Empowering MSMEs - Benefits of Credit Rating in MSME - Part - 8

Upload

resurgent-indiaCategory

view

141download

0

Empowering MSMEs

Role of Banks & Financial Institutions, IT, Skill

Development & Rating Agencies

Analysis and Report by Resurgent India Limited

1

Contents

MSME : Sector Overview

Role of Banks and Financial Institutions in Financing MSMEs

Overall Flow of Financing to MSMEs

MSME Debt Finance from the Formal Sector

Role of Banks

Role of NBFCs

Challenges in MSME Financing

Enabling Environment for Growth of Finance to the MSME Sector

Legal and Regulatory Framework

Policies of Financial Regulator

Financing through SIDBI

Role of Information Technology in MSME Sector

Skill Development of the MSME Sector

Role of Credit Rating Agencies

Benefits of Rating

Agencies for Credit Rating

Process of Credit Rating

Conclusion

About FEDERATION OF INDUSTRY TRADE AND SERVICES

About RESURGENT INDIA

2

MSMEs are nurseries for entrepreneurship, often driven by

individual creativity and innovation, and make significant

contribution to country’s GDP, manufacturing output, exports and

employment generation. Moreover, MSMEs are imperative for

achieving the national objective of growth with equity and inclusion.

Timely financial assistance is one of the key factors for the growth

and prosperity of the MSME sector in India. However, due to factors

such as poor financials, lack of experience and collateral and other

institutional factors, MSMEs are regarded as high risk and therefore

are unable to get adequate and timely financial assistance. Although

several steps have been taken to benefit the flow of credit to the

MSME sector, a lot more is desired by the MSMEs in order to

overcome the challenges faced by the sector.

Today Information Technology has become the corner stone of

every successful business and globalization has forced MSMEs to

think beyond their traditional methods of doing business. Tools such

as Enterprise Resource Planning (ERP) have emerged as necessary

platforms for MSMEs not only to streamline their own business but

also to remain competitive. However, the growth in the number of

MSMEs has not reflected in the growth of MSMEs adopting IT/ITeS.

Lack of IT support and awareness of available technologies are some

of the hindrances faced by MSMEs in adopting IT Services.

Skill Development is another thrust area for improving the

competitiveness of MSMEs. Skill development not only helps in

improving productivity but also fosters entrepreneurship. Despite

India’s large pool of human resources, MSMEs continue to lack

skilled manpower required for Manufacturing, Marketing, Servicing

etc. Most MSMEs are not able to afford the skilled labor. This makes

Skill Development essential for MSMEs to reach the next level of

growth.

Given the importance of MSMEs in achieving the socio-economic

objectives of the country, this sector needs special attention of the

state governments and policy makers.

MESSAGE FROM MD/CEO,

RESURGENT INDIA

LIMITED

3

4

5

MSME – Sector Overview

Indian economy is dominated by a vibrant set of enterprises, which are prestigiously known as

Micro, Small and Medium Enterprises (MSMEs) for their scale of operations. The role of MSMEs in

economic and social development of country is widely acknowledged. They are nurseries for

entrepreneurship, often driven by individual creativity and innovation, and make significant

contribution to country’s GDP, manufacturing output, exports and employment generation. The

labour-capital ratio in MSMEs is much higher than in larger industries. Moreover, MSMEs are better

dispersed and are important for achieving the national objective of growth with equity and inclusion.

Looking to the significance of SME sector, it is estimated that if India wishes to have growth rate of

8-10% for the next couple of decades, it needs a strong SME sector, without which it would be

difficult to realize. In this backdrop, MSME is considered to be fast growing sector of economy. The

sector is gaining more importance to realize theme of 12th Five Year Plan (2012-2017) approach

paper “faster, sustainable & more inclusive growth”. So, this sector offers opportunities of

entrepreneurship to younger generation, new areas of MDPs for management institutes, business

prospects to lending institutions, issues to regulators & policy makers and areas of research to

scholars for making the sector more vibrant and faster.

6

Today there are about 36 million MSMEs in the country and this sector has shown an average

growth of 18% over the last five years. However, only 1.5 million MSMEs are in registered segment

while the remaining 24.5 million that constitute 94% of the units are in unregistered segment.

MSMEs are broadly classified into two sector i.e. manufacturing and services. The units engaged in

manufacturing or producing and providing or rendering of services has been defined as micro, small

& medium under MSMED Act on basis of original investment in plant & machinery and equipment.

The latest 4th all India Census of MSME sector has revealed that of the total working enterprises,

95.05% belong to micro enterprises, 4.74% to small enterprises and balance 0.21% are medium

enterprises. Also it is observed that 45.38% enterprises are operating in rural areas. Though MSE

sector, micro in particular, is of great importance in respect to generating employment and

contributing inclusive growth of the economy, this segment of industry is deeply credit constrained.

7

Role of Banks and Financial Institutions in Financing MSMEs

The overall demand for finances in the MSME sector is estimated to be INR 32.5 trillion. The majority

of these are in the form of debt. The demand for debt varies among enterprises in the sector, with

different expectations and capabilities. The micro and small sub-segments together account for the

majority of the debt demand. As they mostly operate in industries such as retail trade, repair and

maintenance, restaurants and textiles and have a significant demand for working capital. The

average credit requirement for Small enterprises is estimated to be INR 4-4.5 million and cash

continues to be a preferred form of transactions. Medium enterprises are more structured and have

a predictable demand for debt and prefer formal source of finance. The average credit size is higher.

Overall Flow of Finance to the MSME Sector

Major reforms for the MSME sector have taken place in the form of introduction of schemes which

have benefitted the flow of credit to the sector.

8

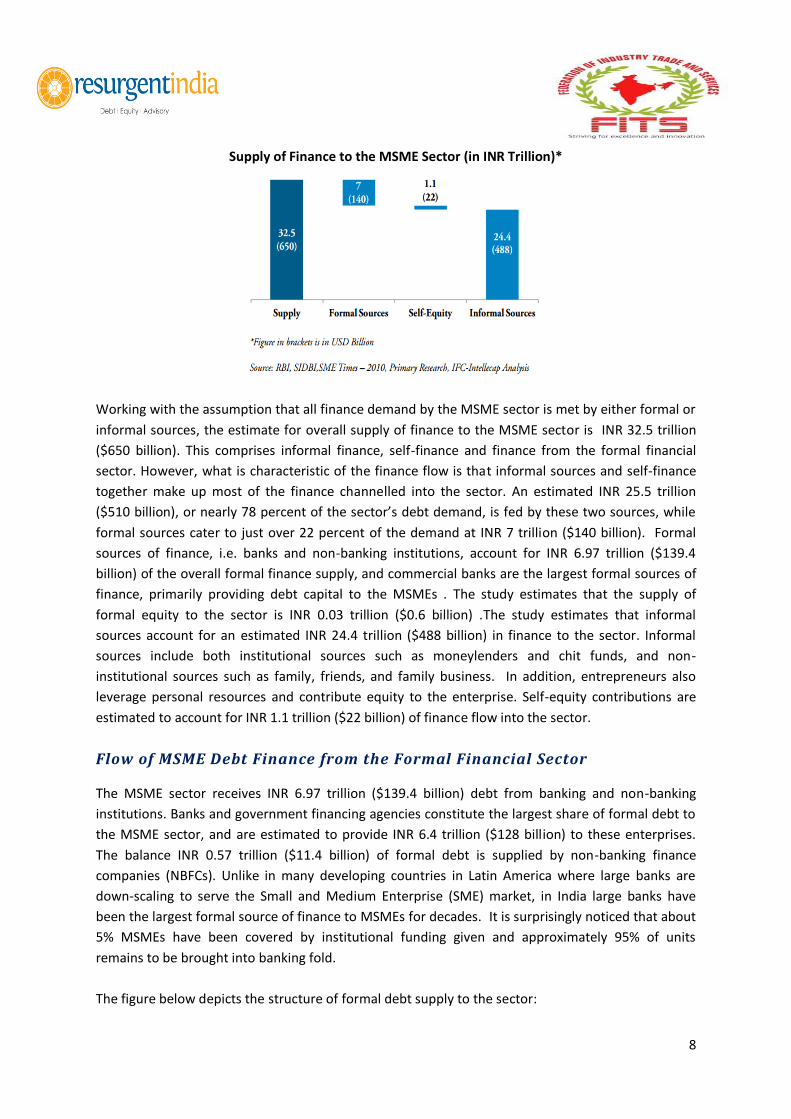

Supply of Finance to the MSME Sector (in INR Trillion)*

Working with the assumption that all finance demand by the MSME sector is met by either formal or

informal sources, the estimate for overall supply of finance to the MSME sector is INR 32.5 trillion

($650 billion). This comprises informal finance, self-finance and finance from the formal financial

sector. However, what is characteristic of the finance flow is that informal sources and self-finance

together make up most of the finance channelled into the sector. An estimated INR 25.5 trillion

($510 billion), or nearly 78 percent of the sector’s debt demand, is fed by these two sources, while

formal sources cater to just over 22 percent of the demand at INR 7 trillion ($140 billion). Formal

sources of finance, i.e. banks and non-banking institutions, account for INR 6.97 trillion ($139.4

billion) of the overall formal finance supply, and commercial banks are the largest formal sources of

finance, primarily providing debt capital to the MSMEs . The study estimates that the supply of

formal equity to the sector is INR 0.03 trillion ($0.6 billion) .The study estimates that informal

sources account for an estimated INR 24.4 trillion ($488 billion) in finance to the sector. Informal

sources include both institutional sources such as moneylenders and chit funds, and non-

institutional sources such as family, friends, and family business. In addition, entrepreneurs also

leverage personal resources and contribute equity to the enterprise. Self-equity contributions are

estimated to account for INR 1.1 trillion ($22 billion) of finance flow into the sector.

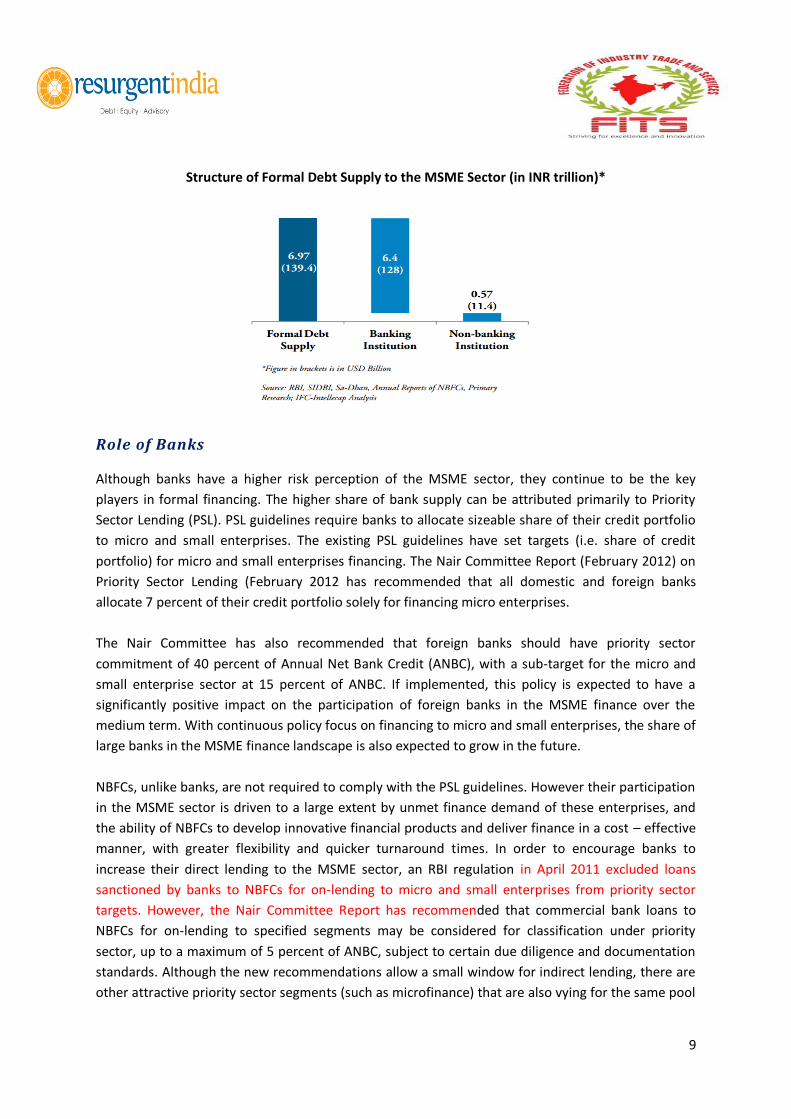

Flow of MSME Debt Finance from the Formal Financial Sector

The MSME sector receives INR 6.97 trillion ($139.4 billion) debt from banking and non-banking

institutions. Banks and government financing agencies constitute the largest share of formal debt to

the MSME sector, and are estimated to provide INR 6.4 trillion ($128 billion) to these enterprises.

The balance INR 0.57 trillion ($11.4 billion) of formal debt is supplied by non-banking finance

companies (NBFCs). Unlike in many developing countries in Latin America where large banks are

down-scaling to serve the Small and Medium Enterprise (SME) market, in India large banks have

been the largest formal source of finance to MSMEs for decades. It is surprisingly noticed that about

5% MSMEs have been covered by institutional funding given and approximately 95% of units

remains to be brought into banking fold.

The figure below depicts the structure of formal debt supply to the sector:

9

Structure of Formal Debt Supply to the MSME Sector (in INR trillion)*

Role of Banks

Although banks have a higher risk perception of the MSME sector, they continue to be the key

players in formal financing. The higher share of bank supply can be attributed primarily to Priority

Sector Lending (PSL). PSL guidelines require banks to allocate sizeable share of their credit portfolio

to micro and small enterprises. The existing PSL guidelines have set targets (i.e. share of credit

portfolio) for micro and small enterprises financing. The Nair Committee Report (February 2012) on

Priority Sector Lending (February 2012 has recommended that all domestic and foreign banks

allocate 7 percent of their credit portfolio solely for financing micro enterprises.

The Nair Committee has also recommended that foreign banks should have priority sector

commitment of 40 percent of Annual Net Bank Credit (ANBC), with a sub-target for the micro and

small enterprise sector at 15 percent of ANBC. If implemented, this policy is expected to have a

significantly positive impact on the participation of foreign banks in the MSME finance over the

medium term. With continuous policy focus on financing to micro and small enterprises, the share of

large banks in the MSME finance landscape is also expected to grow in the future.

NBFCs, unlike banks, are not required to comply with the PSL guidelines. However their participation

in the MSME sector is driven to a large extent by unmet finance demand of these enterprises, and

the ability of NBFCs to develop innovative financial products and deliver finance in a cost – effective

manner, with greater flexibility and quicker turnaround times. In order to encourage banks to

increase their direct lending to the MSME sector, an RBI regulation in April 2011 excluded loans

sanctioned by banks to NBFCs for on-lending to micro and small enterprises from priority sector

targets. However, the Nair Committee Report has recommended that commercial bank loans to

NBFCs for on-lending to specified segments may be considered for classification under priority

sector, up to a maximum of 5 percent of ANBC, subject to certain due diligence and documentation

standards. Although the new recommendations allow a small window for indirect lending, there are

other attractive priority sector segments (such as microfinance) that are also vying for the same pool

10

of funds. Hence, it is not clear if these recommendations will specifically increase indirect financing

for the MSMEs via NBFCs.

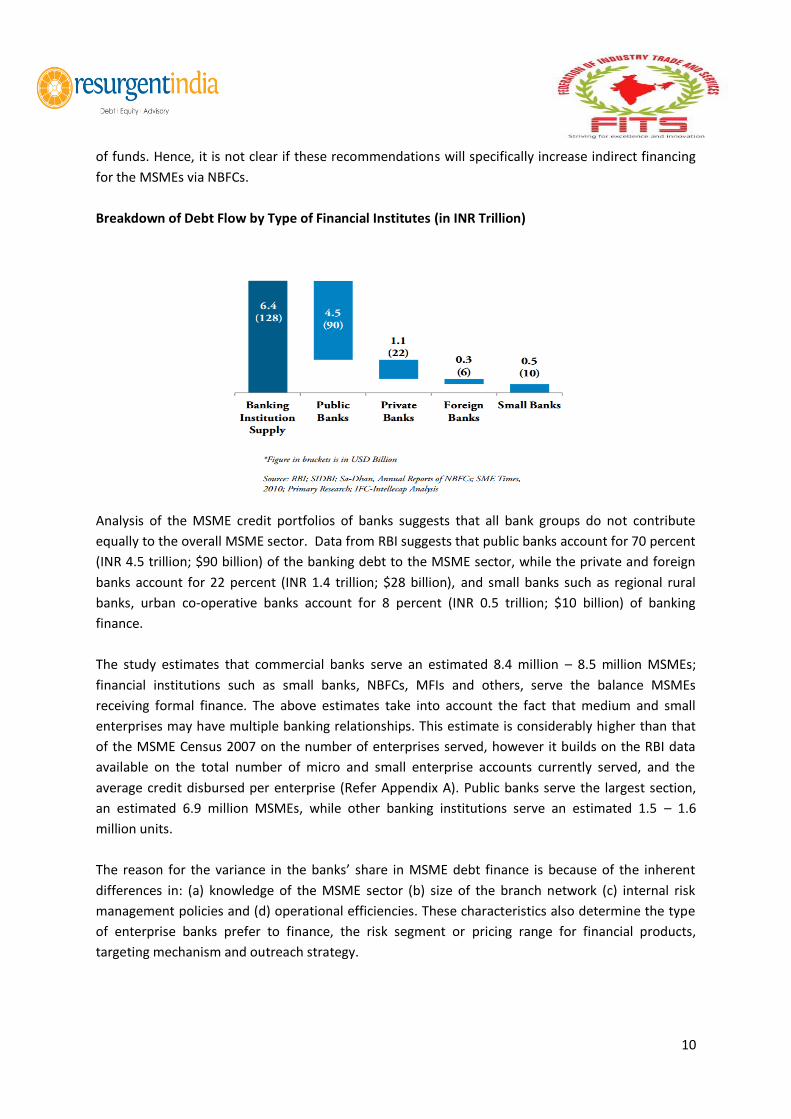

Breakdown of Debt Flow by Type of Financial Institutes (in INR Trillion)

Analysis of the MSME credit portfolios of banks suggests that all bank groups do not contribute

equally to the overall MSME sector. Data from RBI suggests that public banks account for 70 percent

(INR 4.5 trillion; $90 billion) of the banking debt to the MSME sector, while the private and foreign

banks account for 22 percent (INR 1.4 trillion; $28 billion), and small banks such as regional rural

banks, urban co-operative banks account for 8 percent (INR 0.5 trillion; $10 billion) of banking

finance.

The study estimates that commercial banks serve an estimated 8.4 million – 8.5 million MSMEs;

financial institutions such as small banks, NBFCs, MFIs and others, serve the balance MSMEs

receiving formal finance. The above estimates take into account the fact that medium and small

enterprises may have multiple banking relationships. This estimate is considerably higher than that

of the MSME Census 2007 on the number of enterprises served, however it builds on the RBI data

available on the total number of micro and small enterprise accounts currently served, and the

average credit disbursed per enterprise (Refer Appendix A). Public banks serve the largest section,

an estimated 6.9 million MSMEs, while other banking institutions serve an estimated 1.5 – 1.6

million units.

The reason for the variance in the banks’ share in MSME debt finance is because of the inherent

differences in: (a) knowledge of the MSME sector (b) size of the branch network (c) internal risk

management policies and (d) operational efficiencies. These characteristics also determine the type

of enterprise banks prefer to finance, the risk segment or pricing range for financial products,

targeting mechanism and outreach strategy.

11

MSE Finance by PSBs - A decade analysis (2000-2011)

The wonderful growth in absolute term had been registered in credit to MSE sector by Public Sector

Banks during last decade indicates that this sector has huge business potential for banks. Credit to

MSEs has increased over 8 times from Rs.46045 Crores in 2000 to Rs.369430 Crores in 2011 but

percent share of MSE credit to net bank credit (NBC) has consecutively declined from 14.60% in 2000

to 7.80% in 2007. There was sharp increase in percent share of MSE credit to net bank credit from

7.80% in 2007 to 11.10% in year 2008 with marginal hike to 11.30% in year 2009. This higher growth

during the above review period had mainly happened owing to change in the definition of MSEs as

per the provisions of MSMED Act. The investment limit of small (manufacturing) unit was raised

from Rs.1.00 crore to Rs.5 crore and small (services) was added to the sector with an investment in

equipments & instruments up to Rs. 200 lacs. Also the coverage of service enterprises were

broadened by taking tertiary sector into MSE sector such as small road and water transport

operators, small business, professional and self employed and all other service enterprises as per

definition provided under the Act. Further this ratio accelerated to 13.10% in 2010 that might be

because of regulatory change of taking retail trade into service sector. The advances to this sector

further increased to 14.81% in the year 2011. The credit acceleration in the sector had significantly

noticed in absolute growth but proportion of MSE credit in net bank credit has been more or less at

same level of 14% which was way back in year 2000 despite widening the coverage of the MSE

sector. It reveals that real growth in finance to MSE sector is not adequate in the light of significant

contribution of the sector in economy such as employment, manufacturing and export of the

country. Low share of MSE credit does not only hamper equitable growth of economy but also fails

the banks to fulfil their social commitment to the growing society. Banks should therefore, come out

with a strategy to improve the percent share of MSE credit to their net bank credit which is stagnant

between 13-14% since a long period.

Finance to Micro Enterprises: 5 Years analysis (2007-2011)

The latest 4th all India Census of MSME sector has revealed that of the total working enterprises,

95.05% belong to micro enterprises, 4.74% to small enterprises and balance 0.21% are medium

enterprises. Also it is observed that 45.38% enterprises are operating in rural areas. Though MSE

sector, micro in particular, is of great importance in respect to generating employment and

contributing inclusive growth of the economy, this segment of industry is deeply credit constrained.

Analysis of finance to Micro Enterprises by banking industry revealed some of the important findings

mentioned below.

Prescribed share of credit not provided to Micro Enterprises: their share in bank credit is

really ironical because micro gets merely 5-6% place in net credit of domestic banks which is

very negligible

Over 50% banks have less than 7% finance to Micro Enterprises

Sector gets lesser credit under proposed norms of 7% lending to Micro Enterprises

12

Absolute credit surged by 124% (CAGR -31%) : Outstanding credit to the sector by all

scheduled commercial banks (SCBs) had surged by 124% from Rs.213539 crores in year 2008

to Rs. 478527 crores in year 2011 (Table-22).

Enhancement of existing limits contributed higher growth - Target fresh credit: Y-o-Y

growth during review period is showing uneven trend, however, it was 19.94% in year 2009

which further grew by 41.44% in year 2010 and the growth rate was declined to 32.08% in

year 2011. The abnormal acceleration in year 2010 might be occurred owing to the inclusion

of retail trade in service sector and thereafter, normal growth was observed in year 2011.

Sector responds faster - Annual growth rate higher than industry rate : Banks in India are

mandated to register at least 20% YoY growth in credit to Micro & Small enterprises and 10%

annual growth in number of micro enterprises accounts which is now recommended to grow

at least by 15% in terms of number of account every year. Public sector banks have

registered higher growth rate as compared to the stipulated norms of 20% such as 26.64 %

in 2009, 44.36 % in 2010 and 33.70% in 2011. The growth rate of private sector banks was

negative (-0.54%) in year 2009 which further geared up to 38.94% in year 2010 and then

declined to 35.93% in year 2011 which shows compliance of lending norms in terms of

growth rate. However, foreign banks grew their advances by 16.62% & 17.07% in year 2009

& 2010 respectively but had negative growth (-0.78%) in year 2011 which require corrective

measures by foreign banks to adhere to the norms for growth of credit to MSE sector.

93% Financial Exclusion - Key to 12th Plan theme of inclusive growth

It is observed that 92.77% MSME beneficiaries have no finance, 5.18% avail finance from

institutional sources and 2.05% through non-institutional sources. It is an indicator for the

banks that they need to focus on SMEs to achieve national agenda of financial inclusion

because exclusion over 92% of MSME units is indeed a matter of concern in the history of

independence for over 64 years and about 43 years of banks nationalization in our country.

Also the study validates the observation that MSMEs are undoubtedly like big bazar group to

be tapped by formal credit delivery channel because 93% of MSMEs still rely on self finance.

So this sector will be key to realize theme of inclusive growth of 12th Plan.

Role of NBFCs

Non Banking Finance Companies NBFCs :

Non Banking Finance Companies NBFCs provide an estimated INR 0.57 trillion ($11.4 billion) of debt

finance to the MSME sector. The size of credit disbursed ranges from INR 0.3 million ($6000) for

micro enterprises to INR 50-100 million ($1 million – $2 million) for medium enterprises[81]. A large

share of the finance is used for asset purchase. Analysis of the NBFCs’ MSME portfolio and primary

research suggests that enterprises in transport business dominate the portfolio. Engineering, vendor

supply chains and retail trade are among the other key industries served by NBFCs. NBFCs are

companies registered under the Companies Act 1956 and engaged in business of loans, leasing and

hire-purchase. NBFCs function akin to a bank, with few key differences such as: (a) NBFCs are not

part of the payment and settlement mechanism, i.e., NBFCs cannot issue transaction instruments

such as cheques (b) NBFCs don’t have the facility of deposit insurance and credit guarantee.

13

NBFCs are governed by a separate set of regulations with lower compliance overheads, affording

them several operational advantages and the flexibility to adopt innovative business models.

Although NBFCs enjoy considerably lower regulatory overheads, they experience challenges in

raising debt, as all NBFCs cannot accept public deposits

Micro Finance Institutions (MFIs) Microfinance institutions are often incorporated as NBFC-MFIs, and

are mostly active in the unregistered and unorganized microenterprise segment. MFIs are gradually

scaling up from providing individual loans to providing business loans for micro enterprises. The

average size of credit disbursed by MFIs ranges from INR 0.015 million ($300) to INR 1 million

($20,000) per enterprise. Primary research suggest that MFIs accept immovable property such as

land, building and/or hypothecated assets as collateral.

MFIs have extensive fleet-on-street structures for ground operations that enable them to reach

unserved regions. With extensive outreach and experience in joint liability operations, MFIs often

have a better understanding of the enterprise potential and financial performance, helping them in

their customer acquisition strategies.

The study estimates that MFIs supply INR 0.02 trillion ($0.4 billion) of debt to the micro enterprise

segment. In line with broad sector financing trends, short-term working capital accounts for a larger

share of the portfolio. Despite the huge market potential, the current activity of MFIs is limited due

to constraints in accessing capital and other stringent regulatory requirements.

MFI activity in micro enterprise financing is limited to loan sizes of INR 0.05 million ($1,000), or less,

due to recent changes in the regulation. The new regulations for MFIs require them to be structured

as MFI-NBFCs, which will not have more than 15 percent of the loan portfolio in loan assets of INR

0.05 million ($1,000) and above. In other words, 85 percent of the loan portfolio of MFIs must

comprise loan assets, specifically for income generating activities and not exceeding the INR 0.05

million ($1,000) limit.

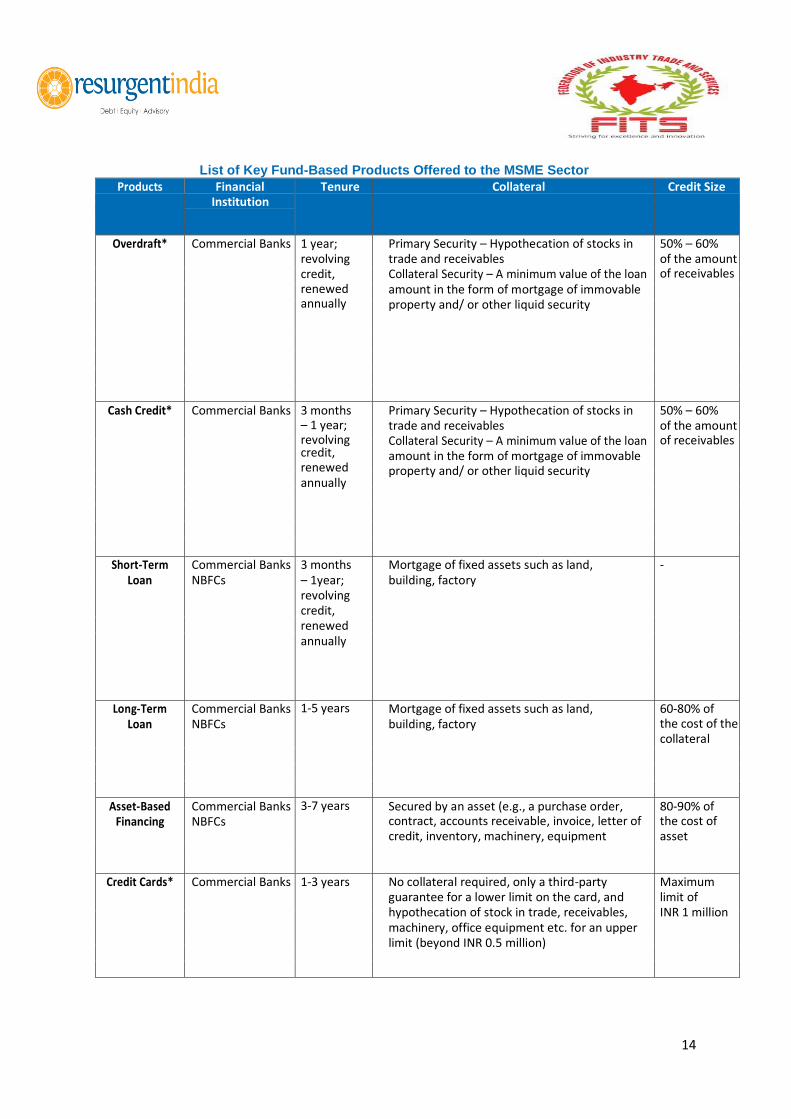

Typical Debt Finance Process and Challenges :

Fund-based products account for an estimated 80 percent of the current flow of formal finance to

the sector

14

List of Key Fund-Based Products Offered to the MSME Sector

Products Financial Institution

Tenure Collateral Credit Size

Overdraft*

Commercial Banks 1 year; revolving credit, renewed annually

Primary Security – Hypothecation of stocks in trade and receivables Collateral Security – A minimum value of the loan amount in the form of mortgage of immovable property and/ or other liquid security

50% – 60% of the amount of receivables

Cash Credit* Commercial Banks 3 months – 1 year; revolving credit, renewed annually

Primary Security – Hypothecation of stocks in trade and receivables Collateral Security – A minimum value of the loan amount in the form of mortgage of immovable property and/ or other liquid security

50% – 60% of the amount of receivables

Short-Term Loan

Commercial Banks NBFCs

3 months – 1year; revolving credit, renewed annually

Mortgage of fixed assets such as land, building, factory

-

Long-Term Loan

Commercial Banks NBFCs

1-5 years Mortgage of fixed assets such as land, building, factory

60-80% of the cost of the collateral

Asset-Based Financing

Commercial Banks NBFCs

3-7 years Secured by an asset (e.g., a purchase order, contract, accounts receivable, invoice, letter of credit, inventory, machinery, equipment

80-90% of the cost of asset

Credit Cards* Commercial Banks 1-3 years No collateral required, only a third-party guarantee for a lower limit on the card, and hypothecation of stock in trade, receivables, machinery, office equipment etc. for an upper limit (beyond INR 0.5 million)

Maximum limit of INR 1 million

15

List of Key Non-Fund Based Products Offered to MSME Sector

Product Financial Institution

Description

Letter of Credit

Commercial Banks NBFCs

Letter of Credit is extended to MSMEs and is mostly used by export-oriented MSME units; however importers too are increasingly making use of products like ‘Buyer’s Credit’. Credit is available for procuring raw material, manufacturing the goods, processing and packaging and shipping the goods. Letters of credit are available against 25%-35% cash margin and mostly on a 100% collateral security in the form of residential property, corporate guarantees or liquid securities

Bank Guarantee

Commercial Banks NBFCs

Bank Guarantees are extended for advance payment, tender money security deposit, for getting orders, for procurement of raw materials among others.

Current Account

Commercial Banks Commercial banks provide the facility of the current account transaction to their MSME customers. The MSME units have to maintain a quarterly average balance in their current accounts. The transaction is permitted in cash, transfer and clearing. Banks also provide internet banking facility to MSME units on these accounts.

Savings Account

Commercial Banks A few of the banks also provide savings accounts to the MSME units. An enterprise has the flexibility to choose the period of deposit from 1 year to 3 years. Surplus funds over a threshold limit with an initial deposit of certain amount is automatically swept (auto-sweep) to Corporate Liquid Term Deposit (CLTD). The rate of Interest for CLTD will be the card rate applicable for the contracted tenure of the deposit. No differential rate of interest is applicable. However, no Loan /Overdraft Facilities are available under the scheme.

Remittance Commercial Banks Most of the banks provide electronic modes of retail payment to the MSMEs through National Electronic Fund Transfer (NEFT) and large value settlements through the Real Time Gross Settlement (RTGS) application

16

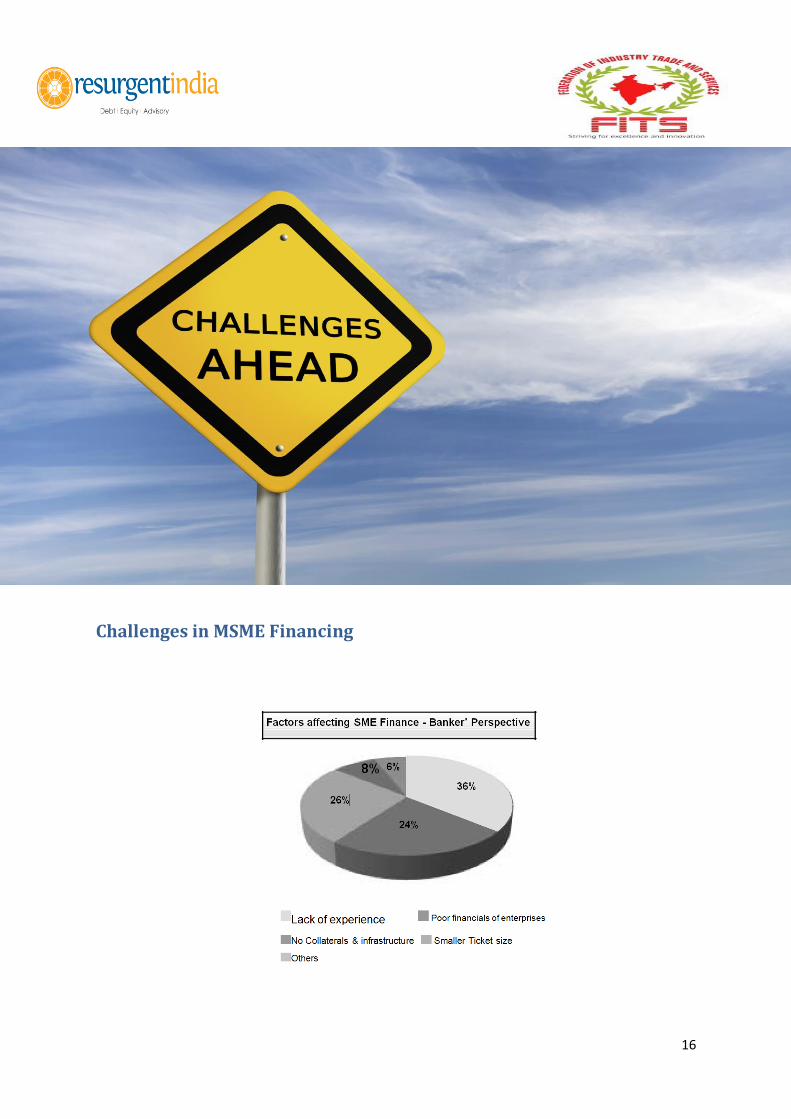

Challenges in MSME Financing

17

Lack of Experience

Entrepreneurs of first generation with lack of experience, has been revealed as the foremost

reasons of poor SME credit, followed by lack of collaterals & infrastructure put together 26%

and poor financials of SMEs by 24% respectively.

Poor Financial of Enterprise

Majority of bankers don’t prefer SMEs for want of proper books of account and infusion of

own contribution into business by promoters. This peculiarity, probably has been observed

in SMEs because most of them are first generation entrepreneurs who fail to bring their own

contribution and also don’t know how to record their business transactions in their books.

Lack of Collateral

Lack of Collateral: Lenders request for collateral to mitigate risks. Now the lack of collateral

is the most widely mentioned obstacle faced by MSMEs is accessing finance. I some cases,

the enterprise is not able to provide sufficient collateral either because it is not firmly

established or it is insufficient in view of the size of the loan requested.

Institutional Factors & others

Low technology innovations and inadequate product branding/marketing tie-up are

observed important non-financial factors of default. Also transaction cost is very high and

the handling of MSME financing is an expensive business. The cost of appraising a loan

application or of conducting a due diligence varies as per the size of financing.

18

Enabling Environment for Growth of Finance to the MSME Sector

The three main pillars of the enabling environment that the study has analyzed are: (a) legal and

regulatory framework (b) government support (c) financial infrastructure support

19

Legal and Regulatory Framework

Micro, Small, Medium Enterprise Development Act, 2006 :

The Micro, Small, Medium Enterprise Development Act, 2006 (MSMED Act) defines the

micro, small and medium enterprise segments, and promotes focused and coordinated

development of policy for the sector.

The MSMED Act led to the setting up of policymaking and monitoring bodies – the National

Board for Micro, Small and Medium Enterprises and MSME Advisory Committee – which

facilitate coordination and inter-institutional linkages among various government

departments related to the MSME sector.

To ensure that the proposed development schemes such as scheme for capacity building,

financial assistance for bar-code etc. receive adequate financing, the MSMED Act proposes

setting up of dedicated government funds.

The MSMED Act also has provisions to address the endemic problems of delayed payments

to MSMEs by large enterprises. Section 15 specifies that buyers make payments to the

MSMEs on mutually agreed dates, and in case dates are not specified, the debtor is required

to pay within 45 days. Section 16 elaborates the penalty in case of delayed payments i.e.

buyers are liable to pay compound interest to the MSME on the payment amount that is

three times the bank rate specified by the RBI (interest is to be paid from the day

immediately after the mutually-agreed date.)

Gaps and Challenges in the MSMED Act:

The definition of MSME in the MSMED Act provides no information on financial

maturity or scale of MSMEs. Financial institutions therefore find it difficult to target

units on the basis of this definition and prefer to use size of annual sales as a metric

to identify MSMEs. These definitions tend to vary across financial institutions.

Due to inconsistency in the definition of MSME across financial institutions and

government, the data on the MSME sector collected and collated by the

government agencies does not always help in segmenting enterprises and providing

targeted services and products.

While the MSMED Act attempts to address the issue of delayed payments through

specific provisions, strict enforcement of these provisions is often not observed in

the sector.

Credit Information Companies (Regulation) Act 2005

The government has enacted the Credit Information Companies (Regulation) Act 2005 (CIC Act) to

facilitate the formation of credit bureaus and strengthen the finance information infrastructure.

20

The CIC Act led to the formation of four credit bureaus in the country. Experiences in

developed countries suggest that access to credit information on historic conduct of the

enterprises tends to reduce the information asymmetry and increases the flow of formal

finance.

The Act regulates the information that credit bureaus can collect and process, however it

also provides RBI the flexibility to expand the type of information captured.

Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act,

2002:

The SARFAESI Act is a legal framework that protects creditor rights and facilitates recovery of non-

performing assets without the intervention of the judicial system. The Act is applicable to all loan

assets created by a commercial bank, and broadly provides three alternative methods of recovering

non-performing assets, namely, (a) securitization (b) asset reconstruction and (c) enforcement of

security.

As the MSME sector is considered to be relatively riskier, limited credit protection can

severely impede supply of finance to the sector; the SARFAESI Act provides a framework to

financial institutions to recover non-performing assets, reducing the risk of non-recovery of

dues.

The Act also provides guidance on formation of Asset Reconstruction Companies (ARCs) to

provide support to commercial banks in managing the sale of non-performing assets. SIDBI

along with other leading commercial banks has set up the India SME Asset Reconstruction

Company Limited (ISARC) to manage non-performing MSME assets of commercial banks.

Many commercial banks have also instituted One-Time-Settlement (OTS) mechanisms that

allow banks to settle transactions with non-performing assets without going into a long-

drawn process as prescribed in the SARFAESI Act.

Policies of Financial Regulator

To ensure formal finance to priority sectors such as agriculture and MSME, Priority Sector Lending

guidelines have been in place for commercial banks since 1972. Under these guidelines, domestic

commercial banks are required to allocate 40 percent of the net bank credit for priority sectors (32

percent norm for foreign banks.

• Lending to micro and small enterprises is covered under priority sector. While domestic public and

private banks do not have any sub-targets, foreign banks are required to allocate 10 percent of the

net bank credit to these enterprises.

• With regards to PSL in MSE, the RBI has accepted all the recommendations of the Prime Minister’s

Task Force Report. Key measures include: (a) commercial banks to achieve 20 percent annual growth

in credit to the sector, (b) 60 percent of the portfolio to be allocated to micro enterprise segment,

and (c) 10 percent annual growth in unique micro-enterprise accounts.

21

• In a recent development, the Nair Committee on Priority Sector Lending has recommended that 7

percent of net bank credit should be allocated to micro enterprises (applicable for both domestic

and foreign banks). The Committee has also recommended that banks should increase micro

enterprise customers at the rate of 15 percent per annum.

• In order to ensure that banks adhere to the priority sector lending guidelines, the RBI requires

banks to deposit unutilized priority sector funds with a special fund managed by SIDBI and NABARD.

The provision works as penalty because the yield on the special fund is much lower than the

potential yield on other PSL-approved sectors.

Policy incentives for MSME finance by banks

I. Prescribed provisioning requirement for ‘standard advances’ under SME advances is merely

0.25% as against 1.00% in case of real estate and 0.40% for other advances, which is a

reward for banks to make lower provision towards buffer capital on SME advances

II. Collateral free loans up to Rs. One crore are secured by CGTMSE guarantee which is highly

liquid at par with cash security as compared to any other collateral in loan accounts

III. Allocation of zero risk weight to SME loans guaranteed by CGTMSE for capital adequacy

requirement

IV. Simplified computation of working capital limit for MSE units on basis of minimum 20% of

their estimated annual turnover up to the limit of Rs.500 lacs.

• In order to ensure the flow of equity to the sector, capital markets regulator Securities and

Exchange Board of India (SEBI), in consultation with the Ministry of Finance, has framed a set of

guidelines to set up a dedicated stock exchange for small and medium enterprises. Both Bombay

Stock Exchange (BSE) and National Stock Exchange (NSE) have set up and launched SME stock

exchanges in 2011.

The government provides financing support to the sector through the

Small Industries Development Bank of India (SIDBI).

SIDBI provides wholesale financing support to small financial institutions such as NBFCs that

operate in the MSME sector.

SIDBI also provides retail finance support to MSMEs, particularly in the growth stage through

schemes such as Growth capital and Equity assistance for MSME (GEMS).

In addition to providing debt finance, SIDBI has also set up SIDBI Venture Capital Limited to

supply equity to the MSME sector.

To minimize the effect of immovable collateral on access to finance for MSMEs, the

government and SIDBI have co-funded a credit guarantee fund, Credit Guarantee Trust for

Micro and Small Enterprises (CGTMSE). Financial assistance from SIDBI – SIDBI has created a

corpus Fund of INR 60 Cr for providing financial support to MSMES with special focus on

technology enterprises. Credit Guarantee Fund Trust for Micro and Small Enterprises

22

(CGTMSE) scheme was launched by the GOI in 2000 to strengthen credit delivery system and

facilitate flow of credit to the MSME sector. To operationalize the scheme, GOI and SIDBI set

up the Credit Guarantee Fund Trust for MSMEs. The scheme provides collateral free funding

up to INR 1 Crore for individual MSMEs. The CGTMSE Scheme is operated through a network

of Banks and FIs called Member Lending Institutions (MLIs).

Credit Linked Capital Subsidy Scheme –

This scheme aims at facilitating technology up-gradation of MSMEs by providing 15 % capital

subsidy for purchase of Plant & Machinery / Improved technology. Maximum limit of

eligible loan for calculation of subsidy under the scheme is Rs.100 lakhs. At present, more

than 1500 well established/improved technologies under 51 sub-sectors have been

approved under the Scheme.

ISO 9000/ISO 14001 Certification Reimbursement scheme for MSMEs offers reimbursement

of expenses up to 75% (subject to a maximum of INR 75,000) incurred towards the

acquisition of ISO 9000/ISO 14001/HACCP certification.

23

Role of Information Technology in MSME sector

Information technology had a great impact in all aspects of life, and the global economy is currently

undergoing fundamental transformation. Information technology has very real impact in most of

industries and usage of these technologies is revolutionizing the rules of business, resulting in

structural transformation of enterprises. Modern businesses are not possible without help of

information technology, which is having a significant impact on the operations of Small and Medium

Sized Enterprises (SME) and it is claimed to be essential for the survival and growth of economies in

general. IT/IS play decisive role in increasing the profitability of the organization. Competitiveness

among the SMEs makes them to think about the use of current available technology. Becoming an

inherent part in large organisations, IT is a mechanism that enables SMEs to respond to customer

requirements efficiently by enabling information to be transmitted. SMEs endeavour to manage the

knowledge sharing process and inter-organizational knowledge. Enterprise Resource Planning (ERP)

is best and effective available technology that can be adopted by Indian SMEs to survive the

competition. Globalisation has forced SMEs to think beyond the traditional methodology, in the

present scenario Indian SMEs are facing competition from within the country as well as from other

developing countries.

24

Technology and SMEs: Since the beginning of 1991, globalization has made the organizations to

think about the adoption of available technology so that they can face the challenges of the

emerging market trends and the competition from the Asian and European SMEs, globalization led

to immense competition and companies, especially in the manufacturing sector, realized the need

for more customer focus and shortened product life cycles. Corporations had to move towards agile

manufacturing, continuous improvement of business processes and business process reengineering.

This required an integration of manufacturing with other functional areas like accounting, marketing,

HR, etc. Enterprise Resource Planning (ERP) system has emerged as a common and necessary

platform among small and medium scale enterprises not only to remain competitive in the global

business scenario but also to streamline their own internal processes to collaborate with their

foreign partners in their supply chain. ERP is generally viewed as necessary infrastructure and is also

a strategic weapon in automating business processes while providing visibility to those processes

throughout the enterprise ERP system consists a suite of software modules that lets an organization

share common data and practices across the enterprise to access information in real-time

environment. ERP if implemented successfully can have a significant impact on organizational

performance through automation and integrating the majority of business processes on small,

medium and large sized organizations. Small and medium sized enterprises (SMEs) have become a

major contributor to the economies of the countries throughout the world. Not only in developed

countries but also in the developing countries like India, during the past 50 years, the small-scale

sector has played a very important role in the socio-economic development of the country. It has

significantly contributed to the overall growth in terms of the Gross Domestic Product (GDP),

employment generation and exports

Although the number of SMEs seems to be growing, there is still need to aware SMEs about the

available technology that can be used for the business and for the proper utilisation, some of the

challenges faced in the implementation of IT/IS are :

Lack of Awareness

Most of the SMEs are not aware of the available technologies that can be implemented for the

better decision making, increasing productivity.

Lack of IT Support

IT personnel are in high demand and are often attracted to bigger companies and MNCs. It is very

difficult for SMEs to attract good IT personnel. It is even more difficult to retain them. Moreover,

good IT personnel are expensive and may not be affordable by most SMEs.

Lack of IT Literacy

Employees in SMEs started from the ground up after working with the company for many years.

Some of them are often holding supervisory and managerial positions. These employees may not be

IT literate and often have high resistance to the changes in the working process that they are

comfortable with after many years.

25

Uneven IT Awareness and Management Skills

As a company grows, new managers are often introduced into the company. There will also be old

managers who are promoted from the rank and file. Some of these managers may not been trained

in the leadership and management skill. These uneven skill among the managers often caused

conflicts during the implementation.

Lack of Experience in Using Consultants

A good consultant often saves time and effort, and help to prevent pitfalls during the IT projects.

However, most SMEs are devoid of experience in working with consultants. The lack of knowledge in

the field of IT makes it difficult for them to identify good consultant for the projects. They often feel

that the consultant cost is too high and they can handle it with their own staff. If the company has

no staffs that possess experience and knowledge in the IT project, avoiding external help often costs

more to the company eventually.

Level of SMEs on the basis of IT/IS adoption:

Level 1: SMEs in the nascent stage of IT adoption having only the basic IT infrastructure in place,

such as the basic level computerization, LAN, etc. can be categorized into this level of IT/IS adoption.

These companies use IT only for basic communication and data processing.

Level 2.SMEs that have computerized certain standalone functions without any cross functional

linkages can be categorized in Level -2 of IT/IS adoption. Organisations at this level would be having

several point applications aimed to automate selective functions. There will be islands of

information with little or no integration between the applications.

Level 3.SMEs that have automated their core business functions, achieved complete process

automation and integration are considered to be in level-3 of IT/IS adoption. This will include

organisations which have integrated transaction processing environments with automation of core

business processes and functions. The firms will be using an enterprise level resource planning

application (ERP) which integrates various business processes across functional departments

Summary

Most of the Indian SMEs are either at level 1 or at level 2 in terms of technology adoption, the main

reason behind this backwardness is lack of literacy and lack of information regarding the technology,

SMEs need to be aware of appropriate technology and people need to be educated accordingly. In

today’s era of globalisation SMEs need to attain level 3 to compete. Enterprise Resource planning

helps SMEs to enjoy unimaginable benefits. Nevertheless the problems of ERP in SMEs are also

present. There are still ups and downs in it

26

Skills Development of the MSME Sector

One of the thrust areas for increasing the competitiveness of MSMEs includes skills development.

Skills development not only helps in improving productivity but also fosters entrepreneurship.

Hence, it is imperative for the concerned governmental agencies, trade associations and MSMEs to

come together and discuss on how to make training programmers relevant and attractive for

MSMEs. The lack of human resources has been a long-standing problem faced by MSMEs in the

country. Despite India’s large pool of human resources, the MSMEs continue to lack skilled

manpower required for manufacturing, marketing, servicing, etc. Majority of the graduates passing

out each face difficulties in getting employed in MSMEs due to the lack of job / role specific skills.

Also, it has never been easy for MSMEs to hire the right workers at affordable prices. Another area

of concern is low focus of MSMEs on skills development. Even though MSMEs are investing in

infrastructure, technology and manufacturing practices, development of skilled manpower still

remains a major concern. There is evidence that suggests that MSMEs that have invested in skill

development have witnessed better business performance. Skill development programs with a blend

of industrial engineering, quality management, general management and soft skills can enable the

MSMEs to reach the next level of growth.

27

Importance

To inculcate entrepreneurial qualities among the youth.

To retrace the high growth path, the MSME sector assumes a pivotal role in driving the

growth engine. The MSME sector in India continues to demonstrate remarkable resilience in

the face of global and domestic economic circumstances.

The sector has sustained an annual growth rate of over 10% for the past few years.

The sector has shown admirable innovativeness and adaptability to survive economic

shocks, even of the gravest nature.

Calibre for employment generation, low capital and technology requirement, promotion of

industrial development in rural areas, use of traditional or inherited skill, use of local

resources, mobilization of resources and exportability of products.

Generates around 100 million jobs through over 46 million units situated throughout the

geographical expanse of the country. With 38% contribution to the nation’s GDP and 40%

and 45% share of the overall exports and manufacturing output, respectively, it is easy to

comprehend the salience of the role they play in social and economic restructuring of India

Skill development of entrepreneurs in MSME sector Initiatives for MSME skill development

1. National Policy on Skill Development 2009

In the last five years India has made progress towards developing the assets to drive skill

training at scale. National Skill Development Corporation 2009 ensured the training

programmes and courses for the same.

2. National Skill Qualification Framework 2013

It is anchored at NSDA and efforts have been initiated to align skilling and education

outcome.

3. Sector Skill council

This ensures that the skill development efforts begin made by all stalk holders in the system

are accordance with the actual needs of industry.

4. Skill India' mission through the Pradhan Mantri Kaushal Vikas Yojana will help increase the

availability of a skilled workforce in the MSME sector.

Includes the following ten major directions to achieve the objective set

Aspiration

Capacity

Quality

28

Synergy

Mobilization and engagement

Global Partnership

Outreach and advocacy

ICT Enablement

Development of trainers

Inclusivity

5. The National Policy on Skill Development and Entrepreneurship, 2015

The objective of the National Policy on Skill Development and Entrepreneurship, 2015 will

be to meet the challenge of skilling at scale with speed and standard (quality). It will aim to

provide an umbrella framework to all skilling activities being carried out within the country,

to align them to common standards and link the skilling with demand centres. In addition to

laying down the objectives and expected outcomes, the effort will also be to identify the

various institutional frameworks which can act as the vehicle to reach the expected

outcomes. The national policy will also provide clarity and coherence on how skill

development efforts across the country can be aligned within the existing institutional

arrangements. This policy will link skills development to improved employability and

productivity.

6. Start-up India Action plan :

Ease of doing business, taxation, access to capital for MSMEs and skilling.

7. Employee Pension Scheme

CRISIL believes the government's proposal to pay the Employee Pension Scheme contribution of 8.33 per cent for all new employees enrolling in the Employees' Provident Fund Organisation for the first three years of their employment is a big incentive for MSMEs.

8. Enterprise and skill development:

Entrepreneurship /skill development programmes launched by the Ministry is one of the key elements for promotion of MSEs (Micro and Small Enterprises) particularly for the first generation entrepreneurs.

The Entrepreneurship Development Programmes (EDPs) are conducted through MSME-DIs (Development Institutes), which focus on improving entrepreneurial skills and developing industry specific skills in areas such as electronics, electrical, food processing, etc. to develop and enhance the skill of the entrepreneurs.

9. MSE - Cluster Development Programme (CDP)

The implementation of MSE-CDP is for the holistic development of selected MSEs clusters through value chain and supply chain management.

29

The Ministry has adopted a cluster development approach as the key strategy for enhancing the productivity and competitiveness as well as capacity building of Micro and Small Enterprises (MSEs) and their collectives in the country. Clustering of units also enables providers of various services, including banks and credit agencies to provide their services more economically, thus reducing costs and improving the availability of services for these clusters.

10. National Competitiveness Programme (NMCP) Schemes

The Ministry announced the formulation of National Competitiveness Programme (NMCP) in 2005 with the objective to support the Small and Medium Enterprises (SMEs) in their endeavour to become competitive and attune themselves to the competitive pressure caused by liberalization.

30

Role of Credit Rating Agencies

Approaching a credit rating agency is a good option for small and medium enterprises (SMEs) given

the problems they face in seeking finance. Rating agencies assess a firm's financial viability and

capability to honour business obligations, provide an insight into its sales, operational and financial

composition, thereby assessing the risk element and highlights the overall health of the enterprise.

They also benchmark its performance within the industry.

Rating agencies usually have eight grades, ranging from SME 1-8, with 1 denoting the highest rating

and 8 the lowest. For providing this service, the agencies charge a fee which is based on the firm's

turnover and ranges from Rs.44,000 to Rs.1.21 lakh. These ratings are valid for a year and can be

renewed by paying an appropriate fee. It is money well spent. For, a good rating means a higher

chance of bagging a loan.

Besides, there is a lot of information asymmetry in the market. A good credit rating provides the

initial confidence for the project and also acts as a final confirmation.

31

Benefits of rating

Concessional funding

A good rating can help you gain faster and cheaper credit for the venture. The agencies that provide

rating for SMEs are Crisil Ratings, SME Rating Agency of India (SMERA), ICRA, Credit Analysis &

Research (CARE), Onicra , and Fitch. These agencies have tie-ups with several banks to offer

preferential interest rates based on ratings. For instance, Crisil Ratings has such a working

arrangement with 35 banks and financial institutions, while SMERA has entered into such pacts with

29 institutions.

According to Crisil Ratings, the interest rate reduction for its clients ranges from 0.5-1.25% and

around 35% of the enterprises have reported a reduction in the loan processing time. SMERA

feedback suggests that enterprises enjoy interest rate concessions to the extent of 0.25% to 1%. Also

in many cases, savings from the reduced borrowing cost exceeds the rating fee.

If a firm gets a good rating, he can even approach other banks to get a better rate bargain than the

one provided by his existing banker.

Better business opportunities

The independent risk evaluation of SMEs by an unbiased third party lends credibility to them and

opens doors for them while dealing with MNCs and Corporates. They can also submit credit rating

for tenders and make themselves more credible to get bigger orders. It also provides easier access to

other sources of finance such as private equity. Better ratings have helped the SMEs retain

customers and suppliers, and negotiate better terms with them.

The government also favours rated SMEs, restricting certain contracts for such firms. It also operates

a performance and credit rating scheme through various credit rating agencies via the National Small

Industries Corporation. The scheme provides a one-time subsidy to SMEs to get rated.

Tools for self-improvement

Another advantage of rating is that the highlighting of strengths and weaknesses acts as a trigger for

self-correction. A regular renewal of ratings not only helps improve a firm's performance but also

builds confidence within the lender fraternity and trading channel. It is like a report card for SMEs.

The analysis helps them to continuously evolve based on the changing regulation, business

requirements and economic scenario.

SMEs are usually deterred by the rigour of rating discipline and fear of low rating, but the latter may

not necessarily be the result of weak financials and can be attributed to various reasons. "The issues

can be easily pointed out in the rating report. The SMEs that want to run a sustainable business take

the feedback positively and try to improvise. It is an opportunity to implement best business

Practices.

Increased visibility

32

Rating increases visibility and credibility on the SME. Since rating is an independent third party

opinion on creditworthiness, it helps in providing confidence to the lenders and various

stakeholders. With higher credibility the SMEs are able to acquire funds from various avenues which

otherwise would not be keen on lending.

Agencies working for Credit rating

National Small Industries Corporation Limited (NSIC)

A PSU established by the Government of India in 1955. It falls under Ministry of Micro, Small &

Medium Enterprises of India. It checks performance and credit rating scheme for Small scale

industries.

There is a need to create awareness amongst Small-Scale Units about the strengths and weaknesses

of their existing operations and to provide them an opportunity to enhance their organizational

strengths. As a step in this direction, a need was felt for introducing a Rating Scheme for the Small

Scale Industries. It is expected that the Rating Scheme would encourage SSI sector in improving its

contribution to the economy by way of increasing their productivity, since a good rating would

enhance their acceptability in the market and also make access to credit quicker and cheaper and

thus help in economizing the cost of credit.

Performance & Credit Rating Scheme for Small Scale Industries has been formulated in consultation with various stakeholders i.e. Small Industries Associations, & Indian Banks’ Association and various Rating Agencies viz. CRISIL, ICRA, Dun & Bradstreet (D&B) and ONICRA. It has the approval of the Government.

SME rating agency of India

SMERA Ratings Limited (formerly SME Rating Agency of India Ltd.) is a joint initiative of Small

Industries Development Bank of India (SIDBI), Dun & Bradstreet Information Services India Private

Limited (D&B) and leading public and private sector banks in India. SMERA commenced its

operations in 2005 as an exclusive credit rating agency for Micro, Small and Medium Enterprises

(MSME) sector in the country. Within a span of eight years, SMERA has assigned ratings to over

28,000 MSMEs across India.

SMERA is registered with the Securities and Exchange Board of India (SEBI) as a Credit Rating Agency

(6th in India). SMERA is also empanelled as an approved rating agency by the National Small

Industries Corporation Ltd. (NSIC) under the ‘Performance & Credit Rating Scheme for Small

Industries’ approved by the Ministry of Small Scale Industries, Government of India.

CARE SME Rating

CARE introduced SME ratings in 2006, which is intended entirely for Small and Medium Scale

Enterprises. CRISIL has two separate scales on which it assigns ratings to SMEs: the NSICCRISIL

33

Performance and Credit Rating (NSIC-CRISIL) scale for small scale industries (SSIs), and the CRISIL

SME Rating scale. CRISIL’s ratings on small and medium enterprises (SMEs) reflect the rated entities’

overall creditworthiness, adjudged in relation to other SMEs. These ratings are entity-specific, and

not specific to debt issuances. CARE is a leading rating agency in India recognized by the major

regulators of the financial market viz SEBI and RBI. CARE’s unbiased opinion is trusted by various

investor communities.

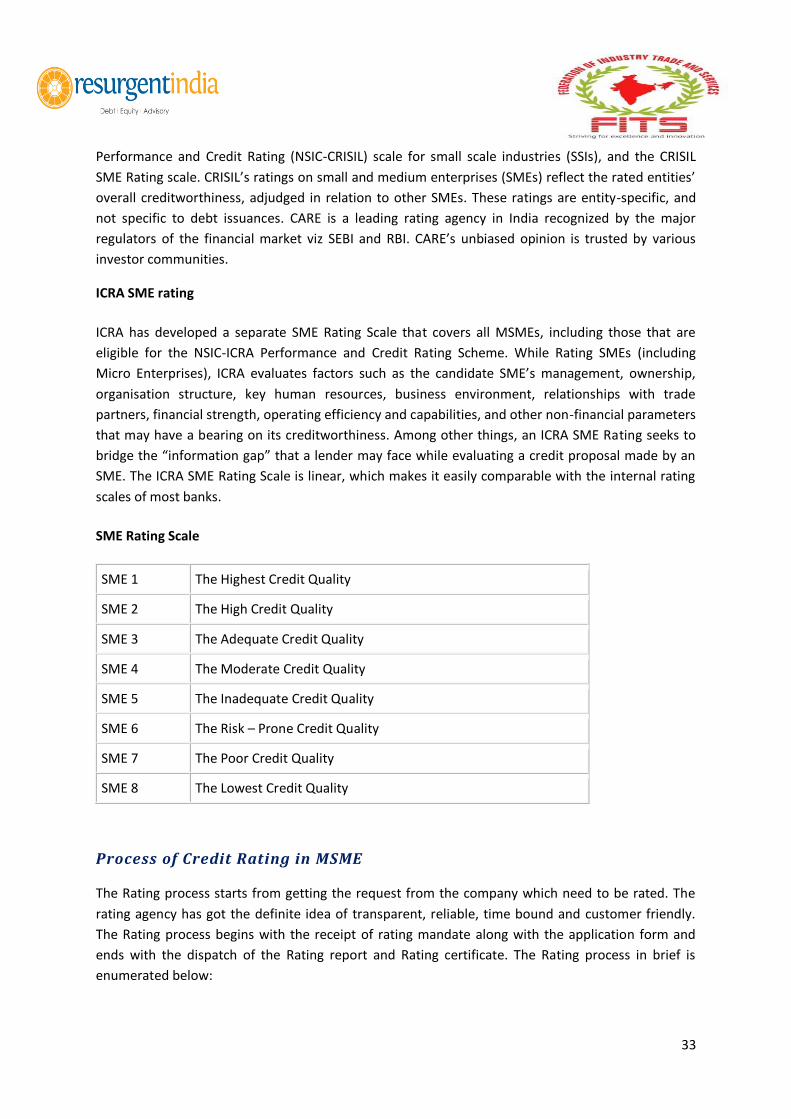

ICRA SME rating

ICRA has developed a separate SME Rating Scale that covers all MSMEs, including those that are

eligible for the NSIC-ICRA Performance and Credit Rating Scheme. While Rating SMEs (including

Micro Enterprises), ICRA evaluates factors such as the candidate SME’s management, ownership,

organisation structure, key human resources, business environment, relationships with trade

partners, financial strength, operating efficiency and capabilities, and other non-financial parameters

that may have a bearing on its creditworthiness. Among other things, an ICRA SME Rating seeks to

bridge the “information gap” that a lender may face while evaluating a credit proposal made by an

SME. The ICRA SME Rating Scale is linear, which makes it easily comparable with the internal rating

scales of most banks.

SME Rating Scale

SME 1 The Highest Credit Quality

SME 2 The High Credit Quality

SME 3 The Adequate Credit Quality

SME 4 The Moderate Credit Quality

SME 5 The Inadequate Credit Quality

SME 6 The Risk – Prone Credit Quality

SME 7 The Poor Credit Quality

SME 8 The Lowest Credit Quality

Process of Credit Rating in MSME

The Rating process starts from getting the request from the company which need to be rated. The

rating agency has got the definite idea of transparent, reliable, time bound and customer friendly.

The Rating process begins with the receipt of rating mandate along with the application form and

ends with the dispatch of the Rating report and Rating certificate. The Rating process in brief is

enumerated below:

34

After getting the request from the company, the company has to file the necessary

application along with list of documents required for the rating agency to conduct the

research about the organization along with the necessary fee. After submitting the

documents, the rating agency team will have direct site visit to the company and they will

have detailed discussion with the management about their vision, problems, benefits etc to

have an over sight about the company. They will also talk to their supplier, customers,

bankers about the performance of the company in terms of timely delivery of finished goods

and inventory management.

After their discussion, the rating agency will start doing the rating process with the preset

conditions laid down for SME with their rating scale.

Once the rating team has finished the rating module, it will be transferred to the rating

committee which will consist of eminent team with industry expertise and they will analyze

the rating formula and the company’s documents. Once they have verified all the

documents, then the rating committee will decide what scale can be allotted to the

company. Once that is decided, then the rating agency will complete the rating and send the

rating report to the company.

The company will have rights to accept all the conditions laid down in the rating report or

they can provide additional information to prove their company to be upgraded. Once the

submitted documents are satisfying the committee, then they will upgrade or maintain the

same standard to the company and submit the same to the company.

Once the rating mechanism is over and rating has been done, then the management of SME

can take the same to the banker for getting the facility for their business improvement.

35

Conclusion

The importance of MSME has been recognized in recent years for its significant contribution in

gratifying various socio-economic objectives such as higher growth of employment, output,

promotion of exports and fostering entrepreneurship. They play a crucial role in the industrial

development of any country. This sector even assumes greater importance now as the country

moves towards a faster and inclusive growth agenda. MSMEs have also shown an ability for

innovation, creativity, and flexibility which qualifies them to respond promptly to changing market

conditions and to adapt the dynamic needs of the consumers.

Therefore, this sector needs special attention of the state government, policy makers and

implementation. This is all the more necessary and a very powerful engine realizing the twin

objectives of “accelerated industrial growth” and “creation of additional productive employment

potential” in rural and backward areas. There are only 1.5 million MSME units are in registered

segment and employment, finance and other activities of only these units are recorded with the

government. There is an urgent need to have a policy to record all units to understand the actual

position of employment as on date and employment generation opportunities exist in this sector in

future. This will enable policy makers to decide the course of action, such as creation of cluster,

providing suitable infrastructure, market, product development, finance etc.

Adequate and timely availability of Finance is one of the most important key inputs for any business.

Although, Banks in India have been providing financial facilities to MSMEs through their branch

offices, regional offices in across the length and breadth of the country, however, there are still

many gaps and challenges and we can say there are still miles to go in order to improve the access to

timely credit to entrepreneurs in the MSME sector.

One of the key challenges faced by MSME sector in India is the lack of skilled labor. Despite the huge

pool of human resources in India, MSMEs struggle to find the required skilled labor at affordable

wages. Even though MSMEs are investing in infrastructure, technology and manufacturing practices,

development of skilled manpower still remains a major concern. There is evidence that suggests that

MSMEs that have invested in skill development have witnessed better business performance. Skill

development programs with a blend of industrial engineering, quality management, general

management and soft skills can enable the MSMEs to reach the next level of growth.

36

About Federation of Industry, Trade and Services (FITS)

Federation of industry, trade & services (FITS) is a proactive and dynamic national chamber working

at the ground level with established national and international linkages.

FITS tends to act as a catalyst in the promotion of all sectors of our economy viz; manufacturing,

trade and services. It favours research-based and time-tested policy initiatives for positive impact on

the economic growth and development of the nation. During the last two decades, the Government

has been focusing on achieving inclusive and sustainable growth by undertaking vast infrastructure

development projects cutting across sectors, creating an enabling environment for inviting greater

private sector participation through regulatory reforms, improving the delivery of public services and

stressing for e-governance and skill development. These measures have started showing results and

in the process the international community too has shown a keen interest in being a part of this

growth-momentum.

With over 1.2 billion population, we are the fourth largest economy of the world with most number

of young, english speaking and technically sound workforce. We have grown to be a global

agriculture power-house after being dependent on the out-side world for green imports for so many

years. Life expectancy and literacy rates in our country have almost doubled and quadrupled in last

few-years.

FITS being a body of the Industry, Trade and Services stands for the Govt.'s call for 'Skilling India for

Global Competitiveness' and thus contribute to socio-economic development and capacity building

in different domains. Through its 1200+ direct and indirect associates spread –over in public and

private sectors, MSMEs, and large corporates, FITS is destined to play its crucial role in the nation

building.

As a policy, FITS engages with Ministries/Deptts. of Govt. of India and state Govts. on issues which

directly or indirectly impacts the industry and trade. It strives for skill development thus enhancing

efficiency, a greater feeling of focusing competitiveness and multiplying business opportunities for

growth. We associate with different Govt. agencies, autonomous bodies, National & International

NGOs, Knowledge partners, RWAs and civil society institutions for effecting improvements in

Corporate social Responsibility, healthcare sector, Waste management, homeland security, social

and domain reforms, education and sanitation etc. to name a few with special thrust for the most

vulnerable sections of the society be it women security and police reforms..

FITS is of the considered opinion that the pro-active support and role of the Central and State Govts.

is crucial for creating a resurgent India . The current political and economic scenario expects all

political formations of the country to join-hand to support the young generation's aspirations for

economic growth.

37

About Resurgent India Limited

DEBT I EQUITY I ADVISORY Resurgent India is a full service investment bank providing customized solutions in the areas of debt, equity and merchant banking. We offer independent advice on capital raising, mergers and acquisition, business and financial restructuring, valuation, business planning and achieving operational excellence to our clients. Our strength lies in our outstanding team, sector expertise, superior execution capabilities and a strong professional network. We have served clients across key industry sectors including Infrastructure & Energy, Consumer Products & Services, Real Estate, Metals & Industrial Products, Healthcare & Pharmaceuticals, Telecom, Media and Technology. In the short period since our inception, we have grown to a 100 people team with a pan-India presence through our offices in New Delhi, Kolkata, Mumbai, and Bangalore. Resurgent is part of the Golden Group, which includes GINESYS (an emerging software solutions company specializing in the retail industry) and Saraf& Chandra (a full service accounting firm, specializing in taxation, auditing, management consultancy and outsourcing). www.resurgentindia.com © Resurgent India Limited, 2016. All rights reserved. Disclosures This document was prepared by Resurgent India Ltd. The copyright and usage of the document is owned by Resurgent India Ltd. Information and opinions contained herein have been compiled or arrived by Resurgent India Ltd from sources believed to be reliable, but Resurgent India Ltd has not independently verified the contents of this document. Accordingly, no representation or warranty, express or implied, is made as to and no reliance should be placed on the fairness, accuracy, completeness or correctness of the information and opinions contained in this document. Resurgent India ltd accepts no liability for any loss arising from the use of this document or its contents or otherwise arising in connection therewith. The document is being furnished information purposes. This document is not to be relied upon or used in substitution for the exercise of independent judgment and may not be reproduced or published in any media, website or otherwise, in part or as a whole, without the prior consent in writing of Resurgent. Persons who receive this document should make themselves aware of and adhere to any such restrictions.

38

Contact Details:

Gurgaon 903-904, Tower C, Unitech Business Zone, Nirvana Country, Sector 50, Gurgaon – 122018 Tel No.: 0124-4754550 Fax No.: 0124-4754584

Kolkata CFB F-1, 1st Floor, Paridhan Garment Park, 19 Canal South Road, Kolkata - 700015 Tel. No. : 033-64525594 Fax No. : 033-22902469

Mumbai Quest Offices Private Ltd The ParineeCrescenzo, 1st Floor Opp. MCA, G-Block, B.K.C Mumbai-400051 T: +91-22-33040667/668 F: +91-22-33040669

Bengaluru SreeLaxmiPlaza, 3rd Floor, No. 61, 24th main, 7th cross, Marenahalli, J.P. Nagar 2nd phase, Bangalore –560 078 Karnataka Tel. No.: +91 80 4153 0757

Chennai C3, KUDIL, 23/22, Easwaran Colony, Sarwamangala Nagar, Nanganaullar, Chennai – 600061

www.resurgentindia.com