ELECTRONIC SUPPLEMENT TO CHAPTER 1wps.prenhall.com/.../objects/375/384212/chapsupps/ch01.pdf ·...

18

ELECTRONIC SUPPLEMENT TO CHAPTER 1 POOLING OF INTERESTS ACCOUNTING The issuance of FASB Statement No. 141 makes pooling of interests accounting for busi- ness combinations a thing of the past under U.S. GAAP. No new pooling combinations will be recorded unless initiated by June 30, 2001. Many of the detailed issues related to pool- ings concern the original recording of the combination. Since there will be no new pool- ings, this material is considerably less important than it was at the writing of the prior edi- tion of this text. The information in this electronic supplement to Chapter 1 is primarily related to the initial recording of poolings. Again, grandfathering of prior poolings makes it useful to understand the recording of past poolings, but you will not need this accounting detail for transactions that will not recur in the future. Conditions for Pooling The pooling of interests concept was based on the assumption that it was possible to unite ownership interests through the exchange of equity securities without an acquisition of one combining company by another. 1 Accordingly, application of the concept was limited to those business combinations in which the combining entities exchanged equity securities and the operations and ownership interests continued in a new accounting entity. In APB Opinion No. 16, the APB sought to prevent pooling of interests accounting for business combinations that were incompatible with the pooling concept. It did this by specifying (in paragraphs 45 through 48 of Opinion No. 16) 12 conditions that had to be met for the pool- ing of interests method to be used. These conditions are summarized under the headings used by the APB. ATTRIBUTES OF COMBINING COMPANIES Two of the conditions for a pooling of interests were classified as attributes of the combining companies. The first condition was that each of the combining companies was autonomous and had not been a subsidiary or divi- sion of another corporation within two years before the plan of combination was initi- ated. The date of initiation was the earlier of the public announcement of the ratio of exchange of stock or the notification of the stockholders of the exchange ratio. The exchange ratio was the ratio of the number of shares of the issuing company’s stock to be exchanged for each share of the other combining company’s stock on the date of con- summation of the pooling. Electronic Supplement to Chapter 1 1 C H A P T E R 1 1 The underlying assumptions of pooling had been challenged by many writers in accounting. For example, see Accounting Research Study No. 5. “A Critical Study of Accounting for Business Combinations,” by Arthur R. Wyatt (New York: American Institute of Certified Public Accountants, 1963).

Transcript of ELECTRONIC SUPPLEMENT TO CHAPTER 1wps.prenhall.com/.../objects/375/384212/chapsupps/ch01.pdf ·...

ELECTRONIC SUPPLEMENT TO CHAPTER 1

POOLING OF INTERESTS ACCOUNTINGThe issuance of FASB Statement No. 141 makes pooling of interests accounting for busi-ness combinations a thing of the past under U.S. GAAP. No new pooling combinations willbe recorded unless initiated by June 30, 2001. Many of the detailed issues related to pool-ings concern the original recording of the combination. Since there will be no new pool-ings, this material is considerably less important than it was at the writing of the prior edi-tion of this text. The information in this electronic supplement to Chapter 1 is primarilyrelated to the initial recording of poolings. Again, grandfathering of prior poolings makes ituseful to understand the recording of past poolings, but you will not need this accountingdetail for transactions that will not recur in the future.

Conditions for PoolingThe pooling of interests concept was based on the assumption that it was possible to uniteownership interests through the exchange of equity securities without an acquisition of onecombining company by another.1 Accordingly, application of the concept was limited tothose business combinations in which the combining entities exchanged equity securitiesand the operations and ownership interests continued in a new accounting entity. In APBOpinion No. 16, the APB sought to prevent pooling of interests accounting for businesscombinations that were incompatible with the pooling concept. It did this by specifying (inparagraphs 45 through 48 of Opinion No. 16) 12 conditions that had to be met for the pool-ing of interests method to be used. These conditions are summarized under the headingsused by the APB.

ATTRIBUTES OF COMBINING COMPANIES Two of the conditions for a pooling of interestswere classified as attributes of the combining companies. The first condition was thateach of the combining companies was autonomous and had not been a subsidiary or divi-sion of another corporation within two years before the plan of combination was initi-ated. The date of initiation was the earlier of the public announcement of the ratio ofexchange of stock or the notification of the stockholders of the exchange ratio. Theexchange ratio was the ratio of the number of shares of the issuing company’s stock to beexchanged for each share of the other combining company’s stock on the date of con-summation of the pooling.

Electronic Supplement to Chapter 1 1

C H A P T E R 1

1The underlying assumptions of pooling had been challenged by many writers in accounting. For example, seeAccounting Research Study No. 5. “A Critical Study of Accounting for Business Combinations,” by Arthur R. Wyatt(New York: American Institute of Certified Public Accountants, 1963).

2 ADVANCED ACCOUNTING

2Paragraph 99 of Opinion No. 16 provided certain exceptions to the test of minority stock held prior to combinationand the 90% “substantially all” test. These exceptions, commonly referred to as the grandfather clause, were intended toprovide a five-year period of transition to the rules of Opinion No. 16. Although the grandfather clause initially was sched-uled to expire on October 31, 1975, it was extended indefinitely by FASB Statement No. 10.

The second condition was that each of the combining companies be independent of the others.This was interpreted to mean that the other combining companies together owned no more than10% of the voting stock of any combining company.

MANNER OF COMBINING INTERESTS There were seven conditions for pooling. First, the combina-tion must have been effected in a single transaction or been completed in accordance with a spe-cific plan within one year after the plan was initiated. Failure to meet the one-year requirement didnot prevent the pooling treatment if consummation was delayed by lawsuits, regulatory agencies,or other factors beyond the control of management.

Second, one corporation (the issuing corporation) must have offered and issued only commonstock in exchange for substantially all (90% or more) of the outstanding voting stock of anothercompany (a combining company) on the date the plan was consummated. The number of sharesassumed to be exchanged excluded shares of the combining company held by the issuing companywhen the plan was initiated, shares acquired by the issuing company before the plan was consum-mated, and shares outstanding after the plan was consummated. If the combining company heldshares in the issuing company, these shares required conversion into an equivalent number ofshares of the combining company and we deducted them from outstanding shares to determine thenumber of shares assumed to be exchanged. The reason for this adjustment was that part of theshares issued by the issuing company were used to reacquire its own shares. Such shares were notissued to acquire stock of the other combining company.2

The third condition for pooling was that none of the combining companies changed the equityinterest of the voting common stock in contemplation of effecting the combination within two yearsbefore initiation of the plan of combination or between the dates of initiation and consummation.

A fourth condition was that each of the combining companies reacquired shares of voting com-mon stock only for purposes other than business combination, and that no company reacquiredmore than a normal number of shares between the dates the plan was initiated and consummated.This restriction on treasury stock transactions generally did not apply to shares purchased for stockoption or compensation plans.

The fifth condition required that the proportionate interest of each individual common stock-holder in each of the combining companies remain the same as a result of the exchange of stock toeffect the combination. For example, if Stockholder A held 100 shares in the other combining com-pany and Stockholder B held 200 shares, then Stockholder B’s interest in the pooled entity musthave been twice that of A’s for the combination to be a pooling of interests.

Condition 6 specified that the voting rights in the combined corporation be immediately exercisableby the stockholders. The final condition required resolution of the combination on the date of consum-mation, with no provisions pending that related to the issue of securities or other considerations.

ABSENCE OF PLANNED TRANSACTIONS The last group of conditions for a pooling of interestsfocused on planned transactions of the combined entity. First, the combined corporation must nothave retired or reacquired stock issued to effect the combination. Second, the combined corporationmust not have entered into financial arrangements (such as loan guarantees) for the benefit of formerstockholders of a combining company. Finally, the combined corporation must not have planned todispose of a significant part of the assets of the combining companies within two years after thecombination. Plans to dispose of assets that represented duplicate facilities were permissible.

If all 12 of these conditions were met, the business combination was accounted for as a poolingof interests; otherwise, the purchase method was used. Exhibit 1 reviews the 12 conditions for apooling of interests.

Computations for the “Substantially All” TestAlthough most of the conditions for pooling are easy to understand, the second condition (the “sub-stantially all” test) under the “Manner of Combining Interests” heading requires illustration.Assume that Pat Corporation and Sam Corporation entered into a plan of business combination onMay 1, 2001, in which Pat acquired Sam’s outstanding stock by issuing one share of Pat stock for

Electronic Supplement to Chapter 1 3

Attributes of Combining Companies1 Autonomous (two-year rule)2 Independent (10% rule)

Manner of Combining Interests1 Single transaction (or completed within one year after initiation)2 Exchange of common stock (the “substantially all” rule: 90% or more)3 No equity changes in contemplation of combination (two-year rule)4 Shares reacquired only for purposes other than combination5 No change in proportionate equity interests6 Voting rights immediately exercisable7 Combination resolved at consummation (no pending provisions)

Absence of Planned Transactions1 Issuing company cannot reacquire shares2 Issuing company cannot make deals to benefit former stockholders3 Issuing company cannot plan to dispose of assets within two years

EXHIBIT 1-1Twelve Condit ionsfor Pooling (APBOpinion No. 16)

Shares Assumed to Be ExchangedSam’s outstanding shares on May 30, 2001 10,000Deduct:

Combining company shares held by issuing company:Sam shares held by Pat on May 1, 2001 �200Sam shares acquired by Pat during May 2001 �200

Equivalent number of issuing company shares held by combiningcompany:

Equivalent number of Sam shares represented bySam’s 200 shares of Pat (200/0.5 exchange ratio) �400

Sam shares outstanding after consummation �600Sam shares assumed to be exchanged in the combination 8,600

Shares Required to Be Exchanged10,000 outstanding shares of Sam on May 30, 2001 � 90% 9,000

90% TestThe 8,600 shares assumed exchanged was less than the required 9,000. Thus, the business combinationwas not a pooling of interests.

EXHIBIT 1-2“Substantial ly Al l”Test for a Poolingof Interests

each two shares of Sam. The agreed-upon exchange ratio was 0.5 to 1. When the plan of combi-nation was initiated. Sam Corporation had 10,000 shares of voting common stock outstanding, ofwhich 200 shares were already owned by Pat. After the plan of combination was initiated, Pat pur-chased for cash an additional 200 shares of Sam stock directly from Sam’s stockholders, and Sampurchased for cash 200 shares of Pat stock from Pat’s stockholders. The business combination wasconsummated on May 30, 2001, with Pat issuing 4,500 shares of its own stock for 9,000 shares ofSam. Sam’s former stockholders continued to hold 600 shares of Sam stock.

To meet the “substantially all” test, Pat Corporation must have issued its own stock for 90%or more of Sam’s stock. Although it appears that the 90% pooling test was met, the computationshown in Exhibit 2 indicates otherwise. The Sam shares held by Pat and the Pat shares held by Samdisqualified the business combination for the pooling treatment, even though Pat issued its ownstock for 90% of Sam’s outstanding shares on the date of consummation of the plan.

Combining Stockholders’ Equities in a PoolingIn a pooling of interests, the recorded assets and liabilities of the separate companies became the assetsand liabilities of the surviving (combined) corporation. Because total assets and liabilities equal thesum of the combining entities, so must the total equities. The capital stock of the surviving corporationmust have equaled the par or stated value of outstanding shares (after the issuance of the new shares).Ordinarily, the retained earnings of the surviving corporation would have been equal to the totalretained earnings of the combining companies, but this was not possible when the par or stated valueof outstanding shares of the surviving entity exceeded the paid-in capital of the combining companies.If total paid-in capital of the combining companies exceeded the par or stated value of outstanding

4 ADVANCED ACCOUNTING

shares of the surviving entity, the amount of the excess became the additional paid-in capital of the sur-viving entity, and the total retained earnings of the combining companies became the retained earningsof the surviving entity. Alternatively, if the par or stated value of outstanding shares of the survivingentity exceeded the total paid-in capital of the combining companies, the combined retained earningsbalance was reduced by the excess, and the surviving entity had no additional paid-in capital.

Recall our simple example from the appendix to Chapter 1. These relationships can be shownthrough a series of illustrations. Assume that immediately before their pooling of interests businesscombination, the stockholders’ equity accounts for Jake Corporation and Kate Corporation were asfollows (all amounts are in thousands):

Jake KateCorporation Corporation Total

Capital stock, $10 par $100 $ 50 $150Additional paid-in capital 10 20 30

Total paid-in capital 110 70 180Retained earnings 50 30 80

Net assets and equity $160 $100 $260

In cases 1 and 2 that follow, the pooling was in the form of a merger, in which Jake Corporationwas the issuing corporation and the surviving entity. In cases 3, 4, and 5, the pooling was in theform of a consolidation, and Pete Corporation was formed to take over the net assets of Jake andKate. Jake and Kate disappeared.

CASE 1: MERGER; PAID-IN CAPITAL EXCEEDS STOCK ISSUEDJake, the surviving corporation, issued 7,000 shares of its stock for the net assets of Kate. In thiscase, the $180,000 total paid-in capital of the combining companies exceeded the $170,000 capitalstock of Jake by $10,000. As a result, Jake had capital stock of $170,000, additional paid-in capitalof $10,000, and retained earnings of $80,000, for a total equity of $260,000. Observe that the netassets of the surviving entity still were equal to the total recorded assets of the combining compa-nies. Jake recorded the pooling as follows:

Net assets (+A) 100

Capital stock, $10 par (+SE) 70

Retained earnings (+SE) 30

To record issuance of 7,000 shares in a pooling with

Kate Corporation.

CASE 2: MERGER; STOCK ISSUED EXCEEDS PAID-IN CAPITALJake, the surviving entity, issued 9,000 shares of its stock for the net assets of Kate. In this case, the$190,000 capital stock of Jake exceeded the $180,000 total paid-in capital of the combining com-panies by $10,000. The result was that Jake would have capital stock of $190,000, no additionalpaid-in capital, and retained earnings of $70,000. Notice that the maximum retained earnings thatcan be combined ($80,000) has been reduced by the $10,000 excess of capital stock over paid-incapital. The entry on Jake’s books was as follows:

Net assets (+A) 100

Additional paid-in capital (�SE) 10

Capital stock $10 par (+SE) 90

Retained earnings (+SE) 20

To record issuance of 9,000 shares in a pooling with

Kate Corporation.

The previous cases illustrated accounting procedures for a merger accounted for as a pooling ofinterests. Accounting procedures for consolidation of Jake and Kate are illustrated by assumingthat Pete Corporation was formed to take over the net assets of Jake and Kate Corporations.

CASE 3: CONSOLIDATION; PAID-IN CAPITAL EXCEEDS STOCK ISSUEDPete Corporation issued 15,000 shares of $10 par capital stock, 10,000 to Jake and 5,000 toKate, for their net assets. In this case, the stockholders’ equity of Pete, the surviving entity, was

Electronic Supplement to Chapter 1 5

3APB Opinion No. 16, paragraph 54.

the same as for Jake Corporation in Case 1. Pete, however, opened its books with the follow-ing entry:

Net assets (+A) 260

Capital stock, $10 par (+SE) 150

Additional paid-in capital (+SE) 30

Retained earnings (+SE) 80

To record issuance of 10,000 shares to Jake and 5,000

shares to Kate in a business combination accounted

for as a pooling of interests.

The $180,000 combined paid-in capital of Jake and Kate exceeded the $150,000 capital stock ofPete, the surviving entity, so the $30,000 excess was the additional paid-in capital of the pooledentity. Also, the $80,000 maximum retained earnings was pooled.

CASE 4: CONSOLIDATION; PAID-IN CAPITAL EXCEEDS STOCK ISSUEDPete Corporation issued 17,000 shares of $10 par capital stock, 11,000 to Jake and 6,000 to Kate,for their net assets. The stockholders’ equity of Pete in this case was the same as Jake’s stock-holders’ equity in Case 2. Pete recorded the consolidation as follows:

Net assets (+A) 260

Capital stock, $10 par (+SE) 170

Additional paid-in capital (+SE) 10

Retained earnings (+SE) 80

To record issuance of 11,000 shares to Jake and 6,000

shares to Kate in a business combination accounted

for as a pooling of interests.

The $180,000 total paid-in capital of the combining entities exceeded the $170,000 capital stockof Pete; therefore, the $10,000 excess was the additional paid-in capital of the pooled entity, andthe $80,000 maximum retained earnings was pooled.

CASE 5: CONSOLIDATION; STOCK ISSUED EXCEEDS PAID-IN CAPITALPete Corporation issued 19,000 shares of $10 par capital stock, 12,000 to Jake and 7,000 to Kate,for their net assets. Pete’s stockholders’ equity in this case was the same as Jake’s stockholders’equity in Case 3. The entry on Pete’s books to record the pooling was as follows:

Net assets (+A) 260

Capital stock, $10 par (+SE) 190

Retained earnings (+SE) 70

To record issuance of 12,000 shares to Jake and 7,000

shares to Kate in a business combination accounted

for as a pooling of interests.

The $190,000 capital stock of Pete, the surviving entity, exceeded the $180,000 total paid-incapital of Jake and Kate, so the maximum pooled retained earnings was reduced by the $10,000excess to $70,000, and the pooled entity had no additional paid-in capital.

SUMMARY BALANCE SHEETS A summary balance sheet for the surviving entity in each of the fivepooling of interests business combinations is shown in Exhibit 3.

TREASURY STOCK IN A POOLING Under the provisions of APB Opinion No. 16, a corporation thatdistributed treasury stock in a pooling of interests would first account for those shares as retired sothat their issuance would be recorded in the same manner as previously unissued stock.3

STOCK OF ONE COMBINING COMPANY HELD BY ANOTHER COMBINING COMPANY The method ofaccounting for the stock of one combining company held by another combining company dependson whether the stock is stock of the surviving entity. An investment in the common stock of the sur-viving entity is returned to the surviving company in the combination and is treated as treasury

6 ADVANCED ACCOUNTING

EXHIBIT 1-3Summary BalanceSheets for theFive Pooling ofInterests Cases

Merger Jake’s Books Consolidation Pete’s Books

Case 1 Case 2 Case 3 Case 4 Case 5

Net assets $260 $260 $260 $260 $260

Capital stock, $10 par $170 $190 $150 $170 $190

Additional paid-in capital 10 — 30 10 —

Retained earnings 80 70 80 80 70

Stockholders’ equity $260 $260 $260 $260 $260

4Ibid., paragraph 55.

stock of the combined entity. Alternatively, an investment by the surviving entity in another com-bining company is treated as stock retired as part of the combination.4

Let us illustrate this requirement by assuming that Kam Corporation owned 200 shares of LaxCorporation common stock at the consummation of the Kam and Lax merger. Kam carried itsinvestment in Lax account at its $3,000 cost. Summary data (in thousands) for Kam and Lax areas follows:

Kam Lax

Investment in Lax $ 3Other assets 197 $300

Total $200 $300Capital stock, $10 par $100 $200Additional paid-in capital 50 30Retained earnings 50 70

Total $200 $300

If Kam was the surviving entity and issued 19,800 shares to Lax (a 1 : 1 exchange ratio), thepooling of interests merger was recorded on Kam’s books as follows:

Net assets (+A) 300

Capital stock, $10 par (+SE) 198

Additional paid-in capital (+SE) 29

Retained earnings (+SE) 70

Investment in Lax (�A) 3

To record merger with Lax Corporation.

If Lax was the surviving entity and issued 10,000 shares of its own stock for 10,000 shares of Kam(a 1 : 1 exchange ratio), the pooling of interests merger was recorded on the books of Lax as follows:

Net assets (+A) 197

Treasury stock (�SE) 3

Capital stock, $10 par (+SE) 100

Additional paid-in capital (+SE) 50

Retained earnings (+SE) 50

To record merger with Kam Corporation.

In each of these examples, the net assets of the surviving entity were $3,000 less than therecorded assets of the combining companies. The related effect on the combined stockholders’equity was to reduce paid-in capital when the investment was in the combining company and torecord treasury stock when the investment was in stock of the surviving entity.

Expenses Related to Pooling CombinationsThe costs incurred to effect a business combination and to integrate the operations of the com-bining companies in a pooling were expenses of the combined corporation. This treatment was

Electronic Supplement to Chapter 1 7

5APB Opinion No. 20, “Accounting Changes,” paragraph 34. Restatement of all prior-period financial statements pre-sented is required for a change in the reporting entity if the results are material.

required by APB Opinion No. 16 and is consistent with the pooling concept of combining opera-tions and shareholders’ interests without an acquisition and without raising new capital.

For example, costs of registering and issuing securities, providing stockholders with informa-tion, paying accountants’ and consultants’ fees, and paying finder’s fees to those who discoveredthe “combinable” situation were recorded as expenses of the combined entity in the period inwhich they were incurred. If Jake or Pete Corporation in the preceding cases had incurred accoun-tants’ fees, consultants’ fees, costs of security registration, and other costs of combining, the com-bined net assets of the surviving entity would have been less and combined expenses would havebeen greater. However, the capital stock and pooled retained earnings recorded at April 1, 2001,would have been the same.

As discussed previously, financial statements of a pooled entity for the year of combinationshould have been presented as if the combination had been consummated at the beginning of theperiod. In addition, if comparative financial statements for prior years were presented, they musthave been restated on a combined basis with disclosure of the fact that the statements of previouslyseparate companies had been combined.5

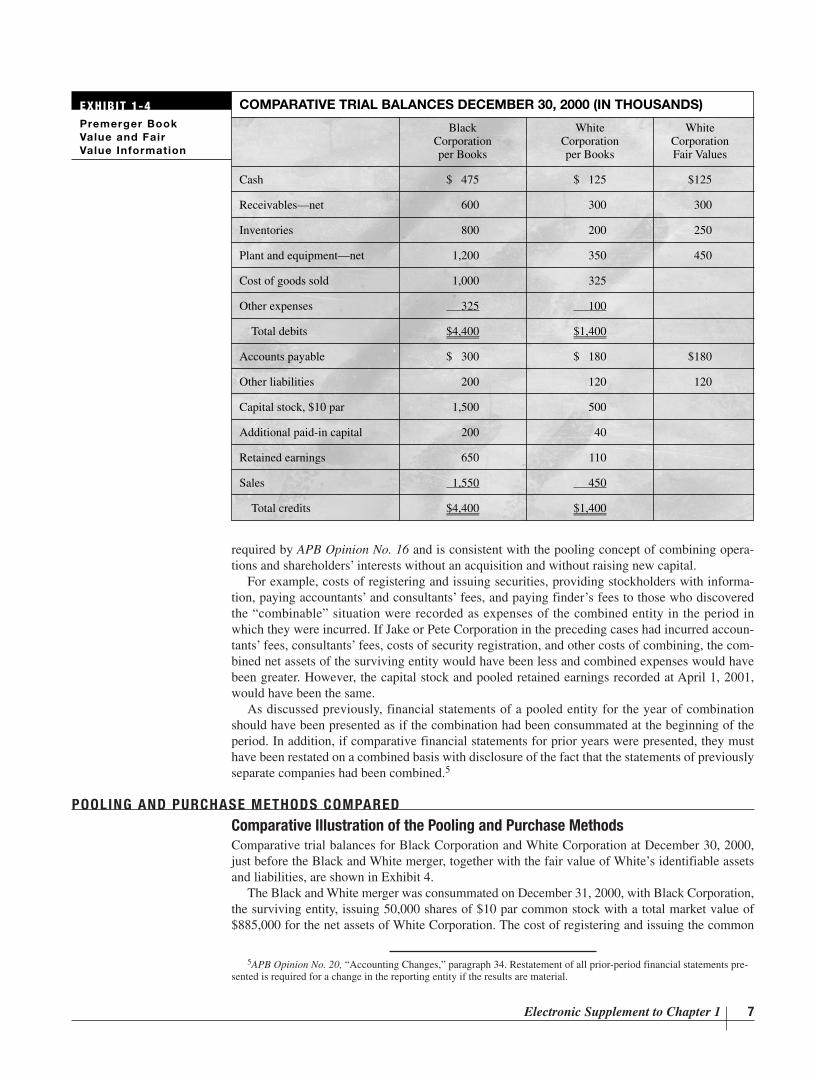

POOLING AND PURCHASE METHODS COMPAREDComparative Illustration of the Pooling and Purchase MethodsComparative trial balances for Black Corporation and White Corporation at December 30, 2000,just before the Black and White merger, together with the fair value of White’s identifiable assetsand liabilities, are shown in Exhibit 4.

The Black and White merger was consummated on December 31, 2000, with Black Corporation,the surviving entity, issuing 50,000 shares of $10 par common stock with a total market value of$885,000 for the net assets of White Corporation. The cost of registering and issuing the common

COMPARATIVE TRIAL BALANCES DECEMBER 30, 2000 (IN THOUSANDS)

Black White WhiteCorporation Corporation Corporationper Books per Books Fair Values

Cash $ 475 $ 125 $125

Receivables—net 600 300 300

Inventories 800 200 250

Plant and equipment—net 1,200 350 450

Cost of goods sold 1,000 325

Other expenses 325 100

Total debits $4,400 $1,400

Accounts payable $ 300 $ 180 $180

Other liabilities 200 120 120

Capital stock, $10 par 1,500 500

Additional paid-in capital 200 40

Retained earnings 650 110

Sales 1,550 450

Total credits $4,400 $1,400

EXHIBIT 1-4Premerger BookValue and FairValue Information

8 ADVANCED ACCOUNTING

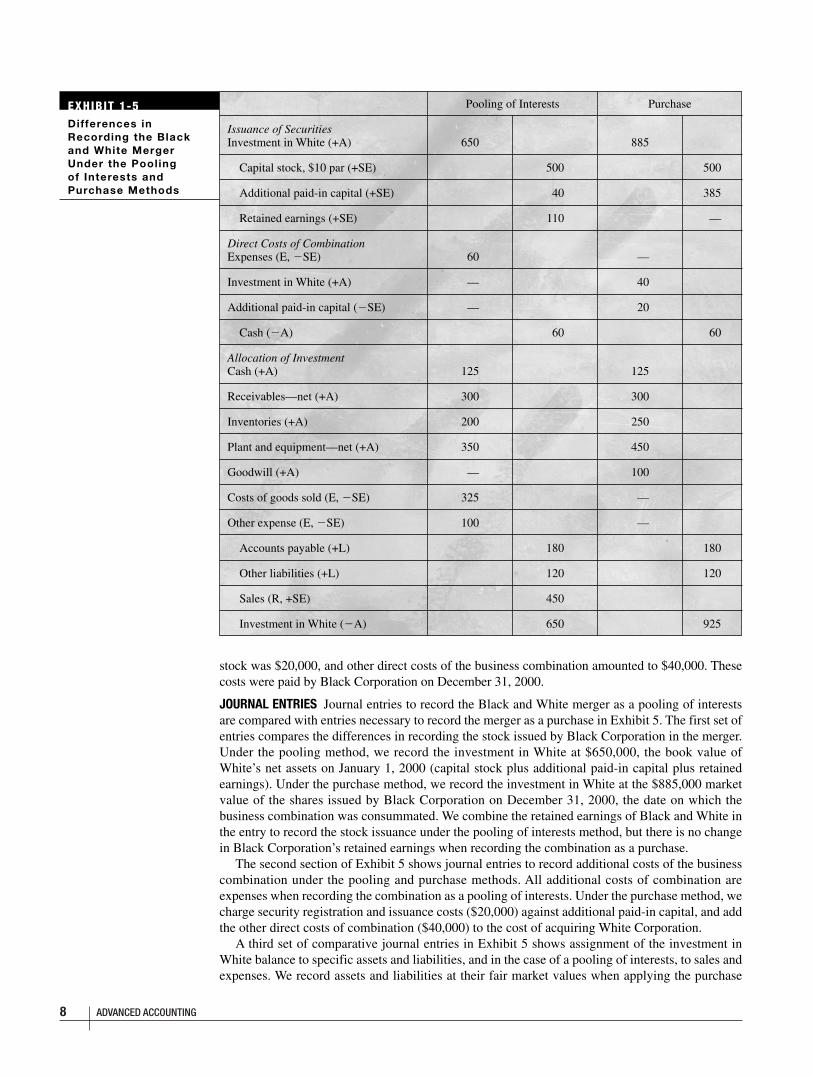

Pooling of Interests Purchase

Issuance of SecuritiesInvestment in White (+A) 650 885

Capital stock, $10 par (+SE) 500 500

Additional paid-in capital (+SE) 40 385

Retained earnings (+SE) 110 —

Direct Costs of CombinationExpenses (E, �SE) 60 —

Investment in White (+A) — 40

Additional paid-in capital (�SE) — 20

Cash (�A) 60 60

Allocation of InvestmentCash (+A) 125 125

Receivables—net (+A) 300 300

Inventories (+A) 200 250

Plant and equipment—net (+A) 350 450

Goodwill (+A) — 100

Costs of goods sold (E, �SE) 325 —

Other expense (E, �SE) 100 —

Accounts payable (+L) 180 180

Other liabilities (+L) 120 120

Sales (R, +SE) 450

Investment in White (�A) 650 925

EXHIBIT 1-5Differences inRecording the Blackand White MergerUnder the Poolingof Interests andPurchase Methods

stock was $20,000, and other direct costs of the business combination amounted to $40,000. Thesecosts were paid by Black Corporation on December 31, 2000.

JOURNAL ENTRIES Journal entries to record the Black and White merger as a pooling of interestsare compared with entries necessary to record the merger as a purchase in Exhibit 5. The first set ofentries compares the differences in recording the stock issued by Black Corporation in the merger.Under the pooling method, we record the investment in White at $650,000, the book value ofWhite’s net assets on January 1, 2000 (capital stock plus additional paid-in capital plus retainedearnings). Under the purchase method, we record the investment in White at the $885,000 marketvalue of the shares issued by Black Corporation on December 31, 2000, the date on which thebusiness combination was consummated. We combine the retained earnings of Black and White inthe entry to record the stock issuance under the pooling of interests method, but there is no changein Black Corporation’s retained earnings when recording the combination as a purchase.

The second section of Exhibit 5 shows journal entries to record additional costs of the businesscombination under the pooling and purchase methods. All additional costs of combination areexpenses when recording the combination as a pooling of interests. Under the purchase method, wecharge security registration and issuance costs ($20,000) against additional paid-in capital, and addthe other direct costs of combination ($40,000) to the cost of acquiring White Corporation.

A third set of comparative journal entries in Exhibit 5 shows assignment of the investment inWhite balance to specific assets and liabilities, and in the case of a pooling of interests, to sales andexpenses. We record assets and liabilities at their fair market values when applying the purchase

Electronic Supplement to Chapter 1 9

method and at their book values under the pooling method. We record the excess of investment cost($925,000) over the fair value of identifiable net assess ($825,000) as goodwill under the purchasemethod. The excess of fair value over historical cost to White, which was allocated to inventories($50,000) and to plant and equipment ($100,000) under purchase accounting, also will increasefuture expenses and decrease future income as compared with the pooling method. Thus, income ofBlack Corporation in subsequent years will be lower if we record the Black and White merger as apurchase rather than a pooling of interests.

FINANCIAL STATEMENTS Exhibit 6 compares the combined financial statements for BlackCorporation for 2000 for the purchase and pooling methods. The differences in the comparativeincome statements result from the combining of sales and expenses under the pooling method but

BLACK CORPORATION COMPARATIVE FINANCIAL STATEMENTSFOR THE YEAR ENDED DECEMBER 31, 2000

Pooling ofInterests PurchaseMethod Method

Income StatementSales $ 2,000 $ 1,550

Cost of sales (1,325) (1,000)

Other expenses (485) (325)

Net income $ 190 $ 225

Retained Earnings StatementRetained earnings January 1, 2000 (as reported) $ 650 $ 650

Increase from pooling 110

Retained earnings January 1, 2000 (as restated) 760

Net income 190 225

Retained earnings December 31, 2000 $ 950 $ 875

Balance SheetAssets

Cash $ 540 $ 540

Receivables—net 900 900

Inventories 1,000 1,050

Plant and equipment—net 1,550 1,650

Goodwill — 100

Total assets $ 3,990 $ 4,240

Liabilities and stockholders’ equityAccounts payable $ 480 $ 480

Other liabilities 320 320

Capital stock, $10 par 2,000 2,000

Additional paid-in capital 240 565

Retained earnings 950 875

Total liabilities and stockholders’ equity $ 3,990 $ 4,240

EXHIBIT 1-6Comparative FinancialStatements forthe Black and WhiteMerger in the Year ofBusiness Combination

10 ADVANCED ACCOUNTING

7APB Opinion No. 16, paragraph 64.

not under purchase accounting. An additional difference is that we charge additional costs of com-bination to expense under the pooling method.

Total assets of Black Corporation at December 31, 2000, were $4,240,000 under the purchasemethod and $3,990,000 under the pooling method. This $250,000 balance-sheet difference is theresult of allocating the excess of cost over book value acquired to inventories, plant and equipment,and goodwill under the purchase method.

The comparative balance sheets in Exhibit 6 show additional paid-in capital of $240,000and $565,000 under the pooling and purchase methods, respectively. Additional paid-in capitalunder the pooling method is equal to the excess of paid-in capital of the combining companies($2,240,000) over the capital stock of the combined entity ($2,000,000). The $565,000 additionalpaid-in capital under purchase accounting is equal to the $200,000 beginning balance, plus$385,000 from the issuance of the 50,000 shares in excess of par value, less the $20,000 cost ofregistering and issuing the securities in the business combination.

The pooled retained earnings of Black Corporation exceed the retained earnings of Black underthe purchase method by $75,000. This difference stems from combining retained earnings under thepooling method, as well as from the income differences discussed earlier. Note that significant differ-ences in accounting for the retained earnings of a combined entity are possible under generallyaccepted accounting principles. Accordingly, users of financial statements of combined entitiesshould be careful not to interpret the reported retained earnings balances as amounts legally availablefor dividends. Such interpretations are questionable when the reports are for separate legal entities,and they are even more suspect when we combine two or more entities into one accounting entity.

DISCLOSURE REQUIREMENTS FOR A POOLINGThe combined corporation must disclose that the business combination was accounted for as apooling of interests. In addition, financial statement notes for the period of pooling should includethe names of the combined companies, a description of the shares issued, the details of the resultsof operations of the separate companies before pooling, the nature of any asset adjustments toadopt the same accounting practices, the details of the effect on retained earnings of changing thefiscal period of a combining company, and a reconciliation of the issuing company’s revenue andearnings with combined amounts after the pooling. When a new corporation was formed in a pool-ing, this last disclosure requirement could be met by disclosing the earnings of the separate com-panies that comprised the combined earnings for the period.7

A S S I G N M E N T M A T E R I A L

W 1-1 Explain the basic differences between the purchase and pooling of interests methods of accountingfor business combinations.

W 1-2 Identify the twelve conditions that must be met for a business combination to be accounted for as apooling of interests.

W 1-3 Ordinarily, the retained earnings of the surviving corporation in a pooling of interests would beequal to the combined retained earnings of the combining companies. Under what conditionswould be combined retained earnings be less than or greater than the total retained earnings of thecombining companies?

W 1-4 The term instant earnings has been cited as an undesirable feature of the pooling of interests method.In what sense does pooling of interests accounting give rise to so-called instant earnings? Explain.

W 1-5 Compare the costs of effecting a business combination under the purchase and pooling of interestsmethods.

W 1-6 Why are purchase and pooling of interests business combinations accounted for differently?

W 1-7 Explain how the direct and indirect costs of combination are recorded for purchase business com-binations and for poolings of interests.

Electronic Supplement to Chapter 1 11

W 1-8 1. Which one of the following items is a requirement for a pooling of interests?a. Fair value accountingb. Amortization of goodwillc. Exchange of common sharesd. Dissolution of all but one of the combining entities

2. A pooling of interests was consummated with the stockholders of the other combining cor-poration exchanging two of their shares for each share of stock of the issuing company. Theexchange ratio in this pooling is:a. 2b. 0.5c. 3d. 1.5

3. The issuing company in a pooling of interests may issue treasury shares for the stock of theother combining corporation if the treasury stock is:a. Acquired for cash to affect the business combinationb. Accounted for on a cost basisc. Reissued at its current market valued. First retired and then reissued

4. Corporation A and Corporation B combined in 2000 in a pooling of interests business com-bination. Which of the following dates is the date of initiation of the plan for this businesscombination?a. A consulting firm arranged a meeting between the officers and directors of the two com-

panies on January 5, 2000.b. A public announcement was made on March 1, 2000, that the exchange ratio would be

1.2 to 1.c. Stockholders were notified that the officers of the two companies had agreed upon the

1.2 to 1 exchange ratio on March 15, 2000.d. Stockholders of the two companies voted to accept the terms of the proposed business

combination on May 15, 2000.

5. Which one of the following criteria is not a condition for a pooling of interests?a. Each of the combining firms must be autonomous.b. The combination must be completed in a single transaction or in accordance with a spe-

cific plan that is completed within one year of its initiation.c. Each combining corporation other than the issuing corporation must be dissolved as of

the date of which the combination is consummated.d. The proportionate interest of each individual common stockholder in each of the combin-

ing companies remains the same as a result of stock exchanged to effect the combination.

6. When retained earnings of a combining company in a pooling are adjusted to conformaccounting principles with those of the pooled entity, the accounting change:a. Disqualifies the combination for pooling of interests treatmentb. Is recorded as an initial entry in the pooled firm’s recordsc. Is unacceptable if the effect is to increase retained earningsd. Is acceptable if the change would have been appropriate for the separate company

W 1-9 1. The criteria for a pooling of interests are not met if:a. The combined entity plans to sell duplicate facilitiesb. The issuing company pays cash for 1% of the shares of the other combining company

between the initiation and consummation datesc. The voting rights relating to the shares issued to effect the pooling will not be effective

until a year after consummation of the pland. The business combination takes more than six months from the date of initiation to complete

2. The exchange ratio in a pooling of interests is the:a. Ratio of the market value per share of the issuing company’s stock to the market value per

share of the combining company’s stock

12 ADVANCED ACCOUNTING

b. Ratio of the total market value of stock issued to the total market value of stock receivedc. Ratio of the number of shares of the issuing company’s stock to be exchanged for each

share of the other combining company’s stock on the date of consummationd. Ratio of the number of shares of the acquired company’s stock to be exchanged for each

share of the issuing company’s stock

3. The expensing of indirect costs of a business combination is required for:a. Purchase but not pooling combinationsb. Pooling but not purchase combinationsc. Both purchase and pooling combinationsd. Neither purchase nor pooling combinations

4. The maximum retained earnings that can be combined in a pooling of interests is reduced bythe excess of:a. Paid-in capital of the combining entities over the capital stock of the pooled entityb. Additional paid-in capital of the combining entities over capital stock of the pooled entityc. Capital stock of the pooled entity over total paid-in capital of the combining entitiesd. Capital stock of the pooled entity over additional paid-in capital of the combining

entities

5. In a pooling of interests business combination, stock of the other combining company heldby the issuing corporation is treated as: a. An investment to be accounted for under the equity methodb. Stock retired in the poolingc. Treasury stock of the pooled entityd. None of the above

6. The capital stock of the surviving entity in a 100% pooling of interests is equal to:a. Capital stock of the issuing company plus the capital stock issued for shares of the other

combining companiesb. Combined capital stock of the combining entitiesc. Capital stock of the pooled entity over the paid-in capital of the other combining entitiesd. None of the above

7. Immediately before the business combination of Posey and Sharrel Corporations in whichSharrel Corporation was dissolved, Posey held 500 shares of Sharrel common stock, andSharrel held 200 shares of Posey common stock. Posey issued 4,750 of its shares for theremaining 9,500 outstanding shares of Sharrel when the business combination was consum-mated. Which statement regarding this pooling of interests is correct:a. The 500 shares of Sharrel stock held by Posey will be treated as shares retired in the pool-

ing of interests.b. The 200 shares of Posey stock held by Sharrel will be treated as treasury shares of the

pooled entity.c. The exchange ratio in this pooling is 0.5 to 1.d. All of the above statements are correct.

W 1-10 Pappy Corporation exchanged 11,000 of its common shares for 33,000 common shares ofSnippy Corporation in consummation of a business combination on July 1, 2000. Just beforeconsummation, Pappy held 2,000 shares of Snippy common stock and Snippy held 1,000 sharesof Pappy common stock. After the business combination, 2,000 shares of Snippy stock remainedoutstanding.

R E Q U I R E D1. What was the exchange ratio in the business combination?

2. How many shares of Snippy common stock were outstanding before consummation of the businesscombination?

3. How many shares will be assumed to be exchanged under the “substantially all” test for a pooling?

4. Is the “substantially all” test for a pooling of interests met in the Pappy-Snippy business combination?

Electronic Supplement to Chapter 1 13

W 1-11 Baloney Corporation and Nayle Company enter into a plan of business combination in whichBaloney will issue one share of common stock for every three shares of Nayle common stock. Onthe date of initiation of the business combination, Baloney held 500 shares of Nayle’s commonstock, and Nayle held 100 shares of Baloney common stock. Between the date of initiation and thedate of consummation, Baloney purchased an additional 400 shares of Nayle common in the stockmarket. Nayle had 50,000 shares of common stock outstanding throughout the period. On the dateof consummation, Baloney issued 16,000 shares of common stock for 48,000 shares of Nayle’scommon stock. Nayle’s old stockholders still hold, 1,100 shares of Nayle common.

R E Q U I R E D : How many shares of Nayle stock are assumed to be exchanged in the combination under the“substantially all” test for a pooling of interests?

W 1-12 [AICPA adopted]1. Dan Corporation offered to exchange two shares of Dan common stock for each share of

Boone Company common stock. On the initiation date, Dan held 3,000 shares of Boonecommon and Boone held 500 shares of Dan common. In later cash transactions, Dan pur-chased 2,000 shares of Boone common and Boone purchased 2,500 shares of Dan common.At all times, the number of common shares outstanding was 1,000,000 for Dan and 100,000for Boone. After consummation, Dan held 100,000 Boone common shares. The number ofshares considered exchanged in determining whether this combination should be accountedfor by the pooling of interests method is:a. 190,000b. 95,000c. 93,500d. 89,000

2. The business combination of Jax Company—the issuing company—and the Bell Corporationwas consummated on March 14, 2000. At the initiation date, Jax held 1,000 shares of Bell. Ifthe combination is accounted for as a pooling of interests, the 1,000 shares of Bell held by Jaxwill be accounted for as:a. Retired stockb. 1,000 shares of treasury stockc. (1,000/the exchange rate) shares of treasury stockd. (1,000 � the exchange rate) shares of treasury stock

W 1-13 Carrier Corporation issued 100,000 shares of $20 par common stock for all the outstandingstock of Homer Corporation in a business combination consummated on July 1, 2000. CarrierCorporation common stock was selling at $30 per share at the time the business combination wasconsummated. Out-of-pocket costs of the business combination were as follows:

Finder’s fee $50,000Accountants’ fee (advisory) 10,000Legal fees (advisory) 20,000Printing costs 5,000SEC registration costs and fees 12,000

Total $97,000

1. If the business combination was treated as a pooling of interests, the acquisition cost of thecombination would have been:a. $3,097,000b. $2,097,000c. $2,080,000d. None of the above

2. If the combination was treated as a purchase, the acquisition cost of the combination wouldhave been:a. $3,097,000b. $3,080,000c. $3,017,000d. None of the above

14 ADVANCED ACCOUNTING

W 1-14 Franklin and Harlow Corporations were combined on April 1, 2000, in a pooling of interests busi-ness combination, and Harlow was dissolved. For the year 2000, the companies had the followingearnings records:

Franklin Corporation (January 1–April 1) $ 40,000Franklin Corporation (April 1–December 31) 660,000Harlow Corporation (January 1–April 1) 200,000

1. Franklin, the surviving corporation, would have reported income for 2000 of:a. $660,000b. $700,000c. $860,000d. $900,000

2. Franklin’s financial statement notes for 2000 should have included:a. A description of all classes of preferred and common stock exchanged in the consumma-

tion of the poolingb. A reconciliation of Franklin’s revenue and earnings with combined amounts after the

pooling of interestsc. A description of any contingent payments that may result in 2001 from the pooling

of interestsd. The cost of acquiring Harlow

W 1-15 Patter Corporation issued 500,000 shares of its own $10 par common stock for all the outstandingstock of Simpson Corporation in a merger consummated on July 1, 2000. On this date, Patter stockwas quoted at $20 per share. Summary balance sheet data for the two companies at July 1, 2000,just before combination, were as follows (in thousands):

Patter Simpson

Current assets $18,000 $1,500Plant assets 22,000 6,500Total assets $40,000 $8,000Liabilities $12,000 $2,000Common stock, $10 par 20,000 3,000Additional paid-in-capital 3,000 1,000Retained earnings 5,000 2,000Total equities $40,000 $8,000

1. If the business combination was treated as a pooling of interests, the pooled retained earningsimmediately after the combination would have been:a. $5,000b. $6,000c. $7,000d. $8,000

2. If the business combination was treated as a pooling of interests, the additional paid-in capi-tal immediately after the combination would have been:a. $5,000b. $4,000c. $3,000d. $2,000

3. If the business combination was treated as a purchase and Simpson’s identifiable net assetshad a fair value of $9,000,000, Patter’s balance sheet immediately after the combinationwould have showed goodwill of:a. $1,000b. $2,000c. $3,000d. $4,000

Electronic Supplement to Chapter 1 15

W 1-16 IceAge Company issued 120,000 shares of $10 par common stock with a fair value of $2,550,000for all the voting common stock of Jester Company. In addition, IceAge incurred the followingadditional costs:

Legal fees to arrange the business combination $25,000Cost of SEC registration, including

accounting and legal fees 12,000Cost of printing and issuing new stock certificates 3,000Indirect costs of combining, including allocated

overhead and executive salaries 20,000

Immediately before the business combination in which Jester Company was dissolved, Jester’sassets and equities were as follows (in thousands):

Book Value Fair Value

Current assets $1,000 $1,100Plant assets 1,500 2,200Liabilities 300 300Common stock 2,000Retained earnings 200

R E Q U I R E D : Assume that the business combination is a pooling of interests. Prepare all journal entries onIceAge’s books to record the business combination.

W 1-17 On January 1, 2000, Placate Corporation held 2,000 shares of Service Corporation common stockacquired at $15 per share several years earlier. On this date, Placate issued 1.5 of its $10 par sharesof each of the other 98,000 outstanding shares of Service in a pooling of interests in which ServiceCorporation was dissolved. Service Corporation’s after-closing trial balance on December 31,1999, consisted of the following (in thousands):

Current assets $ 800Plant and equipment—net 1,500Liabilities $ 200Capital stock, $5 par 500Additional paid-in capital 1,000Retained earnings 600

$2,300 $2,300

R E Q U I R E D : Prepare a journal entry (or entries) on Placate’s books to account for the pooling of interests.(Hint: Do not forget to consider the 2,000 shares of Service held by Placate on January 1, 2000.)

W 1-18 Blair Corporation, the surviving company in a pooling of interests, exchanged 20,000 of itstreasury shares for 10,000 shares of Tuby Corporation’s common stock on July 1. At the timeof the exchange, Tuby held 1,000 shares of Blair stock acquired several years ago at $10 pershare. The equity accounts of Blair and Tuby immediately before the pooling were as follows(in thousands):

Blair Tuby

Capital stock, $10 par $700 $100Additional paid-in capital 40 74Retained earnings 200 45

940 219Treasury stock, 20,000 shares 180

Total stockholders’ equity $760 $219

R E Q U I R E D : Prepare the stockholders’ equity section of Blair’s balance sheet immediately after the busi-ness combination.

W 1-19 Tansy Corporation issued its own common stock for all the outstanding shares of Vatters Corporationin a pooling of interests business combination on January 1, 2000. The balance sheets of the two com-panies at December 31, 1999 were as follows (in thousands):

16 ADVANCED ACCOUNTING

Tansy Vatters

Current assets $15,000 $ 4,000Plant assets—net 40,000 6,000

Total assets $55,000 $10,000Liabilities $10,000 $ 3,000Common stock, $10 par 30,000 4,000Additional paid-in capital 3,000 2,000Retained earnings 12,000 1,000

Total equities $55,000 $10,000

R E Q U I R E D : Prepare balance sheets for Tansy Corporation on January 1, 2000, immediately after the pool-ing of interests in which Vatters was dissolved under the following assumptions:

1. Tansy issued 800,000 of its common shares for all of Vatter’s outstanding shares.

2. Tansy issued 1,000,000 of its common shares for all of Vatters’s outstanding shares.

W 1-20 Gladfresh and Farmstone Corporations entered into a business combination accounted for as apooling of interests in which Farmstone was dissolved. Net assets and stockholders’ equities of thetwo companies immediately before the pooling follow (in thousands):

Gladfresh Farmstone

Net assets $1,000 $800Capital stock, $10 par $ 400 $200Additional paid-in capital 200 300Total paid-in capital 600 500Retained earnings 400 300

Total stockholders’ equity $1,000 $800

R E Q U I R E D :1. Prepare the journal entry on Gladfresh Corporation’s books to record the pooling with Farmstone if

Gladfresh issued 35,000, $10 par common shares in exchange for all Farmstone common shares.

2. Prepare the journal entry on Gladfresh Corporation’s books to record the pooling with Farmstone ifGladfresh issued 77,000, $10 par common shares in exchange for all Farmstone common shares.

W 1-21 Quatro Corporation initiated a plan to pool its interests with Tertio Corporation on January 1, 2000.On this date:

1. Quatro held 40,000 of Tertio’s 750,000 shares of authorized and issued common stock,acquired by Quatro at a cost of $600,000.

2. Tertio held 5,000 shares of Quatro’s $10 par common stock acquired at $60 per share.

3. Tertio held 50,000 shares of its own common stock (treasury shares) reacquired at $30 pershare.

On October 1, 2000, Quatro issued 330,000 of its $10 par shares for 660,000 shares of Tertio. Thestockholders’ equity of Tertio on October 1, just before the exchange of shares in which Tertio wasdissolved, consisted of the following:

Capital stock, $10 par $7,500,000Retained earnings 3,500,000Less: Treasury shares (1,500,000)

Total stockholders’ equity $9,500,000

The direct costs of the business combination consisted of $20,000 to register and issue the commonstock and $380,000 in other costs of combination. These costs were paid in cash by Quatro.

R E Q U I R E D :1. How many of Tertio’s shares are required to be exchanged to meet the “substantially all” test for a pool-

ing of interests?

2. How many of Tertio’s shares will be assumed to be exchanged to determine if the “substantially all” testis met?

Electronic Supplement to Chapter 1 17

3. Prepare the journal entries on Quatro’s books in summary form to record the business combination as a pool-ing. (Hint: Use an “other net assets” account to record Tertio’s net assets other than its investment in Quatro,and make a separate entry to account for Pond’s investment in Tertio and Tertio’s investment in Quatro.)

W 1-22 On January 2, 2000, Dual and Cowbell Corporations merged their operations through a businesscombination accounted for as a pooling of interests. The $300,000 direct costs of combination werepaid in cash by the surviving entity on January 2, 2000. At December 31, 1999, Cowhill held25,000 shares of Dual stock acquired at $20 per share. Summary balance sheet information forDual and Cowhill corporations at December 31, 1999, was as follows (in thousands):

Dual CowhillCorporation Corporation

Current assets $ 6,500 $ 4,500Plant and equipment—net 10,000 10,000Investment in Dual 500

Total assets $16,500 $15,000Liabilities $ 1,500 $ 3,000Common stock, $10 par 10,000 8,000Additional paid-in capital 2,000 3,000Retained earnings 3,000 1,000

Total equities $16,500 $15,000

R E Q U I R E D :1. Assume that the surviving corporation was Dual Corporation and that Dual issued 1,000,000 shares of its

own stock for all the outstanding shares of Cowhill Corporation.a. Prepare journal entries on the books of Dual Corporation to record the business combination.b. Prepare a balance sheet for Dual Corporation on January 2, 2000, immediately after the business

combination.

2. Assume that the surviving corporation was Cowhill Corporation and that Cowhill issued 1,200,000 sharesof its own stock for all the outstanding shares of Dual Corporation.a. Prepare journal entries on the books of Cowhill Corporation to record the business combination.b. Prepare a balance sheet for Cowhill Corporation on January 2, 2000, immediately after the business

combination.

W 1-23 Patio Corporation was formed on January 2, 2000, to consolidate the operations of EPA Corporationand Century Corporation. Summary balance sheets for the two companies at December 31, 1999,were as follows (in thousands):

EPA CenturyCorporation Corporation

AssetsCash $ 3,000 $ 1,000Receivables—net 3,500 1,500Inventories 6,000 7,000Land 1,000 2,000Building—net 7,500 3,000Equipment—net 3,000 5,500

Total assets $24,000 $20,000

Liabilities and Stockholders’ EquityAccounts payable $ 2,700 $ 2,300Bonds payable 3,000 —Capital stock 10,000 6,000Additional paid-in capital 4,300 2,700Retained earnings 4,000 9,000

Total liabilities andstockholders’ equity $24,000 $20,000

A D D I T I O N A L I N F O R M AT I O N1. The stockholders of the combining corporations agreed to the following plan of combination:

a. Stockholders of EPA Corporation were to receive 1,300,000 common shares of $10 par stock of PatioCorporation for their 5,000,000 shares of $2 par capital stock.

18 ADVANCED ACCOUNTING

b. Stockholders of Century Corporation were to receive 1,200,000 common shares of Patio Corporationfor their 1,000,000 shares of $6 stated value capital stock.

c. Both EPA Corporation and Century Corporation were to be dissolved.

2. The business combination was treated as a pooling of interests with January 2, 2000, as the date of initia-tion and consummation of the plan.

3. The inventories of Patio were to be maintained on a FIFO basis. Accordingly, Century’s December 31,1999, LIFO inventory was adjusted to its $8,000,000 FIFO cost.

4. Costs of registering and issuing securities in the combination amounted to $60,000, and other direct costsof combination totaled $140,000. These costs were paid by Patio on January 2, 2000, from cash obtainedfrom the other combining companies.

R E Q U I R E D1. Prepare journal entries on the books of Patio Corporation to:

a. Record the issuance of 1,300,000 shares to the stockholders of EPA Corporationb. Record the issuance of 1,200,000 shares to the stockholders of Century Corporationc. Record payment of the costs of business combination

2. Prepare a balance sheet for Patio Corporation at January 2, 2000, immediately after the business combi-nation has been consummated.

W 1-24 On January 1, 2000, Ainsley Corporation issued 500,000 shares of its capital stock for all of BikerCorporation’s outstanding shares and Biker was dissolved. The fair value of Ainsley’s commonstock on this date was $25 per share. The book values and fair values of Ainsley and Biker atDecember 31, 1999, were as follows (in thousands):

Ainsley Corporation Biker Corporation

Book Value Fair Value Book Value Fair Value

AssetsCash $ 3,000 $ 3,000 $ 1,000 $ 1,000Receivables—net 5,500 5,500 2,000 2,000Inventories (LIFO) 6,000 7,000 3,500 4,000Other current assets 1,500 1,500 500 600Plant assets—net 16,000 19,000 5,000 7,400

Total assets $32,000 $36,000 $12,000 $15,000

EquitiesAccounts payable $ 5,000 $ 5,000 $ 1,800 $ 1,800Other liabilities 3,800 4,000 3,200 3,000Capital stock, $10 par 15,000 3,000Other paid-in capital 3,000 1,200Retained earnings 5,200 2,800

Total equities $32,000 $12,000

R E Q U I R E D : Prepare comparative balance sheets for Ainsley Corporation immediately after the businesscombination, assuming that (a) the combination was a pooling of interests and (b) the combination was apurchase.