Employee Overpayments in OSPA

22

Employee Overpayments in OSPA Oregon Statewide Payroll Services March 11, 2010

-

Upload

daphne-todd -

Category

Documents

-

view

58 -

download

0

description

Employee Overpayments in OSPA. Oregon Statewide Payroll Services March 11, 2010. Class Objective. Raise awareness of the following: Identifying overpayments Choices agencies have in handling overpayments Calculating the overpayment Repayment entries When to request a Corrected W-2. - PowerPoint PPT Presentation

Transcript of Employee Overpayments in OSPA

Employee Overpayments in OSPA

Oregon Statewide Payroll ServicesMarch 11, 2010

2

Class Objective

Raise awareness of the following: Identifying overpayments Choices agencies have in handling

overpayments Calculating the overpayment Repayment entries When to request a Corrected W-2

3

Outline

Overall process Net pay negatives Year-end Specific examples

4

What are some causes of overpayments?

5

How did you find them?

6

What Is Our Responsibility?

To make the Joint Payroll Account (JPA) whole

To make the agency whole To accurately report and pay the

employee’s wages and taxes

7

What Guidelines Do We Have? OAM 45.50.00.PO and PR Collection of

Overpayment Collective Bargaining Agreements Agency Policy and Business Practices IRS and DOR Regulations PEBB Rules and Guidelines

8

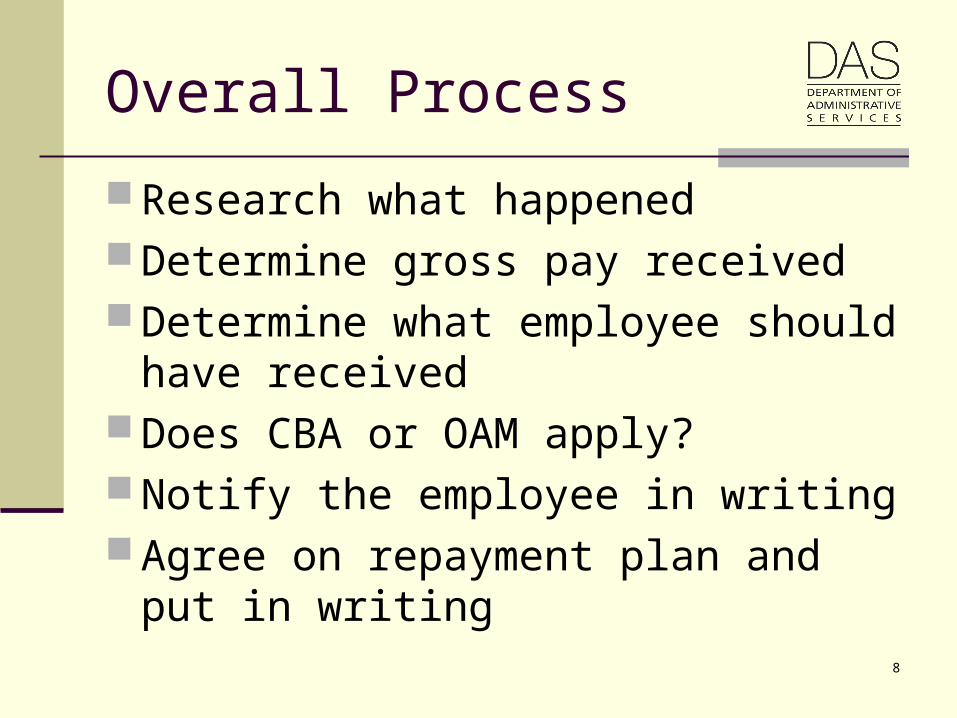

Overall Process

Research what happened Determine gross pay received Determine what employee should have

received Does CBA or OAM apply? Notify the employee in writing Agree on repayment plan and put in

writing

9

Spreadsheet Available

Overpayment RecoveryEmployee Name

Gross Overpayment 3608.00 184 hrs march 06 LWOP 3608EE FICA 7.65% (SS 6.2% MEDR 1.45%) 276.01 OSPS will recover from IRS

ER Share Fica (same calc) 276.01 OSPS will recover from IRSPERS Pickup 216.48 Agency Recovers From PERSPERS Employer Share (8.69% or 11.65%) 313.54 Agency Recovers From PERS

Total To Recover 4414.03

Employee must repay Agency 3331.99 For gross less employee FICA

Reconciliation (No Formulas) Benefit TransactionsUnion Dues To Recover

Recovered From EE Other transactionsRecovered From IRS Leave AdjustmentsRecovered From PERS Total Recovered = Total Agency Costs

10

Written Notice

Amount owed Supporting documentation Opportunity to respond within # days If opportunity for monthly payments

11

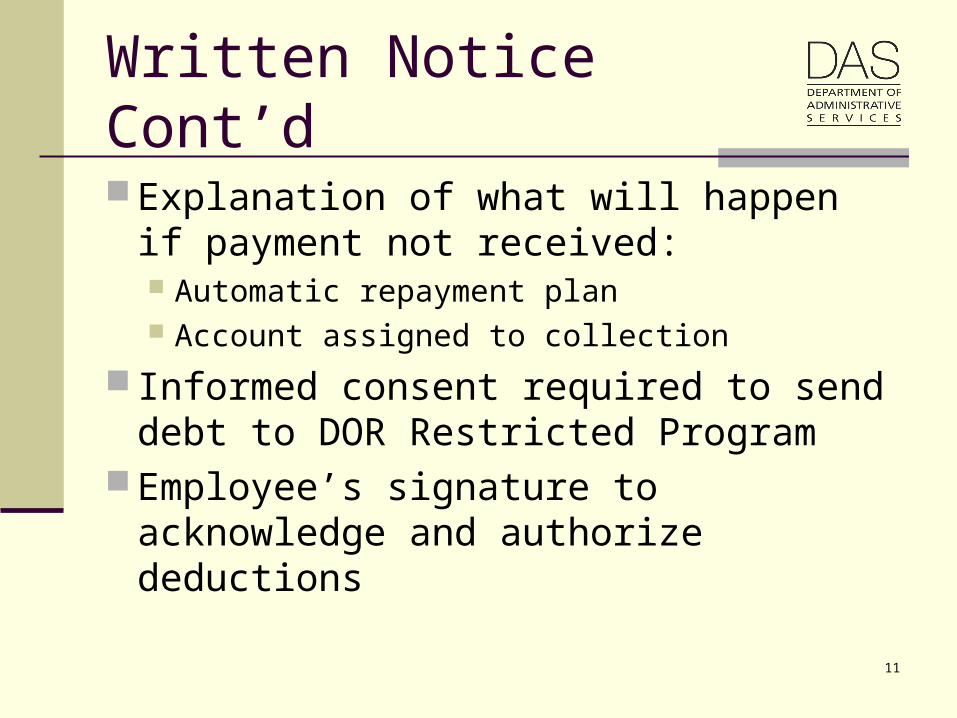

Written Notice Cont’d

Explanation of what will happen if payment not received: Automatic repayment plan Account assigned to collection

Informed consent required to send debt to DOR Restricted Program

Employee’s signature to acknowledge and authorize deductions

12

Informed Consent

DOR Restricted Program requires use of SSN

Section 7, Privacy Act of 1974, 5 USC 552a requires: Whether disclosure is voluntary or mandatory By what statutory or other authority you are

soliciting the SSN How you will use the SSN

13

Informed Consent Cont’d

“Should I not repay the overpayment as agreed, I give my permission to release my SSN to the Oregon Department of Revenue. I understand that my action is voluntary and that the agency will only use my SSN for collection purposes under ORS 292.063 and ORS 293.250.”

14

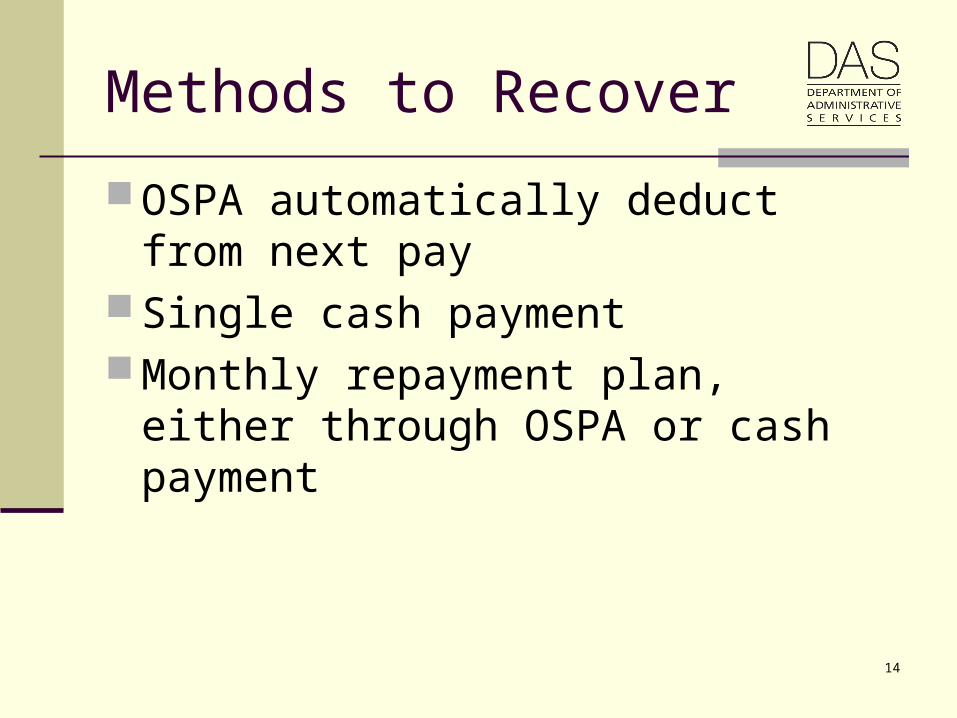

Methods to Recover

OSPA automatically deduct from next pay

Single cash payment Monthly repayment plan, either through

OSPA or cash payment

15

Cash Payment

Agency may receive in any form acceptable to agency

For JPA, DAS, must be: Money order Cashier’s check State warrant Balanced transfer from R*STARS Agency revolving fund check

16

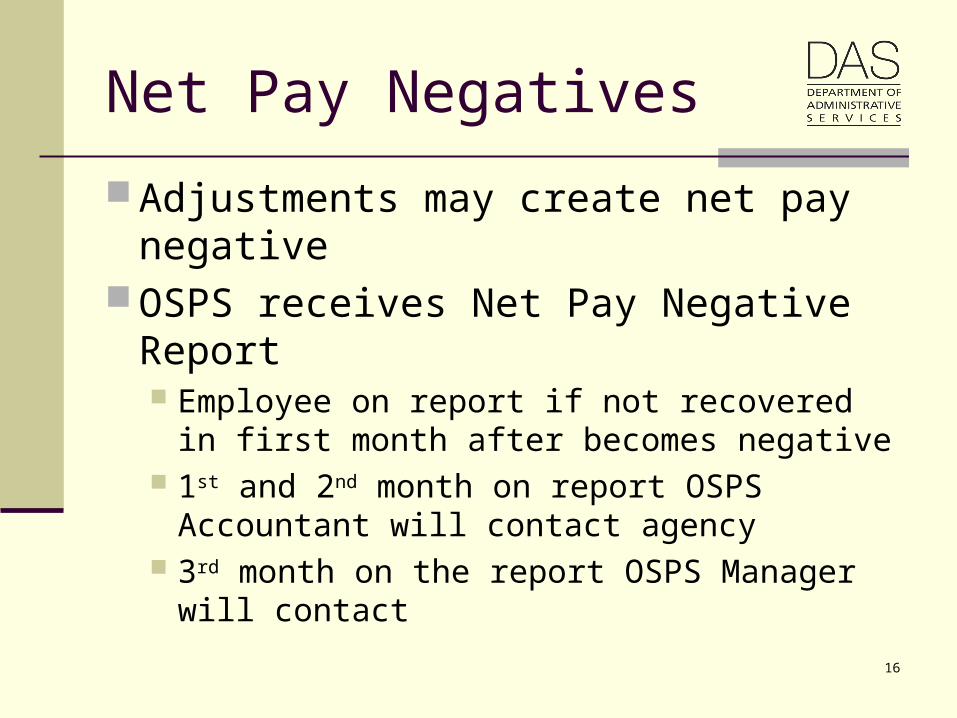

Net Pay Negatives

Adjustments may create net pay negative

OSPS receives Net Pay Negative Report Employee on report if not recovered in first

month after becomes negative 1st and 2nd month on report OSPS Accountant

will contact agency 3rd month on the report OSPS Manager will

contact

17

Net Pay Negatives Cont’d

OAM 45.50.00.PR requires reimbursement to the JPA for net pay negatives

If agency reimburses the JPA, set up an account receivable outside OSPA

18

Overpayments at Year-end

IRS Publication 15 (Circular E) Wages paid in error remain taxable to the

employee until repaid Employee received and had use of the funds Employee does not amend the tax return,

claims deduction in year repaid OSPA Reference Manual,

Recommended Practices, Taxes, Corrected W-2 (W-2c) Year-end

19

What questions do you have?

20

Examples for Class

Employee’s LWOP reported after run 1 Employee received clothing allowance

through both R*STARS and OSPA Employee mistakenly received work-

out-of-class (WOC) through the PPDB

21

Examples Cont’d

Employee compensated by SAIF and had full-time paid leave through OSPA

Employee has domestic partner insurance and no DPT on P050

22

Please remember to do survey in iLearnOregon

Next Forum – March 17, 2:00 to 4:00 pm, Mt. Mazama Rm, 1225 Ferry St. SE

April class – Employee Separations in OSPA

![Payroll Overpayment Challenges Presentation [Read-Only] · employer and the employee is more then $10,000. Types of Overpayments Loans Taxable amount is not subject to federal tax](https://static.fdocuments.us/doc/165x107/5ebc4bc914b20048102f6f0f/payroll-overpayment-challenges-presentation-read-only-employer-and-the-employee.jpg)