EGM Circular DD 10 October-10

158

CIRCULAR DATED 10 OCTOBER 2011 This Circular is issued by C.K. Tang Limited and is important as it contains the recommendation of the Independent Directors (as defined herein) of C.K. Tang Limited and the advice of CIMB Bank Berhad, Singapore Branch to the Independent Directors of C.K. Tang Limited. This Circular requires your immediate attention. Please read it carefully. If you are in any doubt in relation to this Circular, the Selective Capital Reduction (as defined herein) or as to the action that you should take, you should consult your stockbroker, bank manager, solicitor or other professional adviser immediately. If you have sold or transferred all your issued and fully paid-up ordinary shares in C.K. Tang Limited, you should immediately forward this Circular together with the Notice of Extraordinary General Meeting and the attached proxy form to the purchaser or transferee or to the bank, stockbroker or agent through whom you effected the sale or transfer, for onward transmission to the purchaser or transferee. This Circular shall not be construed as, may not be used for the purposes of, and does not constitute a notice or proposal or advertisement or an offer or invitation or solicitation in any jurisdiction or in any circumstance in which such a notice or proposal or advertisement or an offer or invitation or solicitation is unlawful or not authorised, or to any person to whom it is unlawful to make such a notice or proposal or advertisement or an offer or invitation or solicitation. C.K. TANG LIMITED (Incorporated in Singapore) (Company Registration No.: 196100023H) CIRCULAR TO SHAREHOLDERS IN RELATION TO THE PROPOSED SELECTIVE CAPITAL REDUCTION BY C.K. TANG LIMITED PURSUANT TO THE COMPANIES ACT, CHAPTER 50 OF SINGAPORE Independent Financial Adviser to the Independent Directors of C.K. Tang Limited CIMB Bank Berhad (13491-P) Singapore Branch (Incorporated in Malaysia) IMPORTANT DATES AND TIMES Last date and time for lodgement of Proxy Form : 25 October 2011 at 9.30 a.m. Date and time of Extraordinary General Meeting : 27 October 2011 at 9.30 a.m. Venue of Extraordinary General Meeting : RELC International Hotel 30 Orange Grove Road Level 5 (Room 507) Singapore 258352

-

Upload

kigallo-tan -

Category

Documents

-

view

53 -

download

3

Transcript of EGM Circular DD 10 October-10

CIRCULAR DATED 10 OCTOBER 2011

This Circular is issued by C.K. Tang Limited and is important as it contains the recommendation

of the Independent Directors (as defined herein) of C.K. Tang Limited and the advice of CIMB

Bank Berhad, Singapore Branch to the Independent Directors of C.K. Tang Limited. This

Circular requires your immediate attention. Please read it carefully.

If you are in any doubt in relation to this Circular, the Selective Capital Reduction (as defined

herein) or as to the action that you should take, you should consult your stockbroker, bank

manager, solicitor or other professional adviser immediately.

If you have sold or transferred all your issued and fully paid-up ordinary shares in C.K. Tang Limited,

you should immediately forward this Circular together with the Notice of Extraordinary General Meeting

and the attached proxy form to the purchaser or transferee or to the bank, stockbroker or agent through

whom you effected the sale or transfer, for onward transmission to the purchaser or transferee.

This Circular shall not be construed as, may not be used for the purposes of, and does not constitute

a notice or proposal or advertisement or an offer or invitation or solicitation in any jurisdiction or in any

circumstance in which such a notice or proposal or advertisement or an offer or invitation or solicitation

is unlawful or not authorised, or to any person to whom it is unlawful to make such a notice or proposal

or advertisement or an offer or invitation or solicitation.

C.K. TANG LIMITED(Incorporated in Singapore)

(Company Registration No.: 196100023H)

CIRCULAR TO SHAREHOLDERS

IN RELATION TO THE

PROPOSED SELECTIVE CAPITAL REDUCTION BY C.K. TANG LIMITED

PURSUANT TO THE COMPANIES ACT, CHAPTER 50 OF SINGAPORE

Independent Financial Adviser to the Independent Directors of C.K. Tang Limited

CIMB Bank Berhad (13491-P)

Singapore Branch(Incorporated in Malaysia)

IMPORTANT DATES AND TIMES

Last date and time for lodgement of Proxy Form : 25 October 2011 at 9.30 a.m.

Date and time of Extraordinary General Meeting : 27 October 2011 at 9.30 a.m.

Venue of Extraordinary General Meeting : RELC International Hotel

30 Orange Grove Road

Level 5 (Room 507)

Singapore 258352

CONTENTS PAGE

1. INTRODUCTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

2. SELECTIVE CAPITAL REDUCTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

3. CONFIRMATION OF FINANCIAL RESOURCES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

4. RATIONALE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

5. TU3 LLP’S INTENTIONS FOR THE COMPANY AND NO RIGHT OF COMPULSORY

ACQUISITION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

6. SHAREHOLDERS’ APPROVAL. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

7. ADMINISTRATIVE PROCEDURES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

8. EXEMPTIONS BY THE SIC. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

9. ADVICE OF THE IFA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

10. INDEPENDENCE AND RECOMMENDATION OF THE DIRECTORS . . . . . . . . . . . . . . 14

11. EXTRAORDINARY GENERAL MEETING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

12. ACTION TO BE TAKEN BY SHAREHOLDERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

13. INFORMATION RELATING TO CPFIS INVESTORS . . . . . . . . . . . . . . . . . . . . . . . . . . 15

14. RESPONSIBILITY STATEMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

APPENDIX 1 — LETTER FROM TU3 LLP DATED 8 SEPTEMBER 2011 . . . . . . . . . . . . . . 17

APPENDIX 2 — REPORT OF THE FA IN CONNECTION WITH THE SELECTIVE CAPITAL

REDUCTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

APPENDIX 3 — VALUATION SUMMARY ISSUED BY JONES LANG LASALLE PROPERTY

CONSULTANTS PTE LTD . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

APPENDIX 4 — VALUATION REPORT ISSUED BY JONES LANG LASALLE PROPERTY

CONSULTANTS PTE LTD . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

APPENDIX 5 — LETTER FROM THE IFA TO THE INDEPENDENT DIRECTORS OF C.K.

TANG LIMITED . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

APPENDIX 6 — ADDITIONAL INFORMATION ON TU3 LLP . . . . . . . . . . . . . . . . . . . . . . . . 82

APPENDIX 7 — ADDITIONAL INFORMATION ON THE COMPANY . . . . . . . . . . . . . . . . . . 86

APPENDIX 8 — GENERAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

APPENDIX 9 — AUDITED CONSOLIDATED FINANCIAL STATEMENTS FOR THE GROUP

FOR FY 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 108

NOTICE OF EXTRAORDINARY GENERAL MEETING . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153

TABLE OF CONTENTS

1

Except where the context otherwise requires, the following definitions apply throughout this Circular:

“Articles” : Articles of Association of the Company

“Books Closure Date” : The date (to be determined by the Company) on which the

Transfer Books and the Register of Members are closed for

the purposes of the Selective Capital Reduction

“Cash Distribution” : Shall have the meaning ascribed to it in paragraph 2.4 of

this Circular

“Circular” : This circular to Shareholders issued by the Company in

relation to the proposed Selective Capital Reduction

“Code” : The Singapore Code on Take-overs and Mergers

“Companies Act” : The Companies Act, Chapter 50 of Singapore

“Company” or “CKT” : C.K. Tang Limited

“Company Securities” : Shall have the meaning ascribed to it in paragraph 6.1 of

Appendix 6 to this Circular

“Concert Parties” : Parties acting or deemed to be acting in concert with TU3

LLP in connection with the Selective Capital Reduction

“Court” : High Court of the Republic of Singapore

“CPF” : The Central Provident Fund

“CPF Agent Banks” : Agent banks included under the CPFIS

“CPFIS” : CPF Investment Scheme

“CPFIS Investors” : Investors who purchased Shares using their CPF savings

under the CPFIS

“Delisting” : The voluntary delisting of the Company from the Official List

of the SGX-ST under Rules 1307 and 1309 of the Listing

Manual

“Delisting Date” : Shall have the meaning ascribed to it in paragraph 1.3 of

this Circular

“Delisting Proposal” : Shall have the meaning ascribed to it in paragraph 1.3 of

this Circular

“Department Store Property” : The portions of the property at 310/320 Orchard Road

Singapore 238864/238865, which are owned by the Group

and are the subject of the Valuation Summary and Valuation

Report, as set out in Appendices 3 and 4 to this Circular

“Directors” : The directors of the Company (including the Independent

Directors) as at the Latest Practicable Date

DEFINITIONS

2

“EGM” : Extraordinary general meeting of the Company as

adjourned to be held on 27 October 2011, notice of which is

set out on page 153 of this Circular, or any adjournment

thereof

“Exit Offer” : The exit offer made on 31 July 2009 by Oversea-Chinese

Banking Corporation Limited, for and on behalf of TU3 LLP,

to acquire all the Shares other than those held by TU3 LLP

for S$0.83 per Share, conditional upon the approval of the

resolution to approve the Delisting

“FA” or “PwCCF” : PricewaterhouseCoopers Corporate Finance Pte Ltd, the

financial adviser to the Company for the Selective Capital

Reduction

“Fair Market Value” : Shall have the meaning ascribed to it in paragraph 2.4(iii) of

this Circular

“FA Report” : Report from the FA in connection with the Selective Capital

Reduction

“First EGM” : Extraordinary general meeting of the Company that was

proposed to be held on 15 September 2011 and was

subsequently adjourned

“First Notice of EGM” : Notice of extraordinary general meeting of the Company

held on 15 September 2011, which was subsequently

adjourned

“FY” : Financial year ended or ending (as the case may be) on 31

March of a particular year as stated

“Group” : The Company and its subsidiaries

“IFA” or “CIMB Bank Berhad” : CIMB Bank Berhad, Singapore Branch, the independent

financial adviser to the Independent Directors for the

Selective Capital Reduction

“Independent Directors” : The Directors who consider themselves to be independent

for the purposes of making the recommendation to

Participating Shareholders in relation to the Selective

Capital Reduction, namely, Ernest Seow Teng Peng, Cecil

Vivian Richard Wong, Foo Tiang Sooi and Michel Grunberg

“Latest Practicable Date” : 3 October 2011, being the latest practicable date prior to the

printing of this Circular

“Letter” : Letter dated 18 August 2011 sent by the Company to the

Shareholders in relation to the proposed Selective Capital

Reduction

“Listing Manual” : The SGX-ST Listing Manual

DEFINITIONS

3

“LLP Act” : Limited Liability Partnerships Act, Chapter 163A of

Singapore

“Memorandum” : Memorandum of Association of the Company

“Non-Participating

Shareholders”

: Shall have the meaning ascribed to it in paragraph 1.3 of

this Circular

“Notice Date” : 18 August 2011, being the date of the Letter

“Notice of EGM” : Notice of EGM of the Company to be held on 27 October

2011, a copy of which was enclosed in a letter to

Shareholders dated 27 September 2011

“NTA” : Net tangible assets

“Participating Shareholders” : Shall have the meaning ascribed to it in paragraph 2.1 of

this Circular

“Registered Address” : The address of each Shareholder as set out in the Register

of Members

“Register of Members” : The register of holders of the Shares, as maintained by the

Share Registrar

“Selective Capital Reduction” : Selective capital reduction to be undertaken by the

Company pursuant to the Companies Act

“SGX-ST” : Singapore Exchange Securities Trading Limited

“Shareholders” : Registered holders of the Shares

“Share Registrar” : Boardroom Corporate & Advisory Services Pte. Ltd.

“Shares” : Issued and paid-up ordinary shares in the Company

“SIC” : Securities Industry Council of Singapore

“S$” and “cents” : Singapore dollars and cents respectively, being the lawful

currency of the Republic of Singapore

“Tang Holdings” : Tang Holdings Private Limited

“Transfer Books” : The transfer books of the Company, as maintained by the

Share Registrar

“TU2 LLP” : Tang UnityTwo LLP, a limited liability partnership registered

under the LLP Act

“TU3 LLP” : Tang UnityThree LLP, a limited liability partnership registered

under the LLP Act

“TU3 LLP Letter” : The unsolicited letter dated 8 September 2011 from TU3 LLP

to the Company

“TU3 LLP Partners” : TWS and UPL

DEFINITIONS

4

“TU3 Securities” : Shall have the meaning ascribed to it in paragraph 6.1 of

Appendix 7 to this Circular

“TWK” : Tang Wee Kit

“TWS” : Tang Wee Sung

“UPL” : Untien Pte. Ltd.

“Valuation Report” : The valuation report dated 3 October 2011 of the Department

Store Property from the Valuer setting out, inter alia, their

valuation of the Department Store Property which is

reproduced in Appendix 4 to this Circular

“Valuation Summary” : The valuation summary dated 30 June 2011 of the

Department Store Property from the Valuer setting out, inter

alia, their valuation of the Department Store Property which is

reproduced in Appendix 3 to this Circular

“Valuer” : Jones Lang LaSalle Property Consultants Pte Ltd, the valuer

appointed by the Company, in connection with the Selective

Capital Reduction, to value the Department Store Property

and to issue the Valuation Summary and the Valuation

Report

“%” or “per cent.” : Per centum or percentage

The headings in this Circular are inserted for convenience only and shall be ignored in construing this

Circular.

Any discrepancies in the tables in this Circular between the listed amounts and the totals thereof are

due to rounding.

Words importing the singular shall, where applicable, include the plural and vice versa. Words importing

the masculine gender shall, where applicable, include the feminine and neuter genders and vice versa.

References to persons shall, where applicable, include corporations.

Any reference in this Circular to any enactment is a reference to that enactment as for the time being

amended or re-enacted. Any word defined under the Companies Act, the Code or any statutory

modification thereof and not otherwise defined in this Circular shall, where applicable, have the same

meaning assigned to it under the Companies Act, the Code or any statutory modification thereof, as the

case may be, unless the context otherwise requires.

Any reference to a time of day and date in this Circular is made by reference to Singapore time and date

respectively unless otherwise stated.

DEFINITIONS

5

All statements other than statements of historical facts included in this Circular are or may be

forward-looking statements. Forward-looking statements include but are not limited to those using

words such as “expect”, “anticipate”, “believe”, “intend”, “project”, “plan”, “strategy”, “forecast” and

similar expressions or future or conditional verbs such as “if”, “will”, “would”, “should”, “could”, “may”

and “might”. These statements reflect the Company’s and the Non-Participating Shareholders’ current

expectations, beliefs, hopes, intentions or strategies regarding the future and assumptions in light of

currently available information. Such forward-looking statements are not guarantees of future

performance or events and involve known and unknown risks and uncertainties. Accordingly, actual

results may differ materially from those described in such forward-looking statements. Shareholders

and investors should not place undue reliance on such forward-looking statements, and neither the

Company, the Non-Participating Shareholders, the Valuer, the FA nor the IFA undertakes any obligation

to update publicly or revise any forward-looking statements, subject to compliance with all applicable

laws and regulations and/or any other regulatory or supervisory body or agency.

FORWARD-LOOKING STATEMENTS

6

C.K. TANG LIMITED(Incorporated in Singapore)

(Company Registration No.: 196100023H)

Directors: Registered Office:

Ernest Seow Teng Peng

Cecil Vivian Richard Wong

Foo Tiang Sooi

Michel Grunberg

Soh Yew Hock

310 Orchard Road

Singapore 238864

10 October 2011

To: The Shareholders of C.K. Tang Limited

Dear Sir/Madam

PROPOSED SELECTIVE CAPITAL REDUCTION BY C.K. TANG LIMITED PURSUANT TO THE

COMPANIES ACT

1. INTRODUCTION

1.1 First Notice of EGM and Adjournment. On 18 August 2011, the Company issued a First

Notice of EGM to the Shareholders to seek the approval of Shareholders for the proposed

Selective Capital Reduction to be undertaken by the Company. On 13 September 2011, two

days before the First EGM, the Company was directed by the SIC to ask for an adjournment of

the First EGM for the purpose of appointing an independent financial adviser to opine on the

proposed Selective Capital Reduction. In line with this direction, the Directors proposed and the

Shareholders approved that the First EGM be adjourned to 9.30 a.m. on 27 October 2011.

1.2 Circular. The purpose of this Circular is to provide Shareholders with relevant information as

at the Latest Practicable Date pertaining to the Company and to set out the advice of the IFA to

the Independent Directors and the recommendation of the Independent Directors with regard to

the proposed Selective Capital Reduction to be tabled at the EGM. This Circular contains all

information in relation to the proposed Selective Capital Reduction as set out in the Letter.

1.3 Background. On 8 May 2009, the Company and TU3 LLP jointly announced that the Company

had received a delisting proposal (“Delisting Proposal”) from TU3 LLP to seek the voluntary

delisting of the Company from the Official List of the SGX-ST pursuant to Rules 1307 and 1309

of the Listing Manual (“Delisting”). Under the Delisting Proposal, Oversea-Chinese Banking

Corporation Limited, for and on behalf of TU3 LLP, made an exit offer (“Exit Offer”) to acquire

all the Shares other than those held by TU3 LLP for S$0.83 per Share, conditional upon the

approval of the resolution to approve the Delisting. The Exit Offer was made on 24 June 2009,

and on 31 July 2009, the Shareholders voted in favour of the resolution to approve the Delisting

and accordingly, the Exit Offer became unconditional.

The Exit Offer closed on 14 August 2009 and the Company was delisted from the Official List of

the SGX-ST on 24 August 2009 (“Delisting Date”). As at the Latest Practicable Date, TU3 LLP,

TU2 LLP, Kerith Holdings LLP and TWK (the “Non-Participating Shareholders”) own or control

LETTER TO SHAREHOLDERS

7

232,601,053 Shares, representing approximately 98.2 per cent. of the total number of Shares1

and the remaining Shares representing 1.8 per cent. of the total number of Shares are held by

other Shareholders.

2. SELECTIVE CAPITAL REDUCTION

2.1 Realise Value of Shares. The Company proposes to implement the Selective Capital

Reduction and cancel all the Shares held by the Shareholders, except those held by the

Non-Participating Shareholders, to provide the remaining Shareholders (the “Participating

Shareholders”) with an avenue to realise the value of their Shares following the Delisting.

2.2 Reduce Share Capital. The Selective Capital Reduction will involve reducing the share capital

of the Company from S$47,848,113.86 comprising 236,984,226 Shares to S$42,149,988.96

comprising 232,601,053 Shares, representing a reduction of the issued share capital of the

Company by approximately 1.8 per cent.

2.3 Process. The Selective Capital Reduction will be effected by:

(i) cancelling the amount of S$5,698,124.90 constituting part of the total paid-up share capital

of the Company held by the Participating Shareholders; and

(ii) cancelling 4,383,173 of the said Shares constituting part of the total issued share capital

of the Company held by the Participating Shareholders.

2.4 Cash Distribution. The aggregate sum of S$5,698,124.90 arising from the Selective Capital

Reduction (the “Cash Distribution”) will be returned to the Participating Shareholders, on the

basis of S$1.30 for each Share held by each Participating Shareholder that is cancelled as a

result of the Selective Capital Reduction.

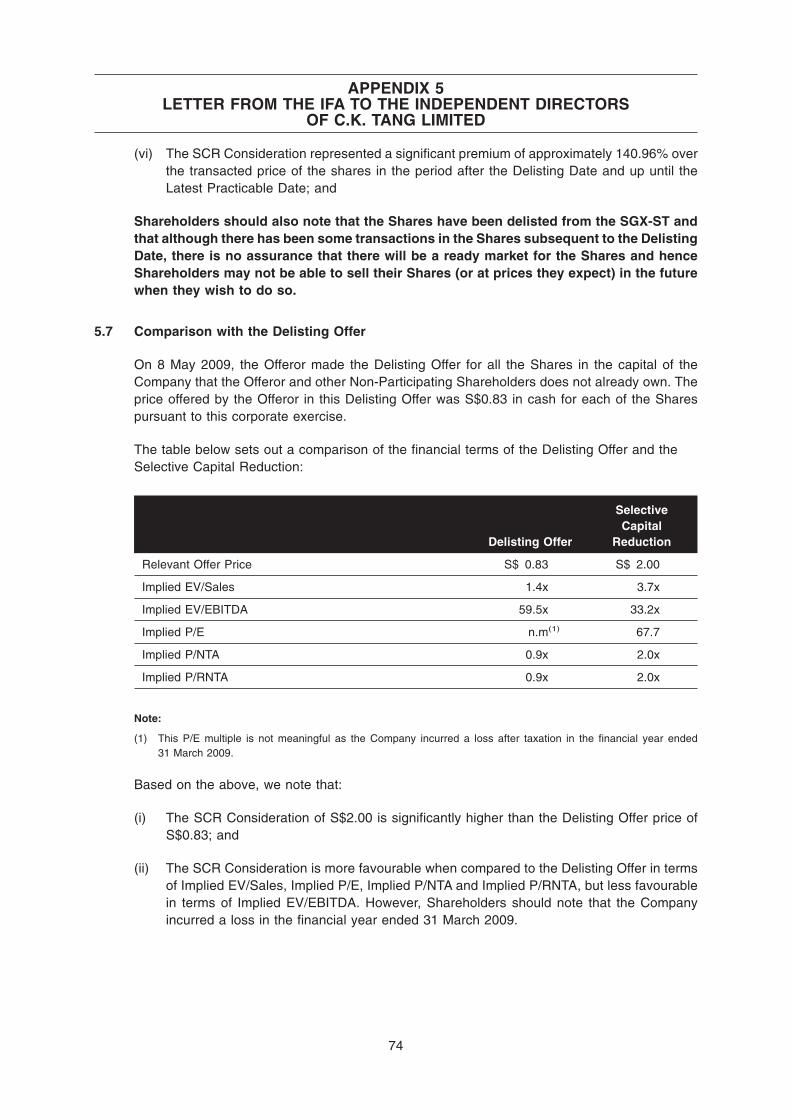

The price of S$1.30 for each Share so cancelled represents:

(i) a premium of 44.4 per cent. over S$0.90 per Share which was the highest price per Share

transacted on the SGX-ST in the 10-year period prior to the Delisting Date;

(ii) a premium of 56.6 per cent. over S$0.83 per Share which was the last transacted price on

the SGX-ST on 6 August 2009;

(iii) a premium of 15.0 per cent. over the fair market value per Share of S$1.13 as set out in

the FA Report (“Fair Market Value”); and

(iv) a premium of 27.5 per cent. over the book value per Share of S$1.02 as at 31 March 2011.

Participating Shareholders will be entitled to any dividends declared, paid or made by the

Company the record date for which is on or before the Books Closure Date.

1 Unless otherwise stated, references in this Circular to percentages of total number of Shares are based on a total of

236,984,226 Shares, which is the total number of issued and paid-up Shares.

LETTER TO SHAREHOLDERS

8

2.5 TU3 LLP Proposal. On 8 September 2011, TU3 LLP wrote to and informed the Company that

it will pay another S$0.70 for each Share held by each Participating Shareholder that is

cancelled as a result of the Selective Capital Reduction, bringing the aggregate payment of each

such cancelled Share to S$2.00. The TU3 LLP Letter was sent to all Shareholders and provides

that such payment is conditional upon the Selective Capital Reduction becoming effective. The

TU3 LLP Letter is set out in Appendix 1 to this Circular.

The aggregate price of S$2.00 for each Share so cancelled represents:

(i) a premium of 122.2 per cent. over S$0.90 per Share which was the highest transacted

price on the SGX-ST in the 10-year period before the Delisting Date;

(ii) a premium of 141.0 per cent. over $0.83 per Share which was the last transacted price on

the SGX-ST on 6 August 2009;

(iii) a premium of 77.0 per cent. over the Fair Market Value; and

(iv) a premium of 96.1 per cent. over the book value per Share of S$1.02 as at 31 March 2011.

3. CONFIRMATION OF FINANCIAL RESOURCES

Oversea-Chinese Banking Corporation Limited confirms that sufficient financial resources are

available to (i) TU3 LLP to satisfy payment of the sum of S$3,068,221.10 representing the total

sum that TU3 LLP will pay to all Participating Shareholders if the Selective Capital Reduction is

effective in accordance with the Companies Act (the “TU3 LLP Payment”) and (ii) the Company

to pay the Cash Distribution if the Selective Capital Reduction becomes effective.

The Company confirms that it has received the TU3 LLP Payment, and that it is authorised to

pay, on behalf of TU3 LLP, to all Participating Shareholders S$0.70 for each Share cancelled

pursuant to the Selective Capital Reduction.

The Directors are of the opinion that the financial resources available to the Company and the

Company’s share capital base following the Selective Capital Reduction will be sufficient for the

foreseeable near-term operating needs of the Company.

4. RATIONALE

The Selective Capital Reduction is an internal corporate exercise that is proposed by the

Company for the Participating Shareholders.

The Selective Capital Reduction would enable the Company to return the aggregate sum of

S$5,698,124.90 to the Participating Shareholders in respect of the cancellation of the Shares

held by them.

Following the Delisting, it has been difficult for the Participating Shareholders to realise their

investment in the Shares given the lack of a public market for the Shares. With the Selective

Capital Reduction, the Participating Shareholders will have an opportunity to realise the value of

their Shares.

If the Participating Shareholders do not approve the Selective Capital Reduction, there is no

guarantee another opportunity will arise in the future for them to realise the value of their Shares.

LETTER TO SHAREHOLDERS

9

PwCCF has been appointed the financial adviser for the Selective Capital Reduction. The FA

Report is set out in Appendix 2 to this Circular. The FA Report, amongst other things, sets out

the analysis for the valuation of the Group. In the analysis set out in the FA Report, the FA has

relied on information contained in the Valuation Summary issued by Jones Lang LaSalle

Property Consultants Pte Ltd as set out in Appendix 3 to this Circular. Based on the analysis set

out in the FA Report, including the qualifications made therein, the FA is of the opinion that the

Fair Market Value per Share is S$1.13.

Although the Fair Market Value per Share is S$1.13, there is no guarantee that the Fair Market

Value will not change as it is dependent on the Company’s future performance and future

economic conditions in Singapore, as well as the impact of the uncertainties surrounding the

current global economic climate. The Non-Participating Shareholders have confirmed that they

have no plans for the redevelopment of the Department Store Property in the foreseeable future.

The Cash Distribution of S$1.30 per Share represents:

(i) an excess of S$0.17 per Share over the Fair Market Value; and

(ii) a premium of 15.0 per cent. over the Fair Market Value.

The Cash Distribution of S$1.30 per Share includes a premium of S$0.17 per Share over and

above the Fair Market Value which is intended to recognise the cost savings and elimination of

the administrative burden borne by maintaining the status of a public company and having

numerous minority shareholders. It is also to provide a gesture of goodwill to the Participating

Shareholders.

5. TU3 LLP’S INTENTIONS FOR THE COMPANY AND NO RIGHT OF COMPULSORY

ACQUISITION

The Company’s retail business was founded by the late Mr. Tang Choon Keng, the father of TWS

and TWK, and has been part of the family’s business for more than half a century. The Company

has a rich history and tradition as Singapore’s premier department store with its flagship store

in the heart of Singapore’s most famous shopping district.

In view of the above, TWS and TWK currently have no intention of (i) discontinuing the traditional

retail business started by their father, (ii) disposing of the Department Store Property, (iii)

redeveloping the Department Store Property, or (iv) entering into any arrangements for a real

estate investment trust in respect of the Department Store Property.

TU3 LLP currently has no intention to (i) propose any major changes to the businesses of the

Company, (ii) redeploy the fixed assets of the Company, or (iii) discontinue the employment of

any of the employees of the Group, other than in the ordinary course of business.

TU3 LLP is not entitled to, and will not avail itself of, the rights of compulsory acquisition under

Section 215 of the Companies Act. It should also be noted that Participating Shareholders

will also have no right and are not entitled to require TU3 LLP to acquire their Shares

under Section 215(3) of the Companies Act.

LETTER TO SHAREHOLDERS

10

6. SHAREHOLDERS’ APPROVAL

Shareholders’ approval is being sought for the proposed Selective Capital Reduction in

accordance with the provisions of the Companies Act.

Pursuant to Section 78G of the Companies Act, the Selective Capital Reduction requires

(i) a special resolution2 to be passed by the Shareholders approving the Selective Capital

Reduction and (ii) the approval and confirmation by the Court of the Selective Capital

Reduction.

A copy of the Order of Court approving the Selective Capital Reduction will subsequently

be lodged with the Registrar of Companies of Singapore (“Registrar”).

The Non-Participating Shareholders and their concert parties will not be voting on the

special resolution relating to the Selective Capital Reduction at the EGM.

7. ADMINISTRATIVE PROCEDURES

The following paragraphs set out the administrative procedures for the Selective Capital

Reduction.

7.1 Books Closure Date. Participating Shareholders registered in the Register of Members as at

the Books Closure Date will be entitled to receive S$1.30 for each Share registered in their

respective names as at the Books Closure Date.

7.2 Settlement of Cash Distribution. Subject to the conditions in paragraph 6 above being

satisfied, on the lodgement of a copy of the Order of Court confirming the Selective Capital

Reduction together with the other documents prescribed under the Companies Act with the

Registrar, the special resolution for the Selective Capital Reduction shall take effect, and

payment of the Cash Distribution pursuant to the Selective Capital Reduction will be made as set

out below.

Participating Shareholders whose Shares are registered in the Register of Members as at the

Books Closure Date will have the cheques for payment of their entitlements to the Cash

Distribution despatched to them by ordinary post at their own risk at the Registered Addresses.

A Participating Shareholder who wishes to record any change in his Registered Address

should notify the Share Registrar, Boardroom Corporate & Advisory Services Pte. Ltd. at

50 Raffles Place, #32-01 Singapore Land Tower, Singapore 048623 of such change before

the Books Closure Date.

7.3 Settlement of TU3 LLP Payment. The Company has received the TU3 LLP Payment and has

been authorised by TU3 LLP to utilise that amount to pay, on TU3 LLP’s behalf, to all

Participating Shareholders S$0.70 for each Share cancelled pursuant to the Selective Capital

Reduction. Participating Shareholders whose Shares are registered in the Register of Members

as at the Books Closure Date will have the cheques for payment of their entitlements to the TU3

LLP Payment despatched to them by ordinary post at their own risk at the Registered Addresses.

A Participating Shareholder who wishes to record any change in his Registered Address

should notify the Share Registrar, Boardroom Corporate & Advisory Services Pte. Ltd. at

50 Raffles Place, #32-01 Singapore Land Tower, Singapore 048623 of such change before

the Books Closure Date.

2 A special resolution requires the approval by a majority of not less than 75% of Shareholders present and voting at the EGM.

LETTER TO SHAREHOLDERS

11

8. EXEMPTIONS BY THE SIC

8.1 Exemptions by the SIC. In its letter dated 4 October 2011, the SIC exempted the proposed

Selective Capital Reduction from Rules 14, 15, 16, 17, 20.1, 21, 22, 28, 29 and 33.2 and Note

1(b) on Rule 19 of the Code, subject to the following conditions:

(i) the Non-Participating Shareholders and their concert parties abstain from voting on the

proposed Selective Capital Reduction;

(ii) the Directors who are acting in concert with the Non-Participating Shareholders abstain

from making a recommendation on the proposed Selective Capital Reduction to the

Shareholders; and

(iii) the Company appoints an independent financial adviser to advise the Shareholders on the

proposed Selective Capital Reduction.

8.2 Independence of Director. In its letter dated 4 October 2011, the SIC ruled that Mr. Soh Yew

Hock is exempted from the requirement to make a recommendation to Participating

Shareholders on the Selective Capital Reduction as he faces a conflict of interest in doing so

being a party acting in concert with the Non-Participating Shareholders. Mr. Soh is a

non-executive director of Tang Holdings which is majority owned (indirectly) and controlled by

TWK. TWK is a Non-Participating Shareholder for the purposes of the Selective Capital

Reduction. Tang Holdings is therefore a party acting in concert with the Non-Participating

Shareholders. Accordingly, Mr. Soh as a director of Tang Holdings is presumed to be a party

acting in concert with the Non-Participating Shareholders and would face a conflict of interest

that would render him inappropriate to join the remaining Directors in making a recommendation

to Participating Shareholders on the Selective Capital Reduction.

8.3 Scope of Responsibility. In view of the relationships between Mr. Soh Yew Hock and Tang

Holdings and between Tang Holdings and TWK as set out in the paragraph above, and as Mr.

Soh faces a conflict of interest with respect to the requirement to make a recommendation to

Participating Shareholders on the Selective Capital Reduction, Mr. Soh has been exempted by

the SIC from the requirement under the Code to make a recommendation to the Participating

Shareholders on the Selective Capital Reduction. However, Mr. Soh remains responsible for the

accuracy of the facts stated or opinions expressed in documents and advertisements issued by,

or on behalf of, the Company in connection with the Selective Capital Reduction.

9. ADVICE OF THE IFA

9.1 IFA. CIMB Bank Berhad, Singapore Branch has been appointed as the independent financial

adviser to advise the Independent Directors in respect of the Selective Capital Reduction.

Shareholders should consider carefully the advice of the IFA to the Independent Directors and

the recommendation of the Independent Directors before deciding whether to vote in favour of

the Selective Capital Reduction at the EGM. The IFA’s advice is set out in its letter dated

7 October 2011 which is reproduced in Appendix 5 to this Circular (the “IFA Letter”).

9.2 Key Factors Taken into Consideration by the IFA. In arriving at its advice, the IFA has relied

on the following key considerations as set out in section 6 of the IFA Letter and reproduced in

italics below. The considerations set out below should be considered and read in conjunction

with, and in the context of, the full text of the IFA Letter. Unless otherwise defined or the context

otherwise requires, all capitalised terms below shall have the same meanings as defined in the

IFA Letter.

LETTER TO SHAREHOLDERS

12

“In arriving at our advice to the Independent Directors on the Selective Capital Reduction,

we have considered, inter alia, the following factors which should be considered and read

in the context of the full text of this Letter:

(i) The P/E, EV/EBITDA and P/NTA multiples as implied by the SCR Consideration is

significantly higher than the mean and median of these multiples of the Comparable

Companies (on a historical basis);

(ii) The SCR Consideration represents a premium of 96.2% over the NTA of the Group as at

FY2011, and represents a premium of 96.2% and 104.7% respectively over the Revalued

NTA of the Group on an existing use basis and on a redevelopment basis, as at FY2011;

(iii) The implied EV/EBITDA and P/E multiples of the Company based on the SCR

Consideration is significantly higher than the range of multiples of the target companies

based on the Precedent Departmental Store Transactions;

(iv) The implied EV/Sales multiple of the Company based on the SCR Consideration is higher

than the EV/Sales of the target companies based on the Precedent Departmental Store

Transactions;

(v) The implied P/NTA multiple of the Company based on the SCR Consideration is higher

than the mean and median P/NTA of the target companies based on the Precedent

Departmental Store Transactions;

(vi) The P/NTA and P/RNTA multiples as implied by the SCR Consideration is higher than the

P/NTA and P/RNTA multiples of the target companies based on the Precedent Real Estate

Transactions;

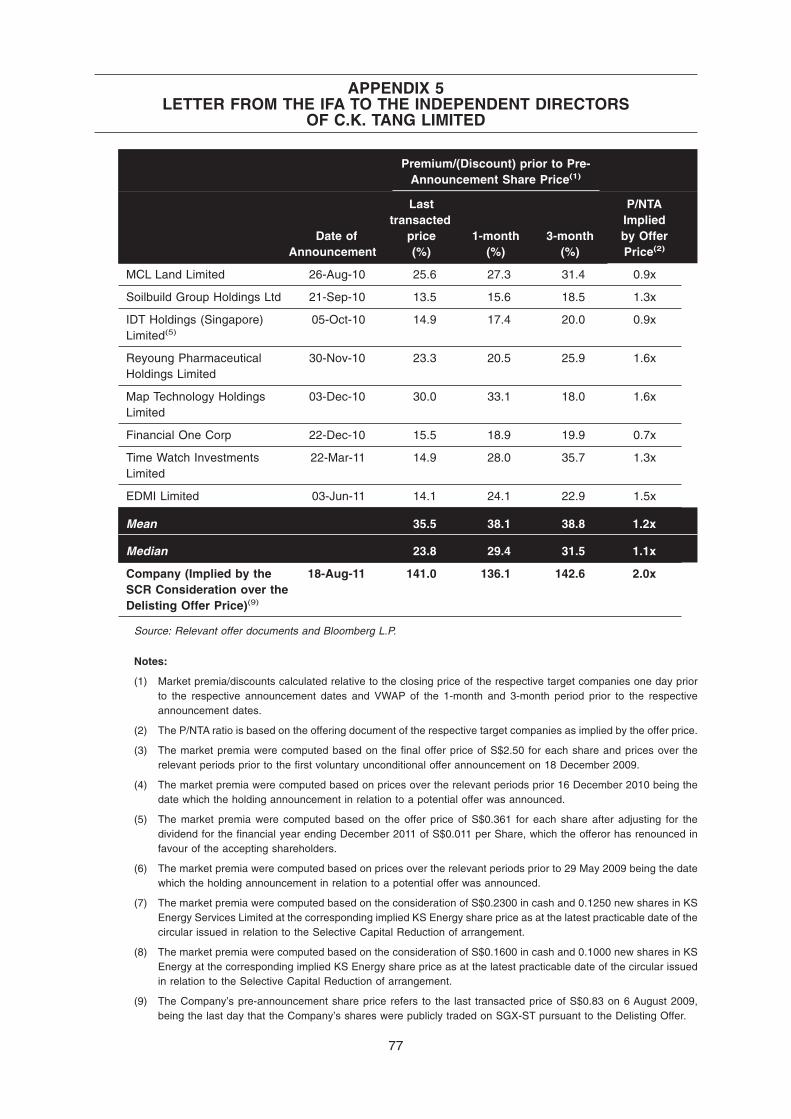

(vii) The SCR Consideration represents a significant premium over all historical VWAP

benchmark of the Shares in the preceding 10 years prior to the Delisting Date, and up until

the announcement of the Selective Capital Reduction;

(viii) The SCR Consideration represents a significant premium of 140.96% over the Delisting

Offer price;

(ix) The SCR Consideration represents a premium of 122.22% over the highest closing price

of the Shares of S$0.900 over the last 10 years prior to the Delisting Offer;

(x) The EV/Sales, P/E, P/NTA and P/RNTA multiples as implied by the SCR Consideration is

more favourable when compared with these multiples as implied by the Delisting Offer;

(xi) The premia implied by the SCR Consideration represents a significant premium to the

average premium implied by the Precedent Delistings;

(xii) No dividend has been paid by the Company in the last 5 financial years;

(xiii) The Offeror already has statutory control of the Company as it owns, or controls, directly

and indirectly, 98.2% of the Shares;

(xiv) The Offeror does not intend to dispose of the Department Store Property, or redevelop the

Department Store Property;

LETTER TO SHAREHOLDERS

13

(xv) The Selective Capital Reduction is currently the only offer available to Participating

Shareholders; and

(xvi) The Shares are illiquid as the Shares has been delisted from the SGX-ST subsequent to

the Delisting Offer in August 2009, and the Offeror has stated that the Selective Capital

Reduction will be the final offer made by the Offeror in respect of the Shares, and that no

further offers will be made by the Offeror;”

9.3 Advice of the IFA. Based on the IFA’s assessment of the financial terms of the Selective

Capital Reduction from a financial point of view, the IFA has advised the Independent Directors

to make the following recommendations to the Participating Shareholders in relation to the

Selective Capital Reduction, as set out in section 6 of the IFA Letter and reproduced in italics

below. The recommendations set out below should be considered and read in conjunction with,

and in the context of, the full text of the IFA Letter. Unless otherwise defined or the context

otherwise requires, all capitalised terms below shall have the same meanings as defined in the

IFA Letter.

“Based upon, and having considered, inter alia, the factors described above and the

information that has been made available to us at the Latest Practicable Date, we are of

the opinion that as of the Latest Practicable date, the Selective Capital Reduction is on

balance, fair and reasonable from a financial point of view. Accordingly, we would advise

the Independent Directors to recommend that, in the absence of a superior offer,

Participating Shareholders should vote in favour of the Selective Capital Reduction.

We recommend that the Independent Directors advise the Participating Shareholders of

our opinion in this Circular. We would also advise the Independent Directors to caution

the Participating Shareholders that they should not rely on our advice to the Independent

Directors as the sole basis for deciding whether or not to vote in favour of the Selective

Capital Reduction.

In rendering the above advice, we have not had regard to the specific investment objectives,

financial situation, tax position or particular needs and constraints of any individual Shareholder.

As each Shareholder would have different investment objectives and profiles, we would advise

that any individual Shareholder who may require specific advice in relation to his investment

objectives or portfolio should consult his stockbroker, bank manager, solicitor, accountant, tax

adviser or other professional adviser immediately. Shareholders should note that the opinion and

advice of CIMB should not be relied upon by any Shareholder as the sole basis for deciding

whether or not to vote in favour of the Selective Capital Reduction.”

10. INDEPENDENCE AND RECOMMENDATION OF THE DIRECTORS

10.1 Independence. All Directors, save for Mr. Soh Yew Hock, consider themselves to be

independent for the purpose of making recommendations to the Participating Shareholders in

respect of the Selective Capital Reduction.

10.2 Recommendation of Independent Directors. The Independent Directors, having considered

carefully the terms of the Selective Capital Reduction and the advice given by the IFA, concur

with the advice given by the IFA in respect of the Selective Capital Reduction as extracted in

paragraph 9 above.

LETTER TO SHAREHOLDERS

14

The Independent Directors are of the opinion that the Selective Capital Reduction is in the best

interests of the Company and accordingly recommend that the Participating Shareholders vote

in favour of the special resolution relating to the Selective Capital Reduction at the EGM.

SHAREHOLDERS ARE ADVISED TO READ THE IFA LETTER SET OUT IN APPENDIX 5 TO

THIS CIRCULAR CAREFULLY.

10.3 No Regard to Specific Objectives. In making their recommendation, the Independent

Directors have not had regard to the specific objectives, financial situation, tax status, risk

profiles or unique needs and constraints of any individual Shareholder. Accordingly, the

Independent Directors recommend that any individual Shareholder who may require advice in

the context of his specific investment portfolio should consult his stockbroker, bank manager,

solicitor, accountant or other professional adviser immediately.

11. EXTRAORDINARY GENERAL MEETING

The EGM will be held at RELC International Hotel, 30 Orange Grove Road, Level 5 (Room 507),

Singapore 258352 on 27 October 2011 at 9.30 a.m., for the purpose of considering and, if

thought fit, passing the special resolution set out in the Notice of EGM.

12. ACTION TO BE TAKEN BY SHAREHOLDERS

You will find enclosed with this Circular, the Notice of EGM and Proxy Form in relation to the

EGM. If you are unable to attend the EGM and wish to appoint a proxy to attend and vote on your

behalf, you should complete, sign and return the Proxy Form in accordance with the instructions

printed thereon as soon as possible and, in any event, so as to reach the registered office of the

Company at 310 Orchard Road, Singapore 238864 no later than forty-eight (48) hours before the

time fixed for the EGM. Your completion and return of the Proxy Form will not prevent you from

attending and voting in person at the EGM if you so wish, in place of your proxy.

If you have previously returned a duly executed Proxy Form to the Company prior to the

adjourned EGM held on 15 September 2011, you do not need to re-submit the Proxy Form

enclosed in this Circular. However, if you wish to re-submit your Proxy Form, you should

write to the Company expressly renouncing and withdrawing your previously submitted

Proxy Form, and submitting a new Proxy Form in its place.

A copy of this Circular is available on the website of the Company at http://www.tangs.com.

Please refer to the Company’s website for further announcements in relation to the Selective

Capital Reduction.

13. INFORMATION RELATING TO CPFIS INVESTORS

CPFIS Investors who wish to attend and vote at the EGM are advised to consult their respective

CPF Agent Banks should they require further information and if they are in any doubt as to the

action they should take, CPFIS Investors should seek independent professional advice.

14. RESPONSIBILITY STATEMENT

The Directors (including any who may have delegated detailed supervision of this Circular) have

taken all reasonable care to ensure that the facts stated and all opinions expressed in this

Circular (other than the FA Report at Appendix 2 to this Circular for which the FA has taken

LETTER TO SHAREHOLDERS

15

responsibility, the Valuation Summary and the Valuation Report at Appendices 3 and 4 to this

Circular for which the Valuer has taken responsibility, the IFA Letter at Appendix 5 to this Circular

for which the IFA has taken responsibility, and paragraph 5 and Appendices 1 and 6 to this

Circular for which TU3 LLP has taken responsibility) are fair and accurate and that no material

facts have been omitted from this Circular, and they jointly and severally accept responsibility

accordingly. Where any information has been extracted or reproduced from published or publicly

available sources (other than the FA Report at Appendix 2 to this Circular for which the FA has

taken responsibility, the Valuation Summary and the Valuation Report at Appendices 3 and 4 to

this Circular for which the Valuer has taken responsibility, the IFA Letter at Appendix 5 to this

Circular for which the IFA has taken responsibility, and paragraph 5 and Appendices 1 and 6 to

this Circular for which TU3 LLP has taken responsibility), the sole responsibility of the Directors

has been to ensure through reasonable enquiries that such information is accurately extracted

from such sources or, as the case may be, reflected or reproduced in this Circular.

In respect of the IFA Letter, the sole responsibility of the Directors has been to ensure that the

facts stated with respect to the Group are fair and accurate.

Yours faithfully

For and on behalf of the Board of Directors of

C.K. TANG LIMITED

Ernest Seow Teng Peng

Director

LETTER TO SHAREHOLDERS

16

17

APPENDIX 1LETTER FROM TU3 LLP DATED 8 SEPTEMBER 2011

18 August 2011

C.K. Tang Limited

310 Orchard Road

Singapore 238864

Dear Sirs

Report in connection with the Proposed Selective Capital Reduction to be undertaken by C.K.

Tang Limited Group (“CK Tang”)

1. INTRODUCTION

CK Tang was delisted from the Singapore Exchange on 14 August 2009 through TU3 LLP, Tang

UnityTwo LLP, Kerith Holdings LLP and Tang Wee Kit (the “Non-Participating Shareholders”)

owning approximately 97.8% of the total number of shares. Subsequently, some of the remaining

minority shareholders had sold their shares to the Non-Participating Shareholders, resulting in

the Non-Participating Shareholders holding approximately 98.2% in CK Tang. Other than the

Non-Participating Shareholders, there are currently approximately another 472 registered

shareholders (the “Participating Shareholders”).

To provide an opportunity for the Participating Shareholders to realise their investments in CK

Tang, the Company is proposing to undertake a selective capital reduction exercise with the view

to cancel all the shares held by the Participating Shareholders (“Selective Capital Reduction”),

should the Participating Shareholders approve the resolution to be tabled at the EGM.

It is in this context that PricewaterhouseCoopers Corporate Finance Pte Ltd (“PwCCF”) has

been appointed to assist CK Tang to determine the underlying value of CK Tang.

2. TERMS OF REFERENCE

This valuation report (“Report”) has been prepared solely for the Board of CK Tang in connection

with the proposed Selective Capital Reduction and is not intended for any legal or court

proceedings.

PwCCF will estimate the Fair Market Value of CK Tang’s retail businesses (“Retail Business”)

so as to determine the sum-of-the-parts valuation of CK Tang as a group, inclusive of the market

value of the department store property (“Department Store Property”).

For the Department Store Property, we have been furnished with a valuation summary of the

Department Store Property (“Valuation Summary”) held by CK Tang. With respect to the

Valuation Summary, we are not experts and do not hold ourselves to be experts in the evaluation

or appraisal of the Department Store Property and have relied solely upon the Valuation

APPENDIX 2REPORT OF THE FA IN CONNECTION WITH THE SELECTIVE

CAPITAL REDUCTION

18

Summary prepared by the Jones Lang LaSalle Property Consultants Pte Ltd (the “Independent

Property Valuer”). The Valuation Summary prepared by the Independent Property Valuer is set

out in Appendix B of the Letter.

We have held discussions with the Directors and the management of the Company and have

examined publicly available information collated by us as well as information, written and verbal,

provided to us by the Directors and the management of the Company and its professional

advisers. We have not independently verified such information, whether written or verbal, and

accordingly we cannot and do not represent or warrant, expressly or impliedly, and do not accept

any responsibility for the accuracy, completeness or adequacy of such information. We have

nevertheless made enquiries and exercised our judgment as we deemed necessary or

appropriate in assessing such information and are not aware of any reason to doubt the reliability

of the information.

The financial information and key assumptions to our valuation analysis contained in this Report

remains the responsibility of management. We have relied on the information provided by the

management but we have not and are not required to carry out an audit or review of the financial

statement or forecast, or any component of the financial statements or forecast of CK Tang. We

have also not made an independent evaluation or appraisal of the assets and liabilities of CK

Tang.

3. SUMMARY OF THE INDICATIVE VALUATION OF CK TANG BASED ON SUM-OF-THE-

PARTS ANALYSIS

To determine the value of CK Tang, PwCCF has estimated the Fair Market Value of CK Tang’s

retail businesses and relied on the market value of the Department Store Property as appraised

by the Independent Property Valuer.

We set out below the indicative valuation of CK Tang as follows:

S$ million Reference

Enterprise Value (“EV”) of Retail Business 8.2 Refer to Section 4

Market Value of Department Store Property 360.0 Refer to Section 5

Enterprise Value 368.2

Less: Net Debt 100.9

Less: Minority Interest (0.003)

Equity Value of CK Tang 267.3

No. of Shares Outstanding (million) 236.99

Fair Market Value Per Share (S$) 1.13

As computed above, the Fair Market Value Per Share based on the sum-of-the-parts valuation

of CK Tang is S$1.13.

APPENDIX 2REPORT OF THE FA IN CONNECTION WITH THE SELECTIVE

CAPITAL REDUCTION

19

4. VALUATION APPROACH OF THE RETAIL BUSINESS

The valuation approach for the Retail Business is its estimated Fair Market Value. Fair Market

Value is defined as the amount for which an asset could be exchanged, or a liability settled,

between knowledgeable, willing parties in an arm’s length transaction.

In arriving at our estimation of the Retail Business’ Fair Market Value, we have relied on the

accuracy and completeness of information furnished to us by the management and other

professional advisers. As such, we have not carried out any work to verify the accuracy,

correctness or completeness of such information. Accordingly, we will not be responsible for the

accuracy and completeness of such information.

By its nature, valuation work cannot be regarded as an exact science, and the conclusions

arrived at in many cases will of necessity be subjective and dependent on the exercise of

individual judgement. There is, therefore, no indisputable single value and we normally express

our valuation expectation as falling within expected ranges.

4.1 Explanation of the Market Approach

Under the Market Approach, the value of the business is determined based on an appropriate

capitalisation multiple derived from the current trading multiples of comparable companies and

applied to the earnings of a company.

The earnings are computed after making adjustments for any non-recurring or extraordinary

revenues or costs and only considering those revenues that are likely to be earned in the normal

course of business.

The market approach entails the following main steps:

— Determination of an appropriate earnings estimate

— Estimation of appropriate valuation multiple based on the comparable companies

— Application of multiple to earnings to determine value, adjusting for any discounts/premia

on the valuation.

APPENDIX 2REPORT OF THE FA IN CONNECTION WITH THE SELECTIVE

CAPITAL REDUCTION

20

The computed enterprise value range for the Retail Business is as set out below:

S$ million Reference

Normalised FY11 EBITDA S$2.343 Refer to Section 4.2

EV/EBITDA Range 3.5x Refer to Section 4.3

Enterprise Value S$8.2

4.2 Estimation of FY11 Normalised Earnings

In estimating the normalised earnings of CK Tang, we have used the audited results for the

financial year ended 31 March 2011 (i.e. FY11). In computing the maintainable earnings, we

have adjusted for any non-recurring or exceptional items. In addition, we have noted

management’s views of the present and future economic and financial environment, expected

business strategies and the general market conditions that CK Tang will continue to operate

under. These assumptions are significant and could substantially impact our valuation analysis.

We have used the earnings before interest, tax, depreciation and amortisation expenses

(“EBITDA”) as the relevant earnings estimate and set out below are the adjustments made to

arrive at the FY11 Normalised EBITDA:

S$ million

FY11 EBITDA 16.906

Adjustment for rental expenses -14.563

Normalised FY11 EBITDA 2.343

4.3 Estimation of Valuation Multiples

The Market Approach requires PwCCF to generate a peer set of companies (“Comparable

Companies”) which have been selected based on similarity of business with CK Tang. PwCCF

has determined the earnings multiple based on the Comparable Companies.

We, however, recognise that the Comparable Companies listed here are not exhaustive and to

the best of our knowledge and belief and after discussion with the management of the Company,

there is no company listed on the SGX-ST which may be considered directly comparable to CK

Tang in terms of composition of business activities, scale of operations, geographical spread of

activities, track record, financial performance, future prospects, asset base, risk profile and other

relevant criteria. Accordingly, any comparisons made with respect to the Comparable

Companies can only serve as an illustrative guide.

APPENDIX 2REPORT OF THE FA IN CONNECTION WITH THE SELECTIVE

CAPITAL REDUCTION

21

4.3.1 Analysis of the Comparable Companies

A brief description of the Comparable Companies is set out as below:

Comparable

Companies Description

Enterprise

Value(2)

Market

Capitalisation(1) Revenue(3)

(S$ million) (S$ million) (S$ million)

Isetan (Singapore)

Limited (“Isetan”)

The group’s principal

activities are operating

department

stores and supermarkets and

trading general merchandise.

The group operates in

Singapore.

64 146 334

Metro Holdings

Limited (“Metro”)

The group’s principal

activities are retailing and

department store operations,

property management and

holding companies. Other

activities include property

investment and development,

building contractors, leisure

operators and hoteliers. The

group operates a chain of

four Metro department stores

in Singapore and another

chain of four stores is held in

Jakarta and Bandung in

Indonesia. Operations of the

group are carried out in

ASEAN countries, Hong

Kong, China and Australia.

394 597 151

(Source: CapIQ as at Latest Practicable Date)

Notes:

(1) The market capitalisation of the Comparable Companies is as at the Latest Practicable Date (Source: Cap IQ).

(2) EV of the Comparable Companies is based on the market capitalisation as at the Latest Practicable Date and the

consolidated net debt and minority interest set out in their latest available announced results as at the Latest

Practicable Date (Source: Cap IQ, SGX-ST announcement).

(3) The revenue of the Comparable Companies is based on the latest available full-year results as at the Latest

Practicable Date (Source: Cap IQ, SGX-ST announcement, annual report).

APPENDIX 2REPORT OF THE FA IN CONNECTION WITH THE SELECTIVE

CAPITAL REDUCTION

22

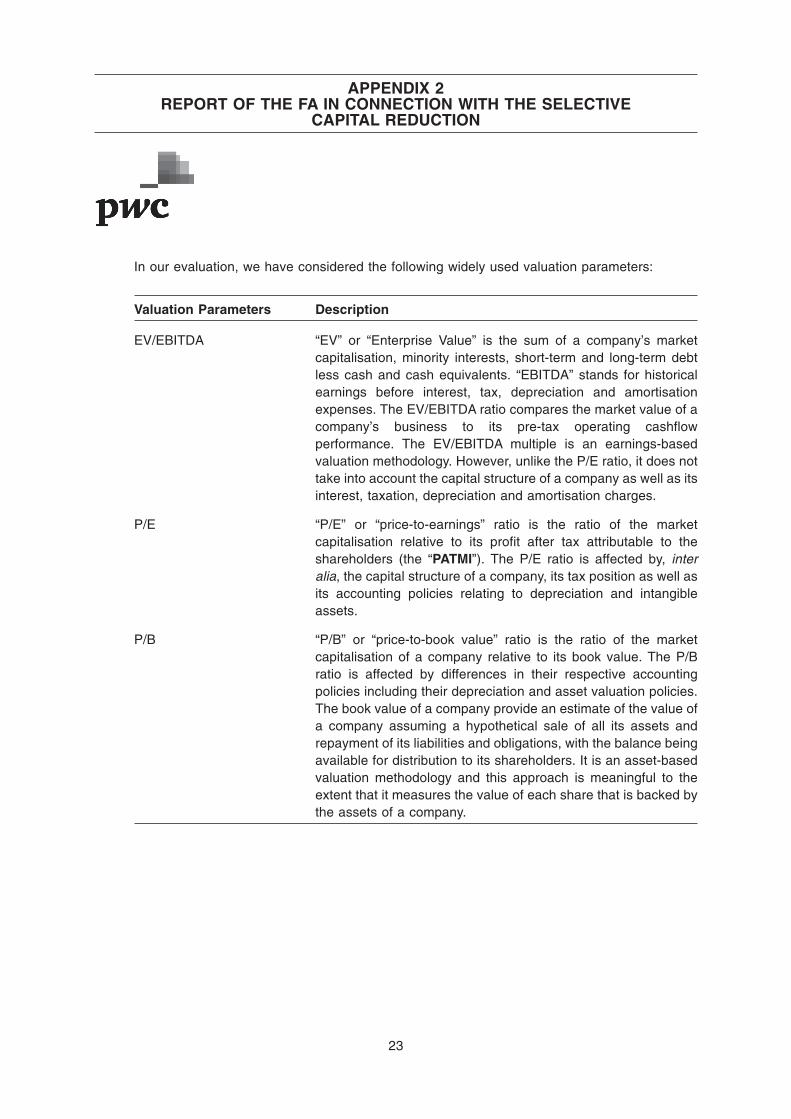

In our evaluation, we have considered the following widely used valuation parameters:

Valuation Parameters Description

EV/EBITDA “EV” or “Enterprise Value” is the sum of a company’s market

capitalisation, minority interests, short-term and long-term debt

less cash and cash equivalents. “EBITDA” stands for historical

earnings before interest, tax, depreciation and amortisation

expenses. The EV/EBITDA ratio compares the market value of a

company’s business to its pre-tax operating cashflow

performance. The EV/EBITDA multiple is an earnings-based

valuation methodology. However, unlike the P/E ratio, it does not

take into account the capital structure of a company as well as its

interest, taxation, depreciation and amortisation charges.

P/E “P/E” or “price-to-earnings” ratio is the ratio of the market

capitalisation relative to its profit after tax attributable to the

shareholders (the “PATMI”). The P/E ratio is affected by, inter

alia, the capital structure of a company, its tax position as well as

its accounting policies relating to depreciation and intangible

assets.

P/B “P/B” or “price-to-book value” ratio is the ratio of the market

capitalisation of a company relative to its book value. The P/B

ratio is affected by differences in their respective accounting

policies including their depreciation and asset valuation policies.

The book value of a company provide an estimate of the value of

a company assuming a hypothetical sale of all its assets and

repayment of its liabilities and obligations, with the balance being

available for distribution to its shareholders. It is an asset-based

valuation methodology and this approach is meaningful to the

extent that it measures the value of each share that is backed by

the assets of a company.

APPENDIX 2REPORT OF THE FA IN CONNECTION WITH THE SELECTIVE

CAPITAL REDUCTION

23

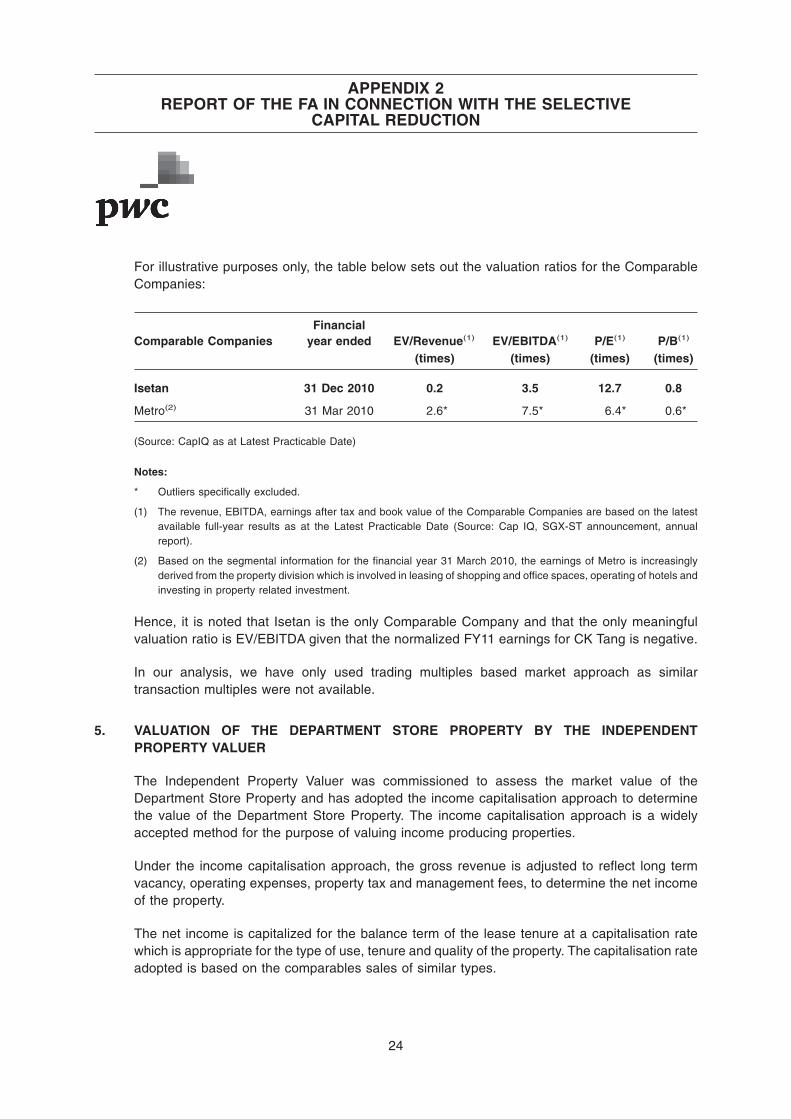

For illustrative purposes only, the table below sets out the valuation ratios for the Comparable

Companies:

Comparable Companies

Financial

year ended EV/Revenue(1) EV/EBITDA(1) P/E(1) P/B(1)

(times) (times) (times) (times)

Isetan 31 Dec 2010 0.2 3.5 12.7 0.8

Metro(2) 31 Mar 2010 2.6* 7.5* 6.4* 0.6*

(Source: CapIQ as at Latest Practicable Date)

Notes:

* Outliers specifically excluded.

(1) The revenue, EBITDA, earnings after tax and book value of the Comparable Companies are based on the latest

available full-year results as at the Latest Practicable Date (Source: Cap IQ, SGX-ST announcement, annual

report).

(2) Based on the segmental information for the financial year 31 March 2010, the earnings of Metro is increasingly

derived from the property division which is involved in leasing of shopping and office spaces, operating of hotels and

investing in property related investment.

Hence, it is noted that Isetan is the only Comparable Company and that the only meaningful

valuation ratio is EV/EBITDA given that the normalized FY11 earnings for CK Tang is negative.

In our analysis, we have only used trading multiples based market approach as similar

transaction multiples were not available.

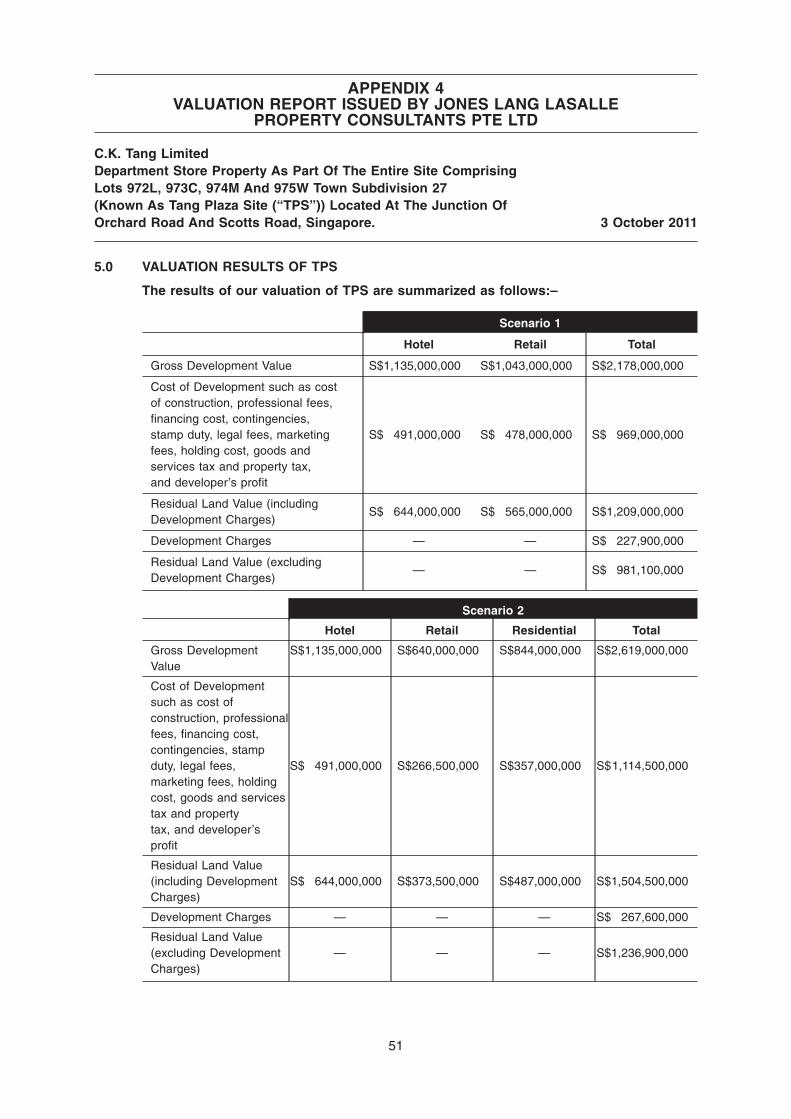

5. VALUATION OF THE DEPARTMENT STORE PROPERTY BY THE INDEPENDENT

PROPERTY VALUER

The Independent Property Valuer was commissioned to assess the market value of the

Department Store Property and has adopted the income capitalisation approach to determine

the value of the Department Store Property. The income capitalisation approach is a widely

accepted method for the purpose of valuing income producing properties.

Under the income capitalisation approach, the gross revenue is adjusted to reflect long term

vacancy, operating expenses, property tax and management fees, to determine the net income

of the property.

The net income is capitalized for the balance term of the lease tenure at a capitalisation rate

which is appropriate for the type of use, tenure and quality of the property. The capitalisation rate

adopted is based on the comparables sales of similar types.

APPENDIX 2REPORT OF THE FA IN CONNECTION WITH THE SELECTIVE

CAPITAL REDUCTION

24

A copy of the Valuation Summary prepared by the Independent Property Valuer is attached at

Appendix B of the Letter. Their opinion of the market value of the Department Store Property for

its existing use as a department store, free from all encumbrances is S$360 million.

6. DETERMINATION OF THE FAIR MARKET VALUE PER SHARE

In determining the Fair Market Value Per Share of CK Tang, we have compared the computed

Fair Market Value Per Share to the revalued NAV (the “RNAV”) of the Group. RNAV is

determined after adjusting mainly for the revaluation of the Company’s key property assets

based on its estimated current market values.

6.1 Analysis of the RNAV of the Group

We have checked with management whether there are any tangible assets which should be

valued at an amount that is materially different from that which is recorded in the audited balance

sheet of the Group as at 31 March 2011.

The audited balance sheet of the Group as at 31 March 2011 has included the market value of

the department store property as appraised by the Independent Property Valuer at S$360 million

hence there is no revaluation surplus or deficit arising in respect of the Department Store

Property as at 31 March 2011.

The following table sets out an analysis of the historical RNAV of the Group:

FYE 31 March FY09 FY10 FY11

Department Store Property Value (S$ million) 340.0 350.0 360.0

Audited RNAV (S$ million) 219.6 223.6 241.5

Audited RNAV Per Share (S$) 0.93(1) 0.94(2) 1.02(3)

(Source: Relevant shareholder circulars, annual reports)

Notes:

(1) Computed based on 236,996,226 fully diluted Shares assuming full conversion of the 12,000 outstanding options

into 12,000 Shares as at 31 March 2009.

(2) Computed based on 236,988,226 fully diluted Shares assuming full conversion of the 4,000 outstanding options

into 4,000 Shares as at 31 March 2010.

(3) Computed based on 236,988,226 fully diluted Shares assuming full conversion of the 4,000 outstanding options

into 4,000 Shares as at 31 March 2011.

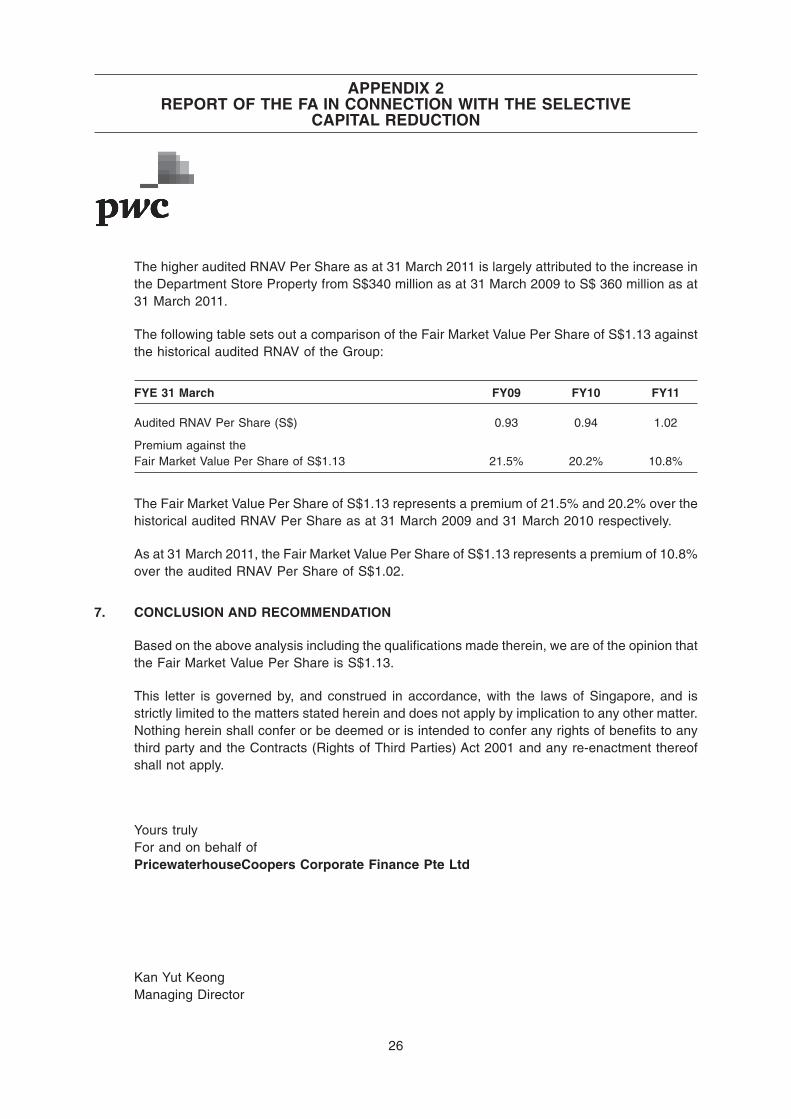

Based on the above, we note that the audited RNAV Per Share as at 31 March 2011 is higher

than both the historical audited RNAV Per Share as at 31 March 2009 and 31 March 2010.

APPENDIX 2REPORT OF THE FA IN CONNECTION WITH THE SELECTIVE

CAPITAL REDUCTION

25

The higher audited RNAV Per Share as at 31 March 2011 is largely attributed to the increase in

the Department Store Property from S$340 million as at 31 March 2009 to S$ 360 million as at

31 March 2011.

The following table sets out a comparison of the Fair Market Value Per Share of S$1.13 against

the historical audited RNAV of the Group:

FYE 31 March FY09 FY10 FY11

Audited RNAV Per Share (S$) 0.93 0.94 1.02

Premium against the

Fair Market Value Per Share of S$1.13 21.5% 20.2% 10.8%

The Fair Market Value Per Share of S$1.13 represents a premium of 21.5% and 20.2% over the

historical audited RNAV Per Share as at 31 March 2009 and 31 March 2010 respectively.

As at 31 March 2011, the Fair Market Value Per Share of S$1.13 represents a premium of 10.8%

over the audited RNAV Per Share of S$1.02.

7. CONCLUSION AND RECOMMENDATION

Based on the above analysis including the qualifications made therein, we are of the opinion that

the Fair Market Value Per Share is S$1.13.

This letter is governed by, and construed in accordance, with the laws of Singapore, and is

strictly limited to the matters stated herein and does not apply by implication to any other matter.

Nothing herein shall confer or be deemed or is intended to confer any rights of benefits to any

third party and the Contracts (Rights of Third Parties) Act 2001 and any re-enactment thereof

shall not apply.

Yours truly

For and on behalf of

PricewaterhouseCoopers Corporate Finance Pte Ltd

Kan Yut Keong

Managing Director

APPENDIX 2REPORT OF THE FA IN CONNECTION WITH THE SELECTIVE

CAPITAL REDUCTION

26

Jones Lang LaSalle Property Consultants Pte Ltd

Jones Lang LaSalle Property Management Pte Ltd

9 Ra�es Place #39-00 Republic Plaza Singapore 048619

tel +65 6220 3888 fax +65 6438 3362

Company Reg No. 198004794D Agency Licence No. L3007326E

Company Reg No. 197600508N

Certi!cate No. SG04/00074

Certi!cate no. SG04/00075

Valuation (Land & Building)

Your Ref :

Our Ref : TKC:CHH:aa:110477

C.K. Tang Limited

310 Orchard Road

Singapore 238864

June 30, 2011

Dear Sir,

VALUATION OF 310 ORCHARD ROAD TANGS STORE SINGAPORE 238864

(THE “PROPERTY”)

We have been instructed by the Board of Directors of C.K. Tang Limited to determine the market value

of the Department Store Property for its existing use belonging to C.K. Tang Properties (Singapore) Pte

Ltd, a wholly-owned subsidiary of C.K. Tang Limited.

We have prepared a valuation summary in accordance with the instructions of the Board of Directors

for the specific purpose of its inclusion in the Letter to be issued in connection with the Selective Capital

Reduction for C.K. Tang Limited.

Unless otherwise defined or the context otherwise requires, all terms defined in the Letter shall have

the same meaning herein.

RELIANCE ON THIS LETTER

The opinion of value contained in this Letter is not a guarantee or prediction but is based on the

information obtained from reliable and reputable agencies and sources, the Board of Directors and

other related parties. Whilst Jones Lang LaSalle Property Consultants Pte Ltd has endeavoured to

obtain accurate information, it has not independently verified all the information provided by the Board

of Directors or other reliable and reputable agencies.

The methodology used in valuing the Department Store Property namely, the capitalization approach

is used to determine the market value for its existing use.

APPENDIX 3VALUATION SUMMARY ISSUED BY JONES LANG LASALLE PROPERTY

CONSULTANTS PTE LTD

27

The resultant value is, in our opinion, the best estimate but it is not to be construed as a guarantee or

prediction and it is fully dependent upon the accuracy of the assumptions made. Every Shareholder

who intends to make a decision concerning the Selective Capital Reduction should understand the

assumptions and methodologies made in the Letter to appreciate the context in which the values are

arrived at and also carry out their independent assessment with regards to the Selective Capital

Reduction. We do not take any responsibility for any decision made by the Shareholders.

We have not carried out investigations on site in order to determine the suitability of ground conditions,

nor have we undertaken archaeological, ecological or environmental surveys. Our valuation is made on

the basis that the aforesaid conditions and surveys are satisfactory.

VALUATION RATIONALE

The valuation of the Department Store Property is assessed based on the market value for its existing

use as a department store.

Existing Use Value

In arriving at our opinion of market value, we have adopted the capitalisation of net income approach.

OPINION OF VALUE

A summary of our valuation and details relating to the Department Store Property is set out in the

following page.

DISCLAIMER

We have prepared this valuation summary which appears in the Letter and specifically disclaim liability

to any person in the event of any omission from or false or misleading statement included in the Letter,

other than in respect of the information provided within the valuation summary. We do not make any

warranty or representation as to the accuracy of the information in any part of the Letter other than as

expressly made or given in this valuation summary.

Jones Lang LaSalle has relied upon the Department Store Property’s data supplied by the Board of

Directors which we assume to be true and accurate. Jones Lang LaSalle takes no responsibility for

inaccurate data supplied by the client and subsequent conclusions related to such data.

The reported analyses, opinions and conclusions are limited only by the reported assumptions and

limiting conditions and are our unbiased professional analyses, opinions and conclusions. We have no

present or prospective interest in the Department Store Property and are not a related corporation of

nor do we have a relationship with the Board of Directors, adviser or other party/parties whom we are

contracting with. The valuers’ compensation is not contingent upon the reporting of a predetermined

APPENDIX 3VALUATION SUMMARY ISSUED BY JONES LANG LASALLE PROPERTY

CONSULTANTS PTE LTD

28

value or direction in value that favors the cause of the client, the amount of the value estimate, the

attainment of a stipulated result, or the occurrence of a subsequent event.

We hereby certify that our valuers undertaking these valuations are authorized to practise as valuers

and have the necessary expertise and experience in valuing similar types of properties.

We have enclosed the general principles adopted in the preparation of this valuation summary.

Yours faithfully,

JONES LANG LASALLE PROPERTY CONSULTANTS PTE LTD

Tan Keng Chiam

B.Sc. (Est. Mgt.) MSISV

AD041-2004796D

Regional Director

APPENDIX 3VALUATION SUMMARY ISSUED BY JONES LANG LASALLE PROPERTY

CONSULTANTS PTE LTD

29

VALUATION SUMMARY

Property : 310 Orchard Road

Tangs Store

Singapore 238864

(The “Property”)

Legal Description : Lots U4579P and U4580W Town Subdivision 27

Tenure : Estate In Fee Simple

Brief Description of

Department Store Property

: A 5-level department store with an office at the 7th storey located

within a 7-storey podium block with 2 basement levels of the

Department Store Property.

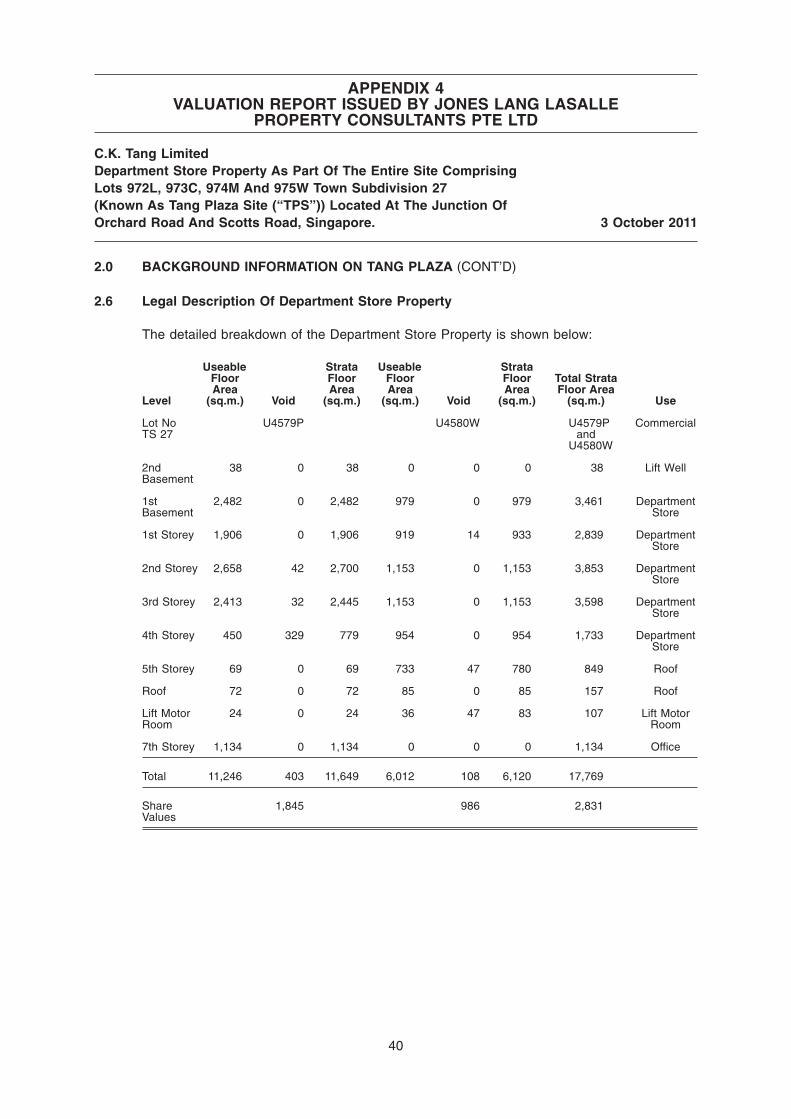

Strata Floor Area : Strata Lot No. Strata Floor Area

U4579P 11,649 sq.m.

U4580W 6,120 sq.m.

Total 17,769 sq.m.*

* including void, lift motor room and roof slabs

Owner : C.K. Tang Properties (Singapore) Ltd

Lease Agreement : The Department Store Property is leased to C.K. Tang Limited for a

term of 5 years commencing from July 1, 2008.

Master Plan Zoning

(2008 Edition)

: ‘Hotel’ with a gross plot ratio of 5.6+.

Market Value for its existing

use as at June 30, 2011

: S$360,000,000/-

(Singapore Dollars Three Hundred And Sixty Million).

JONES LANG LASALLE

TKC:CHH:aa:110477

June 30, 2011

APPENDIX 3VALUATION SUMMARY ISSUED BY JONES LANG LASALLE PROPERTY

CONSULTANTS PTE LTD

30

GENERAL PRINCIPLES ADOPTED IN THE PREPARATION OF VALUATIONS AND REPORTS

These are the general principles upon which our Valuations and Reports are normally prepared; they apply unless

we have specifically mentioned otherwise in the body of the report.

1) VALUATION STANDARDS

All work are carried out in accordance with the Singapore Institute of Surveyors and Valuers (SISV) Valuation

Standards and Guidelines and International Valuation Standards (IVS), subject to variations to meet local

laws, customs, practices and market conditions.

2) VALUATION BASIS

Our valuations are made on the basis of Market Value, defined by the SlSV as follows:

“Market Value is the estimated amount for which a property should exchange on the date of valuation

between a willing buyer and a willing seller in an arm’s-length transaction after proper marketing wherein the

parties had each acted knowledgeably, prudently, and without compulsion.”

3) CONFIDENTIALITY

Our Valuations and Reports are confidential to the party to whom they are addressed or their other

professional advisors for the specific purpose(s) to which they refer. No responsibility is accepted to any

other parties and neither the whole, nor any part, nor reference thereto may be included in any published

document, statement or circular, or published in any way, nor in any communication with third parties, without

our prior written approval of the form and context in which they will appear.

4) SOURCE OF INFORMATION

Where it is stated in the report that information has been supplied by the sources listed, this information is

believed to be reliable and we shall not be responsible for its accuracy nor make any warranty or

representation of the accuracy of the information. All other information stated without being attributed directly

to another party is obtained from our searches of records, examination of documents or enquiries with the

relevant authorities.

5) DOCUMENTATION

We do not normally read leases or documents of title and, where appropriate, we recommend that lawyer’s

advice on these aspects should be obtained. We assume, unless informed to the contrary, that all

documentation is satisfactorily drawn and that good title can be shown and there are no encumbrances,

restrictions, easements or other outgoings of an onerous nature which would have an effect on the value of

the interest under consideration.

APPENDIX 3VALUATION SUMMARY ISSUED BY JONES LANG LASALLE PROPERTY

CONSULTANTS PTE LTD

31

6) TOWN PLANNING AND OTHER STATUTORY REGULATIONS

Information on Town Planning is obtained from the set of Master Plan, Development Guide Plans (DGP) and

Written Statement published by the competent authority. Unless otherwise instructed, we do not normally

carry out requisitions with the various public authorities to confirm that the property is not adversely affected

by any public schemes such as road and drainage improvements. If reassurance is required, we recommend

that verification be obtained from your lawyers.

Our valuations are prepared on the basis that the premises and any improvements thereon comply with all

relevant statutory regulations. It is assumed that they have been, or will be issued with a Certificate of

Statutory Completion by the competent authority.

7) TENANTS

Enquiries as to the financial standing of actual or prospective tenants are not normally made unless

specifically requested. Where properties are valued with the benefit of lettings, it is therefore assumed that

the tenants are capable of meeting their obligations under the lease and that there are no arrears of rent or