Electronic communication in the banking sector

30

Chapter 5 Electronic communication in the banking sector 5.1 Introduction Technology has had a profound impact on the service industry, and the financial-services sector is no exception (Bitner, et al., 2000). Technology shapes how services are delivered to customers. It plays an ever-increasing role in the service industry, and has reduced costs for many organisations and eliminated uncertainties for many customers. Dunkin (2004), however, cautions that these technological changes raise important questions as to the extent to which various customers may prefer face-to-face interactions and communication to the new technology-enabled or electronic-communication channels. In this chapter, the focus will fall on the banking industry of South Africa and on the various ways in which IT has changed the means of communication in banks. Special emphasis will, in addition, fall on one bank in particular, namely Standard Bank of South Africa, whose external communication with customers and internal communication with personnel will be examined very closely. External communication in the context of this study will include Standard Bank’s self-service banking channels, or electronic communication such as Internet banking, ATMs, telephone banking, cellphone banking and the Bank’s official Website. It will also include a discussion on a new and innovative channel entitled “the Messaging channel”, which serves to integrate various messages such as SMSs, facsimiles and e-mail into one integrated channel. Bank branches, however, are still deemed the main means of communication, and are still considered the most important mode of distribution of services to the banking customer. Internal communications include communication through telephones, broadcasting and the Internet. An investigation will focus on the intranet of Standard Bank, as well as on the e-mail system used within the Bank for personnel. This chapter will culminate in an overview of what e-mail could ultimately mean to banks in general. Aspects identified in this section will include e-mail marketing, customer service, security and fraud alerts, data collection and secure online-chat services. 82

Transcript of Electronic communication in the banking sector

Chapter 5

Electronic communication in the banking sector

5.1 Introduction

Technology has had a profound impact on the service industry, and the

financial-services sector is no exception (Bitner, et al., 2000). Technology

shapes how services are delivered to customers. It plays an ever-increasing

role in the service industry, and has reduced costs for many organisations and

eliminated uncertainties for many customers. Dunkin (2004), however,

cautions that these technological changes raise important questions as to the

extent to which various customers may prefer face-to-face interactions and

communication to the new technology-enabled or electronic-communication

channels.

In this chapter, the focus will fall on the banking industry of South Africa and on

the various ways in which IT has changed the means of communication in

banks. Special emphasis will, in addition, fall on one bank in particular, namely

Standard Bank of South Africa, whose external communication with customers

and internal communication with personnel will be examined very closely.

External communication in the context of this study will include Standard

Bank’s self-service banking channels, or electronic communication such as

Internet banking, ATMs, telephone banking, cellphone banking and the Bank’s

official Website. It will also include a discussion on a new and innovative

channel entitled “the Messaging channel”, which serves to integrate various

messages such as SMSs, facsimiles and e-mail into one integrated channel.

Bank branches, however, are still deemed the main means of communication,

and are still considered the most important mode of distribution of services to

the banking customer.

Internal communications include communication through telephones,

broadcasting and the Internet. An investigation will focus on the intranet of

Standard Bank, as well as on the e-mail system used within the Bank for

personnel. This chapter will culminate in an overview of what e-mail could

ultimately mean to banks in general. Aspects identified in this section will

include e-mail marketing, customer service, security and fraud alerts, data

collection and secure online-chat services.

82

Next, an overview of the state of communication in financial institutions

globally, as well as a closer look at how technology has influenced

communication within this industry.

5.2 Financial institutions in the global business environment

Rapid technological advances have wrought significant changes in the global

economic and business environment (Hway-Boon & Yu, 2003). Financial

institutions today are faced with even greater communication challenges than

in the past, as they are increasingly performing on the global stage (Bruno-

Britz, 2005), especially since good communication has always been the key to

transacting business of any kind. Banks should be extra vigilant in their

communications with their clients when compared to organisations in any other

industry, as they are, after all, dealing with their clients’ money and livelihood.

Communicating a bank’s brand and policies and serving customers across

borders in countless languages while operating within the bounds of a large

and ever-increasing number of regulations are vital functions to perform to

remain competitive and to retain the public’s trust. This is especially true when

dealing with something that could potentially be more valuable than money,

namely customer data.

Financial institutions are able to communicate better internally, thereby

creating networks that can span across a state, a nation or an international

border to facilitate all kinds of discussions externally. Discussions occur

through a collaboration space, teleconference calls, virtual meetings and/or e-

mails.

Banks should adopt new technology to meet the evolving communication

needs of both their employees and customers. Bruno-Britz (2005) indicates

that data security is a challenge that has to be factored into any discourse

about global banking and communications. Banks’ reputations are on the line

constantly, as they are required not only to perform every transaction correctly

but also to provide a safe-haven for information. Security issues need to be

addressed and dealt with on a round-the-clock basis, and banks need to be

proactive rather than reactive as far as security threats are concerned.

83

In the banking industry, bank branches alone are no longer able to provide

banking services that could cater for today’s sophisticated and demanding

customer’s every need. The provision of banking services through electronic

channels, namely ATMs, Internet banking, telephone banking, cellphone

banking and banking kiosks, however, has provided an alternative means of

acquiring banking services more conveniently (Hway-Boon & Yu, 2003).

The next section will be used to look back on the history of the South African

banking industry, as well as at the key players influencing the current market.

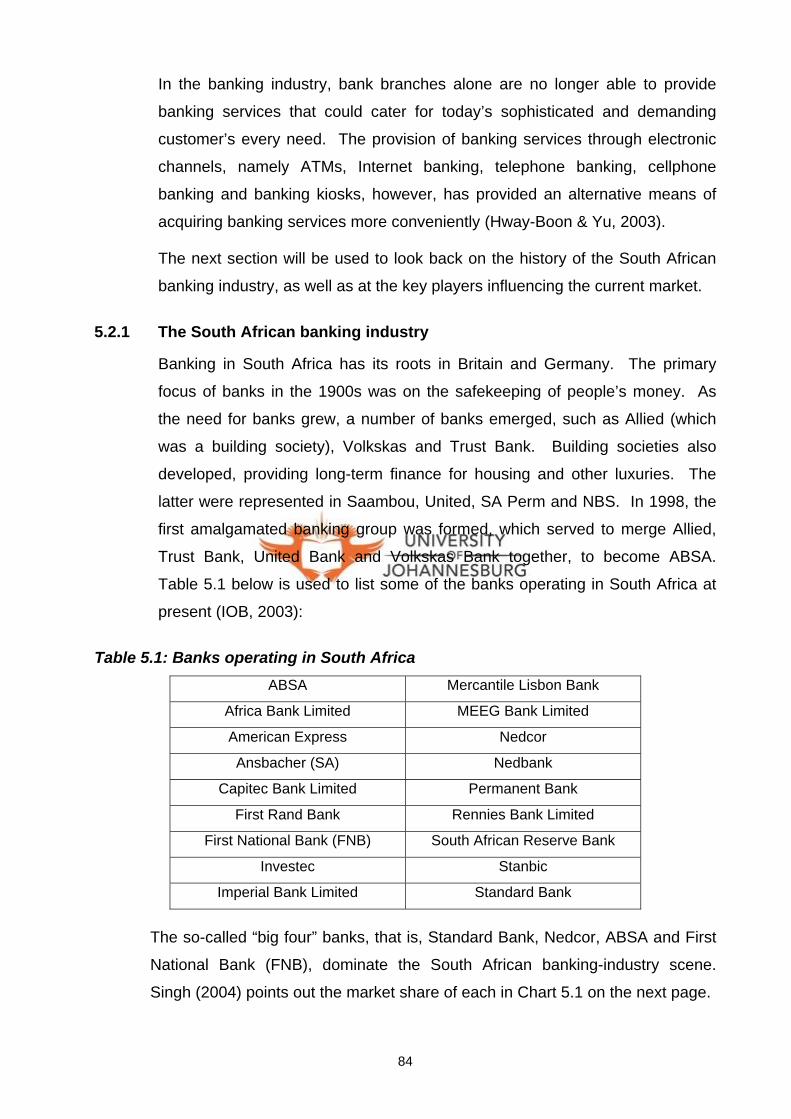

5.2.1 The South African banking industry

Banking in South Africa has its roots in Britain and Germany. The primary

focus of banks in the 1900s was on the safekeeping of people’s money. As

the need for banks grew, a number of banks emerged, such as Allied (which

was a building society), Volkskas and Trust Bank. Building societies also

developed, providing long-term finance for housing and other luxuries. The

latter were represented in Saambou, United, SA Perm and NBS. In 1998, the

first amalgamated banking group was formed, which served to merge Allied,

Trust Bank, United Bank and Volkskas Bank together, to become ABSA.

Table 5.1 below is used to list some of the banks operating in South Africa at

present (IOB, 2003):

Table 5.1: Banks operating in South Africa

ABSA Mercantile Lisbon Bank

Africa Bank Limited MEEG Bank Limited

American Express Nedcor

Ansbacher (SA) Nedbank

Capitec Bank Limited Permanent Bank

First Rand Bank Rennies Bank Limited

First National Bank (FNB) South African Reserve Bank

Investec Stanbic

Imperial Bank Limited Standard Bank

The so-called “big four” banks, that is, Standard Bank, Nedcor, ABSA and First

National Bank (FNB), dominate the South African banking-industry scene.

Singh (2004) points out the market share of each in Chart 5.1 on the next page.

84

Chart 5.1: Market share of the 'Big Four' South African banks (Singh, 2004)

Nedcor20%

First National Bank19%

Other11% ABSA

27%

Standard Bank23%

The big four offer, among others, products and services ranging from savings,

cheque accounts, transmission accounts and notice deposits to fixed deposits.

They also offer long-term finance, credit cards, short-term insurance, medium-

term investment, merchant banking and now, most importantly, Internet-banking

facilities.

Following, a discussion on one of the big four banks, Standard Bank, as to the

various means of communication it uses to reach its customers and staff

members.

5.3 Standard Bank of South Africa and communication

The table on the next page (Table 5.2) provides a summary of the two most

important layers of communication taking place within Standard Bank, namely

communication taking place externally between and among its customers and

business partners, and communication taking place internally between and

among its employees.

85

Table 5.2: External and internal communication of Standard Bank (Author, 2006)

Means of communication

External communication Internal communication

Official Standard Bank Website

Internet banking (SSB)

Internet banking Intranet (Blue Matter) Internet

(Self-service banking) E-mail via Microsoft Outlook

Bank transactions (SSB) AutoBank/ATM and Kiosks Marketing of products and

services to customers

Cellphone banking (SSB)

SMSs Statistics, monitoring of

problems, approvals and information to staff via SMSs

Facsimile Facsimile

Cellphone

PDA/Smartphone − e-mail PDA/Smartphone − e-mail

Telephone banking (SSB) Private branch exchange (PBX)

Telephone calls (local, national and international)

Telephone calls (local, national and international)

Telephone

Facsimile Facsimile Television

Broadcasting Television Videoconferencing Self-service banking via

Internet, telephone and ATM Branches Face-to-face with managers, enquiry staff and tellers

The following section will be used to highlight a discussion on external means of

communication with customers, as summarised in the table above.

5.4 External communication with customers

The phrase “electronic channels”, also known as “innovative distribution

channels”, “Internet banking” or “technology-intensive delivery systems”, is a

collective term used to refer to the various methods of delivering financial

products and information through employing electronic media such as personal

computers, telephones, mobile phones and the Internet (Hway-Boon & Yu,

2003). Despite this dizzying array of electronic media, however, some

customers still insist on doing their banking through a bank branch walk-in.

Banks are, therefore, faced with the constant challenge of providing customers

with as wide a choice as possible when it comes to using banking channels.

86

Standard Bank has adopted retail banking via e-channels as its vehicle for self-

service banking. Its self-service banking comprises the electronic channels

through which the Bank acquires customers and interacts with them. The

electronic channels can be divided into two categories:

• Information-delivery and customer-acquisition channels (sales)

The Web Channel comprises the Website of Standard Bank

(www.standardbank.co.za). The Website contains comprehensive

information on all of the Bank’s products and services, and it provides a

number of interactive tools and calculators that allow customers to

determine product affordability. In addition, the Website contains

application forms through which customers can apply for the Bank’s

products from the comfort and safety of their offices or homes, or even from

their PDAs or Smartphones.

• Transactional channels

Internet banking, cellphone banking, telephone banking and

ATM/AutoBanks allow customers to transact on their accounts any time of

the day or night. Customers may use any channel, or any combination of

channels.

Chart 5.2 below is used to depict the self-service banking channels provided for

customers by Standard Bank, which channels will be discussed next.

Chart 5.2: Customer Self-service Banking channels (Author, 2006)

AutoBank/ATM

The WebTelelphone

banking

Messaging

Internet banking Cellphone banking

5.4.1 The Web

The Web Channel is Standard Bank’s customer electronic-acquisition or sales

channel. Customers can apply for products and services by completing relevant

87

application forms when visiting the Bank’s Website. The Website is one of the

Bank’s primary communication tools. It provides visitors with comprehensive

information on its products, services, financial affairs, history, corporate profile,

and so forth. The site also offers a host of tools, including calculators and a

branch locator.

The Web Channel also assists at implementing the Bank’s business strategy

and the day-to-day management of Blue Matter, the Bank’s intranet. Blue

Matter provides staff with important information on the Bank’s policies and

procedures.

5.4.2 Automatic Teller Machine (“ATM”) or AutoBank

An ATM is defined by Wikipedia (2005) as “an electronic device that allows a

bank’s customers to make cash withdrawals and to check their account

balances without the need for a human teller, or going into a branch”. Many

ATMs allow customers to deposit cash or cheques, to transfer money between

bank accounts, to top up cellphone airtime and even to buy postage stamps.

Most modern ATMs allow customers to identify themselves by inserting a plastic

card with a magnetic stripe that contains their account number. The customer

then verifies his/her identity by entering a passcode or Personal Identification

Number (“PIN”, for short).

At Standard Bank, the ATM is called the “AutoBank”. The AutoBank or ATM

channel includes AutoPlus, AutoBank, AutoCash and AutoBank E machines,

which are easy-to-use, self-service money-management systems. For security

purposes, a personal-identification number (“PIN”) is always requested to

access accounts at an AutoBank. These services maximise customer banking

flexibility when using an AutoBank and can include the following

(Anon. E, 2003):

• Linking accounts to customer ATM cards for easy access.

• Customers can do banking 24 hours a day, seven days a week at any

AutoBank throughout South Africa.

• AutoBank is a Saswitch partner, which means that, for a small additional fee,

the Standard Bank customer can use his/her AutoBank card at other

financial institutions’ ATMs displaying the Saswitch sign.

• Customers can check the details of their accounts without visiting a branch.

88

5.4.3 Cellphone banking

Standard Bank currently offers a SIM-toolkit (“WIG” and “WAP”) cellphone-

banking service. Wireless Internet Gateway (“WIG”) is an SMS-based method

of cellphone banking. To use WIG cellphone banking, customers require a 32K

SIM card. They will also need to download the Standard Bank Cellphone

Banking menu onto their SIM cards.

Using cellphone banking allows customers the luxury of doing their banking at

any time of the day, no matter where they are, and at a reduced cost. It is very

user-friendly, allowing the customer to perform various tasks using his/her

cellphone, which include

• making a balance enquiry

• getting a mini-statement with details of the last five transactions

• transferring money between accounts

• paying accounts

• applying for an overdraft limit

• increasing or decreasing an overdraft limit

• receiving financial information

• recharging Vodacom and MTN prepaid airtime.

5.4.4 Internet banking

“Internet banking” or “online banking” is a term used for performing transactions,

payments, and so forth, over the Internet through a bank’s secure Website.

This can be very useful, especially for banking outside bank hours, and banking

from anywhere where Internet access is available (Wikipedia, 2005).

Internet banking became available in South Africa in 1996. Although the new

technology started out fairly slowly, customers were soon attracted to the

convenience, safety and low cost of this mode of banking. More and more

people are now using Internet banking as their preferred channel for banking

matters. Internet banking usually offers electronic account payments and the

downloading of bank statements for importation into a personal-finance

program. A growing number of banks even operate online to the exclusion of

every other type of service. The year 2001 saw the launch of a bank called

TwentyTwenty, a most successful online-operating bank in South Africa.

89

Singh (2004) concluded from his survey that Standard Bank customers’

preferred mode of banking is Internet-banking, as illustrated in Chart 5.3 below:

60%

27%

10%3%

0%

20%

40%

60%

80%

100%

StandardBank

ABSA Nedbank FNB

Chart 5.3: Internet facilities of banks most used by customers (Singh, 2004)

Chart 5.4 below is used to track the rise in Standard Bank’s monthly Internet-

transaction volumes from 2004 to 2005 (Edkins, 2006):

Chart 5.4: Standard Bank's Internet Banking volumes for 2004 and 2005 (Edkins, 2006)

0

5000000

10000000

15000000

20000000

25000000

JAN

FEBMAR

APRMAY

JUN

JUL

AUGSEP

OCTNOV

DEC

Volume 2004Volume 2005

Edkins (2006) found that, by the end of January 2006, Standard Bank had

accumulated the following Internet-banking statistics:

• 30 million transactions are being performed every month.

• R15 billion is transacted per month on average.

• 454 000 customers are using Internet banking.

90

Most customers are hesitant to bank online unless they can rely on their bank’s

Website technology, and although banks are constantly improving their online

security, it is not enough; banks also have to publicise these improvements in

the media in order to instil greater customer trust (Singh, 2001).

5.4.5 Messaging

The Messaging Channel of Standard Bank is the brainchild of an innovative

idea that enables secure electronic communication (via fax, e-mail and SMS)

with customers through their preferred medium and which relays information to

various business units. Blom (2005) explains its workings in Figure 5.1 below:

Figure 5.1: The Messaging Channel of Standard Bank (Blom, 2005)

Blom (2005) also indicates that the Messaging Channel has improved

communication with customers externally and with business units internally.

Table 5.3 on the next page is used to mirror customer perspective before and

after the introduction of the Messaging Channel. Table 5.4, in its turn, is

indicative of the implications of the Messaging Channel before and after its

implementation, as from the Bank’s perspective:

91

Table 5.3: Before and after the implementation of the Messaging Channel from a

customer perspective (Blom, 2005)

Before Messaging Channel After Messaging Channel The customer received fragmented

messages form different business units at a time dictated by the business units.

The customer now receives consolidated messages (when appropriate) at a time dictated

by the Messaging Channel. The customer was required to go

through multiple registrations for each product and service.

The customer now manages one profile from one place for all products and services.

Customer message preferences on media and products were not recorded.

Customer message preferences on media and products are recorded at the point of

central registration. The customer was serviced from many fragmented databases, as the view was

not consolidated.

Customer enquiries are attended to from one central database.

The customer needed to phone or visit more than one business unit, resulting in

some requests getting lost.

The Messaging Channel ensures end-to-end, integrated fulfilment of outbound and inbound

communication through the Customer Call Centre (CCC), branches and other fulfilment areas. The customer now has more ways to

communicate with the Bank.

Table 5.4: Before and after the implementation of the Messaging Channel from the

Bank’s perspective (Blom, 2005)

Before Messaging Channel After Messaging Channel

Insufficient control from IT security, Group Marketing, Communication and Legal on

business units sending messages.

The Messaging Channel has a governance structure representation from Security and Group Marketing. Communications and

Legal are engaged in the messaging sign-off procedure.

Fragmented messaging was done across all business units, with the result that the Bank

did not have a single view of what it was sending to its customers. The Bank was also paying elevated prices owing to fragmented

rather than aggregated volumes.

There is a centralised query system for the CCC, branch and other support areas. Messaging standards are applied to

achieve economies of scale. Networks are integrated, and optimal infrastructure is in

place and licensed.

No Customer Messaging Profile and Registration (CMPR) process was available

with ongoing updates.

Messaging Channel records all messages sent to customers, as well as their delivery

status. This information can be passed onto business units for the continuous

updating of customer information.

The Messaging Channel is a unified and integrated communication strategy.

This strategy will save time and costs and will increase security. The next self-

service banking channel that will be discussed is that of telephone banking.

92

5.4.6 Telephone banking

Ahmad and Buttle (2002) indicate that telephone banking is a channel for

delivering banking services. Banks use it to supplement their traditional way of

delivering services through branch networks. The main benefit to banks is a

lower cost profile compared to the cost of providing services via branches.

The benefits to customers for using telephone banking are the convenience and

control. Customers are able to do their banking 24 hours a day, seven days a

week, at places convenient and private to them, and at reduced costs. It is no

surprise, then, that the telephone-banking service is growing at such

exponential rates (Ahmad & Buttle, 2002).

In the case of Standard Bank customers, they stand to derive the following

benefits from using telephone-banking services (Moody, 2005):

• Should the customer have access to a fixed line or cellphone, he/she could

call Standard Bank from anywhere in the world, at any time.

• The customer has access to an automated service that can be personalised

to suit his/her needs.

• There are no subscription fees or sign-up costs.

• Bank accounts are only a phonecall away.

The Customer Contact Centre (“CCC”, for short) assists many customers on

registering for telephone banking. It also supports a number of products and

services offered by the Bank, which will be discussed next.

5.4.6.1 The Customer Contact Centre (“CCC”)

The CCC is the primary contact point for Standard Bank customers. Call

centres are defined as “a focus point of contact with the customer when

communicating via electronic media”. In- and outbound call centres are also

included in this definition. Various services at the CCC offer support to most

products offered by the group, and technical experts are available at the

helpdesk area to assist customers at accessing the Internet-banking site.

The ever-expanding media through which customers interacted with the Bank

(e-mail, voice mail, facsimile and telephone calls), in turn, gave rise to expanded

CCCs, which evolved from mere “hotlines” offering a handful of services via the

telephone to fully-fledged one-stop call centres. Some of the vast array of

services and functionalities offered by the CCCs are highlighted in Table 5.5.

93

Table 5.5: Customer Contact Centre services and functionalities (Anon. K, 2005)

Area Functionality

Service fulfilments

• Merging of customer records.

• Answering of voicemail queries.

• Faxing of statements.

• Dealing with electronic account-payment queries.

• Dealing with cellphone-banking queries.

• Internet-banking escalation, PIN resetting and

refunds.

• BlueBean queries and transactions.

E-mail unit

• Support related, which are specific queries to

Internet, Home loans and BlueBean.

• General information is any information related to

general queries and information.

Internet banking

• General Internet-banking information.

• Assistance with Internet-banking site navigation.

• Switching customers onto Internet banking.

• Technical assistance.

• Guiding customers as to effecting transactions and

account payments.

Telephone

banking

• Providing general banking information.

• Assisting clients at using the automated telephone-

banking system.

• Assisting clients at effecting various transactions,

such as balances, statements, ordering of cheque

books, making inter-account transfers, paying

accounts, loading off MTN and Vodacom prepaid

systems, voicemail queries, registration to Voyager

programme, cross and up sell of various banking

products.

The sections above were used to investigate different electronic means of doing

business via various electronic channels. The following section will be used to

focus on branches, which still serve as the hub of business for many banks.

94

5.4.7 Branches Today, banks may still have branches, but thanks to wonderful advances in

technology, they may also be represented by a telephone or cellphone in the

customer’s home, a plastic magnetic stripe on a debit card or a self-service

cash-dispensing machine on the street (Prendergast & Marr, 1994). Bank

branches, therefore, serve two main functions in the modern-day scenario:

• They broaden the service level for customers by providing access points in a

number of different locations.

• They act as places of money (that is, cash and cheques) transfer, facilitating

the physical movement of cash and cheques from sender to receiver.

The future of bank branches, however, has long been a topic of debate, but

Prendergast and Marr (1994) foresee that this time round, we may indeed see a

drastic reduction in their numbers. They hasten to add, however, that self-

service technology will always remain a complement to, rather than a

replacement of, the real thing. It is already evident that cross selling of bank

products through different channels complements the bank branch and justifies

the existence of both human tellers and the bank branch. Jones (1996)

concludes that branch location is still seen as the single most important

influence on a customer’s choice of a bank.

Standard Bank has the following statistics on the number of Standard Bank

branches, service centres and AutoBank E Centres currently operating in South

Africa, as indicated in Table 5.6 below:

Table 5.6: Standard Bank of South Africa’s current branches, service centres and

AutoBank E Centres (Lopes, 2006)

Province Branches Service Centres AutoBank E Centres

Eastern Cape 12 57 16 Free State &

Northern Cape 9 77 7

Western Cape 28 85 9 KwaZulu-Natal 31 64 21

Limpopo 7 19 13 Mpumalanga 9 38 12 North West 7 26 8

Gauteng (Jhb) 53 70 29 Gauteng (Pta) 16 18 5

Total 172 454 120

95

In addition, Lopes (2006) indicates that there are, on average, approximately 25

staff members working in a branch. Standard Bank has 11 000 permanent staff

members presently working in branches all over South Africa, and

approximately 800 flexi-staff members deployed in the branch network.

It would be safe to say, then, that even though branches are still deemed pivotal

to business (Lopes, 2006), it should be noted that customers are increasingly

making use of multiple mediums and channels of communication. He goes on

to point out that branches are very important for the cross selling of products

and the acquisition of walk-in new business. During the technology boom,

banks around the world believed that electronic service and delivery would

eventually replace the traditional branch, but over the past five years, more and

more evidence has surfaced to support the need for a strong presence in the

form of a branch network.

Lopes (2006) goes on to say that customers generally feel more at ease when

discussing money matters with someone they can see and relate to. Electronic

delivery and services are often used as a supplementary channel to the branch

network, with trends reflecting customers using multiple delivery channels.

The next section will be devoted to a closer look at communication internally

between and among employees.

5.5 Internal communication between and among employees

Workplace or internal communications have improved in leaps and bounds in

the course of the 21st century. Today’s employees have more ways than ever

to stay in touch − from their desk phones, mobile phones and PDAs to pagers,

e-mail, instant messaging, facsimiles and tele- and videoconferencing. For

many employees, “work” has, in fact, become synonymous with a series of

activities, rather than with a physical location. And, given the capabilities of our

modern-day real-time communication systems, “work” has also taken on an

immediacy hitherto unknown. In this way, turn-around times for problem-solving

and dealing with requests have shrunk to a mere fraction of those of yesteryear.

The next section will be devoted to a closer look at the internal communications

of Standard Bank and at the way in which employees interact with each other

via the messaging systems and real-time communications, such as

broadcasting, telephones, the Internet, the intranet and e-mail systems.

96

5.5.1 Broadcasting

Frazer (2005) indicates that Standard Bank has a videoconferencing

infrastructure in terms of which 30 units have been installed by the Bank at the

turn of 2005. The average cost per unit was R65 000. He also states that the

operational cost of these 30 units was R156 000 per annum for maintenance

and R98 000 per annum for dial up. Executives and directors use these units

locally, nationally and internationally.

Standard Bank also broadcasts recorded programmes over televisions in some

head offices, such as the head offices in Johannesburg, Durban and Cape

Town. It also broadcasts live cricket over these televisions, since Standard

Bank is the main sponsor of the national teams and the Proteas.

5.5.2 Telephones

Standard Bank has a variety of phone-call usages. Frazer (2005) has gathered

a few statistics on the use of telephones in Standard Bank.

5.5.2.1 Internal-call volumes

The phrase “internal-call volumes” refers to calls that do not travel through the

Telkom network. The volume of extension-to-extension calls for 2005

throughout the Standard Bank Group was 49 million calls.

5.5.2.2 External-call volumes

The volume of calls made via the Telkom network originating from extensions within

the SBIC Group during 2005 amounted to 101 million and includes all calls (local,

national, international, mobile and other), as indicated in Table 5.7 below: Table 5.7: The volume and cost of telephone calls made by Standard Bank via the

Telkom network in 2005 (Frazer, 2005) Call type Volume Cost

Local 41,0 million R 38,0 million

National 22,0 million R 46,2 million

International 0,5 million R 2,2 million

Fixed to mobile 32,0 million R 97,3 million

Other (Telex &

Smart Access) 5,5 million R 13,0 million

Total 101,0 million R196,7 million

97

5.5.2.3 Private Branch Exchange (“PBX”)

The original switchboard has been replaced with automated electromechanical and

electronic switching systems. Using a PBX saves connecting all of a business's

telephone sets separately to the public-telephone network. Apart from telephone

sets, fax machines and modems, many other communication devices can be

connected to a PBX.

There are 700 banks that owned and rented PBXs within the Standard Bank Group

as at the end of 2005. The annual cost for 2005 was R12,9 million for the Telkom-

rented PBXs, and R3,5 million for the maintenance of Bank-owned PBXs.

5.5.2.4 Cellular phones

The use of cellular phones accounts for the Bank’s biggest expense as far as

phonecalls are concerned, because it includes both phone calls and SMSs.

• Cost for Standard Bank’s cellphone usage

The total cost paid to Vodacom, MTN and Cell C during 2005 for cellphone

usage was R8,9 million. This cost includes refunds to staff for business use of

their private cellphones, as well as for Bank-owned phones, as it is not possible

to separate these amounts.

• Cost of cellphone calls

Total cost of fixed-to-mobile calls for 2005 was R97,3 million for the SBIC Group

(this constitutes the cost for calls from our PBX systems to cell numbers,

payable to Telkom).

• Number of SMSs Standard Bank sent to internal staff and customers

A total of 18 million SMSs were sent internally and to customers during 2005, at

a total cost of R3,78 million (18 million x 21 cents).

• Cost of these SMSs

The cost per SMS is 21 cents.

5.5.3 The Internet, intranet and e-mail systems

This section will be devoted to a closer look at the network systems within

Standard Bank, starting with its Internet facility.

5.5.3.1 The Internet

Standard Bank Internet Information Protection Policy states that access to an

Internet session is restricted to business purposes explicitly authorised by

Management. Non-Bank uses, such as downloading of games, viruses,

98

inappropriate graphics, picture files, illegal software and other files for personal

use, are strictly prohibited. The IT Division also has the right to monitor any

activity and/or outgoing Internet traffic.

In addition, no sensitive data such as customer banking details (account

numbers and balances) may, in terms of the Policy, be transmitted across the

Internet in clear text. All the banking applications have to be encrypted end-to-

end, using industry-standard mechanisms.

As a further precaution, the number of staff members who enjoy access to the

Internet are limited, thereby further restricting its use for business purposes

only. These members may include market researchers, the Internet Website-

channel staff and the Intranet-channel staff.

5.5.3.2 The intranet

The Standard Bank intranet has been dubbed the “Blue Matter”, a name derived

from the fact that our brains are largely made up of grey matter. The name,

therefore, is representative not only of human intelligence, knowledge and

information but also of our empowerment and individuality. The Blue Matter has

been developed with Standard Bank staff members as its main focus.

The principal aim with the design of the Blue Matter was to create an intuitive,

interesting and valuable tool, the implementation of which would allow staff

members to connect to all the information they may need effectively to execute

their work functions. And it has since proven itself to be an invaluable, single-

access, consolidated online-information solution. Other benefits to be derived

from the intranet are as follows (Baines, 1996):

• It delivers information on demand through effective information portals.

• It guarantees that the information is the latest and most accurate available.

• It allows information to be “owned”, contributed and maintained by

individuals who would as a rule prepare and maintain the original

information.

• It allows staff members to gain access to the latest versions of regulations,

policies and product and service catalogues.

• It acts as a central document-delivery system through which to distribute

training and learning programmes.

99

It is evident from the foregoing that the intranet offers Standard Bank staff the

possibility of increased productivity, lower cost, with faster delivery of

information to their desks. It also allows staff to become familiar with the

network culture and it electronically enables the organisation to conduct

activities such as procurement online. In addition, the Blue Matter enables

employees to do their banking online through the Internet-banking portal.

5.5.3.3 E-mail systems within Standard Bank

Standard Bank uses Microsoft Exchange Server as its e-mail system. This

software program runs on servers that enable users to send and receive e-mail

and other forms of interactive communication through computer networks. It

collaborates with software client applications such as Microsoft Outlook,

Exchange Server and other e-mail client applications.

E-mail messages are sent and received through client devices such as a

personal computer, a workstation or a mobile device such as a Smartphone/

PDA or a Pocket PC. Staff members are connected to a network of a

centralised computer system compromising servers or a mainframe computer,

where e-mail Inboxes are stored. The centralised e-mail servers connect to the

intranet and private networks, where e-mail messages are sent to and received

from other e-mail users.

5.5.3.4 The functionality of Outlook Express

Outlook offers staff members integrated collaborative messaging features such

as scheduling, contact and task-management capabilities. Outlook also

supports staff members using mobile devices such as Smartphones/PDAs to

synchronise their Inbox, Calendar, Contact and Tasks list, so that the users can

check appointments and other important information. Mobile-device browsers

are also supported through Outlook Mobile Access, which enables HTML,

compressed HTML and Wireless Application Protocol (“WAP”, for short).

The collaboration features of Outlook help users share information quickly and

efficiently. Typical collaborative scenarios include maintaining a shared or

global address list that all members of staff can view and edit, scheduling

meetings that include people and conference rooms (Anon. G, 2004). Standard

Bank has administrators who develop rules and policies that users must follow.

100

The next section will be devoted to a closer look at how an office worker in

Standard Bank has to manage information with the different information

systems at his/her disposal, and at how he/she would use these systems in

his/her communication.

5.5.4 Information management of the information worker in Standard Bank

The ability of information workers or an organisation such as Standard Bank to

accomplish any given task or to realise an objective is directly related to the

ability to find the right information at the right time (Nortje, et al., 2004). The

said authors go on to point out that the functions of the information worker can

loosely be divided into four main categories, namely managing documents,

communication, managing information and decision-making, and that different

information systems are used to perform each of these functions (as discussed

in Chapter 2). The factors that influence the information environment of

information workers in Standard Bank are listed in Table 5.8 below:

Table 5.8: Factors that influence the information environment of the information

worker in Standard Bank (Nortje, et al., 2004) Function Information system

Managing documents

− creation, storage, retrieval and

dissemination

Word processing

Desktop publishing

Document-imaging systems

Communication

− individual, group and team

Networks such as Internet and intranet.

Communication tools such as

facsimile, modems, voice mail, e-mail,

videoconferencing, cellular phones,

PDAs/Smartphones, groupware, etc.

Managing information

− formal and informal information

Spreadsheets

Database-management systems

Decision-making

− strategic, managerial, office and

operational

Decision-support system

The next section will be used to investigate how banks can use e-mail

communication themes in their retail business, with special reference to the way

in which Standard Bank uses these e-mail communication themes.

101

5.6 Banks and e-mailing with customers

In 2005, the Council of Financial Competition (“CFC”, for short) conducted an

investigation into e-mail communications within banks. The Council concluded

as follows:

• E-mail is the most cost-effective channel for marketing products and

services, yet one of the least developed among financial institutions. For

marketing purposes, banks conducted e-mail campaigns as a cost-effective

addition to traditional marketing efforts.

• Since 2002, two key developments have occurred:

1. The rise in popularity of e-mail as a means of communication

E-mail communication has become the primary mode of business

communication world-wide. Electronic-messaging channels are now

considered viable media for taking orders, sending approvals and

contracts, and for discussing sensitive financial issues. In addition, most

financial institutions want to increase their e-mail interaction with their

customers.

2. The growth in e-mail and online fraud

The incidence of online fraud, such as phishing attacks, has raised

dramatically. Webopedia (2006) defines “phishing” as “The act of sending

an e-mail in an attempt to scam the user falsely claiming to be an

established legitimate enterprise in an attempt to scam the user into

surrendering private information hat will be used for identity theft. The e-

mail directs the user to visit a website where they are asked to update

personal information, such as passwords, credit card and bank account

numbers. The website however is counterfeit and set up only to steal the

user’s information”. Light (2005) goes on to point out that any personal or

financial information entered at such a site is routed directly to the

scammer instead.

The CFC also identified five different themes in the e-mail communication

channel used by financial institutions. Chart 5.5 on the next page is used to

indicate these themes, which will be taken under discussion in the next section.

102

Chart 5.5: E-mail communication themes in financial institutions

Online interactive chat services

Data collection

Customer service

Security and fraud alerts

E-mail marketing

5.6.1 E-mail marketing

Financial institutions use the e-mail channel to market a mix of products,

services and online functionalities. They predominantly target existing retail

banking customers. Policies should be in place to restrict marketing to only

bank-related matters. E-mail structures in financial institutions may include one

or more of the following varieties:

• In-house operation

• External vendor

• Combination structure.

Banks generally use their Internet-banking customer database to target their

customers. The e-mail volume may vary in terms of the marketing campaign,

for example:

• Marketing campaign, for example, competitions such as car give-aways.

• Product marketing, for example, investment products, deposits, loans and

Internet-banking products.

• Online services and new online functionality marketing, for example, bill-

payment alerts.

Banks stand to derive the following benefits from e-mail marketing (CFC, 2005):

• Cost benefit as key advantage.

• Customer feedback, such as improving effectiveness and response times.

• Increased Internet-banking usage.

103

• Improving marketing effectiveness, for example, to test e-mails on a small

population first before launching a big campaign.

• E-mail marketing also enables the bank proactively to communicate with

existing prospects and customers instead of passively waiting for them to

return to the Website, to visit a branch or to call on the phone.

The benefits derived from most traditional types of marketing and advertising

are very difficult to measure. With e-mail marketing, on the other hand, one can

easily measure the number of e-mails sent and the rates at which e-mails are

opened or sent back as bounce-backs, “Unsubscribe” and click-throughs

(Goodman, 2005).

5.6.2 Customer services

A large number of financial institutions use the e-mail channel to deal with

customer-service issues. Banks should be very conscious of the security issues

surrounding this channel, however. Generally, banks do not send confidential

information such as account numbers via external e-mails, unless such

information is masked or encrypted. External mail consists of e-mail sent to a

customer's personal e-mail account over the Internet. External e-mails are

insecure and can be interrupted by a third party. Alternative channels are used

to reply, such as telephone banking or a secure-messaging system on the

bank’s Internet-banking Website. Standard Bank’s Messaging Channel is an

example of the latter system.

Banks should provide additional secure-messaging services for customers on

their Internet-banking account facilities. The messaging service can only be

accessed by the customer when he/she has logged onto his/her account using

his/her personal password and PIN. The secure-messaging service enables the

bank and the customer to pass confidential information back and forth.

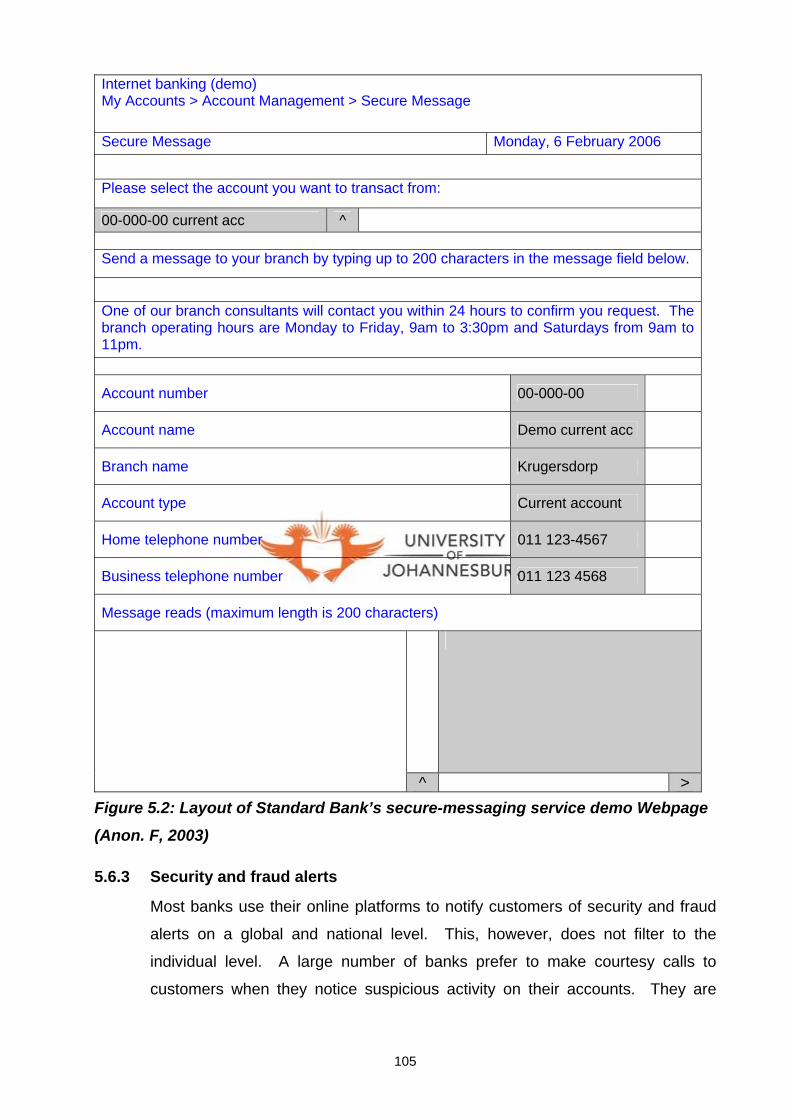

Standard Bank enables Internet-banking customers to send messages to its

branches. As was explained previously, this can be done once customers have

registered for Internet banking or for a self-service banking profile. Customers

log onto their Internet-banking account by indicating their ATM card number,

customer-selected PIN or CSP and a password. Customers then proceed to

the account-management portal, which will enable the Secure Message page,

as in Figure 5.2 on the next page. The grey areas indicate instances where

customers have to select and fill in details in order to send a message:

104

Internet banking (demo) My Accounts > Account Management > Secure Message

Secure Message Monday, 6 February 2006

Please select the account you want to transact from:

00-000-00 current acc ^ Send a message to your branch by typing up to 200 characters in the message field below.

One of our branch consultants will contact you within 24 hours to confirm you request. The branch operating hours are Monday to Friday, 9am to 3:30pm and Saturdays from 9am to 11pm.

Account number 00-000-00

Account name Demo current acc

Branch name Krugersdorp

Account type Current account

Home telephone number 011 123-4567

Business telephone number 011 123 4568

Message reads (maximum length is 200 characters)

^ >

Figure 5.2: Layout of Standard Bank’s secure-messaging service demo Webpage

(Anon. F, 2003)

5.6.3 Security and fraud alerts

Most banks use their online platforms to notify customers of security and fraud

alerts on a global and national level. This, however, does not filter to the

individual level. A large number of banks prefer to make courtesy calls to

customers when they notice suspicious activity on their accounts. They are

105

extremely aware of fraud fears and take significant measures to protect their

customers via data security and compliance policies.

In addition, a bank can also install a security solution to deal with security issues

such as spam and viruses. It is of the utmost importance to protect the

organisation against liability, risk and loss of productivity, and to retain its

customers.

5.6.3.1 Phishing

Butler (2005) states that a phishing attack consists of three distinct parts: the

e-mail message; a fraudulent Website and a hyperlink that leads to the

fraudulent Website. This is explained by Butler (2005) as follows:

1. The e-mail message, appearing to come from a legitimate source, is

carefully designed to trick the recipient into providing sensitive personal

information, which the phisher uses in a fraudulent manner. The message

usually contains a section (the 'bait') that requests the user's assistance in

solving a problem.

2. The fraudulent Website that the phishers set up mimics the graphics and

formatting of a legitimate Website as closely as possible, in order to mislead

the victim deliberately. Well-known online brands are often targeted in this

way. On the Website, the user is prompted to provide confidential personal

information, which the phisher harvests for nefarious ends.

3. The name of the fraudulent Website is hidden in an embedded hyperlink in

an HTML-formatted e-mail in order to disguise the address of the actual

Website the user will be taken to when clicking on the hyperlink.

In November 2005, fraudsters have launched two separate phishing attacks

against Standard Bank Internet-banking and credit-card users.

Panagiotopoulos (2005) indicates that the fraudsters used unsolicited e-mails to

entice unwitting customers to disclose their personal details in order to obtain

access to their bank accounts. He adds that Standard Bank’s IT Security

Division contained the threat in the first hour and a half of each attack, and that

Standard Bank’s Internet service still boasts a 100% safety record.

Panagiotopoulos (2005) has also gathered statistics on just one day in

November 2005 of attacks launched against Standard Bank in Chart 5.6 on the

next page.

106

Chart 5.6: Standard Bank's phishing attack statistics in November 2005

40%

56%

4%

Legitimate Mails Undeliverable/Return External MailsBlocked for Phishing Mails Internal

5.6.3.2 The Mail Marshal program

Standard Bank uses a security program called “Mail Marshal” to monitor,

evaluate and regulate all incoming external e-mails. “Mail Marshal” is an e-mail

security solution specifically designed to deal with e-mail viruses, Trojans, spam

and other malicious attacks and related issues. “Mail Marshal” allows the Bank

to apply its policies and security rules to e-mail at its corporate gateway, thus

defending the Bank against the risks and disadvantages of e-mail use. This

e-mail solution enables the Bank to use e-mail safely, securely and productively.

“Mail Marshal” provides many powerful features to scan and filter all external

incoming messages. Panagiotopoulos (2005) indicates that this software can

scan the content of e-mail messages and attachments as they enter or leave

the Bank. Benefits to be derived from using this solution include the following:

• Blocks spam with a detection rate of 95%.

• Scans for viruses using third-party virus scanners.

• Scans message text, header and attached documents for the presence of

particular phrases.

• Recognises the type and size of attached items.

• Performs many other checks of message content, as specified by the Bank's

e-communication policies and rules.

107

5.6.3.3 Legislation and the bank

Hudson (2005) points out that as e-mail becomes more and more popular as a

means of communication between the bank and its customers, it has become

essential for banks to maintain and control the medium to ensure that it is not

prejudiced in any way. She goes on to say that the increased legal

requirements and responsibilities with respect to the retention, destruction and

restoration of electronic records in line with the requirements for paper-based

records require banks to act proactively to avert a whole host of legal problems.

In addition, should the bank be unable to comply with such legislation, the

directors would be responsible for risk management and for ensuring that

effective internal controls be put into place, as they could be held personally

liable, should the bank be found lacking in this respect (Hudson, 2005).

Following, some of the applicable legislation, laws and guidelines governing

electronic-records management:

• The Electronic Communications and Transactions Act − makes it clear that

electronic communications are to be treated in the same way as other more

traditional means of communication. Specific rules govern the way in which

electronic communications should be managed in order to maintain them

and keep their integrity.

• The Promotion of Access to Information Act − indicates that once a request

to access has been received, steps must be taken to preserve and ensure

the integrity and the originality of the records requested.

• Companies Act (Regulations for the Retention and Preservation of Company

Records)/Close Corporations Act (Administrative Regulations) − sets out the

rules for the retention of company documents for a prescribed period of time.

• The Income Tax Act/Value Added Tax Act − includes specific requirements

for transactions in terms of which documentation is exchanged electronically.

• Supreme Court Act − the rules with regard to the discovery, inspection and

production of documents require that a discovery request be complied with

within a certain period of time, failing which the party could be compelled to

do so under the threat of a fine, or the directors of the company could be

jailed.

• FICA − regulates consumer protection and communication records retention.

108

• FAIS − only licensed providers are allowed to give financial advice to clients,

which should be explicitly stated in all communications, including e-mail.

• The Interception and Monitor Prohibit Act − legislates how and when

communication may be monitored and intercepted.

Hudson (2005) adds to this that the banks use e-mail extensively as a business

tool, as well as a private-message repository for their staff, and that, as such,

they need to protect themselves in terms of legislation requirements that apply

to them, as well as in terms of the costs that may arise out of non-compliance.

5.6.4 Data collection

The main method of data collection across banks is through the registration

process for Internet banking. Despite this, the percentage of customers for

which banks have valid e-mail addresses is low. Data collection, therefore, is

not the only challenge banks are faced with, as maintaining valid and active

e-mail addresses also poses a major problem.

Methods of data collection can include Internet banking and account opening,

as well as opt-in (CFC, 2005). Standard Bank uses Internet-banking and

account-opening application forms as a way of collecting e-mail addresses from

its customers.

Challenges of data collection include the following (CFC, 2005):

• Voluntary participation, which customers could refuse.

• Overcoming customers’ spamming fears.

• Maintaining an active and valid e-mail address.

• Databases need to synchronise accounts, for example, online accounts and

credit-card accounts.

5.6.5 Online interactive chat service

Online interactive chat services are not yet very successful in the financial

industry. It is considered a major security risk and an expensive operation.

Employees will also have to be on duty 24 hours a day and will have to gain

extensive knowledge about banking products and services, as well as the chat

service being used. Alternatively, banks could specialise in having a rapid

response rate to e-mails of approximately two hours or less. Response times

can be monitored to ensure rapidity.

109

A certain bank in the USA has successfully implemented an interactive chat

channel and has been communicating with its customers in this way for more

than 18 months now, with this means of communication proving very popular

with its customers. The bank does not market this service, however, as it does

not continuously staff the channel. When a staff member happens to be

available to discuss with a customer over online chat, that staff member goes

online and engages with the customer. By adopting this approach, the bank

finds that customers are not disappointed, should the opportunity to talk to a

member of staff online not present itself. Instead, customers are pleasantly

surprised when it does happen. Lerche (2005) states that Standard Bank does

not have the security capabilities to implement such a service, however, and

goes on to point out that staff in this service would have endless working hours,

and that it would be too costly and risky to maintain.

5.7 Conclusion

In the world of banking, the developments in information and communication

technology have had an enormous effect on the development of more flexible

payment methods and more user-friendly banking services. Online-banking and

other electronic-payment systems are new, and the development and diffusion

of these technologies by financial institutions is expected to result in a much

more efficient banking system (Akinci, et al., 2004).

New technologies offer banks alternative or non-traditional service-delivery

channels through which to deliver banking products and services to customers.

This is done conveniently and economically, without diminishing the existing

banking level. This chapter was devoted to taking a closer look at the

electronic-communication system of Standard Bank in South Africa.

Standard Bank’s external communications with customers were discussed

under the topics of self-service banking and branches. Self-service banking

comprises electronic means of banking and includes the Website,

ATM/AutoBank, cellphone banking, Internet banking, the Messaging Channel

and telephone banking.

Blom (2005) has created an innovative strategy to integrate all messages from

customers, including faxes, SMSs and e-mails, into one channel, called the

“Messaging Channel”. This is based on a second-generation enterprise

110

communication solution (“ECS”, for short) that includes unified-messaging

applications and unified-communication capabilities as part of its features.

In the section on internal communication, topics such as broadcasting,

telephones and Internet usage were taken under discussion. Standard Bank

has an intranet that constitutes a single, integrated, collaborative information

solution for its staff members. The intranet also has all the most recent news,

developments, policies and information available to personnel. In addition, the

Bank tries to meet challenges regarding e-mail, such as compliance concerns,

information theft, viruses, spam, message volumes, effective management and

corporate responsibility to its employees.

Blom (2005) indicates that, with all the messaging and real-time technologies

that allow greater access to mobility and the expectation of an immediate

response, Bank employees and Bank customers could easily fall prey to feeling

overwhelmed and pressured. Office workers, it would seem, need to acquire

certain management skills when called upon to use these information systems.

This chapter was also used to identify and discuss certain e-mail themes in

banks, with special reference to those in Standard Bank. These themes

included

• e-mail marketing of products and services

• customer services, such as e-mail response times and query management

• security and fraud alerts, such as phishing and legislation

• data collection of e-mail addresses and the maintenance thereof

• secure online chat services.

The next chapter will be devoted to the empirical part of the thesis, where the

survey and its results will be made known and discussed.

111