.266 0.452 0.429 0.441 0.837 0.426 0.398CIOK7 0.430 0.302 0.359 0.359 0.354 0.758 0.360 0.358TMSB1 0.366 0.365 0.475 0.502 0.486 0.468 0.922 0.626TMSB2 0.383 0.390 0.475 0.498 0.474 0.459 0.910 0.616TMSB3 0.331 0.278 0.408 0.495 0.421 0.411 0.873 0.593TMSB4 0.395 0.351 0.500 0.526 0.467 0.453 0.942 0.647TMSB5 0.405 0.304 0.449 0.492 0.418 0.475 0.912 0.657TMSP1 0.496 0.286 0.470 0.531 0.516 0.466 0.691 0.957TMSP2 0.505 0.291 0.449 0.534 0.529 0.425 0.663 0.965TMSP3 0.477982 0.259112 0.390915 0.512978 0.505261 0.461313 0.622494 0.951

14 J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

TMT's knowledge creation process is a potential determinant of TMT belief in MCS innovations. It is alsoconsistent with Nonaka and Takeuchi (1995), and Nonaka and von Krogh (2009), who reported that theprocess of knowledge creation positively influenced the innovativeness of organisations.

The finding of H3 also provides possible explanations for the unexpected results found in H2. Theadaptability to innovations (i.e., the ability to form new knowledge and develop new approaches to existingproblems) is likely to be a greater contributing factor to TMT's belief in MCS innovations than theirpre-existing strategic IT knowledge stock. This idea is further supported by the age demographic of TMT. Ascan be seen in Table 2, TMT members are typically somewhat older, with an average age in this study of41.1 years. Given this trend, it is likely that TMT members underwent their training and studies many yearsago, before MCS innovations became significant. Thus, their strategic IT knowledge stock, no matter howgreat, is likely to becomeobsolete over time. Because of this, TMT's strategic IT knowledgewould bemuch lesssignificant as a factor in influencing TMT's belief in MCS innovations than TMT's knowledge creation process.H2 andH3 therefore suggest that the ability of TMT to adapt to new techniques and incorporate them into theoperations of an organisation ismore important in influencing their belief inMCS innovations than their staticIT knowledge stock.

H4 predicted a positive relationship between CIO's strategic business and IT knowledge and TMT beliefin an integrated MCS innovation. Table 6 (Panel A) shows that the path leading from CIO's strategic

Table 6PLS structural model results.

Panel A: Path coefficient, t-statistics (in parentheses) and R2

Latent variable Path to:

TMT belief in MCS innovation TMT participation in MCS innovation

TMT belief in MCS innovation 0.680 (21.48) ⁎⁎⁎

TMT strategic IT knowledge −0.002 (0.06)TMT knowledge creation 0.396 (7.11) ⁎⁎⁎

CIO's strategic business knowledge 0.231 (4.33) ⁎⁎⁎

TMT/CIO interactions 0.159 (3.2) ⁎⁎⁎

R2 0.43 0.48

Panel B: Indirect EFFECTS and 99% bootstrap confidence intervalsa (in parenthesis)

Latent variable Path to:

Through: TMT participation in MCS innovation

TMT knowledge creation TMT belief in MCS innovation 0.269 (0.167–0.372)CIO's strategic business knowledge TMT belief in MCS innovation 0.157 (0.070–0.262)TMT/CIO interactions TMT belief in MCS innovation 0.108 (0.011–0.201)

a All statistically significant at the 0.01 level.⁎⁎⁎ p b 0.001.

15J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

business and IT knowledge to TMT belief in MCS innovations is statistically significant and in the directionpredicted (β = 0.231; p b 0.001). The results provide evidence supporting CIO's strategic business and ITknowledge plays an important role in influencing TMT belief in an integrated MCS innovation. This resultis consistent with prior literature that has indicated that CIO's strategic business and IT knowledge arepositively correlated with TMT belief in IT innovations (see for example, Armstrong and Sambamurthy,1999; Enns et al., 2001, 2003a,b; Bassellier and Benbasat, 2004; Smalts et al., 2006).

H5 predicted a positive relationship between TMT/CIO interactions and TMT belief in integrated MCSinnovations. The results, as shown in Table 6 (Panel A), support the hypothesis (β = 0.159; p b 0.001). Thisfinding highlights the key role of TMT/CIO interactions in driving TMT's belief in integratedMCS innovations.This result supports prior research indicating that frequent interactions between TMT and CIOs positivelyinfluence TMT belief in IT innovations (Raghunathan and Raghunathan, 1989; Applegate and Elam, 1992).

Fig. 2. The results of the PLS analysis. *, **, and *** indicate that the coefficient is significant at the p b 0.05, p b 0.01, and p b 0.001levels, respectively.

16 J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

We also conducted an additional post hoc analysis to determine whether TMT belief in integratedMCS fully mediates the relationships between the antecedent variables and TMT participation in anintegrated MCS innovation. To test this mediation, we follow Baron and Kenny's (1986) step-wiseapproach. We first tested a model involving the direct relationship of the antecedent variables on TMTparticipation and all the relationships were significant at the 0.05 level. In the second step, we tested thedirect relationship between the antecedent variables and TMT belief in an integrated MCS innovation.All the relationships were significant at the 0.001 level except the path leading from TMT knowledge toTMT belief in integrated MCS which was insignificant. In the third step, we include the directrelationship between TMT belief in an integrated MCS innovation and TMT participation whilecontrolling for the effects of our antecedent variables on TMT participation. The path was significant atthe 0.001 level.

In the final step, we tested the full model involving all the relationships in the above three steps. WhenTMT belief in integrated MCS is included in the model, the direct paths leading from two antecedents (CIOknowledge and CIO/TMT interaction) to TMT participation in integrated MCS become insignificant. Thisconfirms that TMT belief in an integrated MCS innovation fully mediates the relationships between thetwo antecedents (CIO knowledge and CIO/TMT interaction) and TMT participation in integrated MCSinnovation. Also, the significant direct relationship between knowledge creation and TMT participation isreduced when TMT belief in an integrated MCS innovation is included; thus providing support for partialmediation. Following Baron and Kenny (1986), TMT knowledge was excluded from the mediation test asthe direct relationship between this variable and TMT belief in integrated MCS is insignificant. The resultsfrom the post hoc analyses provide strong support for the research model including TMT belief as animportant antecedent to TMT participation in an integrated MCS innovation.

Following the mediation test, we estimated the indirect effects of the antecedents of TMT support onTMT participation in integrated MCS innovation through TMT belief. The results (Table 6; Panel B) showthat at the 0.01 significance level, TMT knowledge creation, CIO strategic business and IT knowledge andTMT/CIO interactions have significant indirect effects (β = 0.269, β = 0.157, and β = 0.108 respectively)on TMT participation through TMT belief in MCS innovation. These significant indirect effects providefurther evidence of the importance of these antecedents to TMT support for TMT participation in anintegrated MCS innovation.

5. Conclusion

This study examines the enablers of TMT support for integrated MCS innovations. The results provideevidence that TMT support can be conceptualised in a two-stage model that combines TMT belief andparticipation in an integrated MCS innovation. The results confirm that TMT participation in MCSinnovations is driven by their belief in the innovations. This result is consistent with calls made in recentliterature which suggest opening the “black box” of TMT support and treating it as a dualistic constructrather than a monolithic construct (Chatterjee et al., 2002; Liang et al., 2007). The results also show thatTMT's knowledge creation process, CIO's strategic business and IT knowledge, and TMT/CIO interactionsinfluence the level of TMT belief in integrated MCS innovations. However, TMT's strategic IT knowledge isfound to be insignificantly related to TMT belief in an integrated MCS innovation.

The findings reported in this study have important implications for theory and practice. It is clear thatthe lack of TMT's knowledge limits their level of involvement in MCS innovation projects. This suggeststhat TMT members need to make the effort to engage in activities that enable them to gain the strategicknowledge necessary for performing their managerial roles including making decisions that relate tostrategic planning that involves MCS innovations.

The results confirm the importance of CIO's business and IT knowledge in generating TMT support forMCS innovations. The strong linkage between the CIO knowledge and TMT belief in an integrated MCSinnovation suggests that CIOs play major roles in making TMT aware of the value of MCS innovations insupporting business strategies and the competitiveness of the organisation. The findings also imply thatthe level of interaction between TMT members and CIO, whether by working closely in teams or throughaccountability of the CIO including whether the CIO directly or indirectly is reporting to TMT, will have asignificant impact on enhancing TMT belief in MCS innovations.

17J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

Examining the antecedents of TMT support for MCS innovations answers the call made by priorresearchers. For instance, Shields and Shields (1998) argue that it is not sufficient to merely investigate therelationship between an independent variable and a dependent variable. Understanding the antecedentsof the independent variables will enrich theoretical and empirical models (Shields and Shields, 1998). Thisstudy addresses this call by examining the key enablers of TMT support for integrated MCS innovationswhich are likely to have an indirect effect on the phenomenon tested in prior management accountingliterature as one of the outcomes of TMT support. The findings of this study will enable future researchersto build and test more comprehensive models that involve TMT support.

The statistical analysis did not support the conjecture that TMT's strategic IT knowledge as anantecedent of TMT support for MCS innovations. A plausible explanation for this could be the arguments ofthe dynamic view of knowledge management which suggests that dynamic knowledge creation processesare more effective for organisations than the static knowledge stock that people possess (Nonaka, 1994;Cook and Brown, 1999). This is simply because static knowledge stocks become obsolete over time and diequickly. Therefore, the ability of TMT to recognise new knowledge and renew their existing knowledge ismore important for enhancing the level of support for integrated MCS innovations than the level ofstrategic IT knowledge that those senior managers possess. Moreover, this study contributes to the currentliterature onMCS innovations by answering a call made in prior studies to investigate the factors thatmightinfluence the decisions of TMT to adopt, implement and use MCS innovations.

An investigation into the antecedents of TMT support for integrated MCS innovations has greatpractical significance. TMT support is strongly linked to the positive organisational effects of the adoption,implementation and use of MCS innovations. If organisational performance is to be enhanced then it isvital to understand the factors that drive TMT to support integrated MCS innovations. Deliberateengagement of TMT in the process of knowledge creation should be encouraged within organisations asongoing processes rather than purposeful and directed short-term knowledge acquisition and renewal.Moreover, organisations that are willing to promote the adoption, implementation and use of suchinnovations should seek to employ CIOs with both strategic business and IT knowledge and activate theprocesses and channels that allow an effective interactions between TMTmembers and the CIO. This couldbe through allowing CIOs to attend key executive meetings and reducing the intermediaries between TMTand the CIO.

The results of this research should be interpreted in light of certain limitations. There are inherentlimitations associated with survey studies that apply. For instance, surveys which attempt to captureperceptions are always susceptible to misinterpretation or a lack of knowledge and truthfulness by therespondents. However, techniques used in this study help alleviate some of these concerns. These includeproviding respondents with a ‘No Basis for Answering’ option in the survey, capturing the same data frommultiple respondents, and testing for discriminant validity. All of these strategies provide evidencesuggesting that such concerns do not threaten the validity of the results.

The test of the two-stage modelling of TMT support requires longitudinal data. However, the data usedto test the model is cross-sectional. Additionally, several researchers suggest that TMT support is driven bydifferent factors depending on the life cycle of the innovations (Agarwal and Prasad, 1997; Carlson andZmud, 1999; Karahanna et al., 1999). Future researchers should adopt a longitudinal study approach toexamine the stage factors of TMT support as well as the other factors which may impact TMT support forMCS innovations at different stages of their life cycle.

Furthermore, this study concentrated its analysis on four antecedents of TMT support for MCSinnovations. Future studies should consider other variables that may drive TMT support for MCSinnovations, such as industry-related pressure, competitors' behaviour with MCS innovations, and thetype of business strategy adopted by organisations. Consideration should also be given to concurrentlyinvestigating the antecedents and consequences of TMT support for MCS innovations within a nomologicalnetwork.

The conceptual model of this study provides a framework for future researchers wishing to build andtest a nomological network examining the antecedents and consequences of TMT support for integratedMCS innovations. The results indicate that TMT support for an integrated MCS innovation arises from acomplex set of factors that simultaneously influence TMT behaviour towards integrated MCS innovations.Understanding this complexity is important to both researchers and practitioners in understanding howorganisations successfully adopt, implement, and use IT-driven MCS innovations.

18 J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

Appendix A. Survey

A.1. Part 1: Management practices at the level of top management in your organisation

The questions in this part focus exclusively on the strategic level managementwithin your organisation.They relate to processes, actions and collaborations among top management team members. Topmanagement team members (TMT) refer to the Chief Executive Officer (CEO), Chief Operational Officer(COO), Chief Financial Officer (CFO), and other senior executives responsible for the various functions andbusiness groups. TMT could also include the Senior Information Systems executive (for example the ChiefInformation Officer “CIO”).

Please indicate the extent to which you agree or disagree with each of the following statements bycircling the relevant number:

A.1.1. Top management team members in my organisation are knowledgeable about…

No basis foranswering

Stronglydisagree

Neutral Stronglyagree

BEK1 The potential and limitations of theorganisation's current informationand communication technologies.

0 1 2 3 4 5 6 7

BEK2 The potential and limitations ofemerging information technologies.

0 1 2 3 4 5 6 7

BEK3 How competitors are applyinginformation technologies.

0 1 2 3 4 5 6 7

A.1.2. Top management team members in my organisation…

No basis foranswering

Stronglydisagree

Neutral Stronglyagree

KSC1 Share ideas/experiences with clients and suppliers. 0 1 2 3 4 5 6 7KSC2 Share ideas/experiences with external experts. 0 1 2 3 4 5 6 7KSC3 Gather information/ideas from competitors. 0 1 2 3 4 5 6 7KSC4 Develop new strategies/business opportunities bydoing their rounds.

0 1 2 3 4 5 6 7

KSC5 Make regular contacts with each other throughscheduled meetings/social events.

0 1 2 3 4 5 6 7

KSC6 Attend business conferences/tradeshows. 0 1 2 3 4 5 6 7KSC7 Share information/ideas/experiences with operationallevel managers.

0 1 2 3 4 5 6 7

KSC8 Demonstrate and model their expertise to othermembers within the team.

0 1 2 3 4 5 6 7

KSC9 Use collaborative technologies (such as decisionsupport systems, online discussion, and email) toshare knowledge and expertise with other memberswithin the team.

0 1 2 3 4 5 6 7

KSC10 Engage in creative and useful conversationswith information technology managers toshare knowledge and expertise.

0 1 2 3 4 5 6 7

KSC11 Use metaphors and analogies in conversationsfor strategy development, strategy articulation, andconcept creation.

0 1 2 3 4 5 6 7

(continued)

No basis foranswering

Stronglydisagree

Neutral Stronglyagree

KSC12 Engage in dialogue with subordinates toexchange various ideas and knowledge.

0 1 2 3 4 5 6 7

KSC13 Converse with competitors to gatherinformation/ideas which can be used in theorganisation.

0 1 2 3 4 5 6 7

KSC14 Plan strategies by using academic/practice-relatedliterature.

0 1 2 3 4 5 6 7

KSC15 Plan strategies by using computer simulationand forecasting.

0 1 2 3 4 5 6 7

KSC16 Gather and summarize information from differentdepartment/business units and make it available fordistribution to other people in the organisation.

0 1 2 3 4 5 6 7

KSC17 Build databases on products/services by gatheringmanagement and technical information.

0 1 2 3 4 5 6 7

KSC18 Convene meetings where new concepts andknowledge are discussed, refined, and documentedin order to be shared with other people within theorganisation.

0 1 2 3 4 5 6 7

KSC19 Use information technologies to collect/transmitnewly created concepts.

0 1 2 3 4 5 6 7

KSC20 Attend business/technology-related events(such as workshops and seminars).

0 1 2 3 4 5 6 7

KSC21 Engage/liaise with peers and subordinates. 0 1 2 3 4 5 6 7KSC22 Experiment with new management practices toimprove their knowledge.

0 1 2 3 4 5 6 7

KSC23 Are keen to understand different groups' visions(such as IT executives, functional managers, etc.).

0 1 2 3 4 5 6 7

KSC24 Read business/IT publications. 0 1 2 3 4 5 6 7KSC25 Use “learning by involvement” in different projectsto increase their knowledge and expertise.

0 1 2 3 4 5 6 7

KSC26 Foster a work environment that is supportive of“learning-by-doing” and risk-taking.

0 1 2 3 4 5 6 7

A.1.2 (continued)

19J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

A.1.3. The CIO (or most senior IT manager) in my organisation is knowledgeable about…

No basis foranswering

Stronglydisagree

Neutral stronglyagree

CIOK1 The IT infrastructure required tosupport the organisation's businessintelligence needs.

0 1 2 3 4 5 6 7

CIOK2 The potential and limitationsof relevant emerging informationtechnologies.

0 1 2 3 4 5 6 7

CIOK3 How competitors are using businessintelligence technologies.

0 1 2 3 4 5 6 7

CIOK4 Timing and investment strategies inemerging technologies.

0 1 2 3 4 5 6 7

CIOK5The organisation's present and futureproducts and services.

0 1 2 3 4 5 6 7

CIOK6 What is considered best practice inthe organisation's industry.

0 1 2 3 4 5 6 7

CIOK7 The business activities of theorganisation's competitors.

0 1 2 3 4 5 6 7

20 J. Lee et al. / International Journal of Accounting Information Systems 15 (2014) 1–25

A.1.4. CIO (or most senior IT manager) involvement with other business executives

No basis foranswering

Not at all To some extent To a greatextent

CIOTMT1: To what extent is the CIO(or most senior IT manager) inyour organisation involved withtop management team members?

0 1 2 3 4 5 6 7

CIOTMT2: In the hierarchical structureof your organisation, how manymanagement layers are therebetween the CIO (or most seniorIT manager) and top managementteam members?

………….. Layers

A.2. Part 2: Top management support

A.2.1. Please indicate the extent to which the top management team of your organisation believes that:

No basis foranswering

Not atall

To someextent

To agreatextent

TMSB1 Business Intelligence Systems have thepotential to provide business benefits to theorganisation.

0 1 2 3 4 5 6 7

TMSB2 Business Intelligence Systems createcompetitive advantages for the organisation.

0 1 2 3 4 5 6 7

TMSB3 Business Intelligence Systems areaccessible to the relevant managersof the organisation.

0 1 2 3 4 5 6 7

TMSB4 Business Intelligence Systems are importantto support business activities/strategies of theorganisation.

0 1 2 3 4 5 6 7

TMSB5 Business Intelligence Systems are securetechnologies to support the businessactivities/strategies of the organisation.

0 1 2 3 4 5 6 7

A.2.2. Please indicate the extent to which top management team of your organisation actively participates in:

No basis foranswering

Not atall

To someextent