Emergence of RMB as an International Currency Webina… · · 2013-07-25Emergence of RMB as an...

23

© Allen & Overy 2013 1 Emergence of RMB as an International Currency Cindy Lo, Partner Allen & Overy, Beijing Office March 2013

Transcript of Emergence of RMB as an International Currency Webina… · · 2013-07-25Emergence of RMB as an...

© Allen & Overy 2013 1

Emergence of RMB as an International CurrencyCindy Lo, Partner

Allen & Overy, Beijing Office

March 2013

2© Allen & Overy 2013

Agenda

– An Overview: the Chinese Government’s policy objectives and key regulatory developments

– Sources of Offshore RMB– Increased use of RMB in cross-border transactions: How does it

affect your business?– RMB trade settlement– Foreign direct investment and loans– RQFII (RMB Qualified Foreign Institutional Investors)– Others

– The Offshore RMB market– Looking ahead: trends and key issues

3© Allen & Overy 2013

An Overview: the Chinese Government’s policy objectives and key regulatory developments (1)– Demand for the Chinese currency is driven by China’s

wide trade network and growing economic weight in the global economy

– Chinese government’s efforts in recent years to encourage the cross-border use of the RMB

– Different stages of RMB internationalisation: Current account items vs. Capital account items

4© Allen & Overy 2013

An Overview: the Chinese Government’s policy objectives and key regulatory developments (2)– “China is determined to pursue the internationalisation of

the RMB on a market-oriented basis.” – Yi Gang, Vice Governor or PBOC and Head of SAFE, 27 January 2013 in Davos, Switzerland

– RMB internationalisation is a policy-driven process and should be closely watched.

5© Allen & Overy 2013

Sources of Offshore RMB

– Sources of funding: “RMB legitimately obtained”– Dim Sum bonds– Reserve accumulated through RMB trade settlement– Offshore RMB bank loans– RMB IPO

– Hui Xian REIT (listed in Hong Kong): the first RMB denominated REIT sold outside of the Chinese mainland

– Offshore FX market

6© Allen & Overy 2013

Increased use of RMB in cross-border transactions: How does it affect your business? – Background

– Gradual relaxation of control over cross-border flow of fund in RMB

– Flow of fund into and out of China– Current account items

– Cross border RMB trade settlement– Capital account items

– Equity investment (ODI/FDI)– Foreign debt and foreign security denominated in RMB– Financial investment (securities and financial derivatives)

7© Allen & Overy 2013

Increased use of RMB in cross-border transactions (1): RMB Trade Settlement– RMB trade settlement

– Current account items– Encouraging cross-border RMB trade settlement is part of a

long-term plan to promote RMB as a reserve currency and reduce China’s exposure to the US Dollar

– Pilot scheme: introduced in 2009 and has been expanded to cover all overseas countries and, since August 2011, all of China

– Corporates incorporated anywhere in China and qualified for foreign trade activities may now freely settle cross-border trades in RMB – No PRC regulatory approval is required

8© Allen & Overy 2013

Increased use of RMB in cross-border transactions (2): Foreign Direct Investment (FDI)– Foreign direct investment and loans: Gradual relaxation of inflow of

RMB– Pre-October 2011 regime for cross-border equity injection

– Application to MOFCOM for new establishment, transfer of equity or capital increase – By the foreign investor and/or onshore subsidiary– Equity investment in RMB generally follow the same process/paper work as the FX equity injection except for

– Specifying using RMB for the injection/payment of consideration– Involvement of central MOFCOM

– Application for PBOC approval– By the onshore RMB settlement bank– Local PBOC ->central PBOC– Paper work: application letter, MOFCOM approval, other supporting documents

– Introduction of new regulatory regime in October 2011– MOFCOM Circular 889– PBOC Circular 23

9© Allen & Overy 2013

Increased use of RMB in cross-border transactions (3): Foreign Direct Investment (FDI) (Continued)– MOFCOM Circular 889

– Definition of “Offshore RMB”– RMB funds derived from (i) onshore (trade settlement, profits from

onshore FIE) and (ii) offshore (dim sum bonds, trade settlement, IPO, conversion and swap, etc.)

– Approval process– Certain categories require approval of central MOFCOM– Compliance with other existing FDI requirements (FDI catalogue, anti-

trust)– Restricted use of proceeds

– Prohibition– Financial investments (in securities market except strategic investment in listed companies and

derivatives)– Entrustment loan

– Refinancing of existing onshore debt?

10© Allen & Overy 2013

Increased use of RMB in cross-border transactions (4): Inbound Lending– PBOC Circular 23

– Loans can be granted to an FIE by its shareholders, group affiliates or offshore FIs

– Prior PBOC approval not required for repatriation to an FIE, defer to other governmental agencies

– Post registration with PBOC – monitor on a post-remittance basis

– Opening of various accounts (separate from each other): upfront payment, registered capital, acquisition, share transfer, foreign debt

– SAFE’s role?

11© Allen & Overy 2013

Increased use of RMB in cross-border transactions (5): Inbound Lending (Continued)– New channel for banks in Hong Kong to deploy RMB

funds: Cross-border RMB Loan Trial Scheme in QianhaiDistrict of Shenzhen– Loan facility of around RMB2 billion provided by 15 Hong

Kong banks to qualified enterprises in Qianhai for the financing of 26 projects in January 2013

– Tenor and interest rates to be set separately– Lower interest rate in offshore RMB loan market: attractive to

Chinese enterprises

12© Allen & Overy 2013

Increased use of RMB in cross-border transactions (6): Foreign Debt and Security Denominated in RMB– Foreign debt and security denominated in RMB

– PBOC and SAFE hold different views towards RMB foreign debt and security– June 2011 PBOC Circular: not treated as foreign debt and

security– April 2011 SAFE Circular: cross-border debt and security in RMB

shall “in principle” be administered as foreign debt and security– Practical difficulties– Clarification from officials of PBOC/SAFE/MOFCOM

13© Allen & Overy 2013

Increased use of RMB in cross-border transactions (7): Financial investment– RQFII (RMB Qualified Foreign Institutional Investors)

– Key regulators: CSRC, SAFE and PBOC– HK subsidiaries of PRC securities firms and fund managers

are now allowed to invest in mainland securities in RMB– Investment scope: RMB instruments traded on PRC

exchange or interbank bond market

14© Allen & Overy 2013

Increased use of RMB in cross-border transactions (8): Financial investment (Continued)

– RQFII was launched in December 2011; Current quota is RMB270 billion (US$43.42 billion)

– According to SAFE, 24 institutions (including 12 fund companies and 12 securities firms) held a combined RMB67 billion as at the end of 2012.

– “China could raise the current investment quotas for QFII and RQFII schemes by nine or 10 times.” – Guo Shuqing, Chairman of CSRC, 14 January 2013 at the Asia Financial Forum in Hong Kong

15© Allen & Overy 2013

Increased use of RMB in cross-border transactions (9): Financial investment (Continued)– Potential opportunities for individual investors

– Qualified Domestic Individual Investor (QDII2)– PRC individual investors directly investing in offshore stocks (e.g.

Hong Kong)– RMB Qualified Foreign Individual Investor (RQFII2)

– To expand QFII scheme to non-PRC individual investors– Separate from the RMB270 billion quota for RQFII

– Pilot plans in the works (PBOC working meetings, January 2013); detailed timetable yet to set– Only short-term loans allowed?– Amount of such loans limited to the amount of profits to which a

foreign investor is entitled to?

16© Allen & Overy 2013

Increased use of RMB in cross-border transactions (10): Outbound Lending by PRC Corporates– New SAFE regulations– PBOC pilot program in Shanghai to allow PRC corporates to

make loans in RMB to their offshore affiliates – To facilitate the utilisation of RMB funds sourced from the PRC

by qualified MNCs in funding their overseas activities– Application to be made through an account bank– If the application is successful, the Shanghai branch of PBOC

will grant a quota for the loan to the applicant– A welcome development, but questions remain

17© Allen & Overy 2013

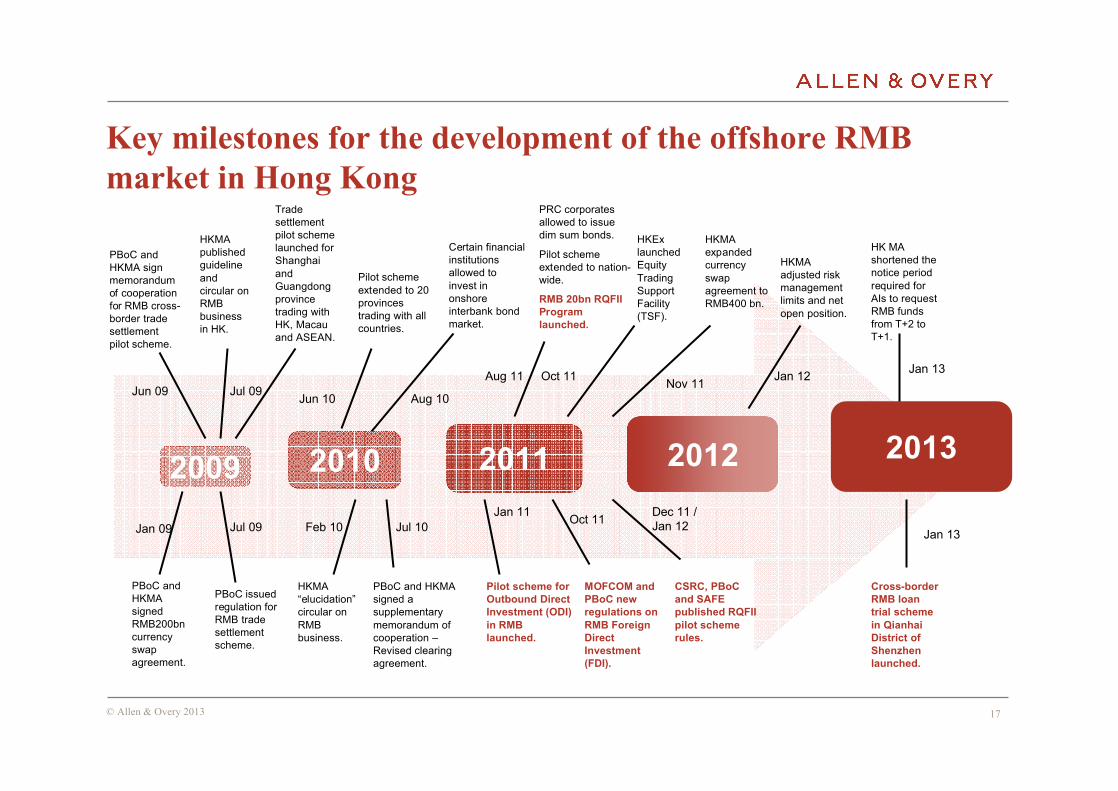

Key milestones for the development of the offshore RMB market in Hong Kong

2011 2012

PBoC and HKMA sign memorandum of cooperation for RMB cross-border trade settlement pilot scheme.

HKMA adjusted risk management limits and net open position.

Jan 12Aug 11

PRC corporates allowed to issue dim sum bonds.

Pilot scheme extended to nation-wide.

RMB 20bn RQFII Program launched.

Oct 11Jan 11

MOFCOM and PBoC new regulations on RMB Foreign Direct Investment (FDI).

Pilot scheme for Outbound Direct Investment (ODI) in RMB launched.

Jun 10

Pilot scheme extended to 20 provinces trading with all countries.

Feb 10 Jul 10

PBoC and HKMA signed a supplementary memorandum of cooperation –Revised clearing agreement.

HKMA “elucidation”circular on RMB business.

Jan 09 Jul 09

PBoC issued regulation for RMB trade settlement scheme.

PBoC and HKMA signed RMB200bn currency swap agreement.

HKMA published guideline and circular on RMB business in HK.

Trade settlement pilot scheme launched for Shanghai and Guangdong province trading with HK, Macau and ASEAN.

Jun 09 Jul 09

Certain financial institutions allowed to invest in onshore interbank bond market.

Aug 10

2009 2010

Oct 11

HKExlaunched Equity Trading Support Facility (TSF).

Dec 11 / Jan 12

CSRC, PBoC and SAFE published RQFII pilot scheme rules.

Nov 11

HKMA expanded currency swap agreement to RMB400 bn.

2013

HK MA shortened the notice period required for AIs to request RMB funds from T+2 to T+1.

Jan 13

Cross-border RMB loan trial scheme in QianhaiDistrict of Shenzhen launched.

Jan 13

18© Allen & Overy 2013

Offshore RMB market: Hong Kong (1)

– Hong Kong leading the pack– Accumulation of CNH funds since 2004– Transfer of CNH funds between accounts and across banks since July 2010– Largest pool of CNH outside the Mainland China – official arrangement with

the PRC government– Generally, no restrictions on use of CNH funds so long as no repatriation

into the Mainland– Interest/exchange rates different from the Mainland– Settle through HK RMB RTGS System

– PBOC as central bank– BOC as settlement bank; clearing agreement with PBOC

– Currently 138 authorised institutions engaged in RMB business in Hong Kong

– The HKMA announced the decision to shorten the notice period required for Authorized Institutions participating in RMB business to request RMB funds from 2 business days (T+2) to 1 business day (T+1) from 16 January 2013

19© Allen & Overy 2013

Offshore RMB market: Hong Kong (2)

– According to data released by HKMA:

62%237.2 billion146.4 billionOutstanding Dim Sum Bonds

Newly issued Dim Sum bonds

Trading settlement in CNH

CNH loans provided by Hong Kong banks

CNH deposits from non-HK residents

CNH deposits and deposit certificates

4%112.2 billion107.9 billion

37%2,630 billion1,910 billion

157%79 billion30.8 billion

N/AOver 4 billionN/A (launched in August 2012)

9%661.6 billion720.2 billion

Year-on-year increase

By end of year 2012

By end of year 2011

20© Allen & Overy 2013

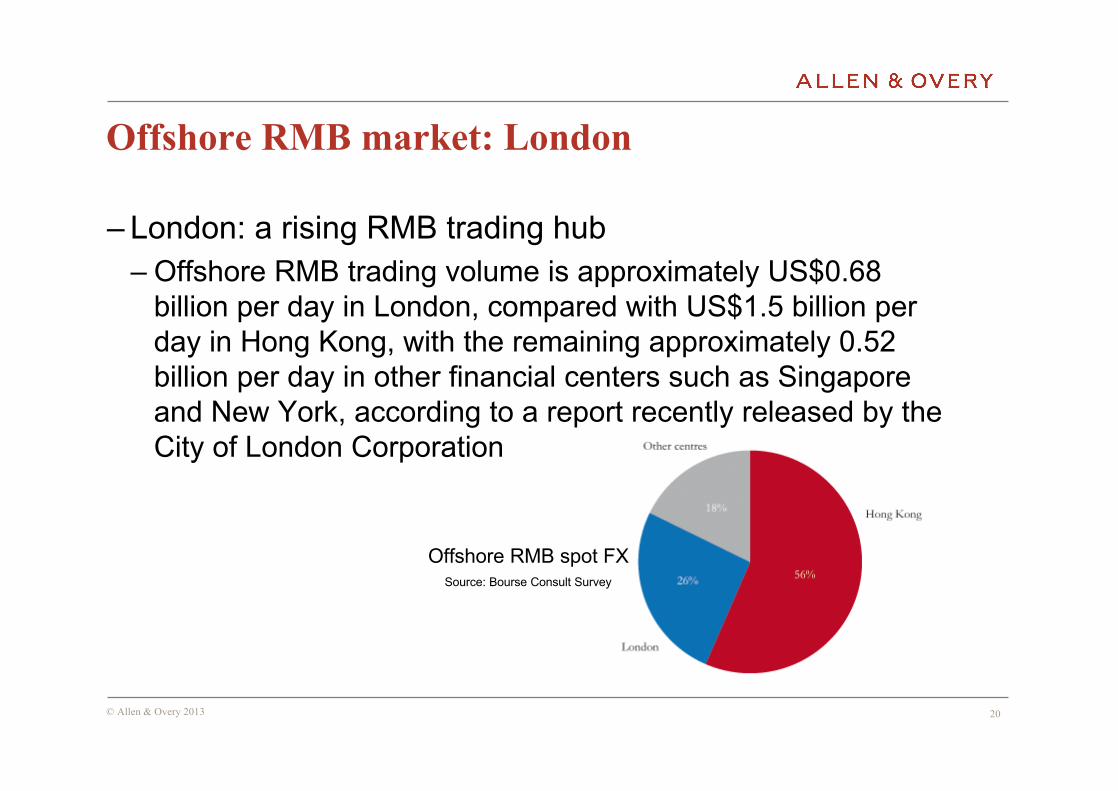

Offshore RMB market: London

– London: a rising RMB trading hub– Offshore RMB trading volume is approximately US$0.68

billion per day in London, compared with US$1.5 billion per day in Hong Kong, with the remaining approximately 0.52 billion per day in other financial centers such as Singapore and New York, according to a report recently released by the City of London Corporation

Offshore RMB spot FXSource: Bourse Consult Survey

21© Allen & Overy 2013

Offshore RMB market: Singapore

– Singapore hard on the heels of Hong Kong?– Trading hub for commodities that China needs– S$30 billion currency swap agreement between China &

Singapore (July 2010)

22© Allen & Overy 2013

Looking ahead: trends and key issues

– Increased liquidity– Diversification of investment products– Opening of the PRC capital market to foreign issuers?

23© Allen & Overy 2013

Questions?

These are presentation slides only. The information within these slides does not constitute definitive advice and should not be used as the basis for giving definitive advice without checking the primary sources.

Allen & Overy means Allen & Overy LLP and/or its affiliated undertakings. The term partner is used to refer to a member of Allen & Overy LLP or an employee or consultant with equivalent standing and qualifications or an individual with equivalent status in one of Allen & Overy LLP's affiliated undertakings.

Webinar slides - RMB Internationalisation (21 March).PPT