Electrical Contractors Association and Local Union 134 I.B ... · 30.06.2015 · Local Union 134...

40

Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2 Withdrawal Liability Valuation as of June 30, 2015 This report has been prepared at the request of the Board of Trustees for the purposes of establishing the basis for withdrawal liability assessments during the July 1, 2015 through June 30, 2016 period. This report may not otherwise be copied or reproduced in any form without the consent of the Board of Trustees and may only be provided to other parties in its entirety. The measurements shown in this report may not be applicable for other purposes. Copyright © 2016 by The Segal Group, Inc. All rights reserved.

Transcript of Electrical Contractors Association and Local Union 134 I.B ... · 30.06.2015 · Local Union 134...

Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2 Withdrawal Liability Valuation as of June 30, 2015

This report has been prepared at the request of the Board of Trustees for the purposes of establishing the basis for withdrawal liability assessments during the July 1, 2015 through June 30, 2016 period. This report may not otherwise be copied or reproduced in any form without the consent of the Board of Trustees and may only be provided to other parties in its entirety. The measurements shown in this report may not be applicable for other purposes. Copyright © 2016 by The Segal Group, Inc. All rights reserved.

101 NORTH WACKER DRIVE, SUITE 500 CHICAGO, IL 60606 T 312.984.8500 F 312.984.8590 WWW.SEGALCO.COM

January 25, 2016

VIA E-MAIL AND U.S. MAIL

Board of Trustees c/o Mr. Sean P. Madix Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2 Chicago, IL Dear Trustees: This report summarizes and reviews the Plan’s status and experience with respect to employer withdrawal liability. It outlines the withdrawal liability method adopted and explains the calculation of the amount of liability of a withdrawn employer. It also establishes the basis for assessments of withdrawal liability for withdrawal during the period July 1, 2015 through June 30, 2016. The actuarial calculations were completed under the supervision of David N. Strom, FSA, MAAA, Enrolled Actuary. The basic participant and financial data used in this report are the same as those used in the actuarial valuation as of July 1, 2015. The benefit provisions included in the calculations are those that were in effect on June 30, 2015.

Please contact us if you have any questions about this report. Sincerely, Segal Consulting, a Member of The Segal Group, Inc. By: ____________________________ ____________________________ John R. Janezic Harold S. Cooper, FSA, MAAA, EA Senior Vice President Vice President and Actuary

Table of Contents

3

Section 1: Actuarial Valuation Summary Important Information about Withdrawal Liability Valuations ......................................................................................................................... 5 Significant Issues in Valuation Year ................................................................................................................................................................. 7 Summary of Key Results .................................................................................................................................................................................. 8

Section 2: Actuarial Valuation Results

A. Determination of Withdrawal Liability ..................................................................................................................................................... 9 B. Unfunded Vested Liability ...................................................................................................................................................................... 11 C. Withdrawal Liability Experience ............................................................................................................................................................ 17 Section 3: Supplementary Information

EXHIBIT A Method for Allocating Withdrawal Liability ................................................................................................................................................ 18

EXHIBIT B Employer Withdrawal Liability Worksheet For Withdrawals from July 1, 2015 Through June 30, 2016 (Pre-Merger Pools for Legacy Plan 2 Employers) ................................................................................................................................................................................................. 22

EXHIBIT C Employer Withdrawal Liability Worksheet For Withdrawals from July 1, 2015 Through June 30, 2016 (Pre-Merger Pool for Former Plan 4 Employers) ................................................................................................................................................................................................. 23

EXHIBIT D Employer Withdrawal Liability Worksheet For Withdrawals from July 1, 2015 Through June 30, 2016 (Pre-Merger Pools for Former Plan 6 Employers) ................................................................................................................................................................................................. 24

EXHIBIT E Employer Withdrawal Liability Worksheet For Withdrawals from July 1, 2015 Through June 30, 2016 (Post-Merger Pools) .................. 25

EXHIBIT F Employer Withdrawal Liability Worksheet For Withdrawals from July 1, 2015 Through June 30, 2016 ................................................... 26

Section 4: Actuarial Certification of Withdrawal Liability

EXHIBIT I Calculation of Unfunded Vested Liability .................................................................................................................................................... 28

EXHIBIT II Withdrawal Liability Pools ........................................................................................................................................................................... 29

Table of Contents

4

EXHIBIT III Actuarial Assumptions and Methods ............................................................................................................................................................ 33

EXHIBIT IV Summary of Plan Provisions ......................................................................................................................................................................... 38

SECTION 1: Actuarial Valuation Summary as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

5

Important Information about Withdrawal Liability Valuations

Withdrawal liability valuations are prepared to assist in the determination and assessment of withdrawal liability by the plan. These measurements include a forecast of future uncertain obligations of a pension plan. As such, the forecast will never precisely match the actual stream of benefits and expenses to be paid. In order to prepare withdrawal liability measurements, Segal Consulting (“Segal”) relies on a number of input items. These include:

Plan Provisions Plan provisions define the rules that will be used to determine benefit payments, and those rules, or the interpretation of them, may change over time. It is important for the Trustees to keep Segal informed with respect to plan provisions and administrative procedures, and to review the plan summary included in our report to confirm that Segal has correctly interpreted the plan of benefits. For an employer withdrawing in a particular plan year, the relevant plan provisions are those in effect at the end of the prior plan year.

Participant Information The present value of vested benefits, upon which withdrawal liability for an employer is determined, is based on data provided to the actuary by the plan. Segal does not audit such data for completeness or accuracy, other than reviewing it for obvious inconsistencies compared to prior data and other information that appears unreasonable. It is not necessary to have perfect data for a valuation: the valuation is an estimated forecast, not a prediction. Notwithstanding the above, it is important for Segal to receive the best possible data and to be informed about any known incomplete or inaccurate data.

Financial Information The withdrawal liability valuation is based on the asset values as of the valuation date, typically using information reported by the auditor. The allocation of the unfunded present value of vested benefits to an employer is based on detailed obligated contribution information for a withdrawn employer, as provided by the plan.

Actuarial Assumptions In measuring the present value of vested benefits for withdrawal liability purposes, Segal starts by developing a forecast of the vested benefits to be paid to existing plan participants for the rest of their lives and the lives of their beneficiaries. This requires actuarial assumptions as to the probability of death, disability, withdrawal and retirement. The forecasted benefits are then discounted to a present value. The actuarial model used to develop the present value of vested benefits for withdrawal liability purposes may use approximations and estimates that will have an immaterial impact on our results. In addition, the actuarial assumptions may change over time, and while this can have a significant impact on the reported results, it does not mean that the previous assumptions or results were unreasonable or wrong.

SECTION 1: Actuarial Valuation Summary as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

6

Given the above, the user of Segal’s withdrawal liability valuation report (or other actuarial calculations) needs to keep the following in mind:

The withdrawal liability valuation report is prepared for use by the Trustees. It includes information relative to the

provisions of ERISA pertaining to withdrawal liability. Segal is not responsible for the use or misuse of its report, particularly by any other party.

Withdrawal liability measurements are as of a specific date — they are not a prediction of a plan’s future financial condition. Accordingly, Segal did not perform an analysis of other potential financial measurements.

Actuarial results in this report are not rounded, but that does not imply precision.

Segal does not provide investment, legal, accounting, or tax advice. This withdrawal liability valuation report is based on Segal’s understanding of applicable guidance in these areas and of the plan’s provisions. The Trustees should look to their other advisors for expertise in these areas.

While Segal maintains extensive quality assurance procedures, withdrawal liability measurements involve complex computer models and numerous inputs. In the event that an inaccuracy is discovered after presentation of Segal’s results, Segal may revise that valuation report or make an appropriate adjustment in the next valuation.

Segal’s withdrawal liability report shall be deemed to be final and accepted by the Trustees upon delivery and review. Trustees should notify Segal immediately of any questions or concerns about the final content.

As Segal Consulting has no discretionary authority with respect to the management or assets of the Plan, it is not a fiduciary in its capacity as actuaries and consultants with respect to the Plan.

SECTION 1: Actuarial Valuation Summary as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

7

Significant Issues in Valuation Year

1. The Multiemployer Pension Reform Act of 2014 (MPRA) amended ERISA to expand PBGC’s guarantee to cover qualified pre-retirement survivor annuities. As a result, the value of this benefit is included in the present value of vested benefits used for determining withdrawal liability as of June 30, 2015.

2. The market value of assets exceeds the present value of vested benefits as of June 30, 2015. Therefore, the unfunded vested liability as of that date is $0, as it was on June 30, 2014. This report has been prepared assuming that the Trustees do not elect to “fresh start” the Plan’s withdrawal liability allocation as of June 30, 2015 as permitted under ERISA Section 4211(c)(5)(E).

SECTION 1: Actuarial Valuation Summary as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

8

Summary of Key Results June 30

2014 2015 Demographic Data:

Number of pensioners and beneficiaries* 6,924 7,033 Number of inactive vested participants 5,242 4,974 Number of active vested participants** 6,579 6,536

Interest Assumptions: Valuation (funding) interest rate 7.00% 7.00%

Unfunded Present Value of Vested Benefits: Present value of vested benefits for withdrawal liability purposes $1,354,818,002 $1,403,576,915 Market value of assets 1,385,939,377 1,418,398,107 Unfunded vested liability for withdrawal liability purposes $0 $0 Withdrawal liability pools established • Basic pool -$60,320,194 $0 • Reallocated pool 0 0

*Excludes 140 alternate payees eligible for a portion of a participant’s benefit under a Qualified Domestic Relations Order in 2014 and 136 in 2015. **Includes former Plan 4 active participants with frozen benefits.

SECTION 2: Actuarial Valuation Results as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

9

The Multiemployer Pension Plan Amendments Act of 1980 (MPPAA), signed into law on September 26, 1980 and amended by the Deficit Reduction Act of 1984 (DEFRA), requires assessment of withdrawal liability on an employer that withdraws from the Plan. In general, “withdrawal” means the employer has permanently ceased operations under the Plan or has permanently ceased to have an obligation to contribute to the Plan.

A withdrawal also may be partial. Partial withdrawals are described in more detail in Section 3, Exhibit A.

If an employer reenters the Plan after incurring withdrawal liability, the withdrawal liability may be abated. This is also described in more detail in Section 3, Exhibit A.

Determination of Unfunded Vested Liability The amount of withdrawal liability is based on the Plan’s unfunded vested liability at the time of withdrawal. The “unfunded vested liability” refers to the value of vested benefits not covered by assets.

For withdrawal liability purposes, “vested benefits” are the benefits that are considered non-forfeitable if the participant incurs a permanent break in service. MPRA amended ERISA to expand PBGC’s guarantee to cover qualified pre-retirement survivor annuities. As a result, the value of this benefit is included in the present value of vested benefits used for determining withdrawal liability as of June 30, 2015. The value of these benefits is based on the Plan provisions as of the same date.

Determinations of the value of the liability for vested benefits are based on a set of actuarial assumptions. The law prescribes that the assumptions and methods used must be reasonable in the aggregate and “offer the actuary’s best

estimate of anticipated experience under the plan.” It also authorizes the PBGC to promulgate assumptions and methods for use by the Plan’s actuary. However, the PBGC has not yet promulgated any assumptions or methods.

The actuary’s “best estimate” of unfunded vested liability for this Plan involves the same actuarial assumptions as are used for plan funding with the exception of the value ascribed to Plan assets (i.e., market value), and the retirement rates for former Plan 4 active participants. Details are provided in Section 4, Exhibit III.

Allocation The Plan’s method of allocation is fully described in Section 3, Exhibit A.

Each pre-merger pool is written down according to its original schedule as allowed under Section 4211.36 of the PBGC regulations under ERISA.

The initial Plan year (June 30, 2013) liability pool is calculated by determining the unfunded vested liability as of that date and subtracting the unamortized amounts of the pre-merger pools. This pool is written down 5% per year over 20 years.

Withdrawal liability pools established after the initial Plan year liability pool are calculated as the unfunded vested liability for that year less the sum of the allocable balances of the pre-merger pools, the unamortized amount of the initial Plan year unfunded vested liability, and any pools established after the initial Plan year. These amounts also are written down 5% per year.

A. DETERMINATION OF WITHDRAWAL LIABILITY

SECTION 2: Actuarial Valuation Results as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

10

Another amount is added to the total amount to be allocated for possible withdrawal liability, namely, the amounts not collected because of bankruptcy, deductibles subtracted from amounts actually assessed, or other limitations on withdrawal assessments specified by law. These uncollected or nonassessable amounts are reallocated among the employer accounts and are also subject to 5% annual write-downs.

The PBGC has affirmed that a multiemployer plan may assess withdrawal liability to employers that withdraw even if the plan currently has no unfunded vested liability.

De minimis Each withdrawal liability assessment is the total of the unamortized balances of the allocation amounts, as defined above, less a de minimis deductible. The deductible is $50,000 but not more than ¾% of the Plan’s unfunded vested liability. This deductible amount is reduced, dollar for dollar, by the amount by which the total of charges prorated to the employer exceeds $100,000.

Payment of Withdrawal Liability The total amount of an employer’s withdrawal liability is not ordinarily payable in a lump sum. The law sets forth a basis for calculating annual amounts, to be paid in quarterly installments unless the plan has fixed some other schedule, and there is a 20-year payment maximum. The payment schedule is more fully detailed in Section 3, Exhibit A.

SECTION 2: Actuarial Valuation Results as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

11

The determination of the unfunded vested liability is based on the actuarial assumptions and methods and plan of benefits described in Section 4 of this report.

Changes Since Prior Year There have been no changes to the actuarial assumptions or plan provisions since the prior valuation.

B. UNFUNDED VESTED LIABILITY

SECTION 2: Actuarial Valuation Results as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

12

Basic Pools The Plan’s unfunded vested liabilities, as calculated for withdrawal liability purposes, for each of the past 20 Plan years are detailed in Charts 1, 2, 3, and 4 for the pre-merger Plans 2, 4 and 6 and the post-merger Plan 2, respectively. The chargeable change for each year and the remaining unamortized balance as of the valuation date are also shown. Pools established for the pre-merger Plan 2 and former Plans 4 and 6 are detailed in Section 3, exhibits B, C, and D. Pools

established for the post-merger Plan 2 are detailed in Section 3, exhibit E.

The chargeable change amount is determined as the unfunded vested liability for a given year less the greater of the sum of the previous unamortized balances or zero. The unamortized balance of each chargeable change is equal to the initial amount with a 5% write-down each year since the establishment of said amount.

CHART 1 Basic Pools as of June 30, 2015 – Pre-Merger Plan 2 Only

Plan Year Ended June 30

Unfunded Vested Liability

Chargeable Change

Unamortized Balance of Chargeable Change

1996 $79,403,387 $58,866,820 $2,943,341

1997 39,633,864 (35,519,490) (3,551,949)

1998 0 (37,159,806) (5,573,971)

1999 0 616,068 123,214

2000 0 646,871 161,718

2001 0 679,215 203,765

2002 83,806,846 84,520,022 29,582,008

2003 87,283,931 8,416,262 3,366,505

2004 47,018,573 (34,905,369) (15,707,416)

2005 36,775,805 (6,628,046) (3,314,023)

2006 49,313,579 15,821,094 8,701,602

2007 0 (45,239,209) (27,143,525)

2008 70,352,930 72,165,346 46,907,475

2009 252,743,990 187,811,741 131,468,219

2010 155,804,147 (82,128,574) (61,596,431)

2011 82,840,889 (62,258,422) (49,806,738)

2012 127,604,514 51,979,077 44,182,215

Total $100,946,009

The chargeable changes for the last 20 years for the pre-merger Plan 2 are summarized in this chart.

SECTION 2: Actuarial Valuation Results as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

13

Since the former Plan 4 used the one-pool method for allocating withdrawal liability, the pool established as of June 30, 2012 is amortized at 5% per year as if the Plan had adopted the presumptive method in the initial Plan year after the merger.

CHART 2 Basic Pool as of June 30, 2015 – Pre-Merger Plan 4 Only

Plan Year Ended June 30

Unfunded Vested Liability

Chargeable Change

Unamortized Balance of Chargeable Change

2012 $16,199,285 $16,199,285 $13,769,392

SECTION 2: Actuarial Valuation Results as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

14

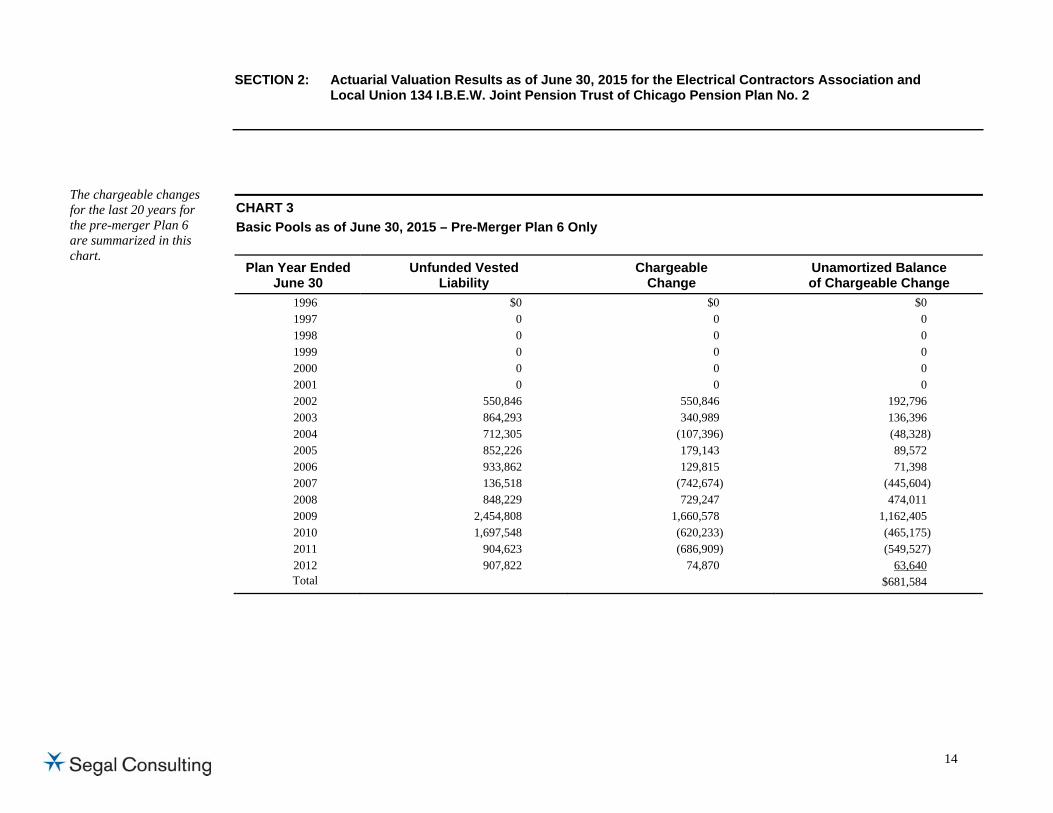

CHART 3 Basic Pools as of June 30, 2015 – Pre-Merger Plan 6 Only

Plan Year Ended June 30

Unfunded Vested Liability

Chargeable Change

Unamortized Balance of Chargeable Change

1996 $0 $0 $0

1997 0 0 0

1998 0 0 0

1999 0 0 0

2000 0 0 0

2001 0 0 0

2002 550,846 550,846 192,796

2003 864,293 340,989 136,396

2004 712,305 (107,396) (48,328)

2005 852,226 179,143 89,572

2006 933,862 129,815 71,398

2007 136,518 (742,674) (445,604)

2008 848,229 729,247 474,011

2009 2,454,808 1,660,578 1,162,405

2010 1,697,548 (620,233) (465,175)

2011 904,623 (686,909) (549,527)

2012 907,822 74,870 63,640

Total $681,584

The chargeable changes for the last 20 years for the pre-merger Plan 6 are summarized in this chart.

SECTION 2: Actuarial Valuation Results as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

15

CHART 4 Basic Pool as of June 30, 2015 – Post-Merger Pools Only

Plan Year Ended June 30

Unfunded Vested Liability

Chargeable Change

Unamortized Balance of Chargeable Change

2013 $66,540,825 ($67,113,371) ($60,402,034) 201

2014 0 (60,320,194) (57,304,184)

2015 0 0 0 To

Total ($117,706,218)

SECTION 2: Actuarial Valuation Results as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

16

Reallocated Amounts Withdrawing employers are charged with prorated shares of the “nonassessable” or “uncollectible” liabilities that are reallocated. Reallocation is more fully described in Section 3, Exhibit A.

Each annual reallocated amount is written down by 5% of the original amount for each full year from the date that it was originally determined to the end of the Plan year preceding withdrawal.

CHART 5 Reallocated Pool as of June 30, 2015 – Post-Merger Pool Only

Plan Year Ended June 30 Initial Value Unamortized Balance

2013 $193,226 $173,903 2014 2014 0 0 2015 2015 0 0

Total $173,903

SECTION 2: Actuarial Valuation Results as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

17

We have been notified of one employer that withdrew from the fund during the last Plan year and one that withdrew in the Plan year ended June 30, 2011.

Currently, six withdrawn employers are making withdrawal liability payments. These serve to fund the Plan in the same manner as employer contributions.

An employer is entitled to be advised, upon its request, of the amount of its potential withdrawal liability.

C. WITHDRAWAL LIABILITY EXPERIENCE

SECTION 3: Supplementary Information as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

18

The Plan determines the liability of an employer that has completely withdrawn on the basis of the statutory presumptive method defined in Section 4211(b) of ERISA.

The liability of an employer for complete withdrawal from the Plan is determined as the sum of the unamortized balances, as of the end of the Plan year preceding withdrawal, of the employer’s prorated shares of each of the following:

(1) the Plan’s unfunded vested liability as of June 30, 1980 (June 30, 2012 for the pre-merger Plan 4) for each pre-merger Plan;

(2) the change in the Plan’s unfunded vested liability as of the end of each subsequent Plan year (to the end of the Plan year preceding withdrawal); and

(3) reallocated amounts that would have been payable to the Plan as withdrawal liability payments for withdrawals in preceding years, except that they were nonassessable under certain statutory provisions or not collectible.

Unamortized Balances The “unamortized balance” of each of these sources of liability assessment is determined by reducing each figure by 5% of its original amount for each full year from the end of the Plan year as of which the charge was originally determined to the end of the Plan year immediately preceding withdrawal.

Initial Amount The Plan’s unfunded vested liability as June 30, 1980 (June 30, 2012 for the pre-merger Plan 4) was determined by subtracting the market value of Plan assets from the value of vested benefits under the Plan.

Annual Changes The change in the Plan’s unfunded vested liability as of the end of any Plan year is determined as follows:

(1) by establishing the Plan’s unfunded vested liability as of the end of that Plan year, and

(2) by subtracting the total, not less than zero, of (a) the unamortized balance of the initial unfunded vested liability for each pre-merger Plan and (b) the unamortized balances of each previous annual change after June 30, 1980 (June 30, 2012 for the pre-merger Plan 4) for each pre-merger Plan and the post-merger Plan.

If the Plan had no unfunded vested liability as of the end of a year, it is entered as zero.

A “positive” change represents an unfunded vested liability greater than the total of the unamortized balances and is therefore an addition to potential liability assessments for future withdrawals. A “negative” change represents an unfunded vested liability lower than the total of unamortized balances and is therefore a credit against amounts that would otherwise determine potential liability assessments for future withdrawals.

EXHIBIT A Method for Allocating Withdrawal Liability

SECTION 3: Supplementary Information as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

19

Reallocated Amounts The total amount, if any, of unfunded vested liability determined in any Plan year after June 30, 1980 (June 30, 2012 for the pre-merger Plan 4) to be nonassessable or uncollectible with respect to employers that withdrew is established as an amount to be prorated among each of the participating employers as an additional withdrawal liability amount. Nonassessable amounts consist of amounts deducted under the de minimis rule (ERISA Section 4209), amounts not payable because of the 20-year limit (ERISA Section 4219(c)(1)), and amounts not payable because of the limitations in the event of sale of all of the employer’s assets (ERISA Section 4225). Uncollectible amounts consist of amounts that the Trustees have determined are uncollectible for reasons arising out of cases under federal bankruptcy law or similar proceedings. They also include any other amount of assessed liability determined by the Plan’s Trustees to be uncollectible.

Each annual amount of reallocable nonassessables and uncollectibles is written down by 5% of the original amount for each full year from the date as of which it was originally determined to the end of the Plan year preceding withdrawal.

Proration to the Employer For determining the amount of its liability in the event of its complete withdrawal, the initial amount of unfunded vested liability, each annual change in the unfunded vested liability and each annual reallocable amount of nonassessable and uncollectible amounts is prorated to an employer on the basis of a ratio of contributions. The ratio is the employer’s obligated contributions to the Plan to total employer contributions made to the Plan during an “apportionment base period,” consisting of the five years ending with the end of the Plan year as of which each of the amounts was determined.

The total of employer contributions with respect to an apportionment base period is reduced by any contributions otherwise included in the total that were made by an employer that withdrew from the Plan in or before the Plan year in which the change or reallocation arose.

SECTION 3: Supplementary Information as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

20

Payment of Withdrawal Liability A withdrawn employer’s withdrawal liability assessment is paid in quarterly installments. The quarterly installment is calculated as one-fourth of the product of:

(a) The average base units in the three consecutive years that produce the highest average within the 10-year period ending before the Plan year of withdrawal, and

(b) the highest contribution rate in the 10-year period ending with the Plan year of withdrawal.

The number of quarterly installments is calculated on the basis of the amount of withdrawal liability and crediting interest at the actuarial valuation rate used for funding purposes. Payments are limited to a maximum of 20 years.

Maintenance of Allocations Even if no employer withdrawal had occurred, the method requires determination annually of the value of the Plan’s unfunded vested liability and of any reallocable uncollectible withdrawal liability amounts. It is also necessary for the Plan to be in a position to allocate liability to any particular employer based on its contribution history. These procedures and records are necessary in order to be able to determine an assessment should withdrawal occur and also to respond, as required by law, to an inquiry from a participating employer as to the amount of its potential liability.

Partial Withdrawal The withdrawal may also be partial. A “partial withdrawal” occurs if there is a 70% decline in the number of contribution base units or there is a partial cessation of the employer’s obligation to contribute. A 70% decline occurs if the contribution base units in the Plan year and the preceding two Plan years (the testing period) are less than

30% of contribution base units for the high base year. The “high base year” is the average of the base units in the two Plan years in which the base units were the highest within the five Plan years preceding the testing period. A partial withdrawal may also occur if an employer ceases to have an obligation to contribute under one or more, but not all of its collective bargaining agreements, and continues work in the jurisdiction, or if the employer permanently ceases to be obligated to contribute for work performed at one or more, but not all, of the facilities covered but continues the work at that facility.

Under a partial withdrawal, the amount of liability is equal to the amount of withdrawal liability for a complete withdrawal (net of any deductible), multiplied by a fraction, which is one minus a ratio. The ratio is that of the employer’s contributory hours in the Plan year following the year of the partial withdrawal to the employer's average contributory hours in the five Plan years preceding the year of the partial withdrawal.

SECTION 3: Supplementary Information as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

21

Plan Reentry PBGC has issued regulations describing the procedure to be followed in the event an employer reenters the Plan after incurring withdrawal liability. Withdrawal liability will be abated if the post-reentry level of contributory hours exceed 30% of the average of the contributory hours in the two Plan years in which the hours were the highest within the five Plan years preceding the Plan year of withdrawal.

Withdrawal liability payments due after plan reentry are abated, provided the employer posts a bond or escrow account equal to 70% of the withdrawal liability payments otherwise due. In the event of a withdrawal following reentry, the withdrawal liability is adjusted to reflect prior withdrawal liability payments.

SECTION 3: Supplementary Information as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

22

_______________________________________________________

1Years not shown have no withdrawal liability component. 2 Original value of changes in unfunded vested benefits, written down 5% per year. 3 Original value of nonassessable and uncollectible withdrawal liability, written down 5% per year. 4 Total Fund contributions for the Plan year listed and the four preceding years, excluding contributions from withdrawn employers who withdrew on or before the date the pool was established. 5 Obligated employer contributions (under the legacy Plan 2 benefit structure only) for the Plan year listed and the four preceding years, including contributions owed but not yet paid.

EXHIBIT B Employer Withdrawal Liability Worksheet For Withdrawals from July 1, 2015 Through June 30, 2016 (Pre-Merger Pools for Legacy Plan 2 Employers)

Employer Name:

Year Ended

June 301

Unamortized Balance of Withdrawal Liability Pools

Contributions During 5-Year Period Ending With Date Pool Established Liability Allocated:

[(5) ÷ (4)] x [(2) + (3)] Basic Pools2 Reallocated Pools3

Total Plan Contributions4

Obligated Employer Contributions5

(1) (2) (3) (4) (5) (6) 1996 $2,943,341 0 $83,822,097 1997 (3,551,949) 0 106,228,262 1998 (5,573,971) 0 131,470,836 1999 123,214 0 152,521,887 2000 161,718 0 178,544,514 2001 203,765 0 206,565,760 2002 29,582,008 0 216,133,040 2003 3,366,505 0 217,492,830 2004 (15,707,416) 0 217,983,135 2005 (3,314,023) 0 218,619,375 2006 8,701,602 0 221,956,860 2007 (27,143,525) 0 236,727,847 2008 46,907,475 0 260,461,520 2009 131,468,219 0 281,855,565 2010 (61,596,431) 0 288,906,275 2011 (49,806,738) 0 289,343,339 2012 44,182,215 0 289,286,530

Gross liability: (Sum of Column 6) The amount above is carried forward to Item 1 of Exhibit F.

SECTION 3: Supplementary Information as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

23

_______________________________________________________

1Years not shown have no withdrawal liability component. 2 Original value of changes in unfunded vested benefits, written down 5% per year. 3 Original value of nonassessable and uncollectible withdrawal liability, written down 5% per year. 4 Total Fund contributions for the Plan year listed and the four preceding years, excluding contributions from withdrawn employers who withdrew on or before the date the pool was established. 5 Obligated employer contributions (under the former Plan 4 benefit structure only) for the Plan year listed and the four preceding years, including contributions owed but not yet paid.

EXHIBIT C Employer Withdrawal Liability Worksheet For Withdrawals from July 1, 2015 Through June 30, 2016 (Pre-Merger Pool for Former Plan 4 Employers)

Employer Name:

Year Ended

June 301

Unamortized Balance of Withdrawal Liability Pools

Contributions During 5-Year Period Ending With Date Pool Established Liability Allocated:

[(5) ÷ (4)] x [(2) + (3)] Basic Pools2 Reallocated Pools3

Total Plan Contributions4

Obligated Employer Contributions5

(1) (2) (3) (4) (5) (6) 2012 $13,769,392 $0 $10,012,773

Gross liability: (Sum of Column 6) The amount above is carried forward to Item 2 of Exhibit F.

SECTION 3: Supplementary Information as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

24

_________________________________________________

1Years not shown have no withdrawal liability component. 2 Original value of changes in unfunded vested benefits, written down 5% per year. 3 Original value of nonassessable and uncollectible withdrawal liability, written down 5% per year. 4 Total Fund contributions for the Plan year listed and the four preceding years, excluding contributions from withdrawn employers who withdrew on or before the date the pool was established. 5 Obligated employer contributions (under the former Plan 6 benefit structure only) for the Plan year listed and the four preceding years, including contributions owed but not yet paid.

EXHIBIT D Employer Withdrawal Liability Worksheet For Withdrawals from July 1, 2015 Through June 30, 2016 (Pre-Merger Pools for Former Plan 6 Employers)

Employer Name:

Year Ended

June 301

Unamortized Balance of Withdrawal Liability Pools

Contributions During 5-Year Period Ending With Date Pool Established Liability Allocated:

[(5) ÷ (4)] x [(2) + (3)] Basic Pools2 Reallocated Pools3

Total Plan Contributions4

Obligated Employer Contributions5

(1) (2) (3) (4) (5) (6) 2002 $192,796 $0 $247,132 2003 136,396 0 384,496 2004 (48,328) 0 585,782 2005 89,572 0 865,854 2006 71,398 0 1,194,513 2007 (445,604) 0 1,718,219 2008 474,011 0 2,090,737 2009 1,162,405 0 2,472,711 2010 (465,175) 0 2,869,920 2011 (549,527) 0 3,172,097 2012 63,640 0 3,242,700

Gross liability: (Sum of Column 6) The amount above is carried forward to Item 3 of Exhibit F.

SECTION 3: Supplementary Information as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

25

_______________________________________________________

1Years not shown have no withdrawal liability component. 2 Original value of changes in unfunded vested benefits, written down 5% per year. 3 Original value of nonassessable and uncollectible withdrawal liability, written down 5% per year. 4 Total Fund contributions for the Plan year listed and the four preceding years, excluding contributions from withdrawn employers who withdrew on or before the date the pool was established. 5 Obligated employer contributions (under the post-merger Plan or any of its pre-merger benefit structures) for the Plan year listed and the four preceding years, including contributions owed but not yet paid.

EXHIBIT E Employer Withdrawal Liability Worksheet For Withdrawals from July 1, 2015 Through June 30, 2016 (Post-Merger Pools)

Employer Name:

Year Ended

June 301

Unamortized Balance of Withdrawal Liability Pools

Contributions During 5-Year Period Ending With Date Pool Established Liability Allocated:

[(5) ÷ (4)] x [(2) + (3)] Basic Pools2 Reallocated Pools3

Total Plan Contributions4

Obligated Employer Contributions5

(1) (2) (3) (4) (5) (6) 2013 (60,402,034) $173,903 $318,460,956 2014 (57,304,184) 0 337,787,475 2015 0 0 378,008,993

Gross liability: (Sum of Column 6) The amount above is carried forward to Item 4 of Exhibit F.

SECTION 3: Supplementary Information as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

26

EXHIBIT F Employer Withdrawal Liability Worksheet For Withdrawals from July 1, 2015 Through June 30, 2016

Employer Name: _____________________________________

1. Liability allocated to employer from pre-merger pools under legacy Plan 2 (from Exhibit B) .......................................................................................................................... __________

2. Liability allocated to employer from pre-merger pool under former Plan 4 (from Exhibit C) .......................................................................................................................... __________

3. Liability allocated to employer from pre-merger pools under former Plan 6 (from Exhibit D).......................................................................................................................... __________

4. Liability allocated to employer from post-merger pools (from Exhibit E) ....................... __________

5. Total liability allocated to employer: (1) + (2) + (3) + (4) ................................................ __________

6. De minimis ........................................................................................................................ $0

7. Deductible: $100,000 + (6) – (5), but not greater than (6) nor less than zero ................... $0

8. Withdrawal Liability1: (5) – (7), not less than zero ......................................................... __________

1Prior to reflecting the impact of partial withdrawal, annual payment limitation and sale of assets, if any.

SECTION 4: Actuarial Certification of Withdrawal Liability as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

27

January 25, 2016

ACTUARIAL CERTIFICATION OF WITHDRAWAL LIABILITY

This is to certify that Segal Consulting, a Member of The Segal Group, Inc., has prepared an Actuarial Valuation to calculate the pools used to assess withdrawal liability to employers who withdraw during the year beginning July 1, 2015. The calculations were performed in accordance with generally accepted actuarial principles and practices. This valuation report may not otherwise be copied or reproduced in any form without the consent of the Board of Trustees and may only be provided to other parties in its entirety.

Certificate Contents

EXHIBIT I Calculation of Unfunded Vested Liability EXHIBIT II Withdrawal Liability Pools EXHIBIT III Actuarial Assumptions and Methods EXHIBIT IV Summary of Plan Provisions

The valuation was based on information supplied by the auditor with respect to contributions and assets and by the Plan Administrator with respect to the data required on participants. We have not verified and customarily would not verify such information, but we have no reason to doubt its substantial accuracy.

I am a member of the American Academy of Actuaries and I meet the Qualification Standards of the American Academy of Actuaries to render the actuarial opinion herein. To the best of my knowledge, the information supplied in this Actuarial Valuation is complete and accurate, and in my opinion the assumptions used, in the aggregate, (a) are reasonable (taking into account the experience of the Plan and reasonable expectations) and (b) represent my best estimate of anticipated experience under the Plan.

_______________________________ David N. Strom, FSA, MAAA Vice President and Actuary Enrolled Actuary No. 14-02851

SECTION 4: Actuarial Certification of Withdrawal Liability as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

28

EXHIBIT I Calculation of Unfunded Vested Liability

The calculations include the following participants as of June 30, 2015 a. Pensioners and beneficiaries (including 1,923 beneficiaries)* 7,033 b. Inactive participants with vested pension rights 4,974 c. Active vested participants** 6,536

The actuarial factors are shown below as of June 30, 2015

1. Present value of vested benefits for withdrawal liability purposes $1,403,576,915 2. Market value of assets 1,418,398,107 3. Unfunded vested liability 0

*Excludes 136 alternate payees eligible for a portion of a participant’s benefit under a Qualified Domestic Relations Order. **Includes former Plan 4 active participants with frozen benefits.

SECTION 4: Actuarial Certification of Withdrawal Liability as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

29

EXHIBIT II Withdrawal Liability Pools (Pre-Merger Plan 2)

Pool Established

June 30

Original Amount Pool Balance on June 30, 2015*

Basic Pool Reallocated Pool Basic Pool Reallocated Pool Total Pools 1996 $58,866,820 $0 $2,943,341 $0 $2,943,341

1997 (35,519,490) 0 (3,551,949) 0 (3,551,949)

1998 (37,159,806) 0 (5,573,971) 0 (5,573,971)

1999 616,068 0 123,214 0 123,214

2000 646,871 0 161,718 0 161,718

2001 679,215 0 203,765 0 203,765

2002 84,520,022 0 29,582,008 0 29,582,008

2003 8,416,262 0 3,366,505 0 3,366,505

2004 (34,905,369) 0 (15,707,416) 0 (15,707,416)

2005 (6,628,046) 0 (3,314,023) 0 (3,314,023)

2006 15,821,094 0 8,701,602 0 8,701,602

2007 (45,239,209) 0 (27,143,525) 0 (27,143,525)

2008 72,165,346 0 46,907,475 0 46,907,475

2009 187,811,741 0 131,468,219 0 131,468,219

2010 (82,128,574) 0 (61,596,431) 0 (61,596,431)

2011 (62,258,422) 0 (49,806,738) 0 (49,806,738)

2012 51,979,077 0 44,182,215 0 44,182,215

* Basic and reallocated pools are written down annually at the rate of 5% of the original amount.

SECTION 4: Actuarial Certification of Withdrawal Liability as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

30

EXHIBIT II (Continued) Withdrawal Liability Pool (Pre-Merger Plan 4)

Pool Established

June 30

Original Amount Pool Balance on June 30, 2015*

Basic Pool Reallocated Pool Basic Pool Reallocated Pool Total Pools 2012 $16,199,285 $0 $13,769,392 $0 $13,769,392

* Basic and reallocated pools are written down annually at the rate of 5% of the original amount.

SECTION 4: Actuarial Certification of Withdrawal Liability as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

31

EXHIBIT II (Continued) Withdrawal Liability Pools (Pre-Merger Plan 6)

Pool Established

June 30

Original Amount Pool Balance on June 30, 2015*

Basic Pool Reallocated Pool Basic Pool Reallocated Pool Total Pools 1996 $0 $0 $0 $0 $0 1997 0 0 0 0 0 1998 0 0 0 0 0 1999 0 0 0 0 0 2000 0 0 0 0 0 2001 0 0 0 0 0 2002 550,846 0 192,796 0 192,796

2003 340,989 0 136,396 0 136,396

2004 (107,396) 0 (48,328) 0 (48,328)

2005 179,143 0 89,572 0 89,572

2006 129,815 0 71,398 0 71,398

2007 (742,674) 0 (445,604) 0 (445,604)

2008 729,247 0 474,011 0 474,011

2009 1,660,578 0 1,162,405 0 1,162,405

2010 (620,233) 0 (465,175) 0 (465,175)

2011 (686,909) 0 (549,527) 0 (549,527)

2012 74,870 0 63,640 0 63,640

* Basic and reallocated pools are written down annually at the rate of 5% of the original amount.

SECTION 4: Actuarial Certification of Withdrawal Liability as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

32

EXHIBIT II (Continued) Withdrawal Liability Pools (Post-Merger)

Pool Established

June 30

Original Amount Pool Balance on June 30, 2015*

Basic Pool Reallocated Pool Basic Pool Reallocated Pool Total Pools 2013 ($67,113,371) $193,226 ($60,402,034) $173,903 ($60,228,131)

2014 (60,320,194) 0 (57,304,184) 0 (57,304,184)

2015 0 0 0 0 0

* Basic and reallocated pools are written down annually at the rate of 5% of the original amount.

SECTION 4: Actuarial Certification of Withdrawal Liability as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

33

EXHIBIT III Actuarial Assumptions and Methods

Investment Return: 7.00%

Administration Expenses: No separate expense charge

Valuation of Assets: At market value

Mortality Rates: Healthy: RP-2014 Blue Collar Mortality Table, set forward one year and projected generationally using Scale MP-2014 (post-retirement based on Healthy Annuitant Table and pre-retirement based on Employee Table)

Disabled: RP-2014 Disabled Retiree Mortality Table, set forward two years and projected generationally using Scale MP-2014

The underlying tables with the generational projection to the ages of participants as of the measurement date reasonably reflect the mortality experience of the Plan as of the measurement date. The mortality tables were then adjusted to future years using generational projection under Scale MP-2014 to reflect future mortality improvement.

The mortality rates were based on historical and current demographic data, adjusted to reflect health characteristics of the area and industry, and estimated future experience and professional judgment. As part of the analysis, a comparison was made between the actual number of deaths by age and the projected number based on the prior year’s assumption.

SECTION 4: Actuarial Certification of Withdrawal Liability as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

34

Termination Rates before Retirement: Mortality Rates (%)*

Age Male Female 20 0.06 0.02 25 0.06 0.02 30 0.06 0.03 35 0.07 0.03 40 0.09 0.05 45 0.14 0.08 50 0.24 0.14 55 0.40 0.20 60 0.68 0.30 *Mortality rates shown for base table.

SECTION 4: Actuarial Certification of Withdrawal Liability as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

35

Termination Rates before Retirement (continued): Disability Rates (%)

Age Legacy Plan 2 Former Plans 4 and 6 20 0.03 0.09 25 0.05 0.10 30 0.07 0.11 35 0.10 0.12 40 0.16 0.15 45 0.25 0.21 50 0.40 0.44 55 3.00 1.16 60 4.53 2.36

Withdrawal Rates* (%)

Age Legacy Plan 2 Former Plans 4 and 6 20 6.00 9.00 25 6.00 9.00 30 5.00 8.00 35 5.00 8.00 40 4.00 7.00 45 4.00 7.00 50 3.00 6.00 55 3.00 6.00 60 3.00 6.00 *Withdrawal rates cease at early retirement age. Rates for non-vested participants are the rates shown

above plus 5%.

SECTION 4: Actuarial Certification of Withdrawal Liability as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

36

Retirement Rates: Age* Legacy Plan 2 Former Plan 6 55-57 7.5% 7.5% 58-60 10 10 61 25 25 62 60 25 63 30 25 64 50 25 65 45 50 66 25 50 67-69 30 50 70 100 100

*if eligible

Former Plan 4 participants are assumed to retire at the earliest eligible age.

Retirement Age for Inactive Vested Participants: 62

Unknown Data for Participants: Same as those exhibited by participants with similar known characteristics. If not specified, participants are assumed to be male.

Definition of Active Participants: Active participants are defined as those with at least 400 hours in the most recent plan year (450 for former Plans 4 and 6), excluding those who have retired as of the valuation date.

Percent Married: 80%

Age and Gender of Spouse: Spouses are assumed to be 3 years younger than male participants and 3 years older than female participants. If not specified, spouses are assumed to be the opposite gender of the participant.

Benefit Election: Married participants are assumed to elect the most valuable form of payment and non-married participants are assumed to elect the single life form of payment.

SECTION 4: Actuarial Certification of Withdrawal Liability as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

37

Allocation Method: Presumptive

Contribution Period for Prorating Liabilities: 5 years

De minimis Deductible: $50,000, or ¾% of the unfunded vested liability, if smaller. The deductible is reduced, dollar for dollar, if the gross assessment is in excess of $100,000.

SECTION 4: Actuarial Certification of Withdrawal Liability as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

38

EXHIBIT IV Summary of Plan Provisions

This exhibit summarizes the major provisions of the Plan included in the valuation. It is not intended to be, nor should it be interpreted as, a complete statement of all plan provisions.

Plan Year: July 1 through June 30

Pension Credit Year: January 1 through December 31

Plan Status: Ongoing plan

Normal Pension: Age Requirement 65 Service Requirement 5 years of Eligibility Service Amount Legacy Plan 2: $55.00 per year of Credited Service, increasing to $75.00 for Credited

Service earned January 1, 2013 and later. Former Plan 4: Applicable accrual rates based on contribution rates for service prior to

January 1, 2006. For service on or after January 1, 2006, $39 per year of Credited Service for participants whose employers contribute at or above the Conforming Contribution Rate per week; a lower pension rate of $7 per year of Credited Service for participants whose employers contribute less than the Conforming Contribution Rate per week.

Former Plan 6: $29 times Credited Service limited to 10 years, plus $35.50 times Credited Service in excess of 10 years.

Early Retirement: Age Requirement 55 Service Requirement 10 years of Eligibility Service (5 years if age 62 or older) Amount Normal pension reduced by 6% for each year of age less than 62

SECTION 4: Actuarial Certification of Withdrawal Liability as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

39

Vesting: Age Requirement None Service Requirement 5 years of Eligibility Service Amount Normal or early pension based on plan in effect when last active Normal Retirement Age 62

Pre-Retirement Death Benefit (Qualified Pre-Retirement Survivor Annuity)*: Age Requirement None Service Requirement 5 years of Eligibility Service Amount 50% of the benefit participant would have received had he or she retired the day

before he or she died and elected the joint and survivor option. If the participant died prior to eligibility for an early retirement pension, the spouse’s benefit is deferred to the participant’s earliest retirement date.

*The Plan provides a more generous pre-retirement death benefit to the surviving spouse and dependent children. However, for withdrawal liability purposes, only the qualified pre-retirement survivor annuity is included.

Optional Forms of Payment: Single Life Annuity

50% Joint and Survivor Annuity

75% Joint and Survivor Annuity

Joint and Survivor Annuity with 100% continuing to the spouse for 120 months after the participant’s death and 50% of the benefit thereafter (not available to former Plan 6 participants)

Participation: After contributions have been made on an employee’s behalf

Credited Service: One year of Credited Service for each calendar year with 1,600 hours of covered employment, with partial credit for 400-1,599 hours and proportional additional credit for hours greater than 1,600. For former Plans 4 and 6, one year of Credited Service

SECTION 4: Actuarial Certification of Withdrawal Liability as of June 30, 2015 for the Electrical Contractors Association and Local Union 134 I.B.E.W. Joint Pension Trust of Chicago Pension Plan No. 2

40

for each calendar year with 1,800 hours of covered employment, with partial credit for 450-1,799 hours and proportional additional credit for hours greater than 1,800.

Eligibility Service: One year of Eligibility Service for each calendar year with 400 hours of covered employment (450 for former Plans 4 and 6), or 1,000 hours of any employment with the same employer

Contribution Rate: Legacy Plan 2: $8.90 per hour, effective June 2015.

Former Plan 4: The highest contribution rate is $144 per week, effective July 1, 2014. The average contribution rate as of June 30, 2015 is $132.5228 per week.

Former Plan 6: $102.50 per week, effective July 1, 2009.

Changes in Plan Provisions: There have been no changes in plan provisions reflected in this valuation.

5564928v3/03320.010

![Bellator 134: The British Invasion Press Conference [Bellator Fighting Championships 134]](https://static.fdocuments.us/doc/165x107/55c4afa0bb61eb74118b4692/bellator-134-the-british-invasion-press-conference-bellator-fighting-championships.jpg)

![[3902] – 134](https://static.fdocuments.us/doc/165x107/617ded9f7069a83eef3cce3d/3902-134.jpg)