Electronic Components Industry in...

21

Commercial Wing, Consulate General of India in Frankfurt 6/22/2016 E LECTRONIC C OMPONENTS I NDUSTRY IN G ERMANY A Market Study The Study starts by giving a general idea of the electrical and electronics industry in Germany along with the most recent facts and figures. It deals with the topic of electronic components in specific. Further, it looks into the potential of increase in Indo-German trade in this sector.

Transcript of Electronic Components Industry in...

Commercial Wing, Consulate General of India in Frankfurt

6/22/2016

ELECTRONIC

COMPONENTS INDUSTRY

IN GERMANY

A Market Study

The Study starts by giving a general idea of the electrical and electronics

industry in Germany along with the most recent facts and figures. It deals

with the topic of electronic components in specific. Further, it looks into the

potential of increase in Indo-German trade in this sector.

6/22/2016

1

Table of Contents

1. Introduction

2. Characteristics of German Electronics Industry

Diverse

Broad Product Portfolio

Capital Goods focus

Intermediate Goods

3. Germany’s Semiconductor Industry

Applications

4. Automotive Electronics

5. Industry 4.0

6. Electronics Manufacturing Services

7. The German Electrical and Electronic Industry

in the International Arena

German Foreign Direct Investment into the E&E Industry Abroad

German Foreign Direct Investment into the E&E Industry Abroad

Trade with India

6/22/2016

2

ELECTRONIC COMPONENTS INDUSTRY IN

GERMANY

A Market Study

The German market for electrical and electronic products and systems is Europe’s

biggest, and the fifth largest worldwide with a turnover of approximately EUR 179

billion in 2015. Employing a workforce of more than 1.5 million at home and abroad,

it is the second largest industry segment in Germany by employees. Germany’s

electrical and electronics firms manufacture more than 100 thousand different

products and systems ranging from microelectronic components to electrical

household appliances, automation systems, lamps and luminaires, electronic medical

equipment, and automotive electronics.

Chart 1

6/22/2016

3

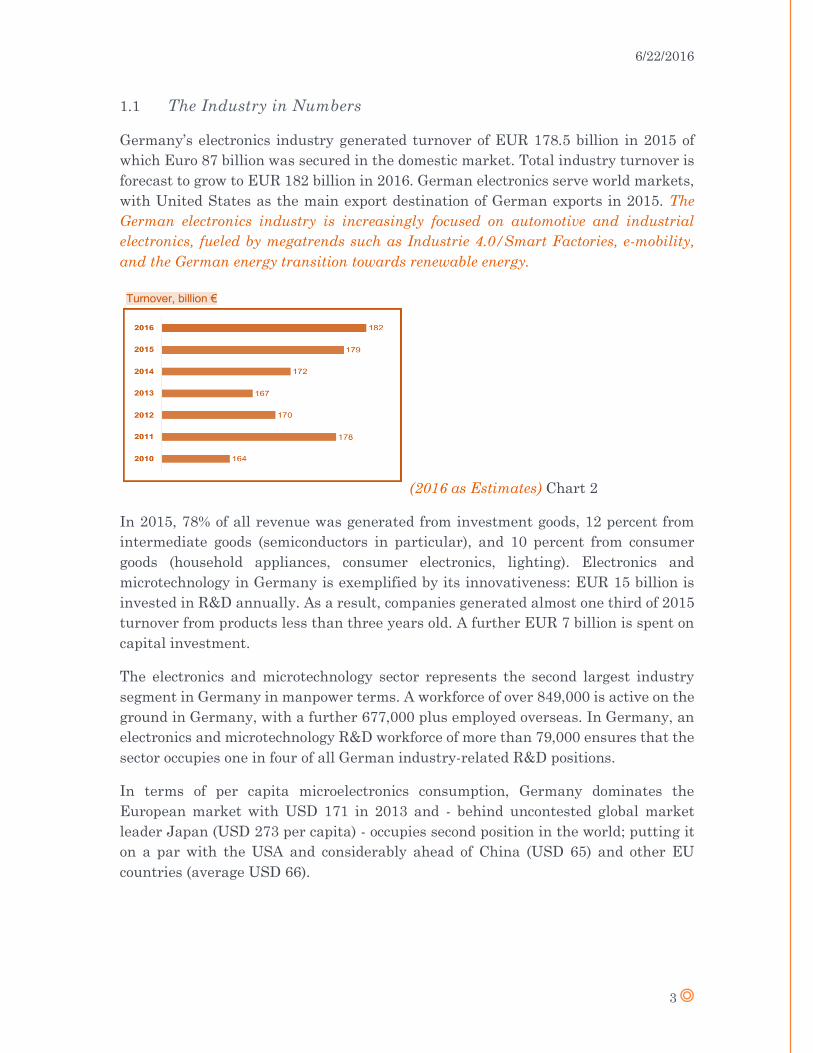

1.1 The Industry in Numbers

Germany’s electronics industry generated turnover of EUR 178.5 billion in 2015 of

which Euro 87 billion was secured in the domestic market. Total industry turnover is

forecast to grow to EUR 182 billion in 2016. German electronics serve world markets,

with United States as the main export destination of German exports in 2015. The

German electronics industry is increasingly focused on automotive and industrial

electronics, fueled by megatrends such as Industrie 4.0/Smart Factories, e-mobility,

and the German energy transition towards renewable energy.

(2016 as Estimates) Chart 2

In 2015, 78% of all revenue was generated from investment goods, 12 percent from

intermediate goods (semiconductors in particular), and 10 percent from consumer

goods (household appliances, consumer electronics, lighting). Electronics and

microtechnology in Germany is exemplified by its innovativeness: EUR 15 billion is

invested in R&D annually. As a result, companies generated almost one third of 2015

turnover from products less than three years old. A further EUR 7 billion is spent on

capital investment.

The electronics and microtechnology sector represents the second largest industry

segment in Germany in manpower terms. A workforce of over 849,000 is active on the

ground in Germany, with a further 677,000 plus employed overseas. In Germany, an

electronics and microtechnology R&D workforce of more than 79,000 ensures that the

sector occupies one in four of all German industry-related R&D positions.

In terms of per capita microelectronics consumption, Germany dominates the

European market with USD 171 in 2013 and - behind uncontested global market

leader Japan (USD 273 per capita) - occupies second position in the world; putting it

on a par with the USA and considerably ahead of China (USD 65) and other EU

countries (average USD 66).

6/22/2016

4

2.1 Characteristics of German Electronics Industry

2.1.1 Diverse sector with high economic importance

The German electrical and electronic industry plays an important part in Germany’s

industrial landscape. On the industry definition used by the German Electrical and

Electronic Manufacturers’ Association (ZVEI) it had nearly 849,000 employees and

generated sales of EUR 179 billion in 2015. That is equivalent to 16% and 13%

respectively of the German manufacturing industry totals. The electrical and

electronic industry is Germany’s second largest industrial sector in terms of the

number of employees and the third largest in terms of sales.

However, the figures alone do not reflect the industry’s importance. The goods it

manufactures are used in turn by companies in other sectors for their production. The

electrical and electronic industry plays a pivotal role in the economy and is closely

intertwined with other sectors. As a result of this interdependence it influences the

success of other sectors. Innovations in the electrical and electronic industry help

increase productivity in user industries. In many cases innovations there build on

innovations in the electrical and electronic industry. The semiconductor segment is a

prime example of the cross-sectional technologies the industry produces. Chips are

used in a wide range of products such as machines, computers, aircraft or telephones.

The electrical and electronic industry’s innovativeness therefore also influences the

competitiveness of other sectors.

2.1.2 Broad product portfolio in a heterogeneous industry

The electrical and electronic industry produces a raft of different goods. It is primarily

a capital goods industry, i.e. it manufactures goods that are used by other companies

for their production.

Capital goods include such products as electric motors, electronic control

equipment, switchgear, and power supply lines.

Electronic components, which include semiconductors, count as intermediate

goods. Intermediate goods are also used in the manufacture of goods. However,

in contrast to capital goods, they are integrated into these goods. The demand

for these two categories of goods comes from industrial companies. The general

economic environment determines the level of activity in the electrical and

electronic industry: in an upswing phase firms produce more and have above-

average demand for intermediate goods and capital goods from the electrical

and electronic industry; in the downswing phase demand declines.

The third category of goods is consumer goods. Here, the product spectrum

includes such goods as televisions, washing machines and light fittings and

electric lamps. Key factors for these goods are above all private consumption

and demographics. As the population declines, the potential for consumption

6/22/2016

5

declines. However, consumer goods – like products in the other two categories

– are also exported. Manufacturers therefore not only look at the development

of demand in Germany. In the electrical and electronic industry as a whole,

exports were to the tune of EURO 174.6 billion in 2015.

2.1.3 German electrical and electronic industry heavily focused on capital goods

According to the ZVEI classification, the German electrical and electronic industry

consists of 18 segments. They can be grouped together under the three production

categories of capital goods, intermediate goods and consumer goods. Capital goods is

the largest category, accounting for a good 78% of output in 2015. The electrical and

electronic industry is therefore more highly specialized on capital goods than

manufacturing industry as a whole where they account for only 46%. Intermediate

goods are the second largest group, accounting for 12% of production (German

manufacturing as a whole: 34%), followed by consumer goods with a share of 10%

(German manufacturing as a whole: 20%).

Almost half of the demand for German electrical and electronic capital goods came

from abroad in 2015. It should be borne in mind here that many of these goods are

integrated into products manufactured in other sectors that are in turn exported (e.g.

machines). The indirect export ratio is therefore higher than the 45% shown in the

statistics. Economic trends outside Germany are therefore very important. Europe is

the main export market for this category of goods owing to its geographical proximity

and the size of these countries‟ economies. However, in recent years Europe has lost

in relative weight in favor of the Americas and especially Asia. The fast-growing Asian

emerging markets especially need capital goods from Germany’s electrical and

electronic industry to develop their economies.

2.1.4 Intermediate goods: Electronic components

ZVEI only classifies one segment as intermediate goods: electronic components.

Semiconductors are an important part of this segment, accounting for 60% of its sales.

Production is very cyclical. However, the segment is not only exposed to general

economic cycles. The production systems for electronic components are very expensive

and very large. When new production facilities come on stream, they often add

sizeable capacities to the market. The problem is that investments in such plants are

often planned at the peak of the cycle but are not brought on stream until the next

down cycle. This gives rise to overcapacities. Not operating the fixed-cost-intensive

production plant at full capacity is usually very costly, so production is stockpiled.

However, because of the enormous pace of innovation in this segment the stockpiled

products rapidly lose value. There are few sectors apart from information technology

that face price erosion on such a scale as electronic components. Prices almost halved

just between 2003 and 2008. Demand for electronic components grew during this

6/22/2016

6

period, so the underlying sales trend still pointed up. However, manufacturers around

the world invested so optimistically in capacities at the turn of the millennium that

the cost block also rose and earnings came under pressure.

Chart 3

Electronic components are used in a wide range of products in the electrical and

electronic industry, also in the form of concealed controls and drives known as

embedded systems. Performing important control functions they play an essential role

as a key technology. The research-intensive segment is a driving force behind the

innovativeness of other sectors; many innovations are based on innovations in

semiconductors. For instance, more powerful chips pave the way for ever smaller

mobile phones that at the same time integrate the functions of navigator, mp3 player

and digital camera.

At 65%, the segment’s export ratio is well above the German electrical and electronic

industry average. Many electronic components are also exported indirectly in products

of other sectors. Asia is Germany’s second largest export market, after Europe, with

a share of 25%. However, Asia is steadily gaining in importance as a production

location, too, and is putting pressure on the competitiveness of German suppliers.

Western manufacturers are reacting by separating development and production. They

are outsourcing production to subcontractors, so-called foundries. They are large,

specialized production plants mostly located in Asia, especially in Taiwan. At home,

manufacturers are focusing on research and the development of new chips.

3.1 Germany’s Semiconductor Industry

Germany is the heart of the European semiconductor industry; ranking among the

top five locations worldwide. The country boasts an unparalleled density of world-

6/22/2016

7

leading device manufacturers and suppliers for materials, components, and

equipment across the value chain. Investment opportunities are many and varied –

covering everything from design and manufacturing to applications. Despite strong

competition from Europe and further afield, German semiconductor companies

remain the European leaders in terms of revenue, enjoying global share of almost five

percent. Across Europe, automotive and industrial semiconductors are the segments

with the strongest annual growth rates (7 percent and 6.5 percent respectively). High

domestic demand is a key driver in both segments.

3.1.1 Semiconductor Applications: Automotive Industry

Germany dominates the automotive semiconductor market with around 20 percent of

global market share. In 2013, the auto industry accounted for 42 percent of all

semiconductor revenue in Germany. Between 2000 and 2013 the German

semiconductor automotive segment grew by 65 percent, and is forecast to keep

growing by 43 percent for the period 2013 to 2018. Highly qualified engineering

personnel and customer proximity are the keys to this success. Constant growth in the

global automotive market and increasing demand for German-made high-quality

vehicles (particularly from emerging countries) have helped make Germany a highly

attractive location for automotive electronics research and investment. German car

manufacturer output is expected to increase continuously over the next years,

reaching an annual output level of more than 17 million vehicles in 2018.

3.1.2 Semiconductor Applications: Industry and power semiconductors

The second largest microelectronics segment in Germany is industrial electronics,

with almost 25 percent share of the domestic semiconductor industry. Strong growth

rates originating from a diversified domestic and international industrial base

consolidate Germany’s globally leading technological development position.

Historically the largest segments are building technology, automation, and electronic

payment systems (combined share of nearly 50 percent), followed by smaller but

promising application areas including power semiconductors.

The German power semiconductor market will provide a number of different market

opportunities in the years ahead. Abandoning nuclear energy by 2022 and switching

to renewable energy sources will require an enormous research effort and investment

in high-performance power semiconductors; especially metal oxide semiconductor field

effect transistors (MOSFET) and insulated gate bipolar transistors (IGBT). Because

they are applied in the high-voltage segment, IGBTs are encroaching into MOSFET

territory and gradually increasing their market share. Within the automotive sector,

the power semiconductor share of the total automobile cost is expected to reach

approximately 30 percent by the end of 2015. While the North American market is

very much in a mature stage, Europe and Germany are likely to drive market demand

for power semiconductors.

6/22/2016

8

Chart 4

4.1 The Automotive Electronics

The automotive electronics market is a cross-sectional industry of the electrical &

electronics and automotive industries. With market share of over 40 percent and

turnover of around EUR 7.2 billion, automotive electronics represents the biggest

6/22/2016

9

segment in the electronic component industry in Germany. With over 55 percent

market share and turnover of almost EUR 4 billion, semiconductor components are

the single most important electronic component within the industry. The worldwide

automotive electronics market is expected to grow at a much faster rate than the

automotive sector as a whole, with Germany becoming an even more important

market as a result.

According to the Federal Statistical Office, automotive electronics companies in

Germany generated turnover of around EUR 7.8 billion in 2012. While a major part

of the turnover is achieved domestically, a healthy export level of 33 percent has

helped stabilize the industry in recent times. The automotive electronics industry in

Germany has grown by 73 percent during the period 2000 to 2012. Moreover, the

global market for automotive electronics is expected to grow at a CAGR of 7.4 percent

for the period 2011 to 2016.

Of the approximately one thousand or so long-established companies in the

automotive industry, around 75 are specifically dedicated to the development and

production of electrical & electronic automotive components. Of course, a diverse

range of companies are active in creating a mixed product portfolio. The variety of

electrical & electronic applications creates niches for players with core value chain

competences – on a globally competitive scale.

Germany’s automotive electronics industry is globally connected. Thirty-three percent

of total industry revenue is generated overseas. And while the European Union - with

40 percent of total export revenue - remains an important market for automotive

electronics products, 60 percent of all exports are sent to non-EU countries. Since

1999, automotive electronics exports have become increasingly important as an

economic driver for the industry in times of domestic recession.

5.1 Industry 4.0

Industrie 4.0 is the German strategic initiative to take up a pioneering role in

industrial IT which is currently revolutionizing the manufacturing engineering sector.

The aim of Industrie 4.0’s strategy is to allow Germany to stay a globally competitive

high-wage economy. The Internet of Things is finding its way into production.

Semantic machine-to-machine communication revolutionizes factories by

decentralized control. Embedded digital product memories guide the flexible work

piece flow through smart factories, so that low-volume, high-mix production is realized

in a cost-efficient way. A new generation of industrial assistant systems using

augmented reality and multimodal interaction will help factory workers to deal with

the complexity of cyber-physical production and enable new forms of collaboration by

digital social media.

6/22/2016

10

The German electrical industry plays a key role when it comes to implementing smart

factories in the manufacturing and smart plants in processing industry. Its know-how,

equipment and systems are the enabler for the transition to digital production that

transcends geographical boundaries.

6.1 Electronic Manufacturing Services in Germany

Chart 5

The European Electronic Manufacturing Services (EMS) provider market is expected

to witness a CAGR of 10.1% between 2011 and 2017. Further demand for cost

6/22/2016

11

reduction will increase the role of EMS providers in the electronics market. Germany

hosts the entire value chain with Europe’s largest electronics industry accounting for

EUR 178 billion in 2011. German EMS accounts for 20% of the European EMS

market. Growth drivers include automotive, industrial, medical electronics and

renewable energy.

A low EMS provider penetration rate (less than 12%), and the increasing number of

electronic products are attractive factors for EMS providers in the automotive

electronics segment. The combination of medical and information technologies ensure

EMS providers with strong positions: contractors will benefit from product trends

such as increasing virtualization, mobile applications, real-time communication, and

diagnostics.

Trends in EMS Segments Due to the importance of electronic assembly cost

optimization for Original Equipment Manufacturers (OEMs), EMS future markets

will also include design, aftermarket services, and supply chain support.

Frost & Sullivan reports the following EMS segments to drive value and growth by

2020:

Supply chain support industry revenue is projected to increase from 8.5% in

2010 to 20% in 2020.

Design services are forecasted to increase from 5.5% in 2010 to 15% by 2020.

Aftermarket services are expected to account for 10% of the EMS provider

market revenue by 2020.

German EMS Industry Landscape is the host to approximately 350-400 EMS

companies. 80% of them are small enterprises with less than EUR 10 million annual

turnover. However, large companies (that have more than EUR 50 million annual

turnover) still constitute around 50% of industry turnover. The European EMS

provider market is expected to witness a CAGR of 10.1% between 2011 and 2017.

6/22/2016

12

Chart 6

6/22/2016

13

7.1 The German Electrical and Electronic Industry in the International

Arena

The global electrical and electronic industry counts as one of the world’s growth

drivers but it is a cyclical industry with strong fluctuations in growth rates. In the

nine years from 1998 to 2007 nominal output was increased by almost 50% to EUR

2,509 billion. That is an average annual rate of 4.5%. In the two boom years 1999 and

2000 the industry’s growth averaged 21%. Production then declined through to 2003

at an average annual rate of almost 8%. Over the next four years it then grew again

at a rate of 6.5% p.a. In 2010 and 11 the production increased by 15 and 11 per cent

respectively before again declining by 3 per cent in 2013. The growth rate in 2015 was

6%.

These ups and downs more or less match the development of world GDP. Only the

upward and downward swings are much more pronounced. It needs to be borne in

mind that when changes take place in the world market, exchange rates have an

important influence. The growth in trade in products of the electrical and electronic

industry was even stronger. The volume of trade almost doubled between 1998 and

2007. The trend shows the same pattern as production: massive growth at the turn of

the millennium followed by a downturn. World trade then picked up again after 2003

before declining slightly in 2007 and plunging dramatically during the world

recession.

7.1.1 Production mainly in Asia

The industry’s global development can be viewed from the supply side and the demand

side of the world market. On the supply side Asia is dominant: the region accounted

for 60% of global electrical and electronic industry output in 2007. China is by far

world’s largest producer. China accounts for half of Asia’s production and almost one-

third of world production in this sector. In the Asia region Japan follows in second

place with a share of 13% of global output, while Korea was third with a share of just

under 7%. Asia has increased its leadership in the global electrical and electronic

industry. Europe is the second largest production region, the Americas follow in third

place. Both regions account for about one-fifth of world output each.

Germany is clearly the biggest producer in Europe with a good 5% share of global

production. Its output is about three times that of the countries in second, third and

fourth place. These countries – Italy, France and the UK – have all seen stronger

declines in their share of output than Germany since 1998. So Germany has increased

its leadership in Europe.

6/22/2016

14

7.1.2 German E&E industry plays a leading international role

Germany’s electrical and electronic industry fared better than the average in the last

decade compared with countries with a similar level of development and with an

electrical and electronic industry of a similar size. The biggest competitor in Europe,

Italy, did not do as well. In France and the UK the electrical and electronic industry

even contracted during this period. The same applies to its chief competitors in Asia

(Japan) and the Americas (USA). However, Germany’s growth is slower compared

with the emerging markets. In China especially production grew at an average annual

rate of 23%, as compared to only 3.5% p.a. in Germany. Overall, despite its good

performance, Germany’s share of global output sank from 5.8% to 5.3%. The country

is the world’s fifth largest producer. However, its share of global exports, which has

always been higher than its share of global output, has remained constant and stood

at around 7.5%. Electrical and electronic products made in Germany continue to be in

strong demand abroad.

7.2 German Foreign Direct Investment into the E&E Industry Abroad

With 60.0 billion euros in 2012, the stock of German foreign direct investment (FDI)

into the Electrical and Electronic (E&E) Industry abroad exceeded its pre-year level

(of revised 58.7 billion euros) by 2.2 percent. Thus, it once again reached a new record

high. In the last ten years alone the involvement abroad has increased from 20.8

billion euros to two and a half times this amount. These figures are from the FDI

survey (2013) conducted by the Deutsche Bundesbank. In 2012 German investments

have been made in 1,506 E&E firms abroad. Those firms have employed a total of

692,000 people and generated annual sales of 136.5 billion euros. The number of firms

into which investments were made has grown slightly by 0.4 percent. Employment

and turnover, in contrast, have dropped slightly by 1.0 and 0.7 percent, respectively.

7.3 Trade with India

7.2.1 Electronics Component Industry in India

In India, the growth of the electronics industry has triggered the expansion of

electronic component industry as well. The electronic components produced in India

include, among others, Picture Tubes, Diodes, Transistors, Power devices, Resistors,

Capacitors, Switches, Relays, Connectors, Magnetic heads, etc.

Even though electronics Industry in India will reach $94.2 billion soon, sources say

65% of them are just imported from other countries. India Electronic and

Semiconductor Association and Indian government hope this import will reduce over

time, but lack of quality components will still be major problem.

Global trend on electronic market is going towards quality components, low cost

surface mount components, high speed manufacturing and automation.

6/22/2016

15

Chart 7: Indian Electronic Component Market

Electronic Component market in India: Indian market is approximately 5.4% of

world market worth of Rs. 48,000 Crore or USD 9.2 Billion in 2009-10.

Chart 8: Growth of Indian Electronics Component Market

Import: Most of the active components are imported. Because there are only few

companies that can manufacture with semiconductor & chip fabrication technology.

Non-original components have major share in this section, as they are cheap and

dumped in the market.

Also in section of passive components, electrolytic capacitor brands are old and didn’t

catch the new technology. For example, Kelton (Kerala Gov. Undertaking) is major

6/22/2016

16

brand of electrolytic capacitor in India. But you won’t find datasheet or product series

on their website. Also India is far behind the manufacturing of surface mount resistors

& capacitors. Most of them are imported.

Domestic: India has good capabilities in PCB, cable and some ferrite products. As

they are very heavy in weight it is not practical to import them.

Also Through hole resistors, connectors, pins, wires are mostly manufactured in India.

Import problems for small companies: Small manufacturing units have limited

requirement and stock capabilities. Sometimes their volume doesn’t meet the MOQ.

Here are some problems they are facing in Import

Can’t find right supplier which gives all components which are needed

Can’t be sure about original brand

Air cargo is expensive while sea cargo is impractical for small package

They need Exim certificate and custom clearing agents.

Sometimes they have to import far more than their inventory.

7.3.2 Trade with Germany

The trade between India and Germany in the field of electrical and electronic

components has a lot of potential.

Electrical, electronic equipment (Product Code ’85) 2010 2011 2012 2013 2014 2015

German exports to India 1176957 1516679 1202271 1106137 1145395 1274265

German exports to world 100920869 106704747 107599388 107645887 110808774 118250428

Indian exports to Germany 446884 420397 377440 386477 341880 358036

Indian exports to World 6556620 8431912 8368414 8489231 6772503 7149506

Indian Imports from World 19239004 23162114 23053741 22428114 24016132 32365633

Chart 9 Euro Thousand

6/22/2016

17

Chart 10

As can be seen above, trade in E&E components between India and Germany has been

increasing over the last 15 years especially the German exports to India. The Indian

exports to Germany (although a bigger part of Indian E&E exports to Germany i.e.

5% than German E&E exports to India i.e. 1%- Chart 11 and 12), are much smaller in

number. This can be due to a lower production level of E&E in India (leading to a lot

of import in this sector). This makes for a clear cut case for inviting German E&E

companies for investing in India since the production sector is not saturated and the

market potential is huge.

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Trade between India & Germany in Electronic Components

German exports to India Indian exports to Germany

Linear (German exports to India)

1%

99%

Chart 11: German Exports of Electronic Componets

Germanexports toIndia

Germanexports toworld

5%

95%

Chart 12: Indian Export of Electronic Components

Indian exportsto Germany

Indian exportsto World

6/22/2016

18

Chart 13

In chart 13, we see that the percentage of German imports to total Indian imports in

this sector is quite small. The reason might be cheaper imports from other Asian

markets. This makes for a wonderful case for German companies in this sector to come

and produce in India which will then entail cheaper final cost for their products.

To summarize from this section, Indian E&E industry is not very development but it

must be noticed that this is an intermediary industry. Many other manufacturing

companies can only be attracted to invest in India if there is sufficient supply of

standardized intermediary products. In this connection, increasing trade as well as

investment in India in this sector should be a priority. Germany, being a world player

can play an important part in this.

5%

95%

Electronic Components: Percentage of German E&E imports in total Indian

imports

India's import from Germany

Indian Imports from World

6/22/2016

19

Summary

Germany’s electronics industry generated turnover of EUR 178.5 billion in

2015 of which Euro 87 billion was secured in the domestic market. Total

industry turnover is forecast to grow to EUR 182 billion in 2016. German

electronics serve world markets, with United States as the main export

destination of German exports in 2015.

The electronics and micro technology sector represents the second largest

industry segment in Germany in manpower terms. A workforce of over 849,000

is active on the ground in Germany, with a further 677,000 plus employed

overseas. In Germany, an electronics and micro technology R&D workforce of

more than 79,000 ensures that the sector occupies one in four of all German

industry-related R&D positions.

According to the ZVEI classification, the German electrical and electronic

industry consists of 18 segments. They can be grouped together under the three

production categories of capital goods, intermediate goods and consumer goods.

Capital goods is the largest category, accounting for a good 78% of output in

2015. The electrical and electronic industry is therefore more highly

specialized on capital goods than manufacturing industry as a whole where

they account for only 46%. Intermediate goods are the second largest group,

accounting for 12% of production (German manufacturing as a whole: 34%),

followed by consumer goods with a share of 10% (German manufacturing as a

whole: 20%).

ZVEI only classifies one segment as intermediate goods: electronic

components. Semiconductors are an important part of this segment,

accounting for 60% of its sales. Production is very cyclical.

Germany is the heart of the European semiconductor industry; ranking among

the top five locations worldwide. The country boasts an unparalleled density of

world-leading device manufacturers and suppliers for materials, components,

and equipment across the value chain. Investment opportunities are many and

varied – covering everything from design and manufacturing to applications.

The automotive electronics market is a cross-sectional industry of the electrical

& electronics and automotive industries. With market share of over 40 percent

and turnover of around EUR 7.2 billion, automotive electronics represents the

biggest segment in the electronic component industry in Germany. With over

55 percent market share and turnover of almost EUR 4 billion, semiconductor

components are the single most important electronic component within the

industry.

The German electrical industry plays a key role when it comes to implementing

smart factories in the manufacturing and smart plants in processing industry.

6/22/2016

20

Its know-how, equipment and systems are the enabler for the transition to

digital production that transcends geographical boundaries.

The global electrical and electronic industry counts as one of the world’s growth

drivers but it is a cyclical industry with strong fluctuations in growth rates.

With 60.0 billion euros in 2012, the stock of German foreign direct investment

(FDI) into the Electrical and Electronic (E&E) Industry abroad exceeded its

pre-year level (of revised 58.7 billion euros) by 2.2 percent. Thus, it once again

reached a new record high.

In India, the growth of the electronics industry has triggered the expansion of

electronic component industry as well. The electronic components produced in

India include, among others, Picture Tubes, Diodes, Transistors, Power

devices, Resistors, Capacitors, Switches, Relays, Connectors, Magnetic heads,

etc. Even though electronics Industry in India will reach $94.2 billion soon,

sources say 65% of them are just imported from other countries.

The percentage of German imports to total Indian imports in this sector is

quite small.

Indian E&E industry is not very development but it must be notived that this

is an intermediary industry. Many other manufacturing companies can only

be attracted to invest in India if there is sufficient supply of standarised

intermediary products. In this connection, increasing trade as well as

investment in India in this sector should be a priority. Germany, being a world

player can play an important part in this.