Employee selection Transforming healthcare through innovation

Upload

dennis-campbellCategory

view

219download

0

DOI: 10.1111/j.1475-679X.2012.00457.xJournal of Accounting Research

Vol. 00 No. 0 xxxx 2012Printed in U.S.A.

Employee Selection as a ControlSystem

D E N N I S C A M P B E L L ∗

Received 30 November 2010; accepted 9 March 2012

ABSTRACT

Theories from the economics, management control, and organizational be-havior literatures predict that when it is difficult to align incentives by con-tracting on output, aligning preferences via employee selection may providea useful alternative. This study investigates this idea empirically using person-nel and lending data from a financial services organization that implementeda highly decentralized business model. I exploit variation in this organiza-tion in whether or not employees are selected via channels that are likely tosort on the alignment of their preferences with organizational objectives. Ifind that employees selected through such channels are more likely to usedecision-making authority in the granting and structuring of consumer loansthan those who are not. Conditional on using decision-making authority, theirdecisions are also less risky ex post. These findings demonstrate employee se-lection as an important, but understudied, element of organizational controlsystems.

1. Introduction

This study examines the relationship between employee selection andmanagement control outcomes. Theories from economics, accounting,

∗Harvard Business School. Accepted by Merle Erickson. I thank Srikant Datar, MariaLoumioti, V.G. Narayanan, Tatiana Sandino, Suraj Srinivasan, Michael Toffel, Peter Tufano,and seminar participants at the Harvard Information, Markets, and Organizations Confer-ence, Northwestern University, University of Minnesota, and Tilburg University for helpfulcomments. I acknowledge the financial support of the Division of Research of the HarvardBusiness School. All errors remain my own.

1

Copyright C©, University of Chicago on behalf of the Accounting Research Center, 2012

2 D. CAMPBELL

and organizational behavior predict that when it is difficult to align in-centives by contracting on output, aligning preferences via employee se-lection may provide a useful alternative (Merchant [1985], Cohen andPfeffer [1986], Akerlof and Kranton [2000, 2005], Simons [2000], Pren-dergast [2008]). Moreover, there is considerable evidence that organiza-tions devote significant resources to employee selection in settings whereit is difficult to contract on output (Heskett, Sasser, and Schlesinger [1997,2003], Goodsell [2004]). Despite the long-standing nature of these theo-ries, the diversity of the disciplines in which they are posited, and theirapparent importance within organizations, empirical evidence is generallylacking.

I address this gap using personnel and lending data from a highlydecentralized organization in which there is a basic management con-trol problem—motivating employees to use decision-making authorityeffectively—that is difficult to solve via measuring and contracting on out-put. I exploit variation within this organization in whether or not employ-ees are selected via channels that are likely to sort on the alignment of theirpreferences with organizational objectives.

In particular, I make use of two features of this organization that give riseto such variation. First, the organization underwent a significant changefrom a highly centralized structure to one that is highly decentralized. Manyof the employees working in the decentralized organization were hiredprior to this change whereas many were hired after it. I use the structurethat the employee was hired into as an indirect indicator of the extent towhich his or her preferences are aligned with the decentralized organiza-tion’s objectives. Second, some employees are screened into the organiza-tion via its normal hiring processes whereas others are referred by existingemployees. Prior literature has demonstrated that job candidates referredby the firm’s current workers are more likely to survive the selection pro-cess and tend to have better posthire career outcomes consistent withhires through this channel being better matched to their respective firms(Fernandez, Castilla, and Moore [2000]). In accordance with this litera-ture, I use the referral source of the employee as an additional indirectindicator of the extent to which his or her preferences are aligned with thedecentralized organization’s objectives.

Using these observable indicators, as well as a unique data set linking spe-cific employees to specific lending decisions, I establish a direct empiricallink between the channel of employee selection and both aspects of the ba-sic management control problem in this setting—the use and performanceoutcomes of employee decision-making authority. In particular, I find thatemployees selected through “more aligned” channels are more likely touse decision-making authority in the granting and structuring of consumerloans than those who are not. Conditional on using decision-making au-thority, their decisions are also less risky ex post. I interpret these findingsin the context of prior literature as demonstrating employee selection as animportant, but understudied element of organizational control systems.

EMPLOYEE SELECTION AS A CONTROL SYSTEM 3

This study makes two primary contributions. First, I contribute to therelatively large and multidisciplinary literature on employee selection as amanagement control mechanism by providing, to my knowledge, the firstdirect empirical evidence of a link between employee selection and bettermanagement control outcomes. In particular, my results provide evidencein support of long-standing management accounting–based models thatposit that control in organizations can be obtained by managing “inputs”(e.g., employee selection) rather than “outputs” (e.g., explicit incentivecontracting on financial performance) (see Merchant [1985] or Simons[2000] for an articulation of this model). Similarly, the findings in this pa-per generally lend empirical support to emerging economic theories onpreference alignment as a solution to contracting problems (Akerlof andKranton [2005], Prendergast [2008]).

Second, this paper extends the accounting-based empirical literature onorganization design. Much of this literature has focused on testing theoriesabout the interrelationships between delegation and incentive compensa-tion and on selected determinants of these two choices (Nagar [2002],Abernathy, Bouwens, and van Lent [2004], Moers [2006], Campbell, Datar,and Sandino [2009]). By focusing exclusively on the explicit incentive com-pensation choice, this research has tended to ignore a variety of othermechanisms that firms might use to achieve management control in del-egated decision environments. The findings in this paper demonstrate thatemployee selection can be a solution to a fundamental accounting prob-lem in many contexts—the difficulty of defining and measuring output—that reduces the ability for explicit contracting to solve the delegationproblem.

2. Prior Literature

The link between employee selection and better management controloutcomes is a topic that has been the subject of considerable theoreticalresearch across literatures as varied as accounting, economics, and organi-zational behavior. Within the accounting literature, the classic input, pro-cess, output model of management control has been a mainstay of text-books for decades (Merchant [1985], Simons [2000]). This model, amongother things, posits that control in organizations can be obtained by man-aging “inputs,” including employees, rather than “outputs” by, for exam-ple, explicit incentive contracting on financial performance. In this way,input based controls are fundamentally ex ante control mechanisms thatare likely to be used when ex post mechanisms of management control likeexplicit performance contracting are difficult or unavailable. Such input-based controls have also widely been referred to as “personnel controls”(Simons [2000], Merchant and Van der Stede [2007]).1 The fundamental

1 The particular mechanisms through which this type of control is exercised have typicallynot been well specified. A considerable amount of case-based evidence suggests that these

4 D. CAMPBELL

insight of these models of control is that more effort placed on screen-ing employees at entry means less emphasis need be placed on monitoringthem once in the organization.

In the organizational behavior literature, Ouchi [1979] posits a form ofmanagement control in organizations called “clan control,” which has fun-damentally similar characteristics to input or personnel controls. In partic-ular, his notion of clan control focuses on management control via norms,shared values, and routines that are facilitated, in part, by the careful selec-tion of employees who are likely to internalize the organization’s desiredvalues. In his theory, such clan control will arise when “rational” forms ofcontrol are unavailable due to difficulty in measuring either behavior oroutput.

The economics literature echoes these insights from a different perspec-tive. Akerlof and Kranton [2000, 2005] propose a theory of identity in or-ganizations in which workers lose utility by deviating from norms of higheffort. The model, not surprisingly, predicts that workers who “identify”with a firm require less incentive pay to motivate effort. Similarly, Falkand Kosfeld [2006] provide experimental evidence that control via explicitincentives is costly and likely to be suboptimal relative to trusting agentswhen their “types” are such that they are nonopportunistic and intrinsicallymotivated.

In related work, Prendergast [2008] directly studies the relationship be-tween contractibility and hiring preferences. His agency theoretic modelpredicts that, in the absence of perfectly contractible performance mea-sures, organizations will hire “biased” agents who are disproportionatelymotivated to carry out only a subset of what the firm cares about with thedegree of bias increasing as contracting measures get worse. The funda-mental insight of his model is that when incentives are difficult to align viaexplicit contracting, aligning preferences through employee selection is aviable alternative.

Similar notions can be seen in the economics-based literature on or-ganizational culture as shared values.2 For example, a key insight of Vanden Steen [2010] is that (1) all agency problems essentially arise from dif-ferences in objectives and (2) shared beliefs and values reduce or elim-inate such differences. While not making the link to employee selectionper se, his model does support a mechanism through which the selectionof employees with particular beliefs or values can be a solution to agencyproblems.

mechanisms include but are not limited to: (1) carefully designed interview processes and/orsystems of referral by existing employees (e.g. Heskett, Sasser, and Schlesinger [1997, 2003];(2) training and indoctrination (e.g. Heskett, Sasser, and Schlesinger [1997, 2003], Merchantand Van der Stede [2007]); and (3) deliberate mechanisms that encourage employee self-selection into and out of organizations (e.g. Frei, Ely, and Winig [2011], Ton [2011]).

2 See Van den Steen [2010] for a thorough review of this literature.

EMPLOYEE SELECTION AS A CONTROL SYSTEM 5

It is worth noting that the theoretical economics literature focuses onemployee preferences as the underlying coordination mechanism, butaccounting-based theories define input controls more generally as thosethat regulate “. . . the antecedent conditions of performance—the knowl-edge, skills, abilities, values, and motives of employees’’ (Snell [1992]). Itis difficult to make clear empirical or even theoretical distinctions betweenconstructs such as preferences or ability, and in practice these constructsare likely to be strongly related—those with higher abilities or lower costsof effort are also likely to have stronger preferences for a given type ofwork. These distinctions, however, are not fundamentally important for thisstudy. Irrespective of whether preferences are shaped by or operate inde-pendently of ability, it remains an open empirical question whether or notagency problems can be effectively mitigated through the presence of par-ticular employee types in the absence of incentives for motivating effort.

Although the theoretical literature on the link between employee selec-tion and incentive alignment is large and diverse, empirical evidence isgenerally lacking with the exception of a growing literature on referral asa hiring source. This literature provides evidence that job candidates re-ferred by an organization’s current workers are more likely to survive theselection process and tend to have better posthire career outcomes thannonreferred counterparts. One reason posited is that the referrer screensthe applicant based on superior information, thus providing a more appro-priate match for the organization. Theoretically, referral may be associatedwith nepotism, which could hinder performance (Goldberg [1982]). How-ever, on balance the existing evidence favors the idea that this hiring sourceprovides better matches between employees and firms (Fernandez, Castilla,and Moore [2000]). As described later, I rely on referral source to proxy forthe extent to which employee and organizational preferences are aligned.

3. Research Setting and Data

The research site for this study is a federal credit union with approx-imately $1.3 billion in assets, 130,000 members, 328 employees, and 23branches operating in a single state in the United Nations.3 The organiza-tion offers traditional financial products and services and counts nationalbanks, community banks, and other credit unions as major competitors.The data for this study come from the organization’s personnel and lend-ing records during the period January 2005–May 2010. Throughout thisperiod, this organization, when compared either to a peer group of same-state credit unions or to a national peer group of similar size, has consis-tently ranked in the top 15% in productivity (revenue per employee), loandefault rates (second lowest), and overall performance (return-on-assets).

3 Credit unions are a form of depository institution that function largely like traditionalbanks but differ in that they are mutually owned and organized by their depositors. Due tothis mutual ownership structure, credit unions typically refer to customers as “members.”

6 D. CAMPBELL

The most salient aspect of the organization for this study is a signifi-cant change undertaken in its business model and management controlsystems by the end of 2004. From this period onward, traditional central-ized policies for everything from waiving fees to underwriting loans werereplaced by a framework that radically decentralized decision-making au-thority. Throughout this paper, I refer to the business model implementedin the period after 2004 as the “new system” and that implemented on orbefore 2004 as the “old system.” The new system has many features that areconsistent with the theoretical literature on employee selection and orga-nizational identity discussed earlier. Namely, output is difficult to measureand contract on, alignment of employee and organizational interests is im-portant, and the selection of employees with particular attributes is increas-ingly relied on as a mechanism to solve this alignment problem.

3.1 DIFFICULTY MEASURING AND CONTRACTING ON OUTPUT

The new system has two interrelated characteristics that give rise to chal-lenges in measuring and contracting on output: (1) objectives are statedin relatively intangible terms and (2) financial outcomes are expected tooccur over relatively long time horizons. Underscoring both of these, thenew system was implemented with an objective of “building relationshipsfounded on trust” with a belief that focusing on building relationshipsthrough member advocacy and service would lead to long-term value cre-ation for both the member and the organization.

Attendant with this objective was a focus on putting members first indecision-making. To facilitate this “member-first” philosophy, authority overvirtually any decision involving a member was heavily decentralized. Forexample, a relevant excerpt from internal documents that were used tocommunicate the change to employees read:

No employee will ever get in trouble for doing what is right for the mem-ber [bold emphasis in original document]. . . Do not consider the systemcapability, policy, or procedure—err on doing whatever is necessary for themember and allow your manager or supervisor to take care of the rest. Fi-nally, be prepared to defend your decision! If your intention is to do whatis right for the member, you have the support of management and yourco-workers.

The decentralization of decision-making authority would have its mostimmediate effect on the organization’s lending practices. As one execu-tive explained: “Employees were given full latitude on rates and overridingour underwriting guidelines. Even [tellers] had this authority.” By contrast,automated risk scoring methodologies were used under the old system todetermine who could or could not get a loan with the institution.

As a mechanism for guiding employee decisions, the organization’s“member-first” philosophy was explicitly codified in a framework inter-nally referred to as “Member, Organization, Employee,” or “MOE.” Ex-tensive efforts were undertaken to communicate this framework, and the

EMPLOYEE SELECTION AS A CONTROL SYSTEM 7

following excerpt from one internal document used in these efforts ex-plains the concept:

. . . MOE was introduced as a tool to help you determine what is right forthe member. MOE—Member, Organization, Employee is your guide. Notsure what’s right in a particular situation? Run it through MOE—in prior-ity order—remembering that the member always comes first and trumpsthe other two. In other words, if a solution is right for the employee or the orga-nization but does not position the member for future success, we will not proceed.[Italic emphasis in original communication.]

The most important aspect of this framework is that it explicitly priori-tizes the customer in the decision-making process, yet also asks employeesto consider the organization when making decisions. The implementationof the MOE framework, and the attendant decision-authority delegated toemployees, is a rather explicit recognition by the top executive team that itis difficult to measure and manage centrally in the new system due to theintangible nature of objectives such as “building relationships,” generat-ing “trust” among members, and “putting the member first.” Decentralizeddecision-making authority, along with the MOE framework, places the in-terpretation of these objectives and the assessment of their tradeoffs withorganizational performance in the hands of individual employees. In short,contracting measures are relatively difficult to develop and apply in the newsystem. This is in contrast to the old system in which standard performancemetrics, such as the number of additional products sold, were used to eval-uate individuals and business units.

3.2 ALIGNMENT OF EMPLOYEE AND ORGANIZATIONAL INTERESTS

The new system yields an obvious incentive alignment problem: motivat-ing employees to use decision-making authority in service provision andto do so in a way that leads to better financial performance in the future.Both aspects of this incentive alignment problem can be seen early in theimplementation of the new system.

Speaking to the challenge of getting employees to use decision-makingauthority, the CEO noted that “We communicated to employees extensivelythat you are empowered, you can circumvent controls, and we really wantmore exceptions. Yet, hesitance to deviate from standard protocols was per-vasive.” Another senior executive attributed much of the reluctance amongemployees to the organization’s previous control systems. She elaborated:“Controls were extremely tight here. Our divisions were run as fiefdoms.You couldn’t even get a fee waived for a member without going throughaccounting.”

The second part of the incentive problem, motivating employees to usedecision-making authority effectively, was also apparent early in the new sys-tem. While well intentioned, much of the early decision making by employ-ees was not well directed. One senior executive elaborated: “There was aperiod early on where employees were doing crazy things like driving across

8 D. CAMPBELL

the state to help members . . . and underwriting $18 loans. We had to askourselves: how do we direct this engagement without dampening it?”

Addressing this problem led the organization to adopt many practicesthat prior literature would predict to find in organizations where outcomesare difficult to measure and contract on. Most important from the perspec-tive of this paper is an increasing reliance on employee selection. However,I first describe two other mechanisms here to provide a more completepicture of the research setting.

First, and consistent with literature in both accounting and economics,the use of subjective performance evaluation is relied on extensively(Baker, Gibbons, and Murphy [1994], Ittner, Larcker, and Meyer [2003],Gibbs et al. [2004]). Each of the organization’s business unit “lead-ers” is accountable for ranking the performance of individuals on theirteam. Subjective performance rankings of employees are based on fac-tors such as how well they were making decisions on behalf of mem-bers rather than focusing on policy or procedure and on how wellthey could articulate the rationales for their decisions. Based on this as-sessment, employees are assigned a performance rating ranging from“A+” to “C.” Each business unit leader is then assigned a bonus poolbased on the size and overall performance of his team during that year.Each leader then allocates a dollar amount to each employee basedon the performance ranking. Subjective performance evaluation of thistype has been in place throughout the implementation of the newsystem.4

Second, there is extensive reliance in this organization on norms andshared values to guide employee behavior (Ouchi [1979], Van den Steen[2010]). Norms for decision-making have evolved at this organization viaat least three mechanisms. The first, as discussed earlier, is the articulationof the “MOE” decision-framework. It is worth noting that, at least by 2009,employees seem to have developed a relatively nuanced and sophisticatedinterpretation of how to apply the MOE decision-filter. Qualitative evidenceof this can be seen in appendix A, where I have provided a random sampleof responses to a question on a survey conducted by the organization acrossits entire employee base.

The question, designed to elicit employees’ understanding of the extentof their decision-making authority as well as its proper application, wasposed as follows: “An employee comes to you with a member situation that,if the decision is made to go ahead with the request, will require working‘outside the box.’ What advice would give the employee on decision makingand execution?” Consistent with the development of norms, the answers tothis question reveal several common elements across employees as follows:

4 In unreported tests, I examined these subjective ratings to test for implicit incentives thatmight influence employee decisions. I find no evidence of such implicit incentives. The like-lihood of a lower rating shows no significant relationship to any of my measures of employeeuse of decision-making authority.

EMPLOYEE SELECTION AS A CONTROL SYSTEM 9

(1) Employees by and large view very few, if any, limits on the decisionsthey can make on behalf of members. (2) Employees do not tend to inter-pret the MOE framework naively. Rather than doing whatever the memberasks for, employees carefully deliberate whether a course of action is in thelong-run best interest of the member and believe that doing so will also bein the long-run best interest of the organization. (3) Employees appear tohold themselves accountable for following up with decisions after they aremade, both in the short and long-term, to ensure the desired outcome forboth the member and the organization.

The second mechanism for norm development is straightforward. Basedon my own interviews and direct observation of work at this organization,employees interact extensively with each other when faced with significantexceptions—both to elicit the views of others who have made such excep-tions in the past as well as to sharpen their own rationale for making or notmaking the exception.

The third mechanism for norm development is due to what is referredto internally as a “detection control” model, which functions by allowingemployees to deviate from formal guidelines, but requires them to explainand document their decisions when they do so. One executive captured theworkings of this control system as follows:

We flag loans that are outside of our lending guidelines. If there is a rateexception, then the employee should log the explanation in [our inter-nal IT system]. If they don’t, we will have a discussion with the managerto make sure the documentation is in the system going forward. If theyput the explanation in [the system], then we don’t review the exceptionfurther.

Importantly, this process emphasizes enforcing the documentation ofemployee rationales for deviation from guidelines rather than monitor-ing the outcomes of individual decisions. This was a deliberate choice un-der the assumption that questioning individual outcomes would effectivelyeliminate willingness to exercise decision-making authority.5 The systemdoes, however, maintain a record of the full history of employee explana-tions for any lending or other decisions that deviate from formal guidelines.In this way, the system facilitates the development of norms by maintainingan archive of past rationales that any employee facing the choice to makean exception can access to see how similar decisions have been handled inthe past.

Although this control system does not punish or reward employeesfor loan outcomes, top management does monitor trends in excep-tion rates over time for risk management purposes. An internal risk

5 This assumption is consistent with the literature on “psychological safety” in organizations(Edmondson [1999]) as well as studies on employee behavior under different monitoringregimes (Campbell, Epstein, Martinez-Jerez [2011]).

10 D. CAMPBELL

management committee conducts periodic reviews to identify trends foremployees with severe deviations in either the rate or magnitude of theirexceptions. In these instances, mentorship and coaching are used to instilldecision-making norms that are more aligned with the overall risk toleranceof the organization.

In short, the organization uses a variety of mechanisms to motivate theeffective use of decision-making authority, all of which are consistent withpractices that prior literature would predict to find in organizations whereit is difficult to measure and contract on outcomes. Similarly, and most im-portantly from the perspective of this paper, this organization has increas-ingly relied on employee selection.

3.3 EMPLOYEE SELECTION

The employee selection process at this organization mirrors its basic in-centive alignment problem of motivating employees to use decision-makingauthority and to do so effectively. In particular, the organization has activelysought to select employees with particular attributes that are indicative ofunderlying preferences for these objectives.

In my own interviews with executives and employees, a primary attributethat surfaced as important could best be described as “empathy.” Variouslydescribed in terms such as “a desire to help others” and “wants to makean impact on others,” this attribute is clearly seen as an indicator for apotential employee’s desire to make decisions on behalf of members. Giventhe high degree of decentralization in the new system, other attributes thatare viewed as important are confidence in decision-making, willingness totake ownership and accept accountability, willingness to take risk, and adesire to learn.6 The organization’s interview process naturally attemptsto screen on these attributes. Typical interview questions include “If ourcomputer system was down and a member walked in and asked you for $500in cash for the trip they were leaving on the very next day, how would youmake that decision?”; “How do you want to be remembered by coworkersand by customers?”; and “How have you changed as an employee in thepast couple of positions that you’ve held?”

Considerable emphasis is also placed on screening new hires once in theorganization to quickly identify those who are overconfident or otherwiselikely to be poor fits with the new system. Particular attention is paid toemployees hired from other financial institutions to determine their abilityto change and adapt to the environment of the new system. Commentingon this mechanism, one senior executive noted: “All new employees areassigned a mentor who they work closely with in decision-making duringthe first few months of their employment. Mentors can and have quicklyidentified employees whose behavior does not respond to coaching andmentoring.”

6 Appendix B provides qualitative evidence on employee perceptions of the importance ofthese attributes.

EMPLOYEE SELECTION AS A CONTROL SYSTEM 11

3.4 MEASURING ALIGNMENT OF EMPLOYEE PREFERENCES WITHORGANIZATIONAL OBJECTIVES

A feature of this organization that I exploit in my empirical tests is thatemployees are selected via different channels—some of which are morelikely than others to sort on the alignment of their preferences with or-ganizational objectives. Many employees in the new system are continuingemployees that were initially hired into the old system. The system thatthese employees were selected into is an almost polar opposite manage-ment control environment, and they were screened based on very differ-ent attributes from those considered important in the new system, such asprior experience in financial services. Under the new system, the executiveteam had come to believe that past experience in another financial institu-tion could be detrimental for a candidate attempting to transition to theirmodel. Consistently, the organization recruited new employees from areasas diverse as health care, retail, and education. The implicit assumptionis that employees selected from traditional financial services organizationswill be too influenced by their own previous experience and the controlstructures in which they operated.

For all intents and purposes, employees hired prior to year-end 2004(“old system employees”) were initially selected into a traditional financialservices organization with policy and procedure-oriented controls. Relativeto employees that are hired into the new system, I expect that old systememployees will have preferences that are less aligned with the organization’sobjectives. This is, of course, tempered by the fact that these employeeschose to remain in the new system. However, the fact that an employee washired into the old system should be a reasonable indirect observable in-dicator that his or her preferences are relatively less aligned than those ofemployees directly hired into the new system (“new system employees”).7

There are also several relevant distinctions among new system employees.Some are referred into the organization by existing employees and somecome through the normal screening process without referral. Further, ofthose that are referred, the source of referral can be either an old or newsystem employee. If new system employees generally have preferences thatare more aligned than those of old system employees, then I expect this toextend to referrals as well. Among new system employees, those referred byother new system employees should be most aligned, those referred by oldsystem employees should be least aligned, and employees who are screenedwithout referral are likely to fall in between. Old system employees may alsohave been referred by other employees when hired into the old system. To

7 This is consistent with Van den Steen’s [2010] economic model of culture as shared beliefsin the context of mergers. Predictions from his model suggest the use of a person’s premergerfirm as an indirect, but observable, indicator of his or her beliefs. To the extent that thosewho select or are selected to stay have preferences that are relatively well-aligned with orga-nizational objectives under the “new system,” this should bias against my ability to identifyempirical differences in employee decision-making patterns.

12 D. CAMPBELL

T A B L E 1Retained Versus Exited Employees in the Old System

Mean Hourly Salary Levels by:

Salary Type Job Title

Financial Member “Leader”All Services Service Performance

Employees Annual Hourly Officer Rep. Rating

Stayed $18.80 $32.40 $16.20 $17.86 $15.86 4.56Left 17.28∗ 28.59 15.50∗∗ 14.74∗∗∗ 12.64∗∗∗ 4.31∗∗∗

Columns 1–5 show average salary levels for employees who stayed and those who left the organization asof year-end 2004 (the final year of the “old system”). The final column shows the average performance ratingof the organization’s “Leaders” (executive level employees) as of year-end 2004. The performance ratingranges from 1 to 5 and was intended to be a measure of the degree to which each leader was likely to fit withthe culture of the “new system.” ∗, ∗∗, and ∗∗∗ denote significant difference in means between employees whostayed and those who left within the same employee category at the 10%, 5%, and 1% levels, respectively.For comparison purposes, pay levels for employees paid on an annual basis are expressed on an hourlybasis, assuming eight working hours per day and 264 working days per year. Pay levels for hourly employeescapture the actual hourly wage rate. Financial Services Officers and Member Services Representatives arethe two job titles that had the largest numbers of employees as of year-end 2004.

the extent that this led to the strongest sorting of employees who “fit” withthe old system, I expect such employees to have the least aligned prefer-ences with the new system.

It is worth considering that if old system employees who remain in thenew system are concentrated among those with lower ability—as might beexpected if they have weaker outside opportunities for instance—the struc-ture that the employee was hired into may serve as an indirect indicator ofgeneral skill levels rather than alignment of his or her preferences with theorganization’s objectives. However, table 1 provides evidence that this is notthe case. The table demonstrates that employees who exited the organiza-tion during the final year of the old system tended to be those with loweraverage wages, suggesting that they are not per se higher skilled or moretalented on average than their counterparts who stayed. This remains trueeven within the two largest job categories at year-end 2004—Member Ser-vices Representative and Financial Services Officer. Similarly, the final col-umn of table 1 demonstrates that performance ratings for executive levelemployees (“Leaders”) who left by year-end 2004 are on average lower thanratings for those who stayed.

Figure 1 illustrates some salient facts about the evolution of the em-ployee selection model at this organization. As of 2005, the first full yearof implementation of the new system, those hired directly into this systemalready account for fully 40% of all employees. This pattern is consistentwith a perceived need for a different “type” of employee in the new system.It also indicates significant underlying turnover of old system employeesas the organization transitioned to the new system. Consistent with differ-ent preferences under the old system, interviews with executives and otheremployees suggest that approximately half of this turnover was voluntaryand due to the discomfort of many old system employees with the level ofdecision-making authority inherent in the new system. The remaining

EMPLOYEE SELECTION AS A CONTROL SYSTEM 13

FIG. 1.—Evolution of employee selection model.

turnover was involuntary as senior management used both formal evalu-ations and informal observation to terminate relationships with employeesthey determined to be least likely to fit well in the new decentralized struc-ture. Figure 1 also shows that the percentage of referred employees risesfrom just over 30% to just over 40% during this period. Relevant, but notshown in figure 1, is the fact that by the end of 2009 over 50% of new em-ployees were referred by existing employees. These patterns demonstrateincreasing reliance on this recruitment channel and are consistent with theliterature on employee referrals as a high-quality source of information formatching potential employees to internal labor markets.

In summary, employee selection has played an increasing role at this or-ganization as a mechanism for aligning employee preferences with organi-zational objectives. I expect such alignment to vary systematically with thechannel of employee selection with the ordering from strongest to weak-est alignment as follows: (1) new system employees referred by new systememployees, (2) new system employees who are not referred, (3) new sys-tem employees referred by old system employees, (4) old system employeeswho are not referred, and (5) old system employees referred by old systememployees. If employee selection is an effective solution to the incentivealignment problem, then I expect to see more use of decision-making au-thority, and stronger resulting performance outcomes, in moving from thefifth category of employee to the first.

3.5 THE LENDING DECISION CONTEXT

While decision-making authority under the new system extends to a widerange of decisions that employees might make on behalf of members, I

14 D. CAMPBELL

focus on lending decisions in my analysis. Lending decisions have signif-icant research advantages over other types of decisions for two reasons.First, employee use of decision-making authority is directly observable inthis context and might include, for example, giving a member a loan whenhe does not meet formal credit-score guidelines. Second, and similarly,performance outcomes of these decisions are eventually observable in theform of default and charge-off rates. Lending decisions are also significantin this industry and represent one of the areas in which this organizationwas most impacted by the change to the new system.

Although the context of lending decisions provides several advantagesfor this study, it is worth noting that incentive contracts could technicallybe written on future default rates. However, holding lower level employ-ees accountable for long-term outcomes over which they have little controloutside of the initial risk assessment would expose them to a substantialamount of risk, potentially making them less willing to use decision-makingauthority irrespective of their judgment about the true quality of a loan.

This challenge has been articulated as a major barrier to contractingon outcomes in the context of bank lending, and studies that have beenconducted in this context point to the exceeding rarity of this practicewith typical incentive contracts based on loan originations rather than out-comes (Baker [2002], Agarwal and Wang [2008], Liberti and Mian [2009],Hertzberg, Liberti, and Paravisini [2010]). Irrespective of particular viewson the feasibility of contracting on loan outcomes, the most relevant factis that this organization does not do so, giving rise to a control problemthat must be addressed via other mechanisms. My primary analyses exam-ine whether this can be accomplished via employee selection.

3.6 DATA

The data used for this study are collected from the organization’s person-nel and lending files during the period January 2005–May 2010. The sam-ple used for subsequent analyses consists of observations on loan, borrower,and employee characteristics for 134,121 unique loans, made to 64,540unique borrowers, by 463 unique employees during this period. Summarystatistics are provided in table 2.

3.6.1. Employee Characteristics. Data on employee characteristics includethe employee’s year of hire into the organization, his job title, and the busi-ness unit in which he works.8 Both job title and business unit may vary byyear. For employees who were referred into the organization, I observe theidentity and year of hire of the employee’s referrer. I use employee and re-ferrer hire years to classify employees into the five categories noted earlier,defining new system employees and referrers as those hired after 2004 and

8 For purposes of this study, a business unit can be a branch, a function such as financialaccounting or real estate, or corporate headquarters.

EMPLOYEE SELECTION AS A CONTROL SYSTEM 15

TA

BL

E2

Sum

mar

ySt

atis

tics

for

Empl

oyee

,Bor

row

er,an

dL

oan

Cha

ract

eris

tics

Sam

ple

Size

and

Vari

able

sU

nit

ofA

nal

ysis

Mea

nM

edia

nSt

d.D

ev.

Min

Max

Em

ploy

eeC

har

acte

rist

ics

Num

ber

Uni

que

Empl

oyee

sN

ewsy

stem

empl

oyee

,ref

erre

dby

new

syst

emem

ploy

ee46

30.

080

0.27

01

New

syst

emem

ploy

ee,n

otre

ferr

ed46

30.

270

0.45

01

New

syst

emem

ploy

ee,r

efer

red

byol

dsy

stem

empl

oyee

463

0.13

00.

330

1O

ldsy

stem

empl

oyee

,not

refe

rred

463

0.36

00.

480

1O

ldsy

stem

empl

oyee

,ref

erre

dby

old

syst

emem

ploy

ee46

30.

160

0.37

01

Ten

ure

inor

gan

izat

ion

(yea

rs)

463

4.21

34.

750

32B

orro

wer

Ch

arac

teri

stic

sN

umbe

rU

niqu

eB

orro

wer

sC

redi

tsco

re64

,540

710

720

74.5

939

383

6D

ebt-t

o-in

com

era

tio

64,5

4037

.92

34.9

421

.86

020

0L

oan

Ch

arac

teri

stic

sN

umbe

rU

niqu

eL

oans

Loa

nam

oun

t13

4,12

113

,519

9,00

018

,865

252,

371,

200

Inte

rest

rate

134,

121

8.93

8.10

4.06

326

Term

inm

onth

s13

4,12

169

6036

040

6A

ppro

ved

loan

has

acr

edit

-sco

reex

cept

ion

134,

121

0.13

00.

330

1A

ppro

ved

loan

has

anin

tere

stra

teex

cept

ion

134,

121

0.24

00.

420

1L

oan

appl

icat

ion

appr

oved

wh

ensy

stem

rule

wou

ldde

ny

(200

7on

ly)

13,6

370.

731

0.35

01

Prio

rle

ndi

ng

expe

rien

ceof

empl

oyee

upto

curr

entl

oan

(#pa

stlo

ans

mad

eby

empl

oyee

)13

4,12

136

0.71

254

341.

450

1,75

2

Prio

rcu

stom

er-s

peci

fic

len

din

gex

peri

ence

ofem

ploy

eeup

tocu

rren

tloa

n(#

past

loan

sm

ade

byem

ploy

eeto

asp

ecifi

ccu

stom

er)

134,

121

1.35

00.

920

20

“New

Syst

em”

den

otes

empl

oyee

sh

ired

afte

rth

eor

gan

izat

ion

’sim

plem

enta

tion

ofit

sde

cen

tral

ized

busi

nes

sm

odel

(pos

t-200

4).

“Old

Syst

em”

den

otes

empl

oyee

sh

ired

prio

rto

the

orga

niz

atio

n’s

impl

emen

tati

onof

its

dece

ntr

aliz

edbu

sin

ess

mod

el(2

004

and

earl

ier)

.Su

mm

ary

stat

isti

csfo

rem

ploy

eech

arac

teri

stic

sar

eba

sed

onth

epo

oled

sam

ple

ofem

ploy

ee-y

ears

from

2005

to20

09;s

umm

ary

stat

isti

csfo

rbo

rrow

erch

arac

teri

stic

sar

eba

sed

onth

efu

llsa

mpl

eof

134,

121

loan

s.T

he

min

imum

loan

term

of0

isdu

eto

the

pres

ence

ofre

volv

ing

cred

itlin

essu

chas

cred

itca

rds

and

hom

eeq

uity

lines

ofcr

edit

.

16 D. CAMPBELL

T A B L E 3Summary Statistics and Distribution of Loans by Type

Loan Type Percent of All Loans Amount Interest Rate % Term

Secured vehicle 49 $13,278 6.88 61.24Personal line of credit 37 4,498 12.72 59.90Mortgage and home equity 14 36,654 6.39 114.72

This table reports distribution of loans along with means of selected variables by loan type. Summarystatistics are based on the full sample of 134,121 loans. Term is measured in months.

old system employees and referrers as those hired prior to and including2004.

There are 214 unique job titles in the data, but many of these are redun-dant. For analysis purposes, I broadly categorize employees as “customercontact” or “corporate and back office” based on job titles and their de-scriptions. Customer-contact employees are those whose jobs put them incontact with customers in the regular course of work including, for exam-ple, employees working in branches and call centers. Corporate and back-office employees largely consist of those working in executive or functionalareas at corporate headquarters or business units other than branches orcall centers.

While relatively broad, this is a good categorization for a variety of rea-sons. First, consistent with the decentralization of decision-making author-ity, every employee was expected to be capable of handling all transactionsso that differences in job tasks do not necessarily track well with differencesin job titles in the new system. This is especially true of customer-facing em-ployees operating in branches and call centers as they handle the majorityof transaction activity. Second, and in recognition of this fact, by 2008 theorganization had itself classified all customer-contact employees into onejob title called “Member Service Representative.” Finally, customer-contactemployees operate at the lowest level of the organizational hierarchy. Thesignificant decentralization of decision-making authority even to lower lev-els in the organization is perhaps the most unique aspect of the new sys-tem, and it is reasonable to expect employee selection to have its strongestpotential effects on management control and incentive alignment at thislevel.

3.6.2. Borrower Characteristics. Data on borrower characteristics includethe borrower’s credit score and debt-to-income ratio at the time his loanapplication is processed.

3.6.3. Loan Characteristics. For each loan made during 2005–2010, I ob-serve the type, dollar amount, interest rate, and term at the time the loanwas funded. There are three broad categories of loans in the data: securedvehicle loans, used primarily for automobile purchases; personal lines ofcredit, including credit cards and signature loans; and mortgages and homeequity loans. The distribution of loans and their characteristics by type areprovided in table 3. In addition to these basic characteristics, I also observe

EMPLOYEE SELECTION AS A CONTROL SYSTEM 17

loan exceptions that are direct indicators for whether an employee exer-cised decision-making authority in a particular lending decision. The twobasic types of lending exceptions are those made in approving, and thosemade in funding, a loan.

Loan approval exceptions occur when an employee overrides the orga-nization’s system-based guidelines in approving a potential borrower for aloan. In general, in the absence of decentralized decision-making author-ity at this organization, borrowers with either credit scores less than 620or debt-to-income ratios above 45% would not qualify for approval. Thebenchmark of denying a loan to a borrower that falls short of either ofthese criteria serves as the counterfactual for what the lending decisionwould be in the absence of decision-making authority. This serves as a usefulbenchmark for examining variation in the use and outcomes of decision-making authority across employees. Throughout this paper, I use the term“system-deny” to denote loans that would have been denied in the absenceof decision-making authority.

I observe loan approval exceptions in the data in two different ways. First,for every loan that was approved over the sample period, I can observewhether it is a “system-deny” loan. That is, whether it is a loan for whicha credit-score exception, debt ratio exception, or both were made. This al-lows me to examine whether these types of loans are systematically moreor less concentrated among different types of employees. In essence, thesedata allow me to examine the probability that a system-deny loan would beobserved conditional on having been approved by a particular employee. Aclear drawback of this measure is that it is a joint probability of a system-deny borrower requesting a loan from the employee and the employeemaking the exception to approve the loan conditional on that request. Thefocus of this study is on the latter, and in some of my tests I will attempt todeal with this issue by controlling for factors that would make it more likelyfor an employee to interact with riskier borrowers.

I also address this issue via the second way in which I observe loan ap-proval exceptions. For the period 2006–2009, I was able to obtain data onall applications from potential borrowers who were denied for loans. Thedata on which specific employees made the denial decision are only avail-able for 2007, so most of my analyses of this particular data are restrictedto this year. While only for a limited portion of my sample period, this typeof data is not typically available in studies on lending decisions, and it al-lows me to directly estimate the probability of an employee approving aloan conditional on the potential borrower not meeting system criteria forapproval.

The second type of loan exceptions—those made in the structuringof approved loans—is relatively more straightforward. These consist pri-marily of rate exceptions occurring when employees structure the loanwith a different rate than is recommended on the “rate sheet” for a loanwith similar characteristics. In the vast majority of cases, though not all,the actual interest rate is lower than the rate-sheet rate, consistent with

18 D. CAMPBELL

employees using decision-making authority largely to reduce rates offeredto members.

As additional controls in my analysis of lending decisions, I constructtwo measures of lending experience in the new system. First, I measure theemployee’s general prior experience with lending decisions in the new sys-tem as the cumulative number of loans made by the employee up to andexcluding the current loan. Second, I measure the employee’s experiencelending to a specific member as the number of prior loans made by theemployee to that member. The cumulative number of loans in both cases ismeasured from January 2005 or from the employee’s hire date, whicheveris later. I include these measures as controls for any potential learning ef-fects over time and because employees who repeatedly interact with specificmembers could reasonably be expected to have better “local information”on the member’s creditworthiness independent of the characteristics of theemployee.

3.6.4. Loan Performance Outcomes. I am able to observe whether an out-standing loan is charged off between January 2008 and May 2010. A charge-off occurs when a loan is written off as uncollectible and is clearly the mostextreme outcome of a poor performing loan. It would be ideal to have in-termediate outcomes such as defaults on payments, but I do not observesuch outcomes in these data. Although the performance outcome is rela-tively extreme, these data allow for direct tests of the performance implica-tions of employee use of decision-making authority in lending decisions.

4. Empirical Tests and Results

4.1 DESCRIPTIVE STATISTICS ON THE USE OF DECISION-MAKING AUTHORITY

Before turning to my primary empirical tests, I first examine severalpatterns in the data that illustrate the nature of employee lending deci-sions. Data in table 2 and figures 2–4 provide strong evidence that decision-making authority is “real” rather than simply formal or perceived.9 Table 2shows that 13% of all loans during 2005–2010 were made with credit-scoreexceptions, 24% were structured with interest rate exceptions, and fully73% of loan applications from “system-deny” borrowers were approved in2007.

Figure 2 demonstrates that decision-making authority is also highlydispersed. With the exception of 2008, a year in which overall loanapplications declined, every employee made at least one lending deci-sion and this remained at approximately 90% of all employees even in

9 I use these terms in the sense of Aghion and Tirole [1997]. Real authority would be lim-ited if employees perceived the threat of implicit punishments from superiors’ monitoring oftheir use of formal authority.

EMPLOYEE SELECTION AS A CONTROL SYSTEM 19

FIG. 2.—Concentration of loan decisions over time.

FIG. 3.—Distribution of number of loans per employee per year.

2008.10 Moreover, the top 20% of employees in terms of loan volume ina given year account for less than 60% of all lending decisions. Lendingactivity would have been highly concentrated in few employees in the old

10 “Back office” employees get opportunities to make loans due to an IT system that routesany “overflow” calls in its call centers randomly throughout the organization. Any employeecan receive a randomly routed call from a member regarding lending or other transactionsand is expected to handle the transaction.

20 D. CAMPBELL

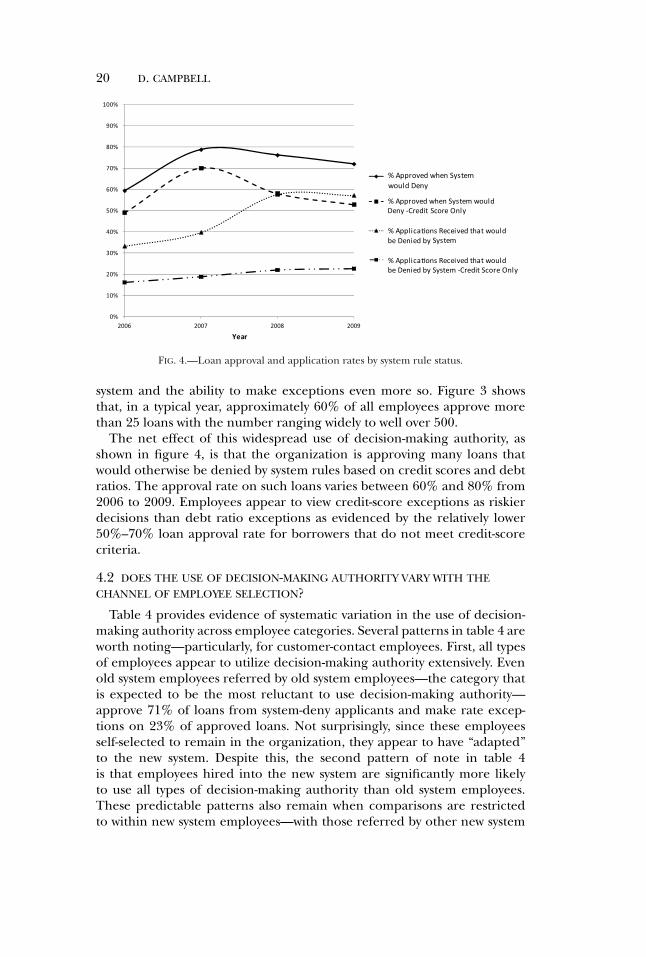

FIG. 4.—Loan approval and application rates by system rule status.

system and the ability to make exceptions even more so. Figure 3 showsthat, in a typical year, approximately 60% of all employees approve morethan 25 loans with the number ranging widely to well over 500.

The net effect of this widespread use of decision-making authority, asshown in figure 4, is that the organization is approving many loans thatwould otherwise be denied by system rules based on credit scores and debtratios. The approval rate on such loans varies between 60% and 80% from2006 to 2009. Employees appear to view credit-score exceptions as riskierdecisions than debt ratio exceptions as evidenced by the relatively lower50%–70% loan approval rate for borrowers that do not meet credit-scorecriteria.

4.2 DOES THE USE OF DECISION-MAKING AUTHORITY VARY WITH THECHANNEL OF EMPLOYEE SELECTION?

Table 4 provides evidence of systematic variation in the use of decision-making authority across employee categories. Several patterns in table 4 areworth noting—particularly, for customer-contact employees. First, all typesof employees appear to utilize decision-making authority extensively. Evenold system employees referred by old system employees—the category thatis expected to be the most reluctant to use decision-making authority—approve 71% of loans from system-deny applicants and make rate excep-tions on 23% of approved loans. Not surprisingly, since these employeesself-selected to remain in the organization, they appear to have “adapted”to the new system. Despite this, the second pattern of note in table 4is that employees hired into the new system are significantly more likelyto use all types of decision-making authority than old system employees.These predictable patterns also remain when comparisons are restrictedto within new system employees—with those referred by other new system

EMPLOYEE SELECTION AS A CONTROL SYSTEM 21

TA

BL

E4

Use

ofD

ecis

ion-

Mak

ing

Aut

hori

tyby

Empl

oyee

Cat

egor

y

Em

ploy

eeC

ateg

ory

Old

Syst

emN

ewSy

stem

New

Syst

emR

efer

red

byO

ldSy

stem

Ref

erre

dby

New

Syst

emR

efer

red

byO

ldSy

stem

Not

Ref

erre

dO

ldSy

stem

Not

Ref

erre

dN

ewSy

stem

Cus

tom

er-C

onta

ctE

mpl

oyee

sN

umbe

rof

uniq

ueem

ploy

ees

2171

3910

146

%lo

ans

wit

hcr

edit

-sco

reex

cept

ion

s11

1115

a,b

16a,

b23

a,b,

c,d

2007

appr

oval

rate

for

syst

emde

nie

dap

plic

ants

7175

a76

a77

a,b

82a,

b,c,

d

%lo

ans

wit

hin

tere

stra

teex

cept

ion

s23

2225

a,b

26a,

b,c

29a,

b,c,

d

Cor

pora

tean

dB

ack

Offi

ceE

mpl

oyee

sN

umbe

rof

uniq

ueem

ploy

ees

4173

2240

9%

loan

sw

ith

cred

it-s

core

exce

ptio

ns

810

a11

a17

a,b,

c15

a,b,

c

2007

appr

oval

rate

for

syst

emde

nie

dap

plic

ants

5457

5981

a,b,

c77

a,b,

c

%lo

ans

wit

hin

tere

stra

teex

cept

ion

s18

23a

2026

a,b,

c21

a,d

“New

Syst

em”

den

otes

empl

oyee

sh

ired

afte

rth

eor

gan

izat

ion

’sim

plem

enta

tion

ofit

sde

cen

tral

ized

busi

nes

sm

odel

(pos

t-200

4).

“Old

Syst

em”

den

otes

empl

oyee

sh

ired

prio

rto

the

orga

niz

atio

n’s

impl

emen

tati

onof

its

dece

ntr

aliz

edbu

sin

ess

mod

el(2

004

and

earl

ier)

.%lo

ans

wit

hcr

edit

scor

ean

din

tere

stra

teex

cept

ion

sar

eba

sed

onth

efu

llsa

mpl

eof

134,

121

appr

oved

loan

s.“S

yste

mD

enie

d”re

fers

tolo

anap

plic

atio

ns

from

appl

ican

tsw

ith

cred

itsc

ores

less

than

620

orde

bt-to

-inco

me

rati

osgr

eate

rth

an45

%or

both

.App

rova

lra

tes

for

syst

emde

nie

dlo

ans

are

base

don

lyon

loan

appl

icat

ion

sre

ceiv

eddu

rin

g20

07.

a,b,

c,an

dd

den

ote

sign

ifica

ntl

ydi

ffer

ent

from

old

syst

em/r

efer

red

byol

dsy

stem

,ol

dsy

stem

/non

refe

rred

,new

syst

em/r

efer

red

byol

dsy

stem

,an

dn

ewsy

stem

/non

refe

rred

empl

oyee

sre

spec

tive

ly,a

tlea

stat

the

10%

leve

lbas

edon

two-

sam

ple

test

sof

prop

orti

on.

22 D. CAMPBELL

T A B L E 5Loan Exception Logits

Credit Score Credit Score Approve | InterestException | Exception | System Would RateApproved Approved Deny (2007) Exception

Panel A: Customer-contact employees

Prior lending experience −0.0002 −0.0002 0.0009 −0.0001(0.0004) (0.0004) (0.0006) (0.00007)

Prior customer-specific 0.059∗∗∗ 0.061∗∗∗ 0.24∗∗ 0.044∗∗∗

lending experience (0.01) (0.01) (0.10) (0.01)Prior year average credit score for −0.009∗∗∗

loans made at business unit (0.00)Credit grade A+ 1.667∗∗∗ −0.503∗∗∗

(0.25) (0.03)Credit grade A 0.487∗∗ 0.02

(0.22) (0.04)Credit grade C −1.018∗∗∗ 0.340∗∗∗

(0.21) (0.04)Credit grade D −1.949∗∗∗ 1.317∗∗∗

(0.18) (0.03)Debt-to-income ratio −0.023∗∗∗ 0.00001∗∗∗

(0.002) (0.000004)Loan amount ($000’s) −0.05∗∗∗ −0.05∗∗∗ −0.018∗∗ 0.01∗∗∗

(0.005) (0.006) (0.007) (0.001)Old system employee, 0.035 0.031 0.262∗∗ −0.038

not referred (0.04) (0.04) (0.13) (0.03)New system employee referred 0.105∗,b 0.127∗∗,b 0.391∗∗ 0.080∗,b,c

by old system employee (0.06) (0.06) (0.17) (0.04)New system employee, 0.143∗∗∗,b 0.131∗∗∗,b 0.502∗∗∗,b −0.052

not referred (0.05) (0.05) (0.13) (0.03)New system employee referred 0.385∗∗∗,b,c,d 0.326∗∗∗,b,c,d 1.776∗∗∗,b,c,d 0.104∗,b,c

by new system employee (0.07) (0.07) (0.42) (0.06)Constant −0.727∗∗∗ 5.688∗∗∗ 20.344 −3.218∗∗∗

(0.19) (0.44) (0.35) (0.14)Observations 112,997 93,751 10,052 112,997

(Continued)

employees showing significantly higher loan exception rates across all ex-ception types.

Some of these general patterns remain for corporate and back office em-ployees, particularly the comparisons between old and new system employ-ees. However, there is little distinction in the use of decision-making au-thority across loan exception types for new system employees who are notreferred when compared to those who are referred by other new systememployees. As noted earlier, it is reasonable to expect employee selectionto have stronger effects in this setting among customer-contact employees,but these weaker patterns may also be due to smaller sample sizes of em-ployees or loans within the corporate and back office employee group.

The patterns documented in table 4 largely remain when lending de-cisions are subjected to a multivariate analysis controlling for factorsother than employee characteristics that are expected to influence thesedecisions. Table 5, panel A, reports estimates from logit models for the

EMPLOYEE SELECTION AS A CONTROL SYSTEM 23

T A B L E 5 — Continued

Credit Score Credit Score Approve | InterestException | Exception | System Would RateApproved Approved Deny (2007) Exception

Panel B: Corporate and back office employees

Prior lending experience −0.0006∗∗ −0.0006∗∗ 0.002 −0.0003(0.0003) (0.0003) (0.0017) (0.0002)

Prior customer-specific 0.02 0.03 −0.72 0.089∗∗∗

lending experience (0.03) (0.03) (0.59) (0.02)Prior year average credit score −0.008∗∗∗

for loans made at business unit (0.00)Credit grade A+ 1.061∗∗∗ −0.670∗∗∗

(0.34) (0.06)Credit grade A 0.841∗∗ 0.025

(0.35) (0.09)Credit grade C −1.549∗∗∗ 0.204∗∗

(0.35) (0.10)Credit grade D −2.723∗∗∗ 1.051∗∗∗

(0.30) (0.08)Debt-to-income ratio −0.031∗∗∗ 0.000003∗∗∗

(0.004) (0.000001)Loan amount ($000’s) −0.03 −0.03 −0.004 0.003∗∗∗

(0.008) (0.008) (0.17) (0.00)Old system employee, 0.288∗∗∗ 0.236∗∗ 0.158 0.096

not referred (0.11) (0.11) (0.22) (0.07)New system employee referred 0.166 0.169 0.725∗∗ −0.125

by old system employee (0.18) (0.18) (0.29) (0.14)New system employee, 0.510∗∗∗ 0.462∗∗∗ 0.058 0.061

not referred (0.14) (0.14) (0.54) (0.09)New system employee referred 0.629∗∗∗ 0.570∗∗∗ 0.444 −0.382∗∗∗

by new system employee (0.18) (0.18) (0.78) (0.13)Constant 0.222 4.332∗∗∗ 25.328∗∗∗ −3.104∗∗∗

(1.28) (1.50) (1.53) (0.29)Observations 21,124 17,526 3,585 21,124

Standard errors in parentheses corrected for clustering within employees. ∗,∗∗, and ∗∗∗ significant at10%, 5%, and 1% levels, respectively. b,c, and d denote significantly different from old system/nonreferred,new system/referred by old system, and new system/nonreferred employees, respectively, at least at the 10%level based on chi-square tests; business unit, year, and loan type indicators included in all specifications.“New System” denotes employees hired after the organization’s implementation of its decentralized busi-ness model (post-2004). “Old System” denotes employees hired prior to the organization’s implementationof its decentralized business model (2004 and earlier). “System Denied” refers to loan applications fromapplicants with credit scores less than 620 or debt-to-income ratios greater than 45% or both. The depen-dent variable in the column labeled “Credit-Score Exception | Approved” is an indicator for whether anapproved loan is one for which a credit-score exception was made in the approval process. The dependentvariable in the column labeled “Approve | System would Deny” is an indicator for whether a loan appli-cation is approved when the system rule based on credit score and debt-to-income ratio would deny theloan. Approval rates for system denied loans are based only on loan applications received during 2007. Thedependent variable in the column labeled “Interest Rate Exception” is an indicator for whether the actualinterest rate is different from the organization’s standard interest rate given the characteristics of the loanand borrower. The excluded category for “Credit Grade” is “B” in all specifications. All models include fixedeffects for loan type, business unit, and year.

different categories of lending exceptions for the sample of customer-contact employees. The excluded category in each model is old systemreferred by old system employees. To control for unobserved heterogene-ity, all models include fixed effects for loan type, business unit, and year.

24 D. CAMPBELL

Reported standard errors are corrected for clustering of observationswithin employees prior to inference.

The first column contains results for the model predicting the probabilityof an approved loan being one for which a credit-score exception was made.The results demonstrate that loans with these exceptions are more likely tobe observed if the employee making the decision has had prior lendingexperience with the borrower, and are less likely for larger loans. Moreimportantly, the predicted patterns in the use of decision-making author-ity across employees remain: conditional rates of credit-score exceptionsare higher for new versus old system employees generally, with the highestrates demonstrated for new system employees referred by other new systememployees.

These results may be confounded if some employee groups are system-atically more likely than others to interact with riskier borrowers. This mayarise if different types of employees are concentrated in particular businessunits due to the hiring preferences of the manager, the local labor market,prior turnover or other factors, and if there are systematic differences inthe types of borrowers that interact with particular business units. By in-cluding business unit fixed effects, I partially control for these potentialconfounding factors. However, the types of borrowers interacting with busi-ness units may change over time. To account for this, the second column inpanel A of table 5 includes the average credit score of borrowers with loansoriginated at the business unit in the prior year. Not surprisingly, increasesin the average credit quality of borrowers interacting with a business unitare negatively associated with the likelihood of observing a loan with anexception. More importantly, the results on differences in conditional ex-ception rates across employee categories are robust to the inclusion of thismeasure.

The results in the first two columns of table 5, panel A, demonstrate thatloans with credit-score exceptions are more likely to be observed amongnew system employees, particularly those referred by other new system em-ployees. The next column shows the flip-side of this, the probability thatthese employees will accept a loan from a borrower who does not meetsystem criteria. In these tests, I control directly for characteristics of theborrower by including the debt-to-income ratio and “credit grade.”11 Thecredit grade, used internally as a way to classify risk, ranges from “A+” to“D.” Cutoff values of credit score are used to grade each borrower, withgrades “C” and “D” consisting of borrowers with scores lower than the sys-tem criteria of 620. I use the credit grade rather than the score in recog-nition of the inherent nonlinearity in credit-score-based lending decisions.The excluded credit grade in these specifications is “B.” Not surprisingly,the results show that employees are more likely to approve loans of lower

11 Variation in credit scores and debt ratios arises in this sample because the system rulewould deny applicants with either credit scores < 620 or debt ratios > 45%.

EMPLOYEE SELECTION AS A CONTROL SYSTEM 25

dollar amounts for borrowers with higher credit scores and lower debtratios.

More notably, the coefficient estimates show that the predicted patternsin the use of decision-making authority across employee categories remain.The coefficient estimates on the employee category indicators from col-umn 3 suggest that, relative to old system employees referred by old systememployees, the implied marginal effects for new system/referred by oldsystem, new system/not referred, and new system/referred by new systememployees are approximately 3%, 4%, and 8%, respectively.

Turning to decisions on the structuring of loans, the last column in panelA of table 5 demonstrates that employees are more likely to make inter-est rate exceptions for loans with higher dollar amounts to borrowers withlower credit scores and higher debt ratios. Borrowers with lower creditscores and/or higher debt ratios would not normally qualify for the or-ganization’s lowest interest rates, so it is not surprising that these are theborrowers for whom employees would offer rate reductions. Results on theuse of this type of decision-making authority across employee categories arenot as strong as those for loan approval decisions. New system employeesreferred by new system employees show the highest conditional rates of in-terest rate exceptions followed by new system employees referred by old sys-tem employees, but nonreferred new system employees show no significantdifferences from either category of old system employee. Relative to oldsystem employees referred by old system employees, the implied marginaleffects for new system/referred by old system and new system/referred bynew system employees are 1.4% and 1.8%. Relative to the 23% mean rateexceptions by old system/referred by old system employees, these implyincreases of approximately 6% and 8%, respectively.

In general, the results on the sample of corporate and back officeemployees in table 5, panel B, are not as strong as those for customer-contact employees. This discrepancy may reflect more significant coordina-tion problems among the numerous and geographically disperse customer-contact employees, but may also arise due to smaller numbers of employeesor loans within the corporate and back office sample.

Overall, the results in this section provide evidence that the use ofdecision-making authority is significantly higher for employees selected viachannels that are likely to sort on the alignment of their preferences withorganizational objectives. I turn next to investigating the effectiveness ofemployee use of decision-making authority.

4.3 DO DECISION-MAKING OUTCOMES VARY WITH THE CHANNEL OFEMPLOYEE SELECTION?

I examine the effectiveness of decision-making outcomes by investigat-ing 18-month charge-off rates for “system-deny” loans approved during theperiod January 2007–November 2008. I am limited to this relatively shorttime frame because I only observe charge-offs occurring during the periodJanuary 2008–April 2010. Summary statistics on charge-off rates, both on

26 D. CAMPBELL

T A B L E 6Charge-Off Rates by System Rule Status and Employee Category

Charge-Off Rates for Loans:

Meeting System Not MeetingCriteria System Criteria

Average 0.40% 1.9%∗

By Employee Category:Old system, referred by old system 0.30% 2.49%∗

Old system, not referred 0.64% 2.19%∗

New system, referred by old system 0.41% 2.17%∗

New system, not referred 0.60% 1.48%∗,b,c,d

New system, referred by new system 0.54% 0.77%a,b,c,d

∗denotes mean charge-off rates are significantly different from those for loans meeting system criteriaat less than the 1% level; where the asterisk is absent, this difference is not statistically significant at leastat the 10% level. a,b,c, and d denote significantly different from old system/referred by old system, oldsystem/nonreferred, new system/referred by old system, and new system/nonreferred employees, respec-tively, at least at the 10% level based on two-sample tests of proportion. Charge-off rates are calculated basedon loans funded during 2007 and 2008 that were charged off within 18 months. “New System” denotes em-ployees hired after the organization’s implementation of its decentralized business model (post-2004). “OldSystem” denotes employees hired prior to the organization’s implementation of its decentralized businessmodel (2004 and earlier).

average and across employee categories, are provided in table 6. Not sur-prisingly, given that they are based on criteria that index the ex ante risk ofborrowers, “system-deny” loans show a significantly higher mean charge-offrate of 1.9% compared to 0.4% for those that meet system criteria.

A potentially better point of comparison would be charge-off rates forloans that just meet system criteria for acceptance. These loans wouldbe accepted in the absence of decision-making authority but would haveex ante risk that is closer to that of system-deny loans. To facilitate this com-parison, I examine the subsample of loans that meet system criteria fordebt-to-income ratios (<45%) but that were made to borrowers with creditscores between 620 and 640. These borrowers meet system criteria but arejust over the threshold credit-score cutoff. The mean charge-off rate forthis sample of 1.88% is almost identical to the 1.9% rate for employee ap-proved system-deny loans. While employees use decision-making authorityto approve a significant percentage of system-deny loans per figure 4 andtable 2, these results suggest that they do so in a way that does not appre-ciably increase short-term risk relative to system-based lending criteria.

Turning to differences across employee categories, table 6 shows a de-clining pattern in charge-off rates as we move from old system/referred byold system to new system/referred by new system employees with the latterdemonstrating lower rates than all other categories. The mean charge-offrate for this category is 0.77%, nearly half that of new system/nonreferredemployees, which shows the next lowest rate at 1.48%. All other categoriesdemonstrate statistically identical mean charge-off rates in excess of 2%.

The results in table 7 demonstrate that these patterns generally holdup under multivariate analysis. This table contains logit models of 18-month charge-off rates conditional on loan, borrower, and employee char-acteristics along with loan-type and year fixed effects for the sample of

EMPLOYEE SELECTION AS A CONTROL SYSTEM 27

T A B L E 7Charge-Off Logits

Customer-ContactEmployees All Employees

SystemDenied:

SystemDenied:

System Credit System CreditDenied Score Only Denied Score Only

Credit grade A+ −1.133∗∗∗ −0.317(0.43) (0.29)

Credit grade A −0.537∗ −0.265(0.30) (0.34)

Credit grade C 1.322∗∗∗ −0.515∗∗∗ 1.449∗∗∗ −0.717∗∗∗

(0.28) (0.18) (0.27) (0.17)Credit grade D 1.377∗∗∗ 1.722∗∗∗

(0.26) (0.25)Debt-to-income ratio −0.003 −0.006 0.00004 0.0005

(0.003) (0.004) (0.00007) (0.0008)Loan amount ($000’s) −0.003 −0.04∗∗ 0.004 −0.02

(0.02) (0.02) (0.01) (0.24)Old system employee, −0.192 −0.168 −0.410∗∗∗ −0.424∗∗∗

not referred (0.15) (0.16) (0.13) (0.14)New system employee referred −0.257 −0.145 −0.433∗∗∗ −0.310∗

by old system employee (0.18) (0.19) (0.16) (0.18)New system employee, −0.383∗∗∗,b,c −0.605∗∗∗,b,c −0.450∗∗∗ −0.594∗∗∗,c

not referred (0.15) (0.17) (0.12) (0.14)New system employee referred −2.249∗∗∗,b,c,d −2.527∗∗∗,b,c,d −2.294∗∗∗,b,c,d −2.377∗∗∗,b,c,d

by new system employee (0.59) (0.72) (0.46) (0.52)Constant −2.624∗∗∗ −1.236∗∗∗ −2.932∗∗∗ −1.261∗∗∗

(0.35) (0.25) (0.31) (0.21)Observations 18,779 7,016 22,356 8,352