Emod: Putting Deflationary Pressure on an Inherently Inflationary System Appalachian Steps Network...

39

Emod: Putting Deflationary Pressure on an Inherently Inflationary System Appalachian Steps Network George Brown Ramsey Risk Management Group July 11, 2013

-

Upload

valerie-wheeler -

Category

Documents

-

view

216 -

download

0

Transcript of Emod: Putting Deflationary Pressure on an Inherently Inflationary System Appalachian Steps Network...

Emod: Putting Deflationary Pressure on an Inherently

Inflationary System

Appalachian Steps NetworkGeorge Brown

Ramsey Risk Management GroupJuly 11, 2013

Ramsey Risk Management Group

Safety

• An age old concept of insurance is that it is designed to make the insured whole. But, can it really?

Ramsey Risk Management Group

If an employee loses the ability to hear or see or walk…

Will any amount of money make them whole?

Ramsey Risk Management Group

If an employee is killed in an unfortunate accident…

Will a lump sum benefit replace the husband, mother, brother, sister?

Ramsey Risk Management Group

No!

• This is why what safety professionals do on a daily basis is so important!

• The employee came to work with 10 fingers and 10 toes and that’s the way we want them to go home!

ZERO INCIDENTS!

Ramsey Risk Management Group

But, accidents do happen

• And when they do, the employee enters the Workers Compensation System.

• The workers compensation system, that most of us deal with, is an inflationary system.

Ramsey Risk Management Group

• An inflationary system is one where all the players make more money when it costs the consumer more money.

• For Workers Compensation’s purposes, the consumer is the employer.

Ramsey Risk Management Group

Think about it:• An employee is injured– Is taken by ambulance– To the emergency room– Referred to the local physician for care– The physician manages the care by setting follow-

up appointments– The preferred provider network gets involved– The lawyer gets involved to see if he can make

money helping the employee– Etc….

Ramsey Risk Management Group

Who’s making money here?

Not the employer!

Ramsey Risk Management Group

Everyone benefits financially, except the employer

• The employee gets paid while rehabilitating.

• The physician/chiropractor/etc. gets paid for scheduling appointments and running tests and doing rehabilitation.

• The agent gets paid. As premiums go up so does the agent’s commission.

Ramsey Risk Management Group

And, yes, the insurance company gets paid…

• Indemnity claims costs below the split point are revenue producers for the insurance company.

• Over the next few years, the split point will increase from $5000 up to $15000, and then it will be indexed further for inflation.

• The traditional model for WC Insurance does not have the resources to allocate to low end claims management.

Ramsey Risk Management Group

“Every dollar in claims cost has a direct and measurable impact on the premium you pay!”

Ramsey Risk Management Group

Claim Reserves

• And yes, Claim Reserves count the same as any other claim…whether they are justified or not.

• And, the employer pays increased premiums based on these reserved claims whether justified or not.

Ramsey Risk Management Group

Fraud

• Fraud costs the employer just like any other claim.

• Many employees assume that it is a victimless crime and that they are only taking money from some huge insurance company.

• But, what the employee needs to understand is that the employer pays directly for the claims cost through additional premiums and it could be up to 2 1/2 times or more of the actual amount of the claim.

Ramsey Risk Management Group

Questions you might ask about your Emod

• What is my emod now?

• Where would I like it to be?

• Is an Emod of 1.00 good?

• How low can I go?– Zero Claims = Minimum Emod

• How can I get there?

Ramsey Risk Management Group

Claim Impact

• The following slides are examples of how claims impact your Emod which directly impact your premium for workers compensation insurance.

• The examples are from an employer with

– Workers Compensation Premium = $268,435.

– NCCI Emod = 1.30

Ramsey Risk Management Group

Typical Emod Worksheet

WORKERS' COMPENSATION RATING WORKSHEET

STATE WT SRP

EXPECTEDEXCESSLOSSES

EXPECTEDLOSSES

EXPECTEDPRIMARYLOSSES

ACTUALEXPECTED

LOSSES BALLAST

ACTUALINCURRED

LOSSES

ACTUALPRIMARYLOSSES

WV-A 0.21 0 170,948 213,640 42,692 363,281 38,500 441,504 78,223WV-B 0.00 0 0 0 0 0 0 0 0WV-C 0.00 0 0 0 0 0 0 0 0WV-D 0.00 0 0 0 0 0 0 0 0

TOTALS 170,948 213,640 42,692 363,281 38,500 441,504 78,223

(A)

WT

(B) (C)EXPECTED

EXCESSLOSSES(D - E)

(D)

TOTALEXPECTED

LOSSES

(E)

EXPECTEDPRIMARYLOSSES

(F)ACTUAL

EXPECTEDLOSSES(H - I)

(G)

BALLAST

(H)

ACTUALINCURRED

LOSSES

(I)

ACTUALPRIMARYLOSSES

0.21 170,948 213,640 42,692 363,281 38,500 441,504 78,223

PRIMARY LOSSES STABILIZING VALUE RATABLE EXCESS TOTALS

ACTUAL(I) C * (1 - A) + G (A) * (F) (J)

78,223 173,549 76,289 328,061

EXPECTED (E) C * (1 - A) + G (A) * (C) (K) 42,692 173,549 35,899 252,140

ARAP FLARAP SARAP MAARAP EXPERIENCE MOD

FACTORS 1.22

(J) / (K) 1.30

Ramsey Risk Management Group

Minimum Mod WORKERS' COMPENSATION RATING WORKSHEET

STATE WT SRP

EXPECTEDEXCESSLOSSES

EXPECTEDLOSSES

EXPECTEDPRIMARYLOSSES

ACTUALEXPECTED

LOSSES BALLAST

ACTUALINCURRED

LOSSES

ACTUALPRIMARYLOSSES

WV-A 0.21 0 170,948 213,640 42,692 363,281 38,500 441,504 78,223WV-B 0.00 0 0 0 0 0 0 0 0WV-C 0.00 0 0 0 0 0 0 0 0WV-D 0.00 0 0 0 0 0 0 0 0

TOTALS 170,948 213,640 42,692 363,281 38,500 441,504 78,223

(A)

WT

(B) (C)EXPECTED

EXCESSLOSSES(D - E)

(D)

TOTALEXPECTED

LOSSES

(E)

EXPECTEDPRIMARYLOSSES

(F)ACTUAL

EXPECTEDLOSSES(H - I)

(G)

BALLAST

(H)

ACTUALINCURRED

LOSSES

(I)

ACTUALPRIMARYLOSSES

0.21 170,948 213,640 42,692 363,281 38,500 441,504 78,223

PRIMARY LOSSES STABILIZING VALUE RATABLE EXCESS TOTALS

ACTUAL(I) C * (1 - A) + G (A) * (F) (J)

0 173,549 0 173,549

EXPECTED (E) C * (1 - A) + G (A) * (C) (K) 42,692 173,549 35,899 252,140

ARAP FLARAP SARAP MAARAP EXPERIENCE MOD

FACTORS 1.49

(J) / (K) 0.69

Ramsey Risk Management Group

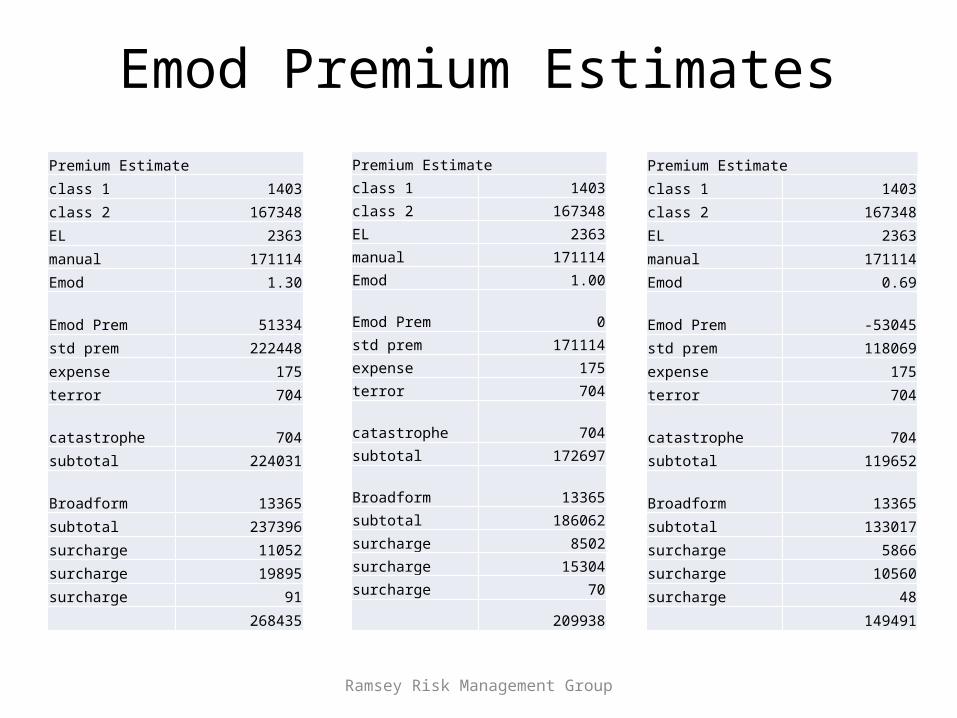

Emod Premium EstimatesPremium Estimate

class 1 1403

class 2 167348

EL 2363

manual 171114

Emod 0.69

Emod Prem -53045

std prem 118069

expense 175

terror 704

catastrophe 704

subtotal 119652

Broadform 13365

subtotal 133017

surcharge 5866

surcharge 10560

surcharge 48

149491

Premium Estimate

class 1 1403

class 2 167348

EL 2363

manual 171114

Emod 1.00

Emod Prem 0

std prem 171114

expense 175

terror 704

catastrophe 704

subtotal 172697

Broadform 13365

subtotal 186062

surcharge 8502

surcharge 15304

surcharge 70

209938

Premium Estimate

class 1 1403

class 2 167348

EL 2363

manual 171114

Emod 1.30

Emod Prem 51334

std prem 222448

expense 175

terror 704

catastrophe 704

subtotal 224031

Broadform 13365

subtotal 237396

surcharge 11052

surcharge 19895

surcharge 91

268435

Ramsey Risk Management Group

What’s it costing?

• 1.3 Emod = $268,435 Premium • .69 Emod = $149,491 Premium• Difference = $118,944 Premium

The impact of claims on the premium this employer pays is almost

$120,000!

Ramsey Risk Management Group

How do Primary Claims impact my Emod?

• Primary Claim with Indemnity– In WV, Indemnity payments start after 3 lost days.

• Assume $1000 claim cost

Ramsey Risk Management Group

Primary Claim Emod Impact WORKERS' COMPENSATION RATING WORKSHEET

STATE WT SRP

EXPECTEDEXCESSLOSSES

EXPECTEDLOSSES

EXPECTEDPRIMARYLOSSES

ACTUALEXPECTED

LOSSES BALLAST

ACTUALINCURRED

LOSSES

ACTUALPRIMARYLOSSES

WV-A 0.21 0 170,948 213,640 42,692 363,281 38,500 441,504 78,223WV-B 0.00 0 0 0 0 0 0 0 0WV-C 0.00 0 0 0 0 0 0 0 0WV-D 0.00 0 0 0 0 0 0 0 0

TOTALS 170,948 213,640 42,692 363,281 38,500 441,504 78,223

(A)

WT

(B) (C)EXPECTED

EXCESSLOSSES(D - E)

(D)

TOTALEXPECTED

LOSSES

(E)

EXPECTEDPRIMARYLOSSES

(F)ACTUAL

EXPECTEDLOSSES(H - I)

(G)

BALLAST

(H)

ACTUALINCURRED

LOSSES

(I)

ACTUALPRIMARYLOSSES

0.21 170,948 213,640 42,692 363,281 38,500 441,504 78,223

PRIMARY LOSSES STABILIZING VALUE RATABLE EXCESS TOTALS

ACTUAL(I) C * (1 - A) + G (A) * (F) (J)

1,000 0 0 1,000

EXPECTED (E) C * (1 - A) + G (A) * (C) (K) 42,692 173,549 35,899 252,140

ARAP FLARAP SARAP MAARAP EXPERIENCE MOD

FACTORS

(J) / (K) 0.003966

Ramsey Risk Management Group

Primary Claim Premium Impact

.003966 X 209,938 X 3 = 2497

For every $1 of Primary Claims Cost, you will pay approximately $2.50 in additional premium.

Ramsey Risk Management Group

How do Medical Only claims impact my Emod?

• Medical Only Claim– Medical Only Claims are reduced by 70%– Any indemnity payments cause you to lose the

discount.• This includes payments for permanent partial disability

• Assume $1000 claim cost

Ramsey Risk Management Group

Medical Only Claim Impact WORKERS' COMPENSATION RATING WORKSHEET

STATE WT SRP

EXPECTEDEXCESSLOSSES

EXPECTEDLOSSES

EXPECTEDPRIMARYLOSSES

ACTUALEXPECTED

LOSSES BALLAST

ACTUALINCURRED

LOSSES

ACTUALPRIMARYLOSSES

WV-A 0.21 0 170,948 213,640 42,692 363,281 38,500 441,504 78,223WV-B 0.00 0 0 0 0 0 0 0 0WV-C 0.00 0 0 0 0 0 0 0 0WV-D 0.00 0 0 0 0 0 0 0 0

TOTALS 170,948 213,640 42,692 363,281 38,500 441,504 78,223

(A)

WT

(B) (C)EXPECTED

EXCESSLOSSES(D - E)

(D)

TOTALEXPECTED

LOSSES

(E)

EXPECTEDPRIMARYLOSSES

(F)ACTUAL

EXPECTEDLOSSES(H - I)

(G)

BALLAST

(H)

ACTUALINCURRED

LOSSES

(I)

ACTUALPRIMARYLOSSES

0.21 170,948 213,640 42,692 363,281 38,500 441,504 78,223

PRIMARY LOSSES STABILIZING VALUE RATABLE EXCESS TOTALS

ACTUAL(I) C * (1 - A) + G (A) * (F) (J)

300 0 0 300

EXPECTED (E) C * (1 - A) + G (A) * (C) (K) 42,692 173,549 35,899 252,140

ARAP FLARAP SARAP MAARAP EXPERIENCE MOD

FACTORS

(J) / (K) 0.001190

Ramsey Risk Management Group

Medical Only Premium Impact

.001190 X 209,938 X 3 = 749

For every $1 of Medical Only Claims Cost, you will pay approximately $.74 in additional premium.

Ramsey Risk Management Group

How do Excess claims impact my Emod?

• Excess Claims– The Emod is designed to rate frequency (primary)

claims and, as such, claims above the split point are discounted by a weighting factor.

• Assume $1000 claim cost in excess of the split point.

Ramsey Risk Management Group

Excess Claim Impact WORKERS' COMPENSATION RATING WORKSHEET

STATE WT SRP

EXPECTEDEXCESSLOSSES

EXPECTEDLOSSES

EXPECTEDPRIMARYLOSSES

ACTUALEXPECTED

LOSSES BALLAST

ACTUALINCURRED

LOSSES

ACTUALPRIMARYLOSSES

WV-A 0.21 0 170,948 213,640 42,692 363,281 38,500 441,504 78,223WV-B 0.00 0 0 0 0 0 0 0 0WV-C 0.00 0 0 0 0 0 0 0 0WV-D 0.00 0 0 0 0 0 0 0 0

TOTALS 170,948 213,640 42,692 363,281 38,500 441,504 78,223

(A)

WT

(B) (C)EXPECTED

EXCESSLOSSES(D - E)

(D)

TOTALEXPECTED

LOSSES

(E)

EXPECTEDPRIMARYLOSSES

(F)ACTUAL

EXPECTEDLOSSES(H - I)

(G)

BALLAST

(H)

ACTUALINCURRED

LOSSES

(I)

ACTUALPRIMARYLOSSES

0.21 170,948 213,640 42,692 363,281 38,500 441,504 78,223

PRIMARY LOSSES STABILIZING VALUE RATABLE EXCESS TOTALS

ACTUAL(I) C * (1 - A) + G (A) * (F) (J)

0 0 210 210

EXPECTED (E) C * (1 - A) + G (A) * (C) (K) 42,692 173,549 35,899 252,140

ARAP FLARAP SARAP MAARAP EXPERIENCE MOD

FACTORS

(J) / (K) 0.000833

Ramsey Risk Management Group

Excess Premium Impact

.000833 X 209,938 X3 = 524

For every $1 of Excess Claims Cost, you will pay approximately $.52 in additional premium.

Ramsey Risk Management Group

Conclusions

• ZERO Incidents =•ZERO Claims Cost = •Minimum Mod = •Lowest Premium

•ZERO INCIDENTS!

Ramsey Risk Management Group

But if you do have claims…

• Claims management from the time of injury forward is essential. • Return to work policies should focus on return to work as soon

as possible from the time of injury. • Indemnity Claims below the split point are very costly to the

employer: example: $1 Claim = $2.50 in additional Premium.• Medical only claims get a 70% Discount: $1 Claim = $.74 in

additional premium.• If you can get the employee back to work prior to 3 days, it

saves the company 70%. And, statistics show that the sooner you can get an employee back to work the more likely it is that they will return to full duty.

Ramsey Risk Management Group

But if you do have claims…

• Triage• Then if the employee is referred, work

towards Work Release/Light Duty/Full Duty/MMI.

• Every year, prior to the Emod promulgation date, negotiate with your insurance carrier to remove or reduce claims reserves. There is no reason to pay for unnecessary reserve cost.

Ramsey Risk Management Group

What Can the Employer Do?

• Manage the claims management process on your own.

Or

• Use a Business Process Outsourcing Model to manage the claim process.

Ramsey Risk Management Group

Manage the claims management process on your own:

• Continue Safety Efforts to avoid claims!• When an injury does occur:

– Triage the injury to determine the appropriate level of care.

– Return to work: every effort should be made to get the employee back to work prior to indemnity. Alternate job assignments should be considered. Work Release/Light Duty/Full Duty/MMI.

Ramsey Risk Management Group

Manage the claims management process on your own:

– Should negotiate with the insurance carrier to remove or adjust unnecessary or inflated reserves prior to the Emod promulgation date.

– Should investigate past, current, and future claims for accuracy.

– Reduce Fraud.

Ramsey Risk Management Group

Or Use Business Process Outsourcing to Manage the Process

• Continue Safety Efforts to avoid claims• When an injury does occur: Care will not be diminished.

– The BPO will set up telephonic medical triage to be used with each injury.

– Return to work: The BPO will use their experience managing claims to work with the employee, the medical provider and the employer to get the employee back to work prior to indemnity, if possible. Alternate job assignments should be considered. The BPO will work with the employee, medical provider and the employer to effect Work Release/Light Duty/Full Duty/MMI.

Ramsey Risk Management Group

The BPO :– Will use their experience to negotiate with the

insurance carrier to remove unnecessary reserves and exaggerated reserves prior to the emod promulgation date.

– Will investigate past, current, and future claims for accuracy.

– Will institute proven procedures to reduce fraud.

Ramsey Risk Management Group

What should an employer look for in a BPO?

• The BPO should have no fiduciary responsibility to anyone but the employer.

• The BPO should work on a capitated, flat fee basis – forced to be efficient.

• The BPO should offer an annual agreement. If the BPO is not performing or conditions change, the employer should be able to leave.

• The BPO should offer a 100% return on investment guarantee.

• The BPO should have references available.

Ramsey Risk Management Group

Questions?