Emerging issues and future trends in the accounting profession- a paper presented at the 49 th...

28

Emerging issues and future trends in the accounting profession- a paper presented at the 49 th induction of ICAN May 2012

-

Upload

oswin-turner -

Category

Documents

-

view

221 -

download

0

Transcript of Emerging issues and future trends in the accounting profession- a paper presented at the 49 th...

Emerging issues and future trends in the accounting profession- a paper presented at the 49th induction of ICAN

May 2012

Agenda

Introduction

Emerging issues

Future trends

Qualities of the Accountant of the Future

Conclusion

Q & A

2May 2012Emerging issues and future trends in the accounting profession

Introduction

13

May 2012Emerging issues and future trends in the accounting profession

Introduction

Change they say is the only constant thing in life. This statement is very true in our profession. In recent times, we are seeing the focus of responsibilities of accountants shifting from recording the various aspects of a corporation’s financial health to joining top executives in a broad based partnership. In this presentation we will look at some emerging issues and future trends in our profession.

4May 2012Emerging issues and future trends in the accounting profession

Emerging issues

25

May 2012Emerging issues and future trends in the accounting profession

Emerging issues

•Globalization and IFRS

•The accountant and corporate scandals

•The call for Auditor rotation

•Accounting for small and medium sized enterprises

•Technological advances

•The need for a global code of ethics

•The increasing need for sustainability reporting

6May 2012Emerging issues and future trends in the accounting profession

Some of the issues facing the accounting profession today include:

Globalization and International Financial Reporting Standards (IFRS)

As trade and investments are increasing across borders, it is becoming more and more important for financial information to be reliable, transparent and comparable. This is particularly important within an international context. Globalisation impacts the international accounting profession mainly in terms of the global flow of capital which is creating much of the pressure for harmonized accounting standards/convergence.

The other big impact of globalization is the way new powers are emerging and changing the flow of capital e.g China and India. These new economic powerhouses will have a significant impact on national economies in all parts of the world.

International accounting and auditing standards are seen as a way to ensure reliability and comparability in financial statements across regions and jurisdictions. They are also seen as a way to restore confidence in the profession as a whole and in capital markets. But the needs and concerns of developing nations are quite different from those of developed ones in this regard. Some people feel the significant costs involved in adopting international standards are not worth the benefits. Other concerns include translation and linguistic concerns.

Emerging issues and future trends in the accounting profession7

May 2012

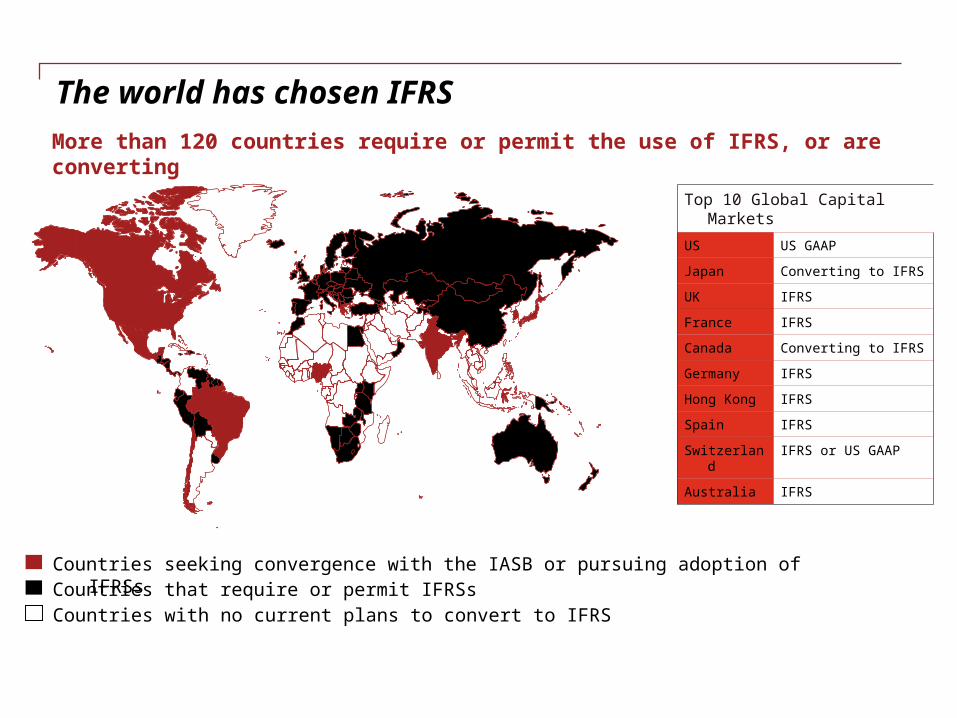

The world has chosen IFRSMore than 120 countries require or permit the use of IFRS, or are converting

Top 10 Global Capital Markets

US US GAAP

Japan Converting to IFRS

UK IFRS

France IFRS

Canada Converting to IFRS

Germany IFRS

Hong Kong IFRS

Spain IFRS

Switzerland IFRS or US GAAP

Australia IFRS

Countries seeking convergence with the IASB or pursuing adoption of IFRSsCountries that require or permit IFRSsCountries with no current plans to convert to IFRS

The accountant and corporate scandalsFraud is not new.

What is probably new or different is the scale and impact of the various corporate scandals. Some of the recent corporate scandals include:

-Xerox(2000)

-Enron (2001)- One of the biggest audit failures of all time

-Worldcom (2002)

-Parmalat (2003)

-Bernard L. Madoff Investment Securities LLC (2008)

-Satyam Computers India(2009)

-Lehman Brothers(2010)

The magnitude of these events has focused public attention on the accounting profession as never before, and has increased the pressure to ensure that universally high standards of accounting practice are in place everywhere. Regulators and legislators are responding quickly. In the US, the Sarbanes-Oxley Act of 2002 created the Public Company Accounting Oversight Board (PCAOB) to oversee the audits of public companies in order to protect investors and the public interest by promoting informative, accurate, and independent audit reports. Similar bodies have been set up in different countries including the Financial Reporting Council in Nigeria.

Emerging issues and future trends in the accounting profession9

May 2012

The Call for Auditor rotation

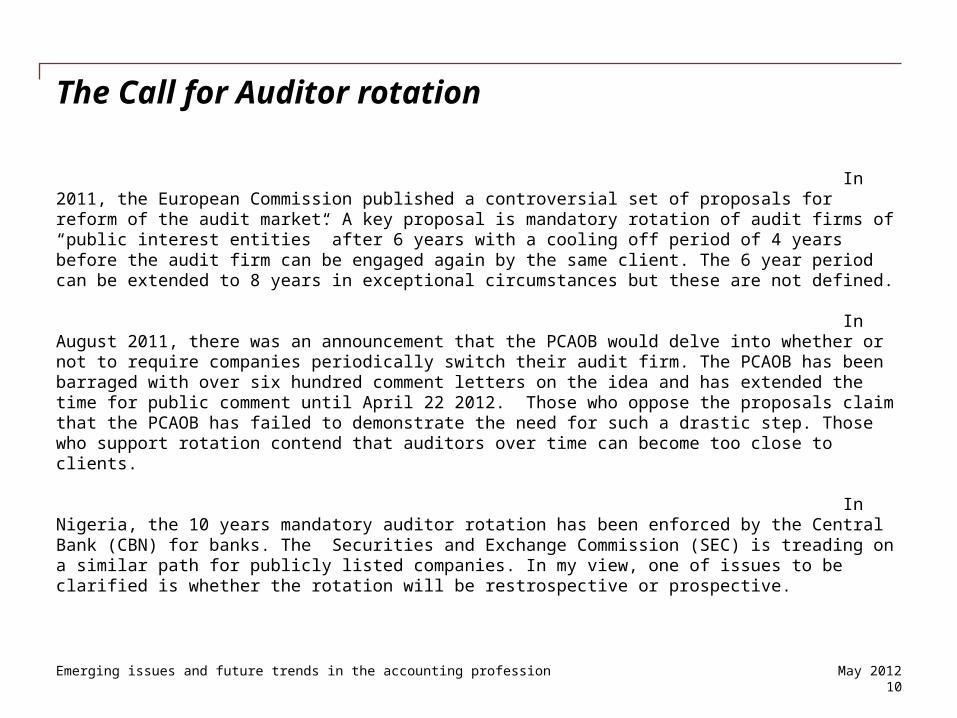

In 2011, the European Commission published a controversial set of proposals for reform of the audit market. A key proposal is mandatory rotation of audit firms of “public interest entities” after 6 years with a cooling off period of 4 years before the audit firm can be engaged again by the same client. The 6 year period can be extended to 8 years in exceptional circumstances but these are not defined.

I

n August 2011, there was an announcement that the PCAOB would delve into whether or not to require companies periodically switch their audit firm. The PCAOB has been barraged with over six hundred comment letters on the idea and has extended the time for public comment until April 22 2012. Those who oppose the proposals claim that the PCAOB has failed to demonstrate the need for such a drastic step. Those who support rotation contend that auditors over time can become too close to clients.

In Nigeria, the 10 years mandatory auditor rotation has been enforced by the Central Bank (CBN) for banks. The Securities and Exchange Commission (SEC) is treading on a similar path for publicly listed companies. In my view, one of issues to be clarified is whether the rotation will be restrospective or prospective.

Emerging issues and future trends in the accounting profession10

May 2012

Accounting for small and medium sized enterprises (SME/MME)

In most developing nations there are only a few large, publicly-traded business entities. SMEs tend to drive the economy. Yet for the most part, international standards have been developed with the needs of large firms in mind.

The needs and concerns of small and medium sized enterprises are quite different from those of large, transnational corporations, when it comes to adoption of international standards.

There is a call for greater recognition by accounting bodies, of SME’s needs, their economic value and their significant importance in many national economies. There is also an urge to build the profile of SMEs by emphasizing their professional capabilities, produce innovative ideas for alternatives to audit for use in the SME environment, and provide greater support for SMEs in terms of standards and guidelines tailored to their needs.

On 9 July 2009, the IASB published an International Financial Reporting Standard (IFRS) designed for use by small and medium-sized entities (SMEs). Addressing the needs of SMEs would increase in importance over the coming years.

Emerging issues and future trends in the accounting profession11

May 2012

Technological advances

The impact of technology affects accountants in all sectors of the profession and in all parts of the globe. The availability of information and the speed at which it is processed creates both challenges and opportunities for our profession across boundaries, borders and time zones. Banks, other financial services companies, software and Internet firms will offer an increasing array of accounting and tax-related products and services.

Consulting and business advisory firms, as well as other non-accountants, will take advantage of new software and analytical tools to provide new accounting-related services. These tools will also make bookkeeping and tax preparation cheaper and easier, reducing demand for lower-value accounting services.

Gradually, the industry and life is changing. Automation is replacing manual data collection and input. Most routine and lower-valued accounting and tax tasks are being outsourced to overseas firms in, for example India, Sri Lanka, Malaysia, etc.

Emerging issues and future trends in the accounting profession12

May 2012

Global code of ethics

There is an increasing push for a global code of ethics to protect the fundamental qualities of the profession, particularly relating to independence.

Auditor independence and agreeing/discussing expectations to prevent and detect fraud are considered important.

The International Ethics Standards Board for Accountants (IESBA), an independent standard-setting board within the International Federation of Accountants (IFAC), has recently updated and strengthened the independence requirements contained in the IFAC Code of Ethics for Professional Accountants (2011). Some of the changes include:

-No practice staff can have directorship in audit clients

-Permissible services for PIEs and SEC became more restricted.

Emerging issues and future trends in the accounting profession13

May 2012

Sustainability reporting

Progression of corporate social responsibility, including sustainability, is becoming more and more important to the profession. There is a push for integrated reporting to become mandatory.

Sustainability and CSR reporting, is a fairly recent trend which has expanded over the last twenty years. Many companies now produce an annual sustainability report and there are a wide array of ratings and standards around. There are a variety of reasons that companies choose to produce these reports, but at their core they are intended to be "vessels of transparency and accountability".

Examples of companies producing sustainability reports include:

-British American Tobacco

-Shell

-Nestle

-Chevron

-Coca-Cola

-Exxon Mobil

-Ford Motors, Intel, Nike etc

Emerging issues and future trends in the accounting profession14

May 2012

Lack of professional resources

Many international institutions are at very different stages of maturation. This results in education programs and certification standards which may not meet international expectations.

In addition, regulatory bodies lack resources and maturity. Capital markets also lack many of the structures and safeguards we have come to take for granted. Professional associations also lack the resources required to advance the accounting profession and meet the expectations of the international profession and the public.

These sophisticated structures and institutions take time and resources to create. The ones in the developed world were not built overnight. And the ones in developing countries will not mature to a comparable level overnight either.

Emerging issues and future trends in the accounting profession15

May 2012

Future trends

316

May 2012Emerging issues and future trends in the accounting profession

Future trends

These trends in our profession are reflective of larger societal shifts. The trends include:

1.Shifting business environment and new opportunities

2.Demographic shifts changing the face of professionals and clients

3.Technology changes

4.High-Touch Client Outreach, Relationships and Service

17May 2012Emerging issues and future trends in the accounting profession

Shifting business environment and new opportunities Many services currently provided by accounting professionals –

especially low value-added or easily automated services, such as data entry, bookkeeping and simple tax returns – will become less profitable and even disappear due to competition, automation and outsourcing.

Growing business complexity, knowledge requirements, regulatory and legal change and client expectations will favor accounting specialists over generalists.

Specialization will lead to increased collaboration and partnering among accounting firms and other financial professionals, both domestically and internationally.

Successful accounting professionals will take on new roles as consultants and advisors, providing performance management, decision support and similar services, with less emphasis on nuts-and-bolts functions such as computation and tax preparation.

Globalization, the health care industry, aging baby boomers and an increased emphasis on sustainability and sustainable business practices will create new opportunities for specialization.

18May 2012Emerging issues and future trends in the accounting profession

Demographic shifts

Aging baby boomers will look for guidance in the areas of financial planning, retirement and estate planning, health and elder care. They’ll turn to accounting professionals advisors as they start and run full- and part-time businesses.

Tech-oriented Generation Y clients will expect to interact with their accounting professionals digitally, using online and self-serve customer support in addition to traditional methods.

Women, who have been starting small businesses at twice the rate of men over the last decade, will increasingly be financial decision makers for businesses, making them an important client segment.

Accounting firms will need to offer flexible work options and increased work/life balance to attract and retain talent. Those that cannot provide this flexibility will be at a competitive disadvantage.

In addition to flexible work options, Generation Y workers will seek tech-savvy employers using up-to-date digital tools. This emerging workforce also expects learning and growth opportunities.

Staffing at firms will need to reflect and support the growing needs of multicultural clients and those conducting international business.

19May 2012Emerging issues and future trends in the accounting profession

Technology changes The amount of time and effort required – and client needs – for data

collection and validation will be substantially reduced.

Data analysis tools and software will greatly increase the opportunities to provide clients with analysis, performance management and decision-support services.

Technology consulting opportunities for accounting professionals will increase. Data management, security and privacy consulting opportunities will be particularly strong.

System integration, training, installation, support and reselling opportunities will increase.

Mobile and any time/any place technologies will allow tax and accounting professionals flexible work options and client interactions while maintaining superior client service standards.

20May 2012Emerging issues and future trends in the accounting profession

High-Touch Client Outreach, Relationships and Service Accounting firms will need to develop or source online marketing

expertise and use their web presence to highlight their skills, areas of specialization and scope.

Online social networks will become a key source of client referrals, prospects and new clients.

Social media will increasingly be used to establish firm reputation and brand.

Automating and improving client service through the use of the Internet and CRM systems will be required to meet growing client support expectations.

21May 2012Emerging issues and future trends in the accounting profession

Qualities of the Accountant of the Future

422

May 2012Emerging issues and future trends in the accounting profession

Qualities of the Accountant of the Future

These will include:

Personal attributes, which include insight, sound professional judgment, project management skills, integrity and ethics

Leadership qualities of strategic thinking, planning and a cross-functional perspective

Broad business perspective, which includes a good understanding of one’s organization and industry, risk management and organizational systems and processes

Functional expertise in the traditional technical skills, including financial management and taxation

Strong communication skills, be well versed in IT, be committed to life time of learning

Ability to combine technical skills with strategic vision, see himself as a professional advisor and business partner.

23May 2012Emerging issues and future trends in the accounting profession

Conclusion

524

May 2012Emerging issues and future trends in the accounting profession

Conclusion

The next decade will witness society’s transition to mobile and social commerce, driven by new technologies that allow consumers and businesses to compete locally and globally. This shift will drive consumers and businesses to turn to accounting and tax professionals for competitive strategies to navigate the global marketplace, not just prepare financial reports and tax returns. As small businesses embrace social networks, so must accounting professionals.

Globalization will be the norm, as small businesses use web access, real-time manufacturing, and mobile marketing to reach across borders for customers and suppliers. Accounting professionals who are knowledgeable in international standards, regulations, and processes will thrive.

Accounting firms will increasingly rely on each other’s capabilities and collaborate to compete more effectively in the international marketplace.

25May 2012Emerging issues and future trends in the accounting profession

Questions???

626

May 2012Emerging issues and future trends in the accounting profession

References

CIMA publication - Accounting trends in a borderless world - November 2010

IFAC News – April 2011

CGA Magazine – Interview with Inter-american Accounting Association’s Pierre Barnes on global accounting issues - May/June 2006

Intuit 2020 report – February 2011

The Accountant Magazine – ISAs most crucial issue facing profession – March 2011

PCAOB website

International Journal of Disclosure and Governance – September 2010

Paper by Prof. Barry J. Cooper, ACCA – The Accountant of the Future (2002)

27May 2012Emerging issues and future trends in the accounting profession

Merci beaucoup