El Salvador: Country Economic Memorandum - All … · El Salvador: Country Economic Memorandum Augt...

152

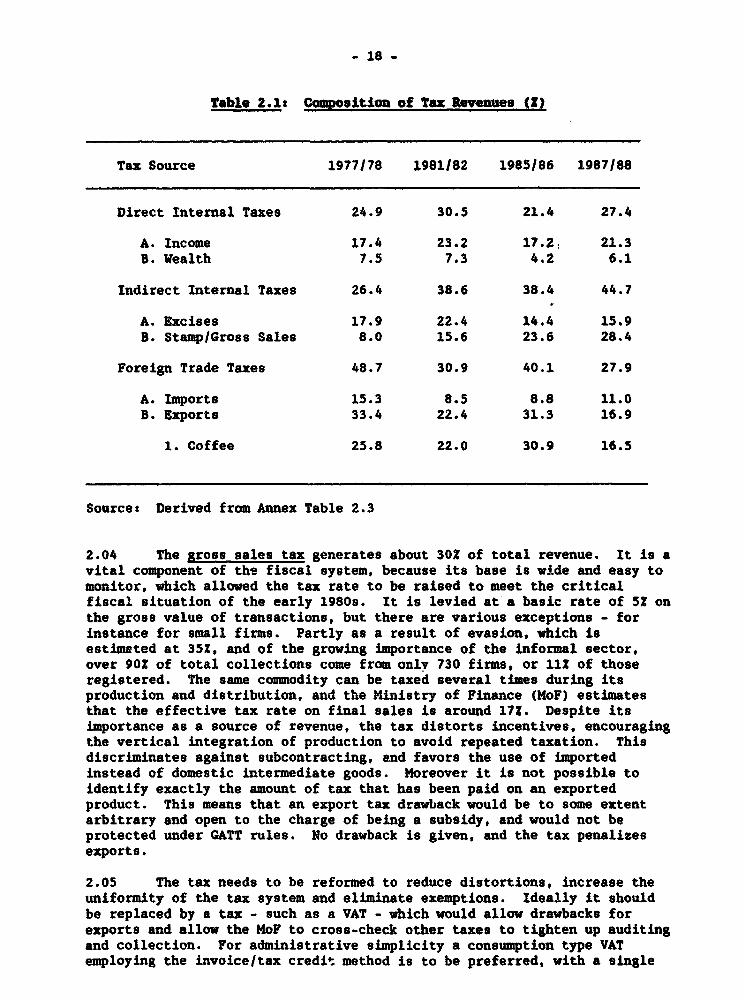

Report No. 781M8M ElSalvador: Country Economic Memorandum Augt 14, 1989 Latin America and theCaribbean Regional Office Country Department II FOROFFICIALUSE ONLY t4 iDms 1 d?,' e -, O (, I 4 O . , . ' 6 .. : > s ^ - - 0~~~~~ Do=- "., 'e 'd .', te " .;bdd Ba < , Thi' -s d -'.,ocmn ha,s -a msrce d.tiuo an ma be ou'se<d by reci, -e-to onl.i tle. gef c of thei of,e@al . . ... Icnet -m~ay no;t otherwise '~~~~ D' / v. 2D ; 57~~~ ... J < _ } ) .> o I~~~ ~Q O ' W B authorization. 0 . . . S 0 3 ', n: .. S, .~~ ~ ~ ~ ~ ~ ~ ~ ~ ~ . .~~~~~~~~ This document has a irsticzed <ltibutIo and maybe usedby-recipients. only in te perfo~mance of teir official duties. Its contents maynotothierwise - - ? be discloseLwitotWoutdd8ank aatoization. - . ~ Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of El Salvador: Country Economic Memorandum - All … · El Salvador: Country Economic Memorandum Augt...

Report No. 781M8M

El Salvador:Country Economic Memorandum

Augt 14, 1989

Latin America and the Caribbean Regional OfficeCountry Department II

FOR OFFICIAL USE ONLY

t4 iDms 1 d?,' e -, O (, I 4 O . , . ' 6 . . : > s ^ - -

0~~~~~

Do=- "., 'e 'd .', te " .;b dd Ba < ,

Thi' -s d -'.,ocmn ha,s -a msrce d.tiuo an ma be ou'se<d by reci, -e-toonl.i tle. gef c of thei of,e@al . . ... Icnet -m~ay no;t otherwise

'~~~~ D' / v. 2D ;

57~~~ ... J <

_ } ) .> o I~~~ ~Q

O ' W B authorization.

0 . . . S

0 3 ', n: .. S,

.~~ ~ ~ ~ ~ ~ ~ ~ ~ ~ .

.~~~~~~~~

This document has a irsticzed <ltibutIo and may be used by-recipients. only in te perfo~mance of teir official duties. Its contents may not othierwise - -

? be discloseLwitotWoutdd8ank aatoization. - . ~

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit - ColonUS$1 - CS

Fis%al YearJanuary 1 - December 31

WEIGHTS AND MEASURES

Manzana (Mz) - 0.59 Hectares (Ha)Metric Ton (MT) - 2Z04.6 lbs.

Spanish Quintal (QQ) - 46 kilograms

GLOSSARY OF ABBREVIATIONS

ADS Salvadoran Demographic AssociationANDA National Water and Sewage AuthorityANTEL National Telecommunications AuthorityBCR Central Reserve BankBFA Agricultural Dewelopment BankBH Mortgage BankCACM Central American Common MarketCBI Caribbean Basin InitiativeCDT Tax Discount CertificatesCEL Electricity Supply UtilityCENTREX Export and Import Documentation CenterCET Common External Tariff of the CACHCIF Including Carriage, Insurance and FreightCONADE National Commission for Displaced PersonsCOPAL Cooperative for cotton ginning, marketing and exportCORSAIN Salvadoran Investment CorporationCPI Consumer Price IndexCPR Prompt Foreign Excha.ae Coneersion CertificatesDIGEPROY Projects Directorate oif wHoPFESAL Family Health Sur:eyFUSADES Salvadoran Found-tion for Economic and Social DevelopmentGDP Gross Domestic ProductICA International Coffee AgreementICO International Coffee OrganizationICOR Incremental Capital Output RatioIDB Interamerican Development BankINAZUCAR National Sugar InstituteINCAFE National Coffee InstituteIRA Institute for Supply RegulationISIC Coffee Research InstituteISSS Salvadoran Social Security InstituteISTA Agrarian Reform InstituteHAG Ministry of Agriculture and LivestockHE Ministry of EconomyMIPLAN Ministry of Planning

MOF Ministry of FinanceMOH Ministry of HealthNPS Non-Factor ServicesNGO Non-Governmental OrganizationNTB Non-Tariff BarrierPERA Agrarian Reform Evaluation Project of MAGPL 480 Public Law 480 - US Food AidSCT Selective Consumption TaxSSMA San Salvador Metropolitan AreaUNDP United Nations Development ProgramUSAID US Agency for International Development

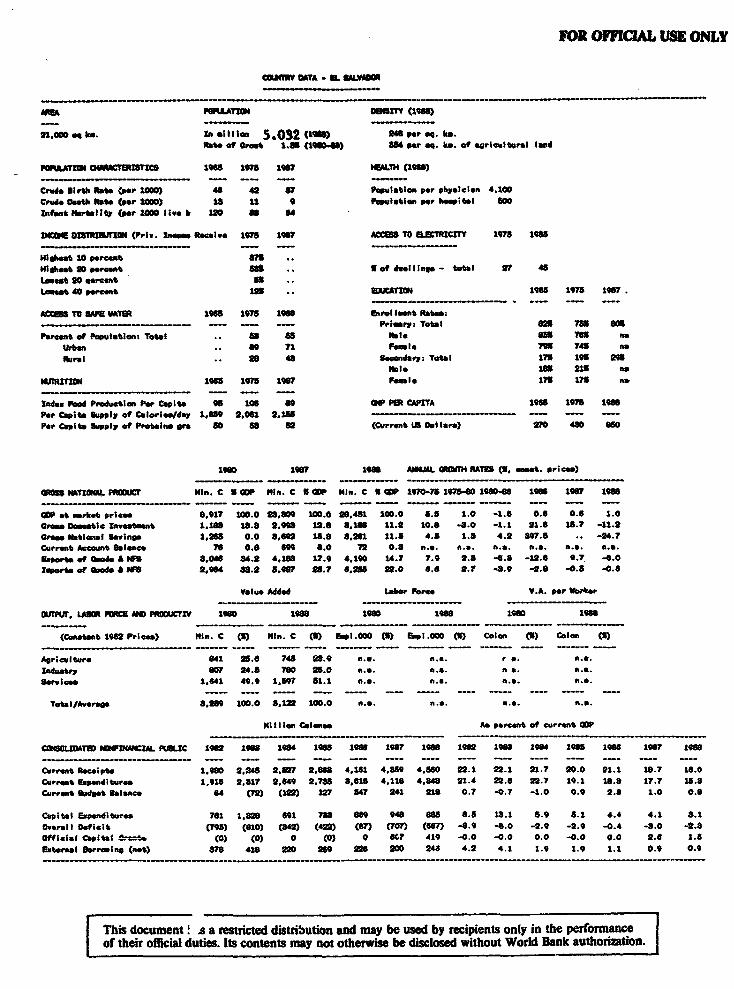

FOR OMFCUL USE ONLY

COer7 MA - I. SALWI

18 oPLATI8 08e61 (195)

u11.o0 eq lIo. In &ilioen 5.032 (16) u par oq. km.Rate of r 1. (1 ) U r eq. km. ft aoricultural lald

POPlaAI _ DVTItI98 S195 1078 16 HEALF14 (19186t )

Crud tIr Rate (por 1000) 48 42 87 Ppulation per phyaician 4.100CrWd Osti Rte (e 100 is 11 9 Pulation VWr hep btal M00Infanti Nsrutai0 (p. 1000 liv. Ic 180 so 84

incu 1wS1m1 l (Priv. nme Reeive 1975 16W TO UEIRRICITY 1t97 19S

iht 10 percenmtHii)s 20 6prct Slt tS de I nag* - toIt 07 48Lmeet 50 teroant 5iLamet 40 percent 1u5 iATri 196 17 I"7

AU6 TO SAM WATS 1968 1975 1966 Enrol lmnt Retee- - - - Primry: Total an 7S5 BOB

Pe rcet of pulation: Total a6 "5 lll* 605 761 naUrban 69 71 Feml, 79 74 nasRural 118US 43 Secondary: Total 171 195 go

ibDi 185 215 ma;URIT 196 17 197 iemle 13 17u no

Idex Feod Prnoductio Per Capita 9 106 a9 OW P6t CAPITA 196 1978 19Par Capita Supply of CIorle/dary 1.61,l 2.061 2,155Per Capita Supply of Pretnea afa sO 88 8 (Current Us Dellar.) 070 480 W

1I90 198?7 1s90 MAM.L C114 RABS (S, cont, price.)

1305 NATQINI. i0MT Min. C S DP nm. C I CDP 141. C * 96P 1970-75 1975-0 190-6 1966 96W 196

-DP at varbet prices 8.917 100.0 19.809 100.0 20.431 100.0 5.8 1.0 -1.5 0.6 0.S 1.0Greaw Doobtle Investent 1.1,8 1s.8 20.99 10.8 8.181 11.2 10.0 -8.0 -1.1 01.6 15.7 -S1.2Groas Natioal Slavine 1,i6 0.0 5.6S0 1S.8 .S2t 11.5 4.8 1.8 4.2 897.8 .. .4.7Current Account blanc. 78 0.8 69 8.0 72 0.8 a.a. n.e. n.a. a.a. a.a. U.e.Exper,a of am"*e NFS 8,04U S .0 4,188 17.9 4,190 14.7 7.9 2.8 -4.8 -12.6 9.7 ? 4.0Iow"rt of CNd aF8 W,s4 88.0 B."t? Q5.7 6.15 92.0 6.e Q.7 -4.9 -0.8 -0.5 -0.5

Value Added Lr Fi V.A. per Worker

OUT LA, BOR ME MPO iCTV 1960 lC19 1960 1986 1980 1966

(Comtnt 1962 Prices) Hin. C (S) "mo. C (5) rEI.000 (S) EmpI.000 (S) Colon (S) Colon (

Agriculture 841 26.6 74t 28.9 n.-. n.c. r c. a.a.induetry 607 24.8 780 Q5.0 n.e. na. n a. n.a.Sevice 1.64 49.9 1.59? 51.1 n.. n... a.a. n.a.

T@tal/Awerse 8.299 100.0 8.12a 100.0 n.e.

Mil lIon Coleane An perrent of curret GDP

COSOLDTE PRW CAL RLIC 1sc2 195 19s 19S 1966 1967 1960 1982 1968 19 195 19w 1987 196

Current ReceiptS 1.990 2,28 2,507 2.8iU 4.11 4,869 4.S60 22.1 22.1 21.7 06.0 01.1 18.7 16.0Currio Eepditurea 1.91S 2,817 2.649 2.785 8,618 4,118 4.848 21.4 22.8 22.7 19.1 18.8 17.7 15.8Current a dget blance f4 (70) (10) 127 547 241 201 0.7 -0.7 -1.0 0.9 2.8 1.0 0.6

Capital Esenditures 761 1.328 691 788 8e9 948 885 8.5 15.1 5.9 5.1 4.4 4.1 8.1Overall Dficit 95) (810) (841) (422) (87 (7) ) (6W7) -8.9 -8.0 -2.9 -2.9 -0.4 -3.0 -2.SOfficial Capia l*u t (0) (0) 0 (o) 0 at? 419 -0.0 -0.0 0.0 -0.0 0.0 2.6 1.SExternal lwrrming (e) 878 428 220 269 22 200 24* 4.2 4.1 1.9 1.9 1.1 0.9 0.9

This document! s a rricted distribution and may be used by recipients only in the performanceof their offlicial duties Its contents may not otherwise be disclosed without World Bank authorization.

011f oCAA - I ALVA06

NOW. OEM me5 VW=9

(Will 2g. Cob....) 1900 1951 1153 115 1156 1no a 14 1 1155

gan C..oito. M a1*. .mw. ON 1.510 0.4101 1.80 8.749 S.073 2.744 3.27 $.01S13* Ornilt f Privett sect.r S,UJ 3.1.0 0.6 8.0 8.1* 4.05 4.41 5.40 41.4

O%nW _t beal _ U * oG U.1 S#. .0 W.* S 7. VA 0.3 8.4 UA U.9C__ Pricelod", (396143) 300.0 11.3 32. JI.3 1. 143.0 11.41 0.4 aw.l

_nnat _3?4S39 A lot 15Com,. P"ice toO. 14.1 U.M3 23. 11.llS 12.0 1." 9 4.6 13.0bS. Credit to Pobl Is twb 1.43 73 .10.6 9.3 UA.I -10.03 W.S 10.4Soak Credit 14 Prftivoto Sest 4.1 -14.1 to." 10.2 17.43 s.211 .4 21.1

6ALm1 OP PAWSfOlSti tttii 2. 1150 1051 1M1 19 £106 *19 1 1157 190 @

- -- (Av w 194(1) offn. Use (M)itert .t Go ado ,W $ 1.31 976 as 3" 64 9i2 we V _ - _

Nrde.di.w (PM5) 1.073 715 V 00 735 M to 7 U 1 n *ole 487.3 40.3obe-Psea Sbeviug 45 1in 16 in 11i of 51U so4 gm Cet 31.6 4.2

*no#, 21.0 2.3larte oa m_ta 1.170 1.1" 1.061 1.06 LU1 1 .11211 1.147 1.21 l Shr.mp 13.3 2.2

tiaradl (P5 8n an5 MS a" 14 on S" 994. SA Ifow" CAC1 * 3.1 16.3teFtor Service 213 s5 010 20 2 me 2o gm 156 l A 10e. 13.5

_mre ben.. 4 (7W (M) (1) (") c5 (13) (M61) (413) Total illB 74.4 100.0U" pit.r Inome (46) (74) OMS (U1S) tl10) (15) (18) 73 M)

Paeut Emipta W 40 sO # 6S As t9 as SFactor P _ANa 19 1S O 1i is 10 in 1 4 1 14 ITmWd. am7 (and Wried)

U l*t- to so) 0 J 44 61 74 is 74 so (5 Oa ilE im) 190 1son._, C.tr_ Tenar 40 a W Ws a1 31l ast No 403. -

#W. Feble . MPb. ar.. 24 1.670Curret Agw_t blame. i i13c) ( 14) (45) (BB) 110 14 sort Teta * Df 27 0

I_r_.a...toed privet. "0.1 161 soLo-Term Cpitael Wlor MS 2W7 st 41 Ws 31 7 9 (41) e -

Ciro" I.v.etina 6 (a) (1) 0 IS 12 0 O 0 Toutl a;tomdies A Olabureed 912 t,17Ot'fileisCapitalGramst 0 0 0 0 0 0 0 0 aNat LT L (9 an dat) so0 19" Z1 13 1an 7 i (U) 9 (61)OisbOsnt i# Mt 2as 40ti US 17 11 r am 11 t 01116M RATIOil_p.gAts titi 10 1n 2.8a 17 11 1t (prt) 1900 311

0*. LT iS1s ot ) 100 14 13 s4 13 U M so (0) 0JOLT P*IIg -*iP. on". 3.3 21.3

Totl Other Itm Q69) 3) sn() (n) (47 on CM) t(o c) ( S wt TeM ib & w O 0.0 0.0U" sort- er. _ ital so 34 0 mm is (13) (44) 0 * N14-*rnted Pri ve. Cb* 2.S 1.3Coieloloiw tN.0 0 0 0 9 9 0 0 0 ---S o.-. d _ imm (3,6) (10o (10 mm a) (1") (90 (on (a) Totel citatumil 45 Ol_aboro 8.6 24.2

COa_n_ I* W* _ tROrvea( ) 31 S1 M1 c) 7 (1) (43) (W) s0Nt_ Crdit from Dv 14 aS aS 17 (66) (1 (36) 0 0

OWOW RATIS 1M0 1titiS 1t1 1i 15 1119011 15s6 10 190 29 LeIti (WI.. use) 1INS 1967 1986

OffgiaI Rote:.o.t.t 0.0 68.0 0.0Calones r Wi (end pried) 2.80O 2.69t 2.300 2.300 2.800 2.800 8.000 8.000 8.000Colon. por N53 (Prted ave.) 2.800 2. 2.200 2.8 2.600 2.800 3.000 6.000 5.000 Gr. DOi bureeeet 3.4 S.4 13.4

Principal Resysn6t 7.9 0.6 11.18biun Rate: M% DOI.herae.t (4.8) (5.2) 2.3Coloe r W Si (and period) - - 3.000 .000 5.000 mntere O.re 10. 11.4 11.8CoEcoet per WUNI (wrid . .) _ _ _ _ _ _ . 5.000 .00 U" Trumfer (18.0) (16.6) (9.8)

1rk*et RateC Oubtsaatanding &Dirb. 140.1 U6i.5 15.4Colon" per ts (en perioe) - - - - - - 8.000 5.000 .006 Debt Oetln i * i. 180.0 25.2 213.7Coloes pr WIM (riod av.) -- - - - - 8.Ot .00 5.000

-- 1-___.

EL SALVADOR

COUNTRY DOUCC HMD3ANDW

TABL Of CONTaNTS

SUMMARY OF MAIN CONCLUSIONS ..................... ..... .. I

I. MACROECONOMlC sITU&TION AND PROSPECTS ................... 4 . .. 1

A. Background ................................................. 1B. Public Finsnces ............................................ 4C. The External Trade Regime and the Current Account .. 6D. Investment Performance and Prospects ....................... 10S. Employment and Wages ;............................ 13F. Summary of Policy Issues ................................... 14

II. GOVERNMENT FIANCES .......................... 17

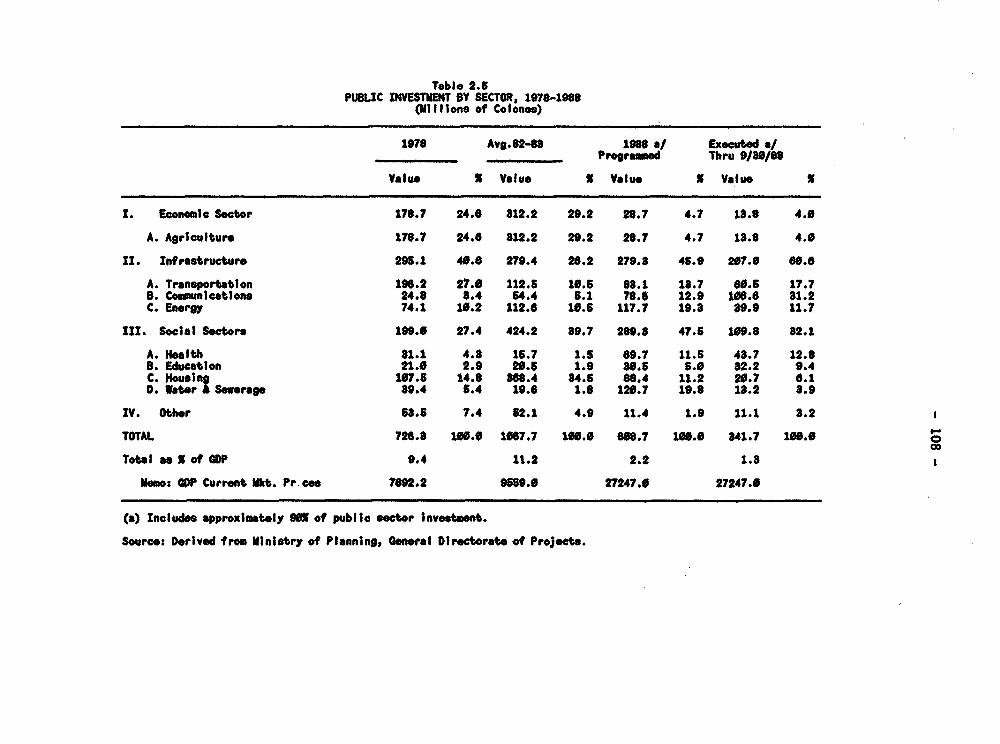

A. Overview ........................... .17D. Taxation ........................... 17C. Public Expenditures ...................... 21

(a) Economic and Functional Classifications ............... 21(b) Wages and Employment .................................. 21Cc) Public Investment ..................................... 23

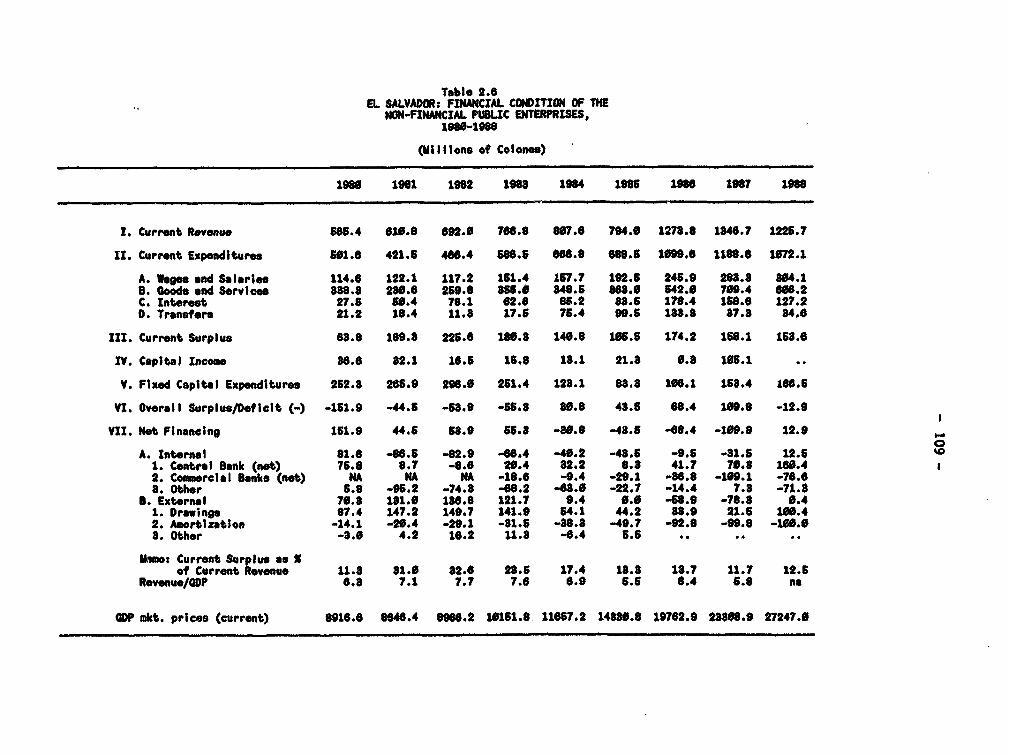

D. Public Enternrises ....................................... 24S. Deficit Financing ......................................... 25F. Fiscal Policy Management ................................... 27

III. TRADE POLICY AND PERFORMANCE ................................... 28

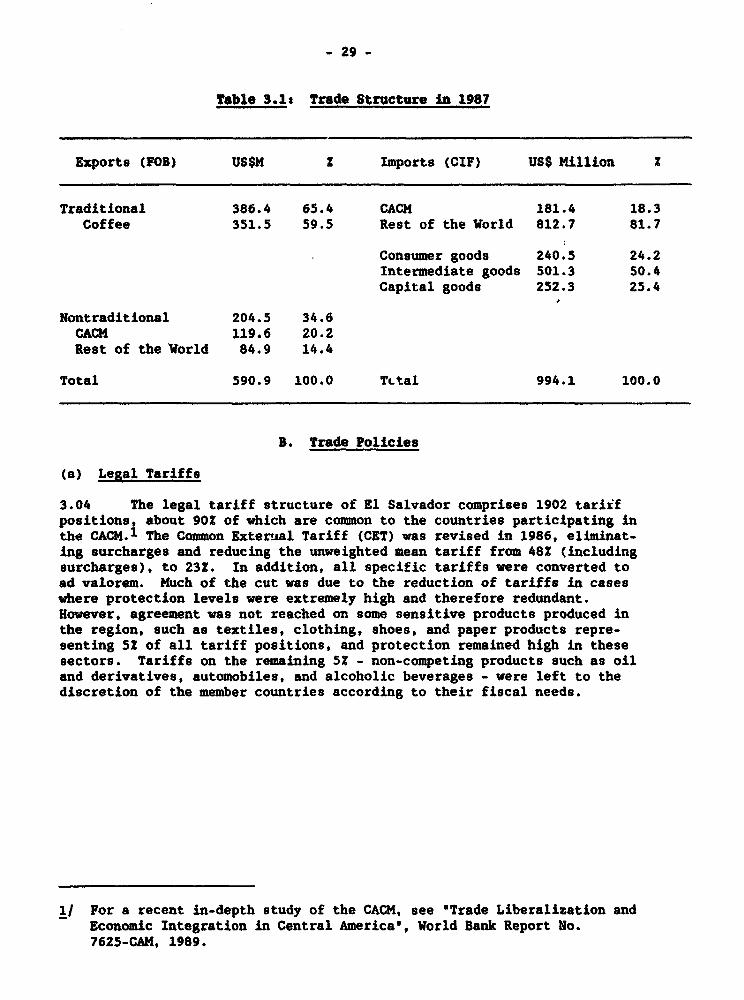

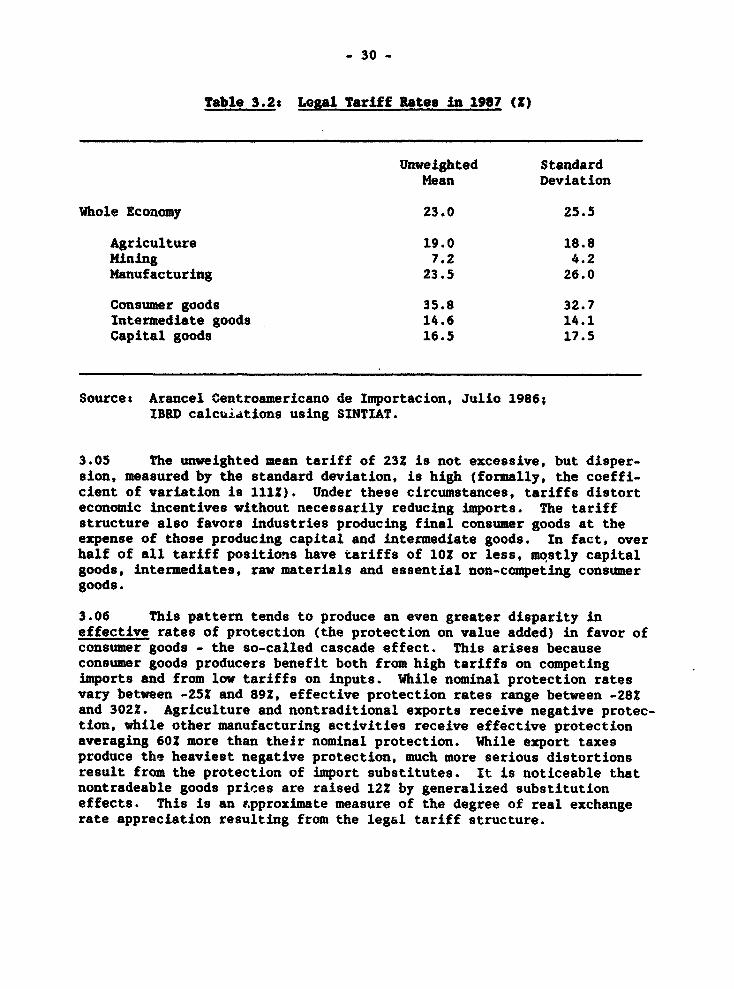

A. Background ............................................... 28B. Trade Policies .. 29

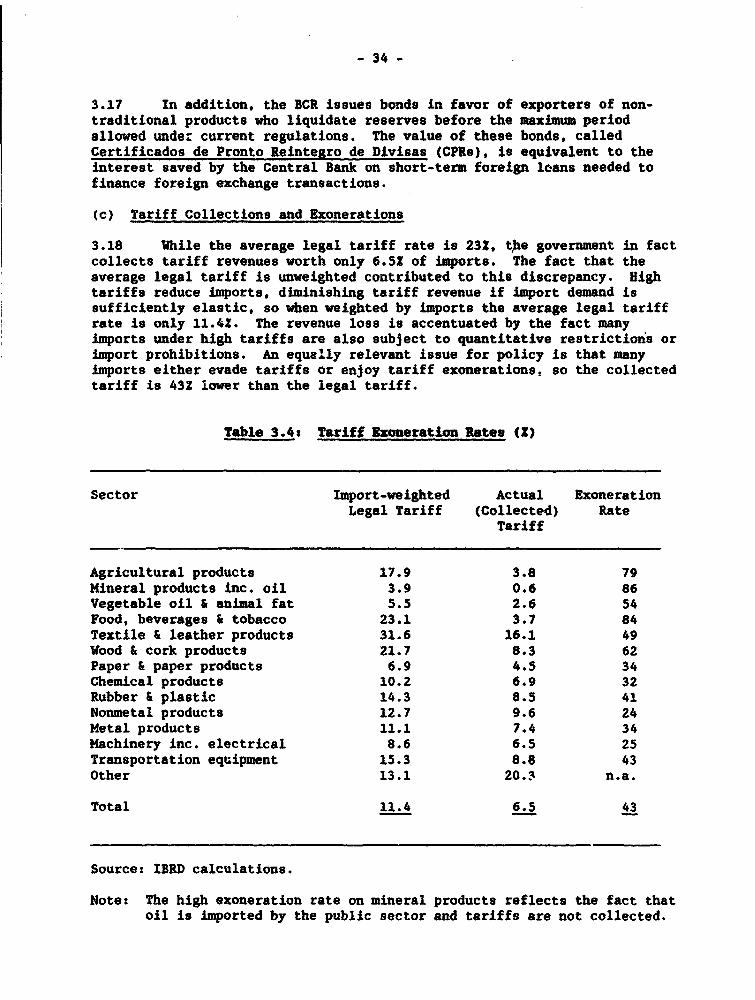

(a) Legal Tariffs .29(b) Non-Tariff Barriers .31(c) Tariff Collections and Exonerations .34

C. Reform Proposals .35

This report is based on the findings of a mission which visited El Salvadorin November/December 1988. The mission was led by Robert Laslett(macroeconomics), and consisted of Tarcisio Castaneda (health andpopulation), Joaquin Cottani (trade) and Baudouin Hubert (indastry) of theBank's staff, and consultants Arthur Mann (public finance). Alvaro Reyes(education and housing) and Eric Shearer (agriculture). Researchassistance was provided by Claudia Riccardi, and Maria Adela Shearercontributed with work on NGOs. The assistance of Felix Jakob (housing) isacknowledged. Merle de Silva wordprocessed the report.

-2-

IV. AGRICULTURE ........ ....... . ...... ......... . , 40

A. Production, Trade and Prices .. * . , ...... 40

(a) Overv'iew.... ................... ...... ... 40(b) Food and Feed Ptoducts * . . . ... 42(c) Coffee .............................. 43(d) Other Products .. . .... ... ... . . ... ........ 45

B. Institutional Issues .... .... ........ * 46

(a) Price and Commodity Policies ..... 46(b) The Agrarian Reform . . ............ 47(c) Agricultural Credit .... 49(d) Irrigation. ............... ...... 49(e) Environment ............ . ........... 50

C. Policy Recommendations. . . ........... .50

V. MANUFACTURING .. ......... ..... .... 52

A. Overview ... 52B. Trade Regi.......... * .. . ........... 54C. Investment Financing . ...... 57D. Price Controls . . . .............................. 59E. Conclusions and Recomendations . .. 59

VI. SOCIAL SECTORS .................. 62

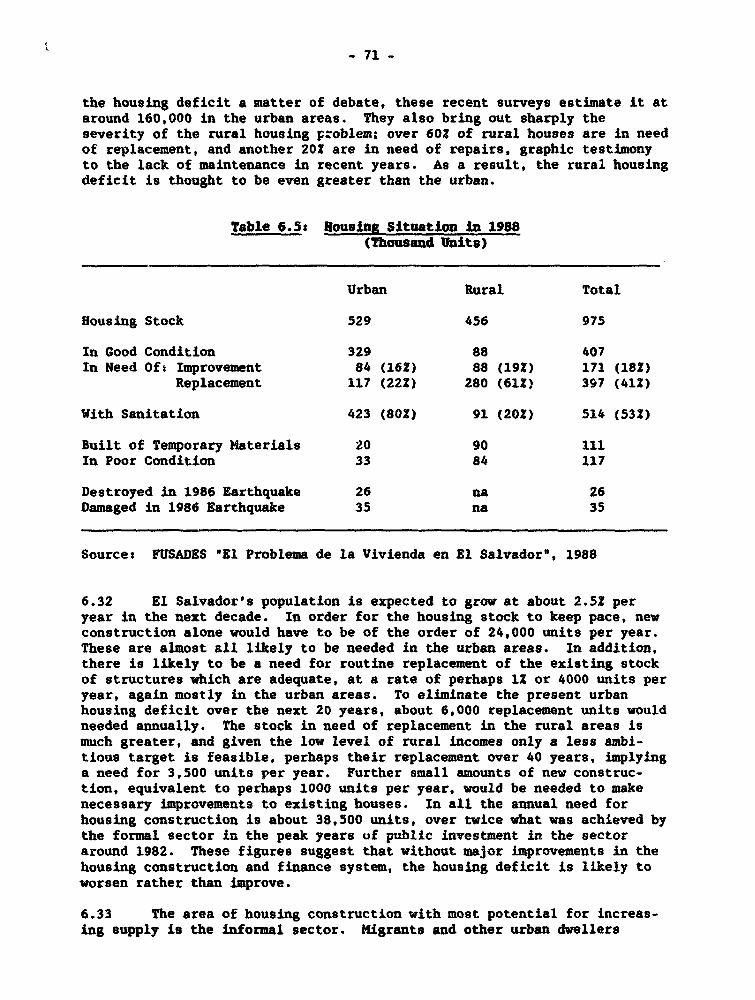

A. Overviw ........ 62B. Populationpn.. .... ......... 63C. Health Services ....... 64D. Education . ... ................. . 67E. Housing. .......................... 69

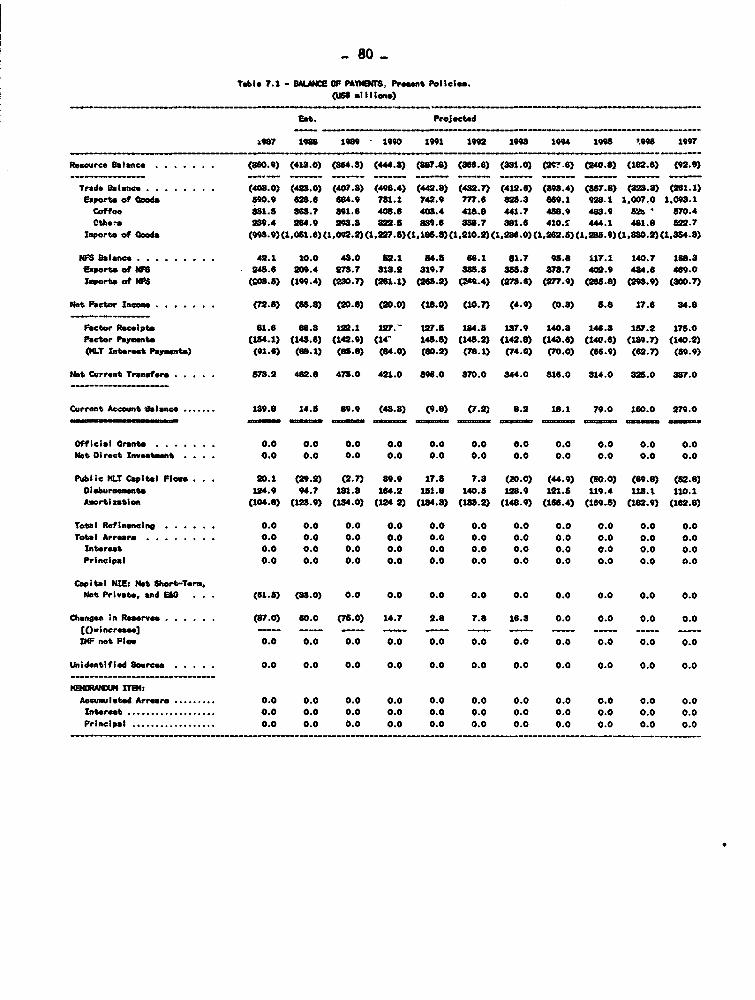

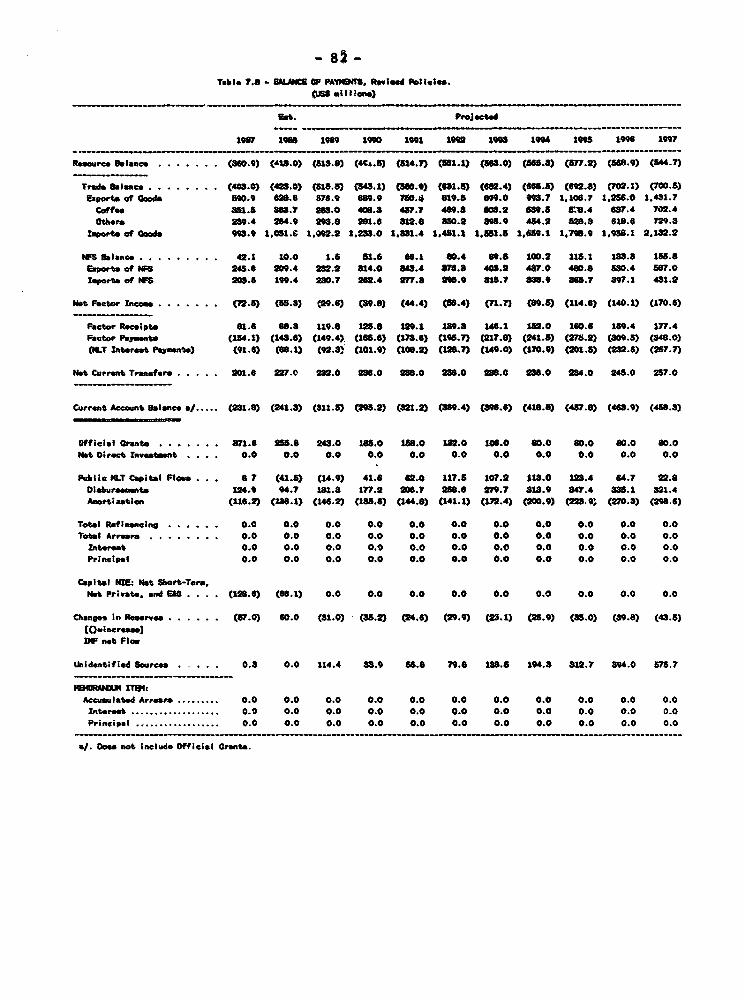

VII. ECONOMIC PROJECTIONS ... 73

A. Introduction ............................................... 73B. Prospects with Present Policies . .74

(a) Assumptions .74(b) Outcome .75

C. Prospects with Economic Policy Changes . . 76

(a) Assumptions . . . . ....................................... 76(b) Outcome . . . . . .................. 77

D. Conclusions ....................... 78

Annex I ................................. ... ......................... 84Annex II........ 86Statistical Appendix ..... .... 91

SUMMARY OF MAID CONCLUSIONS

1. Macroeconomic Situation and Prospects

i. El Salvador's civil war imposes heavy costs which impede economicdevelopment. About 70,000 I4ves have been lost, and it still continues tocause major economic, social and human damage. The proportion of thebudget devoted to national security (272 in 1987) is by far the highest inLatin America, and about 750,000 people have emigrated in the last decade,while another 500,000 are refugees within the country. Coupled wit) analready high population density, El Salvador also has a high rate ofnatural population growth, which combined with internal migration isplacing a heavy strain on the public provision of infrastructure and basicsocial services.

ii. Per capita incomes have stabilized at a low level. GDP fell by222 between 1978 and 1982. Adverse movements in the terms of trade andregional trading problems contributed by cutting exports, but most of thefall came as domestic political turmoil depressed private consumption andinvestment expenditure. The decline was halted in 1983, and since theneconotic growth has averaged only 1.72 a year. Despite war casualties andemigration the population has grown at around 1.4? per year, so real percapita GDP has stabilized at a level similar to that of the early 1960s andremains about 20a below peak.

iii. Emigration, war casualties and military recruitment have allslowed the growth of the labor force. The growth of the workWng agepopulation slowed from 14.8Z in 1970-75 to only 5.12 in 1979-85. The laborsupply declined even faster, since emigrants and military recruits camefrom the age groups with the highest labor force participation. The primeage (20-44) civilian male population was still below its 1978 level in1988. The stock of human capital fell yet more since emigrants had moreeducation than the population as a whole, and school enrollment ratiosdeclined steeply. Recent years have seen an improvement in labor supply,with the growth of the working age population returning to Z.32 a year by1987, and school enrollment recovering to pre-crisis levels.

iv. El Salvador depends heavily on external assistance to meet itsfiscal and trade deficits. In the early 1980s, the public finances cameunder strain as revenue declined with the fall in GDP, and securityexpenditures and public investments grew. The deficit has declined verysubstantially in recent years, mainly at the expense of public investment.There was also some increase in public savings as current expendituresdeclined, mainly in the social sectors, but the tax effort contributednothing to closing the fiscal deficit, and revenues remain at a low level.The development component of public expenditure was thus sacrificed to meetthe urgent need to control the deficit.

v. The deficit is larger than is shown in the budget. Many publicexpenditures are made outside the budget and supported by externalborrowing and grants. In addition, large unacknowledged losses in thenationalized banking system and in public sector lending to agriculture arecontingent liabilities of the public sector. The public sector itself hasreceived sizeable subsidies from the banking system by borrowing at low

- U -

controlled interest rates. Finally the public sector has a large floatingdebt, partly in the form of overdue interest payments.

vi. Improvements in the public finances are necessary for manyreasons. Investment, maintenance and recurrent social expenditures have tob,: .reased to lay the foundations for growth without inflationarydor ;tic financing. Public sector wages need to be selectively increased,as a means of improving efficiency. The public sector must put itself in aposition to cover its outlays from its own resources without r-alying onmajor transfers from abroad. Provision must be made to meet theaccumulated losses of the financial system, to allow it to finance moreproductive investment. And most importantly of all, the public sectorneeds the flexibility to increase public savings in support ofstabilization and adjustment objectives.

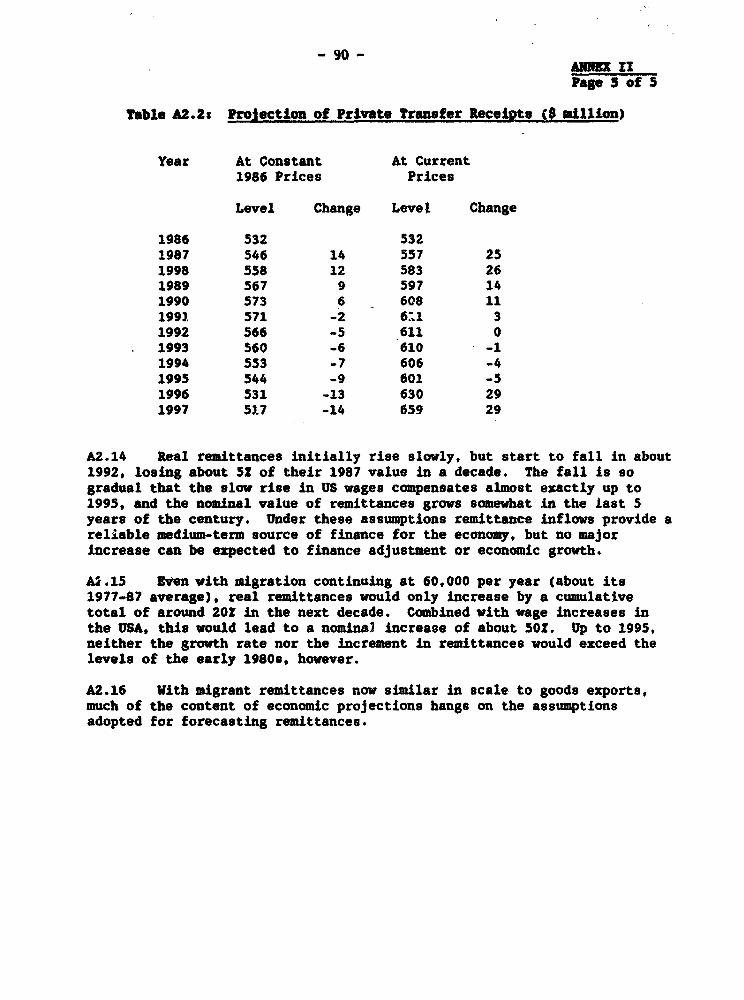

vii. The economy also suffers from major distortions. Particularlyimportant is the appreciation of the real exchange rate as a result ofassistance, remittances, and the trade regime. The resulting incentivespenalize agriculture and manufacturing, cutting their capacity to generateforeign exchange, the so-called "Dutch disease' effect. There is a dangerthat the exceptional levels of foreign exchange inflows responsible for theappreciation will disappear: official tr. -fers are likely to fall in themedium term, and recent surveys and projections of migration suggest thatremittances w4 11 stagnate. Thus the foreign exchange needed for economicgrowth will have to come from the production of tradeable goods.

viii. The current policy of stimulating investment by keeping creditcheap and allocating it preferentially to agriculture and manufacturing isboth distorting and ineffective. Bank credit is available to theproductive sectors at interest rates which are negative in real terms andis rationed by administrative allocations. This worsens the allocation ofinvestment resources and leads to excessive self-financing by someenterprises. It is difficult to identify any effect on investment orgrowth of the favored sectors. Non-bank credit markets seem to be thin ornonexistent and many firms are financing investment out of retainedearnings, which tends to constrain overall economic growth. In addition,the artificially low cost of capital to those able to get credit tends toencourage more capital-intensive techniques of production than the realscarcity of funds would justify, reducing the demand for labor.

2. Public Finances

ix. The tax system has contributed little to solving E1 Salvador'sfiscal problems. Several measures are needed to increase revenues andeliminate unnecessary distortions. The stamp tax needs to be reformed toreduce distortions, increase uniformity and eliminate exemptions. Ideallyit should be replaced by a tax such as a VAT, which would allow drawbacksfor exports and cross-checks on other taxes to tighten up auditing andcollection. Even incorporating all firms into the VAT network a uniformtax rate of 15-162 will be required to yield the same revenue as the 5Xstamp tax. To avoid an ercessively high VAT rate exemptions should be keptto a minimum.

- iii -

x. Another necessary change Is to simplify the design of directtaxes. There are 25 different personal income tax brackets with marginalrates from 7.41 up to 60S. There is no indexation and tax brsckets havefallen considerably in real terms. It would simplify administration todrastically reduce the number of brackets and improve incentives to set themarginal rates in a narrower range (perhaps 10 to 501). The businessincome tax has five tax brackets, with rates ranging from 151 to 351, whichshould be simplified to a single rate in orier to promote economies ofscale both in tax administration and in production.

xi. Tax evasion is at least 402 of the tax collected, and the areasmost prone to evasion are direct taxes and import duties. Income taxsimplification combined with the use of the central taxpayer file, cross-checking with other external data, and more external audits is needed toincrease collections. Almost all direct tax audits are desk studies andmore, less complete, field audits should be made on a larger number oftaxpayers. The tax collection system is ir.efficient, with only 251 of taxcollections withheld at source. Independent professionals are not subjectto withholding or estimated tax payments. Delays in receiving some taxesare also excessive, and the sanctions for proven tax fraud are ineffectire.

xii. Only modest changes should be made to the coffee export tax in theshort run, to avoid loss of revenue. Though it contributes to anti-exportbias, the tax is fiscally vital, having averaged over 201 of centralgovernment revenues during the 19809. Moreover, the tax is easier toenforce than corporate income taxes, from which producers are exempt.However there are some deficiencies in the design of the tax. The fixedcoSt of coffee production is above the tax-free allowance of $45, so thetax falls as a share of profits as the price rises. To make the tax moreprogressive and equitable, it is important to raise the allowance, whichhbS been constant since 1950. If this were to take place at the same timeas a devaluation, it would not necessarily involve a loss of public sectorrevenue.

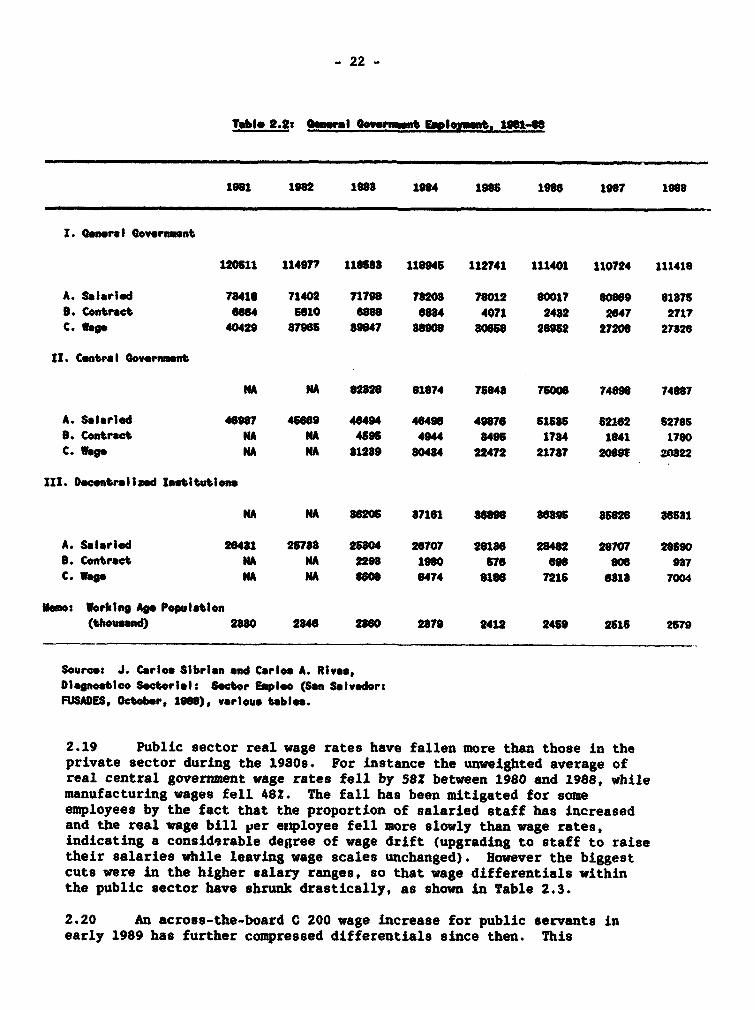

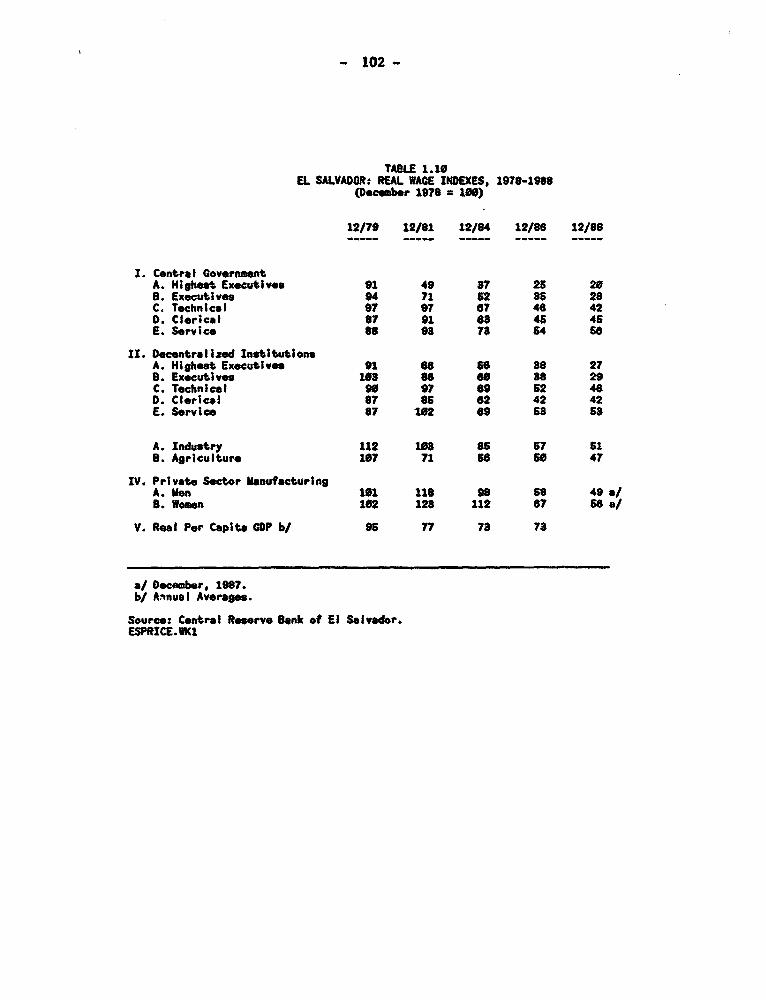

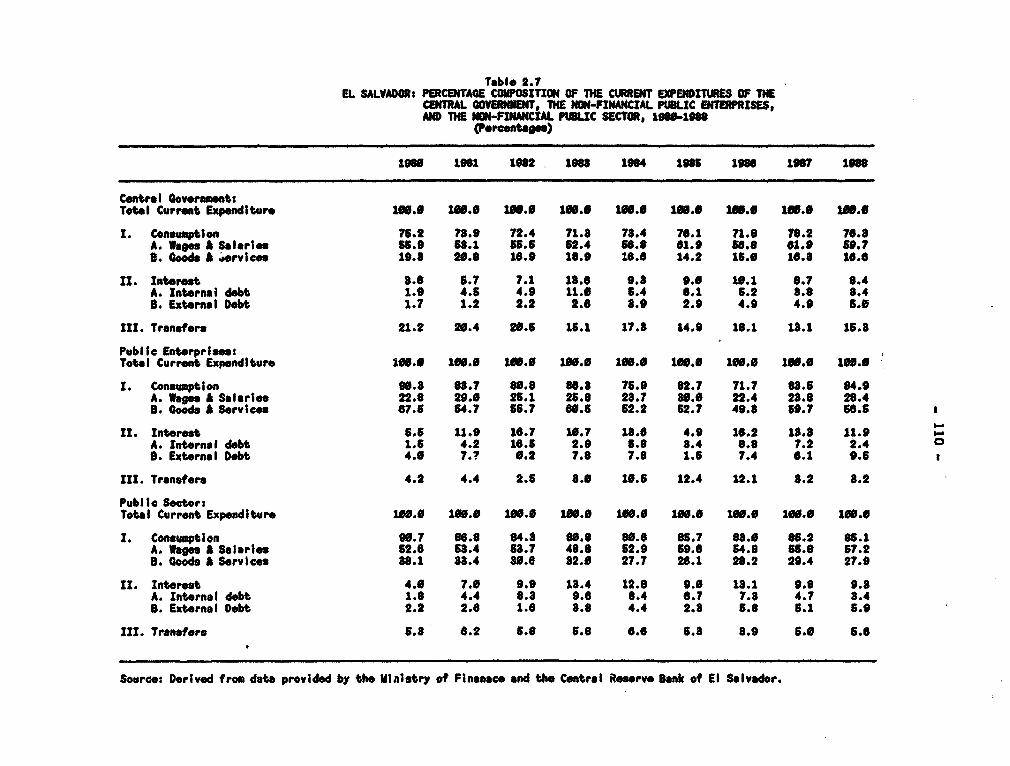

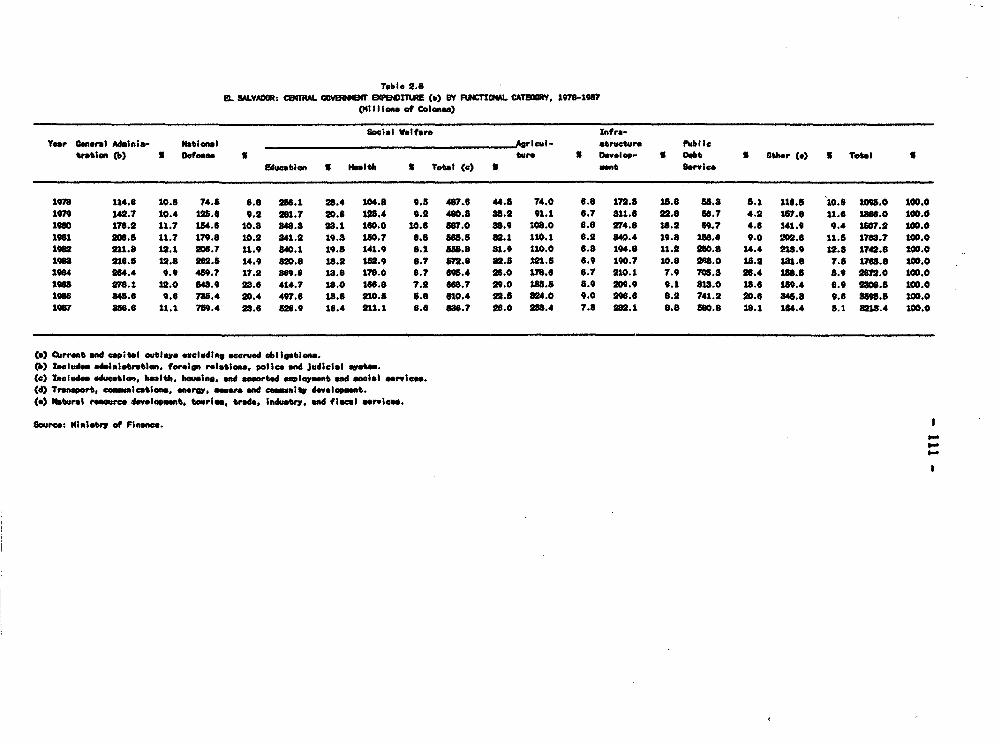

xiii. Defense and interest spending have crowded out public social andeconomic spending. In 1978-79 they took 132 of total expenditures and by1986-87 this had reached 41?. Over the same period spending on socialprograms fell from 401 to 24?, and real per capita social welfare outlaysfell by over 40X. The economic contribution of public spending has beengreatly reduced and needs to be restored. Total general governmentemployment fell from 5.2Z to 4.3Z of the working age population, thoughthere may have been some growth in public enterprise employment.

xiv. Public secto; real wage rate- have fallen more than those in theprivate sector. The fall has been mitigated for some employees by wagedrift (upgrading staff to raise their salaries while leaving wage scalesunchanged). As the biggest cuts were in the higher salary ranges, wagedifferentials within the public sector have shrunk drastically. Thiscombination of wage ratio compression and falling real wages hasundoubtedly affected the ability of the public sector to retain qualifiedpersonnel, posing a major threat to efficiency. Decompression is needed toimprove the provision of public services and assist adjustment efforts.

^ iv-

xv. Public investment in 1984-87 averaged 3.6Z of GDP. While privateinvestment is rising and is consistent with an economic growth rate of 1-22p.a., public investment continued to decline into 1987 anA 1988, and is nowless than is needed to maintain and replace existing assets. Publicinvestment will have to increase, both to complement private investment andto rebuild deteriorated infrastructure.

xvi Public investment is also badly managed and major cht"tges areneeded in the way it is planned and carried out. One source of problems isthe lack of flexibility in investment financed from external sources.Management problems such as poor programming of funds and materialsresulted in substantial under-achievement of public investment targets in1988. The ability of the public sector to manage investment projects islimited partly because of the lack of appropriately qualified personnel.Atiother problem, resulting from the war, is that much of public investmenthas te be directed toward short-term repair and rehabilitation projectsthat do ot add to the capital stock.

xvii. too much government control has led to erosion of publicenterprises prices and investment. Their operating surplus in 1984-87 wasa result of cuts in capital spending rather than improved operatingperformance. This will increase the future financing needs of theenterprises and cut the quality of future services. The real revenues ofthe public enterprises have declined, largely in consequence of consciousgovernment decisions to permit their tariff rates to lag behind the rate ofinflation. Public enterprises should be given more managerial autonomy,within an overall financing and regulatory framework given by government.

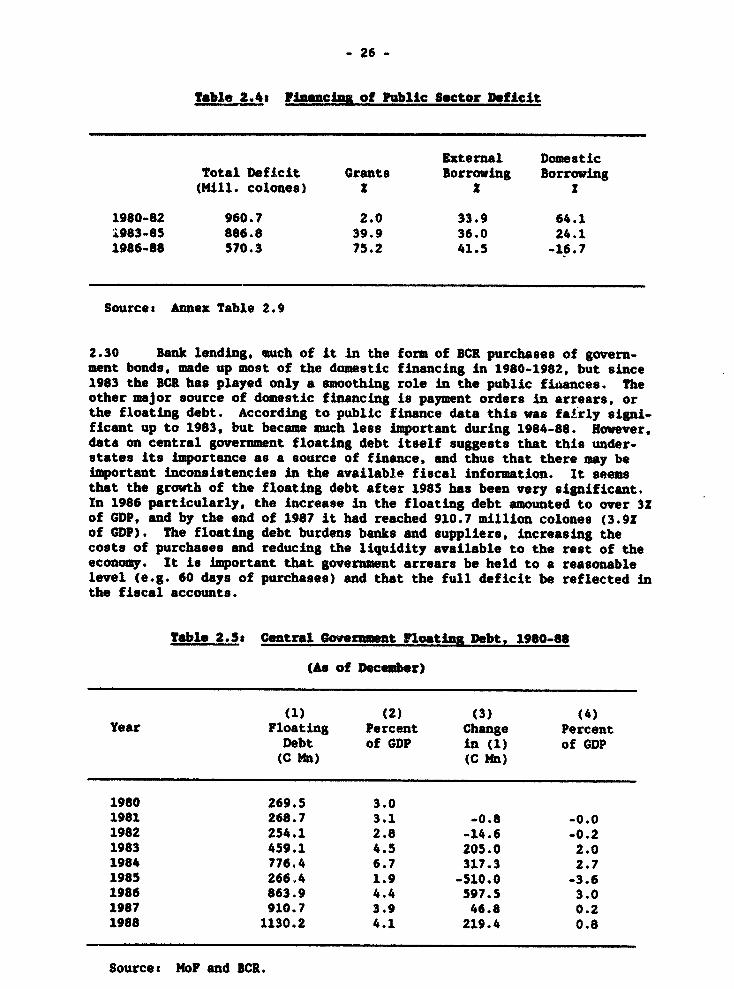

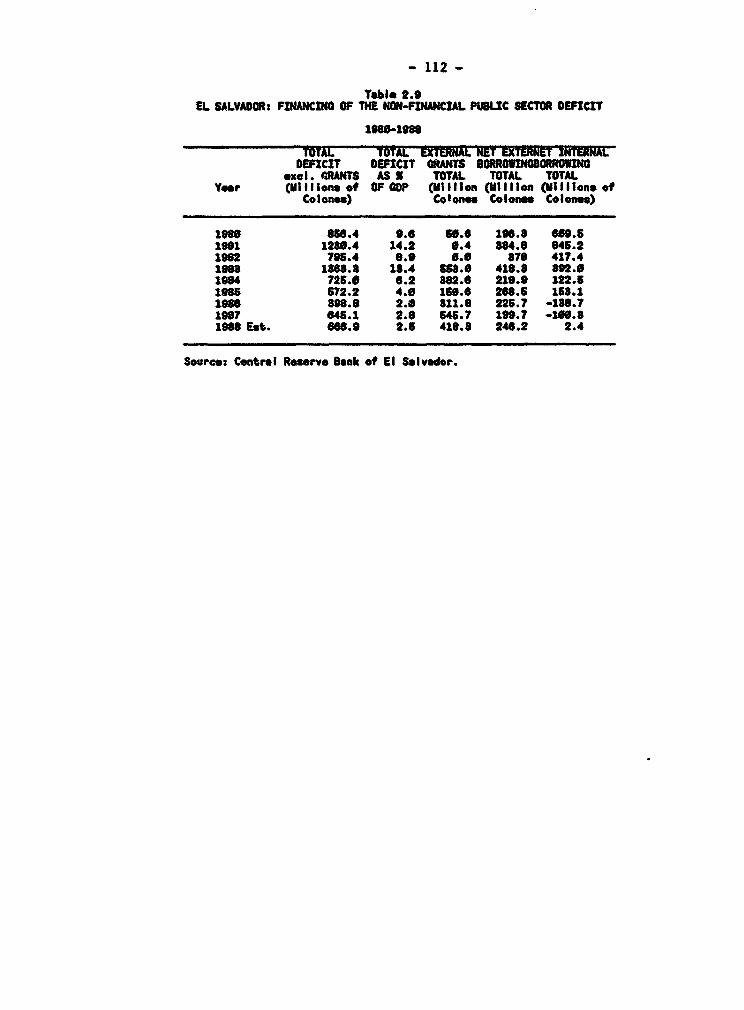

xviii. The public sector deficit has mainly been financed through grantsand external borrowing. Sir:a 1983 external grants have contributed anaverage of 58f of total deficit financing. In contrast recorded domesticborrowing has practically disappeared since 1986. External borrowing hasfunded around one-third of the deficit throughout the decade. Despite thelargely concessional terms of these loans, external debt servicing is anincreasing burden, and it would be unsound in the long term for the publicsector to increase external borrowing unless more growth-oriented policiesare adopted.

xix. There has been major unrecorded domestic financing through paymentorders in arrears, or the floating debt. In 1986 particularly, theincrease in the floating debt amounted to over 32 of GDP. The floatingdebt burdens banks and suppliers, increasing the costs of purchases andreducing the liquidity available to the rest of the economy. It isimportant that government arrears be held to a reasonable level (e.g. 60days of purchases) and that the full deficit be reflected in the fiscalaccounts.

XX. The lack of fiscal policy coordination has negatively affected theuse of fiscal policy for stabilization purposes. The BCI prepares themonetary program, MIPLAN the investment budget, and the MoF the centralgovernment budget, with little reconciliation between these threeexercises. The three bodies should better coordinate their activities toproduce a singie set of numbers on which to base fiscal policy.

3. Trade Policy

xxi. The main aim of trade policy should be to encourage export growthand diversification by tariff reform and real depxf:ciation. There are twomain domestic policy constraints on exports. Firstly, as a result of pastregional import substitution efforts, the structure of production is ill-adapted for exports outside the Central American region. Secondly, thereal appreciation of the currency has reduced the incentives for bothexports and import substitutior.. Reforms in'the system of protection wouldboth necessitate and tend to produce a real depreciation in the value ofthe currency.

xxii. There is a wide dispersion of nominal rates of protection, whichproduces an even greater disparity in effective rates of protection (the.protection on value addei) in favor of consumer goods - the so-calledcascade effect. This arisas because consumer goods producers benefit bothfrom high tariffs on competing imports and from low tariffs on inputs.Agriculture and non-traditional exports on the other hand recelve negativeprotection. While export taxes produce negative-protection, much moreserious price distortions result from the protection of import substitutes.

xxiii. Until February, 1989 this pattern was worsened by the selectiveconsumption tax, which raised the effective protection on consumer goodsstill further relative to intermediate and capital goods and increased thedegree of negative protection on agriculture and non-traditional exports.Exchange controls and other NTBs are of great potential importance in tradeprotection. The authorities could for instance limit the number of importapplications. The Salvadorean authorities should avoid using suchquantitative restrictions on imports to keep the official mazket inbalance. As the gap between official and parallel market rates increases,this would worsen the distortions in the trade system, furthor underminingexport prospects. The authorities should also refrain from using otherITBs such as prior deposits and prohibitions.

xxiv. Tariff exonerations are not achieving their intended effect, andcause a great loss of revenue. Though most exonerations are supposed toapply to intermediate and capital goods, the highest exoneration rates areon consumer goods. Potential duty revenue in 1987 was US$E8 Mn., of whichthe govetnment actually collected US$51.7 Mn. El Salvador should abolishtariff exonerations except those on fuel and on inputs used to produceexport manufactures. This would make the system easier to understand andwould to some extent offset the increase in import demand that would resultfrom eliminating NTBs. There would be a net gain in tariff revenue.

xxv. The distortions arising from the tariff structure itself need tobe reduced if not eliminated. A first step to reduce both the level andthe variance of tariffs would be to set a ceiling on rates, e.g., 402 andto cut tariffs to this level over a 2-3 year period. This would parallelpolicy changes already underway in Costa Rica and Guatemala, and would thustend to harmonize trade policies within the region. The current temporarysuspension of the CET affords an ideal opportunity for E1 Salvador to do

vi -

this. Effective protection for domestic producers would remainconsiderable, but anti-export bias would be reduced and the dispersionamong rates of protection would fall. The proposal to move to a 5-502tariff range is a first move in this direction.

xxvi. A more ambitious step would be to set all trade taxes at a lowuniform rate. This would produce more-or-less uniform effective protectiongreatly reducing dispersion and giving similar incentives for allcategories of production. A small bias against exports would remain, buttheir relative competitiveness would be much improved. It might make senseto eliminate export taxes altogether, replacing them with profits taxationand auctions of quota rights uuder the ICO and in the US sugar market. -

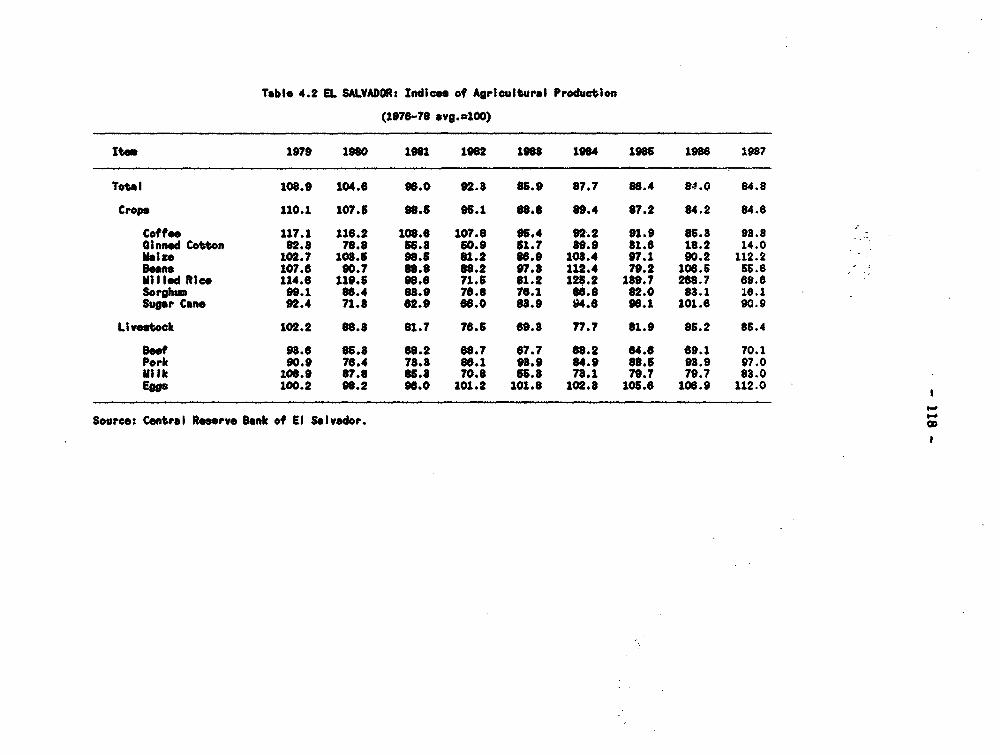

4. Agriculture

xxvii. The agricultural sector shared in the general fall in economicactivity, and in recent years has done worse than the rest of the economy.It is of fundamental importance in terms of exports, income generation,employment and fiscal revenues. Price controls and interest subsidies havecaused high fiscal and efficiency costs, and cannot be sustained in theirpresent form. Many farms cannot service their debts to the banking system,and agricultural prices, after a respite in 1986, have continued to fall inreal terms. The sector thus poses a major policy challenge. Substantialrelief can be expected from improved macroeconomic policies, in particulara real devaluation, but a careful overhaul of government policies andinstitutions is also needed.

xxviii. Falling world prices and real appreciation have hurt the sector(which is the most export-oriented). The real average world price ofagricultural commodities fell by over 40Z betveen 1978 and 1987, and thisin combination with E1 Salvador's real currency appreciation produced a 50Zfall in the real prices received by producers. All types of agriculturalproducts have been severely affected, though domestic market prices fellless than those of export crops.

xxix. Land pressure and overuse are intense. With about 350 people persquare kilometer of cultivable iand the country is the most densely settledin Latin America. Large areas of vulnerable land are being cultivated, andconsequently soil erosion is severe. In addition mangrove forests havebeen decimated by developers and cotton planters, destroying the breedingareas of shrimp and other marine life. Other environmental problemsinclude soil contamination by long-term excessive application ofinsecticides to cotton.

xxx. Agricultural imports have increased, and exports have fallen. ElSalvador's comparative advantage, though obscured by distortions, seems tolie in coffee, fishery products, fruit and vegetables and some basicgrains. TheBe areas will all be benefitted by freeing up prices and tradein the sector, and by Amproved macroeconomic policy signals, cruciallyreal devaluation. At the same time, several subsectors where product ishigh-cost and Inefficient - such as sugar or livestock - will likely

- vii -

decline. Indeed, the overall price level received by farmers could doclinein real terms if trade liberalization proceeds too rapidly. To avoidunnecessary disruption, the reduction of tariff protection for import-substitutes should be spread out over several years.

xxxi. There is a good deal of price intervention. During the pastdecade there have been major increases in state trading, subsidies, pricecontrols and quantitative trade restrictions. There are import targets forstaple foods that compete with domestic produce. The Ministry of Economysets price ceilings, import and export targets and trading margins forseveral consumer goods. INCAFE and INAZUCAR monopolize trade in theirrespective products. The intervention of these diverse agenc0es weakensthe planning and coordinating role of the MAG itself.

xxxii. The agrarian reform of the early 1980s has been difficult andcostly, and the most important economic issue is now how to improve theproductivity of the reformed lands. Cooperatives are heavily indebted, butat interest rates lower than agricultural price inflation, so the debt isfalling in real terms. The fact that they cannot service these debts is anindicator of severe management problems. Rather than continued publicsector subsidies they need training, management reforms to introducetangible property rights for members, better financial arrangements forbasic social services now being charged to overhead, and restructuring ofcredit arrears. Individual proprietor beneficiaries also need strongertechnical and financial support, perhaps through non-governmentalinstitutions.

5. Manufacturing

xxxiii. Industrial production is heavily concentrated in consumer goodswhich are not competitive in world markets. As demand fell, manufacturingoutput fell even more than the rest of the economy. Domestic demand wasresponsible for the bulk of the fall, and a decline in exports ofmanufactures in the early 1980s also contributed. In 1987 output was still212 below its real 1978 level. Unlike agriculture, the poor performance ofmanufacturing is wholly attributable to domestic incentive problems.Industrial sector prices have more-or-less kept pace with those in theeconomy as a whole, resulting in an increasing degree of implicitprotection. Import liberalizatioi and a more competitive financial systemare needed for the sector to develop new markets and grow.

xxxiv. The major influence on incentives is the trade regime. Adopted inthe context of regional integration in the 1960s, import substitutionindustrialization policies have been continued in the 1980s despite theerection of trade barriers within the CACM. The small scale of theremaining protected (domestic) market has accentuated the well-knownpr,blems of these policies. It affords few profitable opportunities forgrowth.

,1

- viii -

xxxv. The 1986 export incentives l"w attempts to counter anti-exportbias. However incentives remain strongly biased in favor of importsubstitution. '- some of the same tax exemptions were given in the pastfor sectoral ( ilopment purposes, the net effect in many case' is toreduce taxation on the sector, rather than change the structu, ofincentives in favor of exports.

xxxvi. Policies to encourage sustainable manufacturing growth thereforeneed to start with trade policy changes in several major areas, includingreal devaluation and trade liberalization. Key policy changes are loweringimport barriers and making rates of protection more uniform amongactivities, by eliminating non-tariff barriers and redt-cing the dispersionof tariff rates. Real depreciation of the currency is also needed toincrease the incentive to produce tradeable goods, both exports, andefficient import suLstitutes.

xxxvii. Faced with the stagnation of the manufacturing sector, thegovernment tried to stimulate output by means ot credit subsidies.Manufacturing has been greatly favored in the allocation of bank lending.Though investment has increased, this policy has not provided a viablebasis for manufacturing to make a sustainable contribution to growth. Ithas also imposed heavy costs on the banking system.

xxxviii. E1 Salvador needs to reduce the entry barriers to the formalsector caused by discretional tax incentives, price controls, sectoraldevelopment laws and credit allocations. A particularly important areawill be the provision of finance, as the demand for new investmentfinancing is likely to increase at the same time as pressure on the bankingsystem from overborrowed incumbent firms. The reform of incentives willboth have to be accompanied by measures to make the allocation of creditmore responsive to market forces, and by measures to strengthen the equitybase of the banking system, particularly moving to interest rates whichmore accurately reflect the cost of capital and injecting new equitycapital into the banking system.

6. Social Sectors

xxxix. One of the most impressive and positive fetetures of El Salvador'sdevelopment record during the last decade has been the general maintenanceor improvement of basic social indicators. Ir.fant mortality fell, theprevalence of communicable diseases has declined, and life expectancy rose.Food availability increased, and malnutrition declined. Despite theseachievements, El Salvador still has some of the gravest social problems inthe region. The rate of infant mortalit7 remains one of the highest inLatin America, income distribution is radically unequal and resources forpublic social services are scarce, reflecting pub'ic finance problems.Some but not all of the resource shortfall has been met by the increasedefforts of NGOs.

. ix -

xl. Rapid natural population growth is one of El Salvador's mostfundamental problems. It has declined recently to 2.7? per annum but isstill among the highest in Latin America. Emigration has slowed the growthof the resident population substantially more, to only about 1.4S from 1978to 1988, but as emigration slows population growth can be expected toaccelerate. Efforts are needed to improve the availability of familyplanning services, pArticularly in the rural areas.

xli. Public health spending has been severely squeezed, and needs to betargeted on the neediest. Efficiency would be improved by emphasizingprimary health care, where coverage is inadequate. The main causes ofdeath are diarrhea and respiratory diseases, and combating them is mainly amatter of improved sanitation and primary health care. Primary carecoverage of the most vulnerable groups however is deficients the MoH issupposed to attend 852 of the population, yet its child care and nutritionmonitoring programs cover only 20-402 of children, and 352 of pregnantwomen. Middle-income groups should be encouraged to use private facilitiesand heath insurance. This would also encourage the development ofadditional private sector infrastructure.

xlii. Primary and hospital care need to be better integrated to improvereferral, diagnosis and early treatment and cut costs. Administrativeexpenditures could be cut since operating units have been decentralized andhospitals operate autonomously. Staffing patterns should be changed toincrease the number of auxiliary and paramedical personnel in relation tothe number of doctors from the current ratio of 2sl to about 4sl or 5:1.The MoH should also be given the incentive to cut personnel costs byallowing it to retain the budget for vacancies eliminated. These changeswould help restore the share of basic goods and services in the MoH budget.

xliii. Primary educational enrollment ratios declined disastrously withthe onset of the civil war, from 79X in 1979 to a nadir of 612 in 1981.Since 1983 they have risen, and the enrollment ratio had reached over 802by 1986. A conspicuous feature of the recent increase has been the rapidgrowth of private schooling, which expanded at an annual rate of 17.42,over six times the rate of growth of public school enrollments. By 1987,private schools accounted for 12.22 of primary pupils, up from 7.6t in1983.

xliv. This increase reflects quality problems in the public schoolsystem and is evidence of a strong demand for education. Firstly, thepublic scbool system suffers from capacity problems because it has beenstarved of investment funds, and suffered major losses of facilities in the1986 earthquake. Secondly, there has been a steady fall in teachers' realsalaries and teachers work only part time. Though pupil-teacher ratioshave been maintained, teacher motivation is poor. Lastly, there has beeninadequate expenditure on books and other educational equipment.

xlv. The public sector should concentrate its scarce educationalresources on the neediest groups, particularly women and rural pupils. Thestrong effective demand for education at all levels, and people'swillingness to pay for it, gives the public sector the opportunity to do

this. Improved vocational and technical training would lay the basis forraising the productivity and wages of the poor in the long run. Theprivate sector would continue to expand to satisfy the demand of othersegments of the population.

xlvi. The housing situation presents persistent serious problems,aggravated by war and earthquake losses. Internal migration adds tohousing demand in the urban areas. Private investment in housing hasincreased almost continuously, both in real terms and in relation to GDP,since the mid-1970s. Public spending on housing has fallen back steeply,and showed no sign of a recovery in 1988 despite the reconstructionactivity after the earthquake. The fall has been sharp enough to reducetotal housing investment.

xlvii. There is a mismatch between houaing supply and demand, which iscausing serious problems in formal sector housing finance. Many unitsremain unsold, despite an overall housing deficit. The problem lies partlyin the rise in nominal interest rates, which has led to heavy front-endloading of loan payments, and the fall in real incomes which has madeformal housing hard to afford. Changes are needed in the credit policiesof the publicly-owned financial institutions, and the coordination betweenconstruction and mortgage financing.

xliii. The area of housing construction with most potential is theinformal sector. Migrants and other urban dwellers unable to afford even aminimal finished house try to obtain a building plot, and construct andupgrade their dwellings in line with their income and needs. This process,almost universal in developing countries, has received little help from thepublic sector in El Salvador though it has been assisted through someforeign aid programs. Obstacles include difficulties in obtaining legaltitle to building plots, and lack of credit.

xlix. The result is a major housing deficit. Measures are needed toassist the informal sector and redirect public subsidies away from highincome housing. Injections of public funds under existing institutionalarrangements are unlikely to produce results. More consistent andcomprehensive planning for the sector are needed to identify demand, andlay the basis for meeting the needs of all sectors. The problems of theurban land market merit special study and policy attention, to meet theneeds of low income families. The aim would be to facilitate thedevelopment of sites and services projects, construction materials creditsand other initiatives which have proven useful in other developingcountries, but which have yet to take root in El Salvador.

7. Projections

1. El Salvador's economic performance is projected with and withoutmacroeconomic policy changes. Without policy changes, GDP growth will beconstrained by lack of access to imports. The economy would be unable togrow as fast as population, so per capita GDP would fall continuously.

- xi -

From 1991 onwards, real GDP would start to contract. The main purpose ofthe scenario is to show just how unsustainable present policies are. Whileadjustment actions carry a shzrt-term cost, the longer term damage fromdoing nothing is certainly greater.

li. Several major policy reforms are assumed for the alternativescenario, which targets a 42 GDP growth rate. Policy measures are taken toincrease exports, savings and the efficiency of investment. The keypolicies are a 502 devaluation, taken at the beginning of 1990 and itssupporting measures, namely, far-reaching trade liberalization, fiscalimprovements, reform of the financial system and enhanced social programs.These changes are assumed to increase investment efficiency, economize onimports and accelerate export growth. They strengthen creditworthiness andthere is substantial external borrowing, much of it in the form ofmultilateral programs.

li. The resource gap stabilizes (in US dollar terms) from 1992onwards, and after increasing to over 92 of GDP in 1990 due to the relativeprice effects of the devaluation, falls steadily to around 62 of GDP by1997. Most of this gap is initially financed by transfers but officialgrants fall throughout the period. As a result, the current accountdeficit increases slowly, reaching a peak of 52 of GDP by 1995. Even givengenerous levels of official financing, there is a need for additionalfinancing, which increases in the late 1990s as multilateral adjustmentlending begins to taper off. Debt indicators remain within reasonablelimits up to 1997, with MLT debt servicing reaching at about 62 of GDP and272 of exports. However they are still increasing and El Salvador willneed either more concessional lending terms in the 1990s, or still morerapid export growth, to make a 42 GDP growth rate feasible.

liii. The economic outturns of the two projections are very different,particularly in terms of the long-term prospects of the country. Under acontinuation of present policies, El Salvador ends the decade i'n a worseeconomic position than at present, with the economy contracting. Under theassumed policy changes, it generally improves its position, but alsoacquires a heavy burden of debt. Both scenarios are dominated by costsinherited from the recent past; weakened competitiveness, low investment,aid dependency, heavy war expenditure and war damage, and weakenedinstitutions. Accordingly, it is hard to make incomes grow. An earlyresolution to the conflict, which is consuming over 252 of public sectorrevenue or 52 of GDP in unproductive expenditures, would clearly be ofenormous benefit to the economy. But as plans should be laid which arefeasible even with the current security situation.

I. MACIOECONOKIC SITUATION AND PR0SPECTS

A. Background

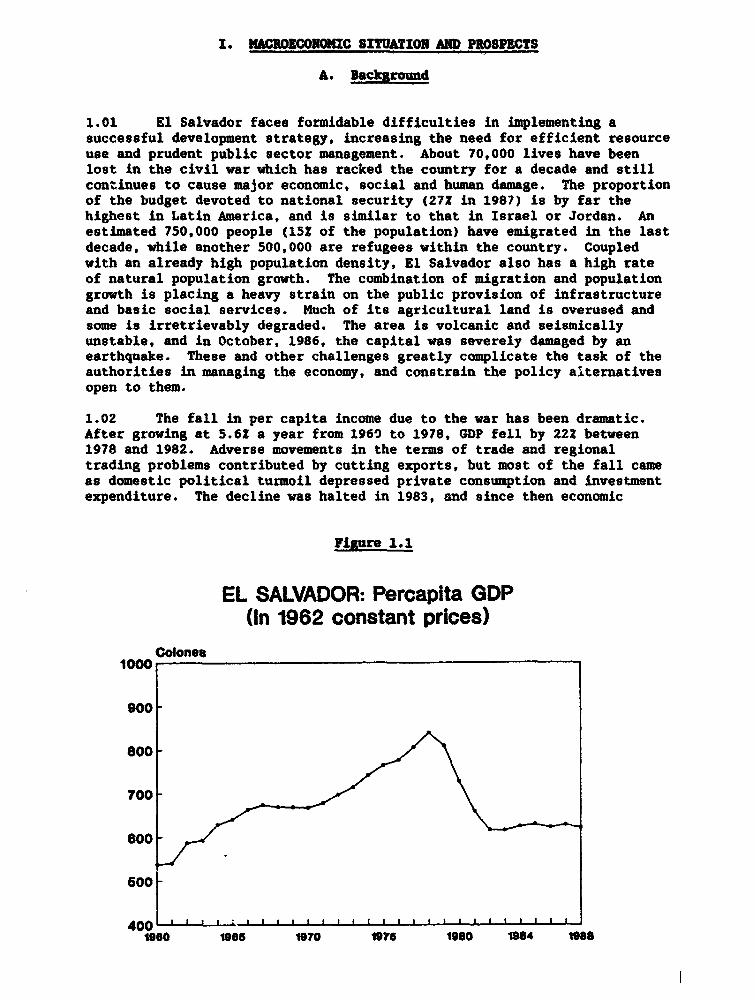

1.01 El Salvador faces formidable difficulties in implementing asuccessful development strategy, increasing the need for efficient resourceuse and prudent public sector management. About 70,000 lives have beenlost in the civil war which has racked the country for a decade and stillcontinues to cause major economic, social and human damage. The proportionof the budget devoted to national security (27Z in 1987) is by far thehighest in Latin America, and is similar to that in Israel or Jordan. Anestimated 750,000 people (15? of the population) have emigrated in the lastdecade, while another 500,000 are refugees within the country. Coupledwith an already high population density, El Salvador also has a high rateof natural population growth. The combination of migration and populationgrowth is placing a heavy strain on the public provision of infrastructureand basic social services. Much of its agricultural land is overused andsome is irretrievably degraded. The area is volcanic and seismicallyunstable, and in October, 1986, the capital was severely damaged by anearthquake. These and other challenges greatly complicate the task of theauthorities in managing the economy, and constrain the policy alternativesopen to them.

1.02 The fall in per capita income due to the war has been dramatic.After growing at 5.6Z a year from 1960 to 1978, GDP fell by 222 between1978 and 1982. Adverse movements in the terms of trade and regionaltrading problems contributed by cutting exports, but most of the fall cameas domestic political turmoil depressed private consumption and investmentexpenditure. The decline was halted in 1983, and since then economic

Figue 1.1

EL SALVADOR: Percapita GDP(In 1962 constant prices)

Colones1000

900

800

700 -

600

400 1 ' ' I1900 1906 1970 1975 1980 1984 1088

growth has averaged only 1.72 a year. The underlying population growthrate is around 2.72, and despite war casualties and emigration thepopulation has grown at around 1.42 per year, so real per capita GDP hasstabilized and remains about 20S below pre-crisis peak levels. High coffeeexport prices and other factors had produced a sharp peak in GDP in thelate 1970s, but the subsequent fall was much greater, and the current levelof $850 per head is similar to that of the early 19609.

1.03 The fall in living standards was even more severe than that i-output. Private consumption spending fell more than GDP in the earlystages of the crisis and remains depressed, so real per capita privateconsumption fell about 25Z. Not only is income depressed in the aggregate,but the already unequal distribution of earned incomes in the San SalvadortIetropolitan Area (SSMA) seems to have grown worse in recent years.Contributing factors have been falling real wages and declining employmentin the formal sector. Over a third of Salvadoran families however arereceiving remittance incomes from abroad which are not captured in theincome distribution data, and this partly offsets the worseningdistribution of earned incomes. Health, nutrition and other socialindicators have remained remarkably stable (Chapter VI), in part due tothis flow of unrecorded incomes to vulnerable groups.

1.04 Despite a jump in the share of public administration and defensein GDP, reflecting the increased role of the public sector in the economy,the sectoral composition of GDP has remained far closer to that of theimnediately pre-crisis period than to that of the early 1960's when percapita incomes were similar to today's. The share of agriculture in totaloutput has increased, as relatively strong demand offset the adverse supplyeffects of rural violence and the major policy distortions affecting thesector. Because of this, the overall share of tradeables in GDP hasremained almost constant in spite of a loss of competitiveness resultingfrom real currency appreciation.

1.05 Transfers played a critical role in stabilizing the economy after1983. The fall in GDP from 1978 to 1982 was spread across all the majorprivate expenditure components, and stopped in 1983 when exports andconsumption abruptly ceased to decline. The export turnaround was mainlybased on traditional crops, whose performance is relatively isolated fromthat f the rest of the economy. Private consumption was subject toconflicting influences: on the negative side there was massive emigration,real wages were declining and employment was only recovering modestly. Onthe other hand, major official transfers were beginning to come in fromabroad, while emigrant remittances were increasing rapidly.

1.06 Demand growth since 1982 has come purely from domestic sources,led by private investment (up 87Z) and public consumption (up 18Z). Thecontribution of the external sector has been negative, with exports growingmore slowly, and imports faster, than GDP. While the increase in privateinvestment is positive for growth, this pattern of growth based on domesticexpenditure will not be sustainable in the medium to long term, since lackof foreign exchange will become a serious constraint on the economy.

-3-

1.07 The longer-term behavior of GDP is closely related to the supplyof factors of production, particularly capital. The availability of bothlabor and capital declined importantly in the crisis years and, though ithas recently improved somewhat, remains well below the levels of the 1960sand 1970s. Private investment has had a part'.cularly strong influence ongrowth, as can be seen from Figure 1.2. From 1980 to 1984, there was notenough investment to maintain the capital stock, which fell by about 14X.Output fell faster than the capital stock, suggesting that a switch to morecapital-intensive production methods in response to increased labor costsand capital subsidies, and capital losses due to violence, expropriation orabandonment of assets were also important. With the recovery of privateinvestment the capital stock began to recover from about 1985, and has nowreturned almost to its historic relation to output.

1.08 Emigration, war casualties and military recruitment have allslowed the growth of the labor force. The growth of the working age(15-64) population slowed from 14.8? in 1970-75 to only 5.1Z from 1979 to1985. As emigrants came from the age groups with the highest labor forceparticipation, the labor supply declined even faster. The loss ofproductive labor due to military recruitment (44,000 from 1978-88) alsofell on these age groups, and the prime age (20-44) civilian malepopulation fell by 3.7? from 1979 to 1985, and had not yet regained its1978 level by 1988. The stock of human capital fell yet more sinceemigrants had an average higher skill levels than the population as awhole, and school enrollment ratios declined steeply. Recent years haveseen an improvement in labor supply, with the growth of the working agepopulation returning to 2.3Z a year by 1987, and school enrollment havingrecovered to pre-crisis levels. Many rural labor markets remainconstrained by emigration, including internal population movements.

Kigure 1.2

EL SALVADOR: Growth RatesGDP and Capital Stock

% per year

10

-6

-10

1951 1085 1960 19805 1970 1975 1980 1985

- GDP growth + Capital Growth

- 4 -

1.09 To sum up, over the last few years with substantial externalassistance the authorities have been able to stabilize the economy, and thetask is now to accelerat. growth and development. An important inter-mediate policy goal wi3. to stimulate efficient investment, in theprivate sector by providiz4 an appropriate framework of incentives, and Inthe public sector by improving project analysis, implementation andfinancing. The success of both sectors will depend on improved publicfinances. This will also help to reduce El Salvador's aid dependency,strengthen the balance of payments, and lay the groundwork for pricestability and reform of the financial sector. Major policy actions aretherefore needed to modify the external trade regime, where both thestructure of protection and the alignment of the exchange rate currentlydistort incentives and impede export growth and diversification. Theeffects of these distortions are particularly strong in the principalproductive sectors, agriculture and manufacturing. As the economy adjuststo new relative prices it will be necessary to protect the poorest segmentsof the population. Experience in other countries strongly suggests thatthe most effective way to do this will be to target government spending onthe social sectors in programs designed to reach these groups.

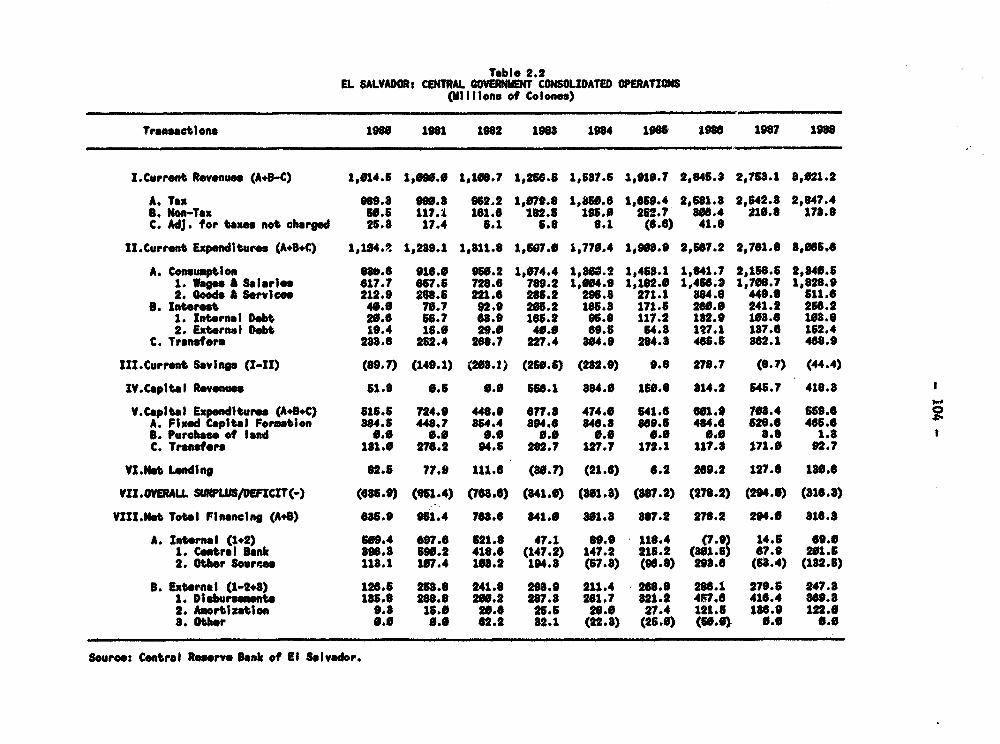

B. Public Finances

1.10 In the early 1980s, the public finances came under strain asrevenue declined with the fall in GDP, security expenditures grew, and thepublic sector made ambitious investments. The deficit increased to unsus-tainable levels, but has declined very substantially in recent years. Asshown in Table 1.1, there has been some relief due to increased grantreceipts, but the improvement has come mainly at the expense of a fallbackin public investment. There was also some increase in public savings;current expenditures declined on account of both public sector real wagesand non-wage recurrent expenditure. The cuts fell mainly on the socialsectors, while debt servicing and security increased rapidly. Apart from

Table 1.1: Public Savings and Investment (I of GDP)

1980-1982 1983-1985 1986-1988

Own Savings 0.3 -0.3 1.5External Grants 0.3 3.3 1.9Total Savings 0.6 3.1 3.4

Public Investment 11.3 7.7 4.0Public Sector Deficit -10.7 -4.6 -0.6

External Borrowing 3.6 2.6 1.0Domestic Borrowing 7.1 2.0 0.4

Memo: DeficitBefore Grants -11.0 -7.9 -2.5

Source: Statistical Annex Table 2.9

-5-

fluctuations due to coffee export tax revenues, the tax effort contributednothing to closing the fiscal deficit, and revenues remain at a low level.The adjustment was thus typical of the pattern found in many countriesundergoing financial crises, whereby the development component of publicexpenditure is sacrificed to meet the urgent need to control the deficit.

1.11 There are several difficulties with these public finance figures.Firstly, expenditures are increasingly made outside the budget and aresupported by borrowing and grants not shown here. This may causeinconsistencies between the major macroeconomic accounts, for instancebetween the balance of payments and the public finances. Secondly thenationalized banking system has incurred large unacknowledged losses whichare contingent liabilities of the public sector. Similar considerationsapply to the public sector's lending to agriculture. The public sectoritself has received sizeable subsidies from the banking system by borrowingat low controlled interest rates. Finally the public sector hasaccumulated a large floating debt, partly in the form of overdue interestpayments. These factors make it difficult to estimate the true financingneeds of the public sector. The actual deficit is probably much largerthan is shown here, and the actions required to make the fiscal positionsustainable are correspondingly stronger.

1.12 The monetary statistics broadly reflect the fiscal picture; up to1983 Lending to the public sector was responsible for the whole of thegrowth in the money stock (M2), while foreign exchange movements were a netsource of monetary contraction. Since 1983 reserve accumulation (mainly inthe form of reduced BCR short term obligations) has caused about 40X of thegrowth in M2, while the contribution of lending to the public sector hasbeen small. Both these changes are attributable to the increased inflow ofofficial transfers from 1983 onwards, and are in sharp contrast to mostcountries' experience during economic crises. Taking the period since 1979as a whole, lending to the private sector has accounted for half of theincrease in the money supply, followed by lending to the public sector(30?) and the accumulation of reserves (20?). However this improvement hasnot been reflected in reduced inflation.

1.13 El Salvador traditionally enjoyed low inflation, with the fixedexchange rate providing an anchor for the price level, but since 1975consumer prices have consistently risen faster than abroad. Theacceleration of inflation up to 1985 can be explained partly by monetaryexpansion and partly by cost pressures. From 1981 to 1985 the money stockrose more rapidly than nominal GDP, and by 1985 the velocity of circulationwas over 20? below its 1977-80 average. Cost pressures also contributed asreal wages rose (despite falling real GDP) reflecting considerable tradeunion power.

1.14 The average inflation rate of 25? since 1985 is harder to explain.There was a reduction in real money holdings, partly because real interestrates had become heavily negative, and by 1988 the velocity was almost backto its pre-1980 level. There were one-time price adjustments in responseto the major devaluation of the Colon in early 1986 but these had workedthrough the system by the end of 1987, and real wages were falling,reducing the importance of cost-push factors. However inflation hascontinued at above 20? through 1988. Two possible explanations for this

- 6 -

are the substitution of US dollars for domestic currency, adding to theeffective money stock, and supply shortages in the agricultural sector (oneof the most rigid and regulated in the economy), particularly in 1988. Toreduce currency substitution will require measures to attract remittanceinflows through the banking system. Policies to improve agriculturalsupply are considered in Chapter IV.

1.15 Improvements in the public finances are thus necessary for manyreasons. Investment, maintenance and recurrent social expenditures have tobe increased, to lay the foundations for growth without resorting toinflationary domestic financing. Public sector wages need to beselectively increased, as a means of improving efficiency. The publicsector must put itself in a position to cover its outlays without relyingon major transfers from abroad, in order to make El Salvador less dependanton aid. Provision must be made to meet the accumulated losses of thefinancial system, in order to put it in a position to finance moreproductive investment. And most importantly of all, the public sectorneeds the flexibility to increase public savings in support ofstabilization and adjustment objectives.

1.16 As a consequence of its fiscal cutbacks and access to grantfinancing, El Salvador does not have a particularly high public sectorexternal debt. At the end of 1987, the debt - at US$1667 Mn - was under352 of GDP, while interest amounted to 8? and total debt service paymentsto under 202 of exporta. Over 95Z of the debt is owed by the publicsector, and private creditors have been steadi':. repaying their foreignborrowings for several years. Almost all of the public sector's debt (952in 1987) is owed to official creditors, particularly USAID, and most of itis on concessional terms. As a reatlt, the average interest rate on theexternal debt was only 4.6? in 1987. Nonethelese net transfers (newlending less amortization and interest) to the public sector, after beinghighly positive in the early 1980s, have now dwindled almost toinsignificance, averaging US$12 Mn in 1986 and 1987.

C. The External Trade Resime and the Current Account

1.17 Because of its heavy dependance on a few export commodities, withunstable international prices, El Salvador suffers from extreme volatilityin its terms of trade.1 With the peak in world coffee prices, El Salvador'sterms of trade reached very favorable levels in 1976-79, about 50? abovetheir long run average. They then collapsed to levels below the long runaverage and (after a respite in 1986) are now as poor as at any time in thelast 30 years. The dependence on coffee also makes the cycle in coffeeproduction extremely important for the economy. Output boomed in the early19808 on the basis of investments made a few years before when coffeeprices were high. More recently investment has been low, and production isstarting to decline. Crop losses due to bad weather in 1988-89 areexacerbating this trend, and growth is suffering correspondingly.

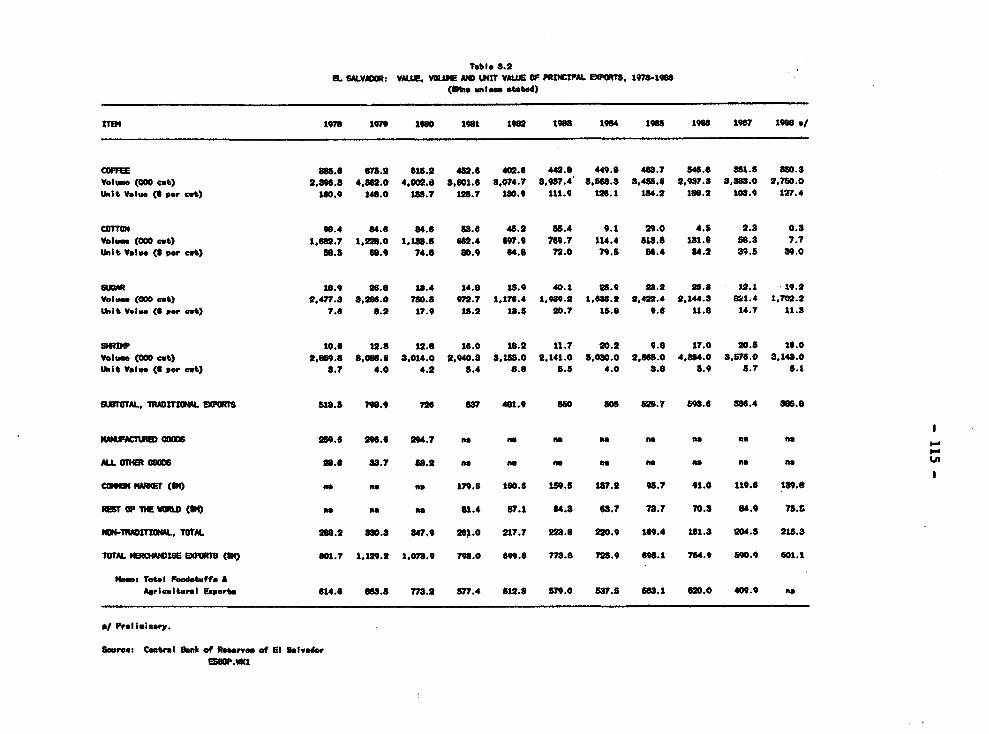

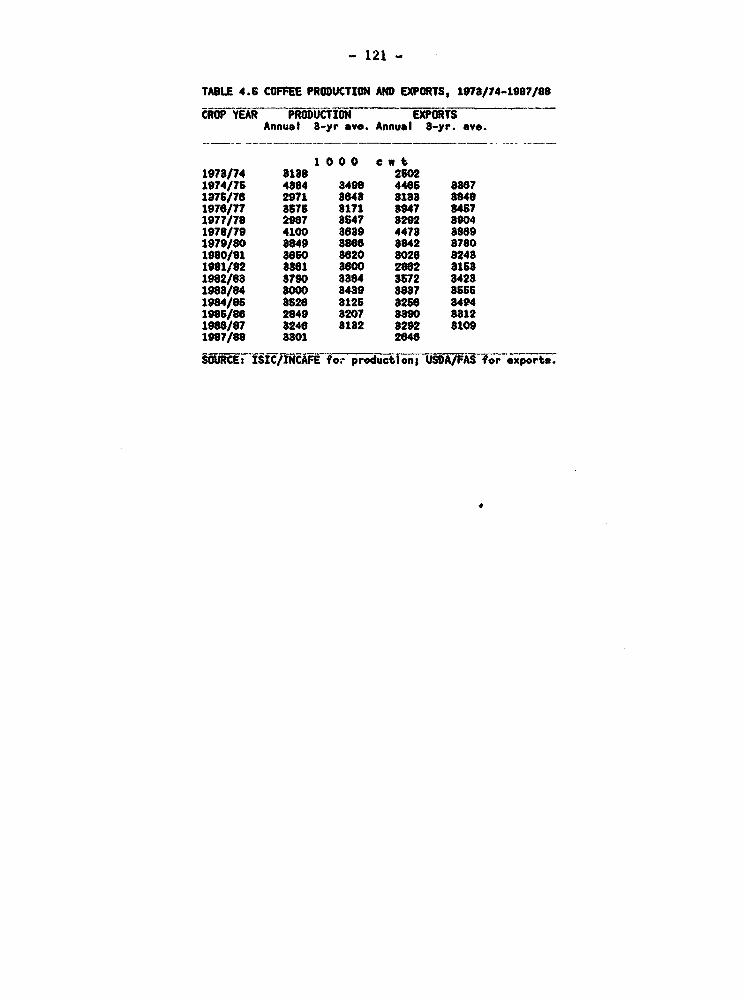

I/ Revenues from coffee have increased in recent years to over 602 ofexport earnings, their highest level since the early 1960s.

- 7 -

1.18 In addition, E1 Salvador's exports are hampered by a realappreciation of the exchange rate. On a purchasing power parity basis thereal effective exchange rate is over 702 more appreciated than in 1980 -despite a 1002 devaluation in 1986. This has had a major impact onincentives, increasing the relative profitability of producing non-tradeables, such as services. The tradeable goods sectors - mainlyagriculture and manufacturing - have seen their share of investment fall inrecent years. Some subsectors have been able to escape the squeeze due tothe appreciation, for instance the manufacture of highly protected import-substitutes and the production of basic grains for the domestic market.Traditional agricultural exports, particularly coffee, enjoyed such highprofitability in the late 1970s that investment remained worthwhile throughseveral years of real appreciation, though margins now appear to be comingunder pressure. Manufactured exports, which enjoy no special privileges,are the most sensitive to real appreciation and have performed poorly forseveral years.

Figure 1.3

El Salvador: Real Exchange Ratebased on wages and the CPI

120

610 ,

1976 1078 1980 1982 1984 1988

Wage-based RER +- CPI-based RER

1.19 The deteriorating trade position has not been reflected in asevere current account deficit, however, because transfer items have beenlarge and positive. After averaging 2.52 of GDP during 1975-80, theresource balance widened abruptly to 6.52 in 1981-85, and after improvingin 1986 has returned to a similar level over the last 2 years. The deficiton factor services has been low because external debt and interest paymentsremained modest. The major offsets were transfer receipts from both

official and private sources; during 1984-88 official grants averaged 5.22if GDP and private transfers 3.6? according to official figures. Eventhese figures may be underestimates; only a very small proportion ofprivate transfers come in through the official banking system, and the bt"lkis estimated rather than recorded. The actual amounts involved may be zFuchlarger, perhaps as much as 11? of GDP by 1987 2 These non-debt-creatingflows have supported levels of economic activity that would otherwise havebeen unsustainable, with obvious short-run benefits in terms of per capitaincomes and welfare. For instance, on official figures, they now financeover 5O0 of merchandise imports.

1.20 By increasing the trade deficit that is compatible with asustainable current account position, transfer inflows have contributed tothe real appreciation of the colon. The problem is similar to that whichfaced Mexico after the 1979 rise in oil prices greatly increased foreignexchange earnings. High coffee earnings in 1976-77, and later transferreceipts combined with restrictive imports policies allowed El Salvador toaccumulate foreign exchange reserves, increasing the money stock, the pricelevel and the real value of the currency. This was an equilibrium for theeconomy, and after the 1986 devaluation there was little premium in theparallel foreign exchange markets until early 1989. Tight money helpedkeep the premium to a low level, while trade taxes and restrictions reducedthe demand for imports. In this situation a devaluation of the officialexchange rate, together with control of domestic credit, would increasereserves, leading to monetary expansion and an increase in the domesticprice level rather than achieving a lasting real depreciation.

1.21 The present system of trade taxes results in a distorted patternof incentives which also discriminates against exports and increases thecost of economic growth. As in the other CACM countries, average tariffrates are not high but there is a wide dispersion of tariff and selectivetax rates giving many import-substituting industries heavy protection.Formal import quotas are not common outside agriculture, but the system ofexchange controls gi gs the authorities the power to selectively restrictthe quantity of imports. The incentive effects of this type of system arewell known from experience in other countries: it is biased againstexports and towards import substitution, particularly for consumer goods.Specific proposals for reform are described in Chapter III.

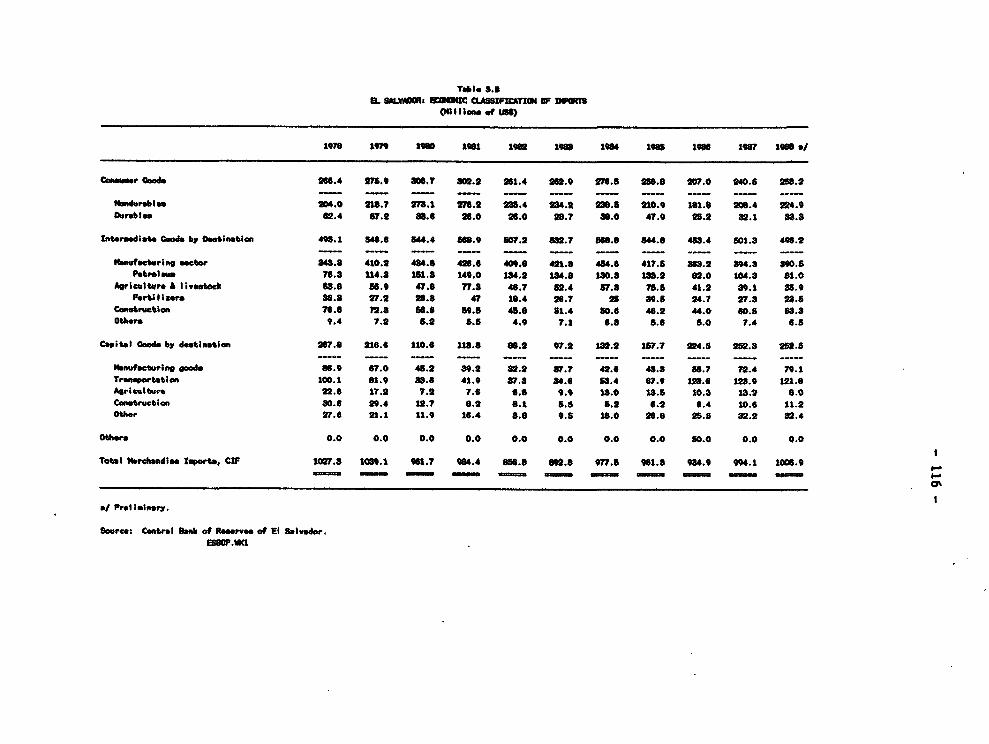

1.22 Poor trade performance has led to substantial real importcompression. Overall exports have fallen from US$950 million in 1977-81 toonly US$680 Mn in 1984-88 due to declines both in volumes and prices,crucially that of coffee. The value of imports also fell up to 1983 butthen recovered so that by 1984-88 they were almost as high (US$980 Mn) asthey had been in 1977-81 (US$990 Mn). Import volumes however have falleneven more than exports, and at constant prices imports of goods and non-factor services fell from 33? of GDP in 1977-79 to only 23Z In 1985-87.

21 See Annex 2. This discreprncy throws in question the credibility oft'e rest of the balance of payments account. If there are additionalcu_rent account transfer inflows, they must be matched by unrecordedoutflows, either for imports or capital flows.

-9-

This import compression is potentially a serious issue for thesustainability of growth, since it indicates a substantial demand forforeign exchange that is not being met through official channels. Howeverthere is reason to believe that some imports excluded from the officialbalance of payments figures are being financed by unofficial transfers.

1.23 Overvaluation improves welfare in the short term because it makesimports cheaper in domestic currency, but is dangerous because of itsnegative incentive effects on tradeables production - particularly exports.Just as they did in Holland with the advent of large-scale natural gasexports, or in Mexico after the 1979 oil price rise, agriculture andmanufacturing in El Salvador are progressively losing their capacity togenerate foreign exchange, the so-called 'Dutch disease' effect. And as inthe Mexican case, there is a danger that the exceptional levels of foreignexchange inflows responsible for the appreciation will disappear. Officialtransfers are likely to fall in the medium term, since they are linked toEl Salvador's exceptional security problems and earthquake damage. Theprospect for private transfers is much more difficult to gauge, since theinformation on them is so poor. The analysis in Annex 2, based on recentsurveys and projections of migration, suggests that the period of rapidly-growing remittances is over. Thus the foreign exchange needed for economicgrowth will have to come from the production of tradeable goo-'

1.24 The management of this Dutch Disease phenomenon is a majormacroeconomic policy issue for El Salvador. At first sight it might appearthat exceptional foreign exchange inflows provide an opportunity to expandaggregate demand through public investment or social spending withoutmeeting a binding foreign exchange constraint. However, this wouldincrease the demand for non-tradeable goods, increasing inflation and theovervaluation of the currency. It is not enough simply to devalue theColon either, since that would lead to a rise in the domestic price levelthat would cancel out the devaluation. Rather trade policy must bechanged, to alter the underlying conditions in the foreign exchange market.

1.25 As real wages have declined in recent years, El Salvador's costcompetitiveness has been restored to the level of the late 1970s. In thissense the 1986 devaluation was successful, and for this reason non-traditional exports began to increase for the first time in a decade in1988. While the fall in real vages has eased the pressure on the absolutelevel of manufactured export profitability and competitiveness, theexchange rate continues to weaken trade performance tairough the bias infavor of non-tradeables. It may therefore be possible to bring thecurrency back to its historic purchasing power parity without a further cutin real wages, using trade liberalization to increase competition and cutmargins.

1.26 The most effective way to achieve a real depreciation would be toliberalize imports from some of their restrictions. The fact that the realappreciation, fueled by transfer inflows, has been accompanied by importcompression, strongly suggests that import restrictions have been a majorinfluence on the exchange rate. The analysis in Chapter III, for inetance,suggests that trade taxes account for an overvaluation of 10-122. Relaxing

- 10 -

trade restrictions would cause an excess demand in the foreign exchangemarkets, which would have to be brought back into balance by a devaluationof the official exchange rate. Rather than making the country worse off(the effect of a devaluation in response to an unsustainable currentaccount deficit) this process would spread the benefits of foreign exchangeinflows to a wider group than before - critically including exporters.

D. Investment Performance and Prospects

1.27 After falling from 19X to 12Z of GDP in the early years of thecrisis in response to severe uncertainty, investment spending has been afairly constant share of GDP. There has however been a marked shift awayfrom public and towards private investment; from 1980-83 to 1984-87, publicinvestment contracted from 6.32 to 3.6Z of GDP, while private fixedinvestment grew from 5.72 to 8.62. This level of private investment isconsistent with an economic growth rate of 1-22 p.a. Each sustained 12increase in the share of private investment in GDP seems to entail about a12 increase in the growth rate, so for a target growth rate of 42, privateinvestment of about 122 of GDP would be required, a rate not seen since thelate 1970s. Public investment continued to decline into 1987 and 1988,despite large commitments of external funds for earthquake reconstruction,and is now well below the level necessary for growth. Public investmentwould have to increase together with renewed growth, both to complementprivate investment and to rebuild deteriorated infrastructure.

1.28 Besides increasing, the composition of private investment needs tochange if long-term growth is to be sustained. For instance, there was amarked rise in the share of residential construction in private investmentfrom 1978 to 1982, which has not yet been reversed. More ceriously, theshare of the tradeables sectors (agriculture and manufacturing) in totalinvestment has continued to decline (from 382 in 1975-78 to 282 in 1980-83and 262 in 1984-87), reflecting the falling competitiveness of thesesectors due to the exchange rate.

1.29 Public policy should aim at increasing the levels of both privateand public investment, and ensuring that their composition is appropriatelytailored for the needs of the economy. To do so successfully will involveaddTessing the current constraints on investment, particularly thoserelating to investor confidence, the availability of investment financing,and the structure of taxation.

1.30 Many of the constraints on private willingness to invest havediminished in recent years. At the height of the crisis there was extremeuncertainty about the physical safety of plant and personnel, an indicatorwhich is the fact that insurance cover for industrial investments wassuspended for several years. Since physical risk is intractable toeconomic policy measures it represents a fundamental constraint, and hashad a particularly severe effect on direct foreign investment, which hasall but dried up. It is extremely difficult to quantify such risks, andfor policymakers to persuade investors to revise their assessment in theshort term. With USAID assistance, insurance cover has now been restoredand premiums on plant (about 5/000) are small, compared with the implicitrisk premiums that investors have appl.ed to El Salvador. However full

- 11 -

investor confidence will not retutn without a settlement of the country'spolitical problems.

1.31 There is increased confidence in the degree of government supportfor private business. Confidence was undermined by lack of officialsupport in labor disputes, and the nationalization of agricultural andservice sector enterprises in 1979-80. The business community acknowledgesthat the government's attitude to labor relations problems has sincechanged in their favor, and the election in 1989 of a government withsubstantial business support has further relieved this uncertainty.

1.32 Excess capacity and confidence in the prospects for sustainedgrowth are important for investment. There was excess capacity to servedomestic and CACM markets due to the fall in demand in 1978-82. As notedabove, capital and output have since been moving towards their historicrelation, and the margin of excess capacity is much reduced. Surveyevidence suggests that industrial capacity utilization Is currently around70X, and that industry is once again investing in plant expansions aimed atthe domestic market. The most important remaining constraint on privatewillingness to invest may therefore be the expectation that growth willremain slow, in part because the authorities have been unwill ag toimplement aggressive expenditure-switching policies, such as devaluation,or fiscal policies consistent with sustainable growth. Credible policiesin these areas would increase private willingness to invest.

1.33 To finance an increase in private investment, it will be necessaryto mobilize increased savings. In the aggregate, private investment isfinanced by the sum of private savings, the public sector surplus ordeficit, and the resource gap, so a package of measures is needed whichwill move all three together. Experience from many countries suggests thatit is difficult to increase private savings in the context of depressedreal incomes, but tnat it is important to end the downward pressure onsavings due to heavily negative real deposit rates - if only to protect thedeposit base of the financial system. A more positive response of privatesavings can be expected later in the adjustment process, when per capitaincomes begin to rise. In El Salvador, a cut in the public sector deficitshould probably be achieved by increasing taxation rather than by furthercutting expenditure. It will be of crucial importance to avoid an increasein the burden of security related spending on domestic fiscal resources, ifthe economy is to be adjusted succe,sfully. An increase in the resourcegap (the excess of imports over exports) can be brought about by relaxingrestrictions on imports. This is also the prerequisite both for a realdevaluation and for improving the structure of incentives, and is thusfundamental to the policy recommendations of the report.