Employment status and -payroll working in the public sector” · “Off-payroll working in the...

44

Employment status and “Off-payroll working in the public sector” June 2017

Transcript of Employment status and -payroll working in the public sector” · “Off-payroll working in the...

Employment status and “Off-payroll working in the public sector”

June 2017

2

Agenda

• Background

• Assessing employment status for tax purposes

• Using HMRC’s web based tool – “CEST” (formerly ESS, formerly ESI)

• What does it mean financially?

• Questions

3

Background Terms of reference

Introductions

• Deloitte’s involvement with the media industry

Participative and constructive

• ALL questions welcomed and strongly encouraged

• The session is for you

• We will provide full explanations of the rules including all generic principles

Follow up questions/helpline

• We will provide an email facility for any further questions

• Plus a hotline if there is anything you want to discuss later

• Please see final slide for contact details

Out of scope

• We won’t be able to provide you with specific advice on your own tax returns

• Well, not without you signing an engagement letter!

4

Background employment status for tax purposes Engaging through an intermediary eg. PSC

Where a client engages an individual (you)

• Who personally performs services, or is under obligation to personally perform services for a client (the BBC)

• The services are provided through an intermediary:

o Usually a personal service company (PSC)

o Sometimes a partnership (LLP)

o Can be an individual (usually children)

• The services are provided under circumstances where, if the contract had been directly with the client, the individual would be regarded for tax purposes as an employee of the client (i.e. the same IR35 test as always)

From 6 April 2017,

• Where the client is a ‘Public Authority’

o all entities subject to the Freedom of Information Act

o so includes the BBC and Channel 4

IR35 applies

Public Sector IR35

applies

5

Background What’s changing and why?

Engaging with the BBC directly as an individual

• The BBC (like every engager) must assess the employment status of individuals for tax purposes, in order to apply the correct tax treatment

• If the assessment is “self-employed” the BBC can pay individuals gross. Individuals must then pay their own tax and national insurance contributions (NIC) to HMRC

• If the assessment is “not self-employed”, the BBC must withhold tax and NIC from payments and remit these to HMRC through the “PAYE” regime

• To assess employment status for tax purposes in practice:

• Up until 5 April 2017 – the BBC applied the bespoke, HMRC agreed, “BBC Test”

• From 6 April 2017 – the BBC will apply the new HMRC web based tool (“CEST”)

• “CEST” stands for “Check Employment Status for Tax”

• Previously, CEST was called the “ESS”, and prior to that the “ESI”

6

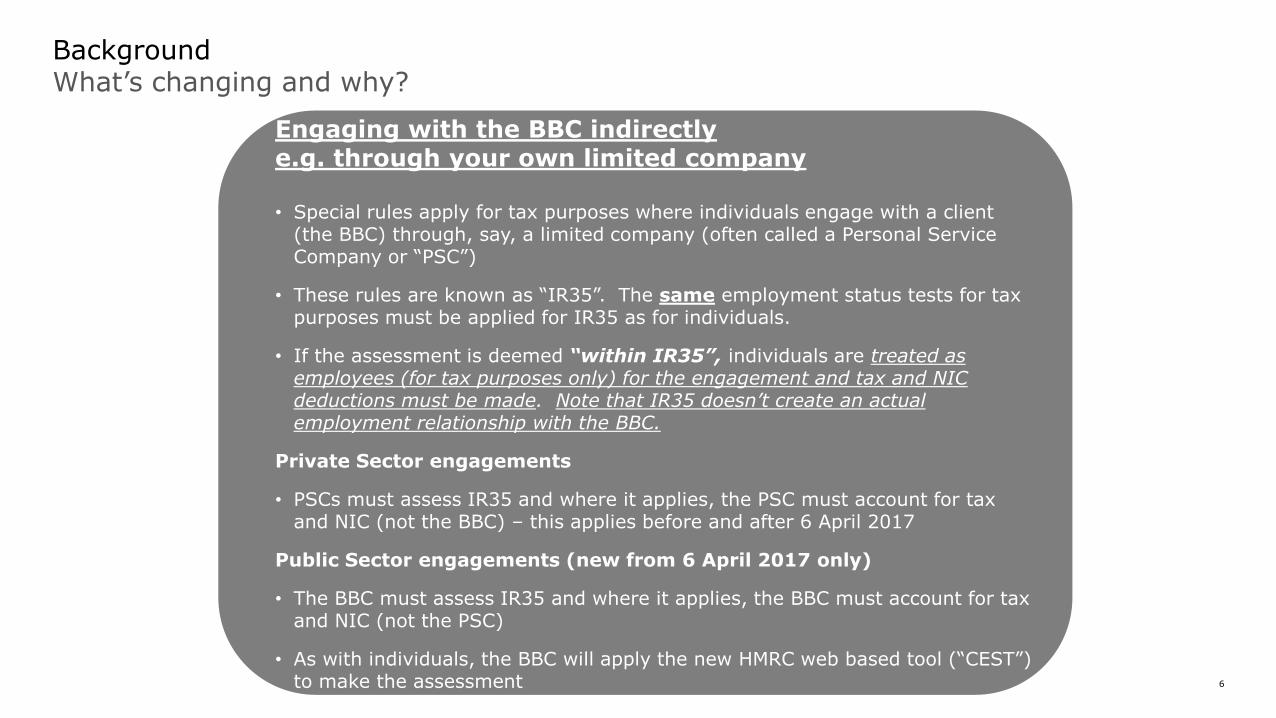

Background What’s changing and why?

Engaging with the BBC indirectly e.g. through your own limited company • Special rules apply for tax purposes where individuals engage with a client

(the BBC) through, say, a limited company (often called a Personal Service Company or “PSC”)

• These rules are known as “IR35”. The same employment status tests for tax purposes must be applied for IR35 as for individuals.

• If the assessment is deemed “within IR35”, individuals are treated as employees (for tax purposes only) for the engagement and tax and NIC deductions must be made. Note that IR35 doesn’t create an actual employment relationship with the BBC.

Private Sector engagements

• PSCs must assess IR35 and where it applies, the PSC must account for tax and NIC (not the BBC) – this applies before and after 6 April 2017

Public Sector engagements (new from 6 April 2017 only)

• The BBC must assess IR35 and where it applies, the BBC must account for tax and NIC (not the PSC)

• As with individuals, the BBC will apply the new HMRC web based tool (“CEST”) to make the assessment

7

Assessing employment status for tax purposes

8

Assessing employment status for tax purposes

What indicators are used to assess employment status?

Provision of own equipment

(more common behind camera)

Control – where & when

(studio / on location)

Personal factors

(e.g. other clients)

Level of integration within the organisation

• In order to determine employment status, many indicators must be considered and applied to each engagement individually

• None of the indicators individually determine the final outcome

• However, the indicators vary in significance, according to the person and the particular engagement they are working on

Indicators are :

Personal service

(vs. substitution)

Control – How & what

(vs. own creative input)

Ability to profit

(£/programme vs. £/hour)

Financial risk

(remediation insurance,

other losses)

9

Assessing employment status for tax purposes Engaging as an individual

Individual pays:

• Income tax

• Class 2/4 NIC

BBC

Individual

Assess Employment

Status

Assessment does not confirm self-

employed

Assessment confirms self-

employed

BBC withholds:

• Tax

• Ee’s NIC

BBC pays:

• Er’s NIC

• Up until 6 April 2017 – the BBC used a bespoke Test agreed with HMRC, to assess employment status for tax purposes.

• From 6 April 2017 – the BBC will now use HMRC’s web based tool to assess employment status for tax purposes:

• This is called “CEST”, which stands for “Check Employment Status for Tax”.

• It used to be called the Employment Status Service (ESS)

• And before that it was the Employment Status Indicator (ESI)

10

Assessing employment status for tax purposes Engaging through a personal service company (PSC)

Private Sector Engagements (and public sector up to 5 April 2017)

IR35 does not

apply

PSC pays:

• Corporation

tax on profits

• Er’s NIC

Individual pays:

• Income tax

on dividends

and salary

• Ee ‘s NIC

BBC

Individual

PSC assesses tax status of engagements

Assessment confirms self- employed for

tax (IR35 does not apply)

Treat as

employed for

tax - apply

IR35

PSC withholds:

• Tax

• Ee’s NIC

PSC pays:

• Er’s NIC

PSC

Assessment does not confirm self-employed for tax

(IR35 applies)

BBC

Treat as

employed for

tax - apply

Public Sector

IR35

BBC withholds

for HMRC:

• Tax

• Ee’s NIC

BBC pays:

• Er’s NIC

BBC assesses tax status of engagements using CEST

PSC

Individual

Assessment confirms self- employed for

tax (IR35 does not apply)

Public Sector Engagements from 6 April 2017

Assessment does not confirm self-employed for tax

(IR35 applies)

Public Sector

IR35 does not

apply

PSC pays:

• Corporation

tax on

profits

• Er’s NIC

Individual

pays:

• Income tax

on

dividends

and salary

• Ee’s NIC

11

Summary - who must “assess and pay” If the CEST assessment does not support “self employed” (IR35 applies)

BBC (will apply Public

Sector IR35)

Individual

PSC

Public sector only from 6 April 2017

Blue = person who must assess employment status for tax, and then deduct and remit tax/NIC if status is “employed” or “treat as employed” or “IR35 applies”

PSC (should apply

IR35)

Individual

BBC

Private Sector at all times

(and public sector up to 5 April 2017)

BBC

Individual

Individuals

12

Using CEST (formally ESS/ESI)

to determine employment status

https://www.gov.uk/guidance/check-employment-status-for-tax

13

Using the CEST (ESS) Three possible outcomes

Employed / Treat as employed / Public Sector IR35 applies

• BBC is required to deduct tax and NIC via PAYE on the payments it makes to you/your PSC (Public Sector IR35)

• You have the option to contact HMRC to agree your employment status and then provide a written confirmation of the outcome from HMRC to the BBC or resolve via self-assessment

• If you wish to seek to agree your status with HMRC, it will be important to (i) keep the BBC informed so we can liaise with you / HMRC as necessary and (ii) pursue the matter sooner rather than later to avoid limitation periods expiring

Self-employed / Public Sector IR35 does not apply

• BBC may pay you/your PSC gross, without tax and NIC deductions

Unable to determine

• You have the option to contact HMRC to agree your employment status and then provide a written confirmation of the outcome from HMRC to the BBC or resolve via self-assessment

• As above, if you wish to agree your status with HMRC, please keep the BBC informed and pursue the matter sooner rather than later.

• If it cannot be shown that you can be correctly assessed as self-employed – PAYE/NIC will apply

14

Using the CEST (ESS) If your CEST assessment is “employed” or “unable to determine”…(1a)

1a) Immediate action you could take if you are not happy with this outcome:

• You can contact HMRC directly (sooner rather than later) yourself to obtain a definitive assessment in writing, being either:

(a) Public Sector IR35 applies – the BBC must treat you as employed; or

(b) Public Sector IR35 does not apply – okay to pay as self-employed

• You will need to provide HMRC with details of other relevant factors not already covered by CEST

• You may wish to speak to your accountant first regarding what other information may be relevant / helpful and what time limits apply

• Keep the BBC informed throughout the process so it can liaise with you / HMRC as necessary

• In the first instance, you should contact the HMRC hotline – details on the HMRC website

• You should provide the BBC with HMRC’s confirmation in writing (together with the additional details you provided HMRC in order to secure their confirmation)

• The BBC will review the details and update your assessment as appropriate

15

Using the CEST (ESS) If your CEST assessment is “employed” or “unable to determine”…(1b)

1b) Where do I stand if HMRC tells me to speak to the BBC?

• We are aware that some individuals who have contacted HMRC have been referred back to the BBC for resolution

• This does not reflect the correct position for two main reasons:

• First, HMRC has a statutory obligation (see below) to make employment status determinations for all individuals (whatever sector they work in)

• Second, in media, where an individual meets the necessary requirements, HMRC has routinely issued rulings on employment status, sometimes called “Lorimer letters” (aka “LP10 letters”)

• The preference is to explain your position to HMRC and obtain an HMRC ruling on your employment status amicably. But if you need to quote legislation:

• Section 8(1) Social Security Contributions (Transfer of Functions, etc) Act 1999, includes an obligation for HMRC to decide a worker’s employment status

• Specifically, HMRC must decide the category of earner the worker is for the purposes of Parts I to V Social Security Contributions and Benefits Act 1992, which categorise earners as “employed earners” or “self-employed earners”); or whether a person is liable to pay NICs of a particular class [i.e. employed class 1 or self-employed class 2/4 NIC) and, if so, the amount.

• Also, if you disagree with HMRC’s decision, you have a right of appeal. You will need to take independent advice should you choose to do so.

16

Using the CEST (ESS) If your CEST assessment is “employed” or “unable to determine”…(2)

2) Do nothing now, but take the matter up when you submit your Self-Assessment Tax Return

• If you believe you have sufficient grounds to claim you are self-employed, you can file your Tax Return on that basis.

• We strongly recommend you take personal tax advice before doing so (ideally sooner rather than later in respect of applicable time limits)

• Keep the BBC informed throughout the process so it can liaise with you / HMRC as necessary

• Sole Traders

• You would request a repayment of any Class 1 NIC withheld

• If HMRC agrees, you would instead pay Class 2 and Class 4 NIC (at a lower rate than Class 1 NIC)

• Tax is payable at the same rate by employees and self-employed individuals but you may be able to claim further expenses

• PSCs

• You would request a repayment of any PAYE and NIC withheld by the BBC

• If HMRC agrees, you may need to re-state the profits in your PSC to take account of the grossed up income including any repayment.

• You may pay additional corporation tax and some income tax on any additional dividends you pay

17

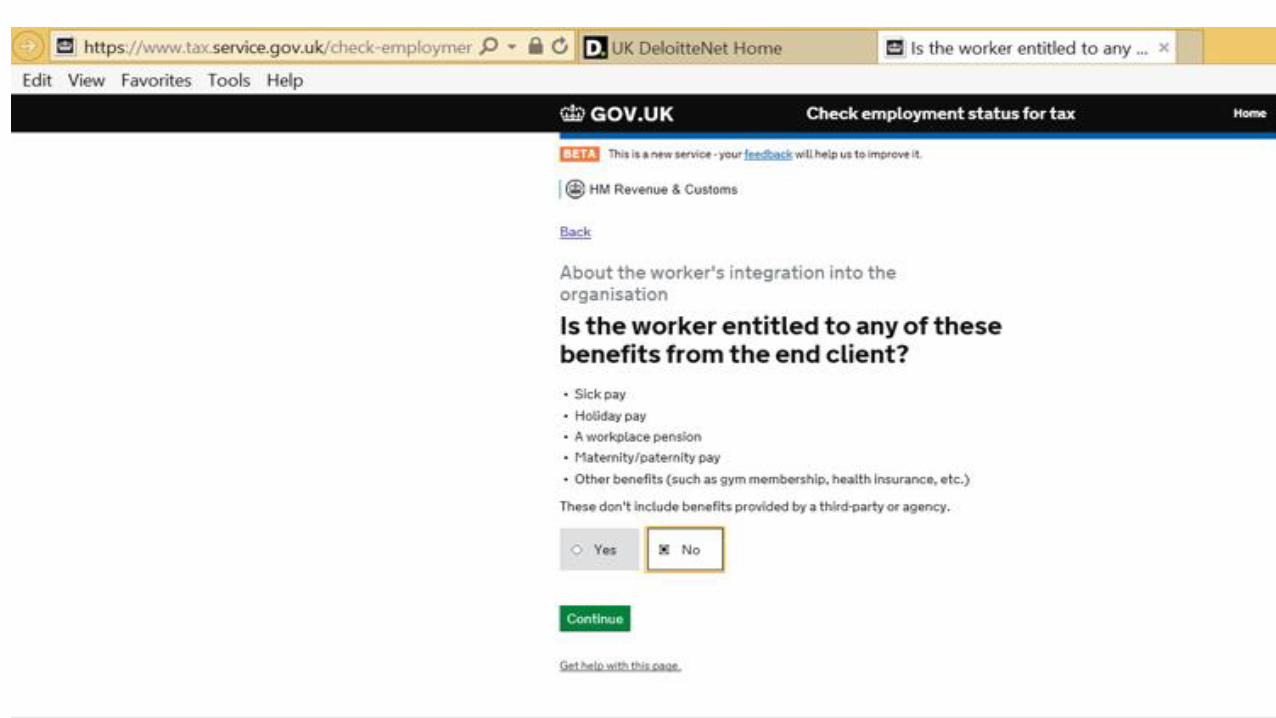

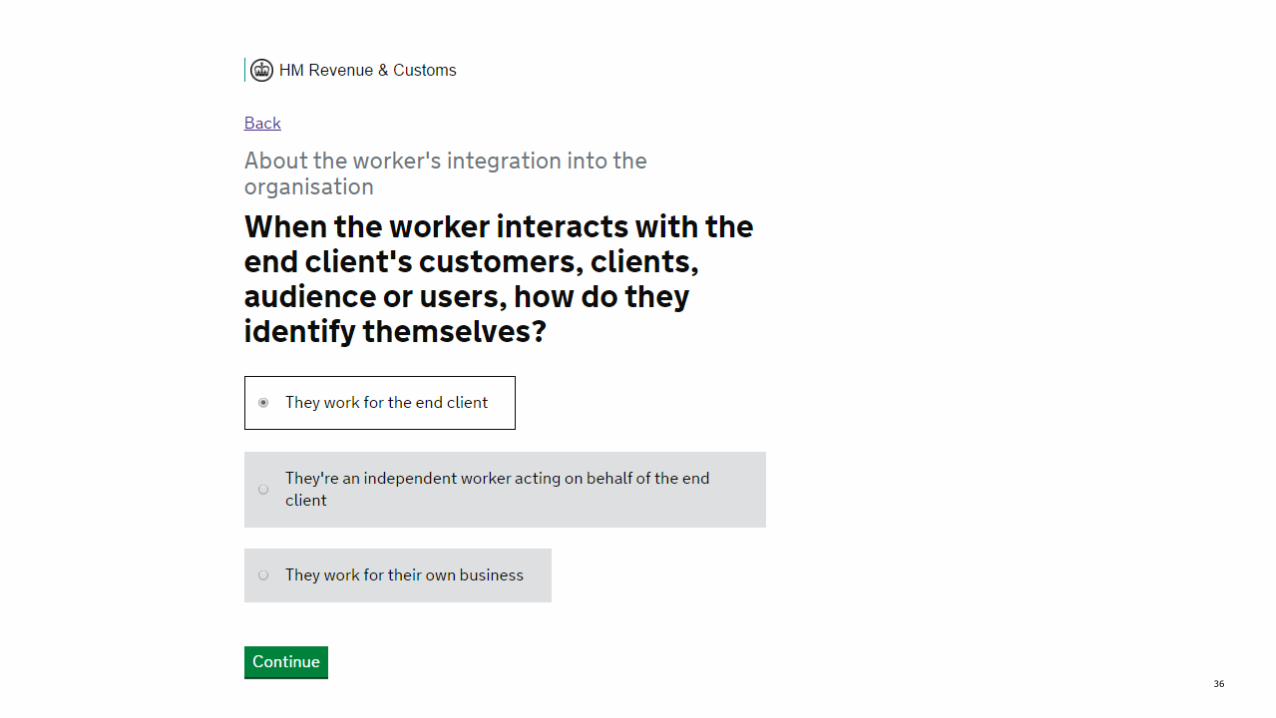

Using the CEST (ESS) Understanding and answering the CEST questions

• Many questions are straight forward

• But the meaning of others is not so clear

• Deloitte has invested considerable time with HMRC in respect of the meaning of these questions

• We will explain the nuances as we work through an end to end scenario

• But please note:

• HMRC will not stand by the output of the CEST unless the questions are interpreted and answered in the way HMRC has explained was intended

• In addition, HMRC has included caveats in CEST to this effect, as we will now see…

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

Note that with this assessment, the tax outcome is broadly the same for you, whether working in the public or private sector.

However, the tax collection process is different in each sector:

• In the public sector, the Fee Payer paying your PSC has to withhold and account for PAYE/NIC under Public Sector IR35;

• In the private sector your PSC is responsible for the PAYE/NIC, under IR35;

• You cannot claim a 5% deduction if Public Sector IR35 applies (this is only relevant for IR35). You will need to claim any other expenses through your PSC regardless of sector – e.g. if you qualify for tax relief on agency fees (covered later)

38

What does it mean financially?

39

Financial impact on you and the BBC

Assessment for tax purposes: Employed Treat as

Employed

Treat as

Employed

Before &

after 6 April

2017

Until 5 April

2017

From 6 April

2017

Engaged as: Individual PSC PSC

Tax collection process: PAYE Payroll

PAYE IR35

PAYE Payroll (Public Sector

IR35)

Individual

Gross fees received by Individual/PSC 40,527 45,000

Employer's class 1 NIC – payable by PSC (4,473)

Salary PSC can pay Individual 40,527 40,527

Employee's class 1 NIC - deducted by BBC (3,896) (3,896) (3,896)

Income tax (PAYE) - deducted by BBC (5,905) (5,905) (5,905)

Corporation tax payable by PSC

Income tax payable by Individual personally

Self employed Class 2 + Class 4 NIC payable by

Individual personally

Net income receivable by Individual 30,726 30,726 30,726

BBC Gross taxable payment to Individual/PSC 40,527 45,000 40,527

Employer's class 1 NIC payable – payable by BBC 4,473 - 4,473

Contract value inclusive of employer’s NIC 45,000 45,000 45,000

40

Key assumptions and findings from the financial analysis

Key Assumptions

• For simplicity, the figures ignore expenses and the 5% deduction which is only available under IR35

Key findings

• Under these assumptions, a gross contract worth £45,000 would be worth £30,726 in net pay terms, whether you are:

• Employed (column 3)

• Operate through a PSC and IR35 applied before 6 April 2017 (column 4)

• Operate through a PSC and Public Sector IR35 applies from 6 April 2017(column 5)

• Current UK tax rules allow individuals who are genuinely self-employed to pay less NIC as they are entitled to fewer state benefits, although this is under review

41

Specific tax deduction Agency fees

An individual employed as an “entertainer” may claim a deduction for agency fees, subject to the following conditions:

• "Entertainer" means an actor, dancer, musician, singer or theatrical artist

• Richard & Judy (Madeley & Finnigan v HMRC [2006])

• Court looked for (and found in their skits) an element of theatrical “performance”

• The fees must be % of earnings from the employment

• A maximum deduction of 17.5% may be claimed

• At the time the fees are paid, the agent is carrying on an employment agency with a view to profit i.e.

• Finding workers employment with employers; or

• supplying employers with workers for employment by them

42

Any Questions?

43

Contact information

Deloitte

Mark Groom

Telephone: +44 207 007 2770

Email: [email protected]

Tim Waterhouse

Telephone: +44 172 788 5133

Email: [email protected]

Telephone

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.co.uk/about for a detailed description of the legal structure of DTTL and its member firms. Deloitte LLP is the United Kingdom member firm of DTTL. This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will depend upon the particular circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of the contents of this publication. Deloitte LLP would be pleased to advise readers on how to apply the principles set out in this publication to their specific circumstances. Deloitte LLP accepts no duty of care or liability for any loss occasioned to any person acting or refraining from action as a result of any material in this publication. © 2017 Deloitte LLP. All rights reserved. Deloitte LLP is a limited liability partnership registered in England and Wales with registered number OC303675 and its registered office at 2 New Street Square, London EC4A 3BZ, United Kingdom. Tel: +44 (0) 20 7936 3000 Fax: +44 (0) 20 7583 1198.