15-04-10 Toscafund Discussion Paper - 2015 UK Election Outcome - Update

Upload

savvas-savouriCategory

view

14download

1

Toscafund Discussion Paper April 2015 The 2015 UK Election outcome – A welcome break from Politics

1

As much as a continuation of coalition is its best outcome let me try to explain why a

Labour/SNP “pact” which removes the Conservatives from Westminster for a short while –

less than twelve months – is actually GOOD NEWS FOR THE CONSERVATIVE PARTY. So good

in fact, that it would ensure it governs in Westminster almost uncontested and without much

need for coalition partners in the years to come. Indeed, I would argue that it is the better

outcome than the Conservative Party being hostage to the SNP from May 8th

. Let me

elaborate.

Suppose, just suppose, a Labour/SNP ‘pact’ is forged in Westminster removing Cameron and

installing Miliband. This is what will then unfold with CERTAINTY.

1. The Scottish Labour Party (SLP) will do what the Gang of Four did in 1981 when they formed the SDP. The SLP WILL leave the

Parliamentary Labour Party. Why? Because only as a party separate from the London leadership can the SLP have any hope

of credibly fighting the SNP for power in Holyrood, not least when elections are held on May 5th

next year. After all, the SLP

risks being totally marginalised and/or its members defecting in the wake of a Westminster “pact” with the SNP. As an

independent party the SLP will for the first time introduce, a small ‘n’, nationalist rival to the SNP. And just as the SNP will

negotiate to extract concessions from Westminster, the SLP could offer to do a deal with its erstwhile party in Westminster,

ONLY if it gets what it wants and so getting defectors from the SNP. For the Parliamentary Labour Party “losing” its strong

representation in Scotland – where it has held over forty seats since the mid sixties - would be a structural body blow. The

Scottish Conservative Party could itself separate from the Parliamentary Party, in its case with the blessing of Conservative

HQ in London’s Milbank House. Why? Because as a separate party the Scottish Conservatives could begin to regain the

support they had enjoyed as recently as the mid sixties, when it had broadly the same MP’s in Scotland as Labour.

Remember the SNP contains many NATIONALISTS who are NATURAL Conservatives. Let me repeat the words I penned in

2010 in the paper “Scottish fiscal independence by 2015?”

Amongst younger elements of the Scottish Conservatives, their prospects in Holyrood have begun to look bleak unless

they somehow distance themselves from the parliamentary party. With this in mind, Murdo Fraser, the Deputy Leader

of the Scottish Conservative Party, suggested it regain its pre-1965 independence.

Whilst Murdo Fraser MSP is no longer deputy leader of his party, he remains a powerful figure within it. For the SNP, the

prospect of independent Labour and Conservative rivals in Scotland would hardly be welcome. It will recognise this as the

Holyrood elections approach to the point it quickly breaks the ties it might have knotted with Labour in Westminster.

GOOD NEWS FOR THE CONSERVATIVES.

2. Seeing how their votes have “back-fired” the 1.5 million natural Conservatives who voted UKIP will return. GOOD NEWS FOR

THE CONSERVATIVES.

3. The SNP is STILL AN INDEPENDENCE PARTY. And in a Pact with the Labour Party in Westminster it will agitate to such an

extent for powers to be transferred to Holyrood that there is NO WAY the rule that “Only English MP’s vote on English laws”

could not come about. In effect the SNP will agitate to neutralise the representation of ALL Scottish Constituency MP’s in

Westminster. GOOD NEWS FOR THE CONSERVATIVES.

4. As much as the surge in the SNP will be a notable factor in providing Labour with - a year in - Government, so too “the

collapse to 15” in Liberal Democrat seats deprives Cameron’s coalition partner of the strength it needs to continue to their

partnership. Of course if the Lib Democrats do surprise on the upside say by holding 25-30 seats then Cameron remains

Prime Minister and the SNP cannot hold him hostage. But let’s imagine that the Liberal Democrats fail to muster more than

15-20 seats. In this case one can be confident Nick Clegg and Danny Alexander have lost their seats. In this event the Liberal

Democratic Party post Clegg will be a very different political party. It will be one almost certainly led by a former Labour

Party member, Vince Cable. In effect the Liberal Democrat Party will shift from being broadly right-of-centre to the left. As

such the Liberal Democrat Party would become more of a rival to Labour than the Conservatives. The Liberal Democrats

would even add to the rivalry faced by the SNP were its Scottish Party to follow Labour and the Conservatives north of the

border in declare effective independence from its Westminster leadership. Remember, seats in Holyrood are allocated not

simply by a first by the post system but on the basis of overall votes. GOOD NEWS FOR THE CONSERVATIVES.

Author:

Dr Savvas Savouri

Contact information

Toscafund Asset Management LLP

90 Long Acre

London WC2E 9RA

England

t: +44 (0) 20 7845 6100

f: +44 (0) 20 7845 6101

w: www.toscafund.com

Toscafund Discussion Paper April 2015 The 2015 UK Election outcome – A welcome break from Politics

2

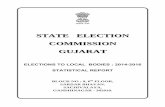

Figure 1 Figure 1 Figure 1 Figure 1 –––– Latest Predicted Election Outcome May, 2015Latest Predicted Election Outcome May, 2015Latest Predicted Election Outcome May, 2015Latest Predicted Election Outcome May, 2015

Note: Calculated from constituency analyses – Professor R. Rose, Founder-Director of Centre for the Study of Public Policy, Uni. of Strathclyde, Glasgow

5. Whatever its showing on May 7th the Conservative Party will have a certain Boris Johnson MP in Westminster, a political

animal who managed to win two mayoral votes across the UK’s capital where Labour holds 38 parliamentary seats to the

Conservatives 28; the Liberal Democrats making up the other 7. As a senior figure in the Conservative shadow Cabinet Boris

Johnson cannot possibly do the party harm. After all, he crash-tests practically every political/personal gaff and comes out

not only almost unscathed, but on occasion more popular. Indeed, one cannot help seeing Johnson’s career in the context of

the Conservative on whom he recently penned a sizeable biography, Churchill. Ahead of a second General Election and

whether in the Shadow Cabinet or even leader of the opposition, The Honourable Boris Johnson MP is GOOD NEWS FOR

THE CONSERVATIVES.

6. Two developments on which there is broad agreement are the impressive display made by Nicola Sturgeon and the often

impressively prime ministerial displays made by Ed Miliband. Indeed, one can only imagine TV coverage of Miliband being

Prime Ministerial in Westminster with Sturgeon close by in the shot. But that’s just it WE CAN ONLY IMAGINE this, because

Nicola Sturgeon already has a seat in Parliament, the Scottish one. In the event of some form of pact between The

Parliamentary Labour Party and the SNP, the person who will most often be caught on camera with Miliband in Westminster

will be Alex Salmond MP. After all each time the SNP boasts on what powers it has transferred from London to Edinburgh be

assured Salmond will be the person sharing the ‘good news’. I can see this playing badly for Labour with English voters,

including Labour supporters. Indeed, English Labour supporters voting UKIP this time might on seeing that party's poor

showing, shift to the Conservatives when the next election is contested. Remember too that every power over tax

transferred to Holyrood means that the SNP become ACCOUNTABLE and IDENTIFIABLE as the hand on the nasty tax tiller.

And as the SNP raises taxes many of the Nationalists within it who are conservative in their fiscal thinking could well depart

to the large C version of their allegiances, particularly if as I have argued it is a largely independent Scottish Conservative

Party. GOOD NEWS FOR THE CONSERVATIVES.

7. In the Election update piece we penned at the beginning of the month, I made this observation:

“Ultimately what will most significantly influence how sterling and Gilts perform is what the OBR and MPC choose to

write and say about the economic policies presented in any Labour/SNP Pact.”

In essence in their authoritative way, the OBR and MPC will hardly help Chancellor Balls. Quoting again from the last

note:

“The MPC would be expected to have something to say on how appropriate its continued monetary restraint was.”

In short, whilst Labour's commitment to abolishing stamp duty for first-time buyers will play well ahead of the general

election, the practicalities of it and its “allies” stated fiscal policies mean that on being the main party of Government Labour

will be associated with the first rise in the base rates in five years, a shift which can hardly help it with mortgaged Britons.

GOOD NEWS FOR THE CONSERVATIVES.

So then, there you have it. Whilst the best outcome for the Conservatives would be continuing their coalition with the

Liberal Democrats, a sojourn in opposition could prove a VERY WELCOME BREAK.

300

262

46

15 10 10 4 3

0

50

100

150

200

250

300

350

CON Labour SNP Lib Dems Other Unionist UKIP Plaid

Se

ats

326 majority

Toscafund Discussion Paper April 2015 The 2015 UK Election outcome – A welcome break from Politics

3

Toscafund Discussion Papers

The 2015 UK Election Outcome - Update, April 2015

Prime Central London Residential Property, March 2015

The 2015 UK Election Outcome, January 2015

The Darkest of Greek Dramas; A Play for Survival, January 2015

Growth of Britain’s Primary Cities, October 2013

Banking-on positive change in London’s property markets, 19 April 2013

Where in the world is this looming food price crisis? 1 March 2013

Britain’s Got Growth II: beating Germany on penalties, 17 January 2013

Seeing a quite different island in 20/20, 21 September 2012

Britain’s Got Growth, 31 May 2012

The building storm over Cyprus – Update, 18 May 2012

The Darkest of Greek Dramas: A Play for Survival, 16 May 2012

London 20/20 – Update, 30 March 2012

Update: Plotting North Korea’s path from regime-change to reunion, 20 December 2011

A Western Balkans crisis: A Europe wide problem, 2 November 2011

Plotting North Korea’s path from regime-change to reunion, 13 September 2011

Update: Scottish fiscal independence by 2015?, 13 June 2011

Cape Fear; South Africa’s chilling outlook, 18 March 2011

Scottish fiscal independence by 2015? 26 July 2010

Clouds darkening over Cyprus, 22 April 2010

Australia and Japan The best and worst of the G20, 26 March 2010

Who could possibly laugh through a Greek Tragedy? 8 February 2010

An employment outlook for London in 20/20, 13 January 2010

An A to Z journey into the economic future, 14 December 2009

An outlook for Canada & Mexico: Seismic Continental drift, 10 November 2009

Taking lessons in history, 5 August 2009

The REAL interest rate story, 20 July 2009

Balkan Four pose a greater risk than the Baltic Three, 30 June 2009

Dissin’ the Dollar, 25 June 2009

Release the Baltic Three, 3 June 2009

Toscafund Economic Papers

Issue 31 – EXITSTENTIAL thinking

Issue 30 – 2015, Thank you for reading

Issue 29 – My grateful nation, October 2014

Issue 28 – UK housing issues and solutions, July 2014

Issue 27 – Scotland’s Special Issue, June 2014

Issue 26 – Just lots of boring words, May 2014

Issue 25 – Vive la difference, April 2014

Issue 24 – Europe in crisis again, as Britain stands out, March 2014

Issue 23 – It’s all just talk really, January 2014

Issue 22 – TOSCANOMICS confronts…, November 2013

Issue 21 – Darn…, August 2013

Issue 20 – On matters United, June 2013

Issue 19 – Oh, Historic times, February 2013

Issue 18 – Why we should welcome Britain’s export earnings softening, December 2012

Issue 17 – Largely un-American, November 2012

Issue 16 – Back to the future, October 2012

Issue 15 – Europe: motoring to recession, August 2012

Toscafund Discussion Paper April 2015 The 2015 UK Election outcome – A welcome break from Politics

4

Toscafund Asset Management LLP

Important Notice

This document is confidential. Accordingly, it should not be copied, distributed, published, referenced or reproduced, in whole or in part, or disclosed by any

recipient to any other person. By accepting this document, the recipient agrees that neither it nor its employees or advisors shall use the information

contained herein for any other purpose than evaluating the transaction. This document, and the information contained herein, is not for viewing, release,

distribution or publication in any jurisdiction where applicable laws prohibit its release, distribution or publication.

This document is published by Toscafund Asset Management LLP (“Toscafund “), which is authorised and regulated by the Financial Conduct Authority (“FCA”)

and registered with the U.S. Securities and Exchange Commission as an Investment Adviser. It is intended for Eligible Counterparties and Professional Clients

only, it is not intended for Retail Clients.

The collective investment schemes managed by Toscafund (the “Funds”) are unregulated collective investment schemes, which pursuant to sections 238 and

240 of the Financial Services and Markets Act 2000 may only be promoted to persons who are sufficiently experienced and sophisticated to understand the

risks involved and satisfy the criteria relating to investment professionals. Persons other than those who would be regarded as investment professionals must

not act upon the information in this document or acquire units/shares in the schemes to which this document relates.

The information contained in this document is believed to be accurate at the time of publication but no warranty is given as to its accuracy and the

information, opinions or estimates are subject to change without notice. Views expressed are those of Toscafund only. The information contained in this

document was obtained from various sources, has not been independently verified by Toscafund or any other person and does not constitute a

recommendation from Toscafund or any other person to the recipient. In furnishing this information Toscafund undertakes no obligation to provide the

recipient with access to any additional information to update or correct the information.

The information contained in this document does not constitute a distribution, an offer to sell or the solicitation of an offer to buy any securities or products in

any jurisdiction in which such an offer or invitation is not authorised and/or would be contrary to local law or regulation. Specifically, this statement applies to

the United States of America (“USA”) (whether residents of the USA or partnerships or corporations organised under the laws of the USA, state or territory),

South Africa and France. Any offering is made only pursuant to the relevant offering document and the relevant subscription application, all of which must be

read in their entirety. No offer to purchase securities will be made or accepted prior to receipt by the offeree of these documents and the completion of all

appropriate documentation.

Prospective investors should inform themselves and take appropriate advice as to any applicable legal requirements and any applicable taxation and exchange

control regulations in the countries of their citizenship, residence or domicile which might be relevant to the subscription, purchase, holding, exchange,

redemption or disposal of any investments in the Funds. In certain jurisdictions the circulation and distribution of this document and the sale of interests in the

Funds are restricted by law. The information provided herein is for general guidance only, and it is the responsibility of any person proposing to purchase

interests in any of the Funds to inform himself, herself or itself of, and to observe, all applicable laws and regulations of any relevant jurisdiction. Prospective

investors must determine that: (i) they have the authority to purchase interests; (ii) there are no legal restrictions on their purchase of interests; and (iii) the

offer or sale of interests is lawful in the jurisdiction applicable to them.

Funds managed by Toscafund have agreed to modify investment terms for certain investors for bona fide commercial reasons, subject to applicable law and

regulation. Lower performance fees were negotiated in the case of certain institutions and individuals who made substantial investments or who agreed to

specified lock-up periods. An investor was also provided with the right to the same preferential treatment agreed with (if so agreed) subsequent similar or

smaller investors. None of the investors with whom modifications have been agreed have any legal or economic links with the funds managed by Toscafund

and/or with Toscafund. To the extent there have been any modifications, these have not resulted in an overall material disadvantage to other investors.

No liability is accepted by any person within Toscafund for any losses or damage arising from the use or reliance on the information contained in this

document including, without limitation, any loss or profit, or any other damage; direct or consequential. No person has been authorised to give any

information or to make any representation, warranty, statement or assurance not contained in the relevant offering document and, if given or made, such

other information, representation, warranty, statement or assurance may not be relied upon. The content of this document may not be reproduced,

redistributed, or copied in whole or in part for any purpose without Toscafund’s prior express consent. This document is not an advertisement and is not

intended for public use or distribution. The source of all graphs and data is as stated, otherwise the source is Toscafund.

For Swiss prospective investors: The Fund has not been approved for distribution in or from Switzerland by the Swiss Financial Market Supervisory Authority.

As a result, the Fund’s shares/units may only be offered or distributed to qualified investors within the meaning of Swiss law. The Representative of the Fund

in Switzerland is Bastions Partners Office SA with registered office at Route de Chêne 61A, 1208 Geneva, Switzerland. The Paying Agent in Switzerland is

Banque Heritage, with registered office at Route de Chêne 61, 1208 Geneva, Switzerland. The place of performance and jurisdiction for Shares/Units of the

Fund distributed in or from Switzerland are at the registered office of the Representative.

Past performance is not an indicator of future performance and the value of investments and the income derived from those investments can go down as well

as up. Future returns are not guaranteed and a total loss of principal may occur. Please note that performance information is not available for five years.

© 2015, Toscafund, All rights reserved.