EMERGING TRENDS & ISSUES LYING, CHEATING, … · EMERGING TRENDS & ISSUES LYING, CHEATING, AND...

21

©2012 EMERGING TRENDS & ISSUES LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW White-collar crimes are non-violent, often complex criminal offenses involving lying, cheating, and stealing. This presentation focuses on the investigation, prosecution, and defense of white-collar crimes. Topics covered will include fraud, corruption, money laundering, obstruction of justice, and other crimes commonly litigated in federal courts, along with the latest laws and legal techniques. This session will also discuss cutting-edge issues specific to white- collar crime concerning criminal law and evidence. DOUG SQUIRES Adjunct Professor of Law Ohio State University Moritz College of Law Capital University School of Law Columbus, OH Doug Squires is an adjunct professor at the Ohio State University Moritz College of Law and the Capital University Law School in Columbus, OH. At Moritz, Squires teaches white-collar crime. At Capital, Squires developed and, for eight years, taught a class in forensic evidence, an advanced evidence course. Doug has authored several published materials on white-collar crime and fraud, including a chapter entitled “Forensic Accounting” in Scientific Evidence in Civil and Criminal Cases, the leading legal text on scientific and technical evidence. Since 2000, Doug has worked as a federal prosecutor in Columbus, OH. In 2009, Doug received the U.S. Department of Justice Distinguished Service Award. Prior to that, Doug worked for seven years as a state prosecutor in California. Doug received a B.A. from Miami University, Oxford, OH, his law degree from the University of San Francisco School of Law, and is licensed to practice law in Ohio and California. “Association of Certified Fraud Examiners,” “Certified Fraud Examiner,” “CFE,” “ACFE,” and the ACFE Logo are trademarks owned by the Association of Certified Fraud Examiners, Inc. The contents of this paper may not be transmitted, re-published, modified, reproduced, distributed, copied, or sold without the prior consent of the author.

Transcript of EMERGING TRENDS & ISSUES LYING, CHEATING, … · EMERGING TRENDS & ISSUES LYING, CHEATING, AND...

©2012

EMERGING TRENDS & ISSUES LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

White-collar crimes are non-violent, often complex criminal offenses involving lying,

cheating, and stealing. This presentation focuses on the investigation, prosecution, and defense of

white-collar crimes. Topics covered will include fraud, corruption, money laundering,

obstruction of justice, and other crimes commonly litigated in federal courts, along with the latest

laws and legal techniques. This session will also discuss cutting-edge issues specific to white-

collar crime concerning criminal law and evidence.

DOUG SQUIRES

Adjunct Professor of Law

Ohio State University Moritz College of Law

Capital University School of Law

Columbus, OH

Doug Squires is an adjunct professor at the Ohio State University Moritz College of Law and

the Capital University Law School in Columbus, OH. At Moritz, Squires teaches white-collar

crime. At Capital, Squires developed and, for eight years, taught a class in forensic evidence, an

advanced evidence course.

Doug has authored several published materials on white-collar crime and fraud, including a

chapter entitled “Forensic Accounting” in Scientific Evidence in Civil and Criminal Cases, the

leading legal text on scientific and technical evidence.

Since 2000, Doug has worked as a federal prosecutor in Columbus, OH. In 2009, Doug

received the U.S. Department of Justice Distinguished Service Award. Prior to that, Doug

worked for seven years as a state prosecutor in California. Doug received a B.A. from Miami

University, Oxford, OH, his law degree from the University of San Francisco School of Law,

and is licensed to practice law in Ohio and California.

“Association of Certified Fraud Examiners,” “Certified Fraud Examiner,” “CFE,” “ACFE,” and the

ACFE Logo are trademarks owned by the Association of Certified Fraud Examiners, Inc. The contents of

this paper may not be transmitted, re-published, modified, reproduced, distributed, copied, or sold without

the prior consent of the author.

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 1

NOTES Goals of the Presentation

DESCRIBE modern white-collar crimes

DEBUNK misconceptions and defenses

DELINEATE courses of action

Disclaimer

The views and opinions of the speaker may not necessarily

be those of the U.S. Department of Justice.

What Is WCC?

1939:

Sociologist Edwin Sutherland

“Occupational crime by persons of high social

status”

Emphasis on social status and greed v. other crimes,

which were the result of poverty

Sutherland criticized the notion that all improper

business dealings are only civil wrongs

(Will discuss civil v. criminal in a moment)

Now:

Lying, cheating, and stealing for gain or advantage

Gain–money, but can also be social status, political

advantage

Why Is There WCC?

“Are you kidding!? I couldn’t make this much money

selling crack in Detroit … Besides, this way, no one

shoots me and I get to wear a suit.”

—Fraudster, Proffer Session

Lyin’, Cheatin’, and Stealin’

There is no list of included offenses; it is constantly

changing

Are federal offenses—focus of this lecture

Fed crimes help us examine WCC

Fed juris based on Commerce Clause

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 2

NOTES Defined by U.S. v. Lopez (SCOTUS 1995)

Regular changes to WCC rules and laws

Laws are added

Agg ID theft with two-year minimum

mandatory prison time

Rules are narrowed

Money laundering (will discuss)

“Like music, lying requires exquisite timing, a consistent

beat, and a melodic quality designed to sooth the most

cynical beast.”

—Robert F. Miller, real estate con-artist; statement to the

U.S. District Court, District of Columbia, 1:05CR00143

Mortgage Fraud

What happened?

The perfect storm

Low interest rates

Red-hot housing market

Mortgage origination boom

New products/markets:

Subprime/Alt-A

New lenders and mortgage brokers

Fee-driven system

Lowered underwriting standards

Securitizations

Trends and opportunities need to be

identified

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 3

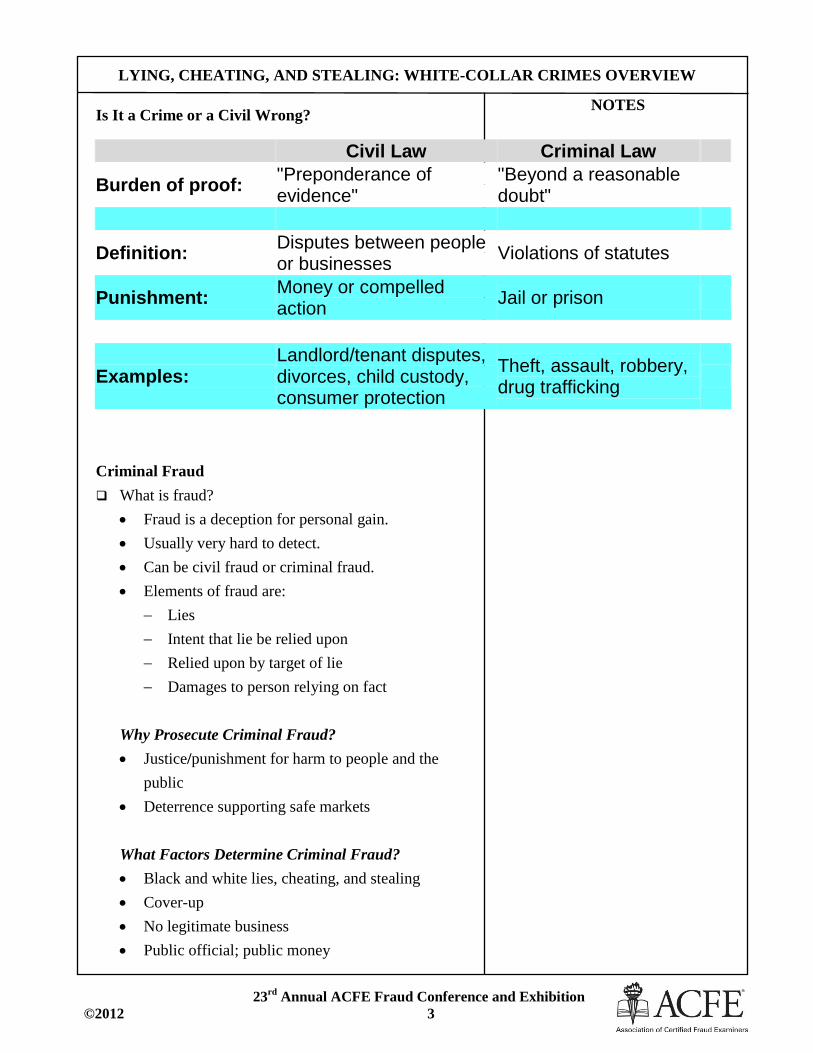

NOTES Is It a Crime or a Civil Wrong?

Criminal Fraud What is fraud?

Fraud is a deception for personal gain.

Usually very hard to detect.

Can be civil fraud or criminal fraud.

Elements of fraud are:

Lies

Intent that lie be relied upon

Relied upon by target of lie

Damages to person relying on fact

Why Prosecute Criminal Fraud?

Justice/punishment for harm to people and the

public

Deterrence supporting safe markets

What Factors Determine Criminal Fraud?

Black and white lies, cheating, and stealing

Cover-up

No legitimate business

Public official; public money

Civil Law Criminal Law

Burden of proof: "Preponderance of evidence"

"Beyond a reasonable doubt"

Definition: Disputes between people or businesses

Violations of statutes

Punishment: Money or compelled action

Jail or prison

Examples: Landlord/tenant disputes, divorces, child custody, consumer protection

Theft, assault, robbery, drug trafficking

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 4

NOTES What Indicators Occur in Most Frauds?

Concealing assets/unexplained wealth

Two sets of books

Destroying records

Fake documents

Payments to fake companies and people

How Are Most Criminal Frauds Proven? Proof of lies, cheating, and stealing usually

documents with lies or missing documents

Profits shown through books and records “following

the money”

Insiders who can testify:

Those who profited excessively must be

convicted insiders.

Employees receiving only “normal” salaries do

not get prosecuted.

Work “uphill” to get to the lies by bosses.

Which Frauds Are Most Often Prosecuted?

Monetary Loss

Victim harm

Deterrence

Prosecuting Corporations

Historically, a corporation could not be guilty of a crime,

only tort damages = civil money to be paid.

Why Hold a Corp. Criminally Liable?

Deter really bad conduct

Encourage due diligence laws followed

New York Central (SCOTUS 1909) 212 U.S 481

Cited as historical basis for corporate criminal

liability.

Defendants: cannot hold corp. liable

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 5

NOTES Congress passed unconstitutional Elkins Act

Corp. liability punishes innocent stockholders

No due process to be heard

Deprivation of presumption of innocence

Court: Corp. criminal liability found

No valid reason not to punish a corporation

Public policy requires monitoring of ISC

In this case it prevents favoritism

First case to extend corp. criminal liability beyond acts

of omission or regulatory offenses.

Deterrence

Does holding corp. liable have general and specific

deterrence?

General: deter others from committing crime

Specific: deter the corporation from future crime

Issue: findings of criminal liability are death

sentence

What Individuals Often Get Prosecuted?

Rogue employees

Should there be a “good faith” defense for

corps?

Not for employees that can “bind” corp.

Big heads

How profited and how much?

Beyond “normal” salary

Commissions and backdoor deals

Button pusher or decision maker

Money Laundering Update

Deferred Prosecution Agreements

Non-prosecution agreements with contingencies,

usually the payment of money in exchange for an

admission of wrongdoing and forgoing future

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 6

NOTES conduct = do this/don’t do this and you will not be

prosecuted

The February 2009 UBS Deferred Prosecution

Agreement

The bank admitted to helping U.S. taxpayers hide

accounts from the Internal Revenue Service (IRS), and

agreed to identify customers and pay $780 million.

UBS AG, Switzerland’s largest bank, entered into a

deferred prosecution agreement on charges of

conspiring to defraud the United States by impeding the

IRS and the Justice Department.

As part of the deferred prosecution agreement and in an

unprecedented move, UBS, based on an order by the

Swiss Financial Markets Supervisory Authority

(FINMA), agreed to immediately provide the U.S.

government with the identities of, and account

information for, certain U.S. customers of UBS’ cross-

border business. Under the deferred prosecution

agreement, UBS also agreed to expeditiously exit the

business of providing banking services to U.S clients

with undeclared accounts. Also, UBS agreed to pay

$780 million in fines, penalties, interest, and restitution.

A criminal information was unsealed that charged UBS

with conspiring to defraud the United States by

impeding the IRS. In 2000, after it purchased the

brokerage firm Paine Webber, UBS voluntarily entered

into an agreement with the IRS that required the

reporting of income and other identifying information

for its U.S. clients who held U.S. securities in a UBS

account. Court documents allege that the agreement

also required UBS to withhold income taxes from U. S.

clients who directed investment activities in foreign

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 7

NOTES securities from the United States. The information

further asserts that, in order to evade those new

reporting requirements, employees and managers within

the cross-border business, with the knowledge of

certain UBS executives, helped U.S. taxpayers open

new UBS accounts in the names of nominees and/or

sham entities. According to court documents, the assets

of the individual’s accounts were then transferred to the

newly created accounts, as to which the U.S. taxpayer

would not be identified as a beneficiary.

The information asserts that this device was used by

UBS to justify evading its reporting obligations and

helped U.S. taxpayers to continue to conceal their

identities and assets from the IRS.

The information also alleges that Swiss bankers

routinely traveled to the United States to market Swiss

bank secrecy to U.S. clients interested in attempting to

evade U.S. income taxes. Court documents assert that,

in 2004 alone, Swiss bankers allegedly traveled to the

United States approximately 3,800 times to discuss

their clients’ Swiss bank accounts. The information

further alleges that UBS managers and employees used

encrypted laptops and other counter-surveillance

techniques to help prevent the detection of their

marketing efforts and the identities and offshore assets

of their U.S. clients. According to the information,

clients of the cross-border business in turn filed false

tax returns, which omitted the income earned on their

Swiss bank accounts and failed to disclose the existence

of those accounts to the IRS.

The DPA specified that in light of the bank’s

willingness to acknowledge responsibility for its actions

and omissions, its cooperation and remedial actions to

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 8

NOTES date, and its promised continuing cooperation and

remedial actions, the government will recommend

dismissal of the charge, provided the bank fully carries

out its obligations under the agreement.

At the time, a press release noted, “Today’s agreement

is but one milestone in an ongoing law enforcement

effort to reassure hard-working and law-abiding

taxpayers who pay their fair share of taxes that those

who don’t will pay a heavy price,” said John A.

DiCicco, Acting Assistant Attorney General of the

Justice Department’s Tax Division. “The veil of secrecy

has been pulled aside, and we will continue to

aggressively pursue those who shirk their federal tax

obligations or assist others in doing so.”

“UBS executives knew that UBS’ cross-border business

violated the law,” said R. Alexander Acosta, U.S.

Attorney for the Southern District of Florida. “They

refused to stop this activity, however, and in fact

instructed their bankers to grow the business. The

reason was money—the business was too profitable to

give up. This was not a mere compliance oversight, but

rather a knowing crime motivated by greed and

disrespect of the law.”

UBS Summary

Severely impacted Swiss bank secrecy

UBS Switzerland’s largest bank

Entered into DPA for impeding IRS in

collection of taxes

Agreed to:

Provide identities and account info. For certain

U.S. customers of UBS cross-border businesses

Stop “undeclared accounts”

Pay $780 million in fines, interest, and rest.

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 9

NOTES Arthur Anderson LLP

Destroyed docs after the noticed investigation of

Enron

Charged with obstruction of justice 18 U.S.C.

1512(b)

Turned in CPA license

SCOTUS reversed, but the partnership did not

survive

Led to creation of 18 U.S.C. 1519

Alteration/destruction of docs in federal

investigation or bankruptcy proceeding

FBAR—Foreign Bank Accounts

Must be reported when filing taxes

The Report of Foreign Bank and Financial

Accounts (FBAR) is required when a U.S. citizen

has a financial interest in or signature authority over

one or more foreign financial accounts with an

aggregate value greater than $10,000. If a report is

required, certain records must also be kept.

In April 2003, the IRS was delegated civil

enforcement authority for the FBAR.

Statutory authority for FBAR

U.S.C. § 5314 the United States Code

F.R. Part 103, the Code of Federal Regulations

A financial account includes:

A bank account, such as a savings, demand,

checking, deposit, time deposit, or any other

account maintained with a financial institution

or other person engaged in the business of a

financial institution. A bank account set up to

secure a credit card account is an example of a

financial account. An insurance policy having a

cash surrender value is an example of a financial

account.

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 10

NOTES Securities, securities derivatives, or other

financial instruments accounts qualify.

Other financial accounts generally encompass

any accounts in which the assets are held in a

commingled fund and the account owner holds

an equity interest in the fund. A mutual fund

account is an example of such an account.

Individual bonds, notes, or stock certificates

held by the filer are not financial accounts.

Public Corruption

Lyin’, Cheatin’, and Stealin’ for Personal Gain: Money

or Improved Position

The Hobbs Act (18 U.S.C. § 1951) prohibits actual or

attempted robbery or extortion affecting interstate or

foreign commerce.

“Extortion” obtaining property by actual or

threatened force; or “under color of official right”

McCormick v. U.S. (SCOTUS 1991)

West Virginia legislator alleged to take

payments from foreign docs

State shortage of docs, so legislation considered

to grant foreign medical grads WVA licenses

Some money not on books as campaign

contributions given as cash in envelopes and not

reported as income

SCOTUS focused on “under color of official

right” language and if it includes campaign

contributions

jury instruction said Hobbs Act violation lies

where McCormick induced cash payment by

extortion

Finding: quid pro quo is necessary to prosecute

for accepting a campaign contribution

Benefit or advantage in exchange for money

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 11

NOTES Evans v. U.S. (SCOTUS (1992)

One year after McCormick

Justice Stevens dissented in McCormick

Authors majority opinion here

County commissioner charged with Hobbs Act

and failure to report income on return

Court focuses on term “inducement” and

whether an affirmative act of inducement is an

element of the offense

Undercover FBI gave $8,000, only $1,000

reported as campaign and tax forms

Lower courts split on if affirmative act by a

public official is required

Majority say a “passive acceptive” okay;

SCOTUS agrees

Some require an affirmative act of

inducement by the public official to support

an extortion charge premised upon “under

color of official right”; this is rejected

Gov. must only show: a public official has

obtained a payment to which he was not

entitled, knowing the payment was made in

return for official acts = quid pro quo of

McCormick

Entrapment as a Defense

In Evans, FBI undercover posed as real estate

developer.

Entrapment at issue

Entrapment can be a complete defense to a crime if

two related elements exist:

Gov. inducement of the crime

Defendant’s lack of predisposition to engage in

the criminal conduct

Okay for government agents or decoy to:

Engage in crime

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 12

NOTES Offer crime

But cannot:

Persuade person to do crime

Or otherwise deceive person to commit crime they

had not intended to commit

The Attorney-Client Privilege

The privilege is designed to promote and facilitate an

individual’s ability to seek legal advice, knowing that

all matters can be discussed candidly and completely

with counsel. This is perfected by protecting disclosure

under most circumstances. (Upjohn v. United States,

449 U.S. 383 (1985)

Although the privilege is designed to provide

confidentiality, its purposes are subverted where the

assertion of the privilege is designed to provide a cloak

of secrecy around the illicit business affairs of an

individual or corporation.

Lawyers have an ethical duty to maintain the privilege

that is shared by the agents of either the lawyer or client

who come into possession of such information. The

courts have long recognized that modern legal practice

requires lawyers to rely upon the services of non-

lawyers. This may include secretarial personnel,

interpreters, investigators, law clerks and accountants.

(United States v. Cote, 456 F.2d 142 (8th

Cir. 1982)

The December 2006 “McNulty Memo” drew criticism

for inadequately protecting the attorney-client privilege

in federal prosecutions since the memo specified that

corporate voluntary production of such information

would be considered in a calculation of “cooperation”

to be ultimately considered in charging decisions. Since

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 13

NOTES August 2008, cooperation will no longer be measured

on whether a corporation under criminal investigation

chooses to waive the attorney-client privilege, nor will

attorney-client or work product materials be demanded.

(USDOJ DAG Mark R. Filip, Principals of Federal

Prosecution of Business Organizations, August 28,

2008, the “Filip Memo.”)

The Accountant-Client Privilege

Federal courts have refused to recognize a pure

accountant-client privilege. (United States v. Arthur

Young & Co., 465 U.S. 805, 836 (1984); United States

v. Mihalich, 2006 WL 2946947)

A limited federal privilege exists extending to tax

advice under the Federally Authorized Tax Practitioner

Privilege, which does not apply to criminal matters or

state tax proceedings.

If a crime involves specific-intent, a defense of good

faith reliance on the advice of an accountant is available

if the defendant fully disclosed all facts to the

accountant, and relied on the account advice in good

faith. (United States v. Duncan, 850 F.2d 1104 (6th

Cir.

1988)

The defense can negate a crimes element requiring

specific intent where the defendant shows she relied on

the advice of her attorney, accountant, or state official

in taking certain actions. (United States v. Swafford,

2005 US. Dist. LEXIS 26890 (E.D. Tenn. Nov. 3,

2005). (See Hot Topic.)

For example, Ohio Senate Bill 371(2008) would have

created an accountant-client privilege, which is the

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 14

NOTES trend in about half the states. The measure would have

little impact on federal cases.

Advice of Counsel as a Defense

The advice-of-counsel defense allows a defendant to

show that there was no wrongful intent underlying his

unlawful actions. The defense proposes that the

defendant lacked the intent needed to commit the

offense, or, in the civil context, that the defendant

lacked the specific state of mind required (or

conversely, acted in “good faith”).

The defense is not always an affirmative defense, but

rather negates an element of the offense itself.

A corporate employee may assert the defense to any

criminal charges or civil suit brought against them,

even if there is no direct attorney-client relationship

between themselves and the corporation’s counsel.

A defendant must show that he fully disclosed all

material facts to his attorney before seeking advice, and

actually relied on his counsel’s advice in the good faith

belief that his conduct was legal.

The Hot Topic of Waiver of Privilege

Raising the advice-of-counsel defense means the

defense generally waives the attorney-client privilege

protecting communications between a client and his

counsel because the client is putting the contents of

those communications at issue by asserting the defense.

For executives, the issue of waiver is made difficult

because the lawyers they often rely upon represent the

corporation, not its executives. It is not clear if

executives can raise the defense in each instance if the

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 15

NOTES executive could not force the corporation to waive the

attorney-client privilege. This creates a problem

because corporate directors and employees frequently

rely on the advice of their corporation’s legal counsel in

matters that could expose them to personal liability.

Courts have been inconsistent as to whether and to what

extent an individual asserting an advice-of-counsel

defense may introduce privileged communications

against the wishes of the corporate privilege holder.

In United States v. W.R. Grace, the district court framed

the question this way: “Whether and under what

circumstances the attorney-client privilege must give

way to a criminal defendant’s Sixth so that a balancing

test should be used to determine when the defendant’s

right to present exculpatory evidence may trump the

corporation’s right to maintain attorney-client

privilege.”

In Ross v. City of Memphis, the Sixth Circuit reversed

the Ross court and held that the corporation’s privilege

could not be made to yield for the defendant, no matter

how much she needed the documents for her defense

because “[a]n uncertain privilege, or one which

purports to be certain but results in widely varying

applications by the courts, is little better than no

privilege at all.”

Practice Pointer

Some commentators suggest executive employment

contracts should specify that directors and corporations

should contract that the corporation will waive its

attorney-client privilege if the director, sued in her

individual capacity, needs to raise an advice-of-counsel

defense.

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 16

NOTES Fraud and Intangible Rights

McNally voided use of intangible rights in 1987

Demonstrates how legislation reacts to

SCOTUS decisions

McNally voided mail fraud prosecution

For intangible rights

Immediately after opinion in 1988

Congress enacted 18 U.S.C. 1346

18 U.S.C. Sec 1346

For mail, wire, and bank fraud as “scheme to

defraud” includes a scheme to deprive another

of the “intangible right of honest services.”

Politicians who profit or better their position by

depriving the public of the intangible right of

honest services are engaged in a scheme to

defraud under mail, wire, and bank fraud

statutes.

Skilling v. U.S. (SCOTUS 2010) 130 S.Ct. 2896 (June

24, 2010)

SCOTUS rejected the vagueness challenge, but

interpreted 1346 to criminalize “only the bribe-and-

kickback core of the pre-McNally case law.”

A violation of 1346 requires the defendant to

receive clear bribes or kickbacks from an insider to

the fraud, in addition to the deprivation of honest

services.

1346 attacked as vague, overbroad, and limited.

Some commentators urge, you need a clear shoebox

full of money for illegitimate promises for an 18

U.S.C. 1346 conviction.

What Are “Intangible Rights as Property?”

Items connected to duties owed to the public and

others, like shareholders.

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 17

NOTES One example is the development of insider trading

as a form of securities fraud.

In 1980s, cases developed a misappropriation

theory:

Cases concentrated on the duty owed to

shareholders by an insider and by individuals

receiving info. from the insider.

Most courts found there must be a duty owed for a

finding of insider trading liability.

Some appellate courts found insider trading liability

based on a misappropriation theory:

“A person who has misappropriated nonpublic

information has a duty to refrain from trading on

it.”

A Reversal and Acquittal After Skilling

On November 16, 2011, the Second Circuit reversed

and dismissed the conviction of former New York State

Senate Majority Leader Joseph L. Bruno for theft of

honest services fraud on his failure to disclose alleged

conflicts of interest.

The reversal was based on the Supreme Court decision

in Skilling, which limited 18 U.S.C. 1346, the honest

services statute, to cases involving bribery and

kickbacks.

Even though some circuit courts have upheld honest

services fraud convictions over Skilling challenges, the

reversal here was no surprise to some since, among

other things, the government conceded error.

Bruno argued that if there was insufficient evidence at

trial to justify a conviction under the Skilling bribery

and kickback theory of honest services fraud, the Court

must bar retrial on double jeopardy grounds. The

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 18

NOTES government argued that sufficiency review under a

standard different from that at the time of trial was

inappropriate and unfair. (The defense did not contend

there was insufficient evidence based on the law at the

time of trial.) At oral argument, the government stated

that the evidence at the new trial would be the same as

in the first.

The Court, declining to enact any black letter law, and

relying considerably on the government’s concession

that the evidence would not change at a second trial,

agreed to analyze the sufficiency of evidence based on

the new, narrower Skilling standard. Nonetheless, after

reviewing the facts, the Court held that the evidence

was sufficient under that standard. Bruno, therefore,

won the battle, but lost the war. The government

announced that it will re-indict him under an honest

services fraud theory based on bribery and kickbacks.

Also in November 2011, a Southern District of New

York jury acquitted William Boyland, Jr., a New York

State Assemblyman, of honest services fraud for

allegedly receiving bribes from David Rosen, the chief

executive of a hospital conglomerate, apparently

because of lack of sufficient proof of a quid quo pro.

Other Charges Used in Public Corruption Cases

Bribery

18 U.S.C. Sec 666—theft or bribery concerning

programs receiving federal funds; 10 years

maximum

Congress enacted 18 U.S.C. § 666 to “protect the

integrity of the vast sums of money distributed

through federal programs from theft, fraud, and

undue influence by bribery.”

Elements:

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 19

NOTES If program receives $10,000 or more in year and

$5,000 or more is at issue

Agent solicits, embezzles, or steals

Person corruptly gives with the intent to

corruptly influence

DOJ policy limits prosecutions “to cases in which

the federal assistance is given pursuant to a specific

statutory scheme that authorizes assistance to

promote or achieve policy objectives. The statute

was not intended to reach every federal contract or

every federal disbursement.”

And to lesser extent:

18 U.S.C. 1001—false material statement or

false writing or document to a federal officer

(exec., leg., or judicial branch); 5 years

maximum

“Federal contempt of cop” charge

Kickbacks

Drive up costs and are ethically bent

The Anti-Kickback Act of 1986, 41 U.S.C. §§51-58

Provides criminal (and civil) penalties for

paying or receiving kickbacks in federal

procurements.

10 years maximum for criminal violation.

Civil recovery of twice the bribe and $10,000

fine for each transaction.

Cases supervised in the Federal Procurement

Fraud Unit in the DOJ Fraud Section.

Protects the integrity of all U.S. government

contracts and subcontracts.

Includes contracts and subcontracts for

“supplies, materials, equipment, or services

of any kind.” [41 U.S.C. § 52(4) & (7).]

Prohibits the solicitation, acceptance, payment,

or offer to pay a kickback.

LYING, CHEATING, AND STEALING: WHITE-COLLAR CRIMES OVERVIEW

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 20

NOTES Id. § 53(1) & (2). Also prohibits including

the amount of any “kickback” in the contract

price. Id. § 53 (3).

Kickback is defined in § 52(2) as:

Any money, fee, commission, credit, gift,

gratuity, thing of value, or compensation of any

kind;

Which is provided, directly or indirectly, to any

prime contractor, prime contractor employee,

subcontractor, or subcontractor employee;

For the purpose of improperly obtaining or

rewarding favorable treatment in connection

with a prime contract or subcontract.

This is the commercial equivalent of bribery. A

contractor who is willing to pay a bribe to a

government official to obtain a government contract

might also be willing to accept a kickback from a

subcontractor, perhaps to help defray the cost of the

bribe.

Note civil kickback penalties under:

Medicare Anti-Fraud and Abuse Act 42 U.S.C.

1320a-7b:

No money for referral of Medicare patients

Stark II 42 U.S.C. 1395nn

No physical self-referrals