Eliza Ahmed Centre for Tax System Integrity Australian National University When tax offices become...

29

Eliza Ahmed Centre for Tax System Integrity Australian National University When tax offices become collection agencies: At what cost?

-

Upload

godfrey-edgar-marsh -

Category

Documents

-

view

216 -

download

1

Transcript of Eliza Ahmed Centre for Tax System Integrity Australian National University When tax offices become...

Eliza Ahmed

Centre for Tax System Integrity

Australian National University

When tax offices become collection agencies: At what cost?

Do tax authorities leave themselves at risk of tax evasion when they become collection agencies for controversial government policies?

1. When tax collectors become collectors for child support and student loans: Jeopardizing or protecting the revenue base? (Ahmed & V. Braithwaite)

2. Tax evasion among graduates repaying student loans: Balancing the books, sending a political message, or flouting the system? (V. Braithwaite & Ahmed)

3. Can justice and shame deter an escalation in tax evasion? (Ahmed & V. Braithwaite)

What does past research tell us?

Financial self-interest (Allingham & Sandmo, 1972; Freiberg, 1990)

Deterrence (Grasmick & Bursik, 1990; Lewis, 1982)

Moral obligation (Grasmick & Bursik, 1990; McGraw & Scholz, 1991; Schwartz & Orleans, 1967)

Shame management (Ahmed, Harris, Braithwaite, & Braithwaite, 2001)

Fairness (Kinsey & Grasmick, 1993; Scholz & Lubell, 1998)

Reactance (Kirchler, 1999)

What does past research tell us? (cont’d)

Trust (Scholz & Lubell, 1998; Tyler, 1997, 2001)

Trust norms (V. Braithwaite, 1998)

What does past research tell us? (cont’d)

STUDY 1Research questions

1. Are taxpayers making additional payments through the tax system less compliant?

2. To what extent does belief in trust norms act as a social constraint, and prevent tax evasion?

Community Hopes, Fears and Actions Survey (Braithwaite, 2000)

7754 randomly sampled Australian citizens were mailed out the survey questionnaires

2040 respondents returned their completed questionnaires

METHOD

Dependent variable: Tax evasion Under-reporting income Engaging in the cash economy Exaggerating deductions

MEASURES

Independent variables

Additional paymentsDeterrence Shame management

- shame acknowledgment

- shame displacement

- shame avoidance Trust norms

RESULTS

Table 1. Correlation coefficients between tax evasion and other variables

☺☺☺ p < .001 ☺☺ p < .01

-.19☺☺☺ Trust norms .13☺☺☺ Shame avoidance .12☺☺☺ Shame displacement -.19☺☺☺ Shame acknowledgment -.16☺☺☺ Deterrence enforcement .13☺☺☺ Additional payments

Correlation coefficientsVariables

Table 2. Standardized beta coefficients from regression analysis predicting tax evasion

☺☺☺ p < .001 ☺☺ p < .01 ☺ p < .05

Variables Model 1 Model 2 Model 3

Additional payments .08☺☺ .08☺☺ .07☺

Deterrence enforcement (DE) - -.10☺☺☺ -.09☺☺

Shame acknowledgment (SA) - -.08☺☺ -.09☺☺

Shame displacement - .10☺☺☺ .09☺☺

Shame avoidance - .06☺ .06☺

Trust norms (TN) - -.15☺☺☺ -.15☺☺☺

Additional payments * DE - - -.02

Additional payments * SA - - .03

Additional payments * TN - - -.14☺☺☺

Adj R square .06 .12 .14

Figure 1. The role of trust norms in moderating the relationship between making additional payments and tax evasion

Trust norms

HighLow

Tax e

vasio

n

.4

.3

.2

.1

0.0

-.1

-.2

___ Additional payments

----- No payments

When policy changes, citizens may protest, but the relationship between citizens and the tax office acts as a protector, ensuring that non-compliance does not spin out of control.

Summary from Study 1

STUDY 2

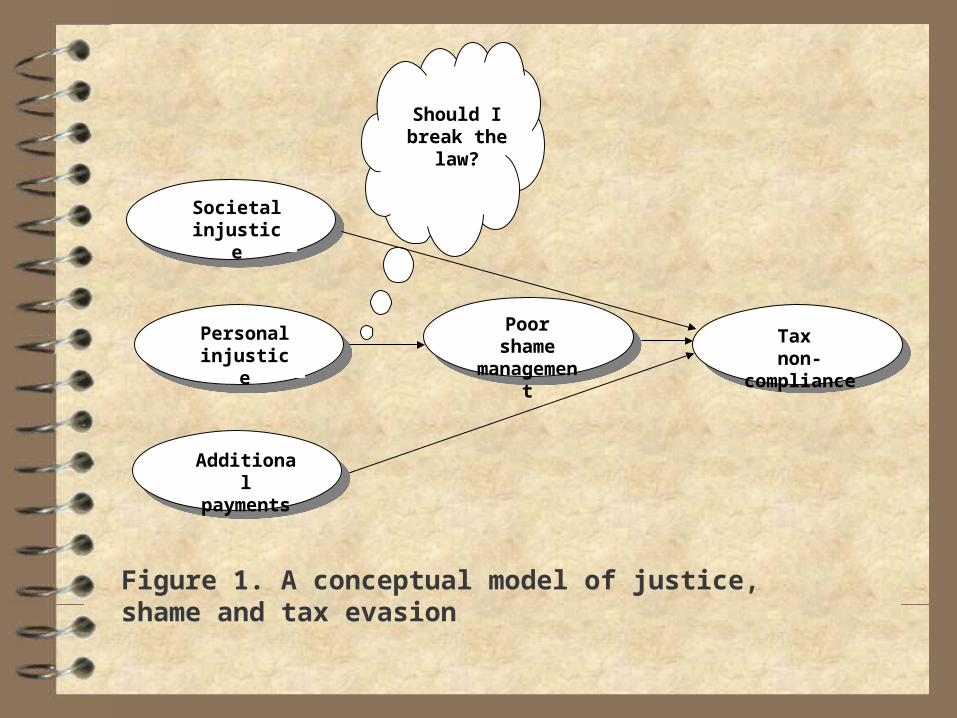

Figure 1. A conceptual model of justice, shame and tax evasion

Societal injustice

Should I break the law?

Additional payments

Poor shame management Tax

non-compliancePersonal injustice

STUDY 2Research aims

1. To explore the extent to which additional payments, perceptions of justice, and shame management play important roles in predicting tax non-compliance

2. To evaluate the theoretical relationships among all variables sketched in Figure 1

METHOD

Graduates’ Hopes, Visions and Actions Survey (Ahmed, 2000)

1500 stratified sampled Australian graduates were mailed out the survey questionnaires

447 respondents returned their completed questionnaires

Tax non-compliance variables Dissociation (desire to game play or disengage) Tax evasion (behaviors of not lodging, under-

declaring income, or over-claiming deductions)

MEASURES

Independent variables

Additional payments Perceived injustice

- societal (unfair social policy)

- personal (unfair exchange) Shame management

- shame acknowledgment

- shame displacement

- shame avoidance

RESULTS

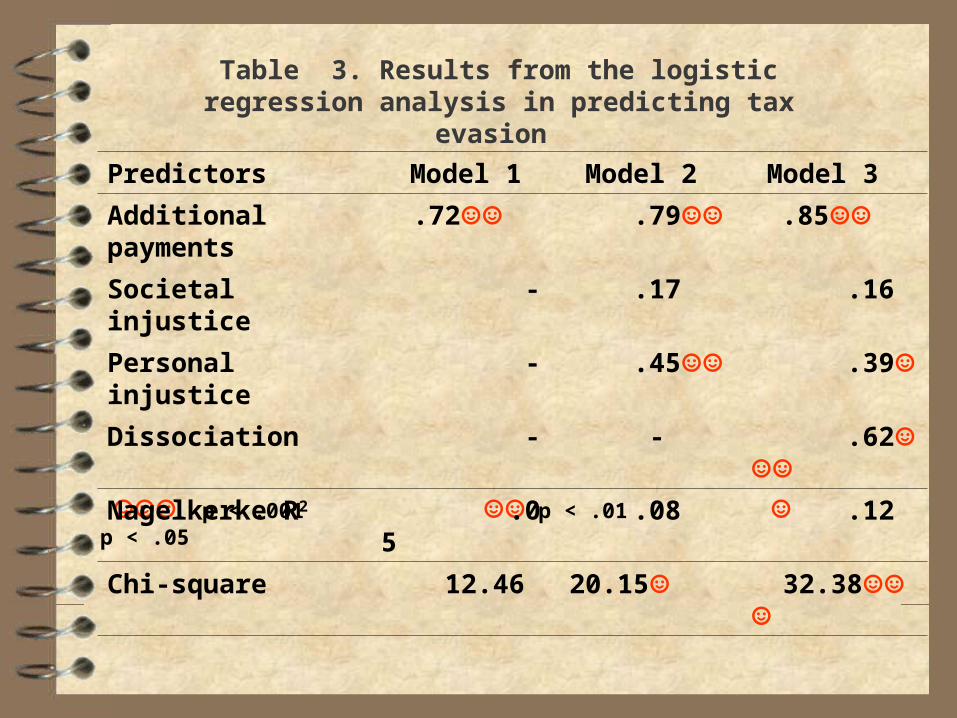

Table 3. Results from the logistic regression analysis in predicting tax evasion

☺☺☺ p < .001 ☺☺ p < .01 ☺ p < .05

Predictors Model 1 Model 2 Model 3

Additional payments .72☺☺ .79☺☺ .85☺☺

Societal injustice - .17 .16

Personal injustice - .45☺☺ .39☺

Dissociation - - .62☺☺☺

Nagelkerke R2 .05 .08 .12

Chi-square 12.46 20.15☺ 32.38☺☺☺

Figure 2. Results of a path analysis showing the relationships among all variables considered in Study 2

.17

.15

.19 .10

-.25-.10

.28

.13

-.12

Shame avoidance

Tax evasion

Shame acknowledgment

Shame displacement

Personal injustice

Societal injustice Dissociation

.12

Table 4. The overall fit indices for the model derived from the path analysis

Chi-square (2) 13.44 (df = 20; p < .86)

CFI (Comparative Fit Index) 1.00

GFI (Goodness of Fit Index) .992

RMSEA (Root Mean Square Error of Approximation) .00

“ ... The one thing that I did find annoying was paying HECS for one or two units where the tutors were hopeless and basically didn’t teach us much at all. I realize it is more the responsibility of the universities to ensure that their tutors are competent, but it is in cases like these that people resent having to pay HECS, ie. when they didn’t learn anything new!”

“The government should realize that investing in tertiary education is investing in the country’s future. By raising fees, introducing up-front fees, ..., they are encouraging people not to study and not to help educate the country. Education should be free, after all people in the army get paid to be educated!”

“I think that HECS should only be repaid if the education received has been of value in gaining employment”

Where to from here?

“Responsive regulation is distinguished (from other strategies ...) both in what triggers a regulatory response and what the regulatory response will be. ... Government should be attuned to the differing motivations of regulated actors. Efficacious regulation should speak to the diverse objectives of regulated firms, industry associations, and individuals within them” (Ayres & J. Braithwaite, 1992)