Emerging from the Global Economic Crisis “Delivering...

37

Emerging from the Global Economic Crisis “Delivering Recovery through a Sustainable Construction Industry” CIB Publication 333 ISBN: 978-90-6363-063-8

-

Upload

duongkhanh -

Category

Documents

-

view

215 -

download

0

Transcript of Emerging from the Global Economic Crisis “Delivering...

Emerging from the Global Economic Crisis “Delivering Recovery through a Sustainable Construction Industry”CIB Publication 333ISBN: 978-90-6363-063-8

EMERGINGFROMTHEGLOBALECONOMICCRISIS:DELIVERINGRECOVERYTHROUGHA

SUSTAINABLECONSTRUCTIONINDUSTRY

AreportforCIBW55BuildingEconomicsinconjunctionwith

SalfordCentreforResearchandInnovationand

BuiltEnvironmentShapingTomorrow

LesRuddockandStevenRuddock

CIBPublicationNumber:333

DISCLAIMERAllrightsreserved.Nopartofthisbookmaybereprintedorreproducedorutilizedinanyformorbyanyelectronic,mechanical,orothermeans,nowknownorhereafterinvented,includingphotocopyingandrecording,orinanyinformationstorageorretrievalsystemwithoutpermissioninwritingfromthepublishers.Thepublishermakesnorepresentation,expressorimplied,withregardtotheaccuracyoftheinformationcontainedinthisbookandcannotacceptanylegalresponsibilityorliabilityinwholeorinpartforanyerrorsoromissionsthatmaybemade.Thereadershouldverifytheapplicabilityoftheinformationtoparticularsituationsandcheckthereferencespriortoanyreliancethereupon.Sincetheinformationcontainedinthebookismultidisciplinary,internationalandprofessionalinnature,thereaderisurgedtoconsultwithanappropriatelicensedprofessionalpriortotakinganyactionormakinganyinterpretationthatiswithintherealmofalicensedprofessionalpractice.ConseilInternationalduBâtimentKruisplein25G3000BVRotterdamTheNetherlandswww.cibworld.nlISBN:978‐90‐6363‐063‐8

INTRODUCTIONThe worldwide economic crisis, starting in the latter half of 2008, has led toconcerted efforts by governments worldwide to revive the economic cycle anddevelopideasofhowbesttoemergefromthecrisissituation.Inthewakeoftheinternationalfinancialcrisisandtheensuingglobalrecession,theconstruction industrymustprepare itselfnowtoaddresstheneweconomicrealityand the sustainability imperative. Inmanypartsof theworld, the global recessionhas hit the construction industry hard. The recovery processmay be slowbut theaftermath of the recession is creating many new opportunities driven by asustainabilityandcarboneconomyagenda.At theCIBWorldCongress2010BuildingaBetterWorld, a ‘GlobalChallenge’wasput forward by the European Construction Technology Platform (ECTP) with theEuropean Commission. This report represents a response to this challenge ofaddressingtheglobaleconomiccrisis.Thefocusofthisreportisconsiderationofthequestion:Whatarethemajorforcesofchangeaffectingtheconstructionindustryandhowshould the global construction industry prepare itself to address economic andbusinesssustainability?Inevitably, theremust be an impact on the size and nature of the industry and aresponse to a changed environment due to such factors as the effectiveness ofstimuluspackages,asgovernmentsuseneworacceleratedpublicsectorspendingonbuildingandinfrastructuretostimulatetheireconomies.Especially,whentheytrytodoso"smartly" so that short termeconomic stimulus isachieved throughpositivelong term investments that, in particular, are deliveredwith green issues, such asenergyefficiency,sharplyinfocus.TherearetwopartstothisReport:Part1reviewsthecurrentstateoftheglobaleconomyandconstructionindustryinthe aftermath of the financial and economic crises of 2008 and the response ofgovernment policies aimed at achieving growth through stimulus programmesenhancingactivitybytheconstructionindustry.Part 2 displays the results of an international questionnaire survey undertaken inApril 2010. The aim of the survey was to ascertain views on the major forces ofchangeaffectingtheconstructionindustryandconsiderhowtheglobalconstructionindustryshouldprepareitselftoaddresseconomicandbusinesssustainability.ThesurveyresultswillbeusedtoinformfutureForesightworkbyBuiltEnvironmentShapingTomorrow.

PART1

THEGLOBALECONOMICSITUATIONANDTHECONSTRUCTIONINDUSTRY

STATEOFTHEGLOBALECONOMYThe economic recession of 2008‐09 has affected all the regions of theworld to agreaterorlesserextentand,asfewsectorshavebeenworsehitthanconstructionbythisglobalrecession,thestateoftheeconomiesofthedifferentregionsoftheworldwill determine prospects for the construction industry. According to theInternationalMonetary Fund (IMF)World EconomicOutlook report ofApril 20101,theglobaleconomicrecoveryhasbeenbetterthanexpectedbut,giventheseverityof the recession, the strength of this recovery is stillmoderate. Those economiesthatareshowingstronglyinthefirsthalfof2010arelikelytoremainattheforefront,asgrowthinothersisrestrainedbytheremainingproblemsinthefinancialsectors.Theestimatefor2010isthatworldoutputisexpectedtorisebyabout4.2%butthevariationinthelevelsofgrowthbetweencountriesisconsiderable.Table 1: Estimated growth rates in GDP for 2010 and 2011 (Source: IMFWorldEconomicOutlook,April2010)YearonYear%GrowthinOutput 2010 2011World 4.2 4.3Advancedeconomies 2.3 2.4US 3.1 2.6Euroarea 1.0 1.5Japan 1.9 2.0UK 1.3 2.5Emerginganddevelopingeconomies 6.3 6.5CentralandEasternEurope 2.8 3.4China 10.0 9.9India 8.8 8.4TheprojectedgrowthratesshowninTable1indicatethattheadvancedeconomiesofWestern Europe and the USA will continue to come out of recession but at aslower rate than the emerging economies, particularly China and India. Thisdistinctionbetweenthegrowthratesofthedevelopedandthedevelopingworldisacontinuation of the pattern, prevalent in the years immediately prior to therecession,when the growth rates in the emerging economieswere 4 ‐ 8% higherthanthoseintheadvancedeconomiesfollowedbyarecessionaryperiodwhichwasdeeperandmoreprolongedintheadvancedeconomies(seeFigure1). 1 IMF World Economic Outlook (April, 2010). IMF, Washington

Figure1:GlobalGDPgrowth(%quartertoquarter,annualised)(Source:IMFstaffestimates)

MaintainingtherecoveryThe continuation of growth activity remains dependent on highly supportivemacroeconomic policies and is subject to a degree of fragility as macroeconomicpoliciesbasedonatransitionofdemandfromthepublicsectortotheprivatesector(atnationallevel)andfromeconomieswithexcessiveexternaldeficitstothosewithexcessive surpluses (at the international level) take effect. The IMFwarns that, inmany advanced economies, the stimulus aspects of fiscal and monetary policiesshouldberetained in2010 inorder toprovideasupportivethrust tomaintainthelevelofactivityandemployment.Buttheseeconomiesalsoneedtourgentlyadoptcrediblestrategiesinthemedium‐termtocontainpublicdebtandlaterbringitdownto more prudent levels. They advise that governments should not start to cutspendinguntil2011,apartfromthosecountrieswithparticularlyhighdebtlevels."Akey concern is that room forpolicymanoeuvres inmanyadvancedeconomieshaseitherbeenexhaustedorbecomemuchmorelimited,"thereportstates.Whatgovernmentscan,andmust,do,ismakepublictheirplanstocutdebtlevels,itargues."Thereisapressingneedtodesignandcommunicatecrediblemedium‐termfiscalconsolidationstrategies.Theseshouldincludecleartimeframestobringdowngrossdebt‐to‐GDPratiosoverthemedium‐term,aswellascontingencymeasuresifthedeteriorationinpublicfinancesisgreaterthanexpected."FinancialSectorReformRegulatory reformof the financial sector is alsoahigh‐priority requirement.Manyemergingeconomieshaveresumedahighrateofgrowthandanumberhavebegunto moderate their stimulus policies in the face of high capital inflows. Given theprospect of relatively weak growth in the advanced economies, the challenge for

emerging economies is to absorb these inflows and nurture domestic demandwithouttriggeringanewboom‐bustcycle.ContinuingpooremploymentprospectsinadvancedeconomiesForecastsbytheOrganisationforEconomicCooperationandDevelopment(OECD)inSpring 2010 2 are similar to those of the IMF. The OECD’s Interim EconomicAssessmentreportstressesthatthemaindangerforrichcountriesisunemployment.In theUS,peopleareexpected to continue to lose their jobsat a faster rate thannewones are createduntilwell into2010. For the EuropeanUnion, thepicture isevenworsewithunemploymentcontinuingtoriseinthatregionuntil2011.A very different economic outlook is forecast for key emerging nations. China canexpecttogrowby10%,Indiabymorethan7%.Theothertwostand‐outnationsareBrazil and Russia. The OECD expects Brazil's economy to rebound and expand byalmost 5% after stagnating in 2009. Russia is also predicted to see that kind ofeconomic improvement in2010.But its turnaroundwillbeevenmoredramatic. In2009,itexperiencedoneoftheworsteconomicslumpsintheworld‐contractingbyalmost9%.These fourBRICcountriesarenotpartof the30‐strongOECDclubbuttheoneOECDmembernationwhoseeconomyshouldperformvigorouslyin2010isalsoaneasternone:SouthKoreashouldreboundtogrowby4.5%inboth2010and2011,afterendingthisyearwithalmostnogrowth.NATIONALFISCALPOLICYRESPONSESTOTHERECESSIONTheinitialresponsetothefinancialcrisiswastousemonetarypolicyasthefirstlineofdefencebutconventionalmonetarymeans(suchasnearzerointerestrates)soonreached their limits in many countries. At the November 2008 G‐20 Summit, theleadersof theG‐20countriespromised touse fiscalpolicies to stimulatedomesticdemand and many other countries have also enacted fiscal stimulus plans inresponse to the global recession. The IMF has recommended that countriesimplement fiscal stimulus measures equal to 2% of their GDP to help offset theglobal contraction3. Countries have used different combinations of governmentspendingandtaxcutstoboosttheirsaggingeconomiesbutmostoftheseplansarebasedontheKeynesianviewthatdeficitspendingbygovernmentscanreplacesomeofthedemandlostduringarecessionandpreventtheunderutilisationofeconomicresources.Consideration of themeasures employed in a selection of countries indicates thevariety and extent of stimulus programmes. The USA combined many stimulusmeasuresintotheAmericanRecoveryandReinvestmentActoflastyear,with$787bn covering a variety of expenditures from tax cuts to infrastructure investment ‐$185 bn to be spent in 2009, and $399 bn for 2010 with the remainder of thespendingspreadovertherestofthedecade.InChina,theStateCouncilapproveda$586bnstimuluspackageinNovember2008.In April 2009, Japan announced a third stimulus plan of 15.4 trillion yen stimulus($153 bn). This new plan included 1.6 trillion yen investment in low‐carbon 2 OECD Interim Economic Assessment, April 2010. OECD, Paris. 3 http://www.imf.org/external/pubs/ft/survey/so/2008/INT122908A.htm

technologyand1.9trillionyenonemploymentprogrammes.Japanhasbeenoneofthe hardest hit nations during the recession, having already experienced a lostdecadewheneconomicgrowthstagnated.Japan'stotalstimulusamountsto5%ofitsGDP.South Korea’s $10.8bn stimulus package in November 2008 included $3.5 bn forregionalinfrastructureandthe2009budgetincludedasimilarstimulus.TheEuropeanUnionpasseda€200bnplanwithmembercountriesdevelopingtheirown national plans, worth €170bn to €200bn in total. In the Netherlands inNovember 2008, the government passed a €6bnplan thatmainly consistedof taxbreaks forbusinesses thatmade larger investmentsandhired short‐termworkers.Thepackagealsoincludedanewprogrammetohelpfindworkfortheunemployed,andfasterpublicsectorinvestment. InJanuary2009,theDutchaddedavarietyofguarantees tohelpensureandencourageexports, corporate loans,andhomeandhospital construction. The UK stimulus package has consisted mainly of bringingforwardspendingplansfrom2010‐11tobeoffsetbyspendingcutsinfutureyears.In February2009,AustraliaannouncedanA$47bn stimuluspackage.Thepackageincluded A$29bn for infrastructure projects such as public housing and schoolconstruction,andA$13bincashhandoutstolowtomiddle‐incomegroups.GENERALOUTLOOKFORTHECONSTRUCTIONSECTORThe construction industry has, historically, been subject to a cyclical pattern ofdevelopment much more excessive than that of the general economy or othersectors of economic activity. The amplification of the peaks and troughs relatespartlytothe‘lumpiness’ofconstructionactivitybeingbaseduponlargeprojects.Lookingatthepatternofglobalconstructionoutputforthelastfourdecades,Figure2 illustrates that a general trendof growthhasbeenpunctuatedby cyclical peaksandtroughsovertheperiod.Figure 2: World Construction Output (US$) since 1970 (Source: United NationsStatisticsDivision:MainAggregatesDatabase)

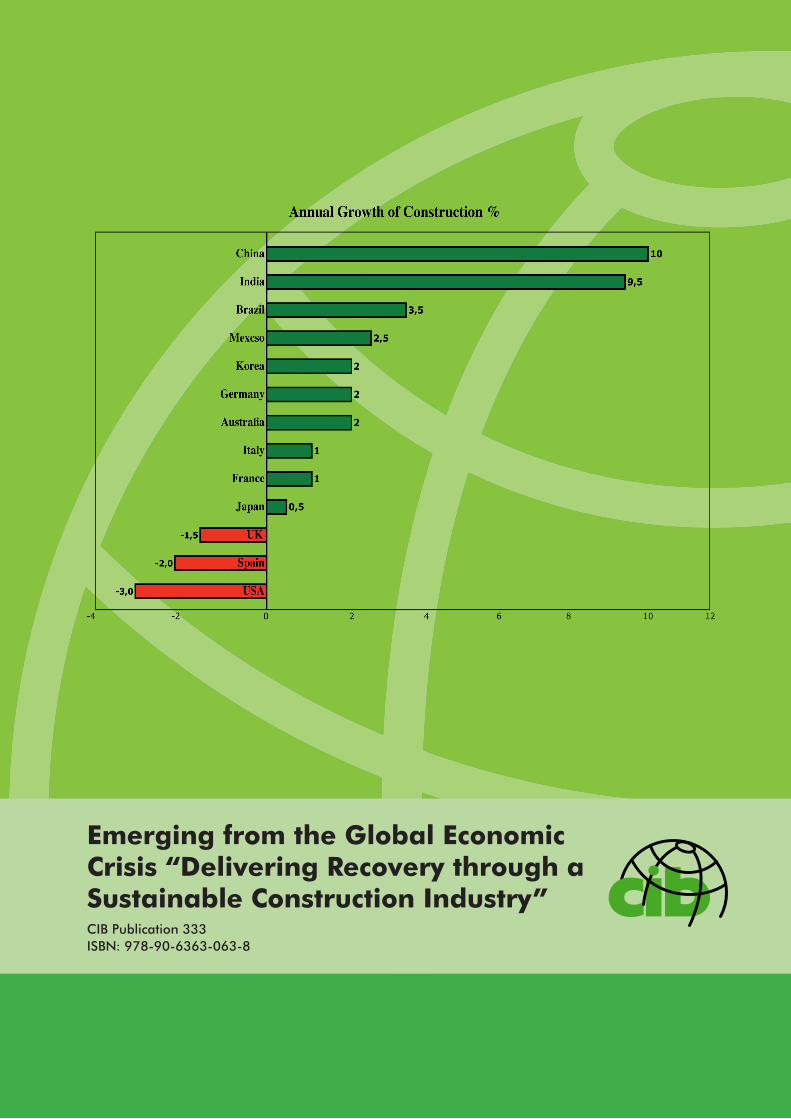

Whilsttheredoesseemtobesomedegreeofregularityinthispatternofgrowthatanaggregate level, therearemajordifferences in thepatternsat regional/countrylevel.The financial crisis has been most keenly felt in North America and Europe andconsequentlytheeffectsonconstructionspendinghavebeenmostsevere intheseregions.Figure 3: Estimatedaverageannualgrowthofconstructionspending inselectedcountries (2008‐2011) (Source: Adapted from World Construction 2009, DavisLangdonandSeahInternational)

Figure 3 indicates that the decline in activity is most severe in those advancedeconomieswiththemajorproblemsarisingfrompropertyassetpricebubbles.Chinaand India,with theircontinuinghighgrowtheconomies, leadtheway ingrowth inconstructionactivity.Developing economies now account for approximately a half of all globalconstructionspendingand,whilsttheUSAremainsthelargestnationalconstructionmarket, itwillsoonbeovertakenbyChina,which isplanningtospend$600billionfromitsreservesoninfrastructureoverthenextfewyears.Figure4showstheriseofChina and the decline of the two industrial giants Japan and the USA in terms ofglobalconstructionspendingoverthelasttwodecadesandaprojectionforthenextfouryears.

Figure 4: Shares of global construction spending (Source: IHS Global InsightConstructionService4)

Again,viewingtheUNdata(country/regionconstructionoutputinUS$)forthelastforty years, there have been vastly different patterns of construction outputdevelopmentindifferentpartsoftheworld.Thegraphsbelowillustratethesituationinselectedregions.Construction activity in Asia is generally still strong. Even though constructionspending is decelerating as globalgrowthcontracts,activity is stillhigherthan anywhere in the world. China ismaking a concerted effort to providelow‐costhousingonavery largescale,has an industrial growth rate wellabovetheworldaverageandismakingconsiderable infrastructure investmentin its under‐developed regions eventhoughtheslowdownintradewiththeUSA and Western Europe has had aneffect.India iswell placed to avoid theworstoftheeconomicrecessionandconstructionactivitymayalsokeeppacewiththatofChinaatalmosttenpercentbut,inrealterms,thesizeofitsconstructionindustryisonlyaroundaquarterofthatofChina.Japanisagaininrecessionand(asshowninFigure 4) the level of construction activity can be expected to continue to bedepressed.

4 ‘China Construction’ IHS Global Insight 2009.

From the late 1990s until 2008, therehad been a low but steady rate ofgrowth in the European constructionindustrybut in2009, therehavebeenmajor falls in activity in WesternEurope, where the most significantdownturns have been in the UK,Ireland, Spain and Italy, where thehousing market is particularly weak.but there has been some growth inEastern Europe, particularly ininfrastructurespending.Businesses are cutting investment inresponse to tight credit conditions,depressed demand and decliningprofitability and it is unlikely thatactivitywillgrowagainin2010.In Australia, the construction industryis feeling the fallout of theweakeningglobaleconomyand,asintheUSAandseveral countries in Western Europe,there has been a bursting of thespeculative housing bubble, whichleavesinfrastructureasthekeyactivitydriver.In South America, as in Europe, thereare significant differences in thesituations of different countries. Theaggregate trend for the region hasbeen cyclical over recent decades butBrazil’s economic growth and the useof oil money for infrastructurespending in Venezuela are positivefactorsfortheindustry.The growth in construction activity inAfricasincetheturnofthecenturyhasbeen largely based on a massiveexpansion in infrastructure provision.InvestmentfromChinaandtheMiddleEasthavebeen(andshouldcontinuetobe)amajorfactor.RECOVERYINTHECONSTRUCTIONSECTORRecoveriesfromrecessionsassociatedwithfinancialcrisestendtogeneratelittlejobgrowth, largely because of the dependence on bank financing of employment‐intensive sectors, such as construction. It follows that restoring the health of

financial systemswillbeneeded tomakean importantcontribution to recovery inthe construction sector. In addition, policymakers need to consider innovativeprogrammesthatfacilitateaccesstocapitalmarketsforthesmallandmedium‐sizeenterprises,whichpredominateintheindustry.IHSGlobalInsight5predictsthattheglobalconstructionmarketwillreturntogrowthin 2010, with a stronger rebound in 2011. This optimism is based on ‘AsiandynamismandNorthAmerican resilience’producingglobal constructiongrowthof5%orabovein2011or2012.Wherewillthegrowthcomefrom?With a decline in residential construction spendingworldwide of around 10% andnon‐residentialconstructionof5%,theboostofstimuluspackagesforinfrastructureistheobvioussourceofgrowth.The‘GreenStimulus’Stimuluspoliciescameaboutinthewakeofthefinancialcrisis,asgovernmentssoughttofindprojectsonwhichtospendmoneythatwouldcreatejobsasquicklyaspossibleandmanygovernmentspaintedtheirstimulusspendingas“green”,partlyinanefforttomakegoodontheirrhetoriconclimatechangeandalsoasawayofreducingtheirrelianceonimportedenergy.ArecentWorldBankstudy6estimatedtheextentofstimulusspendingwhichhada‘Green’componentandwhichwasinthe‘buildingefficiency’category.Table2showstherelativelackofprovisionof‘greenbuilding’stimulusincountriessuchastheUK,FranceandJapancomparedtoSouthKorea,whichhasthelargestgreenbuildingefficiencystimulusofanypackage.Globally,thegreeneconomicstimulushadachievedlittlebytheendof2009,withonlyafractionofthemoneypromisedforenvironmentalprojectsbeingspent,accordingtoastudybytheHSBCbank7.About£56bnofpublicsectorstimulusfundswerespentlastyear,or16%ofthetotal.Ofcourse,themajornationalstimuluspackagelastyearwastheObamagovernment’sRecoveryandReinvestmentAct,animportantaspectofwhich,wasthe$5bn‘WeatherizationAssistanceProgram’(installingweather‐tightwindowsanddoorsinlow‐incomefamilyhouses)but,aftercripplingdelaysduetofinancialadministrationandsupply‐sideissues,theprogrammeonlyretrofittedafractionofhomesandcreatedfarfewerconstructionjobsthanexpected.

5 IHSGlobalInsight.com/Construction 6 ‘Green Stimulus, Economic Recovery and Long-Term Sustainable Development’, The World Bank Development Research Group, Environment and Energy Team. Policy Research Working Paper 5163, January 2010. 7 HSBC Global Research, April 2010.

Table2:Green‘BuildingEfficiency’componentsofdirectstimulusprograms(Source:WorldBank)Region /Country

PeriodYears Totalstimulus (in$USbillion)

Green ‘BuildingEfficiency’stimulus (in$USbillion)

Green‘BuildingEfficiency’stimulus (as %oftotal)

AsiaPacific

Australia 2009‐2012 26.7 2.48 9.3Japan 2009onwards 485.9 12.43 2.6SouthKorea 2009‐2012 38.1 6.19 16.2Africa

SouthAfrica 2009‐2011 7.5 0.1 1.3Europe

EuropeanUnion

2009‐2010 38.8 2.85 7.3Germany 2009‐2010 104.8 10.89 10.4France 2009‐2010 33.7 0.83 2.4UK 2009‐2012 30.4 0.29 0.9Other EUstates

2009 200.6 1.2 0.6Norway 2009 2.9 0.2 6.9Americas

Canada 2009‐2013 31.8 0.24 0.8Mexico 2009 7.7 0.75 9.7USA 10years 972 30.74 3.2In the UK, in the run‐up to theMay election, themain political parties were stillfailingtodetailhowrenewableenergyinfrastructurewillbepaidforandtherehasbeenmuchscepticismintheindustryabouttheimpactoftheproposed£2bnGreenInvestmentbank,withtheInstituteofCivilEngineers,forexample,puttingafigureontherequiredinvestmenttotacklethescaleofthetaskat£40‐50bnperannumandadvocatingtheneedforaNationalInfrastructureInvestmentBankabletodrawon domestic and international capital markets and pension funds to raise thenecessaryfunds.In many countries, measures to encourage sustainability need to be aimed athouseholders. If private householders are to be persuaded to make efficiencysavingsintheirownhomes,therewillalsobeaneedforincentives,withideassuchas a personal tax credit for home improvements and renovations that increaseenergyefficiency (with theattraction that itmight inducesomehealthyborrowingby financially strong people with good credit ratings, to whom even the mostcautiousbankwouldbeconfidentinlending)oran‘eco‐cashback’schemetorewardpeople whomake energy efficiency improvements in their homes. In the currentclimate,aconsolationformanysmallcompaniesisthatthereisalimittohowmuchmaintenancespendingcanbecut,evenifnewinvestmentisslashed.Housingrepair

andmaintenanceworkisbeingmaintainedbutwouldbegivenawelcomeboostbyaninnovativeenergyefficiencyrewardsystem.If the period of recession in the industry in this downturn is to be limited, a vitalquestionis:Howlongwillittakeforstimuluspackagestobearfruit?

PART2

RESULTSOFANINTERNATIONALQUESTIONNAIRESURVEYONTHEECONOMICCONTEXTOFTHE

CONSTRUCTIONINDUSTRYThestudyisaimedatansweringthequestion:Whatarethemajorforcesofchangeaffectingtheconstructionindustryandhowshould the global construction industry prepare itself to address economic andbusinesssustainability?ThesurveywascarriedoutinApril2010.Therespondentstothesurveyrepresentedavarietyofopinionfromtheinternationalconstructionsector.Betweenthem,theycommentedfromthecontextofsixteendifferentcountries,viz:Africa:NigeriaAsia:ChinaandPakistanAustralasia:AustraliaEurope:Denmark,France,Germany,Italy,Netherlands,RepublicofIreland,UK,Spain,SwedenandSwitzerland.NorthAmerica:USASouthAmerica:BrazilA‘SummaryandKeyPoints’isfollowedbyalisting,foreachindividualquestion,ofthe issues raised in respondents’ comments, which are itemised under relevantcategories and the list of bullet points represents the more commonly (i.e. byrespondents from several countries) made points in that category. Most of thecommentsaregeneralintermsofapplicabilitybutcountry/regionspecificissuesareincludedandareindicatedassuchinthetext.

SummaryofandkeypointsfromthequestionnaireresponsesIn terms of pivotal events, the financial and economic crises, with the failure offinancial institutions, brought into focus the importance of the financialmarket inproperlyfundingthepropertyandconstructionmarkets.Catastrophesanddisasters,such as tsunamis and earthquakes, along with global warming, are factors thatimpactgreatlyontheconstructionindustryand,howtheindustryrespondstosuchevents,willbeevidentinthenearfutureasinfrastructuresincountriessuchasHaitiare rebuilt. Market conditions can change very quickly and collaborativeworkingpractices coupled with internationalmergers and acquisitions have led to intensecompetition in the national and international construction market. Thebreakthrough of energy efficient building methods and technologies has beenprevalent worldwide and this is an area that will continue to advance as clientsactively engage in change and innovation. The cost and availability of energyresourcesandrisingmaterialcostshavebeenandwillcontinuetobemajor issuesfortheglobalconstructionindustry.Thekey challenges facedbythe industryappeartovarythroughouttheworldbutsomecommonthemesareapparent. In theaftermathof theglobal financialcrisis,theneedtodevelopnewfinancialmodelshasbecomeimperativeinmanycountriesand theavailabilityof financing isavital challenge. Financial issuessuchasweakbanking and financial institutions in many countries and high interest rates andinflationinothercountries(suchasPakistan)needtobeaddressed.Cashflowsandsecurity of payment are causing concern for business sustainability. In terms ofenvironmentalsustainability,minimisingthecarbonfootprintthroughrefurbishment,redesignandredevelopmentwerehighlightedasparticularlyimportantchallengesinWesternEurope,wherethechallengeistotargetrenovationandretrofittingofolderbuildingstock.Itisrecognisedthattrainingskills,workingpracticesandstrategiesallhave an important role with regards to the future shaping of the industry. Thedevelopmentof integratedsolutionsandBIMareneeded toprovidenewbusinessmodels. Greater stimulus isneeded for thehousing sectorand there is aneed tosustaintheconstructionofgoodquality residentialbuilding.For instance, inBrazil,thecreationofadequateconstructiontechnologiesfor lowincomehousing isseenasamajorchallenge.To deal with the challenge of ensuring business sustainability, the constructionindustryneedstobemoresustainablyconscious.Flexibilityandtheneedtodevelopcapabilityforchangearethemainissues.Maintenanceandadequateprofitlevelandtheretentionofreliablecorebusinesswillbeparamountinthecurrentclimateandafocus on a proper analysis of risk is becoming essential as firms have to ensuresurvival.Becausemanycompaniesareunsureoffuturework,thismakesexpansiondifficult; one solution is to concentrate on the domestic market rather than theriskier international one. Government policies on environmental issues andregulations on sustainability will see construction firms being required to reactappropriately intheirbusinessoperationandstrategy.The industryhastobecomemore sustainably conscious, needing to focus on issues such as the environmentseriouslyandnotmerelyasamarketingapproach.In order to assist the construction industry in pursuing an economic sustainabilityagenda, a green stimulus programme needs to be based around subsidies, grants

andregulations.Asubsidytoencouragehomeownerstoundertakeenergysavingisan obvious measure directly linked to sustainability. The encouragement ofinvestment in new, energy‐efficient infrastructure to replace inadequate ageinginfrastructure would greatly boost construction activity and promote economicgrowth. Public sector intervention and investment is required in transport andenergy generation infrastructure in order to optimise the economic andenvironmental impact. The short‐term orientation of stimulus programmes wascommentedonbymany respondents.The industrymusthavea longer‐termfocuson investment in order for the sustainability impact to be significant. There is anexpectation that construction industry activity will move significantly into retro‐fittingtheexistingbuildingstocktogetherwithatransformationofenergyefficiencyandemphasisonthesocialaspectsofthebuiltenvironment.Theimportanceofthedevelopmentofskillsandtechnologyinordertosupportstimulusprogrammeswasalsonoted.The state of the economy was generally recognised as the key force in drivingchangeinmostpartsoftheworld.Copingwiththesituation,inwhichthelowlevelof demand for construction work was endemic, was a feature of the responses.Although, in some regions, the maintenance of foreign investment to continuefuelling demand was apparent. Government spending on projects such as roads,powerstationsandotherphysicalinfrastructureisavitalfactorindrivingchangeinthe industry. Population increases and an ageing society are having a significantimpact on the focus of the industry. Improvements in energy efficiency,sustainability and the regeneration/retrofit of existing building stock are majordrivers in most parts of the developed world. Methods of controlling cost andfinancingprojectshavealwaysbeenkeyforcesindrivingchangeintheindustry.Respondents were asked to specifymajor issues and trends that will affect theindustryoverthenext20years.Populationgrowthparticularlyinurbanareasandaneed to meet the needs of an ageing population were recognised as majordemographic factors. The speedof economic recovery and the consequent lackofgrowth was a common concern and a general trend in cutbacks in public sectorspendingwas recognised as inevitable inmany debt‐riddendeveloped economies.Oneparticulargovernanceissuewasthedegreeofregulationandcontrolthatcouldhindertheoperationoftheindustry.Thegrowingemphasisonlowcarbonsolutionsand sustainable use of the environmentwill increase but therewas concern overeconomicpressureswhichmayforceamoreunsustainableapproachontheindustry.Responses on social/cultural trends focused on increased globalisation and thechangingagestructureforsocietyasawhole.Intermsoftheindustryitself, itwasrecognised that work was becoming more interdisciplinary and international andrequired more integrated project teams and project delivery. Technologicaldevelopmentswillrequirenewwaysofinteractiontosupportpeopleandprocesses,withemphasisoncreatingvalueforclientsandthemovetogreenertechnologywillcauseaparadigmshiftasitbecomesadoptedbytheconstructionindustry.As far as innovations, opportunities and initiatives that need to be explored areconcerned, the re‐use of resources, recycling and refurbishment and life cycleadaptabilityareinitiativesthatarecurrentlybeingimplementedandwillcontinuetobe for the foreseeable future. Green technologies and energy efficiencywill alsocontinuetobeexploredbytheconstructionindustry.

Question1Whatpivotaleventsfromthepastfewyearsprovidegoodlessonsforthefutureoftheglobalconstructionindustry?EconomicandFinancialCrisis

• The 'credit crisis' and the creation of the property and asset pricebubble/cycle.

• Certainly the sub prime crisis and themortgage crisis originating from theUSA.

• Global economic recession showed the inability of financial institutions toperformtheirrolesproperly.

• The financial crisis showed that the level of activity in the industry is notdeterminedbysupplyanddemandforhousingorotherbuildingsbutalmosttotallybytheavailabilityandcostoffinance.

• Over‐inflatedsaleandleasepricingmechanisms.• Overspendingofpublicclientsonbiginfrastructuralandprestige’sprojects.• Efficiencyandperformanceduetoeconomiccollapsewhichhasnotslowed

theincreasingdemandsofowners.• Financial boom in the first instance (particularlywith amore confident EU

anddevelopmentsintheMiddleEastandFarEast),followedbysharplessonslearntinthecurrentfinancialbust.

CatastrophesandDisasters

• World‐widenaturaldisasters‐suchastsunamisandearthquakes.• Extremeclimateevents'impactonbuilding.• We need to be aware of the urgent need to address the issue of global

warming. In this respect the failure of the Copenhagen summit is perhapsalsoaneventwithimportantlessonsforus.

• Terrorattacks‐9/11.MarketsandCompetition

• Marketconditionscanchangeveryquickly.• The discovery of collusion ‐ cases in several countries.

In fact, crisis‐situations can/should bring new food for thought and lead toactionsof 'restructuringtherulesof thegame',creatingarealshake‐outofbad/non‐professional players in the field and giving the remaininggood/professionalplayersafairchancetoimprovetheirbusinesses.

• Giventhe intensecompetition in thenationalconstructionmarket, the firstlesson would be to pull out of the market; the second one is tointernationalizethebusiness,andthethirdonetolookforanichewithlessercompetition.Allarepainful.(Germany)

• Developmentofnewbusinessfields.• Tendencytointernationalmergersandacquisitions.

• Collaborativeworkingpractices.TechnologicalChanges

• The breakthrough of passive and energy efficient building systems andtechnologies. Clients are actively engaging in change and innovation.(Sweden)

• Advancementsinnanotechnology.• The building industry during the past few years has abused of the use of

labour on site. In the future more industrialized systems should be used.(Spain)

• Internet,communications.CostandAvailabilityofResources

• Oilcrisisandrisingenergycosts.• Riseinmaterialcosts,riseincostsplots.• Foodshortage,watershortageandmaterialsshortage.• GlobalsupplychainQC/QA.

Question2Given the uncertainty of the current business climate, what are themost pressing challenges facing the construction industry in yourregionoverthecomingtwodecades,andwhatstepscantheindustrytake to anticipate and prepare for the future? (Please indicate yourregioninyourresponse)FinancialIssues–AvailabilityofFinanceandFinancialStrategy

• Gettingtheeconomybackintogrowthmode.• Availability of investment and development funds. Government income

shouldbeavailableforinvestmentinphysicalinfrastructure.• Thebanking industry is flaky.Boomandbustcycleshavenotgoneawayso

alwaysbepositionedsoyoucandownsizefast.• Lackoffinancingavailableforhousingcouldfacesometrouble.• Capitalallowancegrantaidshouldberestored.(UK)• Themainchallengeistostayinbusiness.• Financial institutionshavebecomeweakenedto theextent thatperforming

their roleshasbecome restrictive and counterproductive to the growthoftheindustry.(Nigeria)

• Concernsoversecurityofpaymentmustbeaddressed.• Sustainabilityofpublicsectortenders,mostconstructioncompaniesdepend

on government jobs. Cutbacks in public spending on capital investmentprojects.

• Highinterestratesandinflation.(Pakistan)Sustainability

• Newchallengesinsustainableconstruction(social,economicandecological).Thisrequiresustothinkofconstructionasaglobalactionandnotonlyasasumoftechnicalfields.

• Minimising carbon footprint through refurbishment, redesign,redevelopment.

• It isessentialthatemployeesandmanagementaretrainedtothestandardstomeetapproachingsustainableconstructioncriteria.Thegovernmentcouldhelp through investment in training for elements of work in the area ofsustainableconstructionusingdifferentmaterialsandprovidingtherequiredimprovementinqualityofwork.

• Constructionsector isprobablythemost important intheeconomy,forthenext10yearstomodernizebuildingsandconstructnewenergyefficient.

• Attainmentofsustainabilitygoalsthroughsystemicviewandplanning.• Dealing with environmental issues (toxicity, scarcity of materials & fossil

energy).• Contractorsare seriouslyconsideringhowto realize lowcarbonbuilding, in

my country, frightenedby their appeal on their clients, probably unable toweighthighercostsagainstsimpleenvironmentalplus.(Italy)

• Theconstructionindustryshouldfocusitsactivitytowardrehabilitation,duetothehighnumberofrecenthousingbuildings.(Spain)

• Developingaresponsibleattitudetosustainability.RetrofittingofBuildings

• Challenges regarding retrofittingofexistingbuiltenvironmentsanda largerintegrationandresponsibilityofsocial,culturalandarchitecturalvalues.

• There is a substantialneed for renovationand retrofittingofolderbuildingstock. We need to move from an industry primarily oriented to thedemolitionandreplacementofolderbuildingswithnewbuild,toanindustrythatcanearnitswaythroughrenovationandretrofitting.

• Decreasingroleofnewconstructionversustheincreasingroleofbuiltstocksofbuildingsandinfrastructure.

• Improvingexistingbuildingstock.Trainingskills,WorkingPracticesandStrategies

• Thenatureofemploymentstatusandworkingconditionsinconstruction,therestructuringofthesectorsuchthatcompaniesreducetheircommitmenttoconstruction activities and seek diversification, and a more reflectiveapproachtowardsincreasingprofessionalisation.

• The development of the competencies of craft and small enterprises; thedevelopment of integrated solutions + BIM; the collaboration between theactors of the property and construction industry (fromdesign to operationandmaintenance).(France)

• Learningtocollaborate;uptakeofrelationalcontracts;convincingclientsthatthey never can buy at lowest cost and that lower costs come fromcollaboration.

• Sustainingemployment,skills.• Knowledgetransferprogrammes.• Basicallyatpresentthereisaneedtofocusonotheraspectsofwork.Other

options include merging, becoming strictly management contractors,reducingskillsbase,improvingbusinessstrategytocutoutwaste.

• Shortagesofskillswillariseagain,oncetheeconomyrecovers.• Tocompensatetheoverlyretirementwithautomationandinwardmigration

ofskilledlabour.• Integratedplanningandnewbusinesslogics.• Taking actions in a strong focus on client's wishes and expectations;

Beingactiveasarealquality‐player.• Improving knowledge/experiences and skills, continuously working on the

professionalization.• Demonstrating that we supply real value for money and building with a

qualityguarantee.(TheNetherlands)• Changeprocurementsystemsothattheclienthaslesspowerindrivingdown

pricesandthuspurchasingminimumquality.(Germany).• Continuousadaptiontothemarket.

• Quality contractors and designers. Loss of expertise in the workforce.Contracts.Reduceclientresourceswithincreasedrequirements.

• RaiseindustryprofessionalismandlobbyGovernment.• Winningandsustainingbusiness.

HousingandtheHousingMarket

• There is a need to sustain the construction of good quality residentialbuildinginordertosatisfydemand.(France)

• Our most pressing challenge is in create the adequate constructiontechnologyforthelowincomehousingfederalprogram.(Brazil)

• Stagnationinthehousingmarketandthedeclineinhousebuilding.Greaterstimulusisneededforthehousingsector.(UK)

• Challengesforthescaleofurbandevelopmentrequired.(Sweden)Question3Economic turbulence presents major challenges to the constructionindustry and businesses are placing increasing emphasis on theirongoing business sustainability. This implies a simultaneous focus on

economic, social and environmental performance. What are thechallenges, facing construction organizations in having to makestrategic, structural, financial and operational changes in thisenvironment?FlexibilityandDealingwithChange

• The major challenge is to close the efficiency gap, between what can bemadeandwhatisactuallymadeonabroadscaleandtotakeamoreholisticapproach including social and cultural issues to the existing competenceofmakingenergyefficientbuildings.(Sweden)

• Thechallengesarethesameonesthathaveexistedforthelastcentury.Howyoucandevelopandgrowyourbusinesswhilstmaintainingflexibilityinyourfixedcostssoyoucanupanddownsizeasdemandboomsandbusts.

• Maintain technical performance although job reduction policies, adapt tochangingcontext(climate,financialcontext,changesinnormsandextendingcompetition).

• Economic: staff layoffs, redistribution of responsibilities, more efficientstructures considering reduced working week, hot‐desking, multi‐taskoperatives, investor financial options, and rebrandingas appropriate to themoresustainableethosmodels.

• Unfortunately,theevidencesuggeststhatthepremise(wiseadvicealthoughit is) is false. Most businesses are likely to adopt extremely short rangethinkinginresponsetothecurrenteconomicdifficulties.THEchallengeistogettheindustrytoadoptthelongrangehorizonimplicitinthequestion.

• Beingflexibleandalert;Lookingforwardtoopportunities,whichmightcreateaddedvaluetothebusinesses.

• The complexity of the 21st century economy, effects of amore globalisedeconomy, emerging economies, labour market issues and effect on theconstructionsectortoclimatechangeresponses.

• Thegenerallylowcapabilitytochange.• Todevelopcapabilitiestomakechanges.• Pace of change. Organisational behaviour may not fully reflect ongoing

environmentalchange.• Havingvisionandnotjustkeepingthesamepractices.Beingresponsibleisa

challengetosome.MaintainingProfitsandSurvival

• Themainchallenge:nottobuildcheaply,quickly,inordertomaximizeprofitsandthecostofbuildinguserstoupload.Willdesignandbuildsustainable.

• First and foremost: looking for continuity, survival on the long term. Butparallel: how to develop newbusiness cases that providemeaningfulworkforemployees,society,clientsandend‐users.

• Abetterknowledgeofwhataretheimplicationsofthesethemesindecisionmaking.Usually,thebuildersanddeveloperssupportthesedecisionsontherelationsbetweencostsandprices(profits).

• Profitmarginswill be squeezed for the foreseeable future.Maintaining thematerials supply sector in anticipation of the economic upturn could be amajorproblem.

• Constructioncompaniesfightforsurvivalandhaveonlyonegoal:minimumprofit.Iproposetogivethemthroughbetterpricesapossibilitytocareaboutsustainability.

• Retainreliablecorebusiness.UncertaintyandRisk

• Toconcentrateondomesticmarketsortoventureintoriskier(perhapsmoreprofitable)internationalmarkets.

• Riskabsorptioninthecompetitiveprocess.Contractorsmoreinneedofworkbecome unrealistically aggressive in proposals and hurt more businessreasonablecontractors.

• Manycompaniesarenotsureaboutfutureworkasaresulttheycannotplanforfutureexpansion.

• The risks need to be forecasted in time and proper risk analysis to beconductedtocomeupwithcontingencyplansandimplementation.

GovernmentPolicies

• Bringingregulationsintolinewithsustainabilityexpectations.• Topre‐meetthetighteninglegislation.• Ithinkconstructionorganisationshaveoftenwaitedtoseehowgovernment

policies are changing before launching into new markets. So, the currentinterest in climate change and environmental agendawill see constructionorganisations aligning their business streams accordingly. I already observeconstruction companies entering into collaborative arrangements with theenergy and waste sector and this will have implications in terms of whatconstitutes their core business and future funding streams. PPP/PFIarrangementswillcontinuetobeused,albeitunderadifferentguise.

SustainabilityConscious

• Tocreatemoresustainabilityconsciousbusinessesandsegments(onatopofthecompulsorychanges).

• If focusingonenvironmental issues, thendo itseriouslyandnot justdrivenbymarketing/hypes,butfromastrongseriousconvincedattitude.

Question4Afeatureofmanygovernments’economicrecoverypoliciesinthefaceof the global economic crisis has been the use of economic stimulus

activities,whichhave,atthesametime,environmentalandeconomicgrowtheffects(agreenstimulus).Whatfeaturesofsuchplanswillbeeffective in assisting the construction industry to pursue asustainabilityagenda?Subsidies,GrantsandRegulation

• In principle, businesses just running via subsidies/economic stimuluspackagesareoftennot feasible.Nevertheless,asa first step suchpackagescancreateagoodboost.

• Subsidisingprivatehouseownerstoundertakeenergysavingmeasures.• Governmentsponsoredcapitalspendprogrammes.• CapitalallowanceprogramsforLZCtechnologies.• Grantaidtopromotesustainabledesignservices.• Thedevelopmentofnewfinancingsolutions.• Controllingthepriceofhousing.

InvestmentinInfrastructure

• Ifthatmoneyisusedtorebuildthecrumblinginfrastructureinpresentcitieswouldbeahugesupportforconstruction.

• EuropeandNorthernItalyinparticularhaveahugeassettoberefurbished.ContractorshaveobtainedsomethingfromItaliangovernmentbutforaveryshort time.Construction industryneedsa longterm initiative, tocontributeto the reduction of human environmental impact and to produce a stableeconomicgrowth.

• For big interventions (roads, energy generation, hydraulic, oil and gas) thegovernmentinsistsonthesustainabilityaspectsofeachproject.

• Thepublicsectormustinvestmoreoninfrastructureprojects.IneffectivenessofStimulusProgrammes

• The construction industry needs long‐term public investments, not stimuli(thoughtheyarewelcomenow).Stimuluspackagesareshort‐termoriented.

• Longtermfocus‐inordertomaketheindustrychangeentirely,peopleneedtobeawarethisisnotashortintervention,butistheretostay.

• Nobecausestimuluspackagesareeverythingelsebutsustainable.• Short term the impactwill be significant. But long term itwill weaken the

sustainabilityagendaasthefundsdecreaseoraremovedtothe latestbuzzwordeffort.

RetrofitandtheLife‐cycleApproach

• Plansthathaveawholeoflifecycleapproachanddemonstratesustainabilitybyminimisingimpactontheenvironment.

• Retrofitting the existing stock (keeps the smaller guys in business);confrontingclientswhoarenotwillingto'gotheextramile'tofutureprooftheirnewbuildings.

• Asnewconstructionseemstofindeconomyinnewprojects,thefocusshouldbeonstimulusspendingonretrofittingandtransformationregardingenergyefficiencyandsocial issues inexistingbuiltenvironmentsespecially inareaswith lowpurchasepower,eventhoughthis is themostdifficultarea togetpayback. The financial systems for financing the retrofitting of housing ineconomicallydeprivedareascouldbeimproved.

TrainingandEducation

• Cancreateanartificialboomthatresults inanotherrecession.Must lookatreal productivity issues and creating training schemes to educate lowerskilledpeopletodosomethingusefulforalongerperiodoftime.

• Necessitytofocusontheeducationofpeopleworkingforthepropertyandconstructionindustry.

• Anysuchplansmustbestrategic.At themoment, Iobserve that it ismoretactical than strategic and dedicated largely to technology development.Whilstthisisimportant,oneshouldalsoconsidertheskillsissuestofulfilthegreenagenda,aswellassupplychaininfrastructurethatcompaniesneedtodevelop. So, the stimulusmust also ensure the sustenanceof such aspectsthroughe.g. theeducationsystemtosupportdevelopments in theseareas.(UK)

Question5What,generally,arethekeyforcesdrivingchangeintheconstructionindustryinyourregion?

EconomicGrowth• Lackofeconomicgrowthandlowlevelofdemand.• EconomicgrowthandtheforeigninvestmentthatconsiderBraziloneofthe

topeconomiestoinvestinrealestate.GovernmentPolicyandSpending

• Governmentspendingonphysicalinfrastructure.• Government policies, economic trends and dwindling patronage of

professionalsbytheprivateandpublicsectorsclients.• Infrastructureprojectssuchasroads,powerstations,buildingwork.• NationalAssetManagementAgencywhoisbuyinguptoxicdebtaccumulated

fromoverdevelopmentundersold/leasedbuildingstock.Sustainability,EnergyEfficiencyandRetrofit

• Improvements in energy efficiency based in economic terms for newconstructionandintheredevelopedinnercityareasoflargercities.

• Appropriatefinancialandenergyresourceuse.• Future lines of renovation, maintenance & operation vis‐a‐vis stocks of

buildingsandinfrastructure.• Performances in terms of energy and acoustics.

Aseriousconsiderationabouttheopportunitytobegreen,somehow.• Thesustainabilityagendaandperhapsglobalisation.Companiesthatareable

to capitalise fromopportunities abroadwouldbe able to contribute to netGNP.

Demographics

• Increaseinpopulationandtheageofmarriage.• Demographicchangeandanageingsociety.

CostsandFinance

• Thekeyforce,ifitisaforce,isthelackofmoney,sonotmuchconstructionwork isgoingon. It isnotabadtimetobemicrocompany,working locallythrough word of mouth marketing. Of course that is only good if thecustomers have money. Going off government policy and energyconservation, Iperceivethatpolicy isthedriverandtosomeextentretrofitthesolution.

• Selectionofeconomicmost favourablebid,basedon life‐timeperformancecriteriaandintegrateddesignandconstruct.

• Fightingforsurvivalforcontractors/designfirms.• Achievingasustainablemarginina'moreforless'market.• There is high demand of investment in power generation sector, housing,

infrastructureotherfacilitiesbuthighinterestrateisabigproblem.

• Clientdrivenchangesandeconomicnecessity.• Offsite,prefabrication, innovativewaysofsolvingproblemssuchascheaper

importedproducts.Question6Under the following six headings identify specifically two or threemajor issues and trends that you feel will affect the constructionindustry globally and regionally over the next two decades. i)

Demographic ii) Economic iii)Governance iv) Environmental v)Social/Culturalvi)Technological.Demographic

• Ageing people, increasing need for other type of products/projects.Healthcare‐developments, also leading to other needs for the builtenvironment.

• High rates of migration to the UK from Africa and Asia with increasedpressureoninfrastructurecausedbythepopulationincrease.

• Achangeinsizeofflats,flatsthataremoreadaptedtoelderlypeople.• Growthoftheurbanpopulation.• HIV/Aidsandmorepeoplewillmigratefromeconomicallydepressedareas.• Seriousproblem,it’sanexplosion.Halvethepopulationandnoproblem.• Humanpopulationupbutasymptotic.• Intensecompetitionamonghighlyqualifiedyoungprofessionals.• Needsandlabour/staffavailability.

Economic

• Encouraging clients to collaborate to enable constructors to have a steadyflowofworksothattheycankeepintegratedprojectteamstogether, learntogetherandsteadilybringcostsdown.

• Economicgrowth(orlackofit).• Tensionbetweensustainabilityandconsumption.• An up and down recovery so lack of lending, house prices could go

up.(UK/USA)• Dramaticcutsparticularlyinpublicsector.• Affordabilityandfinancing.• Lack of investment capital. Different situations for 'starters' in housing

markets.• ShiftineconomicpowertoChinaandIndiawillmeangrowthininfrastructure

spendinginthesecountries.• Inmanycountries,cutbacks inpublicsectorspendingwilldrasticallyreduce

workload.• More cooperation between big groups and SMEs; SMEs have to look for

bettercapitalisationofthecompany.• Nomoney for capital projects and unwillingness for banks to finance new

projects.• Thedeclineintheworthofthepoundandrisinginterestrates/inflation.(UK)• LCCencouragingadifferentviewofrisk.

Governance• Dialoguewithlocalcommunitieswillbeessential.• Achange ingovernmentcouldquiteeasilyundoanygoodrecoverywork in

sustainableconstruction.• Increasingtensionincountryduetorisingprices.

• Corruption!• Lack of clarity in regulations, leading to a 'wild' growth of different

rules/standards/etc.Unprofessionalattitudeinthegovernmentaldepartments,creatingariskforuncontrolledprocedures(thedilemmabetweenlessrulesandmorecontrol,etc.).

• Developmentofperformancebasedapproaches.• Moregovernmentswillbebankrupt.• Ensuing that project governance supports the optimisation of a project

overall.• ThepoweroftheEUisbeingtested,butalsothechallengesofamoreglobal

marketplace(alsotheriseoftheFarEast).Environment

• Increasingemphasisonsingleplanet livingwhetherthere isglobalwarmingor not; increasing need to protect good arable land to feed the growingpopulationwithconsequentfallinnumbersoflivestock.

• More legislation in this area, but also a more reflective approach by theindustry.

• Systemthinkingontheurbanandcitylevel,holisticapproaches.• Environmentalpressuresarebecomingextremeandburdensome.• Carbonsinkreductionwillcauseaglobalstink.Fightsovermaterialresources

willoccur.Thecostofconstructionwillgoup.Withmyglasshalf full therewill be peace and the majority of construction will be to the ideology ofsustainable construction, therefore cutting out waste, using alternativeconstructionproductsand80%recycledmaterials.

• Increasingcostoffuel.• Likelihoodofmoreunforeseencatastrophes.• If the present eco‐hype is just seen as hype, then it is a short‐time thing,

creatingalong‐termrisk.Backtoreality(apartofhypes,etc.)isneeded.• Carbonabatement.• Changesinclimaticconditions.• Energyandwatersaving,emphasisonlowcarbonsolutions,LCCapproaches.• Moreunsustainableuseoftheenvironmentwillbeontheincrease.

Social/Cultural

• Changing the culture of the industry to focus on collaboration; findingintegrated ways to teach built environment professionals so that they canparticipate effectively in integrated project teams and integrated projectdelivery.

• Globalisation and perhaps more involvement by the industry in the localcommunity.

• Bottom‐up processes, participation, safeguard and develop cultural,architecturalandsocialvalues.

• Socially people in the younger age groups are becoming more and moreuselessatpracticalandsustainablelivingskillsandwon’tbeabletosupporttheolderretiringones.

• Globallydevelopingcountrieswillstarttouseresourcesata levelsimilartodeveloped,causinginflationinconstructioncostintheU.K.Morewomenwillworkintheconstructionsector.Theworkforcecouldbebetterequippedtoworktosustainableconstructionstandards.

• Apathy/hostilityofpublictowardspolitics/politicians.• Cross‐managingcapabilities.• Differentwaysoflivingtogether(groups,families,etc.)willchangetheneed

ofbuilt‐environment.• Integration of multi‐cultural groups changes the need for their

mixed/separatedfacilities.• Dealing with changes in companies, work gets more and more

interdisciplinaryandinternational.• Peopleworkingfromhome.• More families will suffer due to unemployment and the poverty rate will

increase.Technological

• Technologyinnovationisoutstrippingtheabilitytouseandunderstandit.• Photovoltaic and alternative energy sources will improve significantly,

hopefully to cause a paradigm shift to greener technology adoption byconstructionandalliedindustries.

• Trendtowards"offsite/prefabricated"construction.• Greateruseofautomation.• Ongoing technology changes ways of communications/behaviour, leading

also to an increase of possible conflicts.Adecreaseoftime‐to‐marketispossible.

• Developmentanduseofnanotechnology.• Apart from information and communication technologies no major

innovationstobeexpected.• BIM,developmentofprefabrication.• Lessmoneywillbeinvestedinnewtechnology.Othercompaniesmayresort

tocapitalintensiveconstructiontoavoidthecostoflabour.• Consideringthewaypeopleinteractwithnewtechnologyandensuringthat

technologysupportsthepeopleandtheprocessesthatcreatevalueforend‐usersandclients.

• Technological developments associated with sustainability, and newpressuresonskillsneeds.

Question7What innovations, opportunities and initiatives spring mostimmediately to mind for the construction industry to explore, graspandpromoteoverthenextfewyears?

AdaptabilityandRe‐useofResources• Using composite products to harness maximum benefit instead of playing

concreteoffagainststeelandwoodinpureproductforms.• Life‐cycleadaptabilityofprojects;re‐useofmaterials(notnecessarilycradle‐

to‐cradle etc., but in average thinking into life‐cycles).Rainwaterharvestingwillbecriticalforallbuildings.

• Reduce,re‐use,recycleandrefurbish.SocialandCulturalNeeds

• Value and safeguard of existing social and cultural values in existing builtenvironments.

• Recognitionofsocial/culturalneedsandadaptationoftheminarchitecture.Energy

• Developmentofrenewableenergypromotion.• Alternative energy; more energy efficiency, especially energy conservation

forolderbuildings.• "Green"innovations(fromenergy,toC2C).• Zero‐energybuildings.• Microenergygeneration.Joinedupprocurement&delivery.• Greentechnologiesandevenopportunitiesinnuclear.• Initiatives:EnergyPerformanceinBuildingsDirective.

BIM

• BuildinginformationmodellingandVDC.• BuildingInformationSystemsbasedon3‐dimensionalmodelling.

Skills,DevelopmentandKnowledge

• The construction industrymust investmoremoney in skill development sothattheindustrymaybereadyforthefutureboom.

• Creatingskillsforqualitybuilding.• Transferandre‐useofapplied,contextualknowledge.• Trainingitsworkforceforthefuturewithaviablecareerstructure.

International Council for Research and Innovation in Building and Construction

CIB’s mission is to serve its members through encouraging and facilitating international cooperation and information exchange in building and construction research and innovation. CIB is en-gaged in the scientific, technical, economic and social domains related to building and construction, supporting improvements in the building process and the performance of the built envi-ronment.

CIB Membership offers:• international networking between academia, R&D organisations and industry• participation in local and international CIB conferences, symposia and seminars• CIB special publications and conference proceedings• R&D collaboration

Membership: CIB currently numbers over 400 members origi-nating in some 70 countries, with very different backgrounds: major public or semi-public organisations, research institutes, universities and technical schools, documentation centres, firms, contractors, etc. CIB members include most of the major national laboratories and leading universities around the world in building and construction.

Working Commissions and Task Groups: CIB Members participate in over 50 Working Commissions and Task Groups, undertaking collaborative R&D activities organised around:• construction materials and technologies• indoor environment• design of buildings and of the built environment• organisation, management and economics• legal and procurement practices

Networking: The CIB provides a platform for academia, R&D organisations and industry to network together, as well as a network to decision makers, government institution and other building and construction institutions and organisations. The CIB network is respected for its thought-leadership, information and knowledge.

CIB has formal and informal relationships with, amongst oth-ers: the United Nations Environmental Programme (UNEP); the European Commission; the European Network of Building Research Institutes (ENBRI); the International Initiative for Sustainable Built Environment (iiSBE), the International Or-ganization for Standardization (ISO); the International Labour Organization (ILO), International Energy Agency (IEA); Inter-national Associations of Civil Engineering, including ECCS, fib, IABSE, IASS and RILEM.

Conferences, Symposia and Seminars: CIB conferences and co-sponsored conferences cover a wide range of areas of interest to its Members, and attract more than 5000 partici-pants worldwide per year.

Leading conference series include:• International Symposium on Water Supply and Drainage for Buildings (W062)• Organisation and Management of Construction (W065)• Durability of Building Materials and Components (W080, RILEM & ISO)• Quality and Safety on Construction Sites (W099)• Construction in Developing Countries (W107)• Sustainable Buildings regional and global triennial conference series (CIB, iiSBE & UNEP)• Revaluing Construction• International Construction Client’s Forum

CIB Commissions (August 2010)TG58 Clients and Construction Innovation TG59 People in Construction TG62 Built Environment Complexity TG63 Disasters and the Built EnvironmentTG64 Leadership in ConstructionTG65 Small Firms in ConstructionTG66 Energy and the Built EnvironmentTG67 Statutory Adjudication in ConstructionTG68 Construction MediationTG69 Green Buildings and the LawTG71 Research and Innovation TransferTG72 Public Private PartnershipTG73 R&D Programs in ConstructionTG74 New Production and Business Models in ConstructionTG75 Engineering Studies on Traditional ConstructionsTG76 Recognising Innovation in ConstructionTG77 Health and the Built EnvironmentTG78 Informality and Emergence in ConstructionTG79 Building Regulations and Control in the Face of Climate Change TG80 Legal and Regulatory Aspects of BIMTG81 Global Construction DataW014 Fire W018 Timber Structures W023 Wall Structures W040 Heat and Moisture Transfer in Buildings W051 Acoustics W055 Construction Industry Economics W056 Sandwich Panels W062 Water Supply and Drainage W065 Organisation and Management of Construction W069 Housing Sociology W070 Facilities Management and Maintenance W077 Indoor Climate W078 Information Technology for Construction W080 Prediction of Service Life of Building Materials and ComponentsW083 Roofing Materials and SystemsW084 Building Comfortable Environments for All W086 Building Pathology W089 Building Research and Education W092 Procurement Systems W096 Architectural Management W098 Intelligent & Responsive Buildings W099 Safety and Health on Construction Sites W101 Spatial Planning and infrastructure Development W102 Information and Knowledge Management in BuildingW104 Open Building Implementation W107 Construction in Developing Countries W108 Climate Change and the Built Environment W110 Informal Settlements and Affordable Housing W111 Usability of WorkplacesW112 Culture in ConstructionW113 Law and Dispute ResolutionW114 Earthquake Engineering and BuildingsW115 Construction Materials StewardshipW116 Smart and Sustainable Built EnvironmentsW117 Performance Measurement in Construction

PAGE 1

International Council for Research and Innovation in Building and Construction

Publications: The CIB produces a wide range of special publications, conference proceedings, etc., most of which are available to CIB Members via the CIB home pages. The CIB network also provides access to the publications of its more than 400 Members.

Recent CIB publications include:• Guide and Bibliography to Service Life and Durability Research for Buildings and Components (CIB 295)• Performance Based Methods for Service Life Prediction (CIB 294)• Performance Criteria of Buildings for Health and Comfort (CIB 292)• Performance Based Building 1st International State-of-the- Art Report (CIB 291)• Proceedings of the CIB-CTBUH Conference on Tall Buildings: Strategies for Performance in the Aftermath of the World Trade Centre (CIB 290)• Condition Assessment of Roofs (CIB 289)• Proceedings from the 3rd International Postgraduate Research Conference in the Built and Human Environment• Proceedings of the 5th International Conference on Performance-Based Codes and Fire Safety Design Methods• Proceedings of the 29th International Symposium on Water Supply and Drainage for Buildings• Agenda 21 for Sustainable Development in Developing Countries

R&D Collaboration: The CIB provides an active platform for international collaborative R&D between academia, R&D organisations and industry.

Publications arising from recent collaborative R&D ac-tivities include:• Agenda 21 for Sustainable Construction• Agenda 21 for Sustainable Construction in Developing Countries• The Construction Sector System Approach: An International Framework (CIB 293)• Red Man, Green Man: A Review of the Use of Performance Indicators for Urban Sustainability (CIB 286a)• Benchmarking of Labour-Intensive Construction Activities: Lean Construction and Fundamental Principles of Working Management (CIB 276)• Guide and Bibliography to Service Life and Durability Research for Buildings and Components (CIB 295)• Performance-Based Building Regulatory Systems (CIB 299)• Design for Deconstruction and Materials Reuse (CIB 272)• Value Through Design (CIB 280)

Themes: The main thrust of CIB activities takes place through a network of around 50 Working Commissions and Task Groups, organised around four CIB Priority Themes:• Sustainable Construction• Clients and Users• Revaluing Construction• Integrated Design and Delivery Solutions

CIB Annual Membership Fee 2010 – 2013

Membership will be automatically renewed each calen-dar year in January, unless cancelled in writing 3 months before the year end

Fee Category 2010 2011 2012 2013

FM1 Fee level 11837 12015 12195 12378FM2 Fee level 7892 8010 8131 8252FM3 Fee level 2715 2756 2797 2839AM1 Fee level 1364 1384 1405 1426AM2 Fee level 1133 1246 1371 1426IM Fee level 271 275 279 283All amounts in EURO

The lowest Fee Category an organisation can be in depends on the organisation’s profile:

FM1 Full Member Fee Category 1 | Multi disciplinary building research institutes of national standing having a broad field of research FM2 Full Member Fee Category 2 | Medium size research Institutes; Public agencies with major research inter- est; Companies with major research interestFM3 Full Member Fee Category 3 | Information centres of national standing; Organisations normally in Category 4 or 5 which prefer to be a Full MemberAM1 Associate Member Fee Category 4 | Sectoral research & documentation institutes; Institutes for standardisation; Companies, consultants, contractors etc.; Professional associations AM2 Associate Member Fee Category 5 | Departments, fac- ulties, schools or colleges of universities or technical Institutes of higher education (Universities as a whole can not be Member)IM Individual Member Fee Category 6 | Individuals having an interest in the activities of CIB (not representing an organisation)

Fee Reduction: A reduction is offered to all fee levels in the magnitude of 50% for Members in countries with a GNIpc less than USD 1000 and a reduction to all fee levels in the magnitude of 25% for Mem-bers in countries with a GNIpc between USD 1000 – 7000, as defined by the Worldbank. (see http://siteresources.worldbank.org/DATASTATISTICS/Resources/GNIPC.pdf)

Reward for Prompt Payment:All above indicated fee amounts will be increased by 10%. Mem-bers will subsequently be rewarded a 10% reduction in case of actual payment received within 3 months after the invoice date.

For more information contact

CIB General Secretariat:e-mail: [email protected]

PO Box 1837, 3000 BV Rotterdam, The NetherlandsPhone +31-10-4110240;Fax +31-10-4334372Http://www.cibworld.nl

PAGE 2

DISCLAIMER

All rights reserved. No part of this book may be reprinted or

reproduced or utilized in any form or by any electronic,

mechanical, or other means, now known or hereafter

invented, including photocopying and recording, or in any

information storage or retrieval system without

permission in writing from the publishers.

The publisher makes no representation, express or implied,

with regard to the accuracy of the information contained in this book

and cannot accept any legal responsibility or liability in whole or in part

for any errors or omissions that may be made.

The reader should verify the applicability of the information to

particular situations and check the references prior to any reliance

thereupon. Since the information contained in the book is multidisciplinary,

international and professional in nature, the reader is urged to consult with

an appropriate licensed professional prior to taking any action or making

any interpretation that is within the realm of a licensed professional practice.

CIB General Secretariatpost box 18373000 BV RotterdamThe NetherlandsE-mail: [email protected]

CIB Publication 333